United Kingdom Insurtech Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

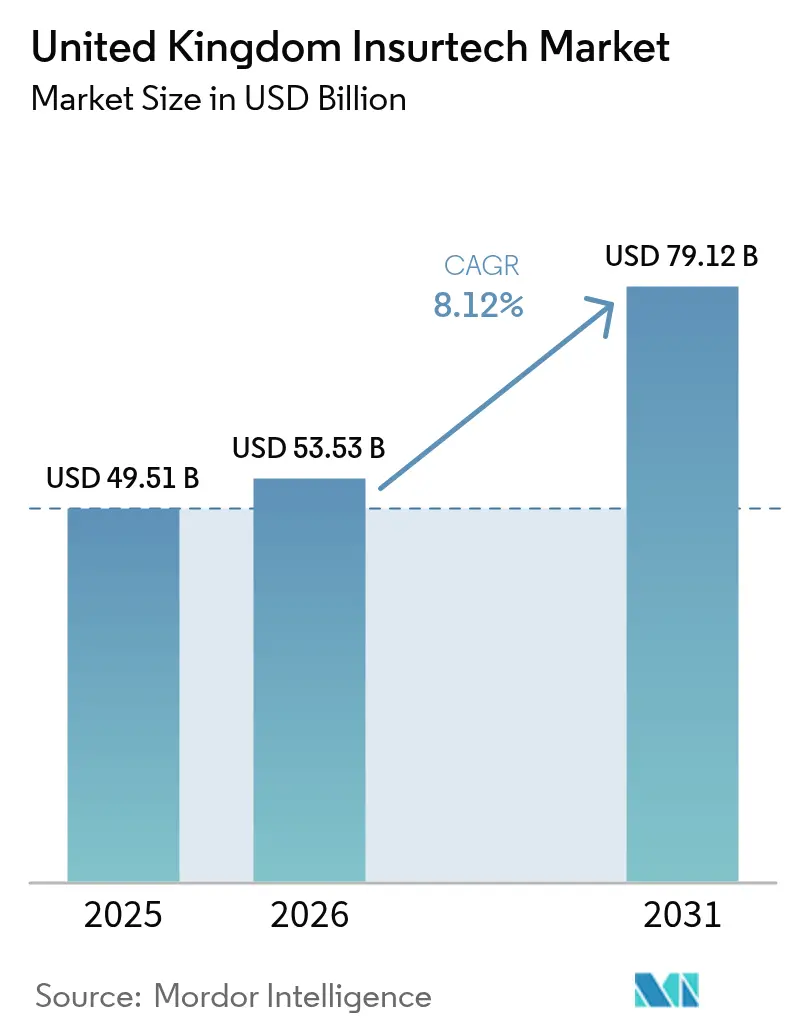

| Base Year Market Size (2025) | USD 49.51 Billion |

| Market Size (2026) | USD 53.53 Billion |

| Market Size (2031) | USD 79.12 Billion |

| Growth Rate (2026 - 2031) | 8.12% CAGR |

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Kingdom Insurtech Market Analysis by Mordor Intelligence

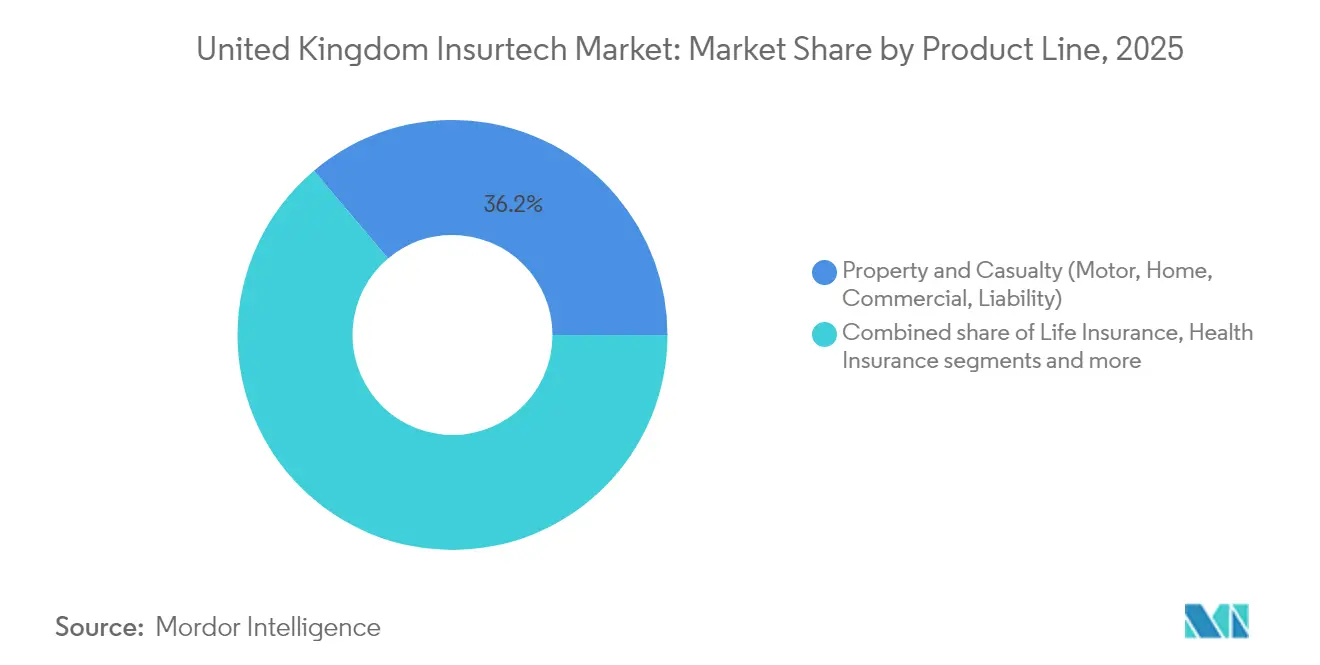

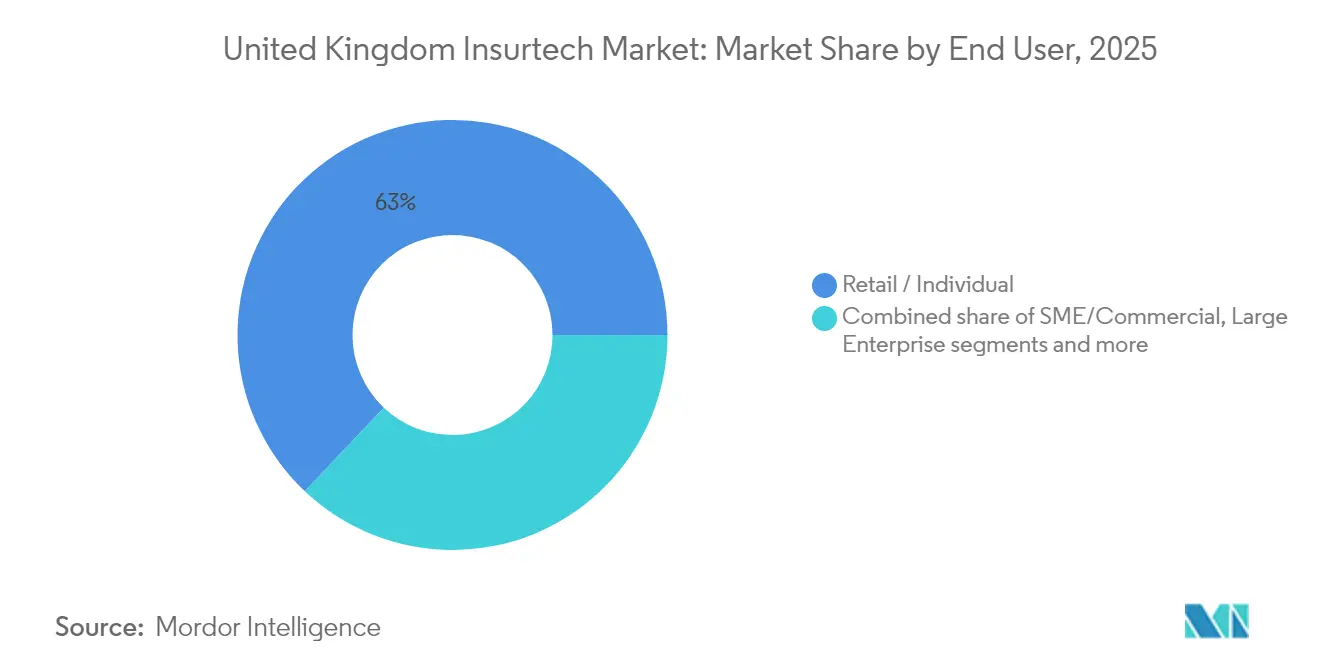

The UK insurtech market size in 2026 is estimated at USD 53.53 billion, growing from 2025 value of USD 49.51 billion with 2031 projections showing USD 79.12 billion, growing at 8.12% CAGR over 2026-2031. London’s concentration of unicorns continues to attract capital and talent, and the Financial Conduct Authority’s (FCA) Consumer Duty framework is forcing every insurer, incumbent, or start-up to prove a measurable customer benefit. At Lloyd’s, smaller syndicates are capturing premium from long-established leaders, signaling a pivot from rate-led to volume-led expansion. Property & Casualty (P&C) remains the largest product line after accounting for 36.7% of 2024 premiums, yet Specialty Lines are gaining the fastest due to cyber and climate-driven risks. Distribution is realigning as agents and brokers still command a 46.7% share, while embedded insurance platforms outpace all other channels with a 13.45% CAGR, underscoring the market’s shift to API-driven, invisible insurance.

Key Report Takeaways

- By product line, P&C accounted for 36.15% of the UK insurtech market share in 2025; specialty lines are advancing at a 12.05% CAGR through 2031.

- By distribution channel, agents/brokers held 46.05% of the UK insurtech market share in 2025, while embedded platforms are expanding at 12.88% CAGR.

- By end user, retail/individual customers represented 62.95% of the UK insurtech market size in 2025; SME/commercial demand is increasing at a 10.12% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Kingdom Insurtech Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~)% Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising penetration of usage-based motor insurance | +1.8% | UK-wide, concentrated in urban centers | Medium term (2-4 years) |

| Acceleration of open-banking style "open-insurance" regulation | +1.5% | UK national, regulatory spillover to EU | Long term (≥ 4 years) |

| Incumbent insurers' cost-out mandates amid inflation squeeze | +1.2% | UK national, particularly affecting Tier-1 insurers | Short term (≤ 2 years) |

| Surge in AI-led claims automation start-ups | +1.0% | UK-wide, London tech hub concentration | Medium term (2-4 years) |

| Untapped SME cyber-risk cover via embedded distribution | +0.8% | UK national, Manchester and Birmingham growth | Medium term (2-4 years) |

| Climate-linked parametric products for UK agriculture | +0.4% | Rural UK, Scotland and Wales focus | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Penetration of Usage-Based Motor Insurance

Motor premiums fell 17% to an average of GBP 777 in 2024, while claims ballooned to GBP 11.71 billion, creating margin pressure that propels telematics uptake[1]RSM UK, “UK Motor Claims Hit Record High,” rsmuk.com . This shift is particularly evident among drivers aged 17-18, who are now benefiting from a 23% reduction in premiums due to their lower-risk behavior, challenging traditional demographic-based pricing models. The FCA's review of premium finance, which affects over 20 million policyholders, has further highlighted the need for data-backed fair-value pricing, adding urgency for insurers to adapt. In response to these dynamics, insurers are increasingly investing in IoT devices, advanced analytics stacks, and scalable cloud solutions to enhance operational efficiency and pricing accuracy. Agile insurtech companies are leveraging these advancements to gain an early market share, while established players face challenges related to legacy systems and technological debt. Consequently, usage-based insurance products, which rely on real-time data and personalized pricing, are becoming a critical profitability lever. This trend is reshaping the UK's insurtech market, driving innovation and competition as insurers strive to meet evolving consumer expectations and regulatory demands.

Acceleration of Open-Insurance Regulation

By 2026, the Joint Regulatory Oversight Committee aims to launch live open-insurance rails, with pilot measures already in motion to test and refine the framework. These rails will leverage standard APIs to facilitate seamless third-party data access, significantly reducing switching costs for consumers and creating opportunities for API-native firms to thrive in a competitive landscape. Starting in 2024, the Consumer Duty mandates insurers to demonstrate genuine and measurable outcomes for their customers, moving beyond mere process compliance, particularly for closed products. Initial responses to this regulation include the introduction of value-enhanced GAP policies and the provision of clearer, more transparent advisory disclosures to improve customer understanding. Embedded platforms are well-positioned to capitalize on these changes, as their architecture is inherently designed to support real-time data sharing, interoperability, and adherence to open standards, making them a natural fit for the evolving insurance ecosystem.

Incumbent Insurers’ Cost-Out Mandates Amid Inflation

UK players, grappling with record claims and declining premiums, are increasingly turning to structural savings to maintain profitability. In 2023, over 55% of carriers initiated core-system upgrades, prioritizing automation, cloud migration, and enhanced cybersecurity measures to address operational inefficiencies. AI-driven claims triage and seamless straight-through processing are emerging as key solutions, offering immediate relief in operational expenses while improving customer experience. Rather than undertaking costly and disruptive system overhauls, carriers are opting for strategic partnerships. These collaborations allow them to integrate specialized capabilities, such as advanced analytics and fraud detection tools, with minimal disruption to existing operations. For B2B insurtech suppliers, this shift has created a surge in demand as players seek solutions that deliver measurable cost savings and operational improvements in a highly competitive market.

Surge in AI-Led Claims-Automation Start-Ups

Qantev successfully raised USD 31.2 million, with ambitions to expand its platform across 12 nations[2]Qantev, “Qantev Raises €30 Million to Scale AI Claims,” qantev.com . This funding will enable Qantev to enhance its technological capabilities and scale its operations to meet the growing demand for AI-based solutions in health and life insurance. Meanwhile, Sprout.ai, hailing from the UK, has clinched GBP 20.2 million in funding, setting its sights on reaching a target of one billion global policyholders by the year 2030. The company plans to utilize this investment to refine its AI algorithms and broaden its market reach, addressing the evolving needs of policyholders worldwide. Data from EIOPA highlights a significant opportunity: only half of European non-life insurers and a mere 24% of life carriers are currently harnessing the power of AI. This underutilization underscores the potential for growth and innovation within the insurance market. The benefits of automation are evident, with claim handling times being reduced by as much as 80% and a notable enhancement in fraud-detection accuracy. In a landscape where only a quarter of UK consumers place their trust in insurers, the push for seamless, AI-driven claims experiences emerges as a pivotal differentiator, offering insurers a chance to rebuild consumer confidence and improve customer satisfaction.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Data-privacy compliance costs post-UK GDPR divergence | -1.2% | UK national, cross-border operations affected | Medium term (2-4 years) |

| Persistent legacy-core integration hurdles at Tier-1 insurers | -0.9% | UK national, concentrated in London financial district | Long term (≥ 4 years) |

| Investor pull-back driving capital scarcity for Series-B+ insurtechs | -0.8% | UK national, London tech ecosystem focus | Short term (≤ 2 years) |

| Rising reinsurer retentions limiting innovative capacity | -0.5% | UK national, Lloyd's market concentration | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Data-Privacy Compliance Costs Post-UK GDPR Divergence

Cross-border operations face challenges due to nuanced differences between the UK and EU regulatory frameworks, necessitating dual compliance. Smaller insurtech companies encounter disproportionately high legal and audit costs, as both jurisdictions enforce stringent algorithmic transparency requirements. The implementation of the Digital Operational Resilience Act (DORA) introduces additional cybersecurity obligations, particularly tightening the oversight of cloud service providers. Variations in the timing and structure of ICO enforcement and penalties between the UK and EU further complicate strategic planning for businesses. Consequently, many start-ups prioritize scaling within the UK market before expanding into the EU, which limits their short-term addressable market but helps conserve financial resources and operational capacity.

Persistent Legacy-Core Integration Hurdles at Tier-1 Insurers

Modernizing mainframes that operate on decades-old business logic presents significant financial challenges. Boston Consulting Group outlines three strategic approaches: centralized, federal, and hybrid, each requiring extensive planning and spanning multiple budget cycles. According to a Deloitte survey, only a small percentage of life insurers have completed modernization initiatives, with larger organizations demonstrating slightly faster progress. Concerns over operational disruptions have led many firms to rely on nightly batch transfers for system integrations, limiting the realization of real-time collaboration goals. As modernization backlogs persist, the penetration of advanced insurtech solutions continues to fall short of its full potential.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Line: Specialty Lines Drive Innovation Despite P&C Dominance

P&C produced 36.15% of 2025 premiums, anchoring the UK insurtech market because the motor and home cover is compulsory or widely purchased. Yet, record motor claims and a 17% average premium fall constrain margins, compelling carriers to boost efficiency and diversify. Specialty Lines meanwhile grow 12.05% annually, a pace that widens their share of the UK insurtech market size through 2031. FloodFlash uses sensors to pay flood claims in a few hours, tackling a GBP 58 billion domestic protection gap. Coalition’s cyber expansion and ManyPets’ focus on chronic-care pet insurance illustrate how niche innovators fill emerging coverage voids.

Agile players are capitalizing on pricing uncertainties stemming from emerging risks like cyber threats, parametric climate challenges, and novel liabilities. These risks introduce complexities in pricing models, creating opportunities for innovative market participants to gain a competitive edge. With parametric triggers, policyholders receive immediate payouts, sidestepping protracted disputes with loss adjusters, which enhances customer satisfaction and operational efficiency. The robust investor interest in data-driven models within Specialty Lines is highlighted by Qantev’s recent oversubscribed fundraising round, reflecting confidence in the sector's growth potential. Furthermore, a regulatory embrace of product innovation, paired with Lloyd’s Blueprint Two digitization efforts, is streamlining the specialty placement process by reducing inefficiencies and improving transparency. As a result, Specialty Lines are poised to increasingly overshadow the sluggish growth of P&C premiums, reshaping the underwriting talent landscape and driving demand for professionals with expertise in emerging risks and advanced analytics.

By Distribution Channel: Embedded Platforms Reshape Broker Dominance

Agents and brokers still manage 46.05% of premiums in 2025, relying on relationship capital, regulatory know-how, and Lloyd’s access for complex placements. This dominance highlights their ability to navigate complex insurance landscapes and provide tailored solutions for clients. However, embedded-insurance platforms are gaining traction, experiencing a robust 12.88% CAGR, which underscores a growing consumer preference for seamless and contextual protection integrated into their purchasing journeys. Eleos Life's collaborations with Assurity and SCOR exemplify how UK start-ups can efficiently export embedded insurance propositions to international markets at minimal marginal costs, showcasing the scalability of such models. Meanwhile, direct-to-consumer platforms are disrupting traditional personal-line commission structures, driven by the UK's strong reliance on price comparison tools. Digital marketplaces, which aggregate various insurance products, complement these trends, but embedded models stand out by eliminating additional steps, offering a more streamlined and user-friendly experience.

With Consumer Duty emphasizing transparent value, embedded insurance flows align well with regulatory expectations by prominently displaying price and coverage details at the point of checkout. This transparency resonates with consumers, fostering trust and simplifying decision-making. In response to these shifts, brokers are integrating quoting APIs and advanced analytics engines to enhance their service offerings and remain competitive in a rapidly evolving market. Bancassurance is also adapting by testing open-insurance APIs, which enable the integration of micro-covers directly into mobile banking journeys, providing customers with convenient and tailored insurance options. While brokers are expected to retain their foothold in managing bespoke corporate risks, their market share in commoditized insurance lines is facing irreversible erosion due to the rise of digital and embedded models. Consequently, the UK insurtech market is shaping a dual-path future, characterized by relationship-driven specialty broking on one hand and high-volume embedded distribution on the other, reflecting the industry's ongoing transformation.

By End User: SME Commercial Segment Emerges as Primary Growth Engine

Retail policyholders accounted for 62.95% of the 2025 premium, driven by compulsory motor, life, and rising private-health uptake. This segment benefits significantly from an aging demographic, which increases the demand for life and health insurance products, and the convenience offered by digital platforms, which streamline policy purchases and renewals. However, intense price competition within the market continues to constrain its growth potential. In contrast, SME and commercial customers are on a robust growth trajectory, expanding at a 10.12% CAGR, outpacing the broader UK insurtech market. SMEs, which previously faced challenges in sourcing adequate coverage through traditional brokers, now gain access to embedded cyber insurance packages seamlessly integrated into their cloud accounting or e-commerce platforms. These plug-and-play solutions address critical protection gaps, offering convenience and tailored coverage. Additionally, government initiatives aimed at accelerating SME digitization amplify the demand for bundled insurance products, as businesses increasingly seek comprehensive and efficient risk management solutions.

Most SMEs lacking in-house risk teams are turning to turnkey solutions that blend coverage with preventive analytics. These solutions provide a comprehensive approach, enabling SMEs to manage risks effectively without the need for dedicated internal resources. Insurtech MGAs are stepping in, offering modular policies that scale with business growth, effectively addressing the issue of underinsurance. These modular policies allow businesses to customize their coverage as their needs evolve, ensuring adequate protection at every stage of growth. Faced with inflationary pressures, business owners are gravitating towards cost-transparent, usage-based products, moving away from traditional blanket coverage that often results in overpayment or insufficient protection. In Scotland and Wales, parametric climate covers are proving vital for rural SMEs, ensuring cash flow protection for their seasonal operations. These covers provide quick payouts based on predefined triggers, such as adverse weather conditions, helping businesses recover faster from disruptions. With this trend gaining momentum, SME premiums are poised to claim an increasing share of the UK's insurtech market by 2031, driven by the growing demand for tailored and innovative insurance solutions.

Geography Analysis

London stands as the epicenter of the UK's insurtech landscape, boasting as many unicorns as the entirety of Europe and reaping the benefits of Lloyd's expansive network. In H1 2024, Lloyd's reported a robust profit of USD 3.89 billion, alongside a 6.5% growth in premiums, reaching a total of USD 38.44 billion, solidifying its stature as a global specialty hub. The Square Mile, with its concentration on venture capital, regulatory expertise, and talent, plays a pivotal role in shaping national trends. However, with rising costs and a shift towards remote work, many start-ups are moving their engineering and back-office operations to Manchester and Birmingham. These cities, bolstered by local authority incentives and a steady stream of data science graduates from universities, are making their mark. Both cities recorded impressive double-digit premium growth in 2024, highlighting their burgeoning significance in the UK's insurtech arena.

Scotland and Wales are increasingly turning to climate-related parametric solutions for agriculture and renewable energy. FloodFlash's deployment in rural areas underscores the potential of sensors in underwriting risks once deemed "uninsurable." These advancements demonstrate how technology is addressing gaps in coverage for previously underserved markets. Meanwhile, Northern England's industrial heritage drives demand for tailored commercial products, ranging from supply-chain interruptions to environmental liabilities. Digital MGAs are stepping in to meet these niche requirements, showcasing the adaptability of the insurtech market to regional needs. While Brexit introduces compliance challenges for cross-border operations, it also empowers the UK to pioneer regulations that favor innovation, staying a step ahead of the EU.

London remains the nucleus for reinsurance backing, with Gallagher Re estimating the global reinsurer capital at a substantial USD 769 billion, underscoring the capacity for UK-led experimentation. Efforts like regional accelerators and digital-skills programs aim to temper London's overwhelming dominance by fostering growth in other regions. However, the capital's unparalleled international connectivity ensures its continued primacy in fundraising and forging partnerships. London’s ability to attract global investors and maintain its position as a hub for innovation and collaboration reinforces its central role in the UK insurtech market, even as other cities rise in prominence.

Competitive Landscape

The UK insurtech market remains notably fragmented, with the top five firms commanding only a modest share of total premiums. Marshmallow, nearing profitability, showcases how harnessing advanced data science and adopting selective underwriting can convert market share into tangible financial success. In a bid to navigate the challenges posed by outdated legacy systems, established insurers are increasingly turning to niche insurtech firms, either through acquisitions or collaborations. This strategic shift highlights the growing importance of leveraging innovative technologies and partnerships to remain competitive in a rapidly evolving market. Additionally, Qantev's recent funding round underscores robust investor faith in the scalability and efficiency of AI-centric business models, further validating the sector's potential for growth and transformation.

Zego's exit from the B2B fleet segment, coupled with a workforce reduction exceeding 100 employees, underscores a heightened focus on disciplined capital management for sustainable profitability. This move reflects a broader trend within the insurtech market, where firms are prioritizing financial stability and operational efficiency over-aggressive expansion. Similarly, ManyPets’ decision to retreat from the US market and intensify its focus on UK pet insurance highlights a strategic reallocation of resources to proven home markets amid tightening funding conditions. These examples illustrate how companies are adapting their strategies to navigate the challenges posed by limited funding and increasing competition, ensuring long-term viability in the market.

Embedded specialists are forging partnerships with retailers, neobanks, and platforms in the gig economy, allowing them to connect with customers without incurring significant marketing expenses. Meanwhile, Lloyd’s syndicates are witnessing a shift as smaller entities leverage digital placement and data-driven risk assessment to capture a larger share of the business, challenging the dominance of historically larger syndicates. While Series B+ financing remains constrained, leading to anticipated consolidation, the low entry barriers enabled by open-API architecture continue to foster the emergence of micro-specialists targeting specific market pain points. The future leaders in this space will be those who combine regulatory fluency, robust capital strength, and technological execution to drive innovation and maintain a competitive edge.

United Kingdom Insurtech Industry Leaders

Zego

Marshmallow

ManyPets (Bought By Many)

By Miles

Urban Jungle

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Lloyd’s reported strong 2024 results, stressing cyber and climate product expansion while advancing “The Future at Lloyd’s” digital blueprint.

- January 2025: The Lloyd’s Market Association announced plans to deepen US engagement, noting that North America already represents 58% of Lloyd’s premium.

- October 2024: Qantev secured USD 31.2 million to scale its AI claim-processing platform.

- September 2024: Blueberry Life rebranded and expanded life-cover options for customers with chronic conditions.

United Kingdom Insurtech Market Report Scope

The insurance sector is home to some of the largest areas ripe for disruption across the Financial Services industry in the coming years. With increasingly demanding consumers, struggling legacy systems, and growing amounts of data at their fingertips, technological advances are offering the insurance market the opportunity to transform the way they do business. The UK InsurTech Market is segmented by the type of Insurances Provided ( Life and non-life; Non-Life can be further segmented into Motor, House, Accident, Pet, Health and Others).

| Life Insurance |

| Health Insurance |

| Property & Casualty (P&C): Motor, Home, Commercial, Liability, etc. |

| Specialty Lines (e.g., cyber, pet, marine, travel) |

| Direct-to-Consumer (D2C) Digital |

| Aggregators/Marketplaces |

| Digital Brokers/MGAs |

| Embedded Insurance Platforms |

| Traditional Agents/Brokers (digitally enabled) |

| Bancassurance (digitally enabled) |

| Other Channels |

| Retail/Individual |

| SME/Commercial |

| Large Enterprise/Corporate |

| Government/Public Sector |

| By Product Line (Insurance Type) | Life Insurance |

| Health Insurance | |

| Property & Casualty (P&C): Motor, Home, Commercial, Liability, etc. | |

| Specialty Lines (e.g., cyber, pet, marine, travel) | |

| By Distribution Channel | Direct-to-Consumer (D2C) Digital |

| Aggregators/Marketplaces | |

| Digital Brokers/MGAs | |

| Embedded Insurance Platforms | |

| Traditional Agents/Brokers (digitally enabled) | |

| Bancassurance (digitally enabled) | |

| Other Channels | |

| By End User | Retail/Individual |

| SME/Commercial | |

| Large Enterprise/Corporate | |

| Government/Public Sector |

Key Questions Answered in the Report

What is the projected value of the UK insurtech market by 2031?

The sector is forecast to reach USD 79.12 billion, growing at an 8.12% CAGR over 2026-2031.

Which product line is expanding fastest?

Specialty Lines are increasing at a 12.05% CAGR, outpacing P&C due to cyber, parametric flood, and climate-related covers.

Why are embedded platforms important to the UK insurtech industry?

Embedded channels integrate cover at checkout, delivering 12.88% CAGR and aligning with open-insurance data-sharing mandates.

What drives SME demand in the UK insurtech market?

SMEs seek turnkey cyber and liability protection delivered through software they already use, resulting in a 10.12% CAGR for the segment.

How dominant is London within the geography mix?

London hosts the most insurtech unicorns in Europe and anchors Lloyd’s, but regional hubs like Manchester and Birmingham are gaining share through lower costs and targeted incentives.

How fragmented is the competitive landscape?

The top five firms account for only a small share of premiums, highlighting a concentrated market structure and presenting substantial opportunities for niche players to enter and compete.

Page last updated on: