Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

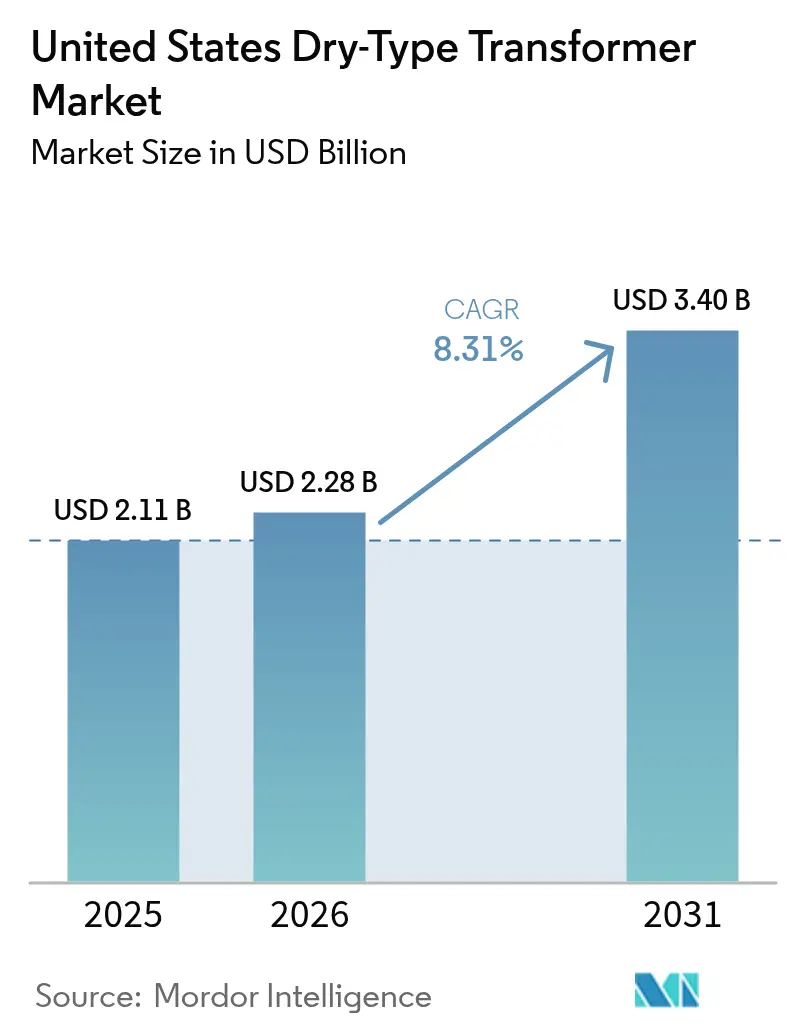

| Base Year Market Size (2025) | USD 2.11 Billion |

| Market Size (2026) | USD 2.28 Billion |

| Market Size (2031) | USD 3.4 Billion |

| Growth Rate (2026 - 2031) | 8.31% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Dry-Type Transformer Market Analysis by Mordor Intelligence

The United States Dry-Type Transformer Market size was valued at USD 2.11 billion in 2025 and estimated to grow from USD 2.28 billion in 2026 to reach USD 3.4 billion by 2031, at a CAGR of 8.31% during the forecast period (2026-2031).

Efficiency regulations, the electrification of buildings and transport, and grid modernization funding are the principal forces shaping demand. The Department of Energy’s Phase-2 standards, now effective in 2029, compress retrofit timelines and accelerate replacement cycles.[1]U.S. Department of Energy, “Distribution Transformer Efficiency Standards,” energy.gov Surge in behind-the-meter battery storage is reshaping specification requirements toward bidirectional, thermally robust designs. Data center incentives under federal infrastructure policy amplify large-order volumes in the Virginia, Texas, and North Carolina corridors. Simultaneously, the reshoring of medium-voltage equipment manufacturing is swelling domestic capacity, although interim supply constraints persist while new plants ramp up production. Material-price volatility and certification bottlenecks temper margins but are outweighed by regulatory and electrification tailwinds that sustain growth opportunities across utility and residential segments.

Key Report Takeaways

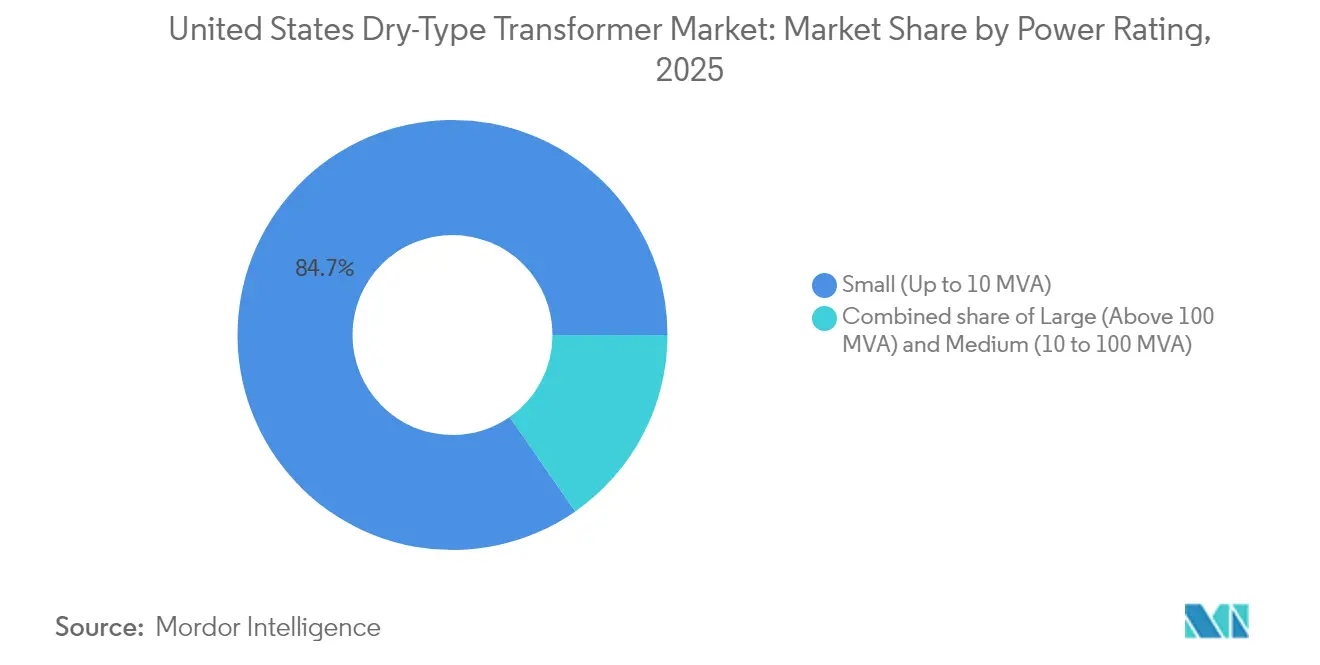

- By power rating, small transformers, up to 10 MVA, captured 84.68% of the US dry-type transformer market share in 2025 and are expected to expand at an 8.46% CAGR through 2031.

- By phase, single-phase units are projected to grow at a 8.92% CAGR, outpacing the three-phase segment’s 7.65% growth to 2031

- By transformer type, distribution transformers accounted for 79.25% of the US dry-type transformer market size in 2025 and are expected to maintain their leadership with an 8.52% CAGR over the forecast period.

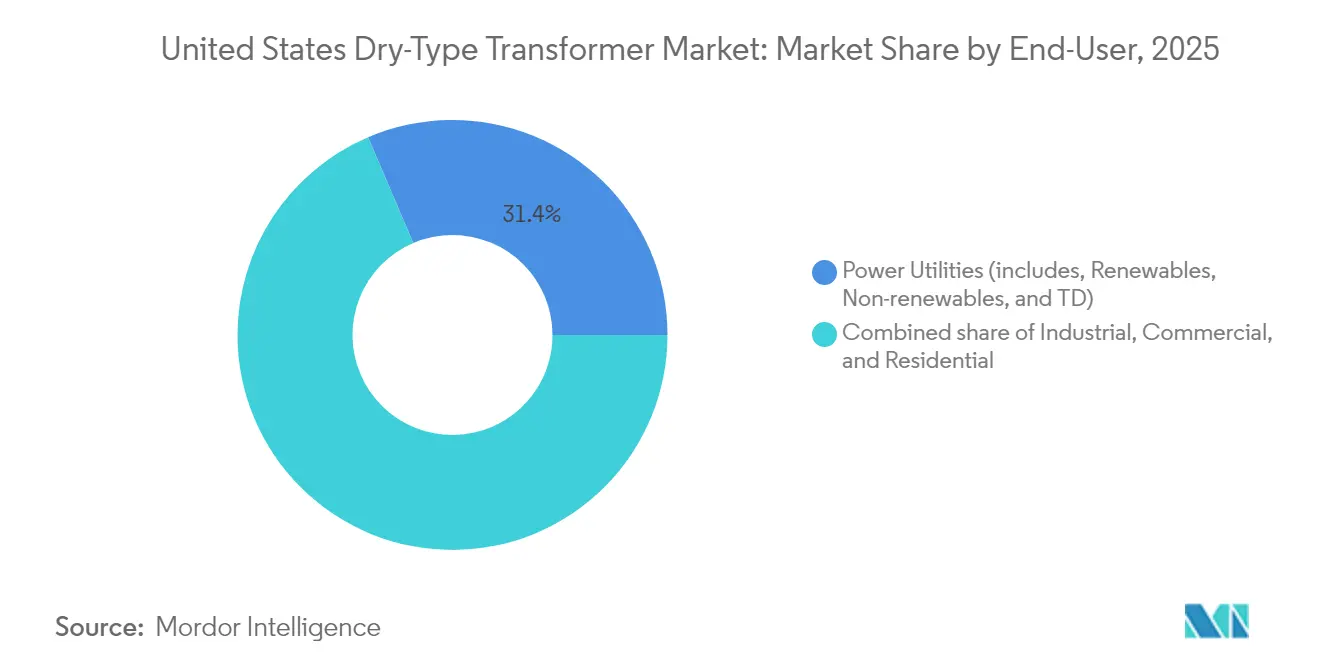

- By end-user, the residential segment is expected to lead growth at a 9.18% CAGR, while power utilities remain the largest buyers, accounting for a 31.42% value share in 2025.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Dry-Type Transformer Market Trends and Insights

Driver Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| DOE efficiency rule Phase-2 enforcement | +2.1% | Nationwide, strongest in industrial states | Medium term (2-4 years) |

| Behind-the-meter battery storage surge | +1.8% | California, Texas, Northeast | Short term (≤ 2 years) |

| Data-center tax incentives | +1.4% | Virginia, Texas, North Carolina | Medium term (2-4 years) |

| Reshoring of medium-voltage supply chains | +0.9% | Midwest manufacturing belt, Southeast industrial zones | Long term (≥ 4 years) |

| Fire-safe transformer mandates in high-rise | +0.7% | Dense urban construction markets | Medium term (2-4 years) |

| Electrification of heat processes challenges | +0.3% | Industrial clusters in chemical, steel, cement sectors | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

DOE Efficiency Rule Phase-2 Drives Retrofit Acceleration

The Department of Energy has set 2029 as the compliance deadline for the second phase of transformer efficiency rules, replacing the earlier 2027 date. The rule demands efficiency gains that are unattainable through minor design tweaks, forcing the outright replacement of many aging dry-type units. A four-year compliance window prompts utilities, campuses, and industrial plants to expedite their procurement strategies. Ancillary upgrades—such as larger termination compartments and improved ventilation—add to project scope and spending. Facilities operating multiple units must synchronize replacements to avoid downtime, elevating batch-order volumes. These dynamics elevate baseline demand across all ratings, creating premium pricing opportunities for suppliers capable of delivering high-efficiency models within compressed lead times.

Behind-the-Meter Storage Transforms Distribution Requirements

California surpassed 2,000 MW of behind-the-meter storage capacity in 2024, with Texas and Northeast states following suit.[2]California Energy Commission, “2024 Total System Electric Generation,” energy.ca.gov Bidirectional power flow and rapid cycling stress conventional transformer designs drive the adoption of vacuum-pressure-impregnated (VPI) coils, which offer enhanced thermal margins. Storage-coupled transformers are specified at capacity ratings 15-20% above nominal load to ride through frequent charge-discharge events. Grid-code revisions that privilege dry-type designs over oil-filled units, primarily for fire safety, further amplify uptake. Manufacturers offering pre-certified bidirectional units gain first-mover advantage, while utilities refine protection schemes to manage harmonics introduced by inverter-based storage.

Data Center Tax Incentives Fuel Infrastructure Investment

The federal infrastructure law enables accelerated depreciation for power hardware deployed at data center sites.[3]Dominion Energy, “Renewable Generation Projects,” dominionenergy.com Northern Virginia’s corridor handles approximately 70% of global internet traffic, resulting in continuous expansion that necessitates redundant transformer banks for N-1 reliability. High-density computing loads require compact, low-loss dry-type units designed for operation in elevated ambient temperatures. The proliferation of edge computing extends these requirements to secondary markets in Texas and North Carolina. Transformer vendors positioned with modular, pluggable designs secure multi-site framework agreements and benefit from predictable roll-out schedules tied to tax-credit milestones.

Supply Chain Reshoring Creates Capacity Constraints

Congress allocated USD 1.2 billion to stimulate domestic manufacturing of medium-voltage equipment in 2024.[4]United States Congress, “H.R.4366 – Domestic Transformer Supply Chain Appropriations,” congress.gov New plants in Georgia, South Carolina, and Tennessee are expected to increase volume beginning in 2026; however, interim supply remains tight, with standard lead times of 60-70 weeks and specialized VPI coils stretching to 18-24 months. Large OEMs, including Hitachi Energy, ABB, and Schneider Electric, are committing capital expenditures exceeding USD 3 billion combined to expand their U.S. capacity. The gap between demand and output forces buyers to place orders earlier, lock in slots, and consider dual-sourcing strategies, sustaining elevated backlog well into 2027.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Copper and aluminum price volatility | -1.2% | Nationwide, pronounced in manufacturing hubs | Short term (≤ 2 years) |

| Lengthy UL-1561 certification lead times | -0.8% | Nationwide | Medium term (2-4 years) |

| Real-estate constraints in legacy substations | -0.6% | Dense urban centers | Long term (≥ 4 years) |

| OEM capacity limits for VPI coils | -0.5% | Nationwide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Material Price Volatility Pressures Margins

Aluminum averaged USD 2,100 per metric ton on the London Metal Exchange in 2024, 15% above the 2023 level, and trading bands indicate continued fluctuations through 2025. Raw materials account for up to 60% of the transformer manufacturing cost, yet supply contracts often fix selling prices months in advance. Price spikes compress margins for OEMs locked into legacy bids, while buyers face surcharges or re-quotations. Copper volatility compounds risk, prompting a shift toward aluminum windings where thermal specs allow. Some utilities adopt cost-adjustment clauses to share risk, but smaller contractors remain exposed, which can stall project awards during high-price intervals.

UL-1561 Certification Creates Deployment Bottlenecks

Underwriters Laboratories now requires 8-12 months to certify new dry-type designs and 4-6 months for derivative models due to testing backlogs.[5]Underwriters Laboratories, “Testing & Certification Services,” ul.com DOE efficiency updates trigger design revisions, which in turn flood the certification queue. Small and mid-size manufacturers, unable to parallel-process multiple product lines, experience shipment delays that erode market share. Data-center and industrial customers seeking custom k-factor units face the longest waits, occasionally resorting to interim rentals. UL is expanding lab capacity, but meaningful cycle-time reductions are unlikely before 2026.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Power Rating: Small Units Anchor Distributed Growth

Small transformers, up to 10 MVA, accounted for 84.68% of 2025 shipments, translating to USD 1.79 billion of the US dry-type transformer market size. Their dominance stems from a distributed architecture that favors numerous localized installations over a few centralized assets. The segment is projected to grow at an 8.46% CAGR, benefiting from residential electrification and retrofit programs. Behind-the-meter storage and industrial heat-pump projects drive specification changes, requiring higher overload capacity and improved cooling. Standardized frame sizes enable economies of scale, but the increasing customization of storage and VFD-driven loads introduces engineering complexity. OEMs able to balance modularity with customization capture premium margins while meeting volume commitments.

Medium transformers (10-100 MVA) service utility substations and critical industrial feeders. Although representing approximately 12.15% of the US dry-type transformer market share in value, growth moderates to 7.05% as utilities focus capital expenditures on distribution-level modernization rather than capacity expansion. Large transformers above 100 MVA remain niche, aligning with transmission-level or hyperscale data center interconnects. Suppliers in this tier emphasize advanced insulation systems and partial-discharge monitoring to meet reliability targets.

By Phase: Single-Phase Upswing Compliments Three-Phase Base

Three-phase models retained a 66.82% share in 2025, underpinned by industrial motor loads and large commercial buildings. However, single-phase units are expected to clock a 8.92% CAGR to 2031, reflecting the boom in EV charging and heat pumps in residential neighborhoods. Utilities in California and New York are forecasting double-digit annual replacements of pole-top single-phase transformers to accommodate higher 240V loads. Level-2 EV chargers and induction cooktops drive peak currents that exceed the ratings of legacy transformers, necessitating proactive replacements. Residential rooftops with solar plus storage further compel bidirectional capability, a specification more commonly available in new single-phase offerings.

Three-phase demand continues in process industries, shifting toward high-efficiency configurations that align with DOE Phase 2 requirements. Vendors differentiate through core material innovations and embedded sensors that enable real-time thermal modeling. Growth softens as energy-intensive industries plateau, yet service-replacement cycles support a steady baseline of orders.

By Transformer Type: Distribution Units Dominate Modernization

Distribution transformers accounted for 79.25% of the US dry-type transformer market size in 2025, totaling USD 1.67 billion. Grid-modernization grants and resilience funding prioritize last-mile assets that improve reliability for residential and commercial users. Smart sensors integrated into distribution units feed utility SCADA platforms, enabling predictive maintenance and enhancing operational efficiency. The DOE Grid Modernization Initiative earmarks USD 3.5 billion for distribution-level upgrades, further sustaining demand.

Power transformers, although smaller in total value, capture specialized opportunities in edge data centers and renewable energy interconnects, where step-up or step-down functions bridge distribution and transmission voltages. Suppliers focusing on modular, skid-mounted designs are gaining traction due to reduced on-site assembly time. Advanced dry-type insulation materials widen the voltage window, positioning dry-type alternatives in applications historically served by oil-filled equipment.

By End-User: Residential Electrification Leads Growth

Power utilities remained the largest purchasers, accounting for 31.42% of 2025 revenue. However, the residential segment is expected to post the highest 9.18% CAGR through 2031, adding more than USD 350 million to the US dry-type transformer market size. Federal tax credits under the Inflation Reduction Act cover up to USD 14,000 per household for heat-pump installs, accelerating service upgrades at the transformer level. EV adoption compounds load growth; the average two-EV household can add 10-15 kVA of evening peak demand. Utilities pre-empt overloads with proactive pole-top replacements, often bundled with advanced metering infrastructure.

Industrial users, representing around 28.15% of the value share, are pivoting to electrified process heat and high-efficiency drives. Transformers designed for variable-frequency operation gain favor, especially in chemical and cement clusters that aim for Scope 1 emission reductions. Commercial buildings often adopt dry-type units during HVAC electrification retrofits, in response to building code bans on fossil-fuel appliances in New York City and San Francisco.

Geography Analysis

National policy harmonizes core specifications, but regional factors create nuanced demand pockets within the US dry-type transformer market. California, New York, and Massachusetts lead the adoption of decarbonization measures, accounting for a combined 27.65% of shipments in 2025. Utilities in these states deploy advanced monitoring features to manage rooftop solar backfeed and wildfire mitigation protocols.

The Southeast emerges as a manufacturing hub, buoyed by Hitachi Energy’s USD 1.75 billion Tennessee expansion and HD Hyundai Electric’s new facility in Georgia. Proximity lowers freight costs and shortens lead times for local utilities. Texas represents a unique dynamic under ERCOT’s isolated grid; the rapid build-out of renewable energy requires transformers with wide voltage-ride-through tolerances. Hurricanes in Gulf Coast states push demand for corrosion-resistant enclosures and elevated pad-mount designs.

Midwestern manufacturing belts focus on industrial electrification. States like Ohio and Indiana leverage reshoring incentives, requesting application-specific units for steel and chemical plants. Snow-belt regions prioritize cast-coil insulation capable of withstanding freeze-thaw cycles. The relatively uniform influence of federal standards ensures that even with regional customizations, suppliers can maintain platform commonality, balancing customization with scale.

Competitive Landscape

The US dry-type transformer market is dominated by global conglomerates, including ABB, Schneider Electric, and Siemens Energy, as well as specialized domestic firms such as MGM Transformer Company and Virginia Transformer Corp. No entity holds a share exceeding 15%, resulting in a moderate level of fragmentation. Scale players leverage integrated supply chains and R&D budgets to deliver high-efficiency models that align with DOE Phase 2 rules. Specialized firms compete on customization speed, localized service, and deep engineering support for niche applications, such as data-center redundancy or industrial heat pumps.

Strategic investment surged in 2024 and 2025. HitaUSEnergy allocated USD 1.75 billion to expand US capacity, targeting reduced lead times for advanced VPI coils. Eaton committed USD 340 million to its South Carolina plant, adding lines dedicated to North American grid standards. HD Hyundai Electric has launched medium-voltage production in Georgia, reflecting OEM confidence in the benefits of reshoring incentives. New entrants may encounter barriers in certification timelines and capital intensity; however, technology partnerships with storage integrators or heat-pump manufacturers offer alternative entry points.

Digitalization is the next frontier. ABB embeds fiber-optic temperature sensors for continuous thermal profiling, while Schneider Electric integrates EcoStruxure gateways for remote diagnostics. Vendors offering turnkey packages—transformers plus condition-monitoring software—differentiate themselves in utility bids by emphasizing the total cost of ownership. Competitive intensity will increase as domestic capacity expands and federal spending programs transition from award to execution phases.

United States Dry-Type Transformer Industry Leaders

ABB Ltd.

Schneider Electric SA

Siemens Energy Inc.

Eaton Corporation Inc

MGM Transformer Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Hitachi Energy has unveiled a breakthrough in dry-type insulation for transmission-level applications, reaching 765 kV.

- April 2025: The Department of Energy finalized 2029 efficiency standards for distribution transformers, triggering accelerated replacement cycles.

- March 2025: Hitachi Energy invested USD 69 million to expand its Ludvika plant, bolstering global supply for U.S. orders.

- February 2025: Eaton Corporation earmarked USD 340 million to enlarge its South Carolina factory with transformer production lines.

- January 2025: HD Hyundai Electric began production at its USD 274 million facility in Georgia, increasing domestic medium-voltage output.

United States Dry-Type Transformer Market Report Scope

The United States dry-type transformer market report include:

By Power Rating

| Large (Above 100 MVA) |

| Medium (10 to 100 MVA) |

| Small (Up to 10 MVA) |

By Phase

| Single-Phase |

| Three-Phase |

By Transformer Type

| Power |

| Distribution |

By End-User

| Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial |

| Commercial |

| Residential |

| By Power Rating | Large (Above 100 MVA) |

| Medium (10 to 100 MVA) | |

| Small (Up to 10 MVA) | |

| By Phase | Single-Phase |

| Three-Phase | |

| By Transformer Type | Power |

| Distribution | |

| By End-User | Power Utilities (includes, Renewables, Non-renewables, and T&D) |

| Industrial | |

| Commercial | |

| Residential |

Key Questions Answered in the Report

How large is the United States Dry-Type Transformer Market in 2026?

The United States Dry-Type Transformer Market size is USD 2.28 billion in 2026, on track toward USD 3.4 billion by 2031.

What is driving the biggest demand spike for dry-type transformers?

DOE Phase-2 efficiency rules and residential electrification initiatives are generating the largest volume of replacement and new-build orders.

Why are single-phase transformers growing faster than three-phase units?

Home heat-pump installations, Level-2 EV chargers, and rooftop solar-plus-storage systems increase single-phase load, pushing utilities to upgrade pole-top units.

How do aluminum and copper price swings affect procurement?

Raw-material volatility can raise transformer costs by 10-15%, prompting utilities to include price-adjustment clauses in contracts or shift windings to lower-cost metals.

Will reshoring cut lead times quickly?

New factories come online in 2026-2027, so most buyers will still face extended delivery times through 2025.

Are dry-type transformers suitable for data centers?

Yes, compact, low-loss dry-type units with advanced cooling and redundancy features are now standard in data-center power designs, aided by federal tax incentives.

Page last updated on: