United States Quick Service Restaurants Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

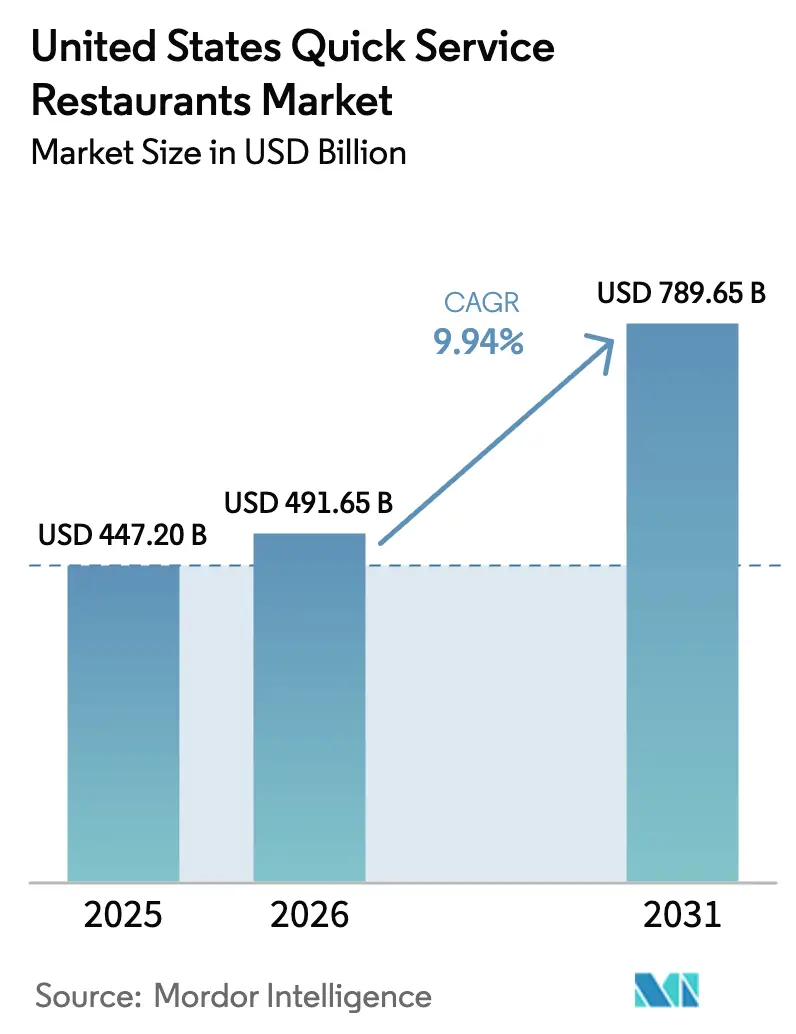

| Base Year Market Size (2025) | USD 447.20 Billion |

| Market Size (2026) | USD 491.65 Billion |

| Market Size (2031) | USD 789.65 Billion |

| Growth Rate (2026 - 2031) | 9.94% CAGR |

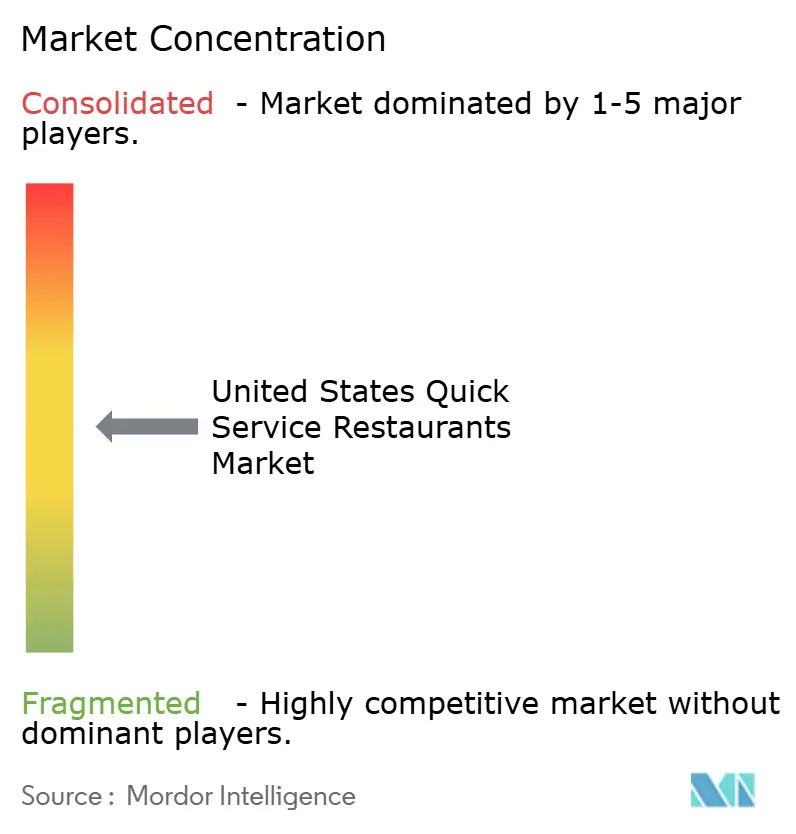

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United States Quick Service Restaurants Market Analysis by Mordor Intelligence

The United States quick service restaurants market size was valued at USD 447.20 billion in 2025 and estimated to grow from USD 491.65 billion in 2026 to reach USD 789.65 billion by 2031, at a CAGR of 9.94% during the forecast period (2026-2031). Brands are leveraging digital ordering, AI-driven kitchens, and rapid franchise expansions to boost revenue and attract more customers. With the help of robotics and voice AI, brands are not only shortening service times but also expanding their delivery reach through ghost kitchens and enhancing sales with data-driven menu boards. As minimum wages rise and food prices climb, operators are increasingly turning to automation. Meanwhile, private-label loyalty programs are fostering repeat visits. The competitive landscape reveals a growing divide: technology-savvy chains are pulling ahead of their resource-limited independent counterparts. Yet, with localized menus and a strong community focus, smaller operators still find opportunities to flourish.

Key Report Takeaways

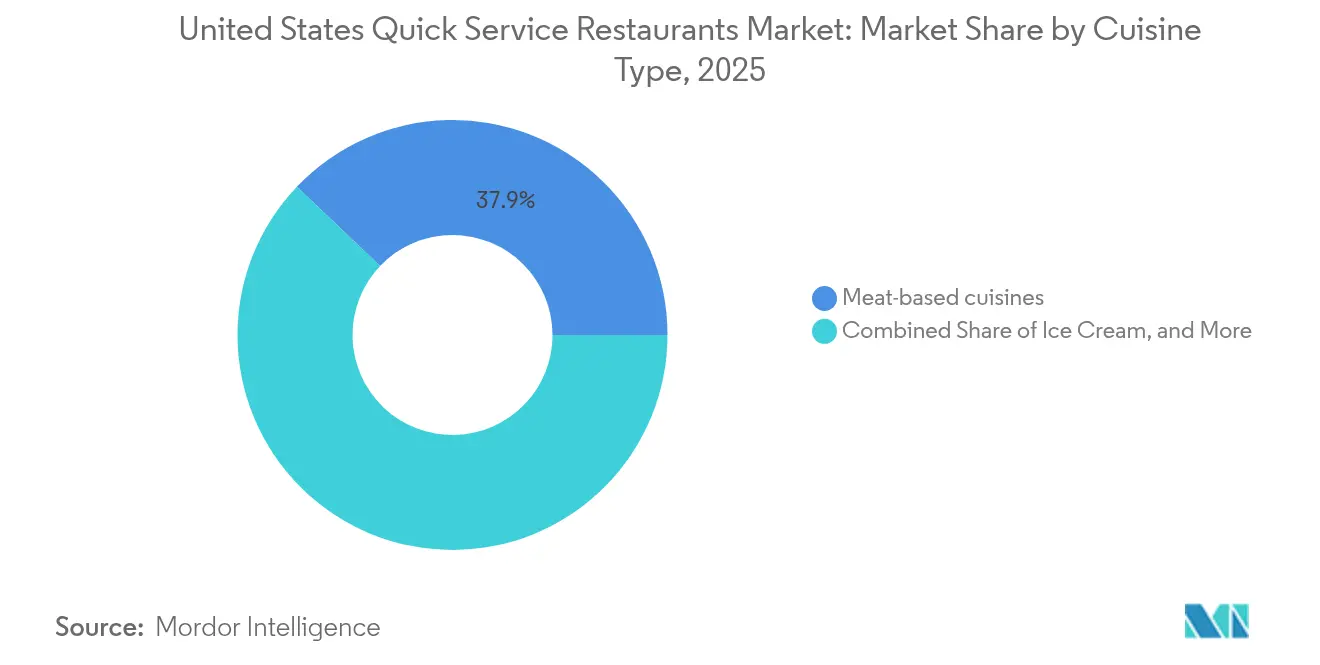

- By cuisine, meat-based concepts led with 37.88% revenue share in 2025; ice cream is expected to post a 12.15% CAGR through 2031.

- By outlet, independent outlets held 57.10% of the United States quick service restaurants market share in 2025, while chained outlets are forecast to expand at a 10.42% CAGR to 2031.

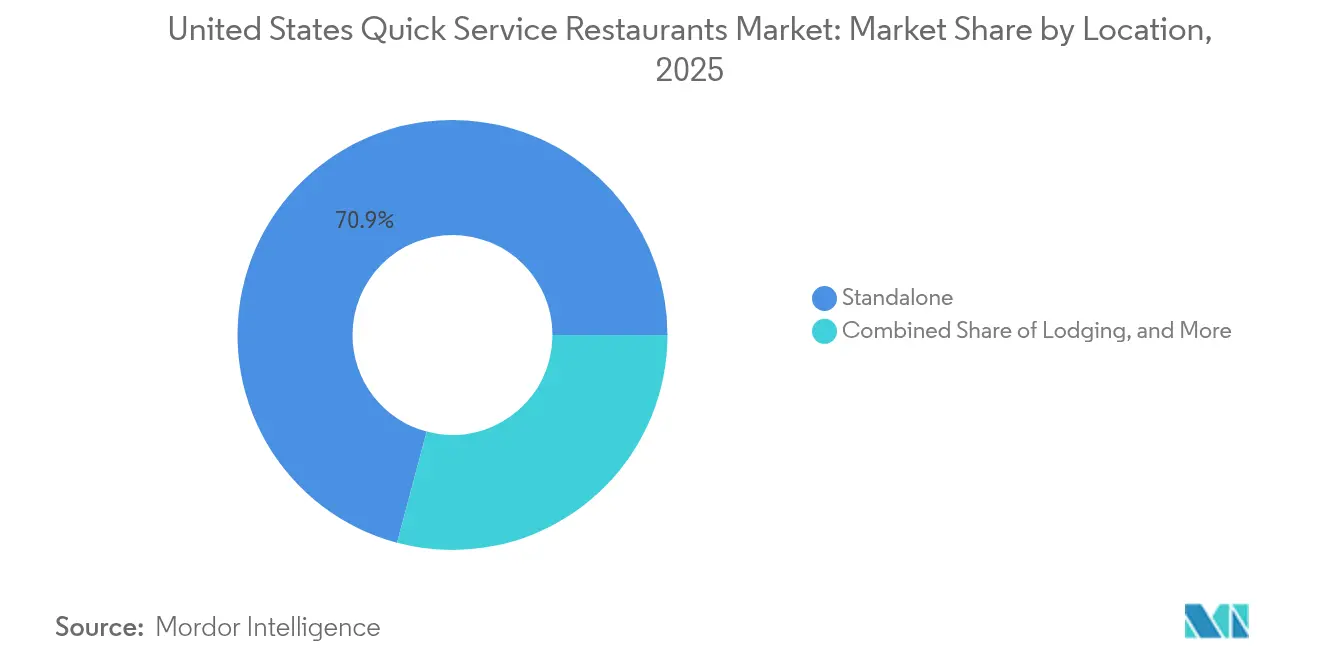

- By location, standalone sites captured 70.85% share of the United States quick service restaurants market size in 2025, and lodging-based venues are advancing at a 12.98% CAGR through 2031.

- By service type, takeaway contributed 46.05% share in 2025; delivery channels are set to grow at a 13.12% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United States Quick Service Restaurants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-Driven Automation and Smart Kitchens | +2.1% | National, with early adoption in urban markets | Medium term (2-4 years) |

| Expansion of Online Food Delivery and Contactless Services | +1.8% | National, strongest in metropolitan areas | Short term (≤ 2 years) |

| Drive-Thru and Self-Service Kiosks Enhancements | +1.4% | National, particularly suburban markets | Short term (≤ 2 years) |

| Expansion of Innovative Service Models like Cloud Kitchens | +1.6% | Urban centers, expanding to secondary markets | Medium term (2-4 years) |

| Menu Diversification and Plant-Based Alternatives | +1.2% | Coastal regions, urban demographics | Long term (≥ 4 years) |

| Strategic Franchise and Footprint Expansion | +1.5% | National, focus on underserved markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Automation and Smart Kitchens

Quick-service restaurants (QSRs) are increasingly turning to artificial intelligence (AI) to address labor shortages and enhance operational efficiency. For instance, Chipotle Mexican Grill has adopted Hyphen's robotic systems for bowl assembly, slashing preparation time by 50% and ensuring consistency across its outlets[1]Source: “Chipotle Mexican Grill Announces Third Quarter 2024 Results,” Chipotle Mexican Grill, chipotle.com. Beyond robotics, smart kitchen technologies encompass predictive inventory management, demand forecasting, and automated quality control, all of which bolster profit margins. As labor costs surge, especially in states like California facing stringent minimum wage laws, the push for operational efficiency intensifies. Furthermore, McDonald's collaboration with IBM highlights the potential of Voice AI in drive-thrus, demonstrating how conversational interfaces can expedite order processing and enhance accuracy.

Expansion of Online Food Delivery and Contactless Services

According to the company’s annual report, digital ordering channels accounted for 36.7% of Chipotle’s total sales in Q3 2025, up from 35.1% for the full year in 2024, underscoring the increasingly critical role of delivery integration in the QSR’s revenue mix. The broadened acceptance of SNAP/EBT on delivery platforms opens doors for new customer acquisitions, particularly targeting lower-income groups who were previously excluded from premium delivery services. While contactless payments surged during the pandemic, their evolution continues with innovations like Panera's palm-scanning and Steak 'n Shake's facial recognition technologies. Such investments in tech not only fortify competitive advantages but also yield invaluable customer data, steering menu tweaks and focused marketing efforts. As the delivery landscape matures, QSR brands are capturing market share in previously hard-to-reach areas due to partnerships with ghost kitchens and the rise of virtual brand concepts.

Drive-Thru and Self-Service Kiosks Enhancements

Drive-thru optimization, a USD 2 billion annual opportunity, is crucial as these channels account for 70% of QSR transactions, underscoring the importance of technological enhancements for market share retention, according to the National Restaurant Association[2]Source: “State of the Restaurant Industry,” National Restaurant Association, restaurant.org. Advanced drive-thru technologies ranging from license plate recognition and predictive ordering based on historical customer behavior to deeper integration with mobile applications not only shorten average service times but also enhance order accuracy. Rising labor costs have further accelerated the adoption of self-service kiosks, which reduce staffing requirements by an estimated 15–20% during peak periods and support upselling through algorithm-driven suggestions. Nonetheless, consumer response to these innovations varies: younger customers tend to embrace digital interfaces, whereas older patrons often favor hybrid models that preserve opportunities for human interaction.

Expansion of Innovative Service Models like Cloud Kitchens

Ghost kitchens are reshaping real estate dynamics for quick-service restaurant (QSR) expansion. Nathan's Famous, for instance, has unveiled plans for 100 new virtual outlets, predominantly nestled within Walmart stores. This move underscores how legacy brands are adeptly tapping into pre-existing retail spaces. Cloud kitchen models slash initial capital outlays by 40-60% when stacked against conventional restaurant setups. They also pave the way for swift market penetration and culinary experimentation, all without the constraints of a physical presence. Through the virtual restaurant model, established QSRs can explore new cuisine categories and pricing tactics, sidestepping any potential cannibalization of their current outlets. Furthermore, delivery-centric operations are reimagining kitchen layouts, prioritizing efficiency over customer-centric designs. This shift not only bolsters profit margins but also accelerates order fulfillment times.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Changing Consumer Preferences and Dietary Trends | -1.3% | National, strongest in health-conscious demographics | Long term (≥ 4 years) |

| Regulatory Compliance Challenges | -0.8% | State-specific, particularly California and New York | Short term (≤ 2 years) |

| Supply-Chain Volatility for Key Commodities | -1.1% | National, with regional variations | Medium term (2-4 years) |

| Rising Food and Labor Costs | -1.6% | National, acute in high-wage states | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Changing Consumer Preferences and Dietary Trends

Recent studies reveal that over 67% of American diners are actively seeking healthier options, posing challenges for traditional quick-service restaurants (QSRs). While there's a growing adoption of plant-based menus, QSR operators grapple with the fact that alternative proteins cost 20-30% more than their conventional counterparts, curbing potential profit margins. Furthermore, as consumers demand transparency in ingredient sourcing and nutritional details, QSRs find themselves needing to overhaul their supply chains and reformulate menus, complicating operations. The trend of home cooking, which surged during pandemic lockdowns, continues to influence how often certain demographic groups dine out at QSRs. Notably, generational preferences are at odds: Gen Z champions sustainability and ethical sourcing, whereas older consumers lean towards value and convenience.

Rising Food and Labor Costs

California's AB 1228 legislation, which sets a minimum wage of USD 20 for quick-service restaurant (QSR) workers, underscores the mounting regulatory pressures squeezing profit margins in the industry, as noted by the California Department of Industrial Relations. Inflation in food commodities is hitting key QSR ingredients hard, with beef prices surging 13.9% year-over-year and egg prices climbing 10.9% in 2024, according to the Bureau of Labor Statistics[3]Source: “Consumer Price Index Summary,” Bureau of Labor Statistics, bls.gov. The hospitality sector continues to grapple with labor shortages, compelling QSR operators to boost wages and enhance benefits. These moves have led to a notable 8-12% annual uptick in operational costs. Testing the elasticity of menu prices shows that consumers push back against hikes beyond 6-8%. This resistance creates a scenario where rising costs outstrip the ability to raise prices, leading to margin compression. Franchise operators find themselves in a tight spot, as pricing strategies mandated by corporate headquarters often clash with the realities of local market conditions and their unique cost structures.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Cuisine: Meat-Based Dominance Drives Innovation

In 2025, meat-based cuisines dominate the market with a 37.88% share, underscoring the American palate's preference for protein-rich options, particularly in burgers, chicken, and specialty meats. Ice cream, positioning itself as a premium dessert, is the fastest-growing segment, boasting a 12.15% CAGR through 2031, due to strategies that extend its operating season. While burger concepts are integrating plant-based alternatives and premium ingredients, pizza segments are harnessing delivery optimizations and customization technologies. Bakeries are capitalizing on breakfast expansions and coffee pairings, boosting both transaction frequency and average order values.

Menu development is shaped by the regulatory landscape, with FDA nutritional labeling mandates pushing for ingredient transparency across all cuisines. Meanwhile, other QSR offerings, spanning ethnic and fusion cuisines, are thriving. They tap into cultural diversity trends and experiential dining, setting themselves apart from conventional American dishes. This trend mirrors a demographic shift: younger consumers are gravitating towards authentic flavors and visually appealing presentations, amplifying their social media engagement and brand loyalty.

By Outlet: Independent Resilience Challenges Chain Efficiency

In 2025, independent outlets hold a commanding 57.10% market share, showcasing an entrepreneurial adaptability and responsiveness to local markets that larger chains find challenging to emulate. Yet, chained outlets are outpacing them with a robust growth rate of 10.42% CAGR. These chains harness operational standardization, invest in technology, and capitalize on supply chain economies, carving out sustainable competitive advantages. Meanwhile, the evolving franchise model is increasingly integrating digital transformation and automation, favoring those operators with deep pockets and technical know-how.

Independent operators grapple with mounting pressures from escalating labor costs and stringent regulatory compliance. These challenges hit harder on smaller businesses, which often lack dedicated administrative resources. In contrast, chained outlets enjoy the luxury of corporate backing, enabling them to wield bulk purchasing power and implement standardized training. This not only simplifies operations but also enhances consistency. The competitive landscape hints at a trend towards market consolidation. Successful independent concepts are either scaling up through franchising or becoming prime targets for acquisition by larger restaurant groups. These giants are on the lookout for deeper local market penetration and opportunities to diversify their menus.

By Location: Standalone Strength Meets Lodging Growth

In 2025, standalone locations command a dominant 70.85% share of the market, underscoring the traditional QSR preference for sites that boast high visibility, easy accessibility, dedicated parking, and drive-thru capabilities. Meanwhile, lodging-based operations are on an impressive growth trajectory, expanding at a 12.98% CAGR. They are effectively tapping into their captive customer bases and leveraging extended operating hours to boost revenue per square foot. Travel-centric locations enjoy a steady stream of customers and the ability to command premium pricing. In contrast, retail-integrated concepts are capitalizing on the advantages of foot traffic and shared infrastructure costs.

Our analysis of location segmentation uncovers strategic openings in markets that remain underserved. Here, traditional standalone developments grapple with real estate challenges and zoning restrictions. QSR operations centered around leisure are nimble, adjusting to seasonal demand shifts. They employ flexible staffing and tweak menus to resonate with both recreational activities and the tastes of tourists. It's noteworthy that regulatory compliance isn't one-size-fits-all. Different location types face distinct challenges. For instance, venues in travel and lodging are often under heightened scrutiny, facing stricter health department regulations and accessibility mandates. These factors play a pivotal role in shaping their operational strategies and determining where they channel their capital investments.

By Service Type: Delivery Acceleration Reshapes Operations

In 2025, takeaway services dominate the market with a 46.05% share, underscoring ingrained consumer habits and operational efficiencies that boost throughput while reducing labor needs. Delivery channels, boasting a robust 13.12% CAGR, are reshaping QSR economics. This transformation is driven by collaborations with third-party platforms and strategic investments in proprietary logistics, broadening their geographic footprint. Meanwhile, dine-in services are evolving, enhancing ambiance and integrating technology. These upgrades, coupled with unique experiential elements, not only justify premium pricing but also encourage longer patron visits.

This evolution in service types underscores lasting behavioral changes, many of which were hastened by pandemic-era shifts. Today, convenience and safety remain paramount in shaping ordering habits. Ghost kitchens, on the other hand, are honing in on delivery efficiency. These kitchens prioritize operational efficiency over customer experience, setting up specialized facilities for this very purpose. Furthermore, food safety standards, dictated by the FDA and local health departments, vary across service types. Notably, delivery operations face stricter mandates, necessitating precise temperature control and packaging. These requirements, in turn, impact both operational costs and menu design choices.

Geography Analysis

Regional performance variations in the U.S. QSR market stem from demographic density, economic conditions, and cultural preferences, leading to distinct growth opportunities across geographic segments. States in the Southeast are witnessing rapid expansion, fueled by population growth, a favorable business climate, and lower operational costs. These factors not only attract franchise investments but also spur corporate expansion initiatives. With a younger demographic profile resonating with QSR target markets and a robust tourism infrastructure, the Southeast is diversifying its QSR locations beyond traditional standalone formats.

Western markets, especially California, grapple with challenges stemming from regulatory compliance, notably the AB 1228 wage legislation and stringent environmental standards. These regulations heighten operational complexities and costs. Yet, California's markets present premium pricing opportunities. Moreover, the region's early embrace of technological innovations offers a competitive edge to operators who invest in advanced systems. Driven by a health-conscious consumer base, California's QSRs are diversifying menus to include plant-based alternatives and organic ingredients, which, despite their higher sourcing costs, yield better margins.

Metropolitan areas in the Northeast boast dense customer bases and a well-established delivery infrastructure, making them prime locations for ghost kitchen expansions and virtual restaurant concepts. However, the Northeast's mature QSR market demands differentiation strategies and premium positioning for growth. Operators are prioritizing convenience, quality, and brand experience over price competition. Furthermore, the influence of state and local authorities on regulations means compliance frameworks vary widely across jurisdictions. This variability necessitates operational flexibility and legal expertise, a challenge more easily navigated by larger chains with dedicated administrative resources.

Competitive Landscape

The market is moderately fragmented, wth established leaders holding a significant market share, while emerging disruptors harness technology and innovative service models to seize growth opportunities. McDonald's Corporation and Starbucks Corporation, through their operational scale, brand recognition, and consistent investments in innovation, have erected barriers that challenge smaller competitors.

Operators with robust capital resources are increasingly favoring AI automation, digital ordering platforms, and optimized delivery systems, enhancing both efficiency and customer experience. Major players are pivoting towards franchise expansion, technology integration, and menu diversification as their primary growth strategies. There's untapped potential in geographic markets that remain underserved, in emerging cuisine categories, and in novel service formats like ghost kitchens, which lower traditional entry barriers.

Patent filings in food automation and digital ordering systems highlight a surge in intellectual property development, hinting at future competitive edges for tech-savvy operators. Compliance with regulations from the FDA and state health departments not only sets operational standards but also demands continuous investment and expertise. This dynamic not only fortifies established players with a compliance infrastructure but also poses a significant hurdle for newcomers.

United States Quick Service Restaurants Industry Leaders

Doctor's Associates, Inc.

Domino's Pizza Inc.

Inspire Brands, Inc.

McDonald's Corporation

Yum! Brands, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- October 2024: Chipotle Mexican Grill announced expansion to 7,000+ locations by 2030, representing an aggressive growth strategy supported by digital sales comprising 37% of total revenue and continued automation investments, including Hyphen robotic systems for bowl assembly operations.

- September 2024: Starbucks Corporation launched a USD 3 billion Reinvention Plan focusing on mobile order optimization, equipment upgrades, and store experience enhancements to address operational challenges and improve customer satisfaction metrics across its network.

- August 2024: McDonald's Corporation expanded partnership agreements with DoorDash and Uber Eats, integrating loyalty programs and promotional strategies to capture increased delivery market share while optimizing third-party platform relationships.

- July 2024: Nathan's Famous announced 100 new ghost kitchen locations, primarily within Walmart stores, demonstrating innovative real estate strategies that leverage existing retail infrastructure for virtual restaurant expansion.

United States Quick Service Restaurants Market Report Scope

Bakeries, Burger, Ice Cream, Meat-based Cuisines, Pizza are covered as segments by Cuisine. Chained Outlets, Independent Outlets are covered as segments by Outlet. Leisure, Lodging, Retail, Standalone, Travel are covered as segments by Location.| Bakeries |

| Burger |

| Ice Cream |

| Meat-based Cuisines |

| Pizza |

| Other QSR Cuisines |

| Chaines Outlets |

| Independent Outlets |

| Leisure |

| Lodging |

| Retail |

| Standalone |

| Travel |

| Dine-in |

| Takeaway |

| Delivery |

| Cuisine | Bakeries |

| Burger | |

| Ice Cream | |

| Meat-based Cuisines | |

| Pizza | |

| Other QSR Cuisines | |

| Outlet | Chaines Outlets |

| Independent Outlets | |

| Location | Leisure |

| Lodging | |

| Retail | |

| Standalone | |

| Travel | |

| Service Type | Dine-in |

| Takeaway | |

| Delivery |

Market Definition

- FULL-SERVICE RESTAURANTS - A foodservice establishment where customers are seated at a table, give their order to a server and are served food at a table.

- QUICK SERVICE RESTAURANTS - A foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables.

- CAFES & BARS - A type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars.

- CLOUD KITCHEN - A foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers.

| Keyword | Definition |

|---|---|

| Albacore Tuna | It is one of the smallest species of tuna found in the six distinct stocks known globally in the Atlantic, Pacific, and Indian oceans, as well as the Mediterranean Sea. |

| Angus beef | It is beef derived from a specific breed of cattle indigenous to Scotland. It requires certification from the American Angus Association to receive the "Certified Angus Beef" quality mark. |

| Asian cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Chinese, Indian, Korean, Japanese, Bengali, Southeast Asian, etc. |

| Average Order Value | It is the average value of all orders made by the customers at a foodservice establishment. |

| Bacon | It is salted or smoked meat that comes from the back or sides of a pig. |

| Bars & Pubs | It is a drinking establishment that is licensed to serve alcoholic drinks for consumption on the premises. |

| Black Angus | It is beef derived from a black-hided breed of cows that don't have horns. |

| BRC | British Retail Consortium |

| Burger | It is a sandwich consisting of one or more cooked beef patties, placed inside a sliced bread roll or bun roll. |

| Café | It is a foodservice establishment serving various refreshments (mainly coffee) and light meals. |

| Cafes & Bars | It is a type of foodservice business that include bars and pubs that are licensed to serve alcoholic drinks for consumption, cafes that serve refreshments and light food items, as well as specialty tea and coffee shops, dessert bars, smoothie bars, and juice bars. |

| Cappuccino | It is an Italian coffee drink that is traditionally prepared with equal parts double espresso, steamed milk, and steamed milk foam. |

| CFIA | Canadian Food Inspection Agency |

| Chained Outlet | It refers to a foodservice establishment that shares brands, operates in several locations, has central management, and standardized business practices. |

| Chicken Tender | It refers to chicken meat prepared from the pectoralis minor muscles of a chicken bird. |

| Cloud Kitchen | It is a foodservice business that utilizes a commercial kitchen for the purpose of preparing food for delivery or takeout only, with no dine-in customers. |

| Cocktail | It is an alcoholic mixed drink made with either a single spirit or a combination of spirits, mixed with other ingredients such as juices, flavored syrups, tonic water, shrubs, and bitters. |

| Edamame | It is a Japanese dish prepared with soybeans (harvested before they ripen or harden) and cooked in its pod. |

| EFSA | European Food Safety Authority |

| ERS | Economic Research Service of the USDA |

| Espresso | It is a concentrated form of coffee, served in shots. |

| European cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Italian, French, German, English, Dutch, Danish, etc. |

| FDA | Food and Drug Administration |

| Fillet Mignon | It is a cut of meat taken from the smaller end of the tenderloin. |

| Flank Steak | It is a cut of beef steak taken from the flank, which lies forward of the rear quarter of a cow. |

| Foodservice | It refers to the part of the food industry which includes businesses, institutions, and companies which prepare meals outside the home. It includes restaurants, school and hospital cafeterias, catering operations, and many other formats. |

| Franks | Also known as frankfurter or Würstchen, it is a type of highly seasoned smoked sausage popular in Austria and Germany. |

| FSANZ | Food Standards Australia New Zealand |

| FSIS | Food Safety and Inspection Service |

| FSSAI | Food Safety and Standards Authority of India |

| Full service restaurant | It refers to a foodservice establishment where customers are seated at a table, give their order to a server, and are served food at a table. |

| Ghost Kitchen | It refers to a cloud kitchen. |

| GLA | Gross Leasable Area |

| Gluten | It is a family of proteins found in grains, including wheat, rye, spelt, and barley. |

| Grain-fed beef | It is beef derived from cattle that have been fed a diet supplemented with soy and corn and other additives. Grain-fed cows can also be given antibiotics and growth hormones to fatten them up more quickly. |

| Grass-fed beef | It is beef derived from cattle that have only been fed grass as feed. |

| Ham | It refers to the pork meat taken from the leg of a pig. |

| HoReCa | Hotels, Restaurants and Cafes |

| Independent Outlet | It refers to a foodservice establishment that operates with a single outlet or is structured as a small chain with no more than three locations. |

| Juice | It is a drink made from the extraction or pressing of the natural liquid contained in fruit and vegetables. |

| Latin American | It includes full-service offerings in restaurants that serve cuisines from cultures such as Mexican, Brazilian, Argentinian, Colombian, etc. |

| Latte | It is a milk-based coffee that is made up of one or two shots of espresso, steamed milk, and a thin layer of frothed milk. |

| Leisure | It refers to foodservice offered as a part of a recreation business, such as sports arenas, zoos, movie theaters, and museums. |

| Lodging | It refers to foodservice offerings at hotels, motels, guesthouses, holiday homes, etc. |

| Macchiato | It is an espresso coffee drink with a small amount of milk, usually foamed. |

| Meat-based cuisines | This inlcudes food items like fried chicken, steak, ribs, etc. where meat is the primary ingredient for the dish. |

| Middle Eastern cuisine | It includes full-service offerings in restaurants that serve cuisines from cultures such as Arabic, Lebanese, Iranian, Israeli, etc. |

| Mocktail | It is an non-alcoholic mixed drink. |

| Mortadella | It is a large Italian sausage or luncheon meat made of finely hashed or ground heat-cured pork, which incorporates at least 15% small cubes of pork fat. |

| North American | It includes full-service offerings in restaurants that serve cuisines from cultures such as American, Canadian, Caribbean, etc. |

| Pastrami | It refers to a highly seasoned smoked beef, typically served in thin slices. |

| PDO | Protected Designation of Origin: It is the name of a geographical region or specific area that is recognized by official rules to produce certain foods with special characteristics related to location. |

| Pepperoni | It is an American variety of spicy salami made from cured meat. |

| Pizza | It is a dish made typically of flattened bread dough spread with a savory mixture usually including tomatoes and cheese and often other toppings and baked. |

| Primal cuts | It refers to the major sections of the carcass. |

| Quick service restaurant | It refers to a foodservice establishment that provides customers convenience, speed, and food offerings at lower prices. Customers usually help themselves and carry their own food to their tables. |

| Retail | It refers to a foodservice outlet inside a mall. shopping complex or a commercial real estate building, where there are other businesses operating as well. |

| Salami | It is a cured sausage consisting of fermented and air-dried meat. |

| Saturated fat | It is a type of fat in which the fatty acid chains have all single bonds. It is generally considered unhealthy. |

| Sausage | It is a meat product made of finely chopped and seasoned meat, which may be fresh, smoked, or pickled and which is then usually stuffed into a casing. |

| Scallop | It is an edible shellfish that is a mollusk with a ribbed shell in two parts. |

| Seitan | It is a plant-based meat substitute made out of wheat gluten. |

| Self-service kiosk | It refers to a self-order point-of-sale (POS) system through which customers place and pay for their own orders at kiosks, enabling totally contactless and frictionless service. |

| Smoothie | It is a beverage made by placing all the ingredients in a container and processing them together, without removing the pulp. |

| Specialty coffee & tea shops | It refers to a foodservice establishment that serves only various types of tea or coffee. |

| Standalone | It refers to a restaurants that have an independent infrastructure setup and not connected to any other business. |

| Sushi | It is a Japanese dish of prepared vinegared rice, usually with some sugar and salt, accompanied by a variety of ingredients, such as seafood—often raw—and vegetables. |

| Travel | It refers to foodservice offerings such as airplane food, dining on long-distance trains, and foodservice on cruise ships. |

| Virtual Kitchen | It refers to a cloud kitchen. |

| Wagyu Beef | It is beef derived from any of four strains of a breed of black or red Japanese cattle that are valued for their highly marbled meat. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: In order to build a robust forecasting methodology, the variables and factors identified in Step 1 are tested against available historical market numbers. Through an iterative process, the variables required for the market forecast are set, and the model is built on the basis of these variables.

- Step-2: Build a Market Model: Market size estimations for the forecast years are in nominal terms. Inflation is considered for average order value, and it is forecasted as per predicted inflation rates in the countries.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables, and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms