Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 2.15 Billion |

| Market Size (2026) | USD 2.26 Billion |

| Market Size (2031) | USD 2.89 Billion |

| Growth Rate (2026 - 2031) | 5.07% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

United Kingdom Sports Drink Market Analysis by Mordor Intelligence

The United Kingdom sports drinks market size is expected to grow from USD 2.15 billion in 2025 to USD 2.26 billion in 2026 and is forecast to reach USD 2.89 billion by 2031 at 5.07% CAGR over 2026-2031. This growth is largely driven by consumers increasingly prioritizing functional hydration that enhances performance, boosts immunity, and promotes overall wellness. While isotonic formulations dominate the market, a growing awareness of nutrition is steering attention towards hypotonic alternatives, known for their rapid fluid absorption. Disruptors, often backed by celebrities, are challenging established brands, leveraging social media clout and direct-to-consumer strategies. Meanwhile, supermarkets maintain their volume leadership, using strategic in-store visibility programs that align sports drinks with fitness products. In response to impending advertising restrictions on high-sugar items, brands are hastening their reformulation efforts, pivoting towards low- or zero-sugar, electrolyte-rich profiles that align with health objectives and meet regulatory standards

Key Report Takeaways

- By product type, isotonic beverages held 85.35% of the United Kingdom sports drinks market share in 2025, whereas the hypertonic/hypotonic segment is forecast to expand at a 6.10% CAGR through 2031.

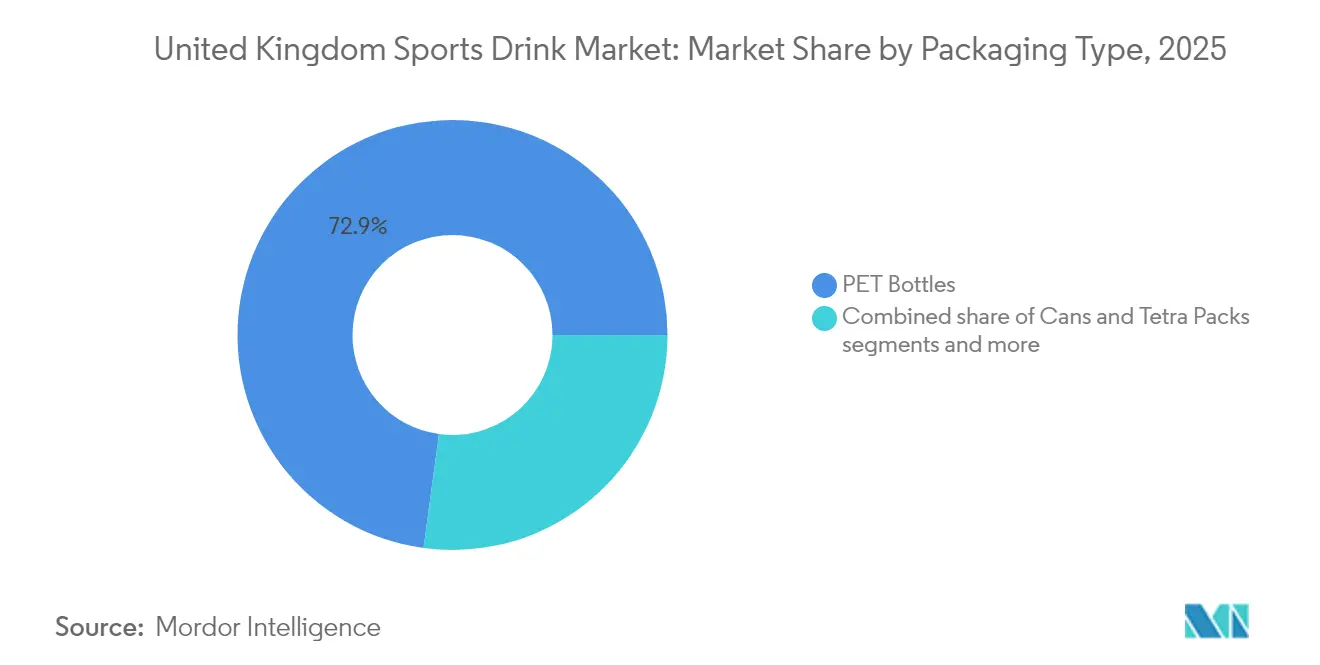

- By packaging, PET bottles commanded a 72.85% revenue share of the United Kingdom sports drinks market size in 2025; pouches/sachets are projected to register the fastest CAGR at 6.88% from 2026-2031.

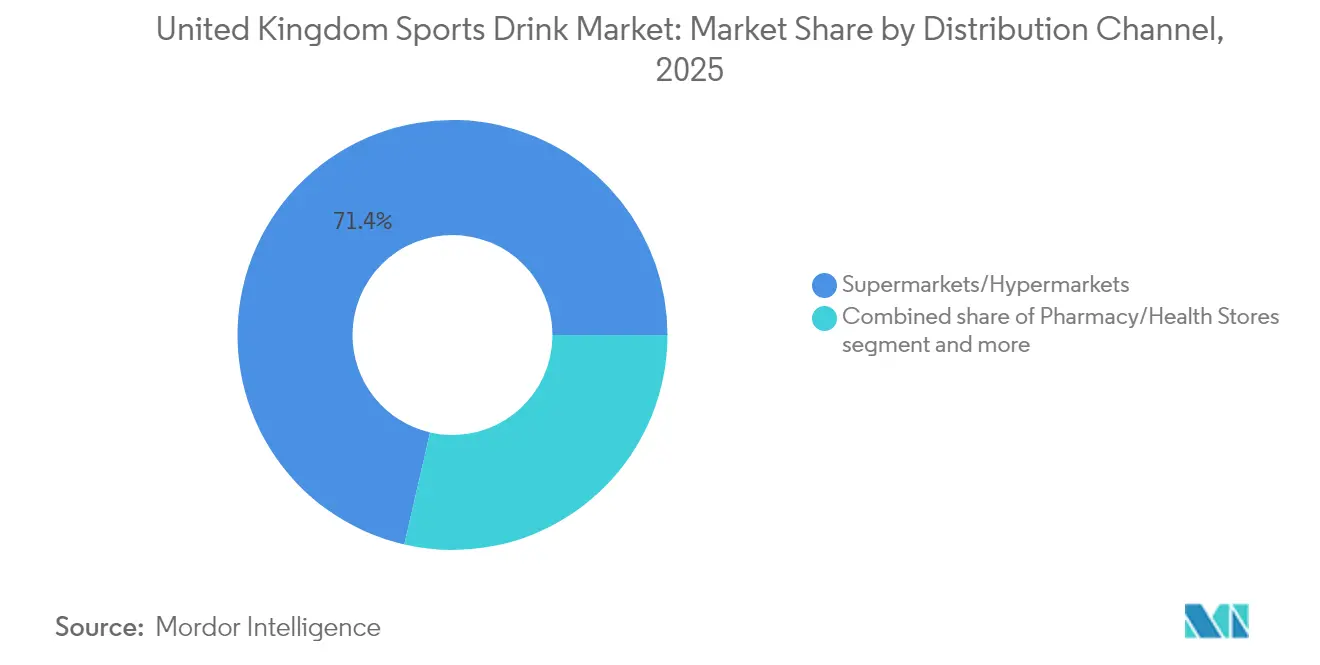

- By distribution channel, supermarkets/hypermarkets accounted for 71.40% of the United Kingdom sports drinks market size in 2025, yet online retail is growing at 8.95% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Sports Drink Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption of sports drinks among gym-goers and fitness enthusiasts | +1.2% | UK-wide, with concentration in urban centers | Medium term (3-4 years) |

| Rise in endurance event across the country | +0.8% | UK-wide, with higher impact in metropolitan areas | Medium term (3-4 years) |

| Product innovation with functional additives | +1.5% | UK-wide | Long term (≥ 5 years) |

| Brand endosements by professional athletes and sports celebrities fueling demand | +0.7% | UK-wide, with higher impact among younger demographics | Short term (≤ 2 years) |

| Growing demand for natural and organic ingredients in sports drinks | +0.9% | UK-wide, with higher adoption in affluent regions | Long term (≥ 5 years) |

| Rising disposable incomes leading to increased spending on premium products | +0.6% | UK-wide, with concentration in high-income areas | Medium term (3-4 years) |

| Source: Mordor Intelligence | |||

Adoption of Sports Drinks Among Gym-Goers and Fitness Enthusiasts

In the UK, a burgeoning fitness culture is reshaping how consumers view sports drinks, pivoting the focus from mere performance enhancement to hydration as a lifestyle choice. Health-conscious individuals—ranging from casual gym-goers and wellness aficionados to active seniors—are on the lookout for hydration solutions that align with broader health objectives like boosting immunity, enhancing energy, and aiding recovery. This shift has sparked heightened interest in beverages enriched with vitamins, minerals, adaptogens, and nootropics. Data from Sport England reveals a notable uptick in fitness class participation in England, with about 6.7 million attendees between November 2023 and November 2024, a rise from the previous 6.2 million [1]Source: Sport England, " Active Lives Adult Survey November 2023-24", sportengland.org. Furthermore, there is a growing consumer preference for low- or zero-sugar options, natural ingredients, and plant-based formulations in the clean-label segment.

Companies are repositioning from sports performance to wellness solutions providers, driven by increased demand for ingredient transparency and sourcing information. The market application of sports drinks has expanded beyond exercise recovery to daily consumption during work and commuting. Companies in the UK energy drinks market have adjusted their market strategy to emphasize cognitive benefits, sustained energy, and hydration. Product innovation has increased, particularly among new market entrants combining hydration with wellness benefits. Companies leveraging digital channels to communicate product benefits and clean-label attributes are gaining market share.

Rise in Endurance Event Across the Country

The UK endurance sports market shows substantial growth, driving increased demand for sports hydration products. IRONMAN 2025 data positions the UK as the second-largest market globally for triathlon participation, with a 39% increase in new participants since 2019. This market expansion creates opportunities in the sports hydration segment, particularly among recreational and semi-professional athletes implementing structured hydration protocols. Additionally, market demand focuses on products delivering specific electrolyte balance, carbohydrate content, and absorption efficiency for both competition and training needs. Research indicates the requirement for hydration solutions adapted to exercise intensity and environmental factors. The UK's variable weather conditions necessitate products suitable for different climate scenarios. Besides, market offerings include temperature-adaptive formulations and varying concentrations for different exercise durations. Companies developing specialized products for specific athletic applications demonstrate strong potential in the UK sports hydration market, supported by continuous growth in endurance sports participation.

Product Innovation with Functional Additives

In the UK, sports drink brands are diversifying their product offerings by incorporating bioactive ingredients that provide functional benefits beyond hydration. The functional beverage market is experiencing rapid growth, driven by Millennials and Gen Z consumers who increasingly demand products tailored to specific health objectives, such as improved gut health, enhanced cognitive performance, and faster post-exercise recovery. A prominent example of this trend is Brighter Boost, a new entrant that utilizes mushroom-derived compounds to boost vitality, strengthen immunity, and alleviate fatigue. This positions the brand as a natural and innovative alternative to conventional sports drinks, appealing to health-conscious consumers. Furthermore, advancements in formulation science are reshaping the market, with a focus on achieving the optimal balance of carbohydrates and electrolytes. Research underscores that hypotonic solutions, particularly those with sodium concentrations of 45 mmol/L or higher and a carbohydrate content of 2-6%, can significantly enhance fluid absorption and retention during intense physical activity, thereby improving hydration and performance outcomes.

Brand Endosements by Professional Athletes and Sports Celebrities Fueling Demand

In the UK sports drinks market, brands are building consumer engagement through strategic partnerships with athletes. These collaborations have developed beyond endorsements into comprehensive partnerships that include co-creation, product development, and equity investments. This approach particularly appeals to Gen Z and millennial consumers, who value authentic connections and cultural relevance in brand communications. For instance, Prime Hydration demonstrated this strategy in May 2024 with its limited edition bottle featuring footballer Erling Haaland. The campaign combined sports and influencer appeal to attract both football fans and digital-first consumers. The partnership with Haaland, a globally recognized athlete, enhanced Prime's market position and brand credibility. Besides, athletes are increasingly becoming brand stakeholders rather than just endorsers, creating stronger consumer trust. UK footballer Harry Kane exemplifies this trend through his investments in health-focused beverage and snack startups. Kane provides strategic input and promotes products aligned with his wellness philosophy, helping brands connect with established fan communities. As consumers become more selective about brand authenticity, these meaningful athlete partnerships serve as trust signals. Companies that develop long-term relationships with sports figures strengthen their market position while establishing new benchmarks for consumer loyalty and brand identity in the UK sports drinks market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adulteration and mislabeling to impact the market | -0.9% | UK-wide | Medium term (3-4 years) |

| Regulatory compliance requirements | -1.1% | UK-wide | Short term (≤ 2 years) |

| Concerns over sugar content driving demand for low-sugar options | -0.8% | UK-wide, with higher impact in health-conscious segments | Medium term (3-4 years) |

| Seasonal demand fluctuations | -0.4% | UK-wide, with higher impact in regions with extreme weather | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Adulteration and Mislabeling to Impact the Market

Concerns over product integrity are causing ripples in the sports drinks market. Scientific investigations have unveiled a gap between what labels claim and the actual formulations. A study on isotonic beverages revealed that 33% of the products, despite being marketed as isotonic, didn't meet the osmolality standards of 270-330 mOsm/kg. This mislabeling not only highlights a significant oversight but also erodes consumer trust. The issue isn't limited to osmolality; many products boast functional claims, yet contain sugars like glucose and fructose. While these sugars can traverse cell membranes, they influence the product's tonicity, even if the technical osmolality standards are met. This growing skepticism, especially among informed athletes, is stunting market growth. As these athletes become more discerning about efficacy claims, brands that prioritize rigorous testing and transparently communicate scientifically validated benefits stand to gain a competitive edge. This advantage becomes even more pronounced as the market matures and regulatory scrutiny tightens.

Regulatory Compliance Requirements

The UK sports drinks market is implementing strategic changes to comply with new regulatory requirements. From October 2025, regulations will prohibit advertisements for high-fat, sugar, or salt (HFSS) products before 21:00 (9 PM). The regulations will also restrict volume-based promotional activities such as "buy one, get one free." These changes primarily impact traditional sports drinks with high sugar content, driving market demand toward low- and no-sugar alternatives. Besides, manufacturers are implementing product reformulation strategies by incorporating natural sweeteners like stevia and monk fruit. They are also enhancing their product portfolio with electrolytes, vitamins, and adaptogens to maintain their market position. The UK Food Standards Agency is facilitating this market transition by optimizing the approval process for regulated products, enabling efficient market entry for new functional formulations. Moreover, the regulatory framework modifications encompass product labeling requirements, mandating clear presentation of ingredients, allergens, nutritional content, and storage specifications. These requirements, in conjunction with increasing eco-labeling initiatives, are influencing product development and packaging strategies. The regulatory evolution is enhancing market transparency and consumer safety while facilitating product innovation in alignment with the UK's health and environmental objectives.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Packaging Type: PET Bottles Face Sustainable Challenger

In 2025, PET bottles command a dominant 72.85% market share, owing to their consumer-friendly design, convenience, and broad acceptance in retail. Their ergonomic and resealable features cater perfectly to today's on-the-go consumers. Yet, this segment grapples with sustainability hurdles. UK retailers, responding to consumer demand and regulatory pressures, are ramping up climate initiatives to curb plastic waste. The British Retail Consortium, with its ambitious roadmap, targets a net-zero retail industry by 2040. This push for sustainable packaging practices could reshape the dominance of PET bottles in the sports drinks arena.

Pouches and sachets are set to outpace all other formats, boasting a projected CAGR of 6.88% from 2026 to 2031. Their rise is attributed to a commendable sustainability profile and distinct functional advantages. Bioplastics, with global production capacity projected to surge from 2.1 million tonnes in 2019 to 6.3 million tonnes by 2027, promise material innovations bolstering the environmental appeal of pouches as per European Bioplastics (EUBP). These pouches, championing a significant material reduction over rigid containers, resonate with Greenpeace's call for UK supermarkets to slash plastic packaging by 50% by 2025. Beyond sustainability, pouches offer tangible benefits: lighter shipping weights, better product-to-packaging ratios, and enhanced portability for the active consumer.

By Product Type: Isotonic Dominates While Hypotonic Gains Momentum

In 2025, isotonic sports drinks dominate the market with an 85.35% share, solidifying their status as the go-to hydration choice for consumers prioritizing balanced electrolyte replenishment. Their popularity is largely due to their compatibility with the body's fluid composition, ensuring quick absorption during physical exertion. Studies show a notable number of athletes consume these drinks weekly. Furthermore, research highlights a significant link between isotonic drink consumption and dental sensitivity (p <0.001), shedding light on a health aspect often overlooked by regular users. The segment's expansion is being propelled by innovations in natural sweeteners and functional additives, which not only preserve the drinks' isotonic properties but also address emerging health concerns.

Though the hypertonic/hypotonic segment is currently smaller, it's set to outpace the market with a projected CAGR of 6.10% from 2026-2031. This growth is attributed to consumers becoming more discerning about their hydration needs. Scientific studies indicate that hypotonic solutions, especially those with sodium levels of ≥45 mmol/L and a carbohydrate content of 2-6%, can boost fluid absorption and retention during high-intensity workouts. This scientific backing is fueling the segment's growth. Performance-driven consumers are gravitating towards these specialized hydration solutions, tailored for specific activities and intensities. Innovations focusing on swift absorption and lower carbohydrate content are elevating hypotonic variants to premium status among dedicated athletes. Meanwhile, hypertonic drinks are carving out a niche in recovery-centric formulations.

By Distribution Channel: Digital Disruption Challenges Retail Dominance

In 2025, supermarkets/hypermarkets commanded a dominant 71.40% share of the UK sports drinks market, due to their widespread accessibility and the trust consumers place in established retail formats. These outlets adeptly employ cross-merchandising tactics, positioning sports drinks alongside gym gear, health snacks, and protein products to spur impulse purchases. Yet, this stronghold faces challenges from shifting regulations and environmental initiatives. Scotland's Deposit Return Scheme (DRS), set to debut in 2024, imposes a 20p deposit on single-use containers to promote recycling. England, Wales, and Northern Ireland are eyeing similar initiatives by 2025 . While these environmentally driven programs are commendable, they could reshape buying habits and inventory strategies in physical stores, possibly steering consumers towards more convenient or eco-friendly options, like bulk online purchases.

At the same time, online retail is carving out a significant niche, forecasting a robust CAGR of 8.95% from 2026 to 2031. This surge underscores a broader digital transformation in UK retail, highlighting the allure of subscription models and personalized recommendations. Prime Hydration stands out, deftly merging e-commerce prowess with strategic partnerships at select physical retailers. Online platforms boost consumer interaction by providing in-depth nutritional details, user feedback, and usage tips. This is particularly vital as consumers increasingly gravitate towards drinks boasting specific benefits, be it energy replenishment, immunity enhancement, or recovery support. Meanwhile, pharmacies and health stores emphasize high-performance, clinically backed products, and vending machines alongside fitness studios cater to a niche yet expanding audience craving instant hydration solutions.

Geography Analysis

In the UK, regional consumption patterns of sports drinks are shaped by demographics, income levels, and lifestyle choices. Urban hubs, notably London, Manchester, and Birmingham, are at the forefront of embracing premium, functional, and plant-based sports drinks. This trend is driven by a higher density of fitness centers, heightened health awareness, and increased disposable incomes. In the fiscal year ending 2023, UK households dedicated 11.2% of their total spending to food and non-alcoholic beverages. Yet, there's a notable income disparity: the lowest 20% of households by disposable income allocated 14.4% to these essentials, contrasting with just 8.5% from the top 20% . Such differences indicate that while affluent urbanites may gravitate towards premium sports drinks, those in lower-income brackets and rural locales are more inclined towards value-centric options.

Geographically concentrated demand peaks are also influenced by participation in organized sports and endurance events. Cities like Leeds, Bristol, and Edinburgh, known for hosting marathons, triathlons, and CrossFit competitions, are emerging as key markets for performance hydration products. In response, brands are tailoring their campaigns, sponsoring local events, and introducing limited-edition flavors exclusive to specific regions.

Furthermore, a clear urban-rural divide in product preferences is evident: city dwellers are more open to innovations such as nootropic-enhanced hydration and eco-friendly packaging, whereas rural consumers tend to stick with traditional electrolyte-based drinks. Additionally, spending on food and drink consumed outside the home saw a slight uptick, rising from GBP 116.9 billion in 2022 to GBP 117.6 billion in 2023, as per the Department for Environment, Food & Rural Affairs. This trend underscores a broader consumer inclination towards convenience and health-focused products, including sports beverages.

Competitive Landscape

The sports drink market in the United Kingdom is moderately consolidated, with a few dominant players competing for market share. Key companies in this market include PepsiCo Inc., Suntory Holdings Ltd, The Coca-Cola Company, and SiS (Science in Sport) Limited. These companies are heavily investing in research and development to introduce innovative and functional products while enhancing their marketing strategies to strengthen brand visibility. Additionally, they are expanding their distribution networks to reach a wider consumer base and maintain their competitive edge.

To sustain their market positions, these companies are adopting diverse strategies such as product innovation, deeper penetration into retail channels, and forming strategic alliances. These alliances include mergers, acquisitions, and joint ventures aimed at improving bottling and distribution capabilities. The competitive landscape has intensified further with the entry of celebrity-backed brands. For example, Prime Hydration, co-founded by influencers Logan Paul and KSI, has quickly captured a significant share of the market. This success is driven by a strategic combination of social media influence, partnerships with prominent influencers, and targeted retail distribution, which has resonated strongly with younger demographics.

Market players are increasingly prioritizing functional innovation and niche positioning over broad market strategies. Science in Sport PLC exemplifies this trend by catering to over 330 professional sports teams globally, including more than 150 football clubs across the United Kingdom, Europe, and the USA, through its specialized endurance nutrition brand. The company employs a dual-brand strategy, with PhD Nutrition focusing on active lifestyle consumers and SiS targeting endurance athletes. This shift toward segment-specific offerings reflects the market's evolution and creates opportunities in emerging niches such as mental performance enhancement, recovery optimization, and sustainable product formulations. These trends highlight the growing importance of specialization and innovation in driving market growth and differentiation in the competitive landscape.

United Kingdom Sports Drink Industry Leaders

-

PepsiCo Inc.

-

Suntory Holdings Ltd

-

The Coca-Cola Company

-

Congo Brands (Prime Hydration LLC)

-

SiS (Science in Sport) PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Más+ by Messi, a sports hydration beverage developed through a collaboration between Lionel Messi and Mark Anthony Group, entered the United Kingdom market through Spar retail locations. The product portfolio included four varieties: Limon Lime League, Berry Copa Crush, Orange d'Or, and Miami Punch.

- March 2025: Lucozade Sport introduced Ice Kick, a new beverage developed in collaboration with England football player Jude Bellingham. The product became available in 500ml bottles, including price-marked variants, and 4x500ml multipacks.

- February 2025: Punchy introduced the first premium hydration canned drinks in the United Kingdom, which represented a notable development in the functional beverage market. The drinks featured natural ingredients combined with hydration benefits, which catered to health-conscious consumers who preferred convenient beverage options. The product launch established Punchy's presence in the premium hydration category.

- May 2024: Boost Drinks expanded its product portfolio by introducing three new beverages in its energy and sport ranges. The company introduced two sugar-free energy drink flavors - Tropical Blitz and Apple & Raspberry. This product introduction aligned with changing consumer preferences, as research demonstrated that one-third of consumers selected sugar-free beverages. The company sought to address the increasing demand in the sugar-free energy drinks segment.

United Kingdom Sports Drink Market Report Scope

Sports drinks are functional beverages designed for individuals requiring instant energy before, during, and after sports training or competition. They are typically enhanced with electrolytes to provide this immediate energy.

The United Kingdom sports drink market is segmented by product type, packaging type, and distribution channels. By product type, the market is segmented into isotonic and hypertonic/hypotonic. By packaging type, the market is segmented into PET bottles, cans, tetra packs, and pouches/sachets. By distribution channel, the market is segmented into supermarkets/hypermarkets, pharmacies/health stores, online retail stores, and other distribution channels. The market sizing has been done in value terms in USD for all the abovementioned segments.

By Product Type

| Isotonic |

| Hypertonic/Hypotonic |

By Packaging Type

| PET Bottles |

| Cans |

| Tetra Packs |

| Pouches/Sachets |

By Distribution Channel

| Supermarkets/Hypermarkets |

| Pharmacy/Health Stores |

| Online Retail Stores |

| Other Distribution Channels |

| By Product Type | Isotonic |

| Hypertonic/Hypotonic | |

| By Packaging Type | PET Bottles |

| Cans | |

| Tetra Packs | |

| Pouches/Sachets | |

| By Distribution Channel | Supermarkets/Hypermarkets |

| Pharmacy/Health Stores | |

| Online Retail Stores | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the current value of the UK sports drinks market?

The market is worth USD 2.26 billion in 2026 and is projected to grow at 5.07% CAGR to 2031.

Which product type leads sales?

Isotonic drinks dominate with 85.35% share in 2025, owing to their balanced carbohydrate–electrolyte profile.

Which distribution channel is growing fastest?

Online retail is expanding at 8.95% CAGR over 2026-2031, driven by subscription models and direct-to-consumer engagement.

What packaging innovations are on the horizon?

Expect increased use of pouches made from bioplastics and higher-recycled-content PET bottles as retailers pursue 2040 net-zero packaging goals.

Page last updated on: