Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

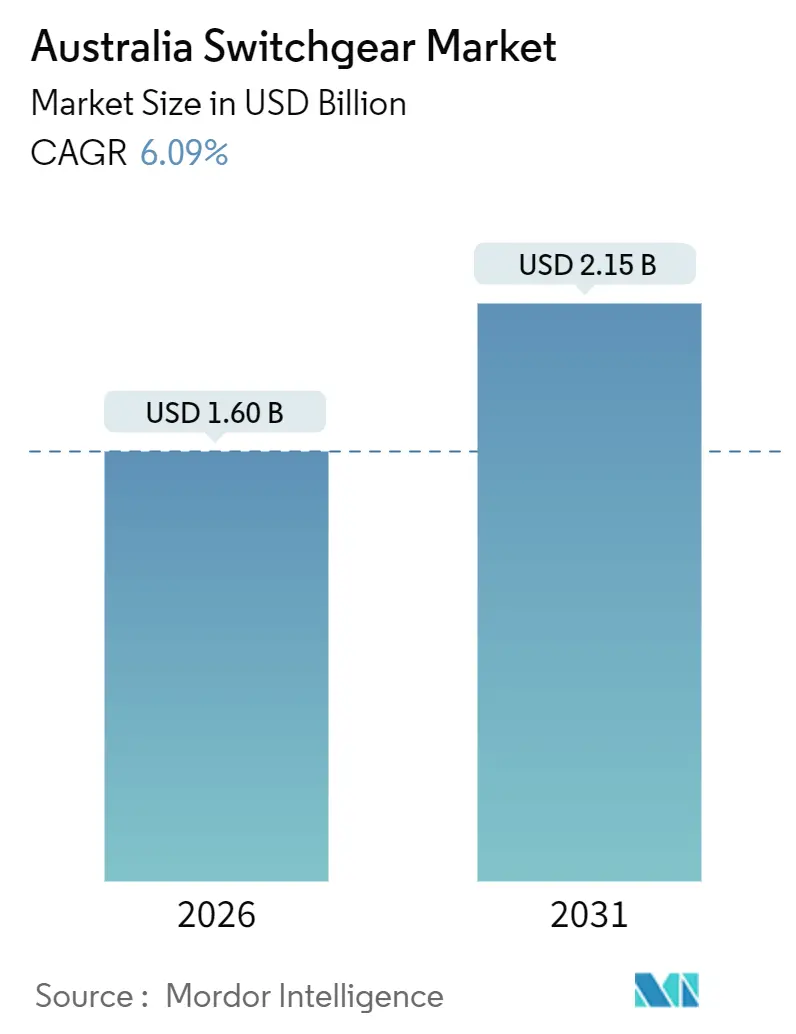

| Market Size (2026) | USD 1.60 Billion |

| Market Size (2031) | USD 2.15 Billion |

| Growth Rate (2026 - 2031) | 6.09% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Australia Switchgear Market Analysis by Mordor Intelligence

The Australia switchgear market size stood at USD 1.60 billion in 2026 and is projected to climb to USD 2.15 billion by 2031, reflecting a 6.09% CAGR over the forecast period. Medium-voltage equipment dominates because renewable energy zone interconnections and distribution upgrades require 11 kV to 33 kV protection, while high-voltage gear is set to accelerate as 500 kV corridors come online.[1] Gas-insulated switchgear leads on value, yet utilities are actively substituting SF₆ with dry-air or vacuum alternatives to meet proposed 2030 bans for installations above 145 kV. Demand is further amplified by grid-scale batteries that create high-fault nodes, data center capacity that is tripling, and mining electrification that pushes hybrid, containerized designs to remote sites. Persistent supply-chain headwinds and insurance costs for SF₆ handling are prompting early procurement, modular construction, and the localisation of final assembly to trim lead times.

Key Report Takeaways

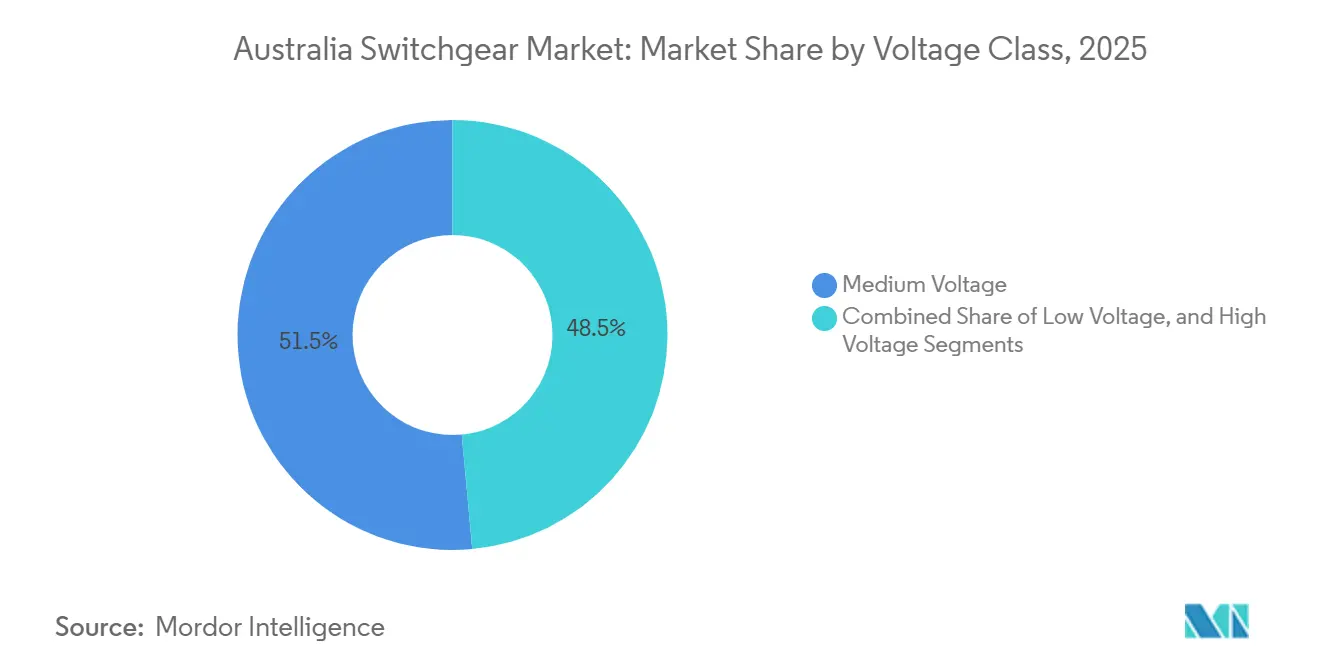

- By voltage class, medium voltage commanded 51.46% of Australia switchgear market share in 2025, while high voltage is forecast to expand at a 6.87% CAGR through 2031.

- By insulation type, gas-insulated designs led with 44.82% revenue share in 2025; solid and vacuum technologies are advancing at a 7.88% CAGR to 2031.

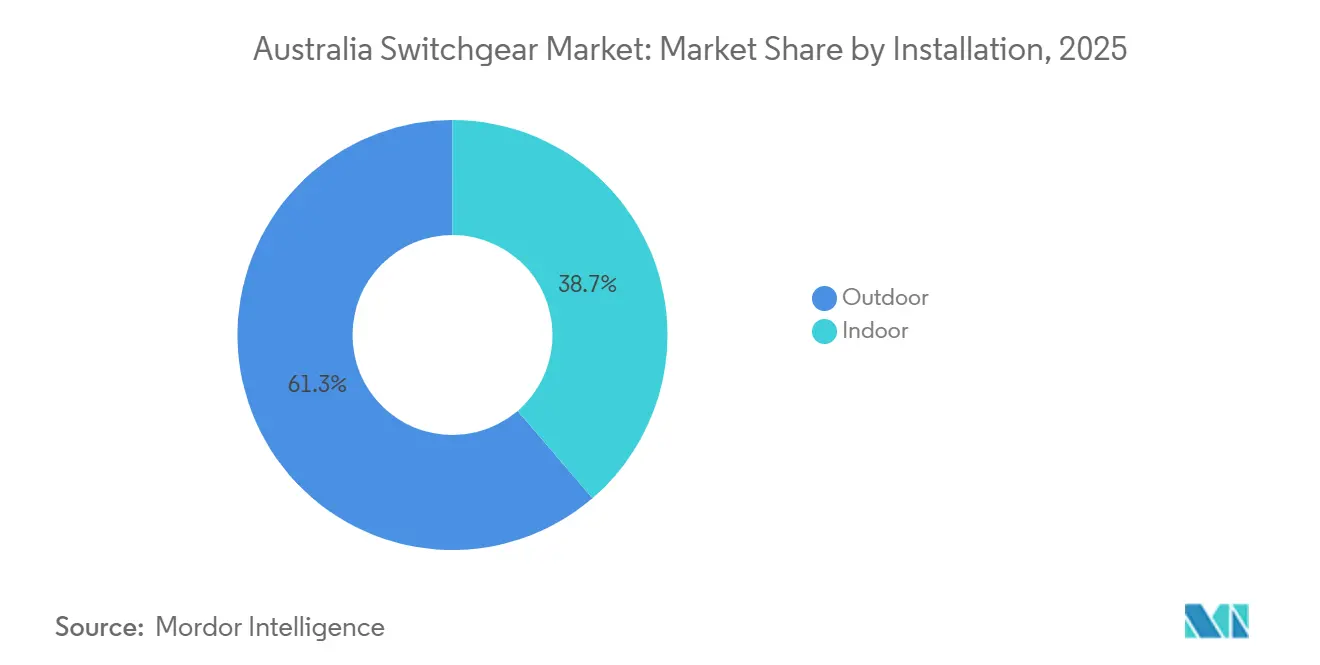

- By installation, outdoor systems accounted for 61.29% of deployments in 2025, whereas indoor installations are projected to grow at a 6.18% CAGR to 2031.

- By end-user, utilities held 47.33% share in 2025, but industrial customers are poised to record the fastest growth at 6.46% CAGR through 2031.

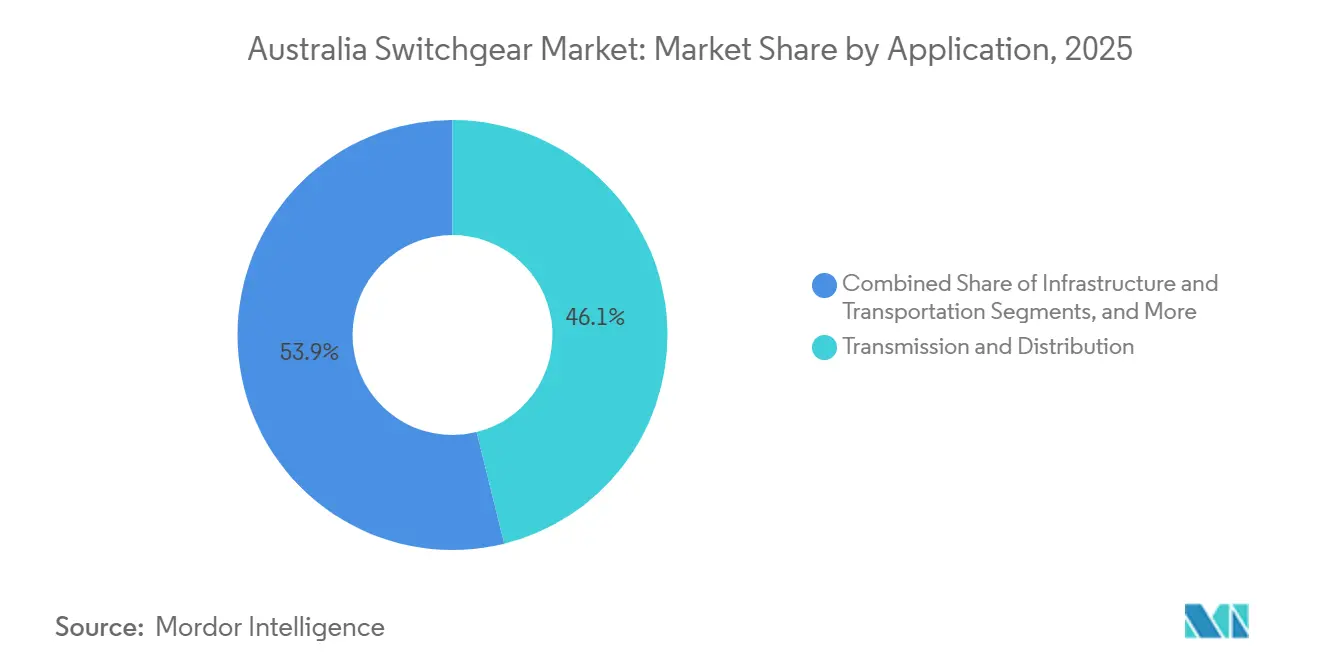

- By application, transmission and distribution captured 46.14% of 2025 revenue; data-centres and critical facilities are predicted to expand at a 7.02% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Australia Switchgear Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Utility-scale Battery Boom Creating New High-fault MV Nodes | +1.2% | National, concentrated in New South Wales, Victoria, Queensland | Medium term (2-4 years) |

| Mandatory Replacement of SF₆ GIS Above 145 kV by 2030 (proposed) | +0.9% | National, with early adoption in New South Wales, Victoria | Long term (≥ 4 years) |

| Federal "Rewiring the Nation" Fund Accelerating 500 kV Builds | +1.5% | National, priority corridors in New South Wales, Victoria, Queensland | Short term (≤ 2 years) |

| Data-centre Capacity Tripling, Demanding Arc-flash-safe LV Switchgear | +0.8% | National, concentrated in Sydney, Melbourne, Perth | Medium term (2-4 years) |

| Mining Decarbonisation Pushes Containerised Hybrid Switchgear to Remote Sites | +0.7% | Western Australia, Queensland, Northern Territory | Medium term (2-4 years) |

| Cyber-secure Digital Substations Becoming a Regulated Requirement | +0.5% | National, led by transmission network service providers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Utility-scale Battery Boom Creating New High-fault MV Nodes

Large battery energy storage systems commissioned since 2025 have shifted fault-current levels, compelling utilities to specify 31.5 kA and 40 kA vacuum breakers instead of legacy 25 kA units. CleanCo’s 500 MWh array and Origin’s 700 MW, 2.8 GWh project each required dedicated 33 kV switchboards to isolate inverter strings. ABB’s modular eHouse for Synergy’s 500 MW battery cut on-site commissioning to six months, highlighting the appeal of factory-tested assemblies. With the market operator forecasting 30 GW of storage by 2030, roughly 600 additional medium-voltage gear sets will be needed nationwide. Distribution companies are also demanding IEC 62271-200 metal-enclosed designs that contain arc energy and protect technicians during maintenance.

Federal Rewiring the Nation Fund Accelerating 500 kV Builds

The AUD 20 billion program underwrites landmark lines such as VNI West, HumeLink, Marinus Link, and Sydney Ring, together requiring more than 200 500 kV and 330 kV breaker bays. Transgrid ordered Hitachi Energy dead-tank breakers for HumeLink in January 2025, while Powerlink Queensland tapped GE Vernova for 69 units rated at 245 kV and above in April 2025. Concessional debt from the Clean Energy Finance Corporation has enabled transmission owners to place long-lead orders two years ahead of construction, tightening delivery windows. Manufacturers are therefore weighing regional assembly hubs to shave twelve-week sea freight delays. These projects lift near-term demand across high-voltage switchgear, transformers, and digital protection relays.

Mandatory Replacement of SF₆ GIS Above 145 kV by 2030

Legislation now being drafted would phase out SF₆ in new installations above 145 kV nationwide, mirroring European policy trajectories. Utilities have responded by piloting vacuum and dry-air substitutes, starting with Ausgrid’s rollout across 50 substations announced in October 2024. Schneider Electric, ABB, and Siemens are offering zero-GWP mixtures compatible with existing GIS footprints, lowering total cost of ownership by eliminating gas-handling fees. Early adopters cite up to 25% insurance savings because contractors no longer face greenhouse gas leak liabilities. Volume pricing is expected to converge with SF₆ variants by 2028 as Australia switchgear market demand rises.

Data-centre Capacity Tripling and Demanding Arc-flash-safe LV Gear

NEXTDC, AWS, and other hyperscale operators plan to increase their portfolio capacity beyond 1.7 GW, with each facility requiring low-voltage boards rated at 100 kA and equipped with 2 ms arc-flash sensors. Schneider Electric’s PowerLogic P7 platform, launched in April 2025, adds Ethernet-based diagnostics that predict failure before downtime. Contractors such as Southern Cross Electrical Engineering integrate switchgear within prefabricated power rooms, shrinking planned outage windows from eight hours to two. The sector’s 99.995% uptime target is driving the adoption of redundant A-B architectures, resulting in orders for duplicate busbars, automatic transfer switches, and continuous thermal monitoring. Resulting volumes will keep the Australia switchgear market growth above the headline average in urban campuses.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 25-week Lead-time Spikes for 40 kA Breakers Due to Global Copper Shortage | -0.8% | National, affecting all voltage classes | Short term (≤ 2 years) |

| Limited Domestic Certification Labs Delaying Type-testing | -0.5% | National, concentrated impact on new product introductions | Medium term (2-4 years) |

| Rising Insurance Premiums for SF₆ Handling Contractors | -0.3% | National, with higher impact in New South Wales, Victoria | Short term (≤ 2 years) |

| Community Opposition to New 500 kV Yards in Peri-urban Zones | -0.4% | New South Wales, Victoria, Queensland peri-urban corridors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

25-week Lead-time Spikes for 40 kA Breakers Due to Global Copper Shortage

Copper prices exceeded USD 10,000 per tonne in 2024 and remained high through 2025, adding nine weeks to average production cycles for heavy-current breakers.[2] GE Vernova confirmed in April 2025 that delivery of 245 kV breakers stretched to 25 weeks, up from 16, because each unit embodies up to 250 kg of copper. Transmission owners now issue purchase orders 18-24 months before energisation and seek fixed-price clauses that pass raw-material risk to suppliers. Alternatives such as aluminium busbars require 60% larger cross-sections, raising enclosure sizes and installation cost. The Australian Energy Regulator permitted contingent capital provisions for overruns exceeding 15% to prevent project delays.

Limited Domestic Certification Labs Delaying Type-testing

Few of the National Association of Testing Authorities' facilities can certify medium-voltage gear, and none can generate 63 kA at 550 kV, forcing high-voltage prototypes to be sent offshore for validation. Foreign testing adds 12-16 weeks and exposes manufacturers to currency fluctuations in euro or yen. Hitachi Energy and Siemens Energy mitigate delays through captive test centers in Europe, giving them a time-to-market edge. A 2024 feasibility study envisions an AUD 50 million domestic lab, but commissioning is unlikely to occur before 2028. Meanwhile, vendors batch similar products to amortize test fees, restricting the cadence of innovation in Australia's switchgear industry.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Voltage Class: High Voltage Drives Transmission Backbone

High-voltage equipment is forecast to expand at a 6.87% CAGR from 2026–2031, fueled by the Rewiring the Nation lines that require 500 kV and 330 kV breakers across four priority corridors. Medium-voltage devices remained the largest slice at 51.46% of Australia switchgear market share in 2025, underscoring the ubiquity of 11 kV to 33 kV in distribution grids and renewable interconnections.

Demand clusters around inverter-rich nodes where battery energy storage and solar farms drive bidirectional flows. CleanCo and Origin projects at 33 kV exemplify this pull, while synchronous condensers installed at Central-West Orana adopted 132 kV breakers to stabilize frequency as coal plants retire. As a result, Australia switchgear market size for medium voltage remains pivotal even as high voltage accelerates. Utilities are specifying breakers with extended DC time-constant ratings to interrupt asymmetrical faults typical of inverter-based resources.

By Insulation Type: Solid and Vacuum Technologies Gain Share

Gas-insulated units held 44.82% in 2025 due to space-constrained urban substations; however, vacuum and solid-dielectric alternatives are growing at a 7.88% CAGR as SF₆ phase-out rules advance. Vacuum breakers dominate up to 40.5 kV ratings because they are maintenance-free and have a 30-year lifecycle.

Ausgrid’s 2024 deal with Schneider Electric to deploy dry-air switchgear highlights the shift, while hybrid yards that combine gas-insulated busbars with air breakers offer 40% footprint savings without environmental penalties. Australia's switchgear market size for solid insulation is expected to expand steadily as Scope 1 emission avoidance generates Australian Carbon Credit Units that offset higher upfront prices. Composite insulators and silicone coatings also mitigate salt fog and coastal pollution in outdoor air-insulated stations.

By Installation: Indoor Deployments Accelerate in Urban Zones

Outdoor switchgear dominated installations at 61.29% in 2025 due to transmission yards and primary substations across sparsely populated regions. However, indoor systems are projected to rise at a 6.18% CAGR as data-centers, mining portals, and secondary urban substations require arc-flash containment and dust exclusion.

Southern Cross Electrical Engineering opted for an indoor 132 kV GIS to shield equipment from Pilbara dust at Mount Keith West, marking a shift in the mining sector. Predictive analytics through IEC 61850 sensors make indoor panels attractive for condition-based maintenance. Australia's switchgear market growth, therefore, hinges on balancing outdoor cost advantages with indoor safety and monitoring benefits, particularly in dense cities adopting building-integrated substations.

By End-User: Industrial Segment Leads Growth Trajectory

Utilities retained 47.33% of 2025 demand, anchored by network reinforcement programs, yet industrial customers are set to register a 6.46% CAGR through 2031 as miners electrify fleets and microgrids. Pilbara haul-truck charging needs 11 kV and 33 kV containerised modules, while Rio Tinto’s Gudai-Darri solar-battery hybrid relies on switchgear hardened for 50 °C heat and vibration.

Australia switchgear market penetration in industrial sites is rising because containerised designs cut installation from six months to six weeks. Ampcontrol is adapting explosion-proof assemblies for surface mines to tap this demand. Manufacturing electrification and petrochemical facility upgrades further diversify the client base beyond the grid monopolies that historically dominated procurement.

By Application: Data-centres and Critical Facilities Surge

Transmission and distribution applications secured 46.14% of revenue in 2025; however, hyperscale data centers are expected to post a 7.02% CAGR through 2031. Each new campus deploys duplicate low-voltage switchboards with 100 kA withstand ratings and real-time thermal scans to honor five-nines availability targets.

Amazon’s AUD 20 billion program earmarked substantial electrical capex, underpinning Australia's switchgear market demand for arc-flash mitigation. Rail, tunnel, and airport projects, such as WestConnex and Sydney Metro, strengthen the infrastructure slice, while renewable integration and battery-storage nodes ensure high-specification medium-voltage gear remains prominent. The mix positions switchgear vendors to leverage both long-cycle utility projects and fast-cycle private facilities.

Geography Analysis

New South Wales, Victoria, and Queensland together accounted for roughly 70% of Australia switchgear market value in 2025 due to dense load centers, large renewable zones, and multi-gigawatt transmission builds. Transgrid’s HumeLink and Sydney Ring alone will need more than 50 500 kV and 330 kV breakers, reinforcing New South Wales as the epicenter for high-voltage orders. Victoria is boosting GIS uptake in Melbourne due to land scarcity and the integration of offshore wind, with AusNet selecting compact 275 kV bays for urban sites.[3] Queensland’s Central and North renewable corridors secured GE Vernova’s April 2025 contract for 69 245 kV units, illustrating steady high-voltage demand.

Western Australia’s Pilbara mining province drives sales of containerized and IP65-rated switchgear. BHP, Rio Tinto, and Fortescue are electrifying operations and building hybrid microgrids that favor ruggedized 11 kV and 33 kV assemblies. South Australia and Tasmania represent emerging pockets. Hornsdale’s pioneering 150 MW battery validated medium-voltage bidirectional schemes, while the proposed 1,500 MW Marinus Link will lift high-voltage requirements at both terminal stations.

The Northern Territory’s remote microgrids and the Australian Capital Territory’s urban infill substations add niche opportunities below 33 kV. Incentives in New South Wales and Victoria for SF₆-free technology encourage early adoption of vacuum GIS, aiding Australia switchgear market penetration for eco-designs. Carbon credits awarded for greenhouse-gas avoidance sweeten the economics, and state agencies are crowding in private capital by recognizing switchgear upgrades within net-zero pathways.

Competitive Landscape

Global manufacturers ABB, Schneider Electric, Siemens, and Hitachi Energy capture roughly 60% of the Australian switchgear market revenue via framework agreements and 24-hour service networks. Schneider Electric ranked first among microgrid integrators in October 2025, illustrating its strategy to bundle switchgear, inverters, and controls into turnkey offerings. Hitachi Energy’s USD 4.5 billion global capacity program, announced in 2024, includes lines dedicated to high-voltage dead-tank breakers suited to HumeLink and Marinus Link timelines.

Local integrators add agility. NOJA Power extends from outdoor reclosers to indoor solid-dielectric gear, capturing distribution utility tenders. Ampcontrol leverages its mining pedigree to offer IP65 enclosures that withstand vibration and dust, while Southern Cross Electrical Engineering bundles switchgear with an EPC scope, winning AUD 125 million in awards in December 2024. White-space potential emerges around SF₆-free MV, containerised hybrid systems, and IEC 62351-compliant digital yards that secure operational technology networks.

Competition intensifies as utilities demand native IEC 61850 connectivity and predictive analytics. Smaller suppliers differentiate through rapid customisation and local inventory but lack the R&D budgets for proprietary vacuum interrupter technology, confining them to low- and medium-voltage niches. Conversely, multinationals can amortise semiconductor-based breaker research across global volumes, sustaining margins despite copper volatility and inflation.

Australia Switchgear Industry Leaders

ABB Ltd.

Schneider Electric SE

Siemens AG

Eaton Corporation PLC

Toshiba International Corporation Pty Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Schneider Electric and UCS Group partnered to deliver intelligent microgrids that integrate switchgear, storage, and renewables for remote industrial clients.

- September 2025: Hitachi Energy supplied 66 kV equipment for AusNet’s 300 MW Mortlake battery, adding 650 MWh of fast-response capacity to the Victorian grid.

- May 2025: ABB delivered a 500 MW eHouse for Synergy’s Collie battery that halved on-site commissioning time.

- May 2025: Siemens Energy won a contract for synchronous condensers and 132 kV gear at Central-West Orana renewable zone to support voltage stability.

- May 2025: Hitachi Energy secured 330 kV SF₆-free breakers for Central-West Orana, reinforcing New South Wales’ renewable integration spine.

Australia Switchgear Market Report Scope

The Australia Switchgear Market Report is Segmented by Voltage Class (Low Voltage, Medium Voltage, and High Voltage), by Insulation Type (Air-Insulated, Gas-Insulated, Hybrid/Mixed Dielectric, and Solid and Vacuum-Insulated), by Installation (Indoor, and Outdoor), by End-User (Utilities, Commercial and Public Infrastructure, Industrial, and Residential and Distributed Energy Hubs), by Application (Transmission and Distribution, Renewable Integration and BESS, Infrastructure and Transportation, Mining and Resources, and Data-Centres and Critical Facilities). The Market Forecasts are Provided in Terms of Value (USD).

By Voltage Class

| Low Voltage (Upto 1 kV) |

| Medium Voltage (1- 36 kV) |

| High Voltage (More than 36 kV) |

By Insulation Type

| Air-Insulated Switchgear (AIS) |

| Gas- Insulated Switchgear (GIS) |

| Hybrid/ Mixed Dielectric |

| Solid and Vacuum- Insulated |

By Installation

| Indoor |

| Outdoor |

By End-User

| Utilities (Transmission and Distribution) |

| Commercial and Public Infrastructure |

| Industrial (incl. Mining, Oil & Gas, Process) |

| Residential & Distributed Energy Hubs |

By Application

| Transmission and Distribution |

| Renewable Integration and BESS |

| Infrastructure and Transportation |

| Mining and Resources |

| Data-Centres & Critical Facilities |

| By Voltage Class | Low Voltage (Upto 1 kV) |

| Medium Voltage (1- 36 kV) | |

| High Voltage (More than 36 kV) | |

| By Insulation Type | Air-Insulated Switchgear (AIS) |

| Gas- Insulated Switchgear (GIS) | |

| Hybrid/ Mixed Dielectric | |

| Solid and Vacuum- Insulated | |

| By Installation | Indoor |

| Outdoor | |

| By End-User | Utilities (Transmission and Distribution) |

| Commercial and Public Infrastructure | |

| Industrial (incl. Mining, Oil & Gas, Process) | |

| Residential & Distributed Energy Hubs | |

| By Application | Transmission and Distribution |

| Renewable Integration and BESS | |

| Infrastructure and Transportation | |

| Mining and Resources | |

| Data-Centres & Critical Facilities |

Key Questions Answered in the Report

What is the forecast value of the Australia switchgear market in 2031?

The market is projected to reach USD 2.15 billion by 2031.

Which voltage class is growing the fastest in Australia?

High-voltage switchgear, driven by 500 kV and 330 kV transmission projects, is forecast to expand at a 6.87% CAGR to 2031.

Why are utilities switching away from SF₆ technology?

Proposed 2030 regulations mandate SF₆-free gear above 145 kV, prompting utilities to adopt vacuum or dry-air insulation that cuts greenhouse-gas liabilities and insurance costs.

How are battery storage projects influencing switchgear demand?

Grid-scale batteries raise fault currents, requiring higher-rating medium-voltage breakers and factory-built eHouses to accelerate installation timelines.

Which companies dominate the high-voltage segment?

ABB, Schneider Electric, Siemens, and Hitachi Energy hold about 60% of revenue through long-term framework agreements with transmission owners.

What supply-chain risks affect switchgear procurement?

Global copper shortages have stretched delivery of 40 kA breakers to 25 weeks, leading Australian utilities to place orders up to two years in advance.

Page last updated on: