Energy & Power

30th JulyUnlocking Market Potential for Solid-State Transformers

3 Min Read

The United Arab Emirates Oil and Gas Upstream Market Report is Segmented by Location of Deployment (Onshore and Offshore), Resource Type (Crude Oil and Natural Gas), Well Type (Conventional and Unconventional), and Service (Exploration, Development and Production, and Decommissioning). The Market Sizes and Forecasts are Provided in Terms of Value (USD).

Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

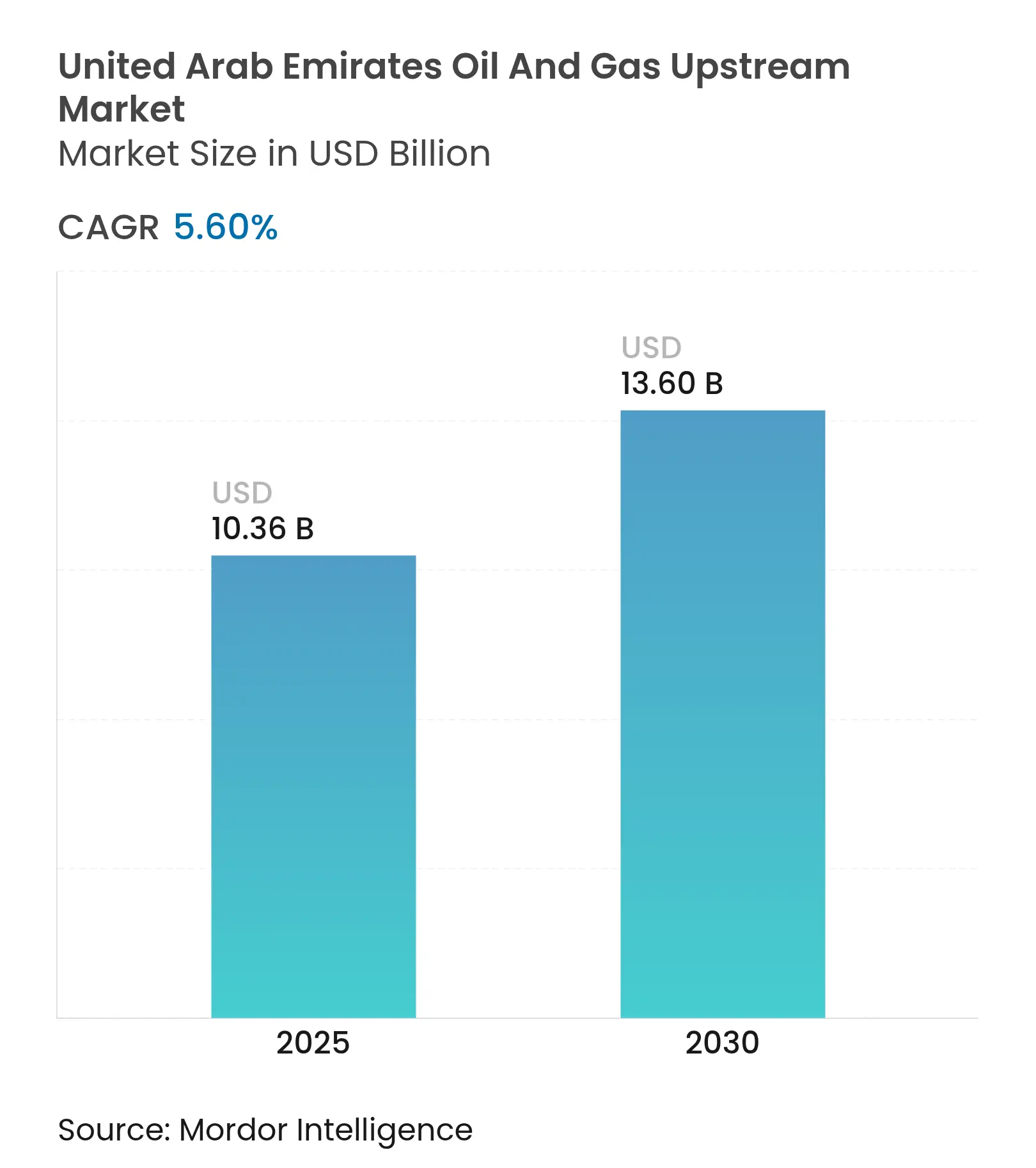

| Market Size (2025) | USD 10.36 Billion |

| Market Size (2030) | USD 13.60 Billion |

| Growth Rate (2025 - 2030) | 5.60 % CAGR |

| Market Concentration | High |

Major Players *Disclaimer: Major Players sorted in no particular order. Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

ADNOC’s USD 150 billion 2023-2027 capital program, which prioritizes sour-gas monetization, unconventional drilling, and AI-enabled optimization, pushes the UAE oil and gas upstream market toward higher recovery factors and lower lifting costs.(1)ADNOC, “Rich Gas Development Project Details,” adnoc.ae Fast-track Production Sharing Contract (PSC) terms cut approval time by two-thirds, enticing IOCs such as INPEX and PETRONAS to expand acreage, while the In-Country Value (ICV) 3.0 policy steers procurement to domestic suppliers, stabilizing local supply chains and employment.(2)Ministry of Industry & Advanced Technology, “ICV 3.0 Framework,” moiat.gov.ae AI tools, including RoboWell autonomous well control and the AR360 reservoir platform, already deployed across more than 30 reservoirs, reduce gas-lift usage by 30% and well interventions by 50%, widening digital adoption gaps between incumbents and new entrants. Finally, LNG export contracts signed in 2025 guarantee multi-year offtake, ensuring that upstream gas projects secure bankable revenues even as OPEC-plus quotas cap crude liftings.

Key Report Takeaways

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Expanding sour-gas monetization projects Expanding sour-gas monetization projects | +1.0% | Abu Dhabi offshore clusters | Medium term (2-4 years) | (~) % Impact on CAGR Forecast:+1.0% | Geographic Relevance:Abu Dhabi offshore clusters | Impact Timeline:Medium term (2-4 years) |

Fast-track concessions to IOCs under new PSC terms Fast-track concessions to IOCs under new PSC terms | +0.8% | Nationwide onshore & shallow-water blocks | Short term (≤ 2 years) | |||

ADNOC’s USD 150 billion 2023-27 upstream roadmap ADNOC’s USD 150 billion 2023-27 upstream roadmap | +0.6% | All producing basins | Long term (≥ 4 years) | |||

In-Country Value (ICV) localization 3.0 In-Country Value (ICV) localization 3.0 | +0.5% | Major industrial zones | Medium term (2-4 years) | |||

AI-powered seismic imaging roll-out AI-powered seismic imaging roll-out | +0.4% | Complex reservoirs | Short term (≤ 2 years) | |||

CCUS-linked brown-field recovery incentives CCUS-linked brown-field recovery incentives | +0.3% | Mature onshore fields | Long term (≥ 4 years) | |||

| Source: Mordor Intelligence | ||||||

Expanding Sour-Gas Monetization Projects

The USD 5 billion Rich Gas Development initiative enhances processing capacity for high-sulfur streams, making previously uneconomic reservoirs bankable and increasing drilling demand in the offshore Hail & Ghasha cluster. The project integrates Linde’s HISORP capture units, locking away 1.5 million tonnes per year within the Ta’ziz complex, reinforcing the cross-value chain of CO₂ and aligning upstream operations with net-zero pledges.(3)Linde, “HISORP CO₂ Capture Technology,” linde.com Specialized high-integrity casing, corrosion-resistant tubing, and multiphase pumps raise per-well service revenues, while premium gas achieves higher realizations in long-term LNG contracts. ADNOC’s strategy thereby recasts sour-gas liabilities into export-grade assets, underpinning a 1.0 percentage-point uplift to the overall CAGR of the UAE oil and gas upstream market. Rising gas feedstock also supplies methanol and hydrogen ventures within the Ta’ziz complex, reinforcing cross-value chain synergies.

Fast-Track Concessions to IOCs Under New PSC Terms

New fiscal terms reduce government participation and widen cost-recovery ceilings, thereby shrinking approval cycles from 18 months to approximately six months. INPEX’s 2024 win of Block 4 exemplifies the speedier regime, with drilling obligations front-loaded to the first three years.(4)INPEX Corporation, “Block 4 Award Announcement,” inpex.co.jp PETRONAS followed with a three-block package, pledging seismic and appraisal wells under the same framework.(5)PETRONAS, “Exploration Licenses in UAE,” petronas.com Accelerated acreage awards drive signature bonuses higher and attract advanced completion technologies from North American shale plays. Service firms able to mobilize crews quickly secure multi-year lump-sum contracts, nudging topline growth for the UAE oil and gas upstream market. The structural shift from joint-venture bidding toward transparent bid rounds also raises competitive tension, unlocking marginal reservoirs.

ADNOC’s USD 150 Billion 2023-27 Upstream CAPEX Roadmap

More than USD 30 billion is allocated for AI-enabled rigs, increasing ADNOC Drilling’s fleet to over 149 units by 2026. Another USD 1.7 billion fund, the Turnwell JV with SLB and Patterson-UTI, is to increase crop drilling days by 15% in unconventional targets. Capital also supports remote-operation centers at Zirku Island, trimming offshore crew counts by 50% and slashing helicopter transfers. Supply-chain bottlenecks, such as top-drive motors, rotary-steerable systems, and HPHT packers, allow service vendors with local inventory to charge premium day rates. Consequently, the roadmap locks in a multi-year backlog and cushions the UAE oil and gas upstream industry against cyclical downturns.

In-Country Value (ICV) Localization Programme 3.0

ICV weighting now accounts for 40% of bid evaluation, compelling foreign suppliers to onshore fabrication or enter joint ventures. The initiative has channeled AED 67 billion (approximately USD 18.2 billion) into domestic procurement since its launch. Local steel mills are now hot-rolling OCTG grades X-95 and G-105, reducing import lead times by an average of 25 days. Service firms that have opened UAE factories, such as Halliburton’s cement-blending plant and Schlumberger’s pressure-pumping base, report bid-win ratios exceeding 65%. Localization also anchors 19,000 Emirati jobs, easing talent shortages in critical disciplines and stabilizing project schedules.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline | |||

|---|---|---|---|---|---|---|

Volatility in OPEC-plus quota compliance Volatility in OPEC-plus quota compliance | -0.7% | National, affecting all upstream production assets | Short term (≤ 2 years) | (~) % Impact on CAGR Forecast:-0.7% | Geographic Relevance:National, affecting all upstream production assets | Impact Timeline:Short term (≤ 2 years) |

Growing renewable-power build-out in federal energy plan Growing renewable-power build-out in federal energy plan | -0.5% | National, with concentration in Abu Dhabi and Dubai | Long term (≥ 4 years) | |||

Talent shortage in HPHT drilling expertise Talent shortage in HPHT drilling expertise | -0.4% | National, concentrated in unconventional and deep-water operations | Medium term (2-4 years) | |||

Tier-III sulfur-emission standards for offshore rigs Tier-III sulfur-emission standards for offshore rigs | -0.3% | Offshore operations, primarily Abu Dhabi marine areas | Short term (≤ 2 years) | |||

| Source: Mordor Intelligence | ||||||

Volatility in OPEC-Plus Quota Compliance

UAE’s Murban exports averaged 1.36 million b/d in 2024, some 250,000 b/d under technical capacity, to stay within OPEC-plus ceilings. Operators must thus retain 10%-15% spare capacity, which distorts rig-utilization schedules and extends payback periods. Drilling contractors idle units yet must keep crews ready, thereby inflating standby costs that are passed through in service pricing. While July 2025 revisions grant the UAE a modest quota bump, the absence of a long-term formula keeps planners cautious. Consequently, operators front-load short-cycle gas wells that convert more quickly, shifting capital expenditures away from large oil platforms.

Growing Renewable-Power Build-out in Federal Energy Plan

Federal energy spending earmarked for solar, wind, and nuclear energy rose from 3% in 2017-2019 to 43% in 2021-2022, redistributing capital away from hydrocarbons. Barakah’s 5.6 GW nuclear fleet already accounts for a quarter of the national load, thereby reducing gas consumption for power generation. The USD 160 billion Net-Zero 2050 budget channels funds to green hydrogen hubs, tightening upstream purse strings after 2027. Investors now discount long-cycle oil projects by 2-3 percentage points, even as LNG export potential sustains gas drilling.

By Location of Deployment: Digitally Optimized Onshore Lead Against Fast-Rising Offshore

Onshore operations controlled 69.5% of the UAE oil and gas upstream market share in 2024, generating USD 7.06 billion of the UAE oil and gas upstream market size, thanks to RoboWell-guided lift-gas cuts and Neuron 5 analytics, which halved unplanned shutdowns.(6)Halliburton, “RoboWell Performance Metrics,” halliburton.com Abundant legacy infrastructure, easy road access, and lower service-day rates sustain cost competitiveness. AI models ingest 240 million data points daily from Northeast Bab alone, enabling 20% longer maintenance intervals and boosting uptime. These factors lock in onshore leadership; yet, growth is comparatively slower at a 4.9% CAGR because most easy barrels are already online.

Offshore, although smaller, is projected to expand ata 6.4% CAGR, lifting its portion of the UAE oil and gas upstream market size to roughly USD 5.2 billion by 2030. ADNOC Drilling’s USD 1.15 billion jack-up acquisition program integrates down-hole streaming sensors and 5G links to Zirku’s control room, located 120 km away, cutting rig headcount by 40%. The SARB digital twin has raised capacity by 25% to 140,000 b/d without requiring extra topside hardware. Such remote operations economics, combined with fresher reserves, render offshore the momentum engine in the UAE oil and gas upstream market.

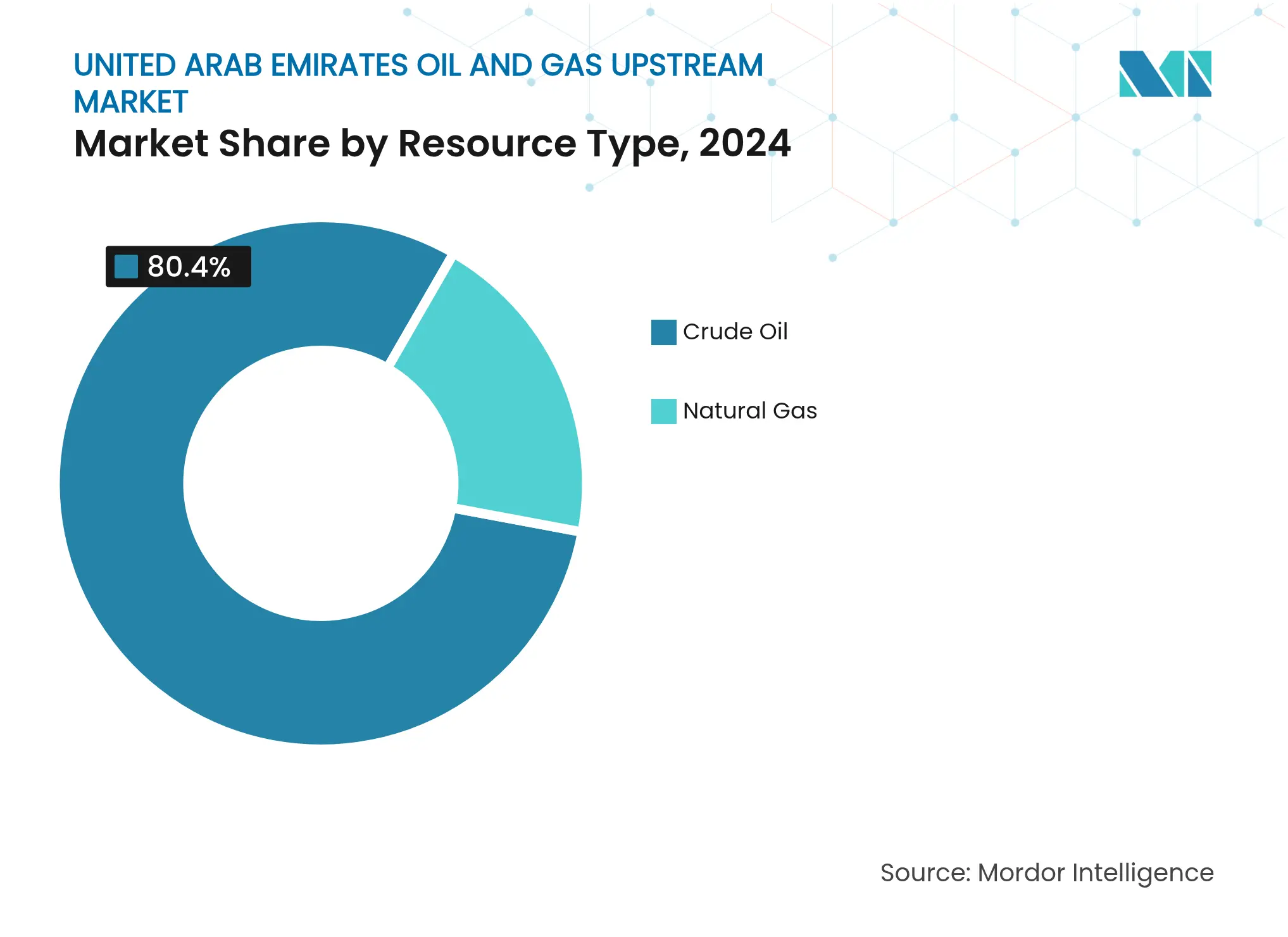

By Resource Type: Gas Monetization Outpaces Oil Dominance

Crude oil still accounted for 80.4% of revenue in 2024, equating to USD 7.90 billion of the UAE's oil and gas upstream market size, yet it faces quota ceilings. Natural gas, although only USD 1.92 billion at the time, is forecast to grow at a 6.9% CAGR, capturing LNG arbitrage and hydrogen feedstock demand. The Rich Gas Development scheme and Ruwais LNG's scale-up beyond 15 million tonnes per year secure 20-year sales to ENN and Indian Oil, ensuring stable cash flows. Gas wells also qualify for CCUS credits, resulting in full-cycle costs falling below USD 2.5/mmbtu net of incentives. Turquoise hydrogen trials at Habshan generate both H₂ and graphene, widening revenue per molecule.

Oil remains strategic: Murban's API 46 and low sulfur keep refinery margins attractive. Yet carbon-adjustment levies in EU markets pressure future crude flows. Therefore, investment is tilting toward gas, explaining its faster expansion within the UAE oil and gas upstream industry.

Note: Segment shares of all individual segments available upon report purchase

By Well Type: Conventional Scale Meets Unconventional Upside

Conventional completions accounted for 69.9% of 2024 spending, driven by relatively easy geology and depreciated infrastructure. The average lifting cost is under USD 4 per barrel of oil equivalent (boe). Unconventional wells, though costlier at USD 8-USD 10/boe, register a 6.5% CAGR, aided by SLB-Patterson Turnwell rigs that reduce drill time to 25 days from 40 days. AI-assisted geosteering boosts lateral exposure by 18%, lifting EURs and narrowing breakevens. Challenges persist, HPHT zones require advanced metallurgy, and Emirati directional drilling talent is limited. Nevertheless, incentives such as 0% royalty for the first five years lure capital. The UAE oil and gas upstream market, therefore, enjoys a blended risk profile, stabilizing cash flows from conventional stock while layering high-growth unconventional barrels.

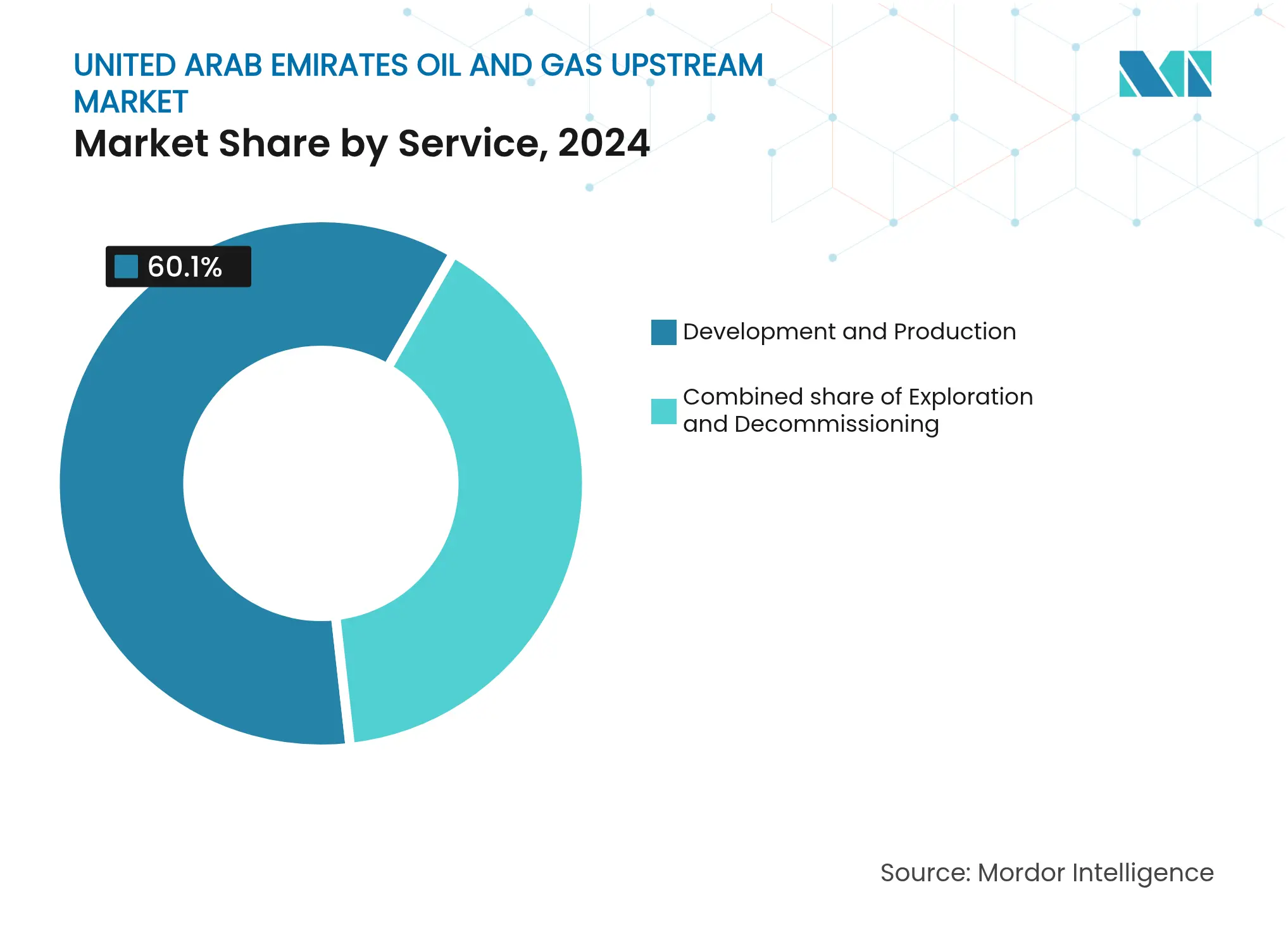

By Service: Production Optimization Dominates; Decommissioning Breaks Out

Development and production services accounted for 60.1% of the 2024 value, illustrating ADNOC’s push to increase recovery through AR360 reservoir AI, which raises the recovery rate by 10 percentage points. Predictive maintenance contracts ensure service companies a steady, annuity-like income. Exploration claims a subdued 13% share amid OPEC limits. Decommissioning, although currently at just 4.5%, is increasing at a 7.8% CAGR as 40-year-old offshore jackets approach retirement. Veolia’s 98% material-recovery process is now being piloted at Das Island, reducing waste disposal by 85%. New ESG rules require zero-leak plugging and topside recycling, expanding spend per platform to USD 25-USD 30 million, well above historical levels.

Note: Segment shares of all individual segments available upon report purchase

Abu Dhabi anchors over 94% of national reserves and funnels most capex; onshore Bab and Bu Hasa clusters alone drew USD 6 billion in 2025 project funds, cementing the emirate’s central role in the UAE oil and gas upstream market. Dubai leverages Jebel Ali Port and free-zone finance to house more than 350 upstream vendors, providing agile logistics and lease financing. Sharjah’s Lamprell yard refurbishes ADNOC Drilling jack-ups, shortening mobilization times and supporting offshore expansion.

Federal integration ensures ICV credits earned in Abu Dhabi flow to SMEs in Ras Al Khaimah and Fujairah, distributing wage and procurement gains. The UAE’s straddling of European and Asian demand hubs enables split cargos; Murban trades on ICE Futures Abu Dhabi while LNG spot desks in Singapore arbitrage east-west spreads. Cross-GCC collaboration with Saudi Aramco on hydrogen certification and with QatarEnergy on CCS knowledge sharing catalyzes regional technology advancement. Simultaneously, domestic renewables, including the 2 GW Al Dhafra solar park, liberate gas for export, elevating the profitability of dry-gas fields.

Reports are available across multiple geographies.

Gain in-depth market insights across regions to support informed decisions.

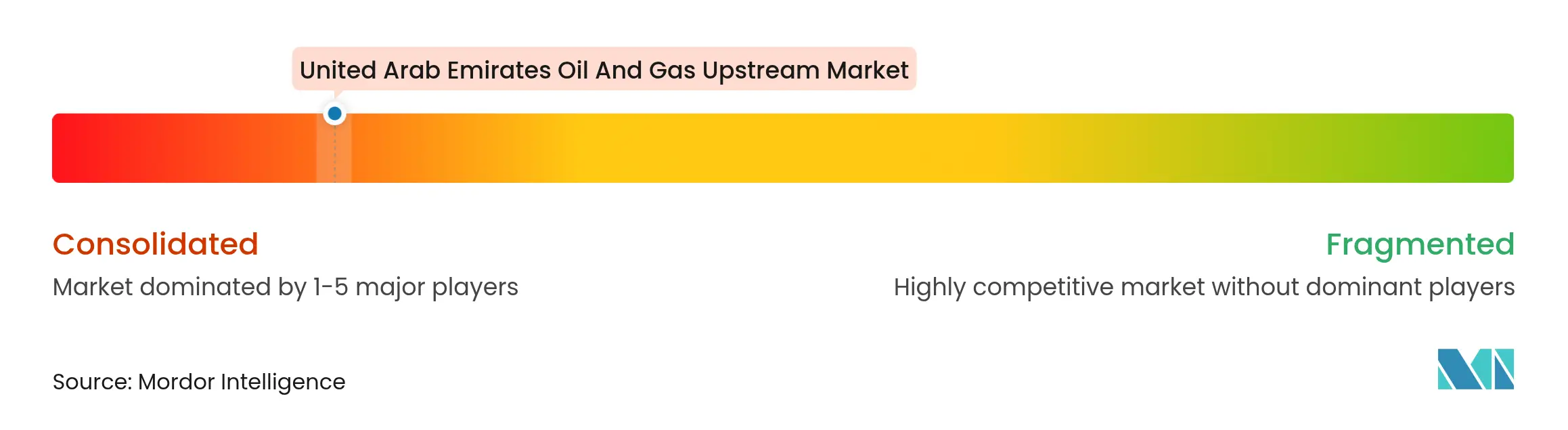

Market Concentration

Market concentration is high: ADNOC holds operatorship stakes above 60% in every producing concession, yet partners with ExxonMobil, TotalEnergies, and ENI for technology and capital. These majors accept minority equity in exchange for stable, long-plateau assets. Service procurement is contestable; Halliburton clinched a USD 1.63 billion integrated drilling award in April 2025, the sector’s biggest single contract, illustrating scale benefits. Schlumberger’s Innovation Factory in Abu Dhabi trains bespoke AI models for down-hole automation, deepening its moat.(7)SLB, “Innovation Factori Abu Dhabi Showcase,” slb.com

ICV scoring reshapes competition: firms with UAE factories secure a 20-30 basis-point bid edge. Baker Hughes partnered with local G42 to launch a cloud-based production-optimization suite, signaling the convergence of IT and oil. Decommissioning attracts newcomers, Veolia and Subsea 7 scout plots at Das Island yard, to capture the 100-platform retirement backlog.

*Disclaimer: Major Players sorted in no particular order

1. Introduction

2. Research Methodology

3. Executive Summary

4. Market Landscape

5. Market Size & Growth Forecasts

6. Competitive Landscape

7. Market Opportunities & Future Outlook

Upstream refers operations stages in the oil and gas industry that involve exploration and production. Oil and gas companies can generally be divided into three segments: upstream, midstream, and downstream. Upstream firms deal primarily with the exploration and initial production stages of the oil and gas industry.

The United Arab Emirates oil and gas upstream market is segmented by location of deployment. By location of deployment, the market is segmented into Onshore and Offshore. The report provides the market size and forecast based on value for all the aforementioned segments.

Unlocking Market Potential for Solid-State Transformers

3 Min Read

When decisions matter, industry leaders turn to our analysts. Let’s talk.