Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 9.49 Billion |

| Market Size (2026) | USD 9.93 Billion |

| Market Size (2031) | USD 12.45 Billion |

| Growth Rate (2026 - 2031) | 4.62% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Kazakhstan Oil And Gas Market Analysis by Mordor Intelligence

Kazakhstan Oil And Gas market size in 2026 is estimated at USD 9.93 billion, growing from 2025 value of USD 9.49 billion with 2031 projections showing USD 12.45 billion, growing at 4.62% CAGR over 2026-2031.

This steady expansion reflects Kazakhstan’s role as Central Asia’s leading hydrocarbon producer, its substantial proven reserves, and ongoing foreign investment in major field developments. Diversified export pipelines, government-backed capacity-expansion programs, and the deployment of digital oilfield and enhanced recovery technologies sustain growth even as OPEC+ quotas and European Union carbon regulations evolve. Upstream operations remain the largest revenue generator, while midstream infrastructure upgrades post the fastest growth. Offshore Caspian Sea projects and large-scale construction contracts drive service demand, reinforcing the country’s transition from a pure upstream player to an integrated energy hub.

Key Report Takeaways

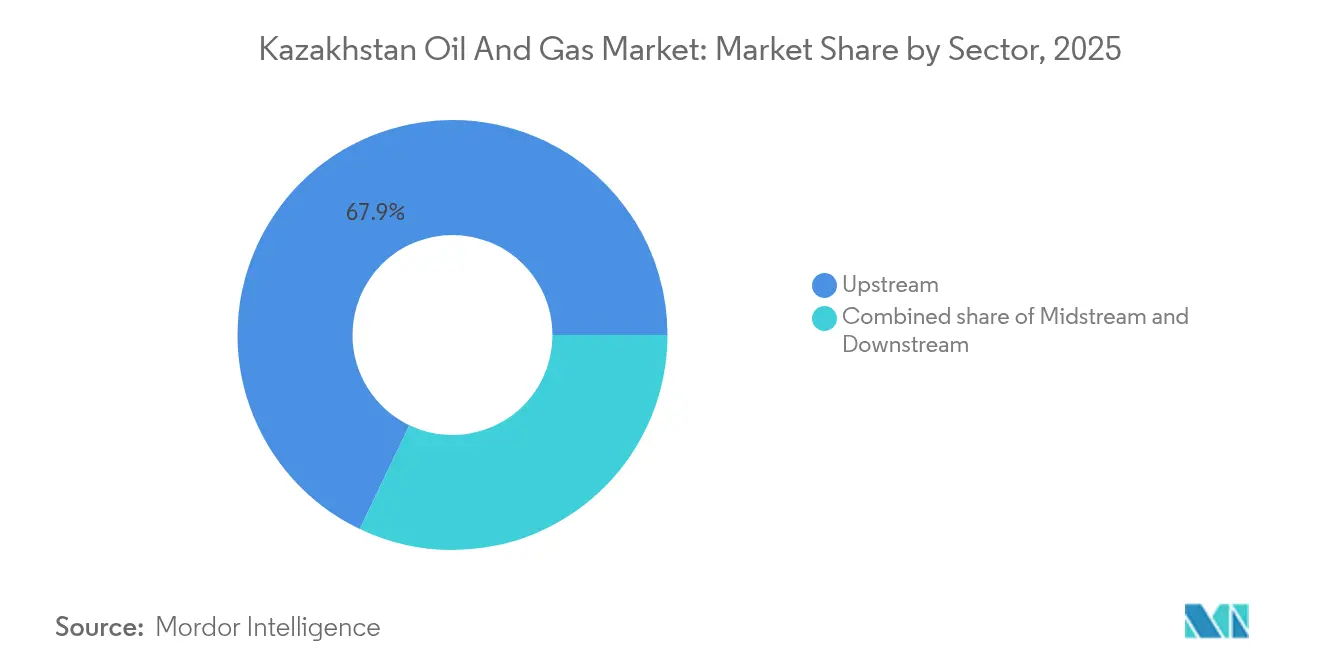

- By sector, upstream held 67.90% of the Kazakhstan oil and gas market share in 2025, whereas midstream is forecast to expand at an 7.74% CAGR through 2031.

- By location, offshore projects accounted for 84.25% of Kazakhstan's oil and gas market size in 2025 and are expected to lead with a 5.63% CAGR through 2031.

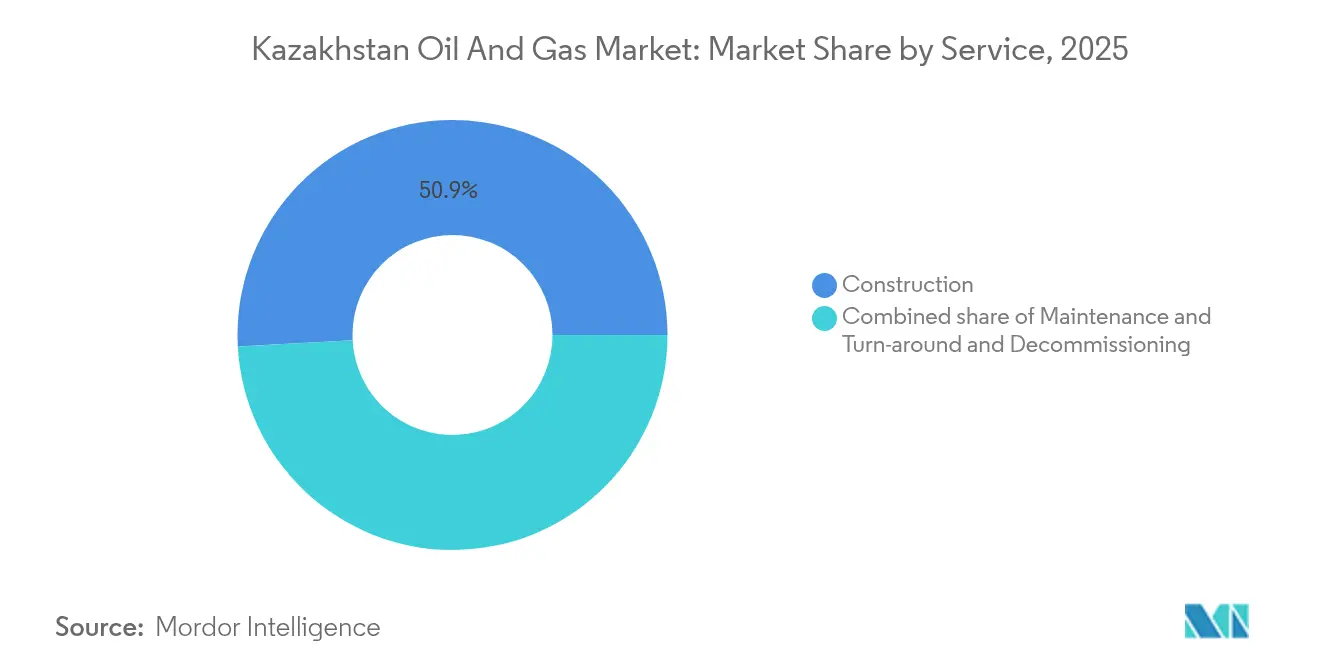

- By service, construction accounted for 50.85% of Kazakhstan's oil and gas market size in 2025 and is projected to grow at a 5.78% CAGR over the same period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Kazakhstan Oil And Gas Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Abundant proven oil & gas reserves | +1.2% | Atyrau and Mangystau regions | Long term (≥ 4 years) |

| Foreign investment in mega-fields | +0.8% | Caspian Sea offshore, Atyrau | Medium term (2-4 years) |

| Government plan to triple refining capacity | +0.7% | Nationwide, focus on Atyrau and Shymkent refineries | Long term (≥ 4 years) |

| Export-route diversification | +0.6% | Trans-Caspian corridors toward European markets | Medium term (2-4 years) |

| Digital oilfield & EOR deployment | +0.5% | Mature onshore fields in Mangystau | Short term (≤ 2 years) |

| Rising EU demand for CPC blend | +0.4% | Export flows to European Union | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Abundant Proven Oil & Gas Reserves

Kazakhstan holds more than 30 billion barrels of proven oil reserves, concentrated in the Caspian Basin, which provides the country with long-term supply security and leverage in export negotiations.[1]Kazakhstan Ministry of Energy, “Annual Energy Statistical Review 2024,” energy.gov.kz Kashagan alone contains close to 13 billion barrels of recoverable oil, keeping the resource base competitive with other global offshore plays. Ongoing government-led seismic surveys continue to identify new structural opportunities, while updated licensing terms under the Ministry of Energy encourage staged development that aligns production profiles with infrastructure capacity. Enhanced oil recovery trials in mature Mangystau fields are already boosting output and extending field life, underscoring the commercial attractiveness of the reserves. The scale of these resources enables Kazakhstan to secure multi-decade supply contracts with refiners across Europe and Asia, thereby reinforcing Kazakhstan's oil and gas market as a reliable growth platform.

Foreign Investment in Mega-Fields (Tengiz, Kashagan)

International operators are anchoring the Kazakhstan oil and gas market through multi-billion-dollar commitments that involve adding new production trains and introducing cutting-edge sour-gas handling technology. Chevron’s USD 45 billion Future Growth Project at Tengiz is slated to add 260,000 barrels per day of new capacity by 2025, integrating sulfur recovery units that lower carbon intensity.[2]Chevron Corporation, “Future Growth Project Fact Sheet,” chevron.com ExxonMobil maintains capital programs in Kashagan despite high-pressure, high-sulfur challenges, reflecting confidence in offshore economics. Joint-venture structures with KazMunayGas facilitate technology transfer and local workforce development, while preserving state control over resources. These projects stimulate demand for fabrication yards, pipeline extensions, and power generation upgrades, resulting in spillover benefits across the broader Kazakhstan oil and gas market.

Government Push to Triple Refining & Petrochemicals Capacity

Kazakhstan's downstream strategy aims to transform the country from a crude exporter into a diversified producer of refined fuels and petrochemical feedstocks. The Ministry of Energy aims to triple refining throughput by 2030, supported by over USD 10 billion in plant upgrades and greenfield complexes. The Atyrau refinery's modernization has already installed hydrocracking and catalytic reforming units, which raise gasoline quality and reduce sulfur emissions. Partnerships, such as the 2024 cooperation agreement between MOL Group and KazMunayGas, emphasize technology sharing to achieve polymer-grade ethylene and propylene output. As these projects ramp up, Kazakhstan secures higher-margin export opportunities and reduces its reliance on imported gasoline and petrochemicals, thereby elevating the resilience of the Kazakhstan oil and gas market to crude-price swings.

Diversification of Export Routes (Middle Corridor, BTC)

Alternative transit corridors lessen geopolitical and operational risk for Kazakhstani producers. The Middle Corridor connects the Caspian Sea to the Baku-Tbilisi-Ceyhan (BTC) pipeline and onward to Mediterranean ports, offering up to 1.2 million barrels per day of non-Russian export capacity by 2025.[3]KazMunayGas, “Pipeline Expansion Projects,” kmg.kz Bilateral agreements with Azerbaijan and Georgia grant favorable tariffs and streamline customs procedures, improving netbacks relative to traditional routes. Meanwhile, incremental upgrades on the Caspian Pipeline Consortium (CPC) system sustain flexibility during maintenance or political disruptions. This network diversification enhances the Kazakhstan oil and gas market’s access to European refiners seeking non-Russian crude, thereby directly supporting revenue stability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Crude-price volatility | -0.8% | Global market exposure, affects all production regions | Short term (≤ 2 years) |

| OPEC+ production quotas | -0.6% | National production limits, affects major fields | Medium term (2-4 years) |

| Aging midstream infrastructure bottlenecks | -0.5% | National pipeline network, concentrated in Atyrau region | Medium term (2-4 years) |

| EU carbon-border taxes on high-emission crude | -0.4% | Export-oriented, European market focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Crude-Price Volatility

Kazakhstan’s fiscal revenues and investment pipelines remain sensitive to Brent price swings, especially when the price is below USD 60 per barrel, as offshore operating margins shrink. Production costs average USD 35–40 per barrel in mature onshore fields and USD 50–55 in complex offshore projects. Although the National Fund cushions short-term revenue gaps, prolonged downturns defer drilling schedules, compress exploration budgets, and raise financing costs. Currency fluctuations between the tenge and the U.S. dollar complicate debt servicing on dollar-denominated borrowings. While major IOCs hedge exposures, smaller domestic firms often lack sophisticated risk-management tools, amplifying cash-flow stress across the Kazakhstan oil and gas market.

OPEC+ Production Quotas

Kazakhstan's 2024 OPEC+ ceiling of 1.468 million barrels per day curtails output at Tengiz and Kashagan, limiting the pace at which new trains can ramp up. Compliance audits impose reporting burdens and create seasonal production cuts that clash with equipment-maintenance cycles. The quota framework forces the Ministry of Energy to balance domestic revenue objectives against commitments to global supply management. Nevertheless, alignment with OPEC+ stabilizes international prices and underpins long-term cooperation with strategic investors, thereby preserving the attractiveness of Kazakhstan's oil and gas market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Sector: Upstream Dominance Drives Market Leadership

Upstream activities accounted for 67.90% of Kazakhstan's oil and gas market size in 2025, reflecting the country's reliance on crude and gas extraction for export earnings. The upstream segment is underpinned by mega-field expansions at Tengiz and the ongoing optimization of Kashagan, which utilize advanced gas-injection and sulfur-recovery systems to drive production growth. Digital twins and real-time reservoir-modeling platforms reduce unplanned downtime and enhance well productivity. Over the forecast horizon, upstream remains a cash-flow engine; however, the 7.74% CAGR expected in midstream illustrates a shift in capital toward pipelines, gas processing, and storage as export corridors widen.

Investor appetite for integrated value chains accelerates the convergence of upstream and pipeline ownership. KazMunayGas leverages stakes in both producing assets and the CPC system, exploiting economies of scale and negotiating power on transit tariffs. Midstream's rapid expansion encompasses compressor-station upgrades and branch lines that feed petrochemical feedstock streams, dovetailing with downstream diversification mandates. By 2031, the Kazakhstan oil and gas market is poised to feature a more balanced revenue mix, although upstream will continue to anchor earnings thanks to its high-margin contributions.

By Location: Offshore Projects Shape Market Dynamics

Offshore ventures accounted for 84.25% of Kazakhstan's oil and gas market share in 2025 and are projected to grow at a 5.63% CAGR through 2031. Capital commitments in the North Caspian keep Kashagan Phase 2 on schedule, with the addition of subsea compression units that mitigate reservoir pressure declines. Discoveries in Block Zhenis and partnerships with CNOOC inject fresh momentum into exploration, while FPSO vessels under evaluation could unlock previously uneconomic deepwater clusters. Elevated service intensity drives higher day rates for offshore rigs and subsea contractors, fueling construction segment growth.

Onshore fields, although smaller in relative market share, continue to serve as laboratories for enhanced recovery. Operators in Mangystau deploy nanofluid injectants and digitized flow-monitoring systems to extract remaining barrels at lower carbon intensity. The spread of these technologies protects baseline production and limits decline rates, keeping onshore assets an important stability factor for the Kazakhstan oil and gas market.

By Service: Construction Leads Infrastructure Development

Construction services accounted for 50.85% of total revenue in 2025, driven by multibillion-dollar projects such as the Tengiz surface facilities, refinery revamps, and petrochemical complexes. The segment is projected to grow at a 5.78% CAGR to 2031. Contractors adopt modular fabrication and digital progress-tracking software that compresses project timelines and controls costs. Sinopec’s polyethylene plant near Atyrau and Lukoil’s Caspian platforms are current marquee jobs generating demand for heavy-lift vessels and specialized welding services.

Maintenance, repair, and overhaul complement construction as Kazakhstan’s asset base ages. ISO-aligned inspection regimes and stricter environmental audits lead to increased spending on corrosion control and integrity management. Decommissioning remains nascent but is expected to increase after 2030, as first-generation projects wind down. Collectively, these trends secure a robust pipeline for domestic and international service firms across the Kazakhstan oil and gas market.

Geography Analysis

Kazakhstan's continental expanse overlays multiple hydrocarbon basins, but the Caspian Sea coast represents the epicenter of upstream investment owing to giant reservoirs at Kashagan, Tengiz, and Karachaganak. Atyrau and Mangystau concentrate drilling, fabrication yards, and export terminals, giving these western provinces the lion's share of sector jobs and related infrastructure. Pipeline corridors radiate westward to the Black Sea and Mediterranean through CPC and BTC, and eastward via the Kazakhstan-China route, affording optionality that few landlocked producers enjoy.

Central and eastern regions host auxiliary gas-processing and petrochemical facilities, benefiting from government inducements to distribute economic activity beyond the oil-rich west. The upgrades at Shymkent refinery and ancillary polypropylene projects illustrate the shift. In the north, proximity to Russian rail networks supports the trade in condensate and LPG, while southern routes toward Uzbekistan and Kyrgyzstan handle the rising regional demand for motor fuels.

Environmental stewardship shapes geographic strategy. Caspian Sea operations adhere to strict spill-prevention protocols mandated by the Committee for Environmental Regulation, which require the use of double-hulled shuttle tankers and rapid-response equipment. Inland basins apply stringent groundwater protection standards to fracturing fluids and produced water disposal. As Kazakhstan pursues carbon-neutral growth by 2060, regional authorities are prioritizing the integration of renewable power into oilfield microgrids, particularly in wind-rich Aktobe province. These measures strike a balance between resource extraction and ecological safeguards, thereby reinforcing the long-term viability of Kazakhstan's oil and gas market.

Competitive Landscape

KazMunayGas dominates the domestic stage through its majority stakes in key upstream, midstream, and refining assets; however, international majors supply capital, technology, and off-take agreements that define project economics. Joint-venture structures—such as Tengizchevroil (Chevron, 50%; KazMunayGas, 20%) and North Caspian Operating Company (TotalEnergies, ExxonMobil, Shell, CNPC, INPEX, KazMunayGas)—illustrate collaborative models that reconcile state control with foreign expertise. Market power centers on access to mega-fields, export pipelines, and downstream value-addition capacity.

Chinese state-owned enterprises expand aggressively. CNPC increases production via incremental stake acquisitions, while Sinopec’s petrochemical projects align with Belt and Road financing, heightening competition in downstream margins. European players, such as TotalEnergies and MOL Group, are pivoting into petrochemicals to diversify their cash flows and hedge against shifts in crude demand. Technology differentiators include digital twins, subsea multiphase pumps, and carbon capture pilots. Patent filings related to advanced EOR and subsea tie-backs increased in 2024, indicating sustained R&D investment.

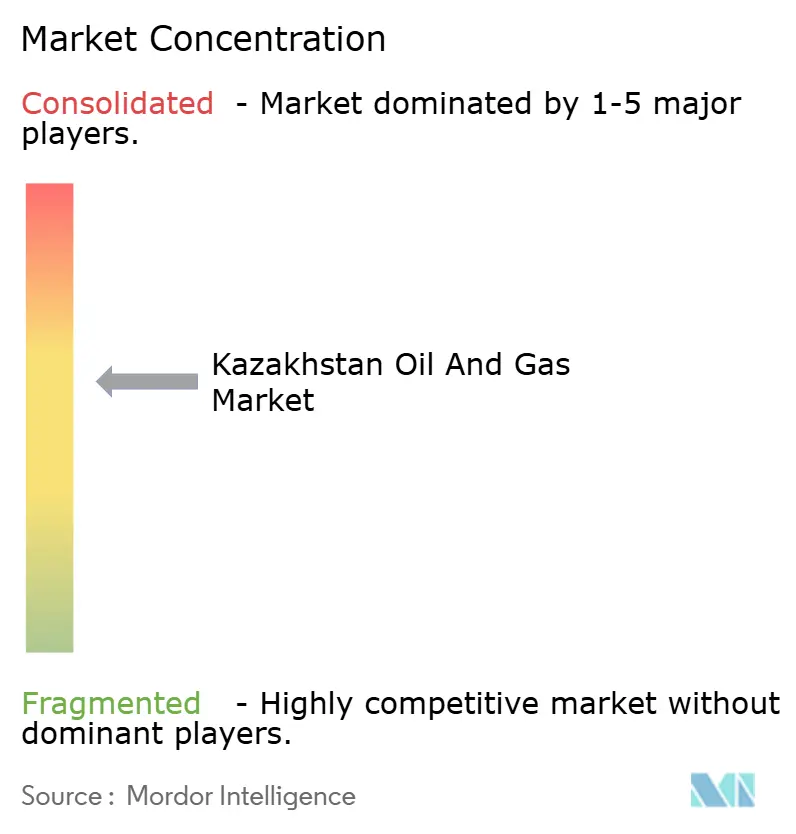

Regulatory oversight under the Ministry of Energy and environmental regulators enforces ISO-aligned standards, raising the bar for new entrants. Local-content thresholds of 30–50% on major builds create growth pathways for domestic engineering firms, although capital-intensive requirements also pose barriers for smaller players. Overall, the Kazakhstan oil and gas market exhibits moderate concentration, with the top five groups controlling a large portion of production and pipeline capacity, yet still leaving niches open for specialized service providers.

Kazakhstan Oil And Gas Industry Leaders

National Company JSC (KazMunayGas)

Chevron Corporation

ExxonMobil Corporation

TotalEnergies SE

PJSC Lukoil Oil Company

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2025: Russia's Gazprom and Kazakhstan have signed a memorandum of understanding, paving the way for the construction of a major gas pipeline from Russia to Kazakhstan.

- June 2025: CNOOC Limited's Hong Kong arm and KazMunayGas have signed a nine-year exploration and production agreement in Kazakhstan, equally dividing investment and operations over a 958-square-kilometre area.

- January 2025: Chevron Corporation announced that its affiliate, Tengizchevroil LLP (TCO), in which it holds a 50% stake, has commenced oil production at the Future Growth Project (FGP) in Kazakhstan's Tengiz oil field.

- November 2024: MOL Group has signed a comprehensive cooperation agreement with KazMunayGas, covering refining, petrochemicals, and retail operations, including USD 500 million in joint investments over a five-year period.

Kazakhstan Oil And Gas Market Report Scope

The oil and gas market refers to the global industry involved in the exploration, production, refining, transportation, and distribution of oil and natural gas resources. It encompasses various activities and sectors related to the extraction and utilization of hydrocarbon reserves.

The Kazakhstani oil and gas market is segmented by sector. By sector, the market is segmented into upstream, midstream, and downstream. For each segment, market sizing and forecasts have been done based on volume (thousand barrels per day).

By Sector

| Upstream |

| Midstream |

| Downstream |

By Location

| Onshore |

| Offshore |

By Service

| Construction |

| Maintenance and Turn-around |

| Decommissioning |

| By Sector | Upstream |

| Midstream | |

| Downstream | |

| By Location | Onshore |

| Offshore | |

| By Service | Construction |

| Maintenance and Turn-around | |

| Decommissioning |

Key Questions Answered in the Report

What is the forecast size of the Kazakhstan oil and gas market by 2031?

The Kazakhstan oil and gas market is projected to reach USD 12.45 billion by 2031, growing at a 4.62% CAGR from 2026 to 2031..

Which segment is expanding the fastest within Kazakhstan's energy value chain?

Midstream infrastructure - pipelines, storage, and gas processing - is expected to grow at an 7.74% CAGR through 2031.

Why are offshore projects crucial for Kazakhstan's future output?

Offshore Caspian fields supply 84.25% of current activity and will lead growth due to large reserves and ongoing Phase 2 expansions.

How is Kazakhstan reducing reliance on Russian transit routes?

The Middle Corridor and upgrades to the BTC and CPC pipelines add 1.2 million barrels per day of non-Russian export capacity.

What role do foreign companies play in Kazakhstan's energy sector?

International majors such as Chevron, ExxonMobil, and TotalEnergies provide capital and technology via joint ventures, accelerating mega-field development and downstream diversification.

How is the government fostering downstream growth?

The Ministry of Energy targets tripling refining capacity with more than USD 10 billion in upgrades and new petrochemical complexes, supported by partnerships like the 2024 MOL Group deal.

Page last updated on: