Market Overview

| Study Period | 2020 - 2031 |

|---|---|

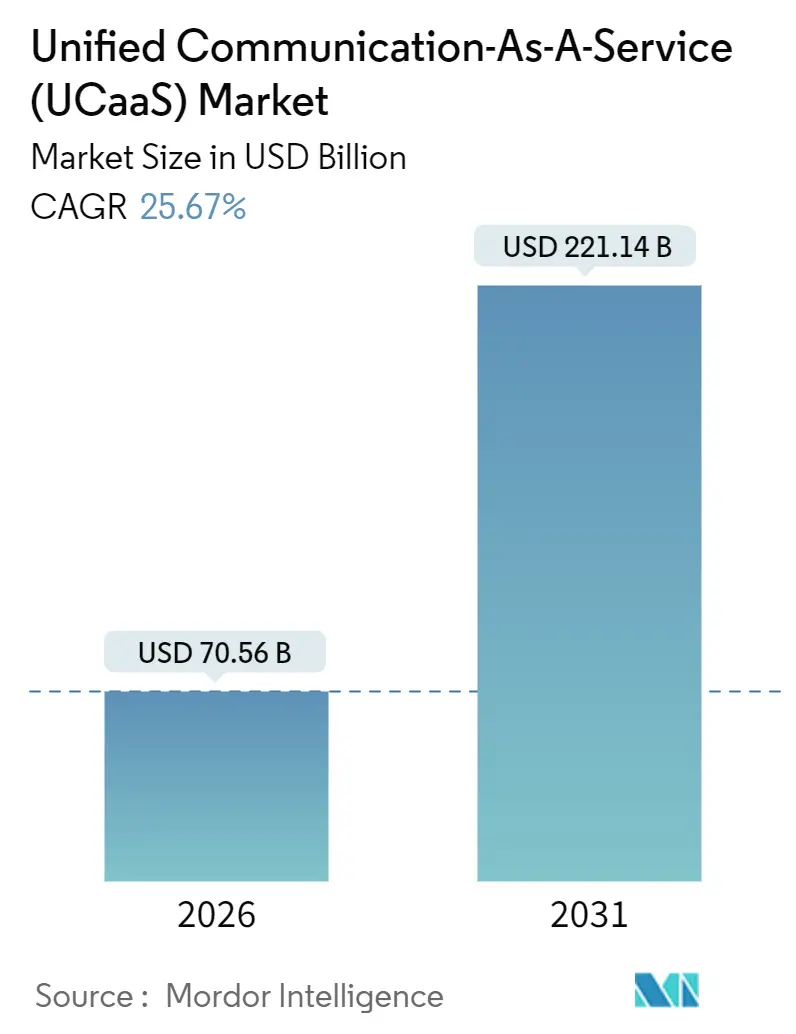

| Market Size (2026) | USD 70.56 Billion |

| Market Size (2031) | USD 221.14 Billion |

| Growth Rate (2026 - 2031) | 25.67% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Unified Communication-As-A-Service (UCaaS) Market Analysis by Mordor Intelligence

The unified communication-as-a-service market presently stands at USD 70.56 billion in 2026 and is projected to reach USD 221.14 billion by 2031, translating to a robust 25.67% CAGR across the forecast horizon, according to Mordor Intelligence. Strengthening demand for subscription-based voice, video, and messaging suites is displacing legacy PBX investments, while public cloud economics accelerate time-to-value for organizations of every size. Collaboration platforms that merge chat, file-sharing, and project management are scaling faster than pure voice workloads, especially where generative AI copilots automate meeting notes and follow-up tasks. Vendors that bundle UCaaS with contact-center and programmable-communications services are expanding wallet share, even as toll-fraud risks and data-sovereignty rules add cost and complexity. Overall, the unified communication-as-a-service market is primed for sustained double-digit expansion as work-from-anywhere models crystallize into standard policy.

Key Report Takeaways

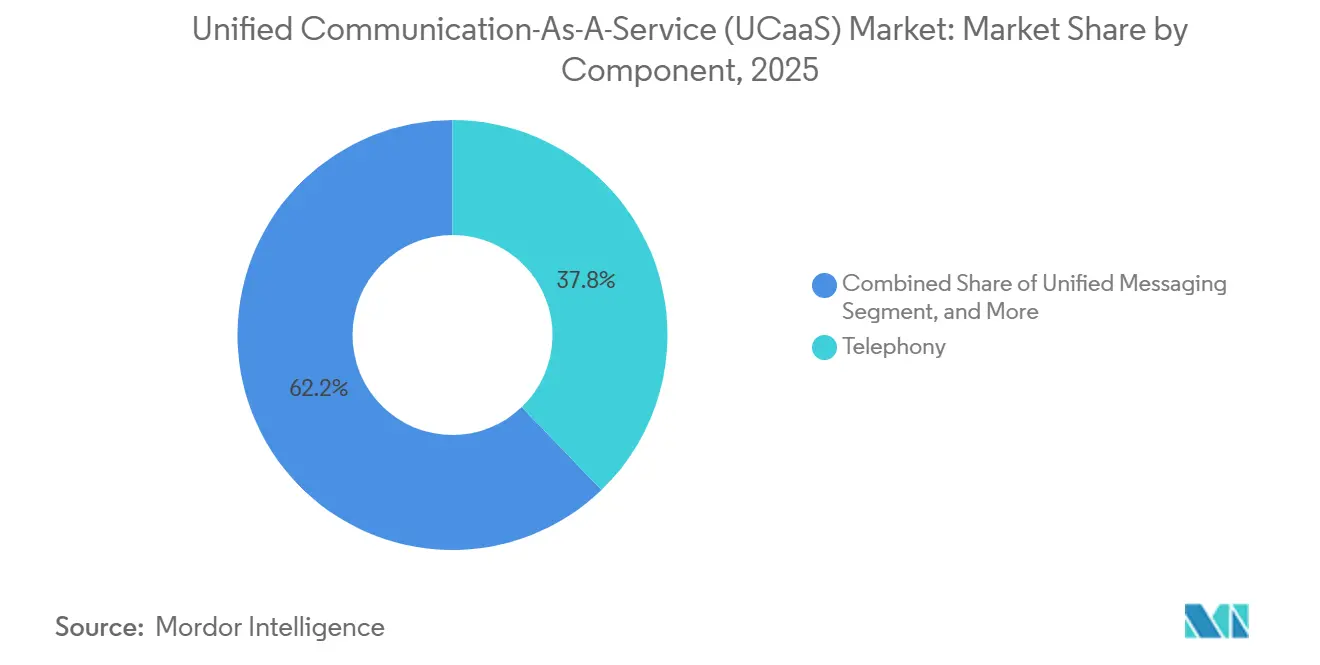

- By component, collaboration platforms held 27.11% of revenue growth potential in 2025 and are tracking a 27.11% CAGR through 2031, outpacing telephony’s 37.81% unified communication-as-a-service market share in the base year.

- By enterprise size, large firms commanded 63.14% revenue share in 2025, while SMEs are advancing at a 26.39% CAGR that narrows the adoption gap.

- By deployment model, public cloud captured 66.71% of the unified communication-as-a-service market size in 2025, yet hybrid architectures are expanding at 26.87% CAGR as regulated users maintain local voice gateways.

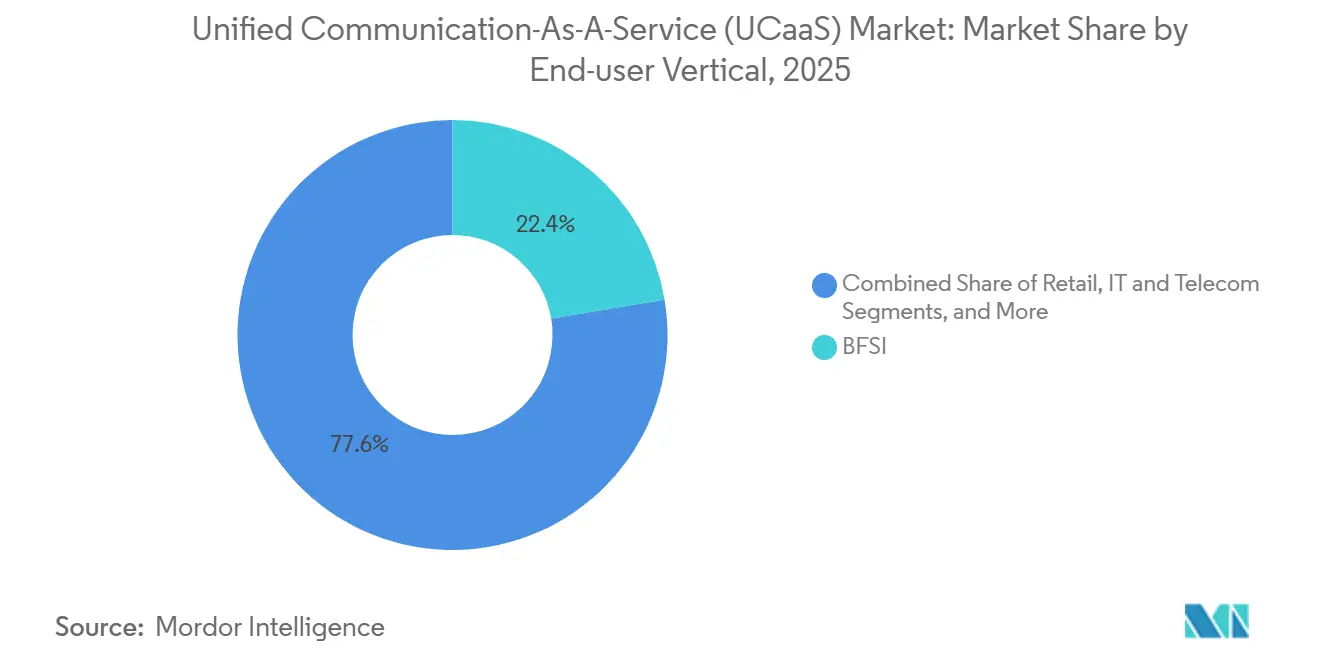

- By end-user vertical, BFSI led with 22.37% revenue share in 2025, whereas healthcare and life sciences register the fastest 27.86% CAGR to 2031.

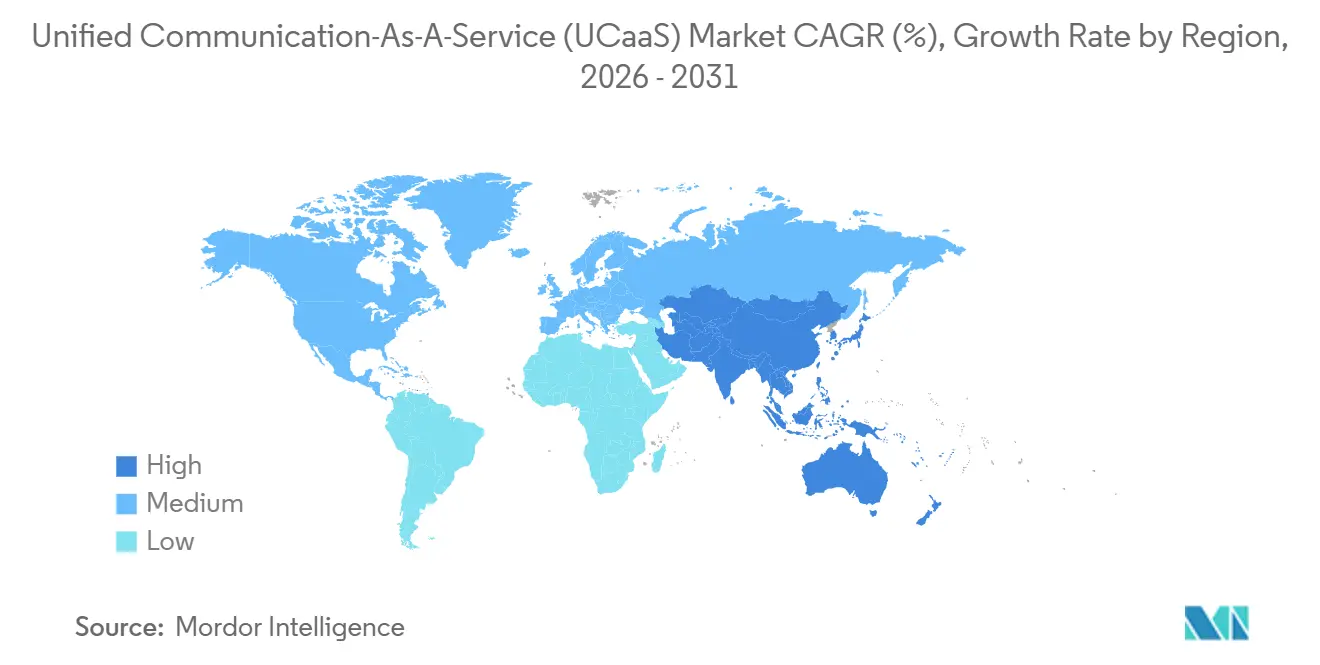

- By geography, North America generated 39.53% of global revenue in 2025, but Asia-Pacific is forecast to grow at 27.14% CAGR on the back of bring-your-own-carrier models.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Unified Communication-As-A-Service (UCaaS) Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Pay-as-you-go OPEX Model Attracts Cost-sensitive SMEs | +4.2% | Global, with pronounced uptake in Asia-Pacific and Latin America | Medium term (2-4 years) |

| Remote and Hybrid Work Policies Cement Work-from-anywhere Demand | +5.8% | Global, led by North America and Europe | Short term (≤ 2 years) |

| Integration of UCaaS with CCaaS and CPaaS Broadens Wallet-share | +3.9% | North America, Europe, and advanced Asia-Pacific markets | Medium term (2-4 years) |

| GenAI Copilots Personalize Real-time Communications for Frontline Staff | +4.6% | Global, early adoption in North America and Western Europe | Long term (≥ 4 years) |

| BYOC and Local Cloud Zones Overcome PSTN Licensing Barriers in Emerging Markets | +3.4% | Asia-Pacific, Middle East, and Africa | Medium term (2-4 years) |

| Edge-native UCaaS Lowers Latency for AR/VR Collaboration | +2.8% | North America, Japan, South Korea, and select European hubs | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Pay-As-You-Go OPEX Model Attracts Cost-Sensitive SMEs

Subscription pricing lowers the barrier to enterprise-grade communications. logged a 12% jump in average revenue per SME user in fiscal 2025 as clients upgraded to bundles with unlimited international calling and CRM plug-ins.[1]8x8 Fiscal 2025 Earnings Call, 8x8 Inc., 8x8.com Further, our preliminary research found that around 62% of CFOs prefer operating-expense IT models for balance-sheet agility. Because contracts run 12-36 months, SMEs can right-size quickly during downturns, which fuels churn but broadens addressable demand for the unified communication-as-a-service market.

Remote And Hybrid Work Policies Cement Work-From-Anywhere Demand

Permanent remote-work mandates mean unified communications have graduated from convenience to continuity. A 2025 Our preliminary research survey found that 68% of enterprises maintain formal work-from-anywhere rules, and 81% plan to grow seat counts at least 15% each year until 2028. Zoom reported 35% annual growth in Zoom Phone seats as customers consolidate video, chat, and voice.[2]Zoom Video Communications Inc. Form 10-K Fiscal Year 2025, sec.gov Because modern clients run on any device, firms spin up numbers in new countries without installing on-premises gear, radically compressing roll-out cycles.

Integration Of UCaaS With CCaaS And CPaaS Broadens Wallet Share

Customers are selecting single-vendor clouds that fuse employee collaboration with customer interaction. Cisco saw Webex Contact Center bookings leap 42% year-on-year in fiscal 2025 as firms sought unified voice, chat, and video histories. Programmable APIs enable banks to embed in-app support and healthcare providers to launch secure teleconsultations. PwC reports that 54% of IT leaders prioritize vendors that package CCaaS and CPaaS with UCaaS to curb total cost of ownership. This convergence enlarges contract sizes and speeds customer experience innovation.

GenAI Copilots Personalize Real-Time Communications For Frontline Staff

Generative AI is now embedded inside meeting clients, where it drafts recaps, sentiment scores, and follow-up tasks. Microsoft began offering these features inside Teams Premium in October 2025, estimating a 30% reduction in post-meeting administration.[3]Microsoft Teams Premium Announcement, Microsoft Corporation, microsoft.com RingCentral’s RingSense surfaces objections and discount prompts mid-call, trimming sales cycles by 18% during trials. IEEE research shows AI-assisted call routing can cut handle time by 22%.[4]AI-Assisted Call Routing Performance Study, IEEE, ieeexplore.ieee.org Such productivity gains reinforce platform stickiness and bolster unified communication-as-a-service market growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Skills Gap in Multi-vendor UC Stacks Prolongs Migration Cycles | -2.7% | Global, acute in regions with limited certified integrators | Medium term (2-4 years) |

| Rising Toll-fraud and SIP-trunk Security Breaches Inflate TCO | -3.1% | Global, with higher incidence in North America and Europe | Short term (≤ 2 years) |

| Voice-quality variance on public internet links | −1.9% | Rural and emerging markets most affected | Medium term (2-4 years) |

| National data sovereignty constraints | −2.1% | Europe and Asia-Pacific primarily | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Skills Gap In Multi-Vendor UC Stacks Prolongs Migration Cycles

Ernst and Young’s 2025 survey shows 47% of IT directors lack expertise in SIP trunking, SBC configuration, and quality-of-service tuning, delaying projects by an average eight months. Dual administration of cloud and legacy gear bloats labor costs, while scarcity of certified engineers pushes professional-services rates to USD 180-250 per hour in North America. Reliance on vendor-managed services reduces expected savings, a headwind to unified communication-as-a-service market adoption.

Rising Toll-Fraud And SIP-Trunk Security Breaches Inflate TCO

The U.S. FCC logged a 40% rise in toll-fraud incidents during 2025. Verizon’s breach report ranks UCaaS as the third most-targeted cloud asset, with 62% of cases involving stolen credentials. Firms must add call-detail monitoring, geo-blocking, and SBC intrusion detection, each layering cost and complexity onto what should be a streamlined cloud service.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Collaboration Platforms Outpace Legacy Telephony

Collaboration suites are expanding at 27.11% CAGR, eclipsing voice-only growth as knowledge workers favor persistent chat, shared files, and AI transcripts. Telephony retained 37.81% unified communication-as-a-service market share in 2025, yet its trajectory lags as organizations migrate call flows into all-in-one workspaces. Microsoft reported a 28% jump in Teams Rooms installations, underscoring hybrid-meeting momentum. Collaboration platforms integrate deeply with third-party apps, letting teams co-edit documents without leaving the interface, a capability that cements daily active use.

Telephony remains vital for high-volume voice operations in health scheduling and insurance claims. RingCentral noted that advanced voice controls still drove 42% of enterprise-tier subscriptions. Audio and video conferencing segments benefit from 4K cameras and noise suppression, while unified messaging sees revival as employees expect voicemail, SMS, and email in one inbox. The component mix signals that real-time voice endures, but value shifts toward multimodal, AI-enriched collaboration.

By Enterprise Size: SMEs Narrow The Adoption Gap

Large enterprises held 63.14% revenue in 2025, buoyed by global contracts and custom integrations. Yet SMEs register a 26.39% CAGR, drawn to self-service portals and mobile clients that erase hardware spend. Zoom disclosed that sub-500-employee accounts climbed to 38% of Zoom Phone bookings in fiscal 2025. This democratization broadens the unified communication-as-a-service market size among firms once priced out of sophisticated call management.

Conversely, large corporations still demand compliance recording, legal hold, and granular identity controls. AT&T added 12,000 enterprise seats for its RingCentral-powered Office at Hand during Q4 2025. SMEs prize rapid deployment, with 8x8 cutting average time-to-first-call to 4.2 hours. The feature gap is closing, though scale, geographic complexity, and SLA rigor keep procurement patterns divergent.

By End-User Vertical: Healthcare Leads Growth Amid Telemedicine Surge

Healthcare and life sciences exhibit a market-leading 27.86% CAGR as providers weave HIPAA-compliant video into patient portals. BFSI retained 22.37% revenue share in 2025 owing to high-volume advice and fraud-alert traffic. Retail integrates UCaaS with point-of-sale to escalate floor queries over video. Government agencies adopt FedRAMP clouds for hybrid work. Education sustains hybrid classrooms, with Zoom Rooms for Education revenue up 31% year-over-year.

The World Health Organization’s 2025 guidance on encrypted telehealth platforms catalyzes healthcare uptake. Financial advisors leverage AI summaries to satisfy record-keeping rules, evidencing how vertical regulations shape feature roadmaps and reinforce unified communication-as-a-service market differentiation.

By Deployment Model: Hybrid Configurations Gain Traction

Public cloud held 66.71% of unified communication-as-a-service market size in 2025, thanks to elastic scale and vendor-managed upgrades. Hybrid models, however, post a 26.87% CAGR, letting firms keep on-premises gateways for data residency and analog device support. Deutsche Telekom reported that 34% of clients chose its Collaboration Hub hybrid path. Public clouds capture greenfield deployments, while hybrid suits brownfield migrations and edge workloads like AR troubleshooting.

RingCentral notes 92% of its seats remain pure public, reflecting SME bias for simplicity. Private cloud persists in defense and healthcare circles needing physical control of call metadata. Cisco saw Webex Edge demand climb 26% as manufacturers process video locally to reduce latency. Deployment diversity signals that the unified communication-as-a-service market balances ease, compliance, and emerging edge intelligence.

Geography Analysis

North America generated 39.53% of 2025 revenue through mature enterprise penetration, dense fiber, and SIP trunk investments. The region’s unified communication-as-a-service market size will still expand steadily as AI features unlock upsell opportunities. Europe benefits from GDPR-compliant data centers in Frankfurt, Amsterdam, and Dublin, enabling multinationals to host traffic locally while supporting 24-language interfaces. Vendors with FedRAMP High or EU Cloud Code of Conduct seals win procurement preference, solidifying positions in government and regulated verticals.

Asia-Pacific is the fastest-growing territory at 27.14% CAGR. Bring-your-own-carrier strategies bypass stringent PSTN licensing in India and Indonesia. Telstra posted 19% UCaaS revenue growth in Australia and New Zealand, while NTT tallied 23% seat gains in Japan. Orange Business Services launched local cloud zones in 14 African states, underscoring sovereign-data trends. As regional data laws proliferate, providers that invest in in-country POPs unlock incremental volumes, enlarging the unified communication-as-a-service market share in emerging economies.

South America demonstrates accelerating uptake in Brazil and Argentina, where macro volatility nudges firms toward OPEX models. The Middle East and Africa trail but register healthy demand from tourism, energy, and public-sector digitization programs spearheaded by UAE and Saudi Vision 2030 initiatives. Overall, geographic expansion remains a crucial lever for vendors looking to surpass unified communication-as-a-service market averages.

Competitive Landscape

The unified communication-as-a-service market is moderately concentrated. The top five vendors Microsoft, RingCentral, Zoom, Cisco, and Verizon collectively control about 48% of 2025 revenue. Microsoft leverages Microsoft 365 bundling; Teams Phone attach among E5 users reached 62% in fiscal 2025. Pure plays emphasize openness, with Zoom and RingCentral exposing APIs and striking white-label carrier deals. Telecom incumbents such as BT and AT&T rebadge legacy voice into managed UCaaS, pairing carrier-grade SBCs with direct Teams routing, thereby attracting risk-averse firms that value guaranteed uptime.

Innovation focus is shifting to edge-native collaboration and AI-guided call handling. USPTO patent filings for AI routing climbed 34% in 2025. Gamma Communications expands across the United Kingdom and Netherlands through targeted acquisitions, proving that regional specialists can still carve profitable niches. Compliance depth remains a differentiator: vendors boasting FedRAMP, HIPAA, and PCI DSS credentials win higher-margin contracts in healthcare and finance. The playing field is therefore splitting between hyperscale suites that compete on breadth and specialists that compete on vertical finesse and regional intimacy.

Mergers and partnerships intensify overlap between UCaaS, CCaaS, and CPaaS, blurring competitive lines. Cisco’s purchase of a European SBC provider for USD 420 million will harden voice security for Webex customers. RingCentral works with Salesforce to embed voice into Service Cloud. Such moves broaden platform stickiness while expanding the unified communication-as-a-service industry footprint into adjacent workflows.

Unified Communication-As-A-Service (UCaaS) Industry Leaders

RingCentral Inc.

Microsoft Corp.

Zoom Video Communications Inc.

Cisco Systems Inc.

8x8 Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: AT&T and RingCentral inked a multi-year pact to co-develop vertical UCaaS solutions, starting with healthcare.

- August 2025: Verizon enhanced BlueJeans with AI meeting highlights and automated action items for North American customers.

- May 2025: RingCentral partnered with Salesforce to integrate video and telephony inside Service Cloud for seamless agent escalation.

- March 2024: Zoom launched Zoom Workplace, bundling meetings, phone, chat, and whiteboard at USD 25 per user and reporting 18% lower TCO for early adopters.

Global Unified Communication-As-A-Service (UCaaS) Market Report Scope

The Unified Communication-as-a-Service Market Report is Segmented by Component (Telephony, Unified Messaging, Audio/Video Conferencing, Collaboration Platforms), Enterprise Size (Small and Medium Enterprises, Large Enterprises), End-user Vertical (BFSI, Retail and e-Commerce, Healthcare and Life Sciences, Government and Public Sector, IT and Telecom, Education, Other End-user Verticals), Deployment Model (Public Cloud, Private Cloud, Hybrid), and Geography (North America, South America, Europe, Asia Pacific, Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

By Component

| Telephony |

| Unified Messaging |

| Audio / Video Conferencing |

| Collaboration Platforms |

By Enterprise Size

| Small and Medium Enterprises |

| Large Enterprises |

By End-user Vertical

| BFSI |

| Retail and e-Commerce |

| Healthcare and Life Sciences |

| Government and Public Sector |

| IT and Telecom |

| Education |

| Other End-user Verticals |

By Deployment Model

| Public Cloud |

| Private Cloud |

| Hybrid |

By Geography

| North America | United States | |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Switzerland | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Malaysia | ||

| Singapore | ||

| Vietnam | ||

| Indonesia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | Nigeria | |

| South Africa | ||

| Rest of Africa | ||

| By Component | Telephony | ||

| Unified Messaging | |||

| Audio / Video Conferencing | |||

| Collaboration Platforms | |||

| By Enterprise Size | Small and Medium Enterprises | ||

| Large Enterprises | |||

| By End-user Vertical | BFSI | ||

| Retail and e-Commerce | |||

| Healthcare and Life Sciences | |||

| Government and Public Sector | |||

| IT and Telecom | |||

| Education | |||

| Other End-user Verticals | |||

| By Deployment Model | Public Cloud | ||

| Private Cloud | |||

| Hybrid | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Switzerland | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Malaysia | |||

| Singapore | |||

| Vietnam | |||

| Indonesia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | Nigeria | ||

| South Africa | |||

| Rest of Africa | |||

Key Questions Answered in the Report

How large is the unified communication-as-a-service market in 2026?

The market stands at USD 70.56 billion in 2026 and is forecast to expand at a 25.67% CAGR through 2031.

Which component is growing fastest within unified communication-as-a-service?

Collaboration platforms are the most dynamic, tracking a 27.11% CAGR as firms bundle chat, file-sharing, and project management.

Why are SMEs accelerating adoption?

Pay-as-you-go pricing converts capital outlay into predictable OPEX, while self-service portals and mobile clients shorten deployment to hours, not weeks.

What regions show the strongest growth?

Asia Pacific posts the quickest pace at 27.14% CAGR, helped by bring-your-own-carrier models and local cloud zones that address data-sovereignty rules.

What security risks face UCaaS buyers?

Rising toll-fraud and SIP-trunk breaches inflate total cost of ownership, prompting firms to deploy geo-blocking, SBC intrusion detection, and multi-factor authentication.

Page last updated on: