Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

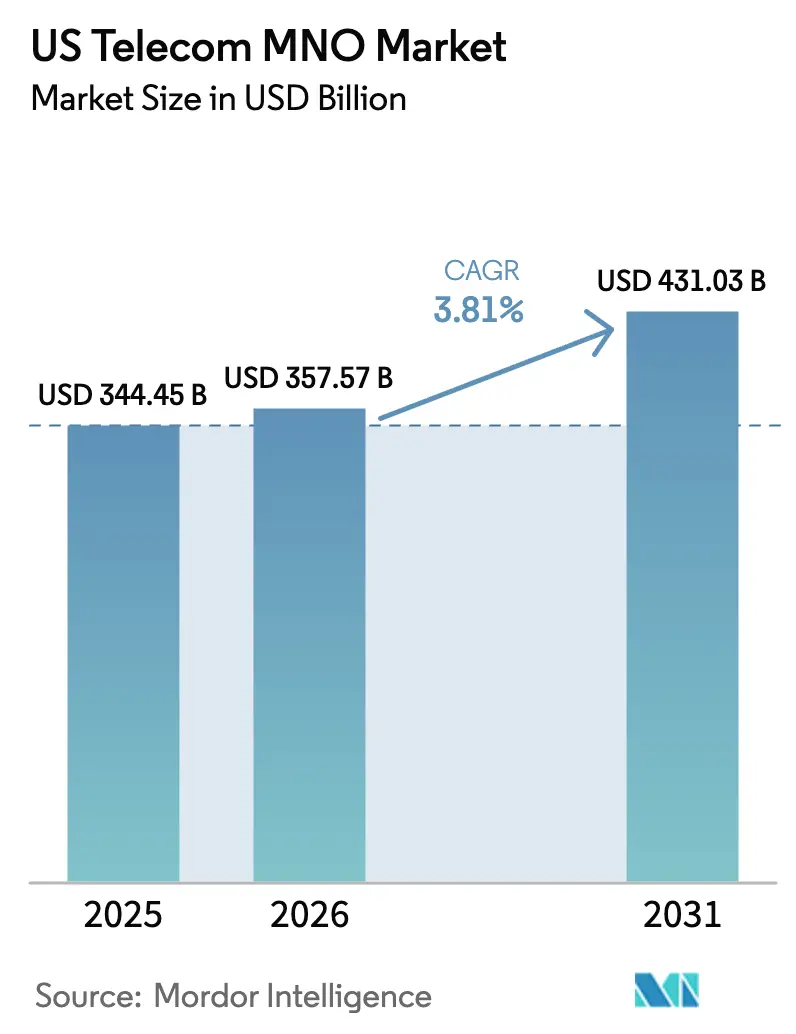

| Base Year Market Size (2025) | USD 344.45 Billion |

| Market Size (2026) | USD 357.57 Billion |

| Market Size (2031) | USD 431.03 Billion |

| Growth Rate (2026 - 2031) | 3.81% CAGR |

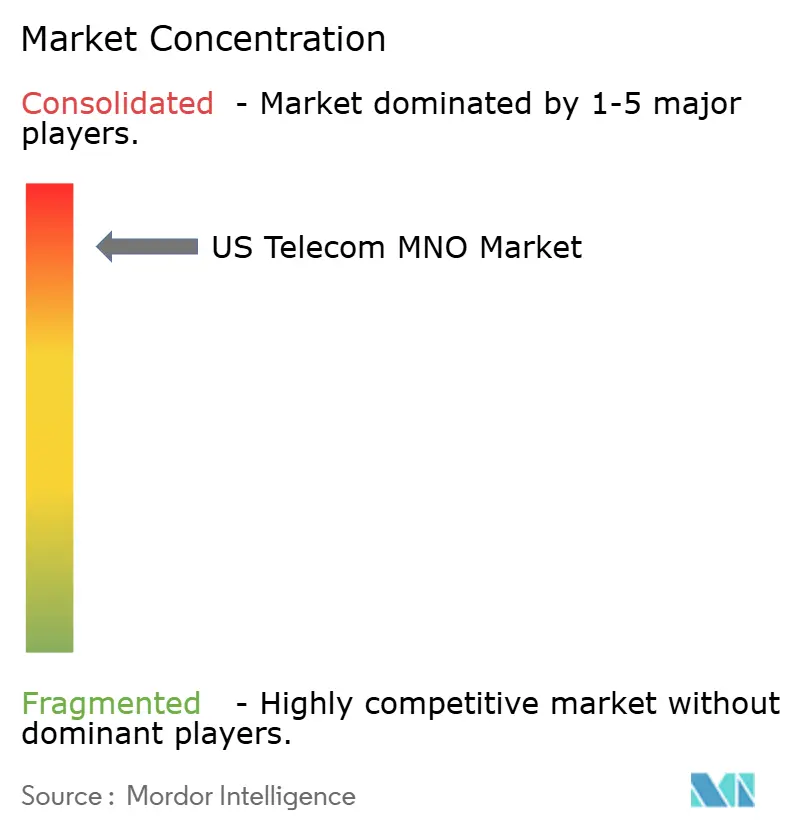

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

US Telecom MNO Market Analysis by Mordor Intelligence

US Telecom MNO market size in 2026 is estimated at USD 357.57 billion, growing from 2025 value of USD 344.45 billion with 2031 projections showing USD 431.03 billion, growing at 3.81% CAGR over 2026-2031.

This steady trajectory reflects a mature arena in which legacy voice and messaging streams shrink while data-heavy applications, private cellular deployments, and integrated enterprise platforms expand margins. Heightened monetization of costly 5G assets is central to growth, with operators rolling out premium service tiers, network-as-a-service propositions, and low-latency edge nodes. Private and public sector subsidies for rural coverage, aggressive monetization of spectrum holdings, and AI-driven network automation continue to widen total addressable revenue pools. Competitive intensity remains contained because three national carriers dominate spectrum depth and retail distribution, allowing disciplined pricing even as prepaid churn rises. Capital discipline, energy optimization, and spectrum refarming collectively underpin operators’ ability to fund continued densification without materially eroding free cash flow [1]Federal Communications Commission, “5G Mid-Band Spectrum Update,” fcc.gov.

Key Report Takeaways

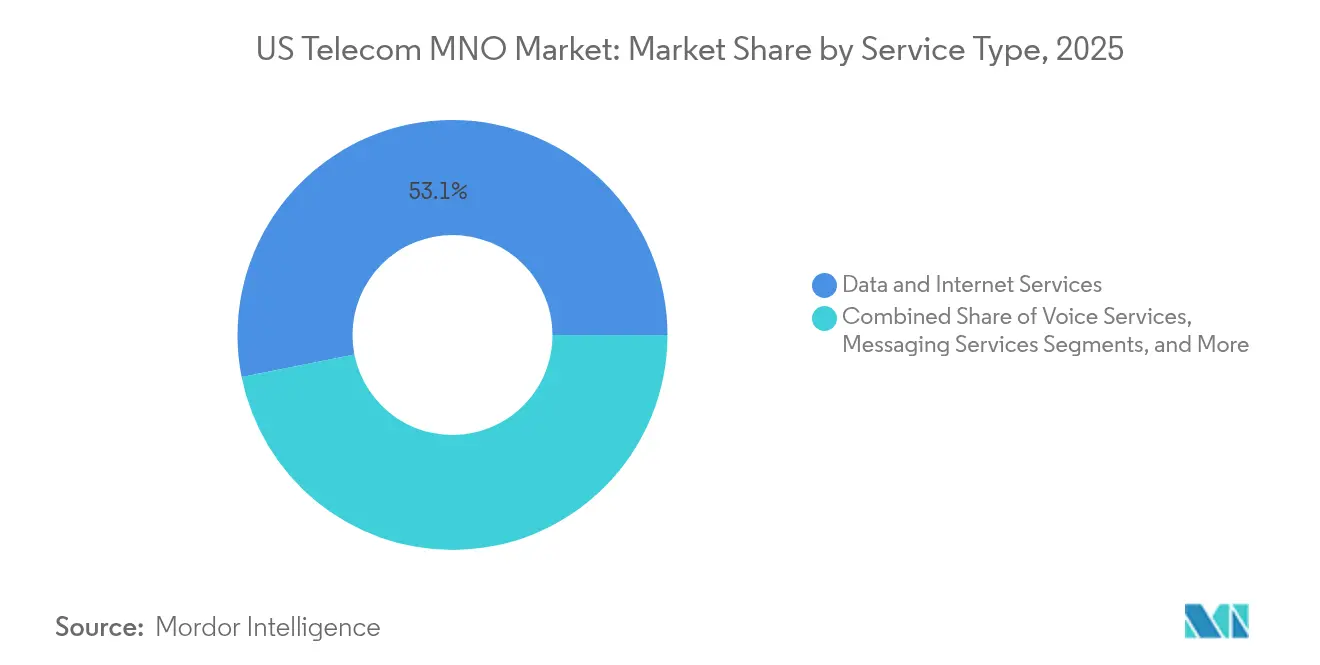

- By service type, data and internet captured 53.12% of the US Telecom MNO market share in 2025. IoT and M2M are projected to advance at a 3.92% CAGR through 2031.

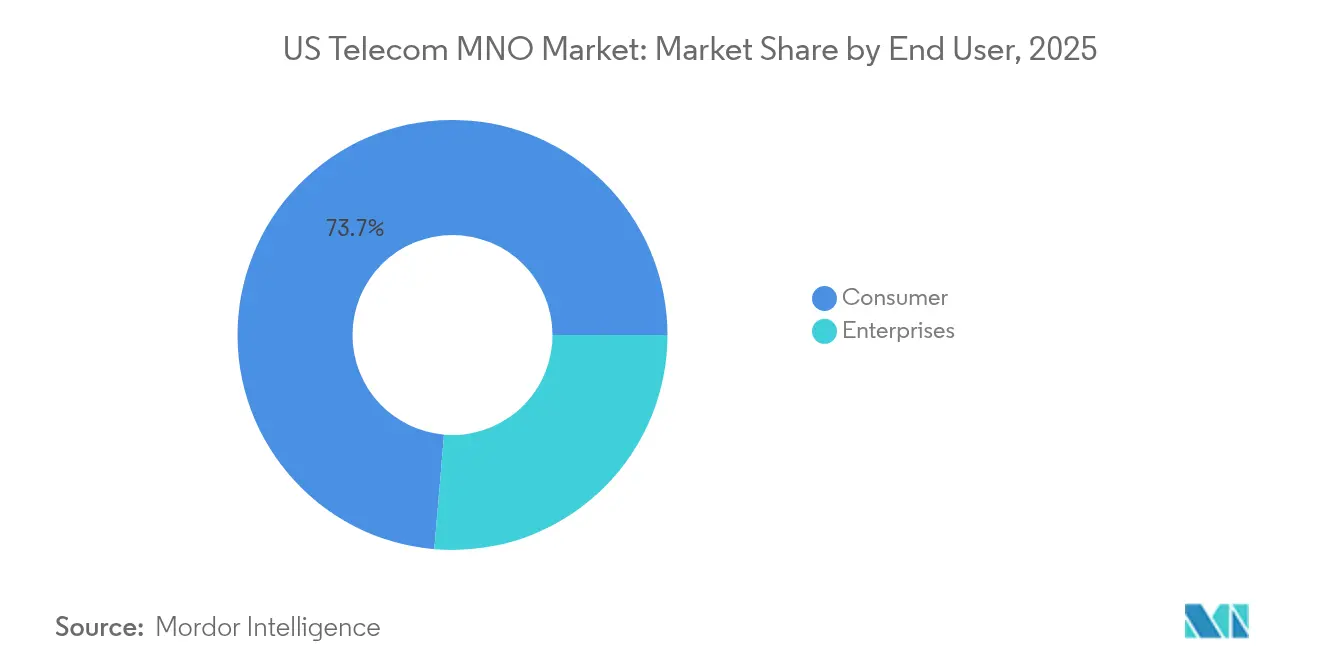

- By end user, the consumer segment held 73.65% revenue share of the US Telecom MNO market size in 2025. The enterprise segment is forecast to post a 4.15% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

US Telecom MNO Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| 5G stand-alone core roll-outs accelerating data monetization | +1.2% | National metro clusters | Medium term (2-4 years) |

| Fixed-wireless access (FWA) displacing legacy copper | +0.8% | Rural and suburban markets | Short term (≤ 2 years) |

| eSIM-only device launches simplifying churn | +0.4% | Urban centers | Medium term (2-4 years) |

| Federal BEAD and middle-mile grants stimulating rural build-outs | +0.6% | Underserved counties nationwide | Long term (≥ 4 years) |

| Private-cellular demand from IIoT and campus networks | +0.5% | Industrial corridors | Medium term (2-4 years) |

| AI-driven RAN optimization lowering OPEX | +0.3% | Nationwide macro and small-cell grid | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

5G Stand-Alone Core Roll-outs Accelerating Data Monetization

Full migration to stand-alone (SA) architecture allows carriers to create virtual slices that guarantee latency and throughput, adding service differentiation unavailable on legacy non-stand-alone deployments. T-Mobile commercialized public-safety slices that already contribute USD 200 million in recurring annual revenue, while Verizon leverages SA to support sub-10 millisecond edge workloads for manufacturing robotics [2]Verizon Communications, “Verizon Announces Commercial 5G SA Core,” verizon.com. Enterprise deals often bundle API exposure so developers can embed carrier-grade authentication and billing directly into applications, a pathway to an estimated USD 20 billion platform revenue pool by 2028 [3]Ericsson AB, “Network API Monetization Opportunity,” ericsson.com. Higher-value network slices translate into 3-5 times the ARPU of mass-market mobile broadband, directly lifting the US Telecom MNO market.

Fixed-Wireless Access (FWA) Displacing Legacy Copper

National FWA subscriptions crossed the 10 million mark by end-2024 as mid-band and C-band spectrum enabled 300 Mbps average downlink in rural clusters. The product directly cannibalizes outdated DSL and coax footprints, fills fiber coverage gaps, and accelerates operators’ payback on 5G radios. FWA also strengthens household bundling, with wireless carriers attaching mobile lines at an 18% higher rate when a home internet account is present. Capacity constraints in dense suburbs trigger active-antenna expansions and spectrum-sharing algorithms, yet economics remain favorable relative to trenching. Rapid customer growth adds 0.8 percentage points to the US Telecom MNO market CAGR through 2027.

eSIM-Only Device Launches Simplifying Churn

Apple, Samsung, and Google now default flagship models to eSIM-only activation in the United States, eliminating physical SIM logistics and slashing carrier fulfillment costs by roughly USD 2 per gross add. Digital provisioning accelerates number portability but also empowers operators to embed instant-on trial offers during device setup. Carriers offset higher churn risk with loyalty bundles tied to cloud storage, streaming, and cybersecurity apps payable via a single click. Conversion analytics indicate a 12% uplift in average lifetime value for accounts onboarded via self-activated eSIM flows. The migration adds 0.4 percentage points of lift to the overall growth rate by enabling frictionless cross-selling of ancillary lines.

Federal BEAD and Middle-Mile Grants Stimulating Rural Build-outs

The USD 42.45 billion Broadband Equity, Access, and Deployment (BEAD) program requires funded projects to deliver at least 100/20 Mbps service, prompting states to prioritize fiber but still allocate wireless funds where trenching costs are prohibitive. By March 2025, 47 states and territories had completed challenge processes and begun obligating awards, accelerating backhaul deployments that mobile carriers can co-opt for macro-tower upgrades [4]National Telecommunications and Information Administration, “BEAD Progress Dashboard,” ntia.doc.gov. Louisiana’s early success shows that coordinated subsidy stacking delivers universal coverage ahead of schedule, highlighting the catalytic role of middle-mile assets that lower transport costs for 5G nodes. Grants collectively contribute 0.6 percentage points to the forecast CAGR for the US Telecom MNO market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Inflation-induced ARPU pressure in prepaid | -0.7% | Price-sensitive urban and rural segments | Short term (≤ 2 years) |

| Fiber over-builds eroding FWA economics | -0.5% | Select suburban counties | Medium term (2-4 years) |

| C-band aviation mitigation costs | -0.2% | National flight paths | Short term (≤ 2 years) |

| Heightened FCC scrutiny on M&A | -0.3% | Nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Inflation-Induced ARPU Pressure in Prepaid

Elevated energy and labor expenses compel carriers to raise plan prices, yet prepaid customers exhibit immediate churn when monthly bills climb by more than USD 5. AT&T’s 2025 upward revisions triggered a temporary 190-basis-point increase in prepaid churn, forcing larger retention credits and marketing spend. Operators now extend inclusive content bundles, high-data allotments, and buy-now-pay-later device financing to defend subscriber counts, trimming EBITDA margin by 40-60 basis points over the near term.

Fiber Over-builds Eroding FWA Economics

Regional electric co-ops, cable incumbents, and municipal utilities collectively announced 5.4 million new fiber passings for 2025-2027. Where fiber overlays mature FWA footprints, operators record up to 30% defection within 12 months as households migrate toward symmetrical gigabit speeds. Carriers pivot by steering new FWA installs toward markets with limited fiber competition and by launching Wi-Fi 7 gateways to bolster in-home performance. Even with mitigation, revenue erosion subtracts 0.5 percentage points from the baseline CAGR projected for the US Telecom MNO market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service Type: Data-Centric Revenues Outpace Legacy Streams

The data and internet category represented 53.12% of 2025 revenue, delivering the single-largest contribution to the US Telecom MNO market size. Unlimited smartphone plans, FWA subscriptions, and enterprise dedicated access collectively underpinned a 7.8% uplift in mobile data traffic per user year-on-year. Premium tiers exploiting carrier aggregation hit verified 5.5 Gbps throughput during 2025 field tests, reinforcing perceived speed leadership and justifying price differentials. Voice and SMS collectively fell below 10% revenue share as over-the-top substitutes drove double-digit usage declines. Meanwhile, IoT and M2M services posted the fastest trajectory, supported by 30 million incremental licensed cellular endpoints and a swelling pipeline of private network installs inside factories, ports, and hospitals. The sub-segment’s 3.92% CAGR through 2031 adds a long-run lift that offsets eroding legacy lines, thereby sustaining expansion in the US Telecom MNO market.

Enterprise data contracts increasingly request SLA-backed throughput and network-slice isolation, commands that draw higher margins and longer-term commitments than consumer lines. Wholesale roaming and virtual operator partnerships add incremental revenue but primarily serve to amortize spectrum assets during off-peak hours. Advanced analytics embedded in self-optimizing networks slash power draw by around 15% and thereby release opex for reinvestment in additional small cells, further reinforcing data-centric positioning across the US Telecom MNO market.

By End User: Enterprise Lines Gain Strategic Weight

The consumer segment still generated 73.65% of 2025 turnover; however, unit growth slowed to low single digits as smartphone penetration neared 90%. To protect yields, carriers package cloud storage, cybersecurity, and premium support inside loyalty bundles that lift revenue per account by 6-8%. In parallel, enterprise subscriptions rose at a 4.15% CAGR and are forecast to reach almost one-quarter of the total US Telecom MNO market size by 2031. Manufacturing, mining, logistics, and university campuses procure stand-alone private networks to enable latency-sensitive automation, CCTV analytics, and asset tracking. Carriers bundle consulting, edge computing, and managed security, turning connectivity into a full-stack offer that secures wallet share and lengthens contract duration. Integrated mobile-edge applications often command multi-year minimum revenue commitments exceeding USD 10 million, a material boost to average contract value throughout the US Telecom MNO industry.

Enterprises also press for open APIs that unlock real-time quality-of-service adjustments, stimulating standardized interface launches such as the Aduna platform. Carriers anticipate platform fees supplementing bandwidth sales, positioning themselves as orchestration hubs across multi-cloud and multi-site environments. Consumer and enterprise businesses increasingly share distributed computing nodes, spectrum assets, and tariff management systems, enabling carriers to sweat capital investments across the full US Telecom MNO market.

Geography Analysis

Although treated as one national market, the United States exhibits pronounced urban-rural performance divergence that impacts deployment schedules and capital intensity. Dense metropolitan clusters captured early 5G stand-alone launches because spectrum-layer cake architectures yield immediate monetization through premium smartphone tiers and network slices. Through 2025, operators installed nearly 11,000 additional C-band radios across the top 50 markets, lifting average downlink speed 28% and shoring up customer satisfaction metrics.

Rural strategy revolves around FWA, low-band coverage, and BEAD-funded fiber backhaul. Nearly USD 7.9 billion of planned BEAD awards are allocated to counties where wireline density is too sparse to justify private investment, enabling carriers to co-locate antennas on fiber-fed poles at subsidized rates. Where terrain frustrates aerial or buried fiber, carriers explore direct-to-device satellite roaming agreements to guarantee emergency coverage. These hybrid models secure voice and text continuity across 99.5% of the US landmass, a milestone operators highlight in marketing aimed at travelers, public safety agencies, and agriculture clients.

Sub-regional differentiation also emerges around the spectrum mix. Mid-band holdings dominate east-coast and Great Lakes clusters, whereas 600 MHz band layers carry a larger traffic share across the Great Plains. Millimeter-wave small cells concentrate in NFL stadiums, downtown promenades, and high-footfall transit terminals, supporting multi-gigabit bursts that accompany immersive fan and retail experiences. Spectrum-sharing trials under the Citizens Broadband Radio Service regime are most active along manufacturing belts from Michigan through Tennessee, reflecting the spread of Industry 4.0 pilots feeding enterprise revenue pools.

Competitive Landscape

Market power remains highly concentrated because Verizon, AT&T, and T-Mobile collectively control a significant share of subscribers, spectrum parcels, and retail storefronts. Such concentration places the US Telecom MNO market on the cusp of a natural oligopoly; price competition stays rational while differentiation centers on network quality, value-added services, and enterprise solution depth. Verizon retains the largest retail base at 157 million connections but has ceded 5G speed leadership to T-Mobile, which leverages its 2.5 GHz trove to post a 158.5 Mbps nationwide average. AT&T counters with enterprise-heavy positioning, bundling wireline, cloud, and security around its FirstNet public-safety franchise.

Each carrier aggressively deploys AI for predictive maintenance, traffic steering, and load balancing, reducing network opex by an estimated 15% and shrinking energy consumption per gigabyte. Strategic moves illustrate divergence: Verizon negotiated a 195,000-square-foot headquarters lease in Manhattan to centralize innovation labs; T-Mobile invested in satellite partner SpaceX to secure early direct-to-device texting and emergency roaming; AT&T focused on integrating network APIs into its Aduna collaboration to target fintech, healthcare, and insurance software developers. Outside the “big three,” regional carriers such as UScellular leverage CBRS and fixed wireless to defend rural bases, while MVNOs lean on price transparency and digital-only care to nibble at prepaid niches.

Competitive experimentation increasingly involves ecosystem alliances. Verizon, Ericsson, and Intel operate an open radio innovation center in Dallas; AT&T joined Qualcomm to pilot RedCap chipsets aimed at industrial sensors; T-Mobile inked an exclusive distribution deal for AR glasses bundled with unlimited 50 Mbps uplink slices. Satellite integration adds another vector: in 2025 Verizon and AT&T completed the first cellphone-to-satellite video call over AST SpaceMobile’s BlueBird platform, signaling early momentum toward direct-to-device coverage for sparsely populated corridors. These collaborative wagers seek to redefine market boundaries and maintain relevance as data traffic compounds.

US Telecom MNO Industry Leaders

Verizon Communications Inc.

AT&T Inc.

T-Mobile US, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Verizon announces new Manhattan headquarters at PENN 2, covering 195,000 ft² for 1,000 staff.

- June 2025: Verizon unveils AI-powered customer overhaul “Project 624” featuring Google AI and 400 additional retail outlets.

- April 2025: Verizon promises free satellite text messaging and a three-year price lock for myPlan users, leveraging LEO partnerships.

- February 2025: AT&T, T-Mobile, and Verizon launch standardized 5G network APIs through the Aduna platform.

- February 2025: AT&T and Verizon run the first cellphone-to-satellite video calls on AST SpaceMobile’s BlueBird satellites.

- February 2025: Verizon bundles Google One AI Premium (2 TB storage) for USD 10 per month inside myPlan and myHome offerings.

US Telecom MNO Market Report Scope

The study provides an in-depth analysis of the telecommunication industry in the United States. The United States telecom market is segmented by service into voice services (wired, wireless), data and messaging services, and OTT and pay TV.

Service Type

| Voice Services |

| Data and Internet Services |

| Messaging Services |

| IoT and M2M Services |

| OTT and PayTV Services |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) |

End-user

| Enterprises |

| Consumer |

| Service Type | Voice Services |

| Data and Internet Services | |

| Messaging Services | |

| IoT and M2M Services | |

| OTT and PayTV Services | |

| Other Services (VAS, Roaming and International Services, Enterprise and Wholesale Services, etc.) | |

| End-user | Enterprises |

| Consumer |

Key Questions Answered in the Report

How large is the US Telecom MNO market in 2026?

It stands at USD 357.57 billion and is projected to reach USD 431.03 billion by 2031, implying a 3.81% CAGR.

Which service line is growing the fastest?

IoT and M2M connections lead with a 3.92% CAGR, benefiting from private cellular and industrial automation roll-outs.

Who are the market leaders?

Verizon, AT&T, and T-Mobile control more than 95% of total revenue, shaping pricing and network investment patterns.

What role does fixed-wireless access play?

FWA surpassed 10 million lines in 2024, providing 300 Mbps household broadband where fiber is not yet economical.

How are federal subsidies influencing expansion?

The USD 42.45 billion BEAD program funds middle-mile and last-mile projects, enabling carriers to upgrade rural towers and backhaul.

Why is 5G stand-alone important?

SA cores enable network slicing and latency below 10 ms, unlocking premium enterprise use cases and multi-gigabit consumer speeds.

Page last updated on: