Dental Tourism Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

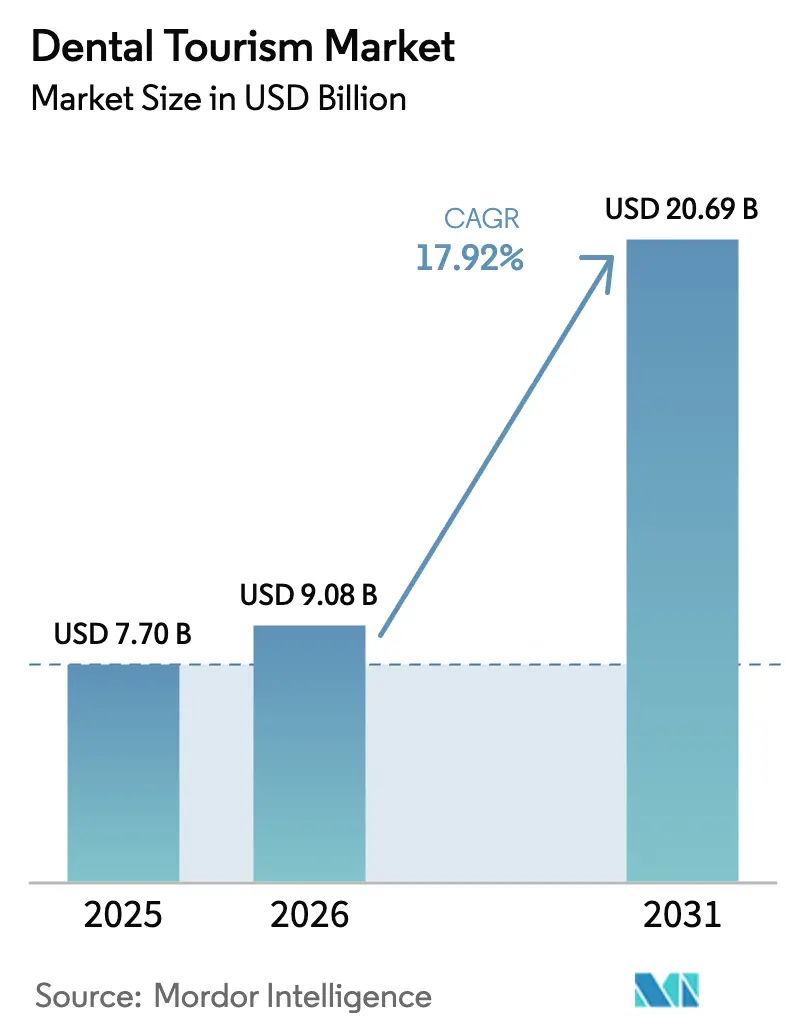

| Market Size (2026) | USD 9.08 Billion |

| Market Size (2031) | USD 20.69 Billion |

| Growth Rate (2026 - 2031) | 17.92% CAGR |

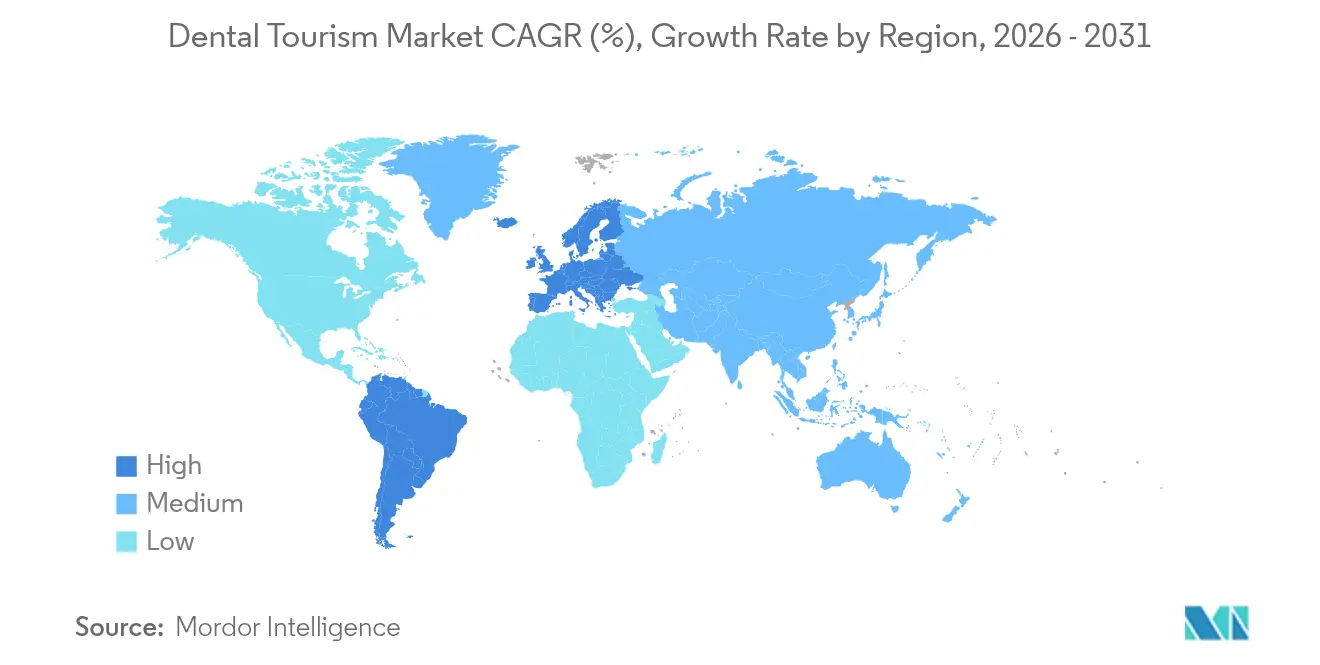

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

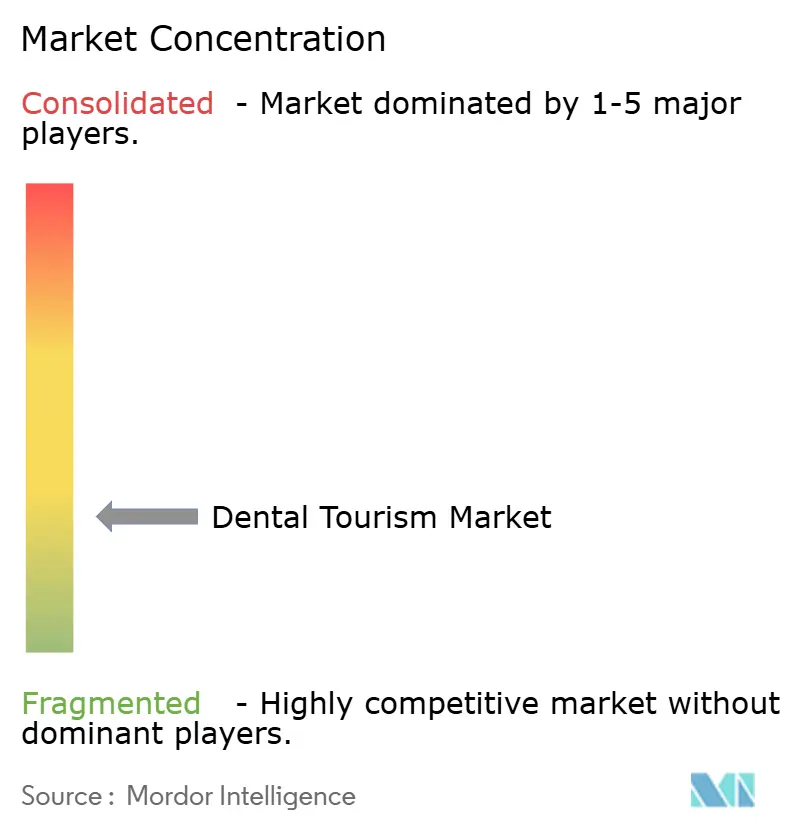

| Market Concentration | Low |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Dental Tourism Market Analysis by Mordor Intelligence

The Dental Tourism Market size was valued at USD 7.70 billion in 2025 and estimated to grow from USD 9.08 billion in 2026 to reach USD 20.69 billion by 2031, at a CAGR of 17.92% during the forecast period (2026-2031). The rebound stems from pent-up demand that accumulated during pandemic-era travel restrictions, persistent price gaps between developed and emerging economies, and a wave of internationally accredited clinics that now market directly to foreign patients through digital channels. Sustained wage inflation in North America and the EU is widening cost differentials, while governments in Asia-Pacific, Eastern Europe, and Latin America have embedded medical travel into national economic policy. Technology adoption—ranging from AI-assisted diagnostics to chairside CAD/CAM milling—shortens treatment windows, making complex work possible within a single overseas trip. Finally, low-cost airlines and destination marketing organizations are bundling care with leisure experiences, turning treatment journeys into integrated vacations.

Key Report Takeaways

- By treatment type, restorative procedures led with 43.62% of dental tourism market share in 2025; oral and maxillofacial surgery is set to post the fastest 19.34% CAGR through 2031.

- By provider, dental clinics controlled 28.10% of 2025 revenue, whereas hospitals are projected to grow at an 18.42% CAGR to 2031.

- By geography, Asia-Pacific captured 35.05% revenue in 2025, while Europe is on track for the highest 18.55% CAGR over the forecast.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Dental Tourism Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Burden of Dental Diseases | +3.2% | Global, with acute impact in aging populations of North America & Europe | Long term (≥ 4 years) |

| High Treatment Cost in Developed Countries | +4.1% | North America & EU core, spillover to Australia & Japan | Medium term (2-4 years) |

| Availability of Latest Dental Technologies and High-Quality Care in Emerging Destinations | +2.8% | APAC core (Thailand, Malaysia, India), Eastern Europe (Hungary, Poland) | Medium term (2-4 years) |

| Uptick in Digital Marketing and Online Patient Reviews | +1.9% | Global, with early gains in social media-savvy demographics | Short term (≤ 2 years) |

| Airline–Clinic Package Partnerships | +1.4% | Regional corridors: US-Mexico, UK-Turkey, Australia-Thailand | Medium term (2-4 years) |

| International Dental-Facility Accreditation Expansion | +2.1% | Emerging destinations seeking credibility: Turkey, India, Philippines | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Burden of Dental Diseases

Oral conditions affect 3.5 billion people worldwide, and prevalence climbs with age, especially in high-income economies where retirees possess both disposable income and heightened expectations for rapid, high-quality interventions. Lengthy domestic waitlists for implant-supported prosthetics or full-mouth rehabilitation push patients toward destinations that guarantee immediate chair time. Thai hospital networks and Hungarian specialty centers now advertise AI-enhanced imaging platforms that reduce diagnostic uncertainty and enable same-trip surgical execution. Diagnocat’s cloud-based cone-beam analytics exemplify such tools, delivering high-precision treatment plans that underpin patient confidence. As global life expectancy rises, this demographic driver will keep the dental tourism market on an upward trajectory for at least the next decade.

High Treatment Cost in Developed Countries

A single implant with crown averages EUR 2,500–3,500 in the UK but only EUR 950–1,400 in Budapest, while an All-on-4 case priced at USD 25,000 in the US falls to USD 10,000 in Cancún. April 2025 import tariffs on dental consumables added roughly 10% to US chairside costs, widening the cross-border savings gap.[1]Source: Zenone, “Impact of Tariffs on U.S. Dental Practices,” zenone.com Insurance caps compound the problem, classifying many restorative or cosmetic procedures as elective and shifting the full bill to patients. Currency-denominated incentives amplify the disparity: Ecuador’s use of the US dollar removes FX risk for North American visitors, whereas euro-zone patients benefit when forint or lira weakness magnifies their purchasing power. The financial logic continues to be the most powerful accelerant for the dental tourism market.

Availability of Latest Technologies and High-Quality Care in Emerging Destinations

Turkey’s private clinics routinely deploy chairside CAD/CAM, 3-D printing of surgical guides, and AI-driven case-planning software. Regional equipment alliances, such as Dentsply Sirona’s multiyear investment in Egypt’s Alexandria University, ensure a pipeline of clinicians trained on the same technologies found in Western teaching hospitals. Accreditation momentum is also evident: Yeditepe University obtained CODA recognition in 2024, granting its graduates licensure parity with US dentists. These technology and quality signals mitigate perceived risk, allowing emerging markets to command a premium procedure mix within the dental tourism market.

Uptick in Digital Marketing and Online Patient Reviews

Instagram, TikTok, and Google My Business have dismantled information asymmetry. An academic review of Colombian clinics linked dedicated social-media campaigns to higher chair utilization and superior financial returns. Viral hashtags such as #TurkeyTeeth made aesthetic makeovers socially aspirational, triggering a 60% jump in UK outbound flows between 2019 and 2024. Enhanced transparency means providers must deliver consistently or risk reputation damage; yet it also democratizes access, allowing small practices in Poland or the Philippines to reach global audiences at low cost. Overall, digital engagement expands addressable demand and accelerates conversion rates.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Challenges With Patient Follow-Up and Post-Procedure Complications | -2.8% | Global, acute in long-haul corridors (US-Asia, EU-Latin America) | Medium term (2-4 years) |

| Cross-Border Medical-Record Transfer Issues | -1.6% | Global, with regulatory complexity in EU-UK post-Brexit | Short term (≤ 2 years) |

| Currency Volatility Affecting Package Affordability | -1.9% | Emerging destinations with volatile currencies: Turkey, Argentina, Eastern Europe | Short term (≤ 2 years) |

| Carbon-Footprint Concerns Among Eco-Conscious Patients | -0.8% | Developed countries with high environmental awareness: Northern Europe, Pacific Coast US | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Challenges With Patient Follow-Up and Post-Procedure Complications

A British Medical Association briefing notes that 86% of overseas dental travelers who later sought corrective treatment at home required additional NHS care.[2]Source: DWF Group, “Dental Tourism: Holiday Horror Stories,” dwfgroup.com Implant osseointegration, orthodontic adjustments, and full-arch restorations demand multiple reviews over months; distance, liability ambiguities, and travel costs deter return visits. Some domestic dentists decline to treat foreign-placed work, citing incomplete records and medico-legal risk. These realities moderate the upper boundary of the dental tourism market, particularly for medically complex or risk-averse patients.

Cross-Border Medical-Record Transfer Issues

Interoperability gaps between national electronic health record platforms force clinicians to rely on emailed PDFs or patient-supplied images, raising data-loss and privacy liabilities. A 2024 scoping study catalogued mounting legal questions around consent, confidentiality, and professional accountability in cross-border teledentistry. Compliance with GDPR, HIPAA, and emerging data-sovereignty laws increases administrative overhead for small clinics. Without streamlined record-exchange standards, postoperative quality assurance and continuity of care remain fragile, dampening growth momentum.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Treatment Type : Complex Procedures Drive Premium Growth

Restorative care dominated 2025 revenue, capturing 43.62% of dental tourism market share on the strength of high-volume crown, bridge, and single-implant cases. At the same time, oral and maxillofacial surgery is forecast to grow at a 19.34% CAGR and account for the largest incremental dental tourism market size through 2031. Demand comes from edentulous or trauma patients who can justify airfare by pairing multiple extractions, sinus lifts, and zygomatic implants in one visit.

Emerging centers advertise same-day implants and digitally guided jaw reconstruction that cut chair time by 70%, while hospital-based teams provide maxillofacial anesthesiology and ICU backup when indicated. Cosmetic orthodontics and veneer bundles continue to lure millennials, but higher-ticket surgical bundles are what propel overall value expansion within the dental tourism market.

By Providers : Hospital Integration Accelerates Growth

Private dental clinics controlled 28.10% of global revenue in 2025, owing to nimble operations and aggressive international marketing. Hospitals, however, are on track for an 18.42% CAGR between 2026 and 2031, lifting their share of the dental tourism market size as they add fully digitized prosthodontic suites inside tertiary campuses. Integrated settings appeal to older travelers who may need cardiology clearance or emergency backup.

Flagship examples include Bangkok’s Bumrungrad International and Kuala Lumpur’s Prince Court, where bundled implant programs pair dental surgery with medical check-ups and hotel transfers. US-based Nuvia Dental Implant Center popularized “teeth-in-24-hours,” demonstrating how process innovation can vault a provider from niche status to mainstream destination. This hospital-clinic hybrid model signals a structural pivot in the dental tourism market toward comprehensive, one-stop facilities.

Geography Analysis

Asia-Pacific held 35.05% of 2025 revenue, powered by Thailand’s 2 million inbound dental patients and Malaysia’s state-backed expansion under its 2022–2030 plan. Superior air connectivity, English-fluent staff, and JCI-accredited clinics allow patients to combine care with resort stays. India and Vietnam leverage vast graduate pipelines to deliver sub-USD 600 implants, while the Philippines has introduced formal accreditation to raise international confidence.

Europe is projected to notch the fastest regional 18.55% CAGR through 2031. Hungary retains leadership in minor restorative work, delivering 40–60% price savings versus the UK. Turkey’s currency dynamics and new Riyadh branch expansions have elevated it to a hub for complex full-arch cases, adding GBP 600 million to its 2024 receipts. Croatia’s Adria Dental Group is consolidating fragmented practices into a pan-EU network, mirroring aviation-style alliances to maximize chair utilization.

In the Americas, Mexico’s border towns treat an estimated 1.2 million US residents annually, offering walk-in clinics steps from Arizona and Texas crossings. Ecuador markets dollar-denominated pricing to erase FX risk, and Costa Rica packages implants with eco-tourism excursions placidway.com.

The Middle East and Africa remain nascent, yet Egyptian and Jordanian providers that integrate Western equipment partnerships have begun to attract Gulf patients seeking shorter flights and culturally aligned care.

Competitive Landscape

The dental tourism market features moderate fragmentation: regional champions coexist with thousands of single-site clinics. Thai hospital groups, Hungarian cluster operators, and Mexican border chains collectively held a substantial percentage of 2024 revenue, indicating no single actor exerts outsized dominance. Competitive strategy falls into three archetypes. Cost leaders exploit labor and currency advantages, exemplified by Indian multispecialty chains quoting USD 450 anterior crowns at scale.

Differentiators invest in technology such as intraoral scanners, 3-D printed zirconia, and AI predictive analytics to justify premium package pricing, as seen in Turkey and Egypt. Integrators wrap dental care, hotel, and tourism into one invoice, a model pioneered by Costa Rica and now copied by airlines partnering with Malaysian hospitals.

Private-equity inflows are rising. Progressive Dental Marketing secured a USD 100 million recapitalization in 2025 to build brand-agnostic patient-acquisition platforms. Meanwhile, equipment vendors like Dentsply Sirona co-locate training academies inside overseas universities, ensuring a captive downstream market for consumables. The next battleground is digital follow-up: teledentistry platforms that feed postoperative data back to source clinicians aim to neutralize continuity-of-care objections. Players that master this link are positioned to capture a disproportionate share of future dental tourism market growth.

Dental Tourism Industry Leaders

Apollo Hospitals Enterprise Ltd.

Medlife Group

Prince Court Medical Centre

Fortis Healthcare Ltd

Bangkok International Dental Center (BIDC)

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2024: The Department of Tourism (DOT) in the Philippines planned to gain global attention in medical tourism by releasing its updated rules and regulations to strengthen the accreditation of dental clinics.

- February 2024: Dentakay, a Turkish provider of dental health tourism, opened its first clinic in Riyadh and expanded its presence in Saudi Arabia and the GCC region.

Global Dental Tourism Market Report Scope

As per the scope of the report, dental tourism refers to individuals traveling abroad to receive medical treatments related to oral health, such as routine checkups, dental implants, braces, and teeth whitening.

The dental tourism market is segmented into treatment type, providers, and geography. By treatment type, the market is segmented into preventive treatment, restorative treatment, oral and maxillofacial surgery (OMS), and others. The other types include orthodontics and dental bonding. By providers, the market is segmented into hospitals, multi-specialty clinics, and others. The other providers include dental clinics and dental laboratories. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. Market sizing and forecasts were made for each segment based on value (USD).

| Preventive Treatment |

| Restorative Treatment |

| Oral and Maxillofacial Surgery (OMS) |

| Others |

| Hospitals |

| Dental Clinics |

| Others |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Treatment Type | Preventive Treatment | |

| Restorative Treatment | ||

| Oral and Maxillofacial Surgery (OMS) | ||

| Others | ||

| By Providers | Hospitals | |

| Dental Clinics | ||

| Others | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

How large is the dental tourism market in 2026?

The sector is valued at USD 9.08 billion in 2026 and is projected to reach USD 20.69 billion by 2031 on a 17.92% CAGR.

Which region leads the dental tourism market?

Asia-Pacific holds the top position with 35.05% of 2025 revenue, supported by Thailand’s 2 million international dental patients and Malaysia’s state program.

What treatment category is expanding fastest?

Oral and maxillofacial surgery is forecast to grow at 19.34% CAGR as patients travel for advanced implant and reconstructive services that justify airfare.

Why are hospitals gaining traction over standalone clinics?

Hospitals combine dental departments with broader medical facilities, offering integrated care and emergency backup, which resonates with older or medically complex travelers, driving an 18.42% CAGR in this segment.

What is the biggest restraint on dental tourism growth?

Difficulty in coordinating post-procedure follow-up across borders remains the primary barrier, subtracting an estimated 2.8 percentage points from the market’s long-term CAGR forecast.

How does accreditation influence patient choice?

International certifications such as JCI or CODA signal quality and safety, reducing perceived risk and making accredited clinics the first choice for many overseas patients.

Page last updated on: