United Kingdom Chemical Logistics Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

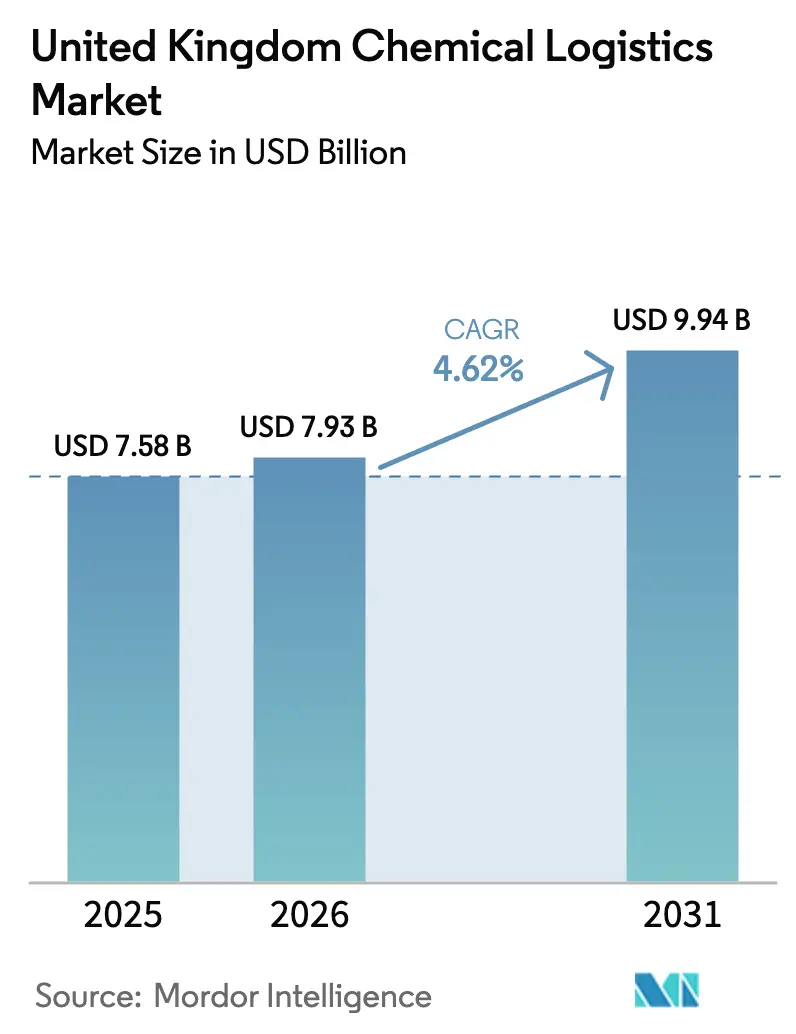

| Base Year Market Size (2025) | USD 7.58 Billion |

| Market Size (2026) | USD 7.93 Billion |

| Market Size (2031) | USD 9.94 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

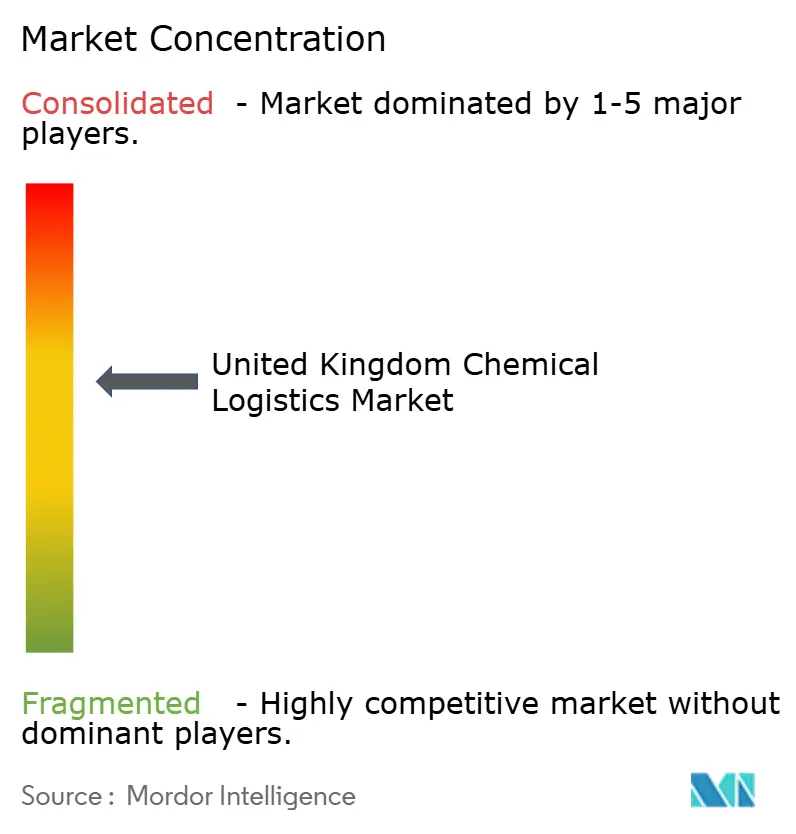

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Chemical Logistics Market Analysis by Mordor Intelligence

The United Kingdom Chemical Logistics Market size was valued at USD 7.58 billion in 2025 and estimated to grow from USD 7.93 billion in 2026 to reach USD 9.94 billion by 2031, at a CAGR of 4.62% during the forecast period (2026-2031). The sector’s sturdy growth reflects a structural shift toward higher-value, specialist services that keep supply chains compliant, decarbonized, and temperature-stable. Rising demand for multimodal corridors serving the Teesside cluster, new hydrogen production projects, and post-Brexit regulatory divergence are all expanding the addressable base of premium logistics contracts. Capacity constraints at key Petrochemical ports, together with a critical shortage of ADR-qualified drivers, are prompting rapid investment in digital scheduling, real-time ADR platforms, and ISO tank fleets. Temperature-controlled transport, particularly for pharmaceutical input, remains the fastest-growing niche, posting an 8.7% CAGR to 2030.

Key Report Takeaways

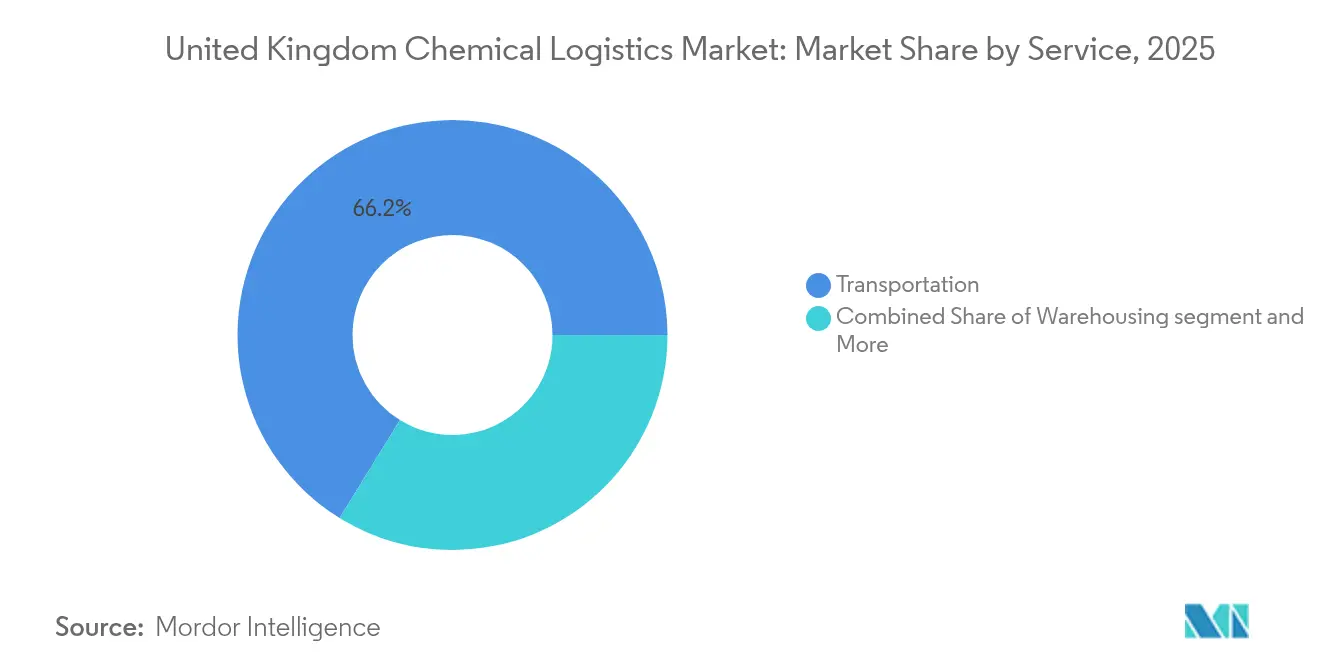

- By service, transportation commanded 66.20% revenue share of the United Kingdom chemical logistics market in 2025, while warehousing and distribution is forecast to grow at a 5.34% CAGR through 2031.

- By end-user industry, oil & gas held 30.40% share in 2025; pharmaceuticals are projected to expand at a 6.68% CAGR through 2031.

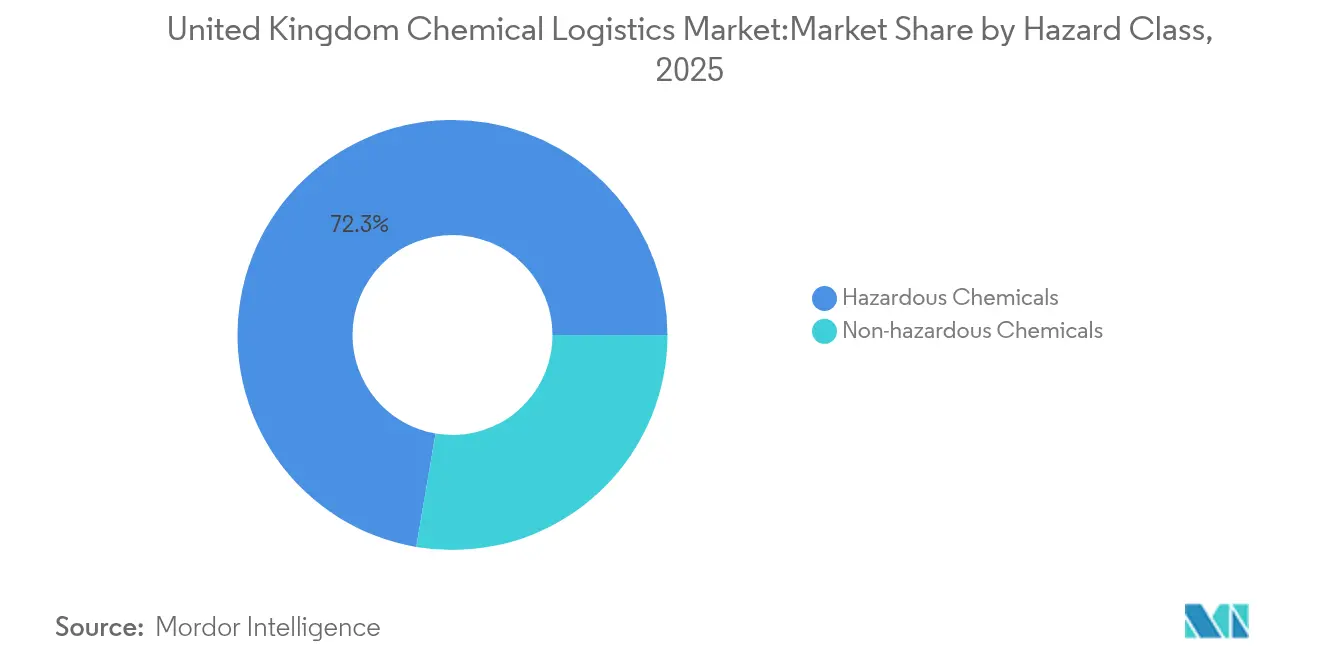

- By hazard class, hazardous chemicals accounted for 72.30% of the United Kingdom chemical logistics market share in 2025; the non-hazardous segment is on track for 7.21% CAGR through 2031.

- By temperature control, non-temperature-controlled logistics made up 60.40% of the United Kingdom chemical logistics market size in 2025, whereas temperature-controlled services are rising at an 8.32% CAGR through 2031.

- By geography, England led with 85.70% of the United Kingdom chemical logistics market in 2025; Scotland is the fastest-growing region, advancing at a 5.82% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Chemical Logistics Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| UK-centric Chemical Cluster Expansion in Teesside | +0.8% | England (Teesside), with spillover to Scotland | Medium term (2-4 years) |

| On-site Storage Capacity Constraints at Petro-Chem Ports | +0.7% | England (Southeast ports), Scotland (Aberdeen) | Short term (≤ 2 years) |

| Digital ADR Compliance Platforms Accelerating Turn-around | +0.6% | National | Medium term (2-4 years) |

| Growing Hydrogen Economy Demand for ISO-Tank Transport | +0.5% | Scotland, England (Teesside) | Long term (≥ 4 years) |

| Sharp Rise in Contract Packaging for Agri-chem Exports | +0.4% | England (East), Scotland | Medium term (2-4 years) |

| Post-Brexit Divergent REACH Rules Creating Logistics Demand | +0.3% | National | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

UK-centric Chemical Cluster Expansion in Teesside

Teesside’s Net Zero Teesside and H2Teesside projects are consolidating chemical production and carbon capture infrastructure, creating specialized transport corridors for CO₂ and hydrogen. BP’s commitment to capture up to 4 million tons of CO₂ annually is stimulating new ISO-tank demand for liquefied CO₂ and blue hydrogen feedstocks. Integration with the East Coast Cluster is shifting traditional point-to-point trucking into circular flows that blend pipeline, rail, and road legs. Logistics providers are therefore investing in modular ISO-tank farms capable of switching between liquid CO₂, ammonia, and hydrogen. Coupled with Teesside’s direct deep-sea access, these capabilities position the region as a launchpad for low-carbon chemical exports. The ripple effect extends northwards as Scottish terminals re-gear to back-haul hydrogen and captured CO₂, reinforcing the United Kingdom chemical logistics market’s resilience.

On-site Storage Capacity Constraints at Petro-Chem Ports

Major terminals such as Immingham are running at 85-90% utilization, materially above the 70-75% efficiency benchmark. Dwell-time inflation has reached 15% since 2023, forcing shippers to split loads and accept 12-18% higher unit transport costs. COMAH zoning and planning rules restrict fast expansion, so operators are pivoting to hub-and-spoke designs backed by GBP 78 million (USD 99.29 million) of new intermediate storage in 2024 [1]Offshore Energies UK, “Supply Chain Roadmap 2025,” oeuk.org.uk. IoT-enabled inventory platforms have cut buffer stock needs by up to 12%, easing but not eliminating the bottleneck. Together, these factors keep warehousing services on a robust growth curve within the United Kingdom chemical logistics market.

Digital ADR Compliance Platforms Accelerating Turn-around

From January 2025, the ADR 2025 code will tighten training and classification rules, particularly for Class 8 and Class 6.1 cargo. Web-based compliance engines now autofill documents, push real-time regulatory updates, and link to truck telematics, reducing terminal turnaround by hours per load. Early adopters report 5-8% higher fleet utilization and markedly lower paperwork error rates. Data-rich journey profiles also unlock route optimization and emissions analytics, which help shippers meet Scope 3 reporting duties. These efficiency gains underpin the 0.6% positive contribution to forecast CAGR for the United Kingdom chemical logistics market.

Growing Hydrogen-Economy Demand for ISO-Tank Transport

Government ambitions for 10 GW domestic hydrogen capacity by 2030, and feasibility work on a low-carbon Iceland-Teesside corridor, are triggering orders for cryogenic ISO-tanks and new loading gantries. Hydrogen’s unique diffusion risk profile raises the bar for valve design, purging, and leak detection, so carriers are integrating fiber-optic sensors and predictive maintenance analytics. Logistics firms able to certify that equipment under ADR Chapter 3.3 Special Provision 653 can handle both cold-compressed and liquid hydrogen stand to gain long-term contracts. The build-up complements renewable exports from Scotland, reinforcing geographic diversification inside the United Kingdom chemical logistics market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited Rail-tanker Slots at Key Terminals | -0.5% | England (Industrial Corridors), Scotland | Medium term (2-4 years) |

| Driver Shortage for ADR Class 8 & 6.1 | -0.4% | National | Short term (≤ 2 years) |

| Strict CO₂-Based Road Tolls on M25 Corridor | -0.3% | England (Southeast) | Medium term (2-4 years) |

| Community Opposition to Bulk Chemical Warehousing | -0.2% | England (Urban/Suburban Areas) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Limited Rail-tanker Slots at Key Terminals

Shared lines with passenger traffic and decades-old loading racks mean chemical trains frequently miss optimal departure windows. The resulting backlogs push shippers toward more road legs, elevating costs and carbon footprints. Digital allocation tools that pool slot requests across multiple operators have raised rail utilization modestly, yet a structural gap remains until new sidings are built. Forward-looking providers mix rail for trunk haul with road final mile to trim emissions while keeping schedules credible. Despite mitigation, the constraint clips 0.5 percentage points from the United Kingdom chemical logistics market’s potential CAGR.

Driver Shortage for ADR Class 8 & 6.1

A 24% deficit of qualified drivers lengthens booking lead times by 3.5 days on average. An ageing talent pool puts succession risk front and center, as 42% of license holders are over 50. In-house academies and simulator-based programs have trimmed certification cycles by 30%, but wage premiums of 18% erode carrier margins. Firms reporting the best retention blend pay increments with clear progression into fleet safety or training roles. Even so, the shortage subtracts 0.4 points from baseline growth in the United Kingdom chemical logistics market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Service: Multimodal Integration Reshapes Transport Dominance

Transportation accounted for 66.20% of the United Kingdom chemical logistics market in 2025, a position underpinned by road haulage, which moves more than 70% of volumes. Warehousing, distribution and inventory management is the fastest-rising category, expanding at a 5.34% CAGR and steadily lifting its portion of the United Kingdom chemical logistics market size. Digitally orchestrated cross-docking, temperature-segmented bays and COMAH-compliant inert-gas storage convert warehouses into margin-rich service hubs.

Integrated service contracts are therefore blurring the lines between trucking and storage. Operators such as Bertschi run inland depots that splice rail spurs into tank-container yards, pairing line-haul decarbonization with just-in-time inventory. The model cuts handling steps and embeds value-added services like blending. As a result, transport’s share will moderate despite absolute growth, while warehousing and “other services” such as customs and regulatory consulting capture more revenue inside the United Kingdom chemical logistics market.

By End-user Industry: Pharmaceutical Segment Outpaces Traditional Leaders

Oil & gas retained a 30.40% share of the United Kingdom chemical logistics market in 2025, but the segment’s outlook is tempered by energy-transition dynamics and refiners’ efficiency drives. Pharmaceuticals, in contrast, are set to rise at a 6.68% CAGR thanks to persistently high R&D spend and stringent temperature specs for active ingredients. Temperature-validated packaging across ambient, refrigerated, frozen, and Cryo bands is now standard for the pharma supply chain.

Second-tier industries such as cosmetics and specialty chemicals lean heavily on flexible, smaller-lot deliveries aligned to rapid formulation changeovers. Logistics providers differentiate on GMP compliance and batch-traceability rather than pure hazard handling. Together, these shifts nudge the United Kingdom chemical logistics market toward nimbler, quality-assured services. Oil & gas players are responding by repurposing ADR tank farms for alternative fuels and carbon-capture intermediates, sustaining asset utilization while the fossil share of throughput declines.

By Hazard Class: Non-hazardous Growth Outpaces Traditional Segment

Hazardous cargo represented 72.30% of 2025 throughput, mirroring the United Kingdom chemical logistics market’s heritage in petrochemicals and corrosives. Non-hazardous materials, however, are forecast to expand 7.21% annually as specialty pharma, food additives, and cosmetic actives multiply. The United Kingdom chemical logistics market size linked to Class 8 and Class 6.1 shipments will keep growing, yet its proportional weight will ease.

ADR 2025 revises definitions, escalating documentation loads, and training intensity. Providers with digital rulesets embedded in booking portals and cab tablets win share by slashing error risk. In parallel, non-hazardous consignments benefit from route simplification and milder packaging, lifting margins slightly. The danger-goods sub-segment has responded with smarter composite IBCs and predictive-maintenance valve kits aimed at closing cost-gaps and improving safety.

By Temperature Control: Pharmaceutical Demand Drives Refrigerated Growth

Non-temperature-controlled services held a 60.40% share in 2025, but refrigerated and frozen lanes are rising at an 8.32% CAGR, supported by the expanding pharma pipeline . Validated 2-8 °C and controlled-room-temperature packaging now features single-use data loggers and real-time GPS. The United Kingdom chemical logistics market share attached to refrigerated moves is therefore widening, especially around the “golden triangle” connecting the Oxford-Cambridge-London R&D hubs.

Process-plant learnings are filtering into distribution: HRS Heat Exchangers’ active heating/cooling skid that cuts capsule production cooling from hours to under 60 minutes for Mayne Pharma is inspiring mobile tote-cooling units. Green initiatives, including reusable phase-change containers and solar-powered reefer units, align decarbonization goals with compliance. Over time, temperature-controlled service upgrades may compress spoilage risk and enhance brand value across life-science supply chains.

Geography Analysis

England captured 85.70% of the United Kingdom's chemical logistics market in 2025, anchored by mature clusters in the Northeast, Northwest, and Southeast. Teesside’s net-zero projects are intensifying north-south flows of CO₂, ammonia, and blue hydrogen, while London’s Ultra Low Emission Zone expansion compels carriers to adopt low-emission trucks . Eastern ports handle rising Agri-chemical volumes linked to a regional economy expected to reach GBP 220 billion (USD 280.06 million) by 2035. Persistent rail-tanker congestion and community pushback on tank farms, however, require tactical warehousing and resilient multimodal routing.

Scotland is the fastest-growing geography at 5.82% CAGR as offshore energy firms pivot towards hydrogen, CCS, and floating wind. Logistics synergies are compelling: 60-80% of oil-and-gas supply-chain skills transfer directly to low-carbon chemical handling. Court rulings on field licenses underscore growing regulatory oversight, yet public funding and cluster decarbonization initiatives offset policy risk. New ISO-tank yards around Aberdeen and Grangemouth are capturing repeated shuttle moves for hydrogen derivatives.

Wales and Northern Ireland together represent a modest share but hold strategic corridor roles. Northern Ireland’s dual-market status under the Windsor Framework requires agile document handling to reconcile UK and EU REACH filings. Wales benefits from deep-sea access and looser planning rules that expedite storage hub approvals. Both regions receive targeted digital-infrastructure grants aimed at lifting end-to-end shipment visibility, cementing their relevance inside an increasingly connected United Kingdom chemical logistics market.

Competitive Landscape

The United Kingdom chemical logistics market shows moderate concentration. Suttons Group, Hoyer Group, and Den Hartogh collectively control a sizeable fleet of stainless-steel road tankers, ISO-tanks, and COMAH-graded depots, enabling end-to-end solutions for hazardous cargo. Suttons’ 2024 purchase of DHL’s UK bulk commodity chemical business expanded its tanker count and deepened its footprint near refineries. Incumbents differentiate via asset breadth, ADR driver pools, and proprietary compliance software that lowers risk for blue-chip shippers.

Meanwhile, temperature-controlled specialists target high-margin pharma flows by offering GDP-certified 2-8 °C services and cryogenic dry-ice replenishment. Digital start-ups leverage cloud booking engines to pool back-hauls, squeezing empty mileage and reducing emission intensity. The global ISO-tank fleet surpassed 882,000 units in January 2025, underscoring equipment scalability that benefits UK import-export circuits.

White-space opportunities include dedicated hydrogen transport and storage, where asset standards are still forming, and integrated customs-plus-storage packages that navigate divergent UK-EU REACH requirements. Competitive intensity is expected to tighten as generalist 3PLs penetrate specialty chemical niches, while established players invest in smart tank telemetry and predictive maintenance to defend margins within the United Kingdom chemical logistics market.

________________________________________

United Kingdom Chemical Logistics Industry Leaders

DHL

Suttons Group

Hoyer Group

Den Hartogh Logistics

Dachser

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Synthomer divests William Blythe Limited for GBP 30 million, sharpening focus on specialty polymers.

- April 2025: DSV completes the EUR 14.3 billion acquisition of DB Schenker, doubling revenue and scaling to 160,000 staff.

- January 2025: Aegis Energy secures GBP 100 million to build five multi-energy refueling hubs for HGV fleets, supporting low-carbon chemical distribution.

- April 2024: GXO Logistics finalizes the buy-out of Wincanton for USD 7.58 per share, adding aerospace and healthcare vertical depth.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the United Kingdom chemical logistics market as every paid movement, storage, and handling activity that moves bulk or packaged chemicals from domestic production and import hubs to end-use points across Great Britain and Northern Ireland. This includes temperature-controlled and hazardous consignments, multimodal transfers, and in-process dwell time that attracts a logistics fee.

Scope exclusion: stand-alone export packaging services performed inside manufacturing plants fall outside our estimate.

Segmentation Overview

- By Service

- Transportation

- Road

- Rail

- Sea/Ocean

- Air

- Warehousing, Distribution & Inventory Management

- Other Services

- Transportation

- By End-user Industry

- Pharmaceuticals

- Cosmetics & Personal Care

- Oil & Gas

- Specialty Chemicals

- Other End-users

- By Hazard Class

- Hazardous Chemicals

- Non-hazardous Chemicals

- By Temperature Control

- Temperature-Controlled (Refrigerated/Heated)

- Non-Temperature-Controlled

- By Geography

- England

- Scotland

- Wales

- Northern Ireland

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed ADR-qualified fleet managers, bulk-tank farm operators, and procurement heads at coatings, pharma, and petro-chem majors across England, Scotland, and Wales. The dialogues clarified mode preferences, average storage dwell, emerging hydrogen-carrier flows, and verified pricing bands that underlay our model.

Desk Research

We started with customs flow tables from HMRC, domestic production data from the Chemical Industries Association, and quarterly tonnage by hazard class published under ADR returns, which together framed the physical pool of product requiring logistics attention. Public filings from leading 3PLs, Port of Liverpool throughput reports, and BEIS fuel-price trackers then helped us pin typical service splits and rate shifts. Paid resources such as D&B Hoovers for company revenues and Dow Jones Factiva for transaction news sharpened volume-to-value bridges. These references are illustrative, not exhaustive; many additional trade journals, regulatory notices, and academic papers informed our desk work.

Market-Sizing & Forecasting

A top-down reconstruction began with 2024 tonnage of chemicals moved domestically, adjusted for average haul length and modal share, then multiplied by blended cost-per-kilometer and warehousing tariffs. Results were cross-checked through selective bottom-up roll-ups of sampled carriers' fleet counts and typical utilization, ensuring no single approach skewed totals. Key variables tracked include seaborne import tonnage, driver ADR license renewals, average diesel surcharge, chemical production index, and Teesside cluster capacity additions. Forecasts to 2030 rely on a multivariate regression that links demand to UK manufacturing GVA, energy input prices, and pipeline project completions, with scenario stress tests supplied by our interview panel. Gaps in bottom-up detail, such as private contractual rates, are bridged by conservative midpoint assumptions vetted in the analyst round-table.

Data Validation & Update Cycle

Modeled outputs pass three tiers of review: automated outlier flags, peer review within the logistics desk, and final sign-off by the transport practice lead. We refresh every twelve months and reopen the file sooner if fuel taxes, COMAH thresholds, or major M&A events materially shift cost structures.

Why Mordor's United Kingdom Chemical Logistics Baseline inspires confidence

Published values often diverge because firms slice the market differently, convert currencies on varying dates, and refresh models at uneven cadences.

Key gap drivers in this space include whether in-plant shuttling is counted, how empty-run factors are treated, and the aggressiveness of post-Brexit trade rebound assumptions; Mordor's choices sit at the mid-point of plausible ranges and are revisited annually.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 7.58 B (2025) | Mordor Intelligence | - |

| USD 4.99 B (2024) | Regional Consultancy A | Excludes rail legs and inland storage; model last updated pre-driver-shortage surge |

| USD 8.21 B (2033) | Global Consultancy B | Bundles freeport duty-suspension warehousing and uses optimistic macro growth path |

In sum, our disciplined scope boundaries, variable selection, and yearly refresh give decision-makers a transparent, repeatable baseline that neither undercounts critical cost centers nor overstates speculative upside.

Key Questions Answered in the Report

What is the current value of the United Kingdom chemical logistics market?

It stands at USD 7.93 billion in 2026 and is forecast to reach USD 9.94 billion by 2031.

Which service segment holds the largest share?

Transportation leads with 66.20% of revenue in 2025, supported by extensive road-tanker fleets.

Why is Scotland the fastest-growing region?

Large-scale hydrogen and carbon-capture investments are boosting specialist logistics demand, driving a 5.82% CAGR through 2031.

How are ADR 2025 regulations affecting logistics?

New digital compliance platforms slash paperwork errors and accelerate turnaround, improving fleet utilization by up to 8%.

What is the main challenge facing UK chemical logistics operators?

A 24% shortage of ADR-certified drivers is lengthening booking lead times and pressuring operating costs.

Where are the biggest growth opportunities?

Temperature-controlled pharmaceutical flows and emerging hydrogen transport corridors offer the highest growth and margin potential.

Page last updated on: