United Arab Emirates Quick Service Restaurant Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

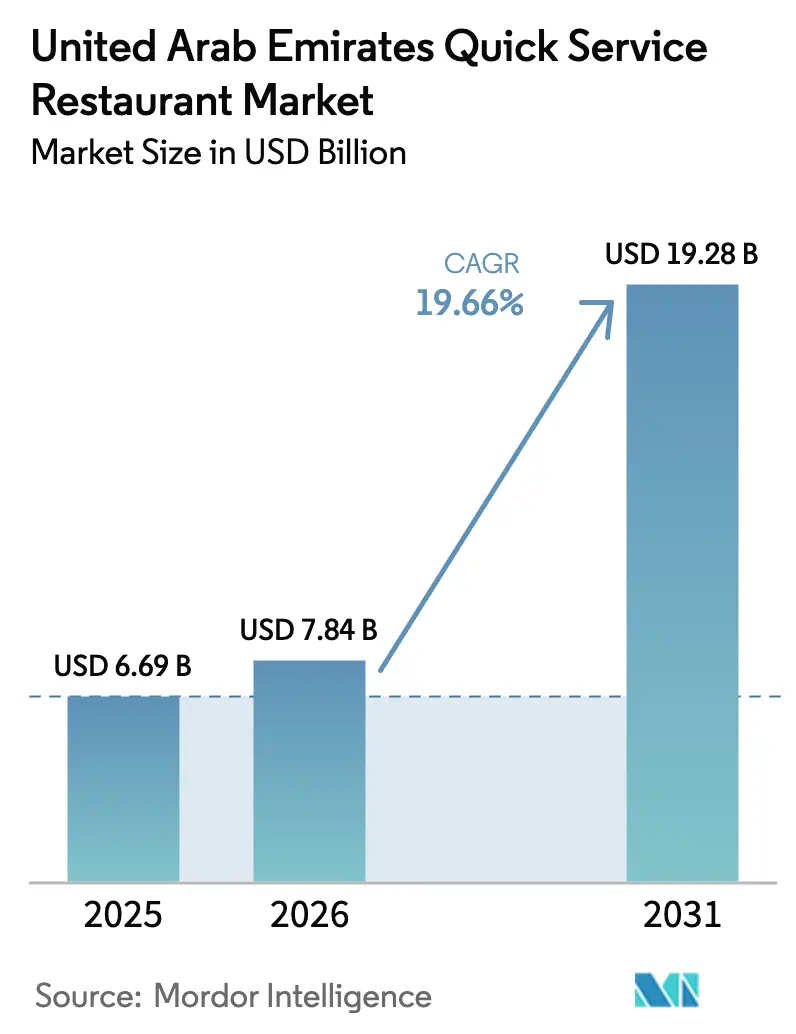

| Base Year Market Size (2025) | USD 6.69 Billion |

| Market Size (2026) | USD 7.84 Billion |

| Market Size (2031) | USD 19.28 Billion |

| Growth Rate (2026 - 2031) | 19.66% CAGR |

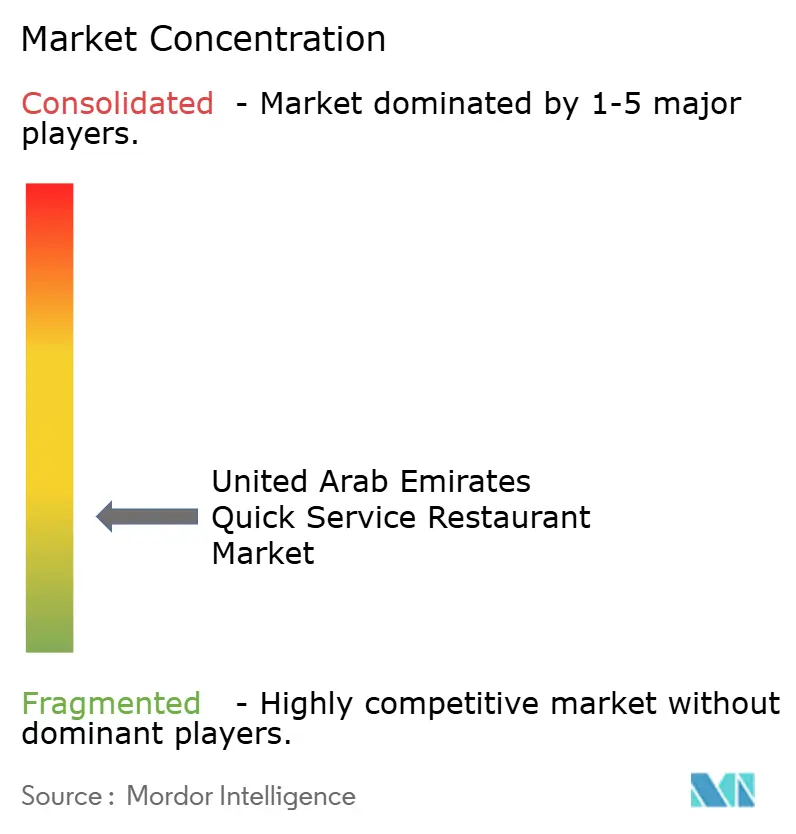

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Quick Service Restaurant Market Analysis by Mordor Intelligence

The United Arab Emirates quick service restaurant market size is expected to increase from USD 6.69 billion in 2025 to USD 7.84 billion in 2026 and reach USD 19.28 billion by 2031, growing at a CAGR of 19.66% over 2026-2031. Cloud kitchens and third-party delivery platforms have reduced the need for large dining spaces, allowing operators to establish themselves in densely populated residential areas with lower capital investments. The expatriate population in Abu Dhabi is expected to grow significantly, concentrating demand in neighborhoods where delivery already accounts for a large share of transactions. The introduction of dynamic commission pricing by aggregators in late 2024 has improved profit margins for high-volume brands, further driving the adoption of delivery services. Independent outlets benefit from shorter menu development cycles, while airports and hotels focus on creating premium venues that increase average transaction values. These combined factors continue to drive significant growth in the United Arab Emirates quick service restaurants market, despite challenges such as rising real estate and labor costs.

Key Report Takeaways

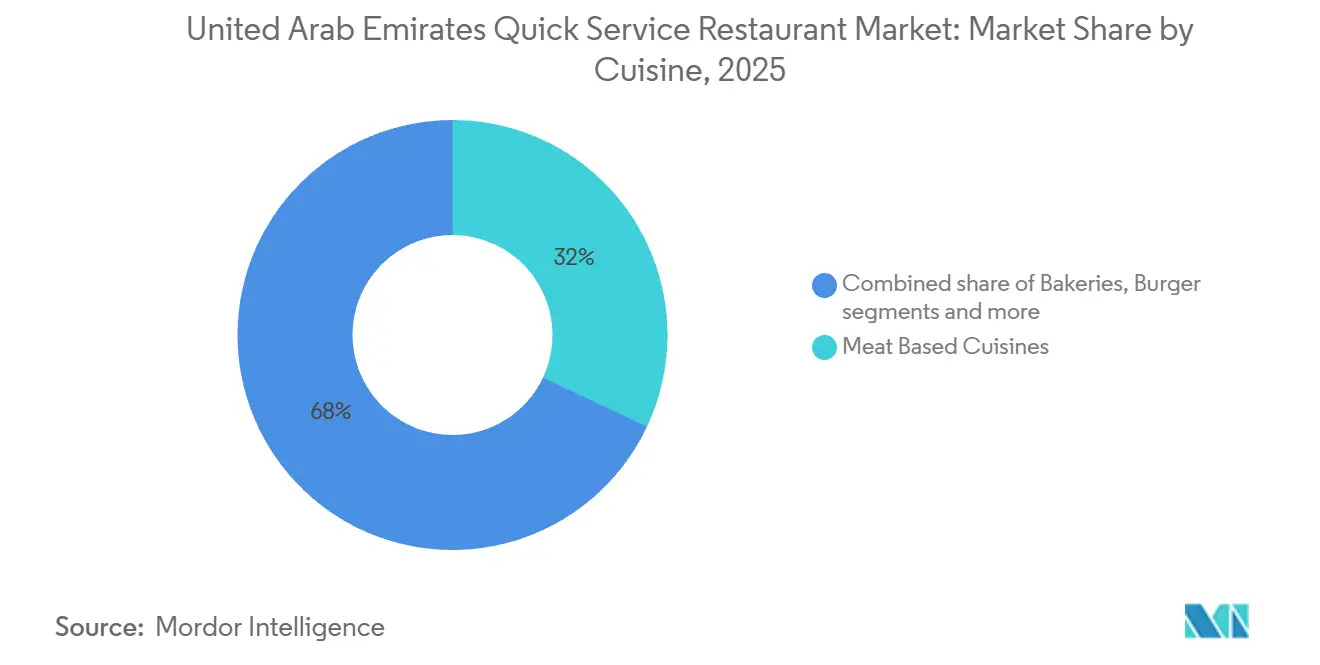

- By cuisine, meat-based formats led with 32.01% revenue share in 2025, whereas pizza is forecast to post the fastest 21.73% CAGR through 2031.

- By outlet, independents captured 53.73% of the United Arab Emirates quick service restaurants market share in 2025 and are advancing at a 20.82% CAGR to 2031.

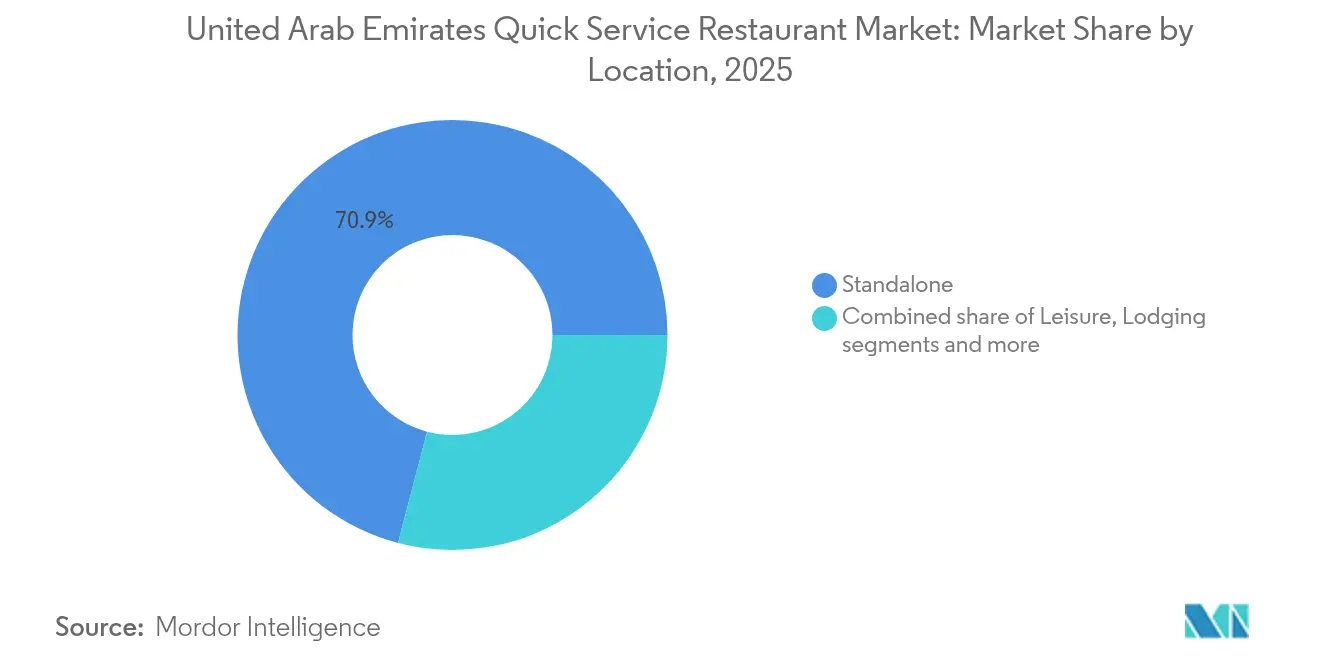

- By location, standalone sites accounted for 71.02% of 2025 spending, while travel-linked venues at airports and transit hubs are projected to expand at 20.91% CAGR.

- By service type, dine-in produced 51.81% of 2025 sales, yet delivery is on track for the highest 21.88% CAGR between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Quick Service Restaurant Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid urbanization alters eating habits favoring quick meals | +3.8% | National, with concentration in Dubai, Abu Dhabi, Sharjah | Medium term (2-4 years) |

| Busy workforce with extended hours prefers convenient food options | +3.2% | National, strongest in Dubai and Abu Dhabi business districts | Short term (≤ 2 years) |

| Proliferation of shopping malls boosts QSR accessibility | +2.4% | National, with emphasis on Dubai, Abu Dhabi, Ras Al Khaimah | Long term (≥ 4 years) |

| Cloud kitchens expand reach without dine-in spaces | +3.5% | National, early gains in Dubai, Abu Dhabi, Sharjah | Short term (≤ 2 years) |

| Dual-income households seek time-saving meal solutions | +2.9% | National, concentrated in urban emirates | Medium term (2-4 years) |

| Airports and hotels host high-traffic QSR outlets | +2.1% | Dubai International, Abu Dhabi International, hotel zones | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid urbanization alters eating habits favoring quick meals

Accelerated urbanization in the United Arab Emirates has reduced meal preparation time for dual-income households, positioning quick service restaurants as the preferred choice for weekday dinners. In 2024, the urban population in the United Arab Emirates reached a significant percentage, with Dubai and Abu Dhabi collectively adding new residents annually. This population growth aligns with increasing average commute times, now exceeding typical durations in Dubai, further limiting opportunities for home cooking. With an employment-to-population ratio among the highest globally, most adults aged 25 to 44 prioritize convenience over cost when choosing meal options. In response, quick service restaurant operators have strategically located outlets near metro stations and residential towers, enabling delivery times of under 20 minutes in high-density areas. This urbanization-driven demand has led standalone quick service restaurants in residential neighborhoods to achieve higher average transaction values compared to mall-based outlets, as customers prioritize proximity over ambiance.

Busy workforce with extended hours prefers convenient food options

The labor market structure in the United Arab Emirates, characterized by a high employment-to-population ratio and long average workweeks, has contributed to time constraints that increase demand for quick service restaurants during peak business hours. In Dubai's business districts, such as Dubai International Financial Centre and Business Bay, office workers create a concentrated lunch demand during midday hours. Quick service restaurant operators in these areas report average transaction times of under 8 minutes, a crucial factor for workers with limited lunch breaks. Additionally, the United Arab Emirates' shift-based economy, where 32% of the workforce is employed in retail, hospitality, and healthcare sectors with irregular hours, drives late-night quick service restaurants demand, peaking during late evening hours. To address this, many Dubai quick service restaurants have extended their operating hours to remain open past midnight. The growing use of mobile ordering apps has further streamlined the process, enabling workers to pre-order meals during commutes and collect them quickly upon arrival. This convenience has resulted in higher order frequency among regular app users.

Proliferation of shopping malls boosts quick service restaurants accessibility

The United Arab Emirates hosts 65 major shopping malls as of 2024, with Dubai accounting for 28 malls that collectively attract 180 million annual visits. These climate-controlled spaces have become social hubs, where families typically spend three to four hours per visit, driving consistent food service demand across multiple dayparts. Mall-based quick service restaurants benefit from anchor tenant agreements that ensure steady foot traffic. Top-performing outlets in Dubai Mall and Mall of the Emirates report revenues 40% higher than standalone locations. The United Arab Emirates' extreme summer temperatures, often exceeding 45 degrees Celsius, make malls the preferred leisure destination for half the year, concentrating quick service restaurant activity in these venues. However, this channel faces challenges from percentage-rent clauses, which can claim 12% to 15% of revenues, requiring operators to meet minimum sales thresholds to avoid lease termination. The United Arab Emirates' ongoing mall expansion, including the USD 1.2 billion Deira Mall set for completion in 2027, will add 2.5 million square feet of retail space. This development presents new opportunities for quick service restaurants but also heightens competition for consumer spending.

Cloud kitchens expand reach without dine-in spaces

Cloud kitchens have separated quick-service restaurant growth from the constraints of real estate availability, enabling operators to meet demand in areas where traditional restaurant rents are high. These delivery-only facilities require lower capital expenditure compared to full-service outlets, resulting in faster payback periods. Dubai Municipality approved new cloud kitchen licenses, indicating growing regulatory acceptance of this model [1]Source: Government of Dubai, “For Food Traders and Establishments,” dm.gov.ae. The cloud kitchen format also supports multi-brand operations within a single kitchen, with some facilities hosting multiple virtual brands that share equipment and labor resources. This operational flexibility has attracted international quick-service restaurant chains looking to test the United Arab Emirates market without committing to full-format establishments. However, the model's dependence on third-party delivery aggregators charging commissions reduces margins and compels operators to maintain minimum order values to remain profitable.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict halal certification requirements complicate menu compliance | -1.8% | National, enforced by ESMA and local municipalities | Long term (≥ 4 years) |

| Health consciousness shifts demand away from high-calorie items | -2.2% | National, strongest in Dubai and Abu Dhabi | Medium term (2-4 years) |

| Food safety compliance demands continuous staff training investments | -1.3% | National, enforced by Dubai Municipality and ADAFSA | Medium term (2-4 years) |

| High rental costs in prime urban locations burden operators | -1.6% | Dubai, Abu Dhabi prime retail and mall locations | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Strict halal certification requirements complicate menu compliance

The Emirates Authority for Standardization and Metrology mandates halal certification for all meat and poultry products sold in the United Arab Emirates [2]Source: Emirates Authority for Standardization and Metrology, “Halal Certification Standards,” esma.gov.ae. This requires quick service restaurant operators to maintain segregated supply chains and dedicated preparation areas. The regulatory framework increases ingredient procurement costs by 8% to 12%, as suppliers must obtain and maintain the UAE.S 2055-1:2015 halal certification. International QSR chains entering the United Arab Emirates market face delays to reformulate recipes and secure approved suppliers, giving established players a first-mover advantage. Additionally, the certification process restricts menu innovation, as each new ingredient requires separate approval. This discourages the introduction of limited-time offers, which are commonly used to attract customers in other markets. Dubai Municipality conducts unannounced inspections of QSR kitchens, with non-compliance penalties including fines of up to AED 50,000 and potential license suspension. While these enforcement measures ensure consumer protection, they impose recurring compliance costs that disproportionately impact independent operators without dedicated regulatory teams.

Health consciousness shifts demand away from high-calorie items

Rising health awareness among consumers in the United Arab Emirates, influenced by government wellness initiatives and social media, has led quick service restaurant operators to reformulate menus and introduce healthier options. With obesity rates in the United Arab Emirates among the highest globally, regulatory authorities have intensified their focus on portion sizes and nutritional labeling [3]Source: World Health Organization, “UAE Health Statistics 2024,” who.int. Dubai Municipality now mandates calorie counts on all menu boards, requiring operators to invest in nutritional analysis and menu redesign. This increased transparency has shifted consumer preferences toward grilled and baked items instead of fried alternatives, impacting margins as healthier ingredients are more expensive than traditional QSR inputs. In response, operators have introduced "better-for-you" sub-brands; however, these typically generate lower average transaction values, reducing overall profitability. Additionally, the growing interest in plant-based proteins has encouraged major chains to test vegan burger options, though adoption remains limited, accounting for a small portion of total orders.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

Pizza formats are projected to achieve a 21.73% compound annual growth rate (CAGR) from 2026 to 2031, marking the fastest growth among all cuisine types. This growth is driven by delivery-friendly packaging and customization options that encourage repeat orders. Meat-based cuisines accounted for a 32.01% market share in 2025, reflecting the United Arab Emirates' (UAE) preference for shawarma, grilled chicken, and burger concepts that adhere to halal dietary requirements. The pizza segment's growth is further supported by lower kitchen complexity, as it requires only ovens and prep stations compared to the multi-station setups needed for burger or fried chicken operations, enabling quicker cloud kitchen deployment.

Burger concepts, while a mature category, continue to evolve by incorporating premium ingredients such as wagyu beef and truffle aioli, appealing to the UAE's high-income demographic. Bakery formats, including croissant and pastry chains, attract morning daypart traffic but face margin challenges due to rising flour costs, which increased by 12% in 2024. Ice cream and dessert quick service restaurants primarily serve as complementary purchases rather than standalone meal options, which limits their growth potential. Other quick service restaurant cuisines, including Asian, Mediterranean, and fusion concepts, benefit from the UAE's multicultural population but remain fragmented across numerous small operators.

By Outlet: Independents Outpace Chains Through Agility

Independent outlets accounted for 53.73% of the market share in 2025 and are projected to maintain a compound annual growth rate (CAGR) of 20.82% through 2031, surpassing chained outlets. Local entrepreneurs benefit from faster decision-making processes and lower overhead costs, allowing them to bypass the royalty fees of 5% to 8% and marketing contributions of 2% to 4% typically associated with franchise agreements. This enables them to offer prices that are lower than those of chains while maintaining comparable profit margins. Furthermore, independent outlets can swiftly adapt their menus to meet hyperlocal preferences, such as incorporating spicier options in areas with a significant South Asian population. In contrast, corporate chains are often constrained by centralized menu planning.

However, independent operators face challenges in securing prime retail locations, as mall landlords generally prefer established brands with a proven track record of attracting foot traffic. Meanwhile, chained outlets, which are expanding at a slower compound annual growth rate, benefit from strong brand recognition and centralized procurement, resulting in a cost advantage on core ingredients. Additionally, chained outlets, particularly in the quick service restaurant segment, leverage their scale to maintain consistent quality and service standards, which further strengthens their market position.

By Location: Standalone Sites Lead but Travel Venues Surge

Standalone locations accounted for 71.02% of the market share in 2025, reflecting the United Arab Emirates' car-centric urban planning, which supports drive-through and curbside pickup formats. Travel-linked outlets at airports and transit hubs are projected to grow at a compound annual growth rate (CAGR) of 20.91% through 2031, driven by Dubai International Airport's planned capacity expansion to 118 million passengers by 2027. Retail locations within shopping malls, contributing 18% of 2025 revenues, face challenges from rising rents, which now average USD 180 per square meter annually in premium Dubai malls.

Leisure venues, such as theme parks and entertainment complexes, represent a niche but high-margin channel, with average transaction values 50% higher than standalone outlets due to captive audiences. Lodging-based quick service restaurants, primarily located in hotels, cater to both guests and external customers; however, hotel food and beverage policies restricting outside brands limit their growth potential. The standalone segment benefits from lower occupancy costs and flexible operating hours, with many outlets operating until 2:00 AM to meet late-night demand. These locations also accommodate drive-through lanes, which account for 35% of transactions at burger and coffee concepts. Travel venues command premium pricing, with airport quick service restaurants charging 30 to 40% more than street-level equivalents, justified by convenience and limited competition.

By Service Type: Delivery Overtakes Dine-In Growth

Delivery channels are projected to grow at a compound annual growth rate (CAGR) of 21.88% from 2026 to 2031, surpassing dine-in's 51.81% market share in 2025 as aggregator platforms streamline the ordering process. While dine-in service remains dominant, it faces challenges from rising labor costs as minimum wages for service staff increased by 15% in 2024 and shifting consumer preferences toward at-home dining. Takeaway formats, which combine the convenience of delivery with lower commission costs, are growing at a CAGR of 19.2%, positioning them as a viable middle ground. The delivery segment's growth is driven by aggregator platforms such as Talabat, Deliveroo, Careem NOW, and Noon Food, which collectively processed over 180 million quick service restaurant orders in 2024. These platforms have made significant investments in dark store infrastructure and 30-minute delivery guarantees, raising customer expectations for speed and reliability.

Dine-in service retains an edge in experiential dining, with customers willing to pay 20% to 25% premiums for ambiance and table service at premium quick service restaurant concepts. However, the labor-intensive nature of dine-in, requiring 8 to 12 staff per outlet compared to 4 to 6 for delivery-only kitchens, reduces profitability in a market where labor costs account for 28% of revenues. Takeaway service, with its lower overhead compared to dine-in and avoidance of aggregator commissions, emerges as the most profitable channel on a per-transaction basis.

Geography Analysis

The United Arab Emirates quick service restaurant market is primarily concentrated in Dubai and Abu Dhabi, which are projected to account for approximately 78% of national revenues by 2025. Dubai's status as a global tourism and business hub, attracting 16 million international visitors in 2024, drives consistent demand for quick service restaurant outlets in hotel zones, shopping districts, and entertainment complexes. In Abu Dhabi, government sector employment and oil-driven economic prosperity contribute to higher per capita quick service restaurant spending, with average transaction values 18% above the national average. The emirate's population growth of 7.5% in 2024, reaching 4.14 million residents, has fueled quick service restaurant expansion into new residential areas such as Yas Island and Al Reem Island.

Sharjah, the third-largest emirate, offers lower operating costs, attracting value-focused quick service restaurant concepts. However, its prohibition on alcohol sales limits the viability of certain restaurant formats. The northern emirates, including Ajman, Ras Al Khaimah, Umm Al Quwain, and Fujairah, present emerging opportunities, with combined quick service restaurant revenues growing at a compound annual growth rate (CAGR) of 23% as infrastructure improvements reduce travel times to Dubai and Abu Dhabi. These emirates benefit from lower real estate costs, with rents averaging 50% below Dubai levels, enabling independent operators to pilot concepts before expanding into premium markets.

The United Arab Emirates's federal structure allows each emirate to establish its own business licensing requirements, creating regulatory complexities for multi-location operators. Dubai Municipality's food safety standards, enforced by the Food Safety Department, serve as the national benchmark, with other emirates largely adopting similar frameworks.

Competitive Landscape

The United Arab Emirates quick service restaurants market is highly fragmented, characterized by the presence of numerous independent operators alongside international franchise networks. This fragmentation is driven by the United Arab Emirates' franchise-based business model, where master licensees such as M.H. Alshaya Company, Americana Restaurants International, and Apparel Group manage multiple global brands under separate legal entities, limiting the consolidation of market share by any single entity. Competitive strategies primarily focus on location density, with major operators securing exclusive concessions in malls and airport terminals, creating localized monopolies in high-traffic areas.

Technology adoption has become a significant differentiator, with operators investing in artificial intelligence-driven kitchen automation, predictive inventory management, and customer data platforms to enable personalized marketing strategies. Opportunities for growth exist in underserved residential neighborhoods, health-oriented concepts, and ethnic cuisine formats catering to the United Arab Emirates' South Asian and Filipino expatriate populations. Additionally, cloud kitchen aggregators are emerging as disruptors in the market. These aggregators operate multi-brand virtual restaurants from centralized facilities, bypassing traditional real estate limitations. By leveraging data analytics, they identify demand gaps and launch targeted concepts within 4 to 6 weeks, a pace that conventional operators cannot match.

Restaurant Brands International, in its 2024 Securities and Exchange Commission 10-K filing, announced plans to expand its Burger King and Tim Hortons presence in the Middle East by adding 150 locations over the next three years, highlighting continued international interest in the United Arab Emirates market.

United Arab Emirates Quick Service Restaurant Industry Leaders

Americana Restaurants International PLC

M.H. Alshaya Co. WLL

The Olayan Group

Apparel Group

AlAmar Foods Co.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Papa John's launched a Croissant Pizza in the United Arab Emirates, featuring a flaky, buttery croissant-style dough base. This product combines traditional pizza toppings with a pastry-like crust texture.

- February 2025: Haldiram's opened a restaurant in the United Arab Emirates at Manazil Al Raffa, Bur Dubai. The facility provides both dine-in and quick service restaurant options, emphasizing authentic Indian flavors and high-quality offerings.

- February 2025: Al Safadi expanded its operations by introducing Oventine, a quick service restaurant inspired by Levantine cuisine. Oventine, the company's first fast-casual venture, serves Lebanese dishes, including flatbreads, wraps, dips, and signature items.

- December 2024: McDonald's United Arab Emirates introduced the McCrispy chicken burger, consisting of a chicken breast fillet paired with shredded lettuce and mayonnaise, served in a potato bun.

United Arab Emirates Quick Service Restaurant Market Report Scope

The United Arab Emirates quick service restaurant market consists of fast-food chains providing standardized, affordable meals with minimal service, focusing on speed through dine-in, takeaway, drive-thru, and delivery options. The market is segmented as follows: by cuisine, including bakeries, burger, ice cream, meat-based cuisines, pizza, and other quick service restaurant cuisines; by outlet, including chained outlet and independent outlet; by location, including leisure, lodging, retail, standalone, and travel; and by service type, including dine-in, takeaway, and delivery. The market sizing has been done in value terms in USD for all the abovementioned segments.

| Bakeries |

| Burger |

| Ice Cream |

| Meat Based Cuisines |

| Pizza |

| Other QSR Cuisines |

| Chined Outlet |

| Independent Outlet |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-In |

| Takeaway |

| Delivery |

| By Cuisine | Bakeries |

| Burger | |

| Ice Cream | |

| Meat Based Cuisines | |

| Pizza | |

| Other QSR Cuisines | |

| By Outlet | Chined Outlet |

| Independent Outlet | |

| By Location | Leisure |

| Lodging | |

| Retail | |

| Standalone | |

| Travel | |

| By Serivce Type | Dine-In |

| Takeaway | |

| Delivery |

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms