Turkey Medical Tourism Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

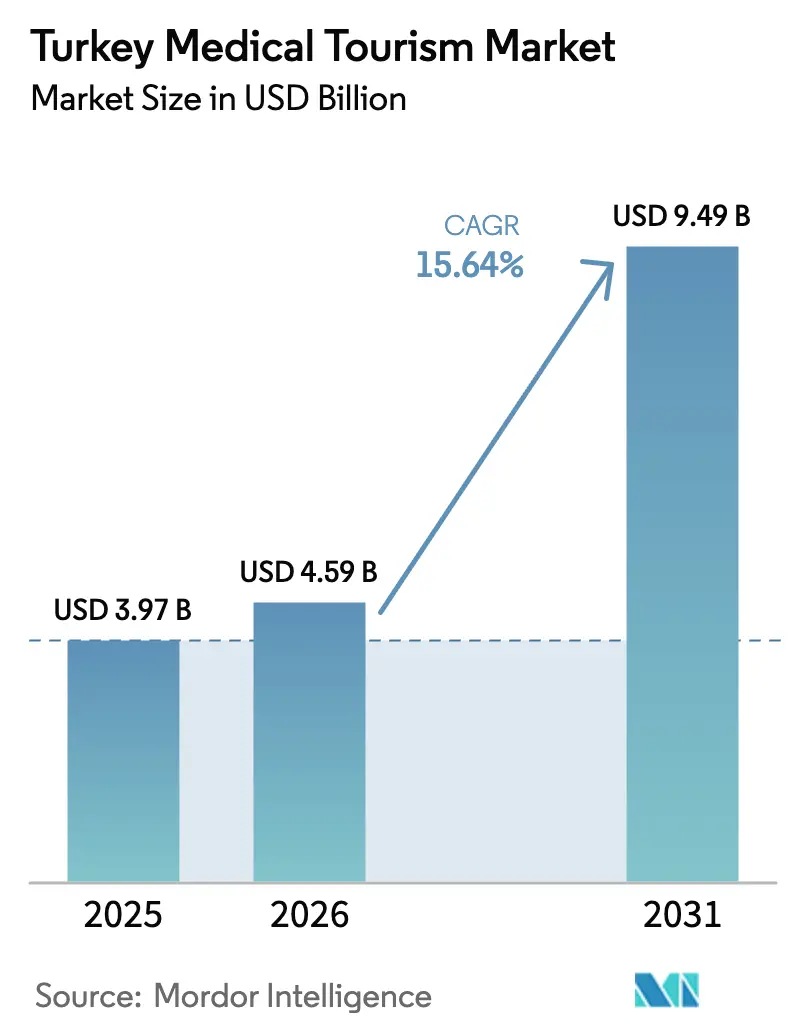

| Base Year Market Size (2025) | USD 3.97 Billion |

| Market Size (2026) | USD 4.59 Billion |

| Market Size (2031) | USD 9.49 Billion |

| Growth Rate (2026 - 2031) | 15.64% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Turkey Medical Tourism Market Analysis by Mordor Intelligence

The turkey medical tourism market size is projected to grow from USD 3.97 billion in 2025 to USD 4.59 billion in 2026, and reach USD 9.49 billion by 2031, growing at a CAGR of 15.64% from 2026 to 2031. Persistent 50-70% price gaps versus Western Europe and North America, 42 Joint Commission International-accredited hospitals, and mandatory registration of every overseas case on the HealthTürkiye portal form the core growth engine for the Turkey medical tourism market. Istanbul’s four-hour flight radius to 129 countries further enlarges the Turkey medical tourism market by reducing travel fatigue for high-acuity patients. Private chains channel foreign invoices in euros or dollars, insulating revenues from lira volatility even as domestic inflation elevates local input costs. Ongoing blockchain pilots for encrypted data exchange are poised to resolve continuity-of-care gaps, a development expected to increase referral confidence among U.K. and German insurers in the Turkish medical tourism market.

Key Report Takeaways

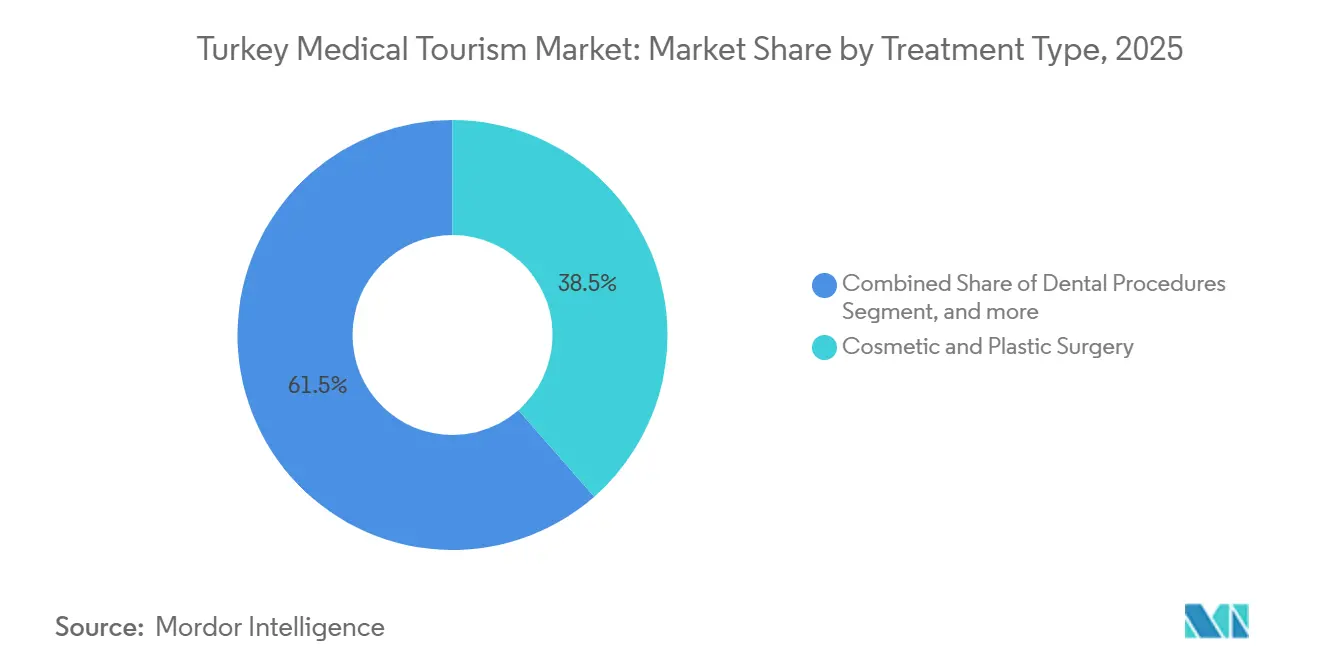

- By treatment type, cosmetic and plastic surgery held 38.54% of the Turkish medical tourism market share in 2025. Oncology procedures in the Turkish medical tourism market are forecast to surge at a 16.56% CAGR through 2031.

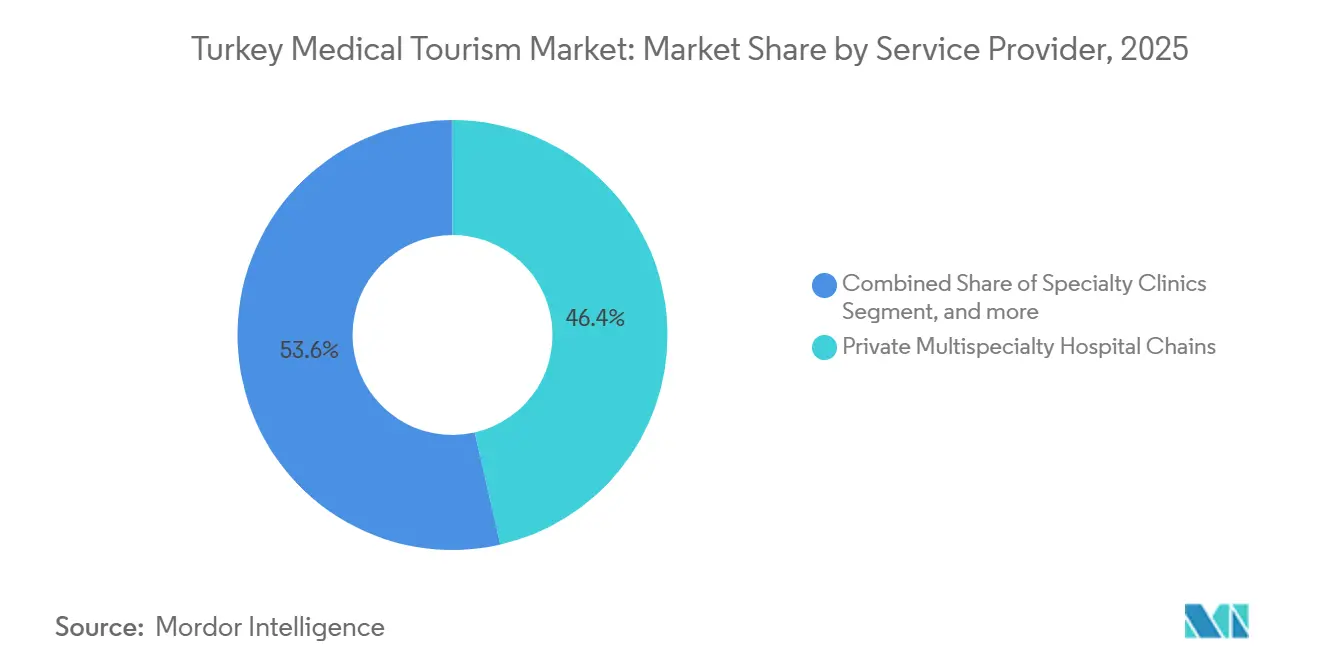

- By service provider, private multispecialty hospital chains captured 46.43% of revenue in 2025, while facilitator agencies posted a 16.32% CAGR, the fastest within the Turkey medical tourism market.

- By age group, the 18-44 cohort generated 53.23% of the 2025 arrivals, while the 65+ cohort is projected to rise at a 16.43% CAGR through 2031 within the Turkish medical tourism market.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Competitive positioning in Turkey includes both locally based firms and those operating across multiple regions. The market landscape in the global medical tourism industry research shows how these players are arranged internationally.

Turkey Medical Tourism Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Cost of Medical Care in Developed Economies | +3.2% | Global, concentrated in North America, Western Europe, UK | Long term (≥ 4 years) |

| Advanced Medical Infrastructure & Accredited Facilities | +2.8% | Global, with spillover to Middle East and Central Asia | Medium term (2-4 years) |

| Government Incentives & Visa Facilitation Programs | +2.5% | National, with early gains in Istanbul, Ankara, Antalya | Short term (≤ 2 years) |

| Strategic Geographic Location & Air Connectivity | +2.1% | Global, particularly Europe, Middle East, North Africa | Medium term (2-4 years) |

| Growth of Thermal-Wellness Integrations | +1.9% | National, Northern Europe, Scandinavia | Long term (≥ 4 years) |

| Blockchain-Enabled Cross-Border Health Data Portability | +1.4% | Global, pilot phase in EU and Middle East | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Cost of Medical Care in Developed Economies

United States health spending reached 17.3% of GDP in 2024 and a rhinoplasty priced at USD 8,000–15,000 domestically costs USD 2,500–4,000 in Turkey, widening arbitrage for self-pay patients[1]OECD, “Health Expenditure Data,” oecd.org. Coronary artery bypass grafts average USD 12,000 in Istanbul, compared to USD 70,000-120,000 in the U.S., underscoring the appeal of the Turkish medical tourism market for complex care. German and Scandinavian insurers have begun writing outbound referrals to accredited Turkish centers, embedding cross-border treatment into formal benefit designs. Hospitals quote in euros, shielding foreign bills from currency swings while sustaining attractive pricing. This structural cost gap is expected to continue funneling patients into the Turkish medical tourism market over the forecast period.

Advanced Medical Infrastructure & Accredited Facilities

Turkey hosts 42 JCI-accredited hospitals, the world’s second-largest cluster, and ten sites hold HIMSS Level 6 or higher digital maturity, demonstrating near-paperless workflows. Acibadem Healthcare Group opened a 127-bed proton and robotic surgery hospital in Kartal in February 2025, underscoring deep capital investment that elevates the Turkey medical tourism market beyond pure cost leadership. Anadolu Medical Center maintains a Johns Hopkins affiliation for oncology protocol transfer, thereby strengthening the credibility of its outcomes. Such infrastructure breadth positions the Turkish medical tourism market to win high-acuity oncology and cardiovascular cases that rival Singapore or Seoul in terms of technology, but at lower prices.

Government Incentives & Visa Facilitation Programs

A May 2025 regulation requires all medical tourists to register through the HealthTürkiye portal, which combines visa processing with quality monitoring and price transparency. Visa-free entry now covers 70+ jurisdictions, and an e-visa adds 40 more markets, eliminating a key administrative hurdle for the Turkish medical tourism market[2]Republic of Turkey Ministry of Foreign Affairs, “Visa Policy,” mfa.gov.tr. The Presidency’s USD 20 billion annual revenue goal drives tax credits for hospitals that build international patient wings and subsidizes Turkish Airlines routes to Gulf and Central Asian cities, lowering acquisition costs for providers. These levers significantly reduce the time-to-treatment for overseas patients and accelerate funnel growth into the Turkish medical tourism market.

Strategic Geographic Location & Air Connectivity

Istanbul sits within four hours of London, Frankfurt, Dubai, and Riyadh, and Turkish Airlines flies to 342 cities across 129 countries, compressing travel fatigue for oncology and cardiac patients. Istanbul Airport processes 200 million passengers annually and operates medical lanes with ambulance transfer capability that shorten curb-to-bed times. Facilitator agencies leverage hub-and-spoke models, routing diagnostics in Baku or Cairo and surgeries in Istanbul, thereby extending the Turkish medical tourism market beyond its borders. As airlines restore pre-pandemic service, Turkey’s proximity advantage over Southeast Asian rivals is expected to deepen.

Restraints Impact Analysis*

| Restraint | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Post-Procedure Follow-Up & Continuity-of-Care Challenges | -1.8% | Global, concentrated in UK, Germany, Netherlands | Short term (≤ 2 years) |

| Currency Volatility & Inflationary Pressures | -1.3% | National, with spillover to international pricing strategies | Medium term (2-4 years) |

| Perceived Geopolitical & Security Risks | -1.1% | Global, particularly North America and Western Europe | Medium term (2-4 years) |

| Limited Interoperability of International E-Health Records | -0.9% | Global, EU and North America most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Post-Procedure Follow-Up & Continuity-of-Care Challenges

An October 2024 Obesity Surgery editorial found 42% of bariatric discharge notes from Turkish providers omitted critical operative details, hindering safe aftercare. The U.K. Foreign Office counts 28 deaths among Britons since 2019 after elective procedures in Turkey, and NHS readmissions for related complications grew 94% in the same span[3]UK Foreign, Commonwealth & Development Office, “Overseas Surgery Guidance,” gov.uk. Only 30% of JCI hospitals offered structured tele-follow-up under Turkey’s 2022 telehealth rule by late 2024. Without standardized 30-day virtual reviews, reputational damage could hinder the growth of the Turkish medical tourism market, despite its price appeal.

Currency Volatility & Inflationary Pressures

Inflation peaked at 85.5% in 2022, then eased to 47.1% by November 2024. However, by January 2025, services inflation had risen to 10.3% year-over-year, leading to increased hospital wage and utility bills. Imports of stents, robotics parts, and radiopharmaceuticals are dollar-denominated, compressing margins even when foreign receipts stay in hard currency. Central bank rates at 50% through early 2025 raise debt costs, slowing new proton center builds that underpin the Turkey medical tourism market. Sustained volatility, therefore, constrains capital expansion until inflation stabilizes in single digits.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type: Oncology Gains as Cosmetic Surgery Matures

Cosmetic and plastic surgery represented 38.54% of the Turkish medical tourism market share in 2025, powered by 470,900 rhinoplasty, liposuction, and breast cases in 2023 that drew German and British travelers. Oncology volumes, supported by CAR-T, proton therapy, and robotic platforms offered at 40-70% discounts to U.S. prices, are advancing at a 16.56% CAGR and will command a larger slice of the Turkish medical tourism market by 2031.

Hair transplantation attracts roughly half of all arrivals, but unlicensed Istanbul clinics undermine margins and trust. Orthopedic and cardiovascular lines appeal to retirees who bundle hip or bypass surgery with thermal-wellness stays in Afyonkarahisar and Bursa. Investment in HIMSS Level 6-7 platforms reduces complications and supports Turkey's medical tourism market positioning on safety as well as savings.

By Service Provider: Facilitator Agencies Scale Digital Platforms

Private multispecialty chains controlled 46.43% of international revenue in 2025, leveraging scale in procurement and marketing to equip proton bays and hybrid ORs. Facilitator agencies posted a 16.32% CAGR and aggregate online demand while handling visas and transfers through 168 overseas offices, forming a vital intake pipeline for the Turkey medical tourism market.

Specialty clinics in the hair and dental fields confront commoditization as price-cutting proliferates among 5,000 Istanbul sites, many lacking licenses. HealthTürkiye’s mandatory registration and data transparency push unlicensed operators toward compliance or exit, potentially concentrating Turkey's medical tourism market revenues in accredited hands. Agencies exploring blockchain health wallets could unlock new insurer partnerships by guaranteeing interoperable discharge data.

By Age Group: Younger Cohorts Drive Volume, Seniors Accelerate Growth

The 18-44 cohort accounted for 53.23% of patients in 2025, securing discounts of 50-70% on aesthetics and dentistry. The 45-64 segment tracks overall growth as they mix elective and medically necessary treatments. The 65+ cohort is the fastest-growing, expanding at a 16.43% CAGR through 2031, driven by orthopedic, cardiac, and oncology bundles, bolstered by insurer reimbursements from Scandinavia.

Tele-clinical oversight still reaches only 30% of JCI sites, which tempers uptake among seniors who require structured follow-up. The successful rollout of blockchain-backed health-record portability and mandatory tele-consultation windows would improve trust and push higher-ticket geriatric cases deeper into the Turkish medical tourism market.

Competitive Landscape

The Turkish medical tourism market is fragmented, with 42 JCI-accredited hospitals competing against thousands of clinics, many of which are unlicensed, particularly in hair transplantation. Chains such as Acibadem, Memorial, and Medicana invest in proton, robotic, and digital ecosystems, pitching safety and outcomes over price. Acibadem’s 2025 Kartal launch expanded network capacity to 25 hospitals, reinforcing its dominance in oncology.

Facilitator portals, such as FlyMedi and Medproper International, capture customer acquisition economics that once resided within hospital marketing teams, prompting hospitals to shift toward performance-based alliances. Blockchain pilots for cross-border data portability, documented in a September 2025 peer-reviewed study, position early adopters to win insurer contracts by guaranteeing seamless follow-up. Regulatory scrutiny via HealthTürkiye raises compliance expenses for small clinics and may accelerate consolidation, nudging the Turkey medical tourism market toward a more structured quality hierarchy.

Turkey Medical Tourism Industry Leaders

Remed Health

Euro Health Medical Tourism

ROMOY Health Tourism and Consulting

Doc's Health Tourism Agency

AkayLife

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Acibadem Healthcare Group opened its 127-bed Kartal Hospital with proton therapy and robotic suites

- July 2024: Vera Clinic unveiled its New Generation Hair Implementation, revolutionizing hair transplantation with cutting-edge techniques and treatments. By integrating Stem Cell Therapy with Sapphire FUE and OxyCure Therapy, Vera Clinic is setting a benchmark in hair transplantation. This advanced methodology ensures heightened precision and agility, leading to an impressive 99% follicular survival rate. Consequently, patients benefit from hair that is not only denser but also thicker.

- April 2024: Haus of Nomads Travel, a boutique travel agency, launched medical tourism services that combine healthcare excellence and luxurious travel experiences in Antalya, Turkey. In partnership with top-tier clinics and board-certified doctors, Haus of Nomads Travel will offer high-quality medical procedures such as aesthetic dental treatments, hair transplants, and cosmetic surgeries.

Turkey Medical Tourism Market Report Scope

As per the scope of the report, medical tourism (also called medical travel, health tourism, or global healthcare) is a term used to describe the rapidly growing practice of traveling across international borders to seek healthcare services.

The Turkey Medical Tourism Market Report is Segmented by Treatment Type (Cosmetic & Plastic Surgery, Dental Procedures, Oncology Treatments, Hair Transplantation, Orthopedic Procedures, Cardiovascular Procedures, and Other Treatment), Service Provider (Private Multispecialty Hospital Chains, Specialty Clinics, Public / University Hospitals, and Medical Tourism Facilitator Agencies), Age Group (18-44 Years, 45-64 Years, and 65+ Years), and Geography (Turkey). The report offers the value (in USD million) for the above segments.

| Cosmetic & Plastic Surgery |

| Dental Procedures |

| Oncology Treatments |

| Hair Transplantation |

| Orthopedic Procedures |

| Cardiovascular Procedures |

| Other Treatment |

| Private Multispecialty Hospital Chains |

| Specialty Clinics |

| Public / University Hospitals |

| Medical Tourism Facilitator Agencies |

| 18-44 Years |

| 45-64 Years |

| 65+ Years |

| By Treatment Type | Cosmetic & Plastic Surgery |

| Dental Procedures | |

| Oncology Treatments | |

| Hair Transplantation | |

| Orthopedic Procedures | |

| Cardiovascular Procedures | |

| Other Treatment | |

| By Service Provider | Private Multispecialty Hospital Chains |

| Specialty Clinics | |

| Public / University Hospitals | |

| Medical Tourism Facilitator Agencies | |

| By Age Group | 18-44 Years |

| 45-64 Years | |

| 65+ Years |

Key Questions Answered in the Report

How large is Turkey medical tourism market in 2026?

The Turkish medical tourism market size is projected to reach USD 4.59 billion in 2026 and is expected to climb to USD 9.49 billion by 2031.

Which specialty is growing fastest?

Oncology procedures are expanding at a 16.56% CAGR to 2031 due to proton therapy, CAR-T, and robotic surgery capacity.

What portion do private chains hold?

Private multispecialty chains captured 46.43% of 2025 revenue from international patients.

Why do European patients prefer Turkey?

They gain 50-70% cost savings, four-hour flight times, and care in 42 JCI-accredited hospitals, boosting confidence.

What platform is mandatory for overseas patients?

The HealthTürkiye portal has processed every foreign patient since May 2025, covering visa, data, and quality checks.

Which age group is rising quickest?

Patients aged 65+ are growing at a 16.43% CAGR through 2031 as they seek bundled cardiac, orthopedic, and oncology packages.

Page last updated on: