Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

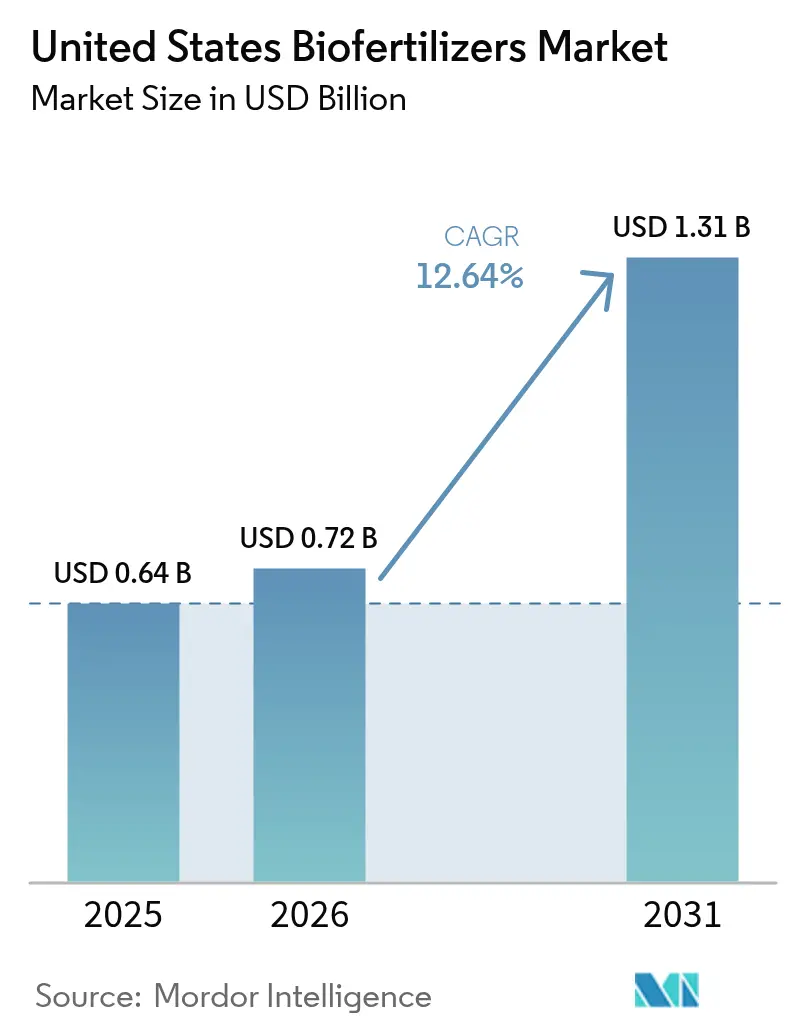

| Base Year Market Size (2025) | USD 0.64 Billion |

| Market Size (2026) | USD 0.72 Billion |

| Market Size (2031) | USD 1.31 Billion |

| Growth Rate (2026 - 2031) | 12.64% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Biofertilizers Market Analysis by Mordor Intelligence

The United States biofertilizers market size is expected to grow from USD 0.64 billion in 2025 to USD 0.72 billion in 2026 and is forecast to reach USD 1.31 billion by 2031 at 12.64% CAGR over 2026-2031. Steady federal incentives, volatile synthetic fertilizer prices, and surging demand for sustainably grown food are reshaping crop-input strategies across major production regions. Row-crop growers are integrating microbial solutions to trim nitrogen costs, while specialty producers adopt certified biological inputs to protect premium price points. Technology upgrades in microbial consortia, seed-treatment delivery, and encapsulation are widening product functionality, and venture-backed firms are accelerating time-to-market through aggressive scale-up partnerships. Although competitive fragmentation prevails, leading incumbents leverage fermentation capacity, distribution reach, and regulatory experience to defend share in this expanding arena.

Key Report Takeaways

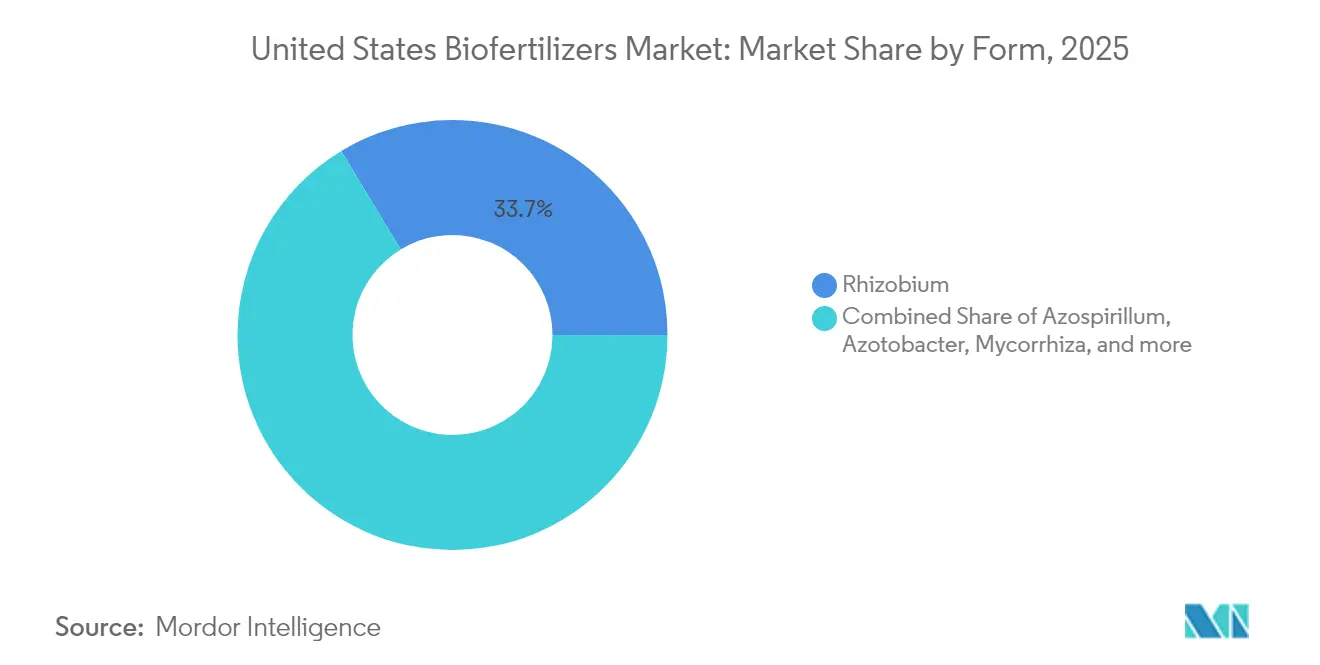

- By form, Rhizobium formulations led with 33.65% of the United States biofertilizers market share in 2025, and are projected to post the fastest 12.98% CAGR through 2031.

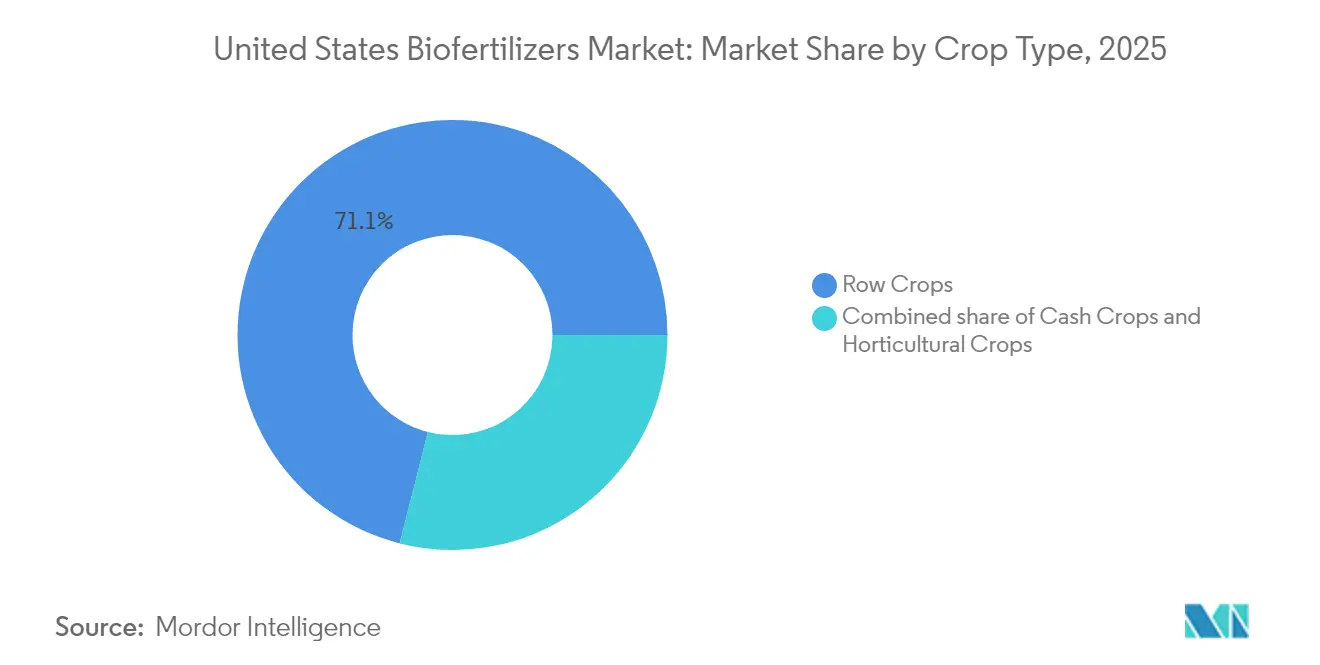

- By crop type, Row Crops accounted for 71.05% of the United States biofertilizers market size in 2025, and are forecast to expand at a 13.44% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Biofertilizers Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising adoption of regenerative agriculture | +2.1% | Midwest corn-belt, expanding to Plains states | Medium term (2-4 years) |

| U.S. federal incentives for carbon-smart farming | +1.8% | National, with concentrated benefits in commodity regions | Short term (≤ 2 years) |

| Cost advantage over synthetic fertilizers | +1.5% | National, with highest impact in high-input cropping systems | Short term (≤ 2 years) |

| Rapid growth of organic packaged food demand | +1.3% | California, Pacific Northwest, Northeast specialty regions | Medium term (2-4 years) |

| Emerging microbial consortia technologies | +1.1% | National, with early adoption in research-intensive regions | Long term (≥ 4 years) |

| Venture-capital funding into ag-bio startups | +0.9% | National, concentrated in innovation hubs | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of regenerative agriculture

United States Department of Agriculture (USDA) conservation programs now enroll 15.4 million acres in cover-cropping, reduced-tillage, and nutrient-management schemes that reward microbial input use[1]Source: UNITED STATES DEPARTMENT OF AGRICULTURE, “Partnerships for Climate-Smart Commodities Funding List,” usda.gov. Independent meta-analysis of 47 on-farm trials shows biological inoculants lift corn-soybean system profits USD 34 per acre when paired with diversified rotations. Carbon-credit aggregators such as Indigo Ag, Inc. pay growers USD 15–20 per verified ton of soil carbon, and regenerative protocols often specify nitrogen-fixing microbes as eligible practices. These stacked revenue channels shorten product payback periods to a single season for many growers. Peer-to-peer networks, including Practical Farmers of Iowa, amplify success stories through 90 farmer field days each summer, tightening the feedback loop that turns early adopters into regional advocates. As social license to operate becomes a branding requirement for grain merchandisers, regenerative benchmarks further lock biofertilizers into corporate-sourcing scorecards.

Rapid growth of organic packaged food demand

United States organic food sales climbed to USD 61.9 billion in 2024, and packaged segments recorded 8.4% growth, outpacing produce for the first time[2]Source: ORGANIC TRADE ASSOCIATION, “U.S. Organic Industry Survey 2025,” ota.co. Supermarkets added 3,400 private-label organic SKUs during 2024, locking retailers into supply agreements that guarantee organic-certified acreage expansions. National Organic Program rules forbid synthetic nitrogen and most mined phosphorus, making biofertilizers a compulsory line item for compliance. Organic processors now offer price premiums of USD 0.40 per pound for tomatoes documented with microbial nutrition plans, giving growers an economic escalator to offset higher per-unit product costs. Restaurant-chain sustainability pledges, notably by Chipotle Mexican Grill, Inc., further amplify pull-through by linking menu carbon footprints to supplier practices that privilege bio-based fertilizers.

U.S. federal incentives for carbon-smart farming

The Inflation Reduction Act channels USD 19.5 billion into the United States Department of Agriculture (USDA) programs that subsidize biological inputs through Conservation Stewardship Program enhancements of USD 40–60 per acre on qualifying fields. Partnerships for Climate-Smart Commodities directed USD 3.1 billion toward 141 projects, and 67% of them list microbial fertilizers as a core intervention that documents greenhouse-gas cuts. Early evidence from a USDA-funded Iowa State University pilot indicates a reduction in nitrous-oxide equivalents per acre when rhizobial seed treatments replace one-third of synthetic nitrogen. As cost-share contracts run five years, biofertilizer vendors secure recurring demand streams while farmers de-risk trials. State programs compound the pull; Minnesota’s Soil Health Financial Assistance Program adds USD 15 per acre on top of federal dollars for microbial adoption in impaired-watershed counties. Together, these incentives create a multi-layered safety net that accelerates volume growth well before commodity-price signals alone would justify the switch.

Cost advantage over synthetic fertilizers

Natural-gas volatility kept anhydrous ammonia above USD 1,100 per short metric ton for nine of the past 18 months, the third-highest streak of the century. Land-grant university budgets show that every USD 100 rise in ammonia lifts direct input costs USD 12 per corn acre, eroding margins at fixed cash-rent rates. Supply-chain risk adds a hidden premium; spring 2025 barge delays on the Mississippi River pushed spot urea 18% higher, whereas on-farm stored inoculants insulated participating growers from price spikes. Forward-pricing tools offered by cooperatives now bundle biofertilizers with fuel and herbicide contracts, spreading risk across a broader input basket that CFOs can hedge more easily. As lenders tighten working-capital covenants, the ability to cut prepaid fertilizer bills becomes a deciding factor in operating-loan approvals.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited farmer awareness in corn-belt states | -1.4% | Midwest commodity regions, rural agricultural communities | Medium term (2-4 years) |

| Inconsistent field performance across climates | -1.1% | National, with highest impact in extreme climate zones | Short term (≤ 2 years) |

| Short product shelf-life in liquid formulations | -0.8% | Southern states, long-distance distribution routes | Short term (≤ 2 years) |

| Regulatory uncertainty around microbial strains | -0.6% | National, affecting innovation pipeline development | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited farmer awareness in corn-belt states

Surveys by Stratovation Group show only 24% of corn-soybean operators in Iowa, Illinois, and Indiana have trialed biologicals, and 41% of non-users cite “no trusted local data” as a chief barrier. Extension staff-to-farmer ratios deteriorated to 1:1,750 in 2024, curtailing hands-on demonstrations that historically accelerated technology transfer. Peer-reviewed yield studies often reference coastal or irrigated environments, deepening skepticism in rain-fed heartland systems. Tile-drainage installers and crop consultants, who strongly influence input decisions, receive limited formal training in microbiology, so their recommendations trend toward conventional fertilizers. Retailer incentives compound inertia; co-ops earn higher margins on bulk anhydrous ammonia than on packaged inoculants, subtly steering sales conversations. Absent robust testimonials from trusted neighbors, many producers defer biological adoption until cost-share payments surpass perceived risk.

Inconsistent field performance across climates

Variability in soil organic matter, pH, and moisture regimes drives a 15–30% swing in measured efficacy across regional trials, dampening confidence in product claims. High-temperature episodes above 100°F in Texas’ High Plains can push rhizobial mortality to 60% within two days of application unless protected by spore-coating technology. Conversely, saturated spring soils in the Red River Valley limit oxygen diffusion, stalling aerobic bacterial activity for weeks. Manufacturers pursue climate-zonal strain selections, yet the catalog remains thin for arid-alkaline conditions prevalent in the Southwest. Insurance products that guarantee yield outcomes are still embryonic, leaving growers to shoulder performance risk. Until data repositories catalog multi-year, multi-soil outcomes at the county scale, agronomists will continue to recommend stepwise, rather than full-rate, adoption.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Form: Rhizobium Dominance Drives Nitrogen Innovation

Rhizobium captured 33.65% of the United States biofertilizers market share in 2025, reflecting decades of validated nitrogen-fixation performance in soybeans and pulses. The segment is projected to scale at a 12.98% CAGR through 2031 as inoculation rates climb among corn-belt growers who seek to hedge fertilizer exposure. The United States biofertilizers market size benefits from seed-treatment compatibility that positions Rhizobium products as a turnkey addition to precision-planting routines. Competitive differentiation increasingly hinges on strain heat tolerance, pelleting stability, and shelf-life guarantees.

The Azospirillum and Azotobacter categories maintain niche relevance in non-leguminous cereals, supplying up to 20 kg of atmospheric nitrogen per hectare under split application regimes. Mycorrhizal formulations expand nutrient-uptake efficiency in high-value horticultural crops, where root health influences fruit quality premiums. Phosphate-solubilizing bacteria command double-digit growth in phosphorus-limited calcareous soils of the southern United States. Multi-organism consortia emerge as the frontier, bundling Rhizobium, Bacillus, and Trichoderma strains for holistic soil-health outcomes that win organic certification endorsements.

By Crop Type: Row Crops Scale Meets Horticultural Premium

Row Crops accounted for 71.05% of the United States biofertilizers market size in 2025, and at the same time, growing at 13.44% CAGR through 2031 on the strength of combined corn and soybean acres. Usage intensity is rising because variable-rate applicators reduce per-acre labor costs and facilitate seamless integration with broadacre production schedules. Nationwide carbon-credit pilots elevate adoption further by monetizing nitrogen-use reductions at the farm-enterprise level.

The use of biofertilizers in Horticultural Crops is rising due to the stringent United States Department of Agriculture National Organic Program standards that prohibit most synthetics. Organic strawberry and leafy-green acreage in California and Arizona must document input provenance, which drives demand for OMRI-listed inoculants. Cash Crops, including cotton and sugar beet, sit between scale and premium paradigms and present an emergent target for companies engineering climate-adapted microbial blends. The United States biofertilizers market share in Cash Crops is projected to widen as pilot results translate into harvest-quality improvements that fetch contracting bonuses.

Geography Analysis

California remains the largest single-state purchaser, underpinned by organic produce sector that mandates biological nutrient solutions Specialty vineyards, orchards, and vegetable farms prioritize soil-microbiome management to safeguard terroir attributes, and the state’s clear regulatory pathway under Senate Bill 1522 accelerates commercial rollouts.

Midwest adoption momentum stems from combined Conservation Stewardship Program incentives and heightened nitrogen-price risk. Producers in Iowa and Illinois increasingly integrate seed-applied inoculants that deliver logistical simplicity and consistent stand establishment. Alltech, Inc.’s new Nicholasville, Kentucky, plant will manufacture 66,000 gallons of liquid biofertilizer per shift to shorten lead times in the region and ensure product freshness en route to farm retailers.

Southern and Western growers balance climate stress with diverse cropping patterns, and the winter-vegetable industry favors climate-adapted granular formulations that withstand 110°F in-field temperatures, while Texas cotton producers experiment with encapsulated nitrogen fixers to offset high urea costs. Pacific Northwest apple orchards lean on mycorrhizal inoculants that promote phosphorus uptake in volcanic soils, and Washington State University trial networks supply localized efficacy data that strengthen purchasing confidence among family-run operations.

Competitive Landscape

The United States biofertilizers market remains fragmented; the top five manufacturers hold a minor combined share. Novozymes A/S leads by leveraging back-integrated fermentation and the February 2024 merger with Chr. Hansen Holding A/S to form Novonesis A/S, a biosolutions group. Other major players include Rizobacter Argentina S.A., Symborg Inc., Kula Bio, Inc., and Sustane Natural Fertilizer, Inc.

Market entrants differentiate through encapsulation science, as illustrated by AgroSpheres, Inc., whose AgriCell technology shields microbes from ultraviolet degradation and tank-mix shear forces. Another disruptor, MustGrow Biologics Corp., applies mustard-derived bioactive compounds to a carbon-rich carrier that meets USDA National Organic Program criteria and extends shelf life to 30 months at ambient storage. Intellectual-property footprints are expanding; BioConsortia, Inc. now holds 40 United States patents covering trait-stacked microbial consortia.

The Strategic alliances accelerate the route-to-market. Indigo Ag, Inc. rolled out the CLIPS automatic dry-powder applicator in September 2024, easing the burden of last-mile seed-box treatments for retailers. DPH Biologicals LLC introduced Envelix Prime to bridge the liquid-granular divide for blended fertilizer compatibility, and Syngenta Crop Protection, LLC partnered with Intrinsyx Bio, Inc. to co-develop endophyte-based seed treatments that reduce phosphorus inputs by up to 20% in small-grain cereals. Private-equity interest is building as fund managers seek decarbonization plays aligned with the United States Securities and Exchange Commission climate-disclosure rules.

United States Biofertilizers Industry Leaders

Novonesis A/S

Rizobacter Argentina S.A.

Symborg Inc.

Kula Bio, Inc.

Sustane Natural Fertilizer, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Nitricity (United States) secured USD 50 million in Series B funding to expand its organic nitrogen bio-fertilizer (Ash Tea) production, which uses almond waste as raw material. The company plans to establish a new facility in Delhi, California, to serve U.S. and global markets, with operations anticipated to begin in 2026.

- July 2025: Alltech Inc.'s Crop Science division received a USD 2.34 million grant from the USDA's Fertilizer Production Expansion Program (FPEP). The grant will support the construction of a USD 4.6 million biofertilizer manufacturing facility in Nicholasville, Kentucky, United States, covering 15,000 square feet.

- November 2024: Innovafeed's U.S. operations received a USD 11 million grant from the United States Department of Agriculture (USDA) to produce insect-based organic fertilizer (insect frass) for plant nutrition in Illinois.

United States Biofertilizers Market Report Scope

The United States Biofertilizers Market Report is Segmented by Form (Azospirillum, Azotobacter, Mycorrhiza, Phosphate Solubilizing Bacteria, Rhizobium, Other Biofertilizer), Crop Type (Cash Crops, Horticultural Crops, Row Crops). The Market Forecasts are Provided in Terms of Value (USD) and Volume (Metric Tons).

Form

| Azospirillum |

| Azotobacter |

| Mycorrhiza |

| Phosphate Solubilizing Bacteria |

| Rhizobium |

| Other Biofertilizer |

Crop Type

| Cash Crops |

| Horticultural Crops |

| Row Crops |

| Form | Azospirillum |

| Azotobacter | |

| Mycorrhiza | |

| Phosphate Solubilizing Bacteria | |

| Rhizobium | |

| Other Biofertilizer | |

| Crop Type | Cash Crops |

| Horticultural Crops | |

| Row Crops |

Market Definition

- AVERAGE DOSAGE RATE - The average application rate is the average volume of biofertilizers applied per hectare of farmland in the respective region/country.

- CROP TYPE - Crop type includes Row crops (Cereals, Pulses, Oilseeds), Horticultural Crops (Fruits and vegetables) and Cash Crops (Plantation Crops, Fibre Crops and Other Industrial Crops)

- FUNCTION - The crop nutrition function of agricultural biological consists of various products that provide essential plant nutrients and enhance soil quality.

- TYPE - Biofertilizers enhance soil quality by increasing the population of beneficial microorganisms. They help crops absorb nutrients from the environment.

| Keyword | Definition |

|---|---|

| Cash Crops | Cash crops are non-consumable crops sold as a whole or part of the crop to manufacture end-products to make a profit. |

| Integrated Pest Management (IPM) | IPM is an environment-friendly and sustainable approach to control pests in various crops. It involves a combination of methods, including biological controls, cultural practices, and selective use of pesticides. |

| Bacterial biocontrol agents | Bacteria used to control pests and diseases in crops. They work by producing toxins harmful to the target pests or competing with them for nutrients and space in the growing environment. Some examples of commonly used bacterial biocontrol agents include Bacillus thuringiensis (Bt), Pseudomonas fluorescens, and Streptomyces spp. |

| Plant Protection Product (PPP) | A plant protection product is a formulation applied to crops to protect from pests, such as weeds, diseases, or insects. They contain one or more active substances with other co-formulants such as solvents, carriers, inert material, wetting agents or adjuvants formulated to give optimum product efficacy. |

| Pathogen | A pathogen is an organism causing disease to its host, with the severity of the disease symptoms. |

| Parasitoids | Parasitoids are insects that lay their eggs on or within the host insect, with their larvae feeding on the host insect. In agriculture, parasitoids can be used as a form of biological pest control, as they help to control pest damage to crops and decrease the need for chemical pesticides. |

| Entomopathogenic Nematodes (EPN) | Entomopathogenic nematodes are parasitic roundworms that infect and kill pests by releasing bacteria from their gut. Entomopathogenic nematodes are a form of biocontrol agents used in agriculture. |

| Vesicular-arbuscular mycorrhiza (VAM) | VAM fungi are mycorrhizal species of fungus. They live in the roots of different higher-order plants. They develop a symbiotic relationship with the plants in the roots of these plants. |

| Fungal biocontrol agents | Fungal biocontrol agents are the beneficial fungi that control plant pests and diseases. They are an alternative to chemical pesticides. They infect and kill the pests or compete with pathogenic fungi for nutrients and space. |

| Biofertilizers | Biofertilizers contain beneficial microorganisms that enhance soil fertility and promote plant growth. |

| Biopesticides | Biopesticides are natural/bio-based compounds used to manage agricultural pests using specific biological effects. |

| Predators | Predators in agriculture are the organisms that feed on pests and help control pest damage to the crops. Some common predator species used in agriculture include ladybugs, lacewings, and predatory mites. |

| Biocontrol agents | Biocontrol agents are living organisms used to control pests and diseases in agriculture. They are alternatives to chemical pesticides and are known for their lesser impact on the environment and human health. |

| Organic Fertilizers | Organic fertilizer is composed of animal or vegetable matter used alone or in combination with one or more non-synthetically derived elements or compounds used for soil fertility and plant growth. |

| Protein hydrolysates (PHs) | Protein hydrolysate-based biostimulants contain free amino acids, oligopeptides, and polypeptides produced by enzymatic or chemical hydrolysis of proteins, primarily from vegetal or animal sources. |

| Biostimulants/Plant Growth Regulators (PGR) | Biostimulants/Plant Growth Regulators (PGR) are substances derived from natural resources to enhance plant growth and health by stimulating plant processes (metabolism). |

| Soil Amendments | Soil Amendments are substances applied to soil that improve soil health, such as soil fertility and soil structure. |

| Seaweed Extract | Seaweed extracts are rich in micro and macronutrients, proteins, polysaccharides, polyphenols, phytohormones, and osmolytes. These substances boost seed germination and crop establishment, total plant growth and productivity. |

| Compounds related to biocontrol and/or promoting growth (CRBPG) | Compounds related to biocontrol or promoting growth (CRBPG) are the ability of a bacteria to produce compounds for phytopathogen biocontrol and plant growth promotion. |

| Symbiotic Nitrogen-Fixing Bacteria | Symbiotic nitrogen-fixing bacteria such as Rhizobium obtain food and shelter from the host, and in return, they help by providing fixed nitrogen to the plants. |

| Nitrogen Fixation | Nitrogen fixation is a chemical process in soil which converts molecular nitrogen into ammonia or related nitrogenous compounds. |

| ARS (Agricultural Research Service) | ARS is the U.S. Department of Agriculture's chief scientific in-house research agency. It aims to find solutions to agricultural problems faced by the farmers in the country. |

| Phytosanitary Regulations | Phytosanitary regulations imposed by the respective government bodies check or prohibit the importation and marketing of certain insects, plant species, or products of these plants to prevent the introduction or spread of new plant pests or pathogens. |

| Ectomycorrhizae (ECM) | Ectomycorrhiza (ECM) is a symbiotic interaction of fungi with the feeder roots of higher plants in which both the plant and the fungi benefit through the association for survival. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market-size estimations for the forecast years are in nominal terms. Inflation is not a part of the pricing, and the average selling price (ASP) is kept constant throughout the forecast period.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms.