Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 7.62 Billion |

| Market Size (2026) | USD 7.75 Billion |

| Market Size (2031) | USD 8.46 Billion |

| Growth Rate (2026 - 2031) | 1.76% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Home Textile Market Analysis by Mordor Intelligence

The United Kingdom home textile market size is expected to grow from USD 7.62 billion in 2025 to USD 7.75 billion in 2026 and is forecast to reach USD 8.46 billion by 2031 at 1.76% CAGR over 2026-2031. Market resilience is rooted in unavoidable replacement cycles for bedding and bath linen, the appeal of wellness-oriented products, and a gradual rebound in hospitality refurbishments despite persisting cost-of-living pressures [1]Office for National Statistics, “Family Spending in the UK: April 2022 to March 2023,” ons.gov.uk. Intensifying e-commerce adoption, sustained interest in sustainable fibres, and duty-free sourcing from Pakistan and India under the Developing Countries Trading Scheme (DCTS) further underpin expansion. At the same time, Brexit-related customs friction, volatile cotton prices, and strict UK fire-safety regulations curb profitability, prompting retailers to pursue omnichannel efficiencies and innovation in smart antimicrobial fabrics to defend margins. Competitive intensity remains high as digital-native entrants challenge incumbents on price transparency, while established chains emphasize circular-economy initiatives to retain customer trust.

Key Report Takeaways

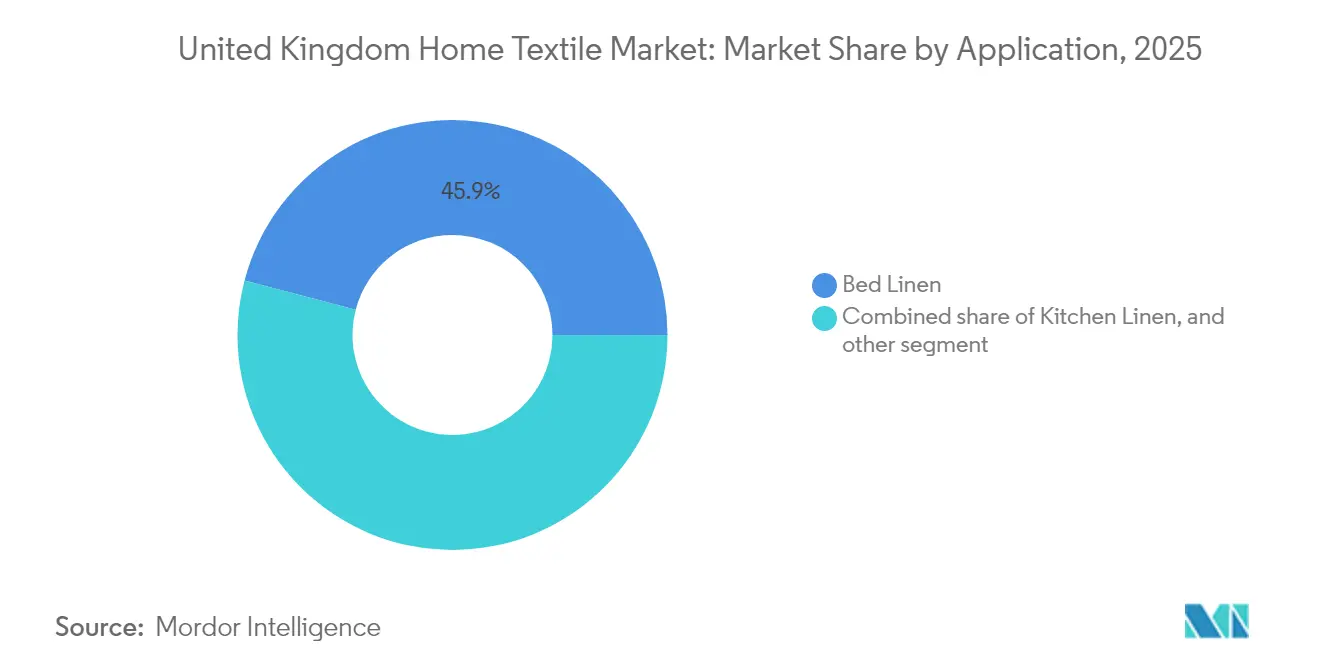

- By application, bed linen led with 45.92% of the United Kingdom home textile market share in 2025, whereas smart bedding is projected to post the fastest 8.48% CAGR through 2031.

- By material, cotton commanded 65.79% share of the United Kingdom home textile market size in 2025, while bamboo–hemp blends are on track for a 9.64% CAGR to 2031.

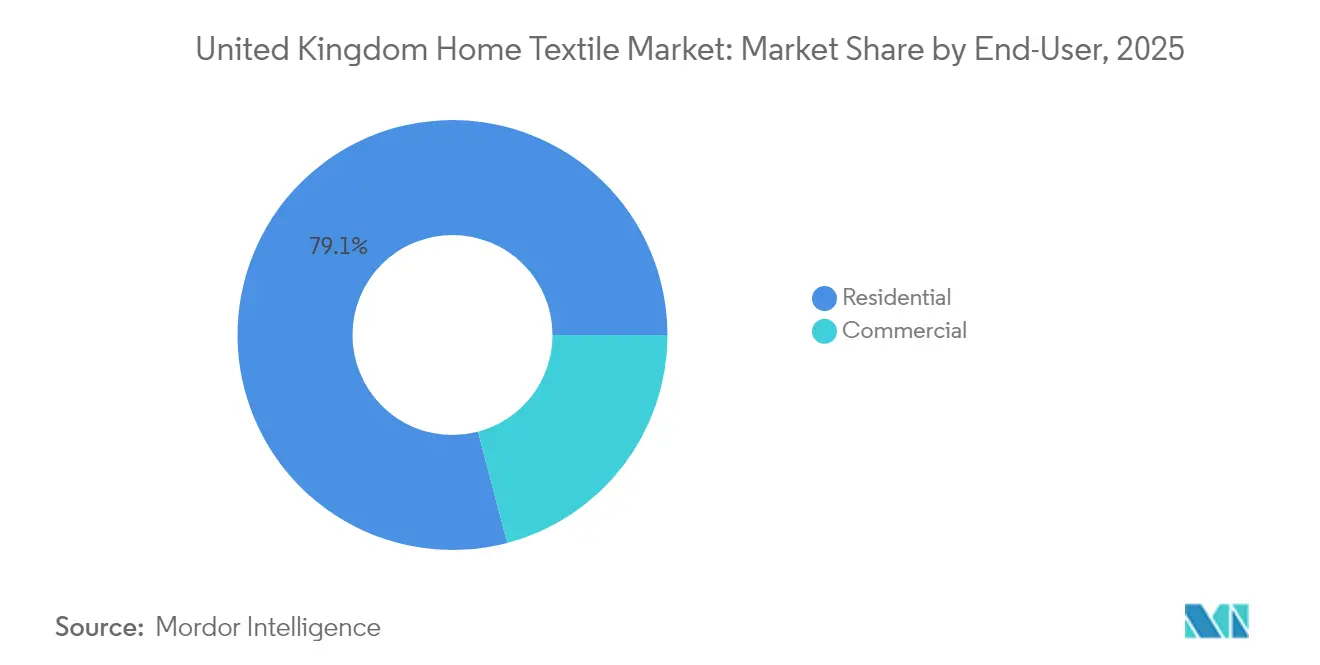

- By end-user, residential consumption accounted for a 79.10% share of the United Kingdom home textile market size in 2025, yet hospitality demand is forecast to accelerate at an 8.07% CAGR during 2026-2031.

- By distribution channel, offline retail retained a 62.70% share of the United Kingdom home textile market size in 2025, but online sales are expected to expand at a 11.72% CAGR to 2031.

- By geography, England dominated with 84.40% of the United Kingdom home textile market size in 2025, whereas Northern Ireland is set to grow the quickest at a 6.21% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Millennials’ wellness & “home sanctuary” focus | +0.4% | England, Scotland, urban centres | Medium term (2-4 years) |

| E-commerce & social-commerce penetration | +0.3% | Nationwide | Short term (≤ 2 years) |

| Sustainability-led material substitution | +0.2% | England, Scotland, and affluent areas | Long term (≥ 4 years) |

| Hospitality refurbishment cycles | +0.3% | Tourist hubs | Medium term (2-4 years) |

| Duty-free Pakistani/Indian linen under DCTS | +0.2% | Import-dependent regions | Short term (≤ 2 years) |

| Smart & antimicrobial fabric adoption | +0.1% | Premium segments | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Millennials’ Wellness and “Home Sanctuary” Focus Reshapes Purchasing Priorities

Millennials prioritize sleep quality, mental well-being, and cohesive interior aesthetics, elevating demand for temperature-regulating duvet covers, hypoallergenic sheets, and coordinated décor collections. United Kingdom household spending data show higher discretionary outlays on home comfort among under-40 cohorts, confirming a structural shift toward premium-priced textiles perceived as health investments. Persistent hybrid-work patterns sustain time spent at home, reinforcing willingness to upgrade functional bedding. Brands that combine soothing color palettes with functional finishes such as antimicrobial or moisture-wicking treatments are benefiting from repeat purchases. Subscription-based refresh programs for linens are also gaining traction among young professionals who value convenience and hygiene assurances.

E-commerce and Social-Commerce Penetration Accelerates Channel Transformation

Online participation in clothing and home categories at leading retailers reached 33% in 2024 and continues to rise as high-quality product imagery, virtual room visualizers, and frictionless returns overcome tactile barriers [2]Marks & Spencer Group, “Half Year Results for the 26 Weeks Ended 28 September 2024,” corporate.marksandspencer.com. Influencer-led product drops on Instagram and TikTok now account for a growing share of decorative-textile sales, encouraging agile collections and limited-run collaborations. Parcel-shop pickup and same-day click-and-collect options anchor omnichannel convenience, while last-mile carbon reporting appeals to sustainability-minded shoppers. Smaller direct-to-consumer labels leverage targeted ads and drop-shipping to enter the United Kingdom home textile market quickly, squeezing legacy chains that must reconcile store overheads with online price transparency.

Sustainability-Led Material Substitution Drives Innovation and Premium Positioning

Consumers scrutinize fiber provenance, water consumption, and end-of-life options, pushing retailers to stock GOTS-certified organic cotton, bamboo viscose, and mechanically processed hemp. Circular take-back schemes supported by national charity partnerships divert linen, towel, and curtain waste from landfill, accelerating recycling infrastructure adoption. James Cropper’s polycotton-separation breakthrough adds momentum by enabling fiber recovery from hospitality sheets [3]Packaging Europe, “James Cropper Reveals Process for Transforming Waste Polycotton into Paper,” packagingeurope.com. Retailers actively communicate material certifications and water-saving dye processes, allowing price premiums of 10%–15% above conventional lines while defending gross margins from raw-cotton volatility.

Hospitality Refurbishment Cycles Ahead of United Kingdom Tourism Push Generate Commercial Demand

Post-pandemic refurbishment budgets among hotels, restaurants, and holiday lettings drive a burst of bulk purchasing for flame-retardant drapery, high-thread-count sheeting, and antimicrobial toweling compliant with BS 5867 and BS 7176 fire-safety norms. Tourist-attracting regions in England and Scotland lead early-cycle upgrades as international arrivals rebound, while government grants for energy-efficient retrofits indirectly stimulate demand for insulating curtains. Contract buyers prefer suppliers that can guarantee color continuity across seasons and provide cradle-to-grave textile recycling certificates, allowing premium pricing for compliant manufacturers.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Cost-of-living squeeze on discretionary spend | -0.3% | Nationwide, low-income cohorts | Short term (≤ 2 years) |

| Volatile cotton & freight costs | -0.2% | Import-dependent supply chains | Medium term (2-4 years) |

| UK fire-safety compliance costs | -0.1% | Commercial segments | Long term (≥ 4 years) |

| Brexit-related customs friction | -0.1% | EU-sourcing retailers | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Cost-of-Living Squeeze Dampening Discretionary Spend Pressures Volume Growth

Persistent inflation and rising mortgage payments compel households to defer non-essential textile purchases. ONS expenditure tables highlight year-on-year declines in decorative cushion and throw sales, with shoppers concentrating activity around promotional events. Value retailers that offer smaller pack sizes and buy-now-pay-later options are absorbing share from mid-market brands. Consequently, revenue mixes tilt toward staple SKUs, forcing merchants to upgrade pricing analytics and markdown discipline to protect profit.

Volatile Cotton and Freight Costs Create Margin Pressure and Planning Challenges

Global cotton futures continue to swing on climate uncertainties and geopolitical tensions, complicating contract planning. Simultaneously, container spot rates remain 35% above 2019 benchmarks, with vessel bunching around major United Kingdom ports elevating demurrage risk. Large retailers mitigate exposure via blended yarn compositions, multi-origin sourcing, and derivative hedging, whereas smaller players struggle to pass surcharges to price-sensitive customers. The heightened cost base incentivizes shift toward higher-margin smart bedding and certified sustainable lines.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bed Linen Dominance Faces Smart Technology Disruption

Bed linen maintained 45.92% of the United Kingdom home textile market share in 2025, underpinned by non-negotiable hygiene replacement cycles. Yet the smart bedding subsegment is forecast to record an 8.48% CAGR, reflecting rising appetite for phase-change, moisture-wicking, and sensor-enabled sleep solutions. Overall, United Kingdom home textile market size gains in this category stem from professional couples and older adults seeking measurable health benefits, encouraging retailers to bundle pillows, protectors, and connected lighting for subscription deliveries. Bath linen registered steady replenishment demand bolstered by hotel renovations, while kitchen textile volumes benefited from sustained home-cooking habits established during pandemic lockdowns. Carpet and rug sales diverged: premium wool pieces advanced via artisan channels, whereas price-led synthetic rugs faced heavy discounting in warehouse clubs.

Rapid smart-bedding growth foreshadows the gradual erosion of the traditional bed-linen share. Product development pipelines increasingly feature convertible to designs and naturally derived antimicrobial finishes, driving average ticket values up. Suppliers with proprietary technology partnerships or R&D alliances capture first-mover advantage. Meanwhile, compliance with OEKO-TEX and United Kingdom fire-safety norms remains non-negotiable, preserving entry barriers for differentiated innovators.

By Material: Cotton Leadership Challenged by Sustainable Alternatives

Cotton contributed 65.79% of the United Kingdom home textile market share in 2025, benefiting from consumer familiarity, skin comfort, and product breadth. Nevertheless, bamboo–hemp blends are projected for a 9.64% CAGR, leveraging low water footprints and fast growth cycles to appeal to eco-conscious shoppers. Linen is also regaining favor among premium consumers seeking relaxed aesthetics and higher durability, while mechanically recycled polyester retains relevance for price-competitiveness and easy-care properties. Rising certification costs and erratic cotton pricing motivate retailers to diversify fiber portfolios; the resulting choice of architecture empowers shoppers to trade up for tangible sustainability credentials. Meryl Fabrics’ zero-microfiber-shedding nylon demonstrates how synthetic innovations can coexist with natural-fiber evolution .

Fiber substitution alone is not sufficient. Retailers increasingly pair classic cotton weaves with proprietary antimicrobial or thermo-adaptive coatings, creating premium offers without forcing radical consumer learning curves. Such hybrid propositions preserve cotton’s emotional resonance while unlocking incremental margin.

By End-User: Residential Dominance Masks Commercial Opportunity

Residential buyers accounted for 79.10% of United Kingdom home textile market size in 2025, driven by pandemic-induced nesting and ongoing hybrid work trends. Yet the commercial segment—especially hospitality—will expand at an 8.07% CAGR as hotels, care homes, and student residences refresh interiors. Contract buyers demand flame-retardant and industrial-laundry-compatible fabrics, enabling vendors to command higher price points. Spike-proof mattress protectors and stain-release draperies rank high on replacement lists, while subscription models for towel rentals gain popularity among boutique hotels seeking operational predictability.

Residential and commercial purchasing converges around performance expectations: antimicrobial proof points developed for healthcare continually migrate into consumer lines. Brands able to cross-pollinate innovations across segments optimize capacity utilization and widen earnings resilience.

By Distribution Channel: Online Surge Transforms Traditional Retail

Offline venues—department stores, specialty chains, supermarkets—held 62.70% share in 2025, yet web channels will post a robust 11.72% CAGR through 2031. Enhanced augmented-reality showroom apps allow shoppers to visualize curtains and bedding in actual room colors, mitigating tactile disadvantages. Major retailers tout 1-hour click-and-collect promises while integrating return drop boxes at transit hubs to streamline reverse logistics. Social-commerce “shop the look” posts translate inspiration into immediate checkout, favoring nimble in-stock operators.

Digital acceleration forces brick-and-mortar incumbents to rationalize square footage and convert under-performing aisles into micro-fulfillment nodes. Pure-play e-tailers simultaneously invest in show-and-ship pop-ups to provide limited tactile exposure where considered purchases require hand-feel confirmation.

Geography Analysis

England continues to set demand benchmarks thanks to 84.40% of the United Kingdom home textile market share in 2025, robust distribution infrastructure, and higher disposable incomes that support premium bedding adoption. High port capacity around Felixstowe and Southampton reduces landed costs for imported fibers, permitting rapid assortment rotation for trend-driven décor lines. Consumer appetite for functionally superior bedding—antimicrobial protection and climate regulation—remains strongest in London and South-East commuter belts, where time-poor professionals place a premium on sleep quality.

Northern Ireland’s 6.21% forecast CAGR through 2031 stems from affordable housing, renewed construction, and tariff-free exchange with Ireland under dual-market compliance allowances post-Brexit. Local retailers increasingly source Pakistan-origin linens via DCTS benefits, passing savings to consumers while maintaining margin. Extended mortgage terms in Belfast and Derry preserve renovation budgets earmarked for soft-furnishings upgrades.

Scotland and Wales exhibit moderate expansion, propelled by leisure-accommodation revamps in Edinburgh, Glasgow, Cardiff, and coastal holiday lets. Both regions display cultural affinity for wool throws and plaid motifs, sustaining demand for locally woven items and niche artisan fabrics. Rural logistics challenges prompt shoppers to favor omnichannel “order ahead, collect in town” models that cut delivery surcharges. Across all three non-English regions, community-led recycling initiatives backed by UKFT’s automated textile-sorting pilot enhance awareness of sustainable disposal avenues, indirectly nudging new purchases toward certified sustainable fibers.

Regulatory Landscape

United Kingdom home textile suppliers and retailers operate under product safety and labeling rules, alongside border and tariff requirements that changed after Brexit. Fire-safety compliance remains a key gatekeeper for commercial drapery and upholstery-related textile applications aligned to BS 5867 and BS 7176. The Furniture and Furnishings (Fire) (Safety) (Amendment) Regulations 2025 came into force on 30 October 2025, removing display label requirements and extending the time limit for enforcement legal proceedings from 6 to 12 months.

Policy direction is also shifting. A UK government consultation to reform the Furniture and Furnishings (Fire) (Safety) Regulations 1988 ran from 31 March 2026 to 23 June 2026, signaling movement toward more modern, risk-based approaches (including smoulder-focused testing) and reduced reliance on chemical flame retardants. On the trade side, use of preferential tariffs under the UK-EU Trade and Cooperation Agreement depends on documenting rules of origin, while duty treatment for imported home textile products continues to be determined by commodity codes in the UK Integrated Tariff Schedule and schemes such as the Developing Countries Trading Scheme (DCTS).

Value Chain Analysis

The United Kingdom home textile value chain runs from fiber and yarn inputs (cotton and alternative fibers) through fabric formation, dyeing and finishing (including antimicrobial and flame-retardant treatments where required), cut-and-sew manufacturing, and then to brand owners and retailers that handle design, merchandising, and compliance. Because the segment is import-heavy, inbound logistics and customs documentation are central steps, followed by warehousing, allocation, and distribution across offline and online channels, including department stores, specialist home retailers, supermarkets, and online marketplaces. Reverse logistics is increasingly embedded through returns handling and emerging take-back and recycling routes, especially for hospitality and contract linen flows.

Operational friction points highlighted by industry bodies and sector coverage include freight cost volatility, skills shortages across logistics and furnishings-related trades, and the need to manage compliance and labeling at the SKU level. Trade associations such as UKFT and BITA work alongside manufacturers and retailers as enabling nodes, providing guidance on technical compliance, sourcing, and supply chain management. UKFT also launched a quarterly roundtable series in October 2025 focused on product technical compliance and sourcing. Digital tools are becoming more visible in delivery and fulfillment operations, and industry reporting indicates a higher share of deliveries being digitally tracked by 2026, supporting tighter inventory control and improved customer experience for bulky home categories that often bundle textiles with furnishings.

Competitive Landscape

The United Kingdom home textile market is moderately fragmented. Dunelm, Marks & Spencer, and John Lewis safeguard share through vertically integrated design, private-label exclusives, and loyalty-scheme data analytics. Specialized digital-native challengers such as Soak & Sleep and Piglet in Bed win wallet share with transparent pricing and nano-batch color launches that excite social-media audiences. Meanwhile, incumbent supermarkets rationalize bulky furniture to refocus shelf space on fast-moving towels and sheets, as evidenced by Marks & Spencer’s exit from large-item categories in 2024.

Technology investment differentiates winners: antimicrobial license agreements with Toray Textiles Europe protect margin through patent exclusivity, and proprietary sleep-tracking integrations lock in ecosystem stickiness. Brands innovating in textile-to-textile recycling—leveraging James Cropper’s fiber-recovery know-how—bolster ESG credentials that resonate with millennials and institutional hotel buyers alike. Consolidation prospects remain high as mid-tier labels without omnichannel capabilities struggle to finance compliance upgrades and marketing.

Retailers also court commercial clients. Contract-grade lines engineered for 200-wash durability and 350-thread-count comfort secure lucrative repeat orders from chain hotels and care homes. The B2B focus tempers consumer-cycle volatility and provides testbeds for performance technologies destined for residential upsell.

United Kingdom Home Textile Industry Leaders

Dunelm Group plc

IKEA (UK)

NEXT plc

John Lewis & Partners

Amazon (Home & Kitchen UK)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Regulatory change is creating room for compliant product redesign and premiumization, especially where performance textiles intersect with safety and sustainability. The UK government consultation that closed on 23 June 2026 on reforming the Furniture and Furnishings (Fire) (Safety) Regulations 1988 points to updated test regimes and reduced dependence on chemical flame retardants. That shift supports opportunities for suppliers that can deliver compliant flame performance through fiber blends, barrier technologies, and finishing innovation, while retaining comfort and aesthetics for hospitality-grade curtains, bedding, and protective covers.

Circularity infrastructure and traceable environmental data are also becoming more actionable levers for differentiation across residential and contract channels. Government and industry initiatives referenced in the market context, including the UK Circular Economy Strategy focus on textiles and the National Textile Recycling Infrastructure Plan (2025-2035), reinforce demand for take-back partnerships, fiber-to-fiber recycling solutions (including handling of polycotton blends), and verifiable chain-of-custody. Retailers that are already emphasizing circular-economy initiatives and technology-led product propositions, such as smart and antimicrobial bedding, have a pathway to combine higher-value assortments with service add-ons. These include refresh subscriptions, recycling certificates for hospitality buyers, and lower-friction omnichannel returns and collection models that reduce the total cost to serve.

Recent Industry Developments

- June 2026: Dunelm opened a new 34,000 square foot superstore as part of its ongoing physical expansion program. The larger-format footprint supports broader home assortments, where bed and bath textiles benefit from adjacency merchandising and higher basket sizes. Continued store rollout also strengthens last-mile capability when stores are used as convenient collection and returns points.

- June 2026: NEXT extended its licensing agreement with the furniture and interiors brand Nina Campbell, with filings also outlining a potential ownership path. The move supports faster product refresh cycles in home categories, including soft furnishings and decorative textiles that trade on brand equity. Licensing-led portfolio expansion adds competitive pressure on incumbents that rely on private label alone for design differentiation.

- November 2024: Dunelm completed the acquisition of a 100% shareholding in the Home Focus Group in Ireland (Home Focus at Hickey's). The transaction broadened Dunelm's regional footprint and created additional sourcing and distribution leverage for homewares, including core textile lines. It also increased scale advantages in procurement and inventory planning amid freight and raw material volatility.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this methodology, the market counts the value of home textile products sold in the United Kingdom for household and light commercial use, where the main use is inside the home, such as bedding, bath, kitchen, upholstery fabrics, and floor covering textiles.

Scope exclusions: We exclude hard home decor items and furniture. We also avoid double counting installation or non-textile flooring services.

Segmentation Overview

- By Application

- Bed Linen

- Bath Linen

- Kitchen Linen

- Upholstery

- Others (Carpets and Area Rugs)

- By Material

- Cotton

- Linen

- Synthetic Fibers

- Other Materials (Wool, Hemp, Silk, Jute, Bamboo etc.)

- By End-User

- Residential

- Commercial

- By Distribution Channel

- Offline

- Online

- By Geography

- England

- Scotland

- Wales

- Northern Ireland

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary and build a reliable demand context for the United Kingdom. We reviewed public statistics and market signals such as the UK Office for National Statistics for household spending and retail trends, HM Revenue and Customs trade data for textile imports and exports, and Eurostat for supporting textile and apparel indicators.

To anchor category behavior, we also referred to sources such as UK Fashion and Textile Association publications and British Retail Consortium updates, plus peer reviewed studies that discuss textile consumption patterns and fiber shifts. Company annual reports, investor presentations, and retailer updates helped validate channel mix and pricing direction. A paid subscription for company financials and a shipment-level import export database were then used selectively when public reporting was not detailed enough. The sources listed here are illustrative, and additional public and paid references were used for cross-checks and clarification during the study.

Primary Interviews and Surveys

Primary work focused on interviews and structured surveys with manufacturers, brand owners, distributors, and retail channel stakeholders, and it was balanced with views from procurement and category managers who track demand changes closely. Since this is a UK market, we ensured coverage across England, Scotland, Wales, and Northern Ireland to confirm product mix differences and channel intensity, and then used the inputs to validate assumptions that were unclear from public data.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 25% | CXOs: 12% | |

| Mid tier: 55% | Functional/Unit leaders: 31% | |

| Smaller Players: 20% | Managers: 57% |

Market-Sizing & Forecasting

Sizing starts with a top-down build that reconstructs United Kingdom demand from household goods spending and home-related retail baselines. We then split that demand into home textile uses using category shares supported by trade and retail signals. The model is subsequently checked with selective bottom-up approximations, where sampled price points are multiplied by estimated volumes, and where supplier and channel checks help adjust totals when the first pass looks stretched.

A few practical inputs that guide the math include: home textile category mix across bedding, bath, kitchen, upholstery, and floor covering textiles, online versus store-based share shifts, import intensity for key textile categories, fiber mix movement between cotton and synthetics, and price progression observed in retailer ranges. Where gaps appear, they are handled using conservative proxy ratios, for example using similar textile subcategories with clearer reporting. These assumptions are then re-tested during interviews so we do not carry forward a weak premise.

For forecasting, we lean on scenario analysis supported by simple time-series smoothing on the most stable inputs, such as category-level retail direction and import value trends. We then apply expert-agreed ranges for pricing and mix changes. When the numbers were expected to diverge, the final trajectory was kept within what channel participants described as realistic for replenishment-driven categories.

Data Validation & Update Cycle

Validation is done through multiple checks that compare outputs against independent signals, including retail direction, trade values, and reasonable price bands by product type. Outliers are reviewed, assumptions are revisited, and follow-up calls are triggered when a major variance cannot be explained by seasonality, channel shifts, or mix change.

Before sign-off, the model goes through a multi-step internal review so that calculation logic, unit consistency, and year-on-year movement are aligned across the workbook. Reports are refreshed annually, and interim updates are made when material events occur, such as sudden price inflation, trade disruptions, or demand softness that changes category behavior. Right before delivery, a fresh analyst pass is completed so the client receives the latest updated view.

Mordor Intelligence's United Kingdom Home Textile Market Size Measured Against Other Published Estimates

Published market sizes can look different even when they use the same market name, because the counted products, the included end uses, and how pricing is handled are often not aligned. Differences also come from the year chosen as the base, the treatment of imports versus domestic supply, and how online retail is measured versus broader household goods spending.

By tracking import value direction, category-level retail movement, and refresh cadence within the model, Mordor Intelligence keeps the United Kingdom home textile total tied to sell-through realities across bedding, bath, kitchen, upholstery fabrics, and floor covering textiles, rather than blending in adjacent homeware lines. In addition, some publishers use manufacturing revenue or assume a more aggressive price growth path, which can shift the total away from a consumer-market value view.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 7.62 B (2025) | |

| Trade Data Digest A | USD 4.03 B (2023) | This estimate appears to anchor the market closer to a narrower definition and an earlier base year. It may undercount domestic sell-through by leaning heavily on limited category coverage and slower channel re-basing for online. |

| Industry Outlook Desk B | USD 8.51 B (2025) | The higher number is consistent with broader inclusion rules, where adjacent home bedding or soft furnishings can be folded in. It also appears to apply price escalation more aggressively without enough channel-level checks. |

Taken together, the spread is mainly explained by what gets included as home textiles, and by how pricing and channels are updated year to year. Our approach keeps the total traceable to clear demand indicators and repeatable steps, which makes it easier for buyers to map market value back to real category movement.

Key Questions Answered in the Report

How large is the United Kingdom home textile market in 2026?

The United Kingdom home textile market size is USD 7.75 billion in 2026 and is expected to reach USD 8.46 billion by 2031 at a 1.76% CAGR.

Which application leads demand for household textiles?

Bed linen remains the leading application with 45.92% United Kingdom home textile market share in 2025, though smart bedding is the fastest-growing niche at an 8.48% CAGR.

What fiber types are gaining popularity beyond cotton?

Bamboo and hemp blends are expanding at a 9.64% CAGR as eco-conscious consumers seek lower-impact alternatives, while linen is enjoying a premium resurgence.

How quickly are online channels expanding?

Online sales are projected to grow at a 11.72% CAGR through 2031, steadily eroding offline dominance as virtual visualization tools improve confidence in remote purchasing.

Which United Kingdom region offers the highest growth potential?

Northern Ireland is forecast to grow at 6.21% CAGR to 2031, benefiting from housing-market momentum and cross-border trade with Ireland.

What key challenge restrains retailer margins?

Volatile cotton and freight costs compress margins, compelling retailers to diversify sourcing and invest in higher-value smart or sustainable product lines.

Page last updated on: