Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

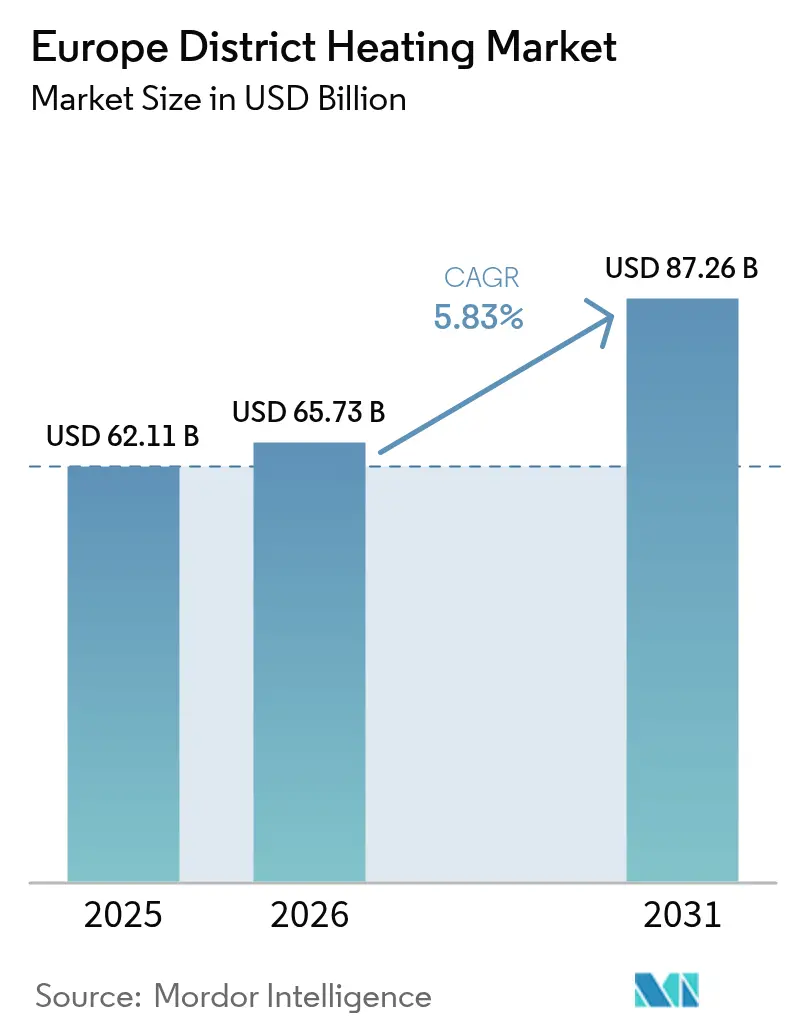

| Base Year Market Size (2025) | USD 62.11 Billion |

| Market Size (2026) | USD 65.73 Billion |

| Market Size (2031) | USD 87.26 Billion |

| Growth Rate (2026 - 2031) | 5.83% CAGR |

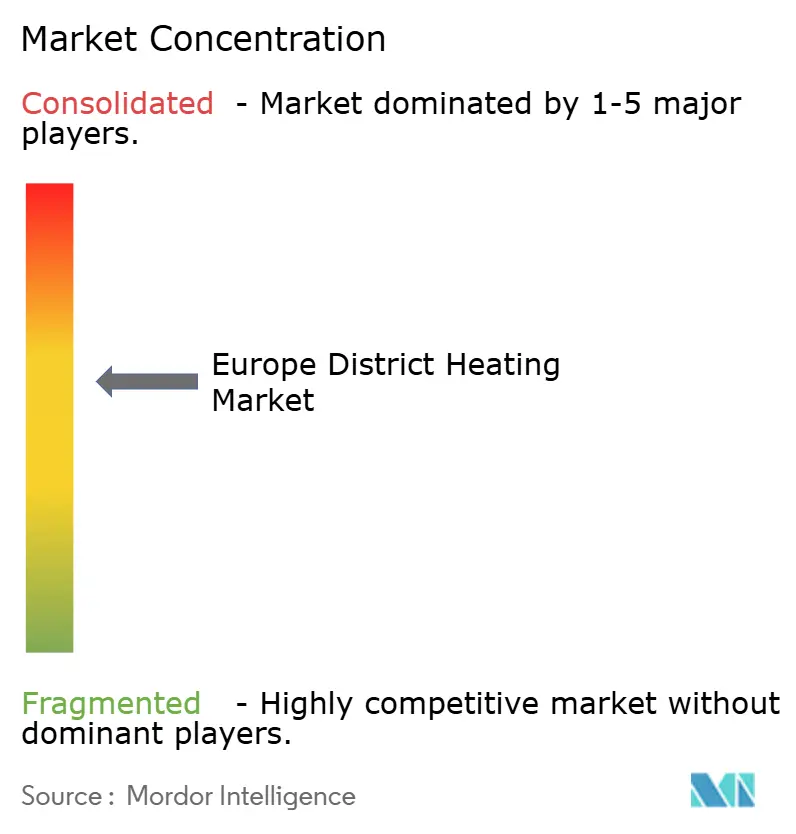

| Market Concentration | Medium |

Major Players*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Europe District Heating Market Analysis by Mordor Intelligence

European district heating market size in 2026 is estimated at USD 65.73 billion, growing from 2025 value of USD 62.11 billion with 2031 projections showing USD 87.26 billion, growing at 5.83% CAGR over 2026-2031. The expansion reflects regulatory mandates that prioritize rapid decarbonization of building‐level heat, rising energy prices that sharpen the competitiveness of network solutions, and the accelerating integration of renewables into legacy distribution grids. Mandatory boiler phase-outs in Germany and the Netherlands, green bond–backed municipal financing, and the growing monetization of data-center waste heat are set to redefine supply-side economics across most urban hubs. Simultaneously, large-scale heat-pump deployment, improved pipe materials, and digital optimization platforms are reducing lifecycle costs, enabling utilities to scale while maintaining stable tariffs. Competitive intensity is rising in Nordic markets, where next-generation low-temperature schemes are gaining dominance, and it is expanding to Central and Southern Europe as new concession tenders are announced.

Key Report Takeaways

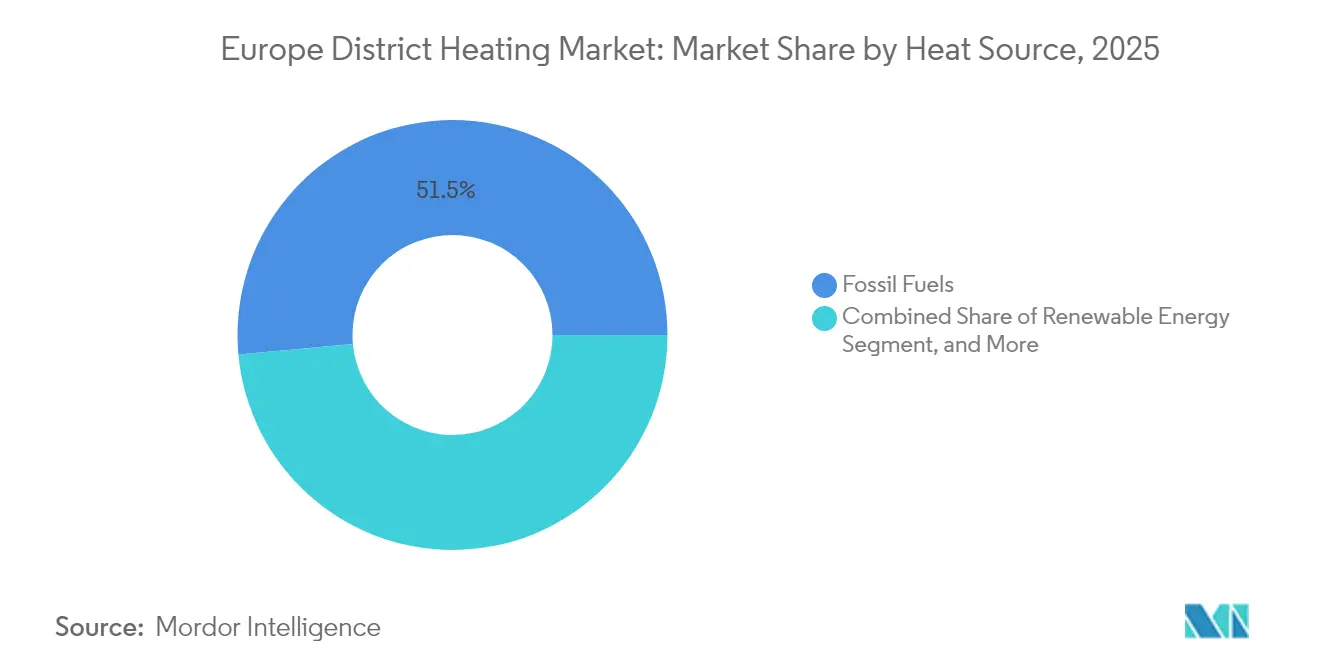

- By heat source, fossil fuels led with a 51.45% share of Europe's district heating market in 2025, while renewables recorded the fastest growth rate of 10.8% CAGR through 2031.

- By plant type, combined heat and power held a 56.75% share of the European district heating market size in 2025; large-scale heat pumps are forecast to grow at a 14.05% CAGR to 2031.

- By network temperature, 3rd-generation systems captured a 60.35% share of the European district heating market in 2025, whereas 5th-generation networks are expected to expand at a 16.9% CAGR through 2031.

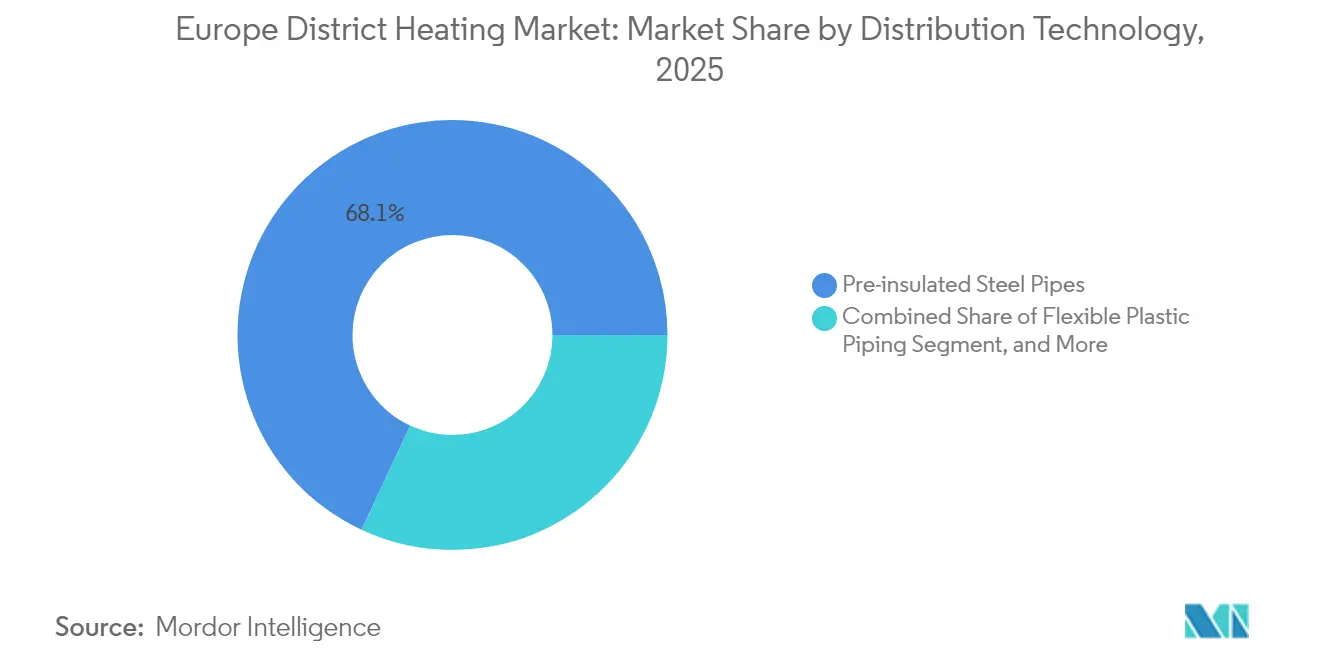

- By distribution technology, pre-insulated steel pipes commanded 68.05% share of the European district heating market in 2025; flexible plastic piping advances most rapidly at 11.85% CAGR.

- By end user, the residential sector accounted for a 46.05% share of the European district heating market in 2025; public and institutional users posted the highest 8.75% CAGR from 2025 to 2031.

- By country, Germany accounted for 23.55% of the European district heating market in 2025, with Nordic states displaying penetration rates above 50% in residential heating.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Europe District Heating Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid build-out of 4th-generation low-temperature networks in Scandinavia | +1.20% | Nordic countries, spill-over to Central Europe | Medium term (2-4 years) |

| Mandatory phase-out of individual gas boilers in Germany and Netherlands | +1.80% | Germany, Netherlands, expanding EU-wide | Short term (≤ 2 years) |

| EU Carbon Border Adjustment Mechanism accelerating industrial switching | +0.90% | EU-wide, strongest in industrial clusters | Medium term (2-4 years) |

| Surging data-center waste-heat recovery contracts in Northern Europe | +0.70% | Nordic countries, extending to Western Europe | Long term (≥ 4 years) |

| District cooling synergies in Southern Europe’s urban redevelopments | +0.60% | Southern Europe, Mediterranean cities | Long term (≥ 4 years) |

| Green-bond financing windows driving municipal network expansions | +0.50% | EU-wide, high-credit municipalities | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rapid Build-out of 4th-Gen Low-Temperature Networks in Scandinavia

Scandinavian utilities are standardizing 4th-generation networks that operate 20–45 °C below legacy systems, reducing distribution losses by up to 30% and enabling the cost-effective use of ambient and waste-heat resources. Projects such as Lund’s Cool DH and Sweden’s SEK 18 billion EcoDataCenter 2 combine large-scale heat pumps (COP > 4.0) with recycled industrial heat, slashing fuel costs while creating anchor loads for future grid extensions. Nordic design codes now form the basis of EU technical specifications, accelerating technology transfer into Central Europe.

Mandatory Phase-out of Individual Gas Boilers in Germany and Netherlands

Germany's Building Energy Act obliges new heating systems to source 65% renewable energy from 2024, effectively eliminating new fossil boilers and triggering a surge in district heating connections in land-constrained urban cores. [1]International Energy Agency, “Germany’s Building Energy Act and the Renewable Heat Mandate,” iea.org The Netherlands follows with a fully electric mandate for new builds by 2025 and hybrid heat-pump requirements for retrofits by 2026, reinforcing network economics in dense municipalities. Federal and local grants of up to EUR 21,000 (about USD 24,700) for renewable heating support payback periods under eight years.

EU Carbon Border Adjustment Mechanism Accelerating Industrial Switching

CBAM’s phased introduction places an explicit carbon cost on imports of cement, steel, and aluminum, prompting energy-intensive plants to seek low-carbon district heating to remain competitive in EU markets. [2]Centre for European Reform, “CBAM and the Future of European Industry,” cer.eu Early adopters secure long-term concessions, locking in heat offtake while de-risking municipal investment in grid extensions.

Surging Data-Centre Waste-Heat Recovery Contracts in Northern Europe

EU efficiency rules require data centers above 1 MW to valorize waste heat, catalyzing roughly 60 recovery projects across Northern Europe. Google’s Hamina facility and at North’s 250 MW campus in Denmark illustrate how hyperscale operators trade free cooling for district-heating revenue streams, while cities capture high-grade heat for residential zones.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High retrofit costs for legacy 3rd-generation networks | -1.40% | EU-wide, especially Central and Eastern Europe | Long term (≥ 4 years) |

| Lengthy concession-award cycles and municipal tender delays | -0.80% | EU-wide, intense in smaller cities | Medium term (2-4 years) |

| Skills shortage in large-diameter pre-insulated pipe welding | -0.60% | EU-wide, acute in Germany and Nordics | Short term (≤ 2 years) |

| Competing on-site heat-pump economics in mild-climate zones | -0.90% | Southern Europe, Western coasts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Retrofit Costs for Legacy 3rd-Gen Networks

Central- and Eastern-European grids require EUR 500-800 per meter to re-pipe and decouple outdated boilers, stretching municipal debt envelopes and causing multi-year postponements of planned conversions. [3]European Investment Bank, “Financing the Modernisation of District Heating in Central Europe,” eib.org

Lengthy Concession-Award Cycles and Municipal Tender Delays

Smaller municipalities often spend 24–48 months navigating stakeholder consultations, environmental studies, and EU procurement rules, delaying revenue generation and discouraging private bidders. [4]Energy Post, “Why Municipal Tenders for Heating Networks Stall,” energypost.eu

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Heat Source: Renewable Integration Accelerates Despite Fossil Dominance

Fossil fuels retained 51.45% of the European district heating market share in 2025, primarily due to the continued use of entrenched gas and coal boilers, which remain economical when carbon prices are low. However, renewables post the fastest 10.8% CAGR to 2031, driven by the compatibility of biomass co-firing with existing furnaces, the abundance of geothermal energy in the Pannonian Basin, and growing industrial-waste heat offtake contracts. Nordic grids already surpass 42.6% renewable penetration, setting a precedent for the rest of the bloc. Solar-thermal fields, now costing EUR 20-50/MWh, scale quickly in Spain and France, smoothing summer demand dips through seasonal storage. Hybrid setups combine biomass baseloads with high-temperature heat pumps, enabling fossil-free, dispatchable heat that meets new emission reduction targets.

Geographically, geothermal pilot wells in Hungary and Croatia gain EU modernization grants, while Italy and Germany test deep-drilling rigs for 200 °C aquifers. Data-center waste heat joins the renewable basket, supplying stable 65–80 °C streams into 4GDH circuits. Seasonal intermittency drives the buildup of water-pit storage tanks with a capacity exceeding 100,000 m³ in Denmark, resulting in a 5–7 EUR/MWh reduction in marginal supply costs.

By Plant Type: Heat Pumps Challenge CHP Dominance

Combined heat and power units retained a 56.75% share of the European district heating market size in 2025, valued for dual energy streams and grid-balancing flexibility. Yet large heat pumps expand at 14.05% CAGR, spurred by cheaper renewable electricity and refrigerant advances that lift COPs above 5. Berlin’s 75 MW wastewater heat pump underscores a shift toward centralized electrified heat. Hybrid plants blend CHP turbines for winter peaks with variable-speed heat pumps for shoulder seasons, optimizing network return temperatures below 55 °C.

Nordic OEMs are ramping up production capacity; Sweden’s new 500,000-unit factory signals economies of scale that will push capital costs below EUR 500/kW by 2027. CO₂-based systems from Danish research institutes target dense urban neighborhoods, where flammability limits the use of synthetic refrigerants. Utilities retrofit existing CHPs with post-combustion carbon capture to protect sunk assets while reducing emission factors.

By Distribution Technology: Flexible Solutions Gain Market Share

Pre-insulated steel still dominates at 68.05% share for trunk lines, but flexible plastic pipes grow 11.85% CAGR as cities choose no-dig installation and tight bend radii to minimize road closures. Polymer innovations halve weight, reducing on-site crane hours and cutting installed costs 15–20%. Bio-based PEX and fully circular recycled pipes cut cradle-to-gate emissions by up to 90%, meeting new EU product environmental footprint rules. District cooling variants with vapor diffusion barriers now handle chilled brine at 0 °C without insulation freeze-up, opening revenue in Mediterranean retrofit projects.

Advanced substations incorporate smart valves and ultrasonic meters that relay return-temperature data in real time. Utilities deploy AI software that continuously minimizes ∆T, avoiding peak boil-offs and extending plant maintenance intervals.

By End User: Public Sector Leads Decarbonization Efforts

Residential applications remained the largest at 46.05% market share in 2025, reflecting decades of apartment-block connections in former Soviet and Nordic nations. Yet public and institutional customers register the highest 8.75% CAGR as governments enforce green-public-procurement rules that favor network solutions. Municipalities bundle schools, hospitals, and administrative offices into anchor loads, guaranteeing bankability for new concessions. Commercial developers integrate network connections in building permits to satisfy nearly zero-energy requirements under Directive 2024/1275.

Large industrial parks pivot to district heating to hedge CBAM-related exposure. Notably, breweries and food processors adopt heat networks to valorize low-grade process heat, securing ISO 50001 certification.

Geography Analysis

Germany constitutes 23.55% of European demand, propelled by building codes that outlaw fossil boilers in new dwellings and enforce municipal heat-planning by 2026 for major cities. More than one-third of Berlin, Hamburg, and Munich dwellings already connect to grids, and federal subsidies cover 30% of eligible connection costs. Digital twin pilots in Flensburg lower annual CO₂ emissions by 15% through dynamic temperature control, showcasing future operating models.

The Nordic cluster remains Europe’s technology frontier. Finland channels data-center waste heat into urban grids, with Google’s Hamina site alone offsetting natural-gas use for 20,000 households. Sweden invests SEK 10 billion in network upgrades through 2029, focusing on integrating biochar and high-temperature heat pumps. Denmark maintains price caps on recovered excess heat, prompting ongoing regulatory fine-tuning to preserve investor margins. Norway explores small modular reactors dedicated to district heating, signaling interest in nuclear-heat baseloads. Southern Europe emerges as a cooling-forward opportunity. Barcelona’s LNG cold-recovery plant yields 131 GWh annually, avoiding 32,000 tCO₂ and acting as a blueprint for other Mediterranean ports. France’s MaPrimeRénov program has awarded 500,000 renewable-heat grants, scaling ground-source heat pump uptake that dovetails with emerging 5GDHC grids. Italy’s Brescia waste-heat initiative proves viability in mixed-use redevelopments. The United Kingdom, still at 2% penetration, accelerates pilot concessions such as East London’s 6,500-home network, positioning for catch-up growth post-2026.

Competitive Landscape

Europe’s district heating arena reveals moderate fragmentation: regional utilities dominate local franchises while technology vendors jostle for plant and pipe retrofits. Vattenfall, ENGIE, and Veolia spearhead green-capex programs exceeding EUR 20 billion (USD 23.55 billion) through 2029, capitalizing on integration know-how and municipal partnerships. Carrier’s EUR 12 billion (USD 14.13 billion) purchase of Viessmann Climate Solutions signals convergence between appliance majors and utility operations, broadening turnkey capabilities in heat pumps and network substations.

Digital competencies become decisive. Gradyent’s AI engine helps Stadtwerke Flensburg cut peak supply temperatures by 15 °C, reducing gas use and opening export prospects for software layers atop legacy SCADA. Danfoss collaborates with Google and Hewlett Packard Enterprise on waste-heat-reuse frameworks that bundle drives, valves, and cloud analytics into single contracts. Engineering houses such as Ramboll launch white-label platforms to capture feasibility and EPC contracts in municipalities lacking in-house expertise.

New entrants target niche gaps: Steady Energy prototypes 50 MW thermal SMRs tailored for urban networks, promising sub-EUR 45/MWh baseload heat without combustion. Kamstrup’s ultrasonic meters with embedded edge-AI detect fraud and optimize billing cycles, raising switching costs for utilities once deployed at scale.

Europe District Heating Industry Leaders

Vattenfall AB

Danfoss A/S

Energie SA

Statkraft AS

Logstor A/S

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Vattenfall confirmed a SEK 170 billion (USD 17.95 billion) investment plan (2025-2029) with SEK 10 billion (USD 1.06 billion) for district heat.

- May 2025: Veolia teamed with Star Energy on pan-European geothermal projects for district heating.

- March 2025: Fortum partnered with Steady Energy to develop Finnish SMRs for heat applications.

- February 2025: Fortum released 2024 results highlighting its Espoo Clean Heat programme and final coal-unit closure.

Europe District Heating Market Report Scope

The Europe District Heating Market Report segments the market by Heat Source, encompassing Fossil Fuels, Renewable Energy (including Biomass, Geothermal, and Solar-Thermal), and waste heat from Industrial and Data Centres. Further categorization includes Plant Type, such as Combined Heat and Power (CHP), Boiler-Based Plants, and Large-Scale Heat Pumps; Distribution Technology, featuring Pre-insulated Steel Pipes, Flexible Plastic Piping, Substations and Heat Exchangers, and Control and Monitoring Systems; and End Users, which span Residential, Commercial, Industrial, and Public and Institutional sectors. The report geographically focuses on Germany, France, Austria, Sweden, the United Kingdom, Italy, and the Rest of Europe, providing market forecasts in USD value.

By Heat Source

| Fossil Fuels |

| Renewable Energy (Biomass, Geothermal, Solar-Thermal) |

| Industrial and Data-Centre Waste Heat |

By Plant Type

| Combined Heat and Power (CHP) |

| Boiler-Based Plants |

| Large-Scale Heat Pumps |

By Distribution Technology

| Pre-insulated Steel Pipes |

| Flexible Plastic Piping |

| Substations and Heat Exchangers |

| Control and Monitoring Systems |

By End User

| Residential |

| Commercial |

| Industrial |

| Public and Institutional |

By Country

| Germany |

| France |

| Austria |

| Sweden |

| United Kingdom |

| Italy |

| Rest of Europe |

| By Heat Source | Fossil Fuels |

| Renewable Energy (Biomass, Geothermal, Solar-Thermal) | |

| Industrial and Data-Centre Waste Heat | |

| By Plant Type | Combined Heat and Power (CHP) |

| Boiler-Based Plants | |

| Large-Scale Heat Pumps | |

| By Distribution Technology | Pre-insulated Steel Pipes |

| Flexible Plastic Piping | |

| Substations and Heat Exchangers | |

| Control and Monitoring Systems | |

| By End User | Residential |

| Commercial | |

| Industrial | |

| Public and Institutional | |

| By Country | Germany |

| France | |

| Austria | |

| Sweden | |

| United Kingdom | |

| Italy | |

| Rest of Europe |

Key Questions Answered in the Report

What is the current size of the European district heating and cooling market?

The market stands at USD 65.73 billion in 2026 and is projected to grow to USD 87.26 billion by 2031.

Which segment is growing fastest within the district heating and cooling market?

Large-scale heat pumps lead with a 14.05% CAGR thanks to falling electricity prices and high system efficiency.

Why are 5th-generation networks important?

They operate at ambient temperatures, cutting distribution losses and enabling simultaneous heating and cooling with low-grade heat sources.

How will EU policies affect industrial users?

The Carbon Border Adjustment Mechanism adds a carbon cost to imports, incentivizing factories to connect to low-carbon district heating to stay competitive.

What financing models support new network construction?

Municipalities increasingly issue green bonds, directing at least one-third of raised capital to district heating and cooling projects at lower interest rates.

Which countries are leading in data-center waste-heat recovery?

Finland, Denmark, and Sweden host the majority of Europe’s 60-plus recovery projects, leveraging stringent energy-efficiency regulations and cold climates.

Page last updated on: