Submarine Market Size and Share

Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Market Size (2026) | USD 14.14 Billion |

| Market Size (2031) | USD 25.06 Billion |

| Growth Rate (2026 - 2031) | 12.12% CAGR |

| Fastest Growing Market | Asia-Pacific |

| Largest Market | North America |

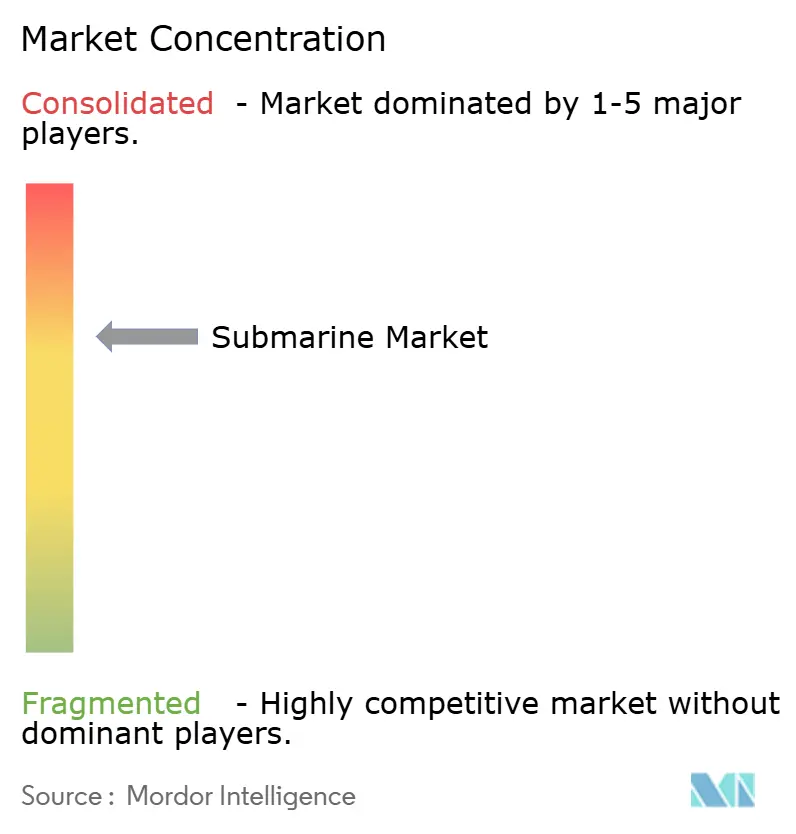

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Submarine Market Analysis by Mordor Intelligence

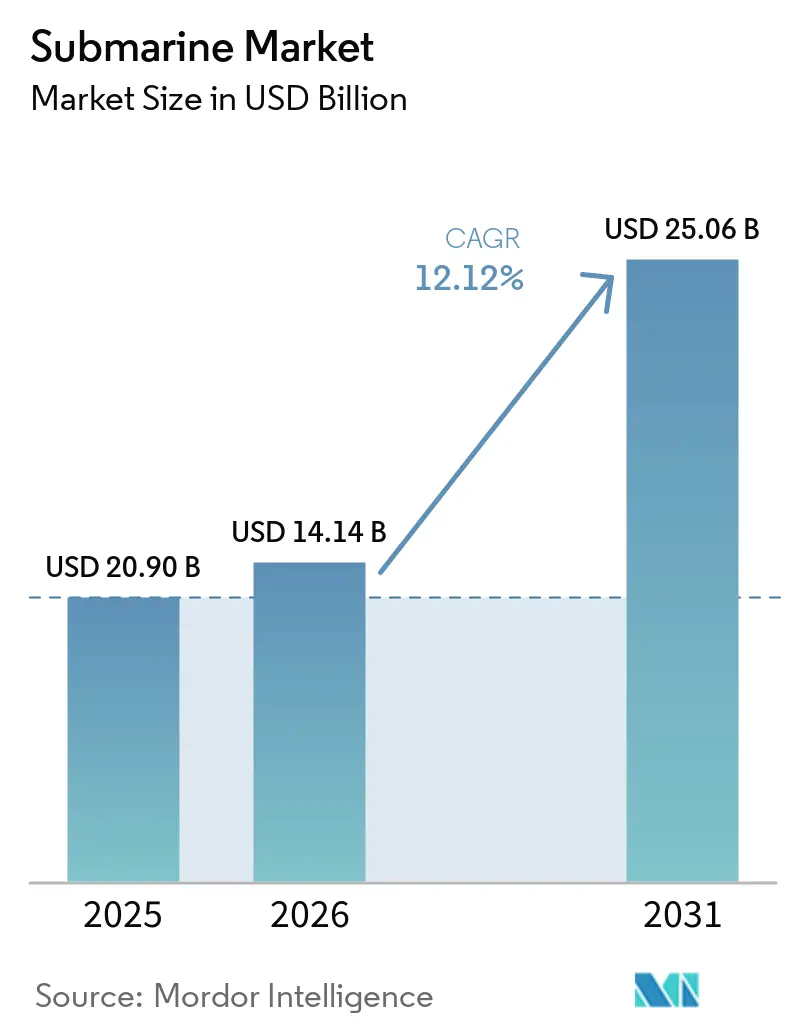

The submarine market size was valued at USD 20.90 billion in 2025 and is estimated to grow from USD 14.14 billion in 2026 to reach USD 25.06 billion by 2031, at a CAGR of 12.12% during the forecast period 2026-2031. The lower 2026 base reflects a procurement timing reset after several large multi-hull awards were concentrated in 2025, making the forward growth profile more useful than year-to-year declines for judging underlying demand. Growth is sustained by overlapping deterrence-renewal programs, broader conventional fleet expansion across the Indo-Pacific, and a rising policy focus on undersea infrastructure protection. The US alone requested USD 25.4 billion for submarine combatants in its FY2026 weapons acquisition plan, which shows how strongly major defense budgets are leaning toward undersea capability.[1]Office of the Under Secretary of Defense, “Program Acquisition Cost by Weapon System, United States Department of Defense Fiscal Year 2026 Budget Request,” United States Department of Defense, comptroller.war.gov Parallel replacement cycles, including the Columbia-class in the US, the Barracuda-class in France, and the Type 212CD in Northern Europe, are creating a long procurement pipeline that extends into the next decade. The strategic case is also widening beyond classic deterrence and sea-denial missions because subsea cable security is now treated as a critical infrastructure risk by policy institutions, which supports surveillance and patrol demand alongside combat demand.

Key Report Takeaways

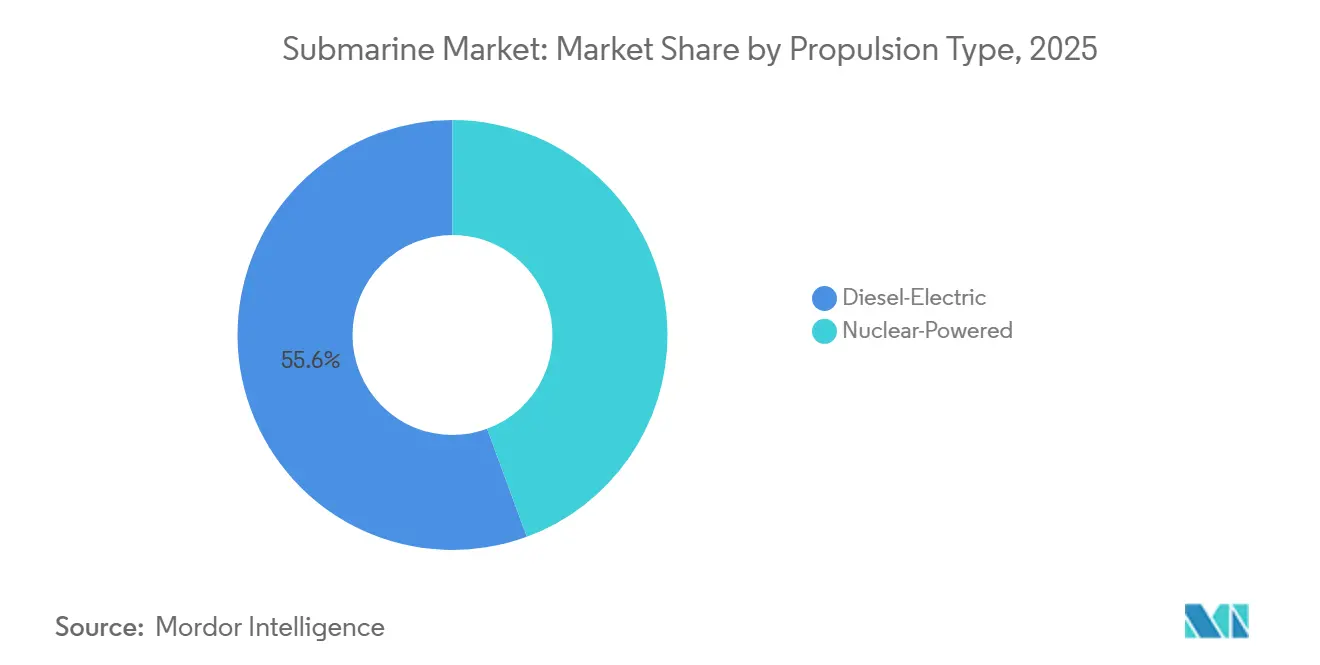

- By propulsion type, diesel-electric submarines held 55.62% of the submarine market share in 2025, while nuclear-powered submarines are projected to expand at a 14.21% CAGR through 2031.

- By combat role, attack submarines accounted for 48.70% of the submarine market size in 2025, while ballistic-missile submarines are forecast to grow at 13.13% CAGR through 2031.

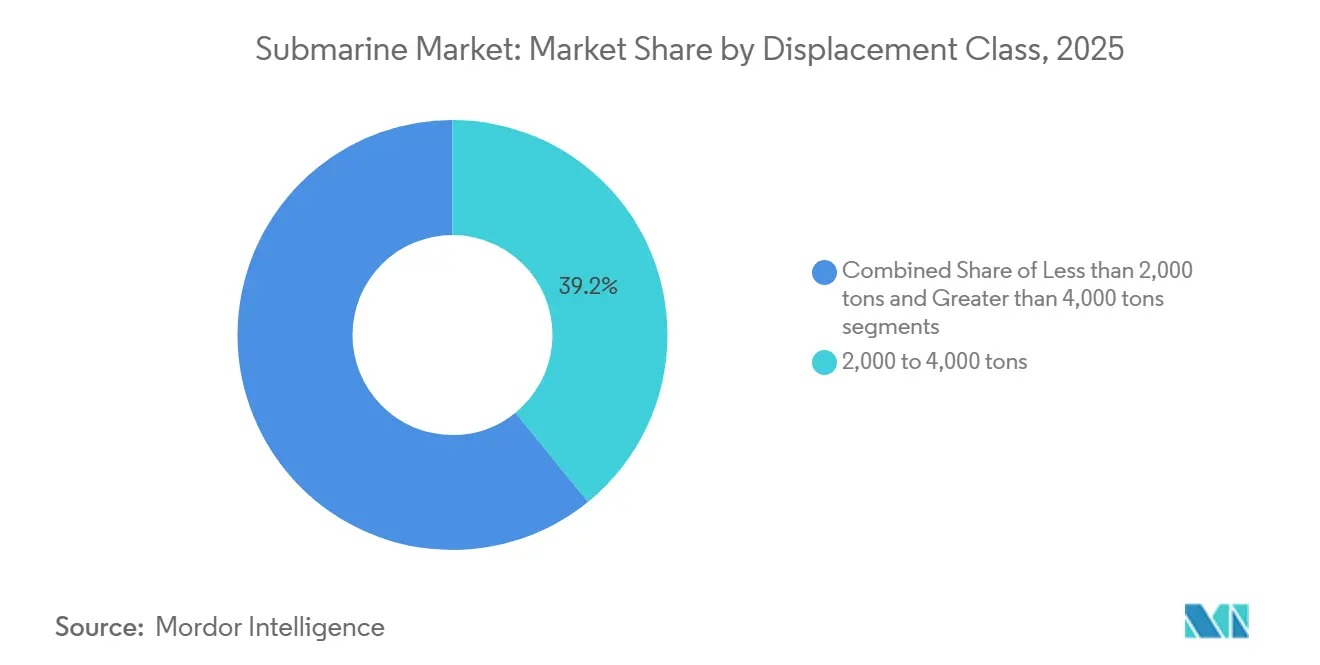

- By displacement class, the 2,000 to 4,000-ton range commanded 39.15% of the submarine market size in 2025, while the more than 4,000-ton class is projected to advance at 12.91% CAGR through 2031.

- By component, hull and structural modules led with 37.64% revenue share in 2025, while combat and sensor suites are forecast to record the highest CAGR of 14.01% through 2031.

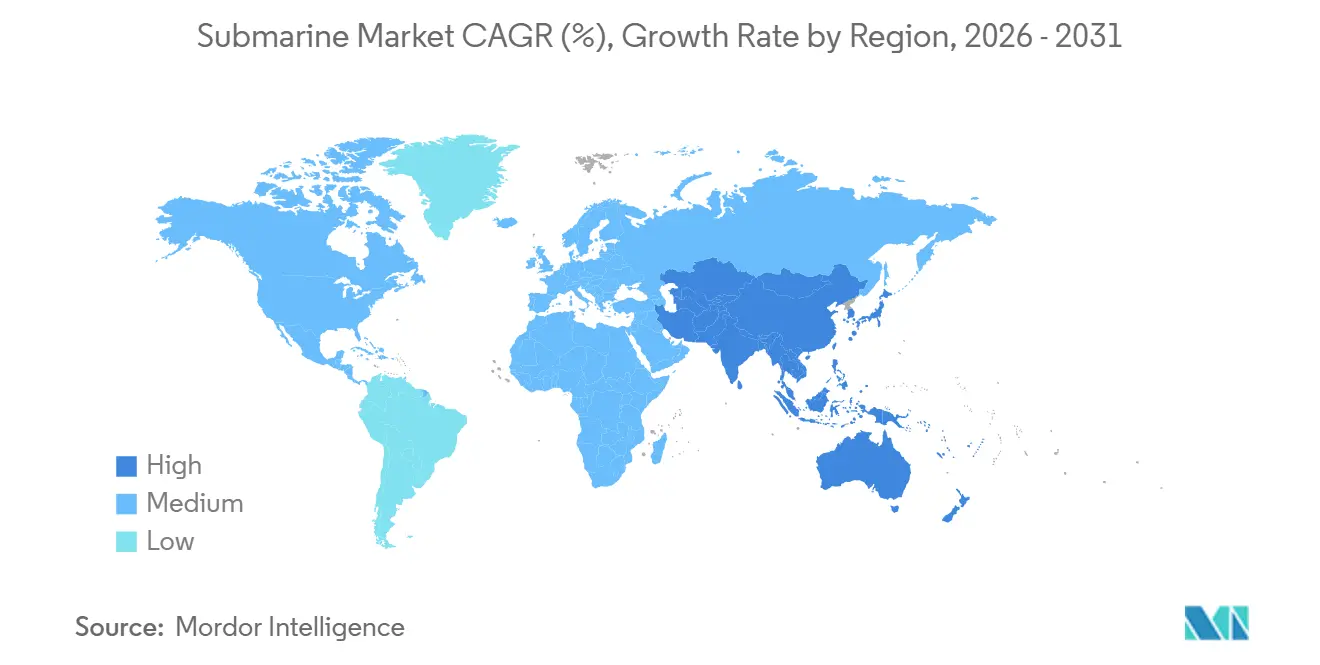

- By geography, North America captured 36.05% of the submarine market share in 2025, while Asia-Pacific is projected to expand at a 13.76% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Submarine Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising defense-modernization budgets among Tier-1 navies | +3.2% | Global, concentrated in North America and Europe | Medium term (2-4 years) |

| Escalating Indo-Pacific maritime tensions | +2.8% | APAC core, spill-over to MEA | Medium term (2-4 years) |

| Fleet-replacement cycles in legacy nuclear operators | +2.1% | North America, Europe | Long term (≥ 4 years) |

| Adoption of AIP and Li-ion batteries extending submerged endurance | +1.5% | Global, early gains in APAC and Europe | Medium term (2-4 years) |

| AUKUS pact triggering allied fleet expansion | +1.4% | North America, APAC, Australia | Long term (≥ 4 years) |

| Need to secure subsea data-cable infrastructure | +0.8% | North Atlantic, Indo-Pacific, Baltic Sea | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Defense Modernization Budgets Catalyze Submarine Procurement

The submarine market is benefiting from defense budget growth directed toward platforms with strategic persistence, survivability, and deterrence value. The US FY2026 Department of Defense (DoD) budget requested USD 12.2 billion for Virginia-class boats and USD 11.5 billion for Columbia-class boats.[2]Office of the Under Secretary of Defense, “Program Acquisition Cost by Weapon System, United States Department of Defense Fiscal Year 2026 Budget Request,” United States Department of Defense, comptroller.war.gov Northern Europe is also reinforcing the order book, with Norway raising its Type 212CD order to 6 boats under a NOK 46 billion (USD 4.5 billion) package, bringing the combined German-Norwegian program to 12 boats. The demand cycle is stronger than in the 2010s because nuclear recapitalization and conventional procurement are moving together rather than replacing one another in a staggered fashion. That overlap means authorizations are reaching shipyards faster than physical capacity is expanding, which delays recognition into later years, even when budgets have already been approved. In practical terms, the submarine market is being pushed upward by funding certainty, but the pace of realized revenue still depends on how quickly certified yards and suppliers can absorb that workload.

Escalating Indo-Pacific Maritime Tensions Drive Multi-Country Procurement

The submarine market is also being widened by a larger buyer base across the Indo-Pacific, where procurement is no longer limited to a few established operators. Tensions in the region are pushing more navies to treat submarines as central tools for sea denial, maritime surveillance, chokepoint control, and deterrence signaling. This shift matters because it expands demand beyond a handful of Tier-1 navies and creates overlapping acquisition schedules across China, India, Japan, South Korea, Australia, and Pakistan. The result is not only greater hull demand but also greater competition over technology transfer, local production, and combat-system integration. The procurement pattern is therefore becoming broader and less cyclical, which gives the submarine market a stronger demand base than one driven only by traditional nuclear operators. It also means future awards are more likely to be shaped by regional security alignment, industrial offsets, and delivery reliability rather than by platform performance alone.

AUKUS Pact Reshapes Allied Fleet Architecture and Supplier Roles

AUKUS is reshaping the submarine market, as the pact affects not just Australian demand but also supplier roles across the US, the UK, and allied industrial networks. Lockheed Martin Corporation was selected in May 2026 as the preferred combat system integration partner for Australia's future nuclear submarine fleet, covering integration, training, sustainment, and sovereign combat-system capability.[3]“Lockheed Martin Named Preferred Combat System Integration Partner for Australia's Next-Generation Nuclear Subs,” Lockheed Martin, news.lockheedmartin.com That selection shows that AUKUS is already moving from policy design into practical industrial allocation, with combat systems, training pipelines, and sustainment capability being assigned early. The strategic effect is larger than the boat count because AUKUS ties long-cycle submarine demand to a shared industrial architecture that will influence design choices, supplier access, and export viability for years to come. It also puts additional pressure on Western production schedules because the same industrial base must support domestic fleet needs, allied commitments, and future transfer arrangements. For the submarine market, AUKUS is therefore both a demand accelerator and a capacity stress test.

AIP and Li-Ion Batteries Redefine The Diesel-Electric Submarine's Combat Value

The submarine market is gaining support from improvements in air-independent propulsion (AIP) and lithium-ion (Li-ion) battery systems, which extend submerged endurance and reduce exposure during patrols, changing the value proposition of advanced conventional boats in regional missions, especially in littoral waters and contested chokepoints where endurance, quieting, and ambush posture matter more than global transit range. As these systems mature, the operating gap between high-end diesel-electric boats and nuclear boats narrows in specific mission sets, which strengthens the commercial case for advanced conventional procurement. That matters to navies that want credible undersea capability without the industrial, political, and financial burden of nuclear propulsion. It also supports deeper investment in batteries, fuel cells, power management, and low-signature systems rather than solely on the hull. In the submarine market, this technology shift helps preserve the revenue lead of diesel-electric platforms even while nuclear programs expand faster in value terms.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ultra-high acquisition and lifecycle costs | -1.8% | Global, most acute in North America and Western Europe | Long term (≥ 4 years) |

| Skilled labor bottlenecks in submarine yards | -1.4% | North America, Western Europe | Medium term (2-4 years) |

| Arms-control and nuclear-proliferation treaties | -0.8% | Global | Long term (≥ 4 years) |

| Supply-chain scarcity of marinized semiconductors | -0.7% | Global, concentrated in North America and East Asia | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Ultra-High Acquisition and Lifecycle Costs Cap Order Throughput

The submarine market remains constrained by the simple fact that modern submarine programs absorb a very large share of naval capital budgets. Congressional Research Service data placed the FY2026 Virginia-class procurement cost at USD 5 billion per boat, making it difficult to scale fleet plans even for major naval powers. The Congressional Budget Office estimated the Columbia-class program at USD 130 billion for 12 submarines and also projected higher long-run submarine spending pressure across the Navy's shipbuilding plan. This cost burden forces many navies to make hard tradeoffs between new builds, sustainment, missiles, and workforce support. In the submarine market, demand is real and strategic urgency is high, but order throughput still depends on what governments can fund over the full program life rather than at contract signing.

Skilled Labor Bottlenecks Constrain Western Build Rates

The submarine market is also limited by a shortage of qualified labor across nuclear-certified and high-precision production lines. Congressional Research Service data showed that Virginia-class production averaged 1.1 boats per year by November 2024, against a target of 2 boats per year, highlighting the gap between desired output and actual delivery capacity. The same source noted that the Navy has committed USD 9.8 billion to submarine industrial base development since FY2018, confirming that capacity growth is now a strategic policy issue rather than a plant-level problem. The Congressional Budget Office also described a supplier base with limited redundancy, where many critical inputs have no alternative source, and schedule slippage can spread quickly through the build sequence. Labor shortages matter beyond the US because submarine work depends on specialist welding, quality assurance, reactor-related processes, combat-system integration, and long apprenticeship cycles. The submarine market, therefore, faces a clear mismatch between rising demand and the time required to develop a workforce capable of safely executing these programs at scale.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Propulsion Type: Conventional Platforms Hold The Revenue Lead While Nuclear Programs Expand Faster

Diesel-electric submarines accounted for 55.62% of the submarine market in 2025, keeping conventional propulsion as the largest revenue pool. That leadership reflects the broader number of active buyers across Asia-Pacific, Europe, and selected South American fleets, where conventional boats fit both budget limits and operating requirements. The segment benefits from mission flexibility, as these submarines are well-suited for coastal defense, chokepoint control, intelligence patrols, and special-forces insertion. The submarine market, therefore, still relies on conventional procurement for its volume base even as more attention shifts to nuclear recapitalization. This balance also explains why conventional programs remain commercially important for yards that do not participate in nuclear construction.

Nuclear-powered submarines are projected to grow at a 14.21% CAGR through 2031, making them the fastest-growing propulsion segment by value. Growth is being driven by high-ticket SSBN and SSN programs, where each boat carries a contract value much larger than that of a diesel-electric unit. In the submarine industry, this creates a two-speed structure in which conventional orders support breadth while nuclear awards drive value concentration. The technology gap is also becoming less pronounced as better batteries and AIP systems improve the endurance and combat relevance of advanced conventional boats. Within the submarine market, that means conventional propulsion should continue to hold the largest share, while nuclear propulsion captures a rising share of spending growth.

By Combat Role: Attack Boats Lead Current Demand While Deterrence Boats Gain Momentum

Attack submarines accounted for 48.70% of the submarine market size in 2025, supported by the large number of SSN and SSK programs now moving through procurement and delivery. Their lead reflects operational utility, as navies use attack boats for anti-surface warfare (ASuW), anti-submarine warfare (ASW), intelligence gathering, escort duties, and regional sea-denial missions. These boats also align with the broadest customer set, from advanced nuclear navies to countries buying diesel-electric fleets for national waters. The submarine market continues to rely on this role for installed fleet depth, as attack boats meet both peacetime and wartime requirements. That wide mission profile keeps the segment structurally resilient even when procurement timing shifts between programs.

Ballistic-missile submarines are forecast to expand at 13.13% CAGR through 2031, making them the fastest-growing combat role in value terms. Growth is tied to overlapping recapitalization cycles among nuclear-armed states, which is unusual because several deterrent fleets are being renewed within the same broad time window. The UK's Dreadnought program remains a great and sustained effort, with the House of Commons Library noting its scale and long delivery horizon. In the submarine industry, that overlap creates a concentrated wave of capital spending on a small number of very high-value platforms. For the submarine market, the result is a role mix in which attack boats lead on current revenue breadth while SSBNs drive the sharpest long-run value expansion.

By Displacement Class: Mid-Sized Boats Anchor Volumes While Heavy Platforms Lift Spending

The 2,000 to 4,000-ton displacement class accounted for 39.15% of revenue in 2025, reflecting the central role of medium-displacement boats in active procurement programs. This class serves the most common operating profile because it balances endurance, payload, crew size, and deployability without moving into the cost structure of large nuclear boats. It is especially relevant for navies focused on littoral surveillance, choke-point denial, and regional response missions. The submarine market has a stable baseline in this class because many export and alliance-aligned programs sit in this middle band. Boats below 2,000 tons remain relevant for smaller navies, but their contribution remains limited by narrower capabilities and lower contract values.

The more than 4,000-ton segment is projected to grow at 12.91% CAGR through 2031, driven by large nuclear platforms and selected heavyweight conventional programs. Growth here comes from the scale of SSN and SSBN construction, where boat size rises alongside payload, reactor integration, missile capacity, and endurance requirements. This tier pulls in the largest development budgets, the most demanding industrial work, and the greatest concentration of value per unit. In the submarine market, heavy-displacement growth reinforces the value concentration already visible at the nuclear end of the spectrum. That trend does not displace mid-sized boats in volume, but it does shift spending weight toward a smaller number of large strategic platforms.

By Component: Structural Work Leads Current Revenue While Combat Electronics Grow Fastest

Hull and structural modules accounted for 37.64% of component revenue in 2025, making them the largest cost center in current platform construction. Pressure hull sections, modular structures, ballast architecture, and integration-heavy fabrication work still account for a large share of build value across most submarine types. This part of the submarine market remains labor-intensive and schedule-sensitive because structural work sits at the core of the production sequence. It also benefits directly from any increase in boat count, regardless of whether the order is conventional or nuclear. For that reason, structural modules continue to anchor the revenue profile of the component mix.

Combat and sensor suites are forecast to grow at a 14.01% CAGR through 2031, making them the fastest-expanding component group. The shift reflects rising spending on combat management systems, sonar, electronic warfare (EW), target classification, and other mission electronics that can materially raise boat effectiveness before hull numbers increase. Within the submarine industry, this is an important change because differentiation is moving toward software, processing, and detection performance rather than resting only on platform architecture. It also means retrofit and upgrade demand can expand even when full new-build programs move more slowly. Across the submarine market, electronics are therefore taking a larger share of value as operators prioritize survivability, situational awareness, and the quality of weapons employment.

Geography Analysis

North America accounted for 36.05% of the submarine market in 2025, making it the largest regional contributor to revenue. The region's position rests mainly on US procurement scale, long-cycle SSN and SSBN recapitalization, and sustained industrial-base funding. Congressional Research Service and CBO data together show that the US is committing large resources to submarine construction while still facing schedule pressure, supplier concentration, and workforce limits. Canada adds a meaningful future demand layer through the Canadian Patrol Submarine Project, where the government advanced the procurement process in August 2025.[4]“Government of Canada Advances to Next Step in Canadian Patrol Submarine Project Procurement,” Government of Canada, canada.ca In the submarine market, North America combines the largest order values with the clearest evidence that industrial capacity is becoming a strategic constraint rather than a temporary execution issue.

Asia-Pacific is the fastest-growing region, with the submarine market expected to advance at 13.76% CAGR through 2031. Growth comes from simultaneous procurement and fleet expansion across China, India, Japan, South Korea, and Australia, giving the region an unmatched breadth of demand. The strategic environment is pushing countries to pursue a mix of indigenous development, foreign collaboration, and technology-transfer frameworks. That broadens the submarine market because the region is not growing from one national program alone, but from several large programs moving in parallel. It also increases competition among suppliers because each buyer assigns different weights to local construction, political alignment, delivery speed, and long-term sustainment.

Europe held a meaningful share of revenue in 2025 and remains one of the most program-dense regions in the submarine market. Germany and Norway expanded the 212CD program to 12 boats in total, while German shipyards have received federal support for upgrades to production capacity. Europe also shows how the submarine market can combine sovereign demand with export ambition, as several regional yards compete abroad while serving domestic naval programs. South America remains smaller in current value terms, but Brazil gives the region a visible long-horizon role through its conventional buildout and nuclear ambition. The Middle East and Africa still represent a modest share, yet infrastructure security concerns and regional naval modernization are supporting incremental interest in undersea capability.

Competitive Landscape

The submarine market is moderately concentrated at the top because only a small group of certified yards can design and build nuclear-powered submarines. That structure assigns the highest value to state-backed or state-linked industrial ecosystems with deep regulatory clearance, a long operating history, and a dense supplier network. Barriers remain high because submarine work requires specialized facilities, trusted labor pools, complex quality systems, and long validation cycles. In the submarine market, this protects incumbent yards and limits new entry at the nuclear tier. The competitive picture is more open in conventional boats, where more shipbuilders can compete on AIP, batteries, combat systems, local assembly, and export packages.

The submarine market is becoming more competitive in the diesel-electric segment, as multiple builders compete simultaneously for the same international tenders. TKMS remains a strong force in medium-displacement AIP platforms and continues to deepen relationships through orders and negotiation pipelines, including its September 2025 move into formal Project-75I contract negotiations with Mazagon Dock Shipbuilders in India.[5]“Milestone in Indian Submarine Program, TKMS Enters Contract Negotiations with Mazagon Dock Shipbuilders, MDL, for P75I Program,” TKMS Group, tkmsgroup.com Saab strengthened its position when Poland selected the A26 for the Orka program, and Saab also received an added SEK 9.6 billion (USD 1.03 billion) order for the final production phase of two Blekinge-class submarines in October 2025. These moves show that competition in the submarine market now depends on full-package offers rather than on hull design alone.

Technology transfer, sovereign production, and systems integration are becoming the clearest differentiators in the submarine market. TKMS also expanded its value chain position through a framework agreement with Atlas Elektronik for DM2A5 heavyweight torpedoes for the 212CD fleet, tying platform sales to weapons integration and lifecycle relevance. Compliance remains another filter because export-control rules, non-proliferation safeguards, and alliance standards shape which supplier-buyer combinations can realistically close. The submarine market, therefore, rewards companies that can pair platform capability with policy alignment, industrial cooperation, and credible long-term support. That is why the competitive field appears concentrated in strategic platforms but still dynamic in advanced conventional and mission-system packages.

Submarine Industry Leaders

Naval Group

General Dynamics Mission Systems, Inc. (General Dynamics Corporation)

HD Hyundai Heavy Industries Co. Ltd.

thyssenkrupp Marine Systems GmbH (thyssenkrupp AG)

Huntington Ingalls Industries, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2026: Mazagon Dock Shipbuilders Limited (MDL) concluded cost negotiations with Germany’s Thyssenkrupp Marine Systems (TKMS) for the INR 99,000 crore (USD 10.28 billion) Project 75(I) submarine program. This agreement positions MDL to construct six advanced diesel-electric attack submarines equipped with fuel-cell-based AIP technology.

- April 2026: The US DoD awarded an AUD 276 million (USD 197 million) contract to support Australia's nuclear submarine acquisition plans. This contract is intended to support the AUKUS security pact involving Australia, the US, and the UK.

- January 2026: The Norwegian government approved the procurement of two additional Class 212CD submarines. Following the official signing of the contract, TKMS received a significant order extension under the ongoing 212CD program, marking one of the largest orders in the company's history. This decision increases the total number of submarines planned for the Royal Norwegian Navy from four to six.

Global Submarine Market Report Scope

A submarine is a vessel designed for autonomous underwater operation, distinguishing it from submersibles, which have more limited underwater capabilities. Submarines also encompass remotely operated vehicles and vessels of medium or smaller sizes.

The submarine market is segmented by propulsion type, combat role, displacement class, component, and geography. By propulsion type, the market is classified into nuclear-powered submarines and diesel-electric submarines. By combat role, the market is segmented into attack, ballistic missile, and guided missile. By displacement class, the market is segmented into less than 2,000 tons, 2,000 to 4,000 tons, and greater than 4,000 tons. By component, the market is classified into hull and structural modules, propulsion systems, combat and sensor suites, and energy storage (batteries, AIP). The report also covers the market sizes and forecasts for the submarine market in major countries across different regions. For each segment, the market size is provided in terms of value (USD).

| Nuclear-Powered |

| Diesel-Electric (Conventional and AIP) |

| Attack (SSN/SSK) |

| Ballistic-Missile (SSBN) |

| Guided-Missile (SSGN) |

| Less than 2,000 tons |

| 2,000 to 4,000 tons |

| Greater than 4,000 tons |

| Hull and Structural Modules |

| Propulsion Systems |

| Combat and Sensor Suites |

| Energy Storage (Batteries, AIP) |

| North America | United States | |

| Canada | ||

| Europe | United Kingdom | |

| France | ||

| Germany | ||

| Rest of Europe | ||

| South America | Brazil | |

| Rest of South America | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Israel |

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| By Propulsion Type | Nuclear-Powered | ||

| Diesel-Electric (Conventional and AIP) | |||

| By Combat Role | Attack (SSN/SSK) | ||

| Ballistic-Missile (SSBN) | |||

| Guided-Missile (SSGN) | |||

| By Displacement Class | Less than 2,000 tons | ||

| 2,000 to 4,000 tons | |||

| Greater than 4,000 tons | |||

| By Component | Hull and Structural Modules | ||

| Propulsion Systems | |||

| Combat and Sensor Suites | |||

| Energy Storage (Batteries, AIP) | |||

| By Geography | North America | United States | |

| Canada | |||

| Europe | United Kingdom | ||

| France | |||

| Germany | |||

| Rest of Europe | |||

| South America | Brazil | ||

| Rest of South America | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Israel | |

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

Key Questions Answered in the Report

What is the current size of the submarine market and where is it headed by 2031?

The submarine market was valued at USD 20.90 billion in 2025 and is forecast to reach USD 25.06 billion by 2031, with growth projected at 12.12% CAGR over 2026-2031.

Why does the 2026 base look lower than the 2025 value?

The lower 2026 base reflects a procurement timing reset after several large multi-hull contracts were concentrated into 2025, rather than a structural fall in long-term demand.

Which propulsion segment leads revenue today?

Diesel-electric submarines led revenue in 2025 with a 55.62% share, supported by a broader buyer base across Asia-Pacific, Europe, and selected South American fleets.

Which part of the business is growing fastest by component?

Combat and sensor suites are projected to grow fastest at 14.01% CAGR through 2031 as navies increase spending on combat management systems, sonar, and EW.

Which region is growing fastest through the forecast period?

Asia-Pacific is forecast to grow fastest at 13.76% CAGR, supported by simultaneous fleet expansion across China, India, Japan, South Korea, and Australia.

What is the main bottleneck limiting delivery growth?

Industrial capacity remains the main constraint, especially skilled labor, supplier concentration, and the slower-than-target build rate at Western yards, even though budgets and demand remain strong.

Page last updated on: