United Kingdom Lime Market Analysis by Mordor Intelligence

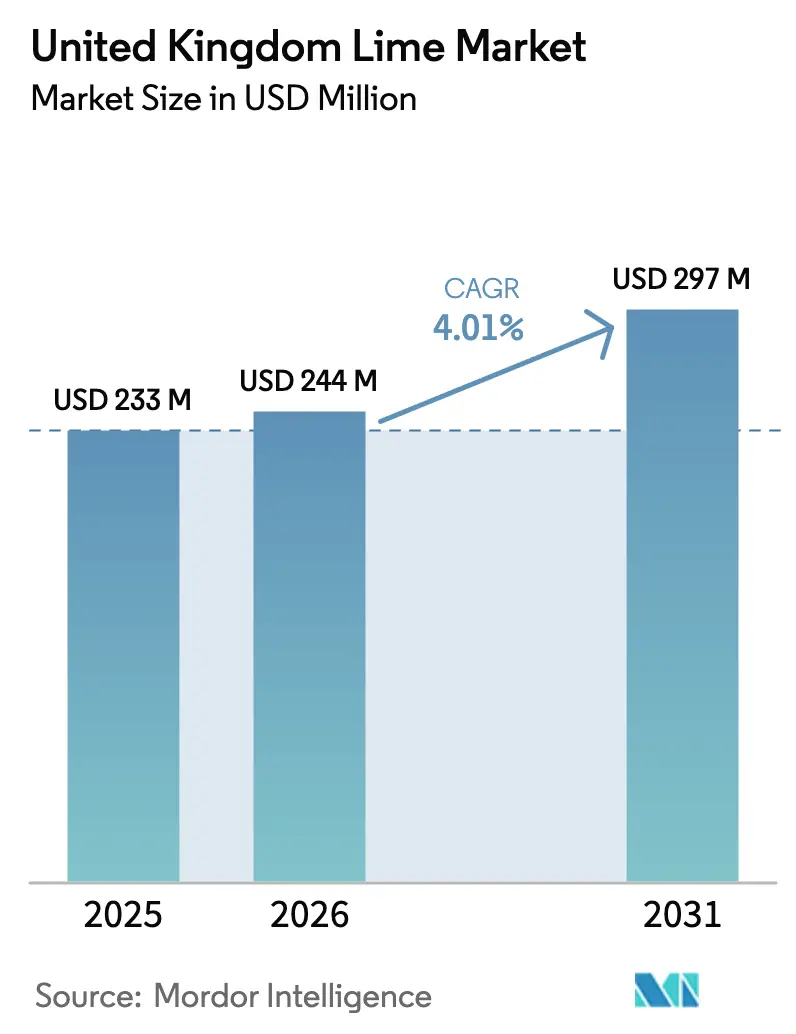

The United Kingdom lime market size is expected to grow from USD 233.0 million in 2025 to USD 244.0 million in 2026 and is forecast to reach USD 297.0 million by 2031 at a 4.01% CAGR over 2026-2031. Import dependence defines the United Kingdom lime market, because domestic output is negligible, and the country ranked fifth worldwide for lime and lemon imports in 2023. Spain remains the anchor supplier, yet post-Brexit phytosanitary friction and freight rate swings that climbed back above USD 4,000 per forty-foot equivalent unit in late 2024 are steering buyers toward South American origins. Scale economies in ripening, pack-house automation, and multi-origin procurement keep the top five firms in control significant share of 2025 revenue, limiting headroom for new entrants. Demand drivers include the growing popularity of ready-to-drink cocktails, the increasing adoption of Mexican cuisine, and the shift toward clean-label products, encouraging beverage manufacturers to use natural lime juice and oil.

Key Report Takeaways

- By geography, England accounted for 60% of the United Kingdom lime market demand in 2025, whereas Scotland is forecast to post the fastest growth at 7.2% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

United Kingdom Lime Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in popularity of Mexican-style cuisine | +1.2% | London, Manchester, Edinburgh, and Glasgow | Medium term (2–4 years) |

| Growth of ready-to-drink (RTD) cocktail segment | +1.5% | National impulse retail and on-trade | Short term (≤ 2 years) |

| Retailer commitments to year-round lime availability | +0.6% | All United Kingdom regions | Long term (≥ 4 years) |

| Rising demand for natural citric acid replacements | +0.8% | Beverage and food hubs in England | Medium term (2–4 years) |

| E-commerce fresh-produce delivery expansion | +0.5% | Metropolitan England and Scotland | Short term (≤ 2 years) |

| Brexit-driven sourcing diversification incentives | +0.4% | Import-dependent supply chains nationwide | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Popularity of Mexican-Style Cuisine

Mexican dishes have graduated from niche to staple on restaurant menus across the United Kingdom, elevating the use of fresh lime in tacos, marinades, and salsa. Fast-casual chains and independent taquerias in London, Manchester, and Bristol now depend on steady citrus deliveries to meet higher footfall. Recipe sites and meal-kit services reinforce the habit at home, specifying fresh lime juice and zest for authenticity. Younger diners value bold flavors and are willing to pay a premium for genuine ingredients, locking limes into regular baskets. The combined demand from retail and foodservice significantly enhances the long-term market growth rate.

Growth of Ready-to-Drink Cocktail Segment

The ready-to-drink cocktail category expanded rapidly in 2025, with a significant surge in impulse channels, directly boosting industrial demand for lime juice and oil. Brands such as Fever-Tree now derive the majority of domestic sales from non-tonic mixers that showcase margarita and mojito profiles. Beverage processors choose natural lime inputs to secure clean-label claims that resonate with health-conscious consumers. Lightweight cans and sustainable packaging broaden distribution into festivals, travel hubs, and convenience stores. Faster on-shelf rotation results in a noticeable increase in projected growth.

Retailer Commitments to Year-Round Lime Availability

United Kingdom grocers treat uninterrupted lime supply as a key loyalty lever, shifting origins between Brazil, Mexico, Peru, Spain, and Vietnam to bridge seasonal gaps. Multi-origin programs require compliance with Global Good Agricultural Practices (GLOBALG.A.P.) and Linking Environment And Farming (LEAF) Marque standards, effectively raising entry barriers for uncertified growers. Consistent shelf presence conditions shoppers to treat limes as an everyday staple rather than an occasional purchase. Retailers also publicize transparent sourcing on pack labels to meet corporate responsibility goals.

Rising Demand for Natural Citric Acid Replacements

Manufacturers are phasing out synthetic citric acid and replacing it with real lime juice and oil to meet clean-label expectations and comply with tightening additive regulations. The global natural citrus-flavor market has grown significantly in 2025, with beverages accounting for the majority of applications, and lime gaining share as orange prices soar. Lime delivers both flavor and functional pH control, allowing brands to meet sulfite caps without artificial preservatives. Clear guidance from food safety authorities gives formulators the confidence to scale natural recipes nationwide.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile import logistics and freight costs | -0.9% | All United Kingdom ports | Short term (≤ 2 years) |

| Phytosanitary interceptions on Mexican shipments | -0.6% | Dover, Felixstowe, and Southampton | Medium term (2–4 years) |

| Labor shortages in pack-houses | -0.5% | Kent, Lincolnshire, and Tayside | Medium term (2–4 years) |

| Cold-chain energy price escalation | -0.4% | National refrigerated infrastructure | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Phytosanitary Interceptions on Mexican Shipments

Asian citrus psyllid and citrus black spot spur heightened border scrutiny. Random inspections can trigger rejections costing GBP 500 to GBP 2,000 (USD 625 to USD 2,500) per container and delay delivery by up to a week [1]Source: Fresh Produce Consortium, “UK Border Notifications Data January-April 2025,” freshproduce.org.uk . Mexico sends most fruit to the United States, leaving United Kingdom buyers to compete for the limited compliant volume. Some importers pilot rapid-DNA pest detection to cut hold times, yet the technology remains costly. Ongoing biosecurity measures are projected to slightly impact the forecasted growth rate.

Cold-Chain Energy Price Escalation

Commercial electricity averaged GBP 0.25-0.30 per kWh (USD 0.31-0.38) in 2025, lifting refrigeration expenses by up to 60% [2]Source: UK Government, “Energy Statistics and Prices,” Department for Energy Security and Net Zero, gov.uk. Large retailers install solar and heat pumps, but small distributors lack capital buffers. Energy now represents as much as 18% of cold-chain operating costs for limes held at 10-13 °C. Looming carbon taxes on fossil-based grid power threaten to raise tariffs further, compounding cost pressure. Higher power prices negatively impact the market growth.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Geography Analysis

England accounted for 60% of national demand in 2025, driven by population density, proximity to entry ports, and a sophisticated foodservice ecosystem. London’s cosmopolitan palate underpins premium-varietal sell-through, while Kent and Lincolnshire pack-houses streamline distribution into major retailers. Growth is challenged by labor shortages and increasing power costs, which place pressure on smaller operators. England will retain its leadership due to its infrastructure scale, even as diversification unfolds.

Scotland is set to record the fastest 7.2% CAGR amid post-pandemic whisky tourism and a vibrant cocktail scene in Edinburgh and Glasgow. Distilleries that integrate mixology experiences boost lime usage in whisky sours and highballs. Longer logistics chains add one to two days of transit and elevate spoilage pressures, but importers with direct delivery programs gain an edge. Rising disposable income also expands premium lime adoption across urban Scottish consumers.

Wales and Northern Ireland represent modest portions of the United Kingdom lime market, mirroring national trends with a slight lag. Urban centers such as Cardiff and Belfast sustain foodservice uptake but lack the critical mass seen in England. Both regions depend significantly on English distribution hubs, which help manage inventory risk but increase lead times. Future growth will track demographic expansion and supermarket penetration of exotic and organic assortments.

Regulatory Landscape

Agricultural lime placed on the United Kingdom market falls under the national fertiliser rule set, anchored by The Fertilisers Regulations 1991 and retained EU-derived provisions such as the EC Fertilisers (England and Wales) Regulations 2006. These frameworks drive mandatory product declarations at delivery, including the specific liming material type, neutralising value (NV), and granulometric (sieve) analysis, with defined tolerances such as variation limits of 5% on declared NV and sieve pass percentages.

In parallel, industry quality assurance is shaped by the AgLime Quality Standard (AQS), a voluntary scheme verified by Kiwa and benchmarked to BS EN 13971 performance concepts. In March 2026, DEFRA issued updated fertiliser regulatory reform proposals focused on modernising standards and improving supply chain resilience, which matters for suppliers that depend on consistent testing, documentation, and audited quality systems. For lime used beyond land application, additional oversight applies, including Food Standards Agency requirements for any lime-based products classed as feed additives and environmental permitting expectations under LAPC/LAPPC regimes for industrial lime processes.

Value Chain Analysis

The United Kingdom lime value chain starts with limestone quarrying and processing into agricultural liming materials that meet fertiliser declaration requirements, including stated neutralising value and particle-size distribution. Because lime is bulky and low unit-value, transport economics shape sourcing radii, and downstream movement is typically organised around local-to-regional haulage into agricultural merchant networks.

Midstream, merchants and agronomy service providers bundle lime with soil pH testing, nutrient planning, and application support, while professional spreading contractors deliver field execution for large-area treatment programs. Industry coordination and quality benchmarking are supported by the Agricultural Lime Association (ALA) under the Mineral Products Association umbrella, including the AQS program for independent chemical and granulometric certification. Bottlenecks in the chain mainly concentrate on logistics and service capacity, so integrated offerings (supply, testing, and spreading) and verified product consistency tend to differentiate suppliers when competing for farm programs and large account contracts.

Competitive Landscape

The United Kingdom lime market is highly concentrated, with the top players dominating a significant share of the revenue. These companies utilize purchasing power and automated ripening processes to ensure a consistent supply. Worldwide Fruit Ltd, backed by Dole’s global farming network, controls sourcing from multiple hemispheres and operates automated ripening rooms that guarantee consistent fruit maturity for supermarket programs [3]Source: Dole plc, “Dole UK Operations and Sustainability Report,” dole.com. Minor Weir and Willis Ltd specializes in foodservice-grade Key limes and maintains year-round volume through grower alliances in Mexico and Brazil. Their dominance also lets them negotiate favorable freight contracts that cushion margin swings tied to volatile shipping rates.

Fresca Group Ltd strengthens retail presence with premium private-label lines that meet stringent Global Good Agricultural Practices (GLOBALG.A.P.) and Linking Environment And Farming (LEAF) Marque requirements. Westfalia Fruit International leverages vertically integrated orchards in South Africa and South America to supply both conventional and organic Persian limes, appealing to grocers focused on traceability and sustainability. AMT Fruit Ltd concentrates on exclusive supermarket supply deals and uses in-house quality labs to meet the tight cosmetic standards demanded by large chains. Collectively, these firms complement the leaders by filling specialty, organic, and private-label niches that broaden category reach.

All five companies are scaling automation, blockchain-based traceability, and renewable energy projects to meet retailer sustainability scorecards and reduce operating costs. Investment in artificial-intelligence demand forecasting helps align imports with weekly sales curves, cutting waste and improving shelf life. Strategic diversification into finger lime and other exotic varietals positions the group to tap premium segments that carry higher margins and spur category value growth. As compliance costs and energy prices remain elevated, the market is projected to consolidate further around these integrated players, reinforcing their ability to expand the United Kingdom lime market through 2031.

Market Opportunities and Future Outlook

One core opportunity in the United Kingdom lime market is improving the penetration and regularity of soil pH correction against agronomic targets. Guidance commonly cites target soil pH levels of about 6.5 for cropped land and 6.0 for grassland (with lower targets on peaty soils). Industry and technical references also point to annual agricultural lime usage around 1.5 to 1.8 million tonnes, down from historical highs above 7 million tonnes, leaving room for solutions that pair verified product quality, including AQS-aligned specifications, with advisory-led programs that turn periodic buying into managed soil-health routines.

A second whitespace area is service and technology enablement, where GPS soil sampling and variable-rate application can improve placement efficiency and reduce over-application on higher-pH zones. Suppliers and merchants that package soil testing, prescription mapping, and spreading capacity into a single offer can shift procurement discussions from lowest delivered price to neutralising-value-per-pound applied and field performance. Policy and compliance changes also shape commercial focus, with DEFRA fertiliser regulatory reform activity in 2026 pointing to an active standards environment, and decarbonisation initiatives in lime and cement clusters increasing attention on production footprint and traceable, audited supply chains for farm-facing customers.

Recent Industry Developments

- May 2026: Longcliffe Quarries announced a multi-million-pound investment to build a new granulated lime manufacturing plant at its Brassington Moor Quarry, with the facility planned to be operational by the end of 2026. The investment adds domestic capability in higher-value granulated formats that can support easier handling and more flexible application windows for farm customers.

- September 2025: Buxton Lime commissioned a new milk of lime plant at its Tunstead Quarry. The commissioning expands on-site processing capability, strengthening supply options for industrial and environmental applications that require consistent slurry quality and reliable local availability.

- March 2024: Coca-Cola launched Coca-Cola Original Taste Lemon and Coca-Cola Zero Sugar Lemon in the United Kingdom. The rollout reinforced activity in citrus-flavoured beverages, supporting incremental demand for lemon and lime flavour inputs across branded and private-label formulation pipelines.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the market covers lime (edible limes) sold for consumption in the United Kingdom, counted as the value of fruit traded through importers, distributors, and retail and foodservice channels.

Scope exclusions: We exclude industrial lime and lime-based chemicals used for construction, steel, mining, and water treatment, and we do not count value added from downstream processed products like beverages or flavors.

Segmentation Overview

- United Kingdom

- Production Analysis

- Production Volume

- Area Harvested and Yield

- Consumption Analysis (Value and Volume)

- Trade Analysis (Value and Volume)

- Import Market Analysis

- Import Value and Volume

- Key Supplying Markets

- Export Market Analysis

- Export Value and Volume

- Key Destinations Markets

- Import Market Analysis

- Wholesale Price Trend Analysis and Forecast

- Regulatory Framework

- Logistics and Infrastructure

- Seasonality Analysis

- Production Analysis

Data Sources, Market Sizing, and Validation

Desk Research

Desk research started with public statistics that show the demand and supply balance for limes in the United Kingdom, which is the main reason the market sizing is import-led. We used sources such as HM Revenue and Customs trade data, UN Comtrade mirror trade, and FAOSTAT for global production context to explain availability by season.

To cross-check volumes and price direction, we also reviewed publications and datasets from sources such as the Office for National Statistics and the UK Department for Environment, Food and Rural Affairs (for broader horticulture context), alongside peer-reviewed papers on citrus supply chains and post-harvest losses. Company filings, importer and wholesaler presentations, association websites, and reputed press were used to confirm channel structure and typical markups. Paid subscriptions were referenced selectively for company financials, news screening, and shipment-level import checks. These sources are illustrative, and many other public and paid references were also reviewed to collect data, validate assumptions, and clarify open questions.

Primary Interviews and Surveys

Primary work focused on validating how imported limes move through the UK, how price changes pass through to buyers, and what shifts demand between retail and foodservice. We spoke with a mix of importers, distributors, category managers, and foodservice buyers across key consuming regions, then used their inputs to confirm assumptions on wastage, average selling prices, and seasonality swings.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 27% | CXOs: 14% | |

| Mid tier: 57% | Functional/Unit leaders: 29% | |

| Smaller Players: 16% | Managers: 57% |

Market-Sizing & Forecasting

The core model is built using a top-down demand reconstruction where import volumes, re-export adjustments, and indicative wholesale-to-retail price ladders are converted into annual market value for the United Kingdom. We then corroborated totals using selective bottom-up checks, such as sampled distributor price lists multiplied by estimated throughput, and channel checks for foodservice versus retail splits so the totals do not drift away from real trading behavior.

Inputs that materially move the model include import volumes by season, average unit values from customs lines, retail and foodservice price progression, shrink and wastage rates in transit and at store level, and menu demand signals from the hospitality cycle. For forecasting, scenario analysis was used because supply shocks and freight swings can change realized prices quickly, and the assumptions were tuned using consensus views from interviewees on expected availability, currency pass-through, and substitution with other citrus when prices spike. Where data gaps appeared in price series for certain months, we used conservative smoothing and rechecked against trade unit values so short-term spikes did not overstate the annual average.

Data Validation & Update Cycle

Validation happens in layers, starting with checks that the implied consumption aligns with import totals after accounting for re-exports and reasonable loss factors. We also compare the modeled average selling price trend against independent signals like customs unit values and observed retail pricing direction, and any large variance is reviewed and explained before sign-off.

Before publication, the full model is reviewed by another analyst to catch anomalies in units, currency conversion timing, and year-on-year jumps that are not supported by market events. Reports are refreshed annually, and interim updates are triggered if there is a material change such as a sustained supply disruption or a sharp and lasting shift in import pricing. Right before delivery, we complete a final pass so clients receive the most current view available.

Mordor Intelligence's United Kingdom Lime Market Size Compared With Other Published Estimates

Published market values for the UK lime space can look far apart because the word lime is used for different products, and because some publishers build the number from industrial demand pools instead of edible fruit trade. Differences also show up when one estimate uses a different base year, applies aggressive price growth, or converts currencies using a different timing.

Some external estimates bundle quicklime and hydrated lime used in construction, metallurgy, and water treatment. In Mordor Intelligence, the count is limited to edible lime fruit value moving through UK trade and consumption channels, which excludes industrial lime derivatives and their downstream pricing layers.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 233 M (2025) | |

| Industry Publisher A | USD 487.3 M (2026) | Uses an industrial lime definition that includes quicklime, hydrated lime, and lime slurry, so the value reflects chemical and construction uses rather than edible fruit demand. |

| Market Publisher B | USD 1.0 B (2023) | Appears to apply a broad industrial scope and higher value assumptions across multiple applications, which can inflate totals versus fruit-only trade-based sizing. |

The spread in the table is mainly explained by product scope and by how prices are constructed, not by small differences in growth rates. By keeping the demand pool tied to observable UK import flows and realistic channel price ladders, the resulting number stays traceable to clear steps that can be repeated and checked year after year.

Key Questions Answered in the Report

How large will lime demand in England become by 2031?

England is projected to maintain roughly 60% of total United Kingdom lime consumption, implying about USD 0.18 billion of the United Kingdom lime market size by 2031 if regional mix holds.

Which product type grows fastest through 2031?

Finger lime posts the strongest 11% CAGR due to chef endorsement, premium grocer listings and e-commerce subscription boxes.

Why are freight costs a risk for lime importers?

Container rates on critical routes swung from USD 1,500 to more than USD 4,000 in 2024, and limes rely on refrigerated containers that attract a 25-35% premium, compressing already thin margins.

What certifications do suppliers need to list limes with supermarkets?

Global Good Agricultural Practices (GLOBALG.A.P.) for conventional and Soil Association for organic claims are effectively mandatory, while Linking Environment And Farming (LEAF) Marque adoption demonstrates integrated farm management and biodiversity compliance.

Page last updated on: