Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

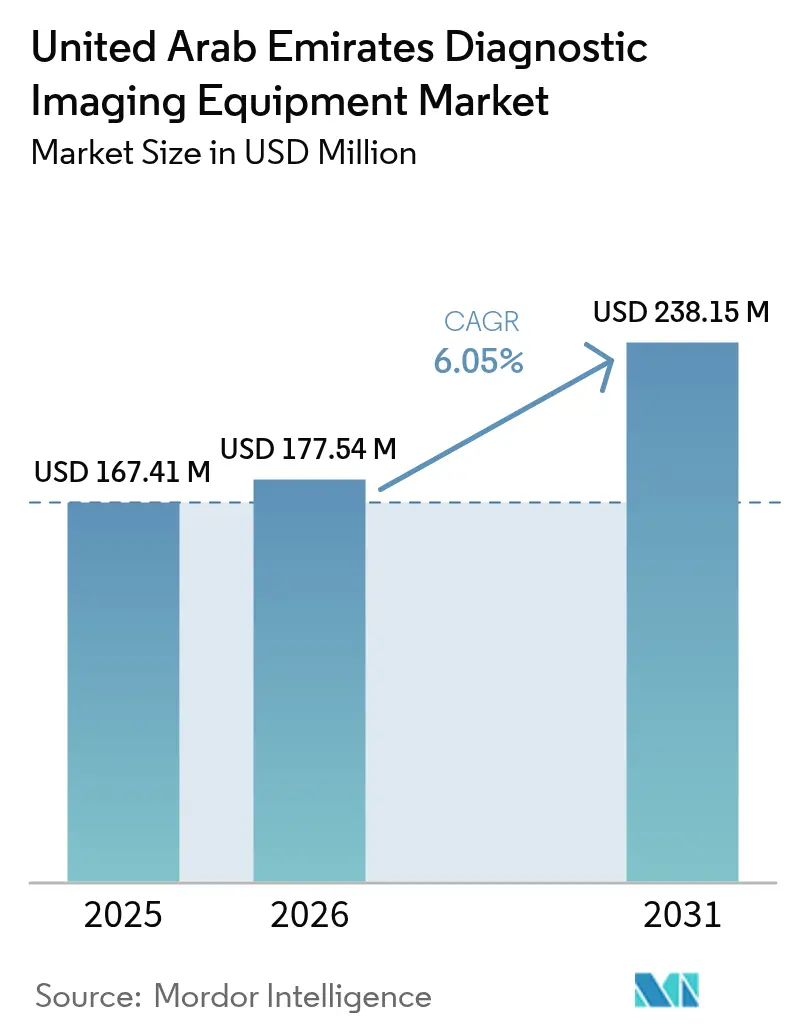

| Base Year Market Size (2025) | USD 167.41 Million |

| Market Size (2026) | USD 177.54 Million |

| Market Size (2031) | USD 238.15 Million |

| Growth Rate (2026 - 2031) | 6.05% CAGR |

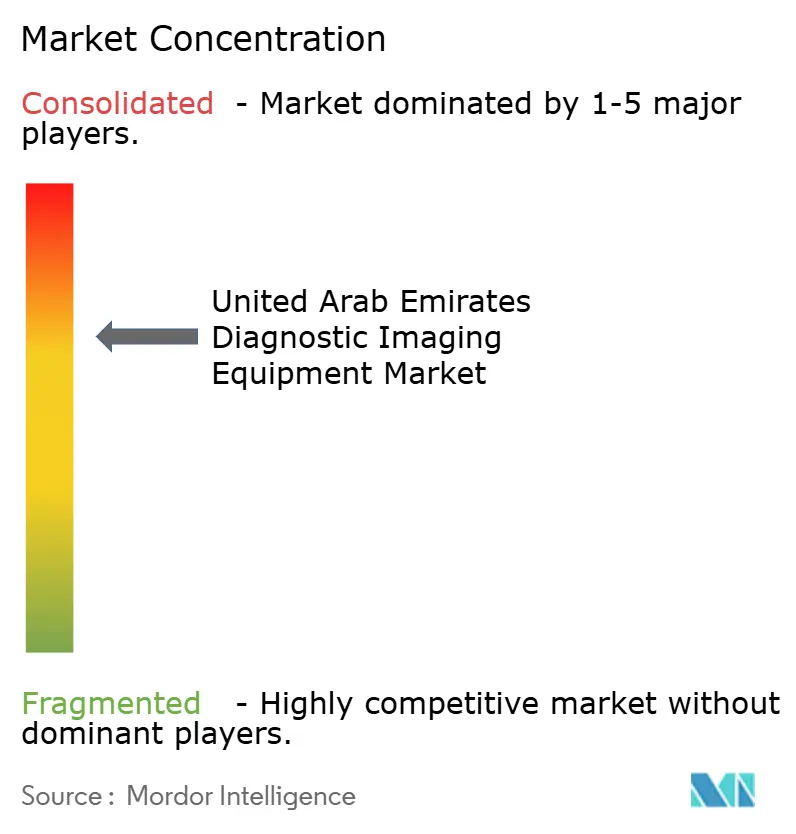

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

United Arab Emirates Diagnostic Imaging Equipment Market Analysis by Mordor Intelligence

The United Arab Emirates Diagnostic Imaging Equipment Market size is expected to grow from USD 167.41 million in 2025 to USD 177.54 million in 2026 and is forecast to reach USD 238.15 million by 2031 at 6.05% CAGR over 2026-2031.

Spending momentum is being driven by the nationwide health-insurance mandate that eliminates out-of-pocket fees for scans, alongside government investments under the "We the UAE 2031" health initiative. Hospitals are shifting from standalone systems to AI-ready, cross-sectional modalities, while private providers are scaling operations to capitalize on the growing medical tourism market. Long-term vendor-managed service contracts are mitigating the risks of technology obsolescence, thereby extending replacement cycles. Furthermore, locally hosted cloud PACS and AI-enabled teleradiology networks are enhancing radiologist efficiency, expanding the scope of reimbursable exams. However, the market faces key challenges, including the high cost of 3 Tesla MRI and PET-CT systems (exceeding USD 2 million), a shortage of certified service engineers in the northern emirates, and stringent data-residency regulations that complicate offshore image archiving.

Key Report Takeaways

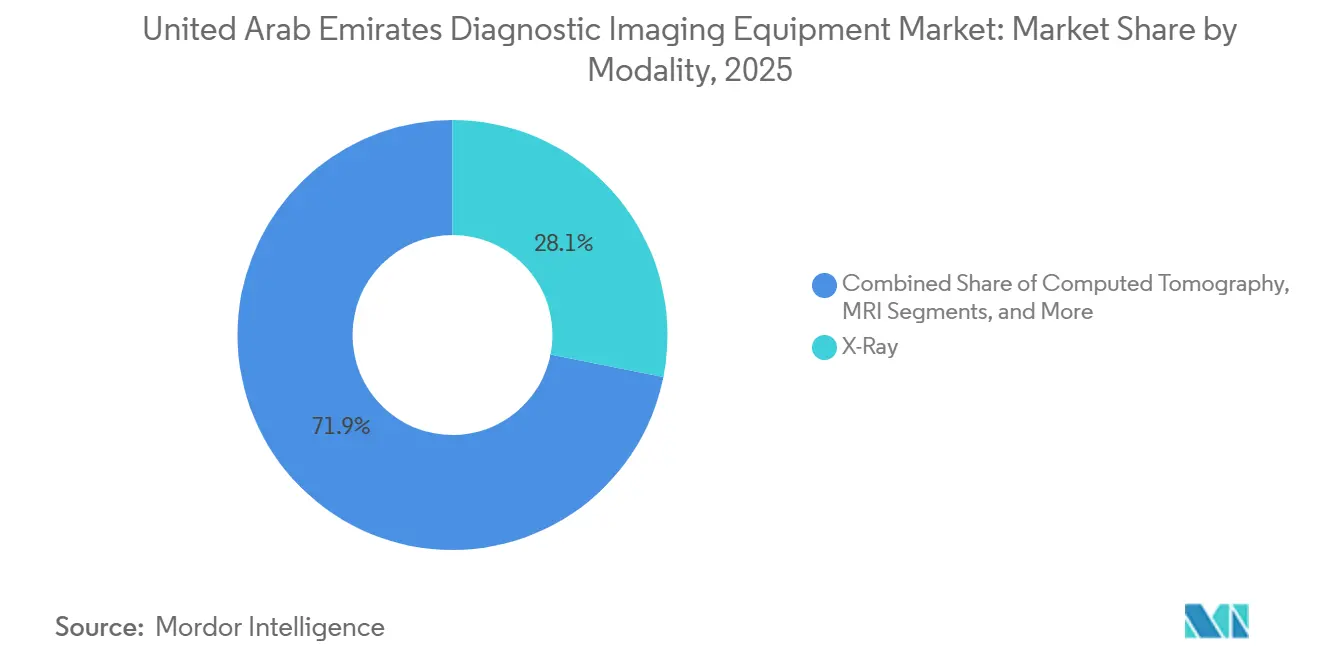

- By modality, X-ray systems led the UAE diagnostic imaging equipment market with a 28.12% share in 2025, while CT is forecast to expand at an 8.43% CAGR through 2031.

- By portability, fixed room-based platforms captured 72.54% of the UAE diagnostic imaging equipment market size in 2025; mobile and portable units represent the fastest-growing slice at a 7.43% CAGR to 2031.

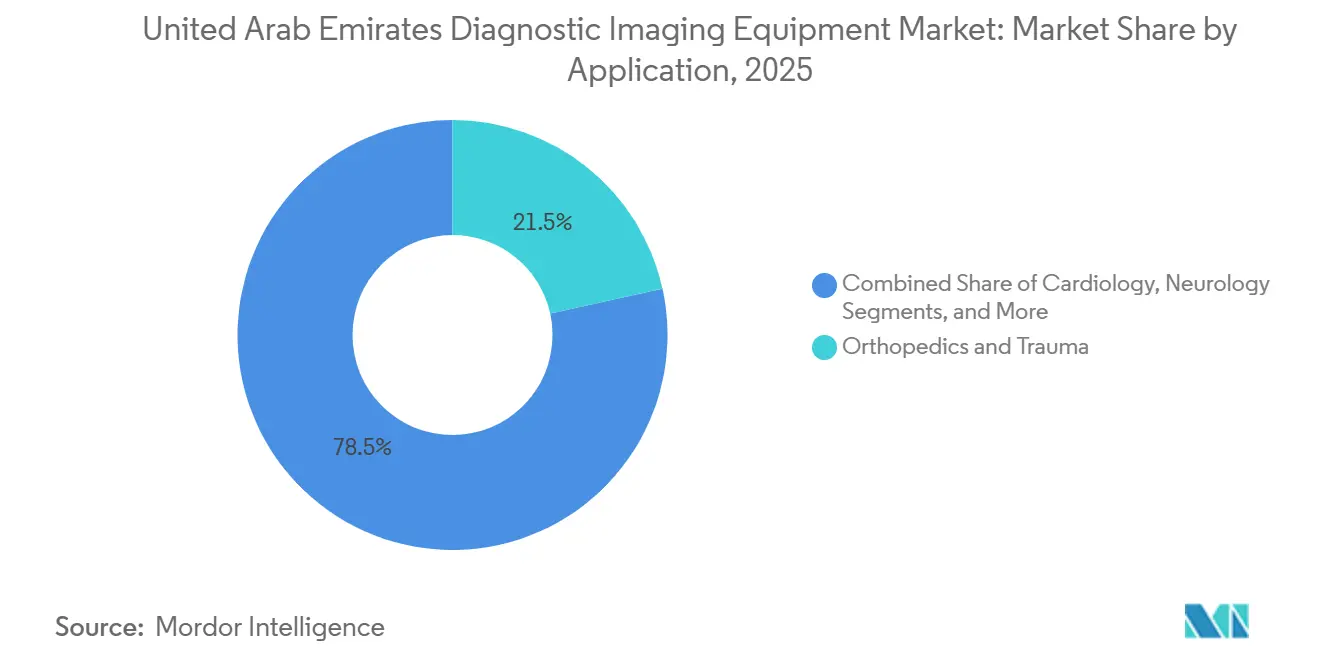

- By application, cardiology imaging is projected to post an 8.78% CAGR, outpacing orthopedics and trauma, which accounted for 21.54% of the UAE diagnostic imaging equipment market share in 2025.

- By end user, hospitals absorbed 62.54% of 2025 spending, yet diagnostic imaging centers are advancing at a 7.54% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

United Arab Emirates Diagnostic Imaging Equipment Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Funding under “We The UAE 2031” Strategic Health Pillar | +1.2% | National, concentrated in Abu Dhabi and Dubai | Medium term (2-4 years) |

| Mandatory National Health Insurance Boosting Imaging Volumes | +1.5% | National, effective across all emirates | Short term (≤ 2 years) |

| Growing Inbound Medical-Tourism Flows (Dubai & Abu Dhabi) | +0.9% | Dubai and Abu Dhabi | Medium term (2-4 years) |

| AI-Enabled Teleradiology Networks Easing Radiologist Shortage | +0.8% | National, early uptake in Abu Dhabi | Long term (≥ 4 years) |

| Expansion of Mobile/POC Imaging Suites in Hospitality & Events | +0.4% | Dubai, Abu Dhabi, northern emirates | Medium term (2-4 years) |

| Long-Term Vendor-Managed Equipment Service Contracts (PPP) | +0.7% | National, led by private groups | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Government Funding under “We the UAE 2031” Strategic Health Pillar

To position itself among the top 15 global health systems, Abu Dhabi is channeling sovereign capital into strategic healthcare advancements. A Dh4.7 billion endowment, coupled with a USD 2 billion infrastructure investment, is directed toward imaging-focused tertiary centers. A key project, the Hamdan Bin Rashid Cancer Hospital, is slated to open in 2026, equipped with advanced integrated PET-CT suites. Regulatory mandates require 100% AI integration by 2025, driving the replacement of outdated scanners with AI-enabled MRI and CT platforms. Sovereign wealth funds Mubadala and ADQ are co-investing in health-tech startups, ensuring capital directly supports vendor order books rather than operational subsidies. These initiatives establish stable procurement cycles, favoring manufacturers that provide reconstruction algorithms, radiomics software, and cloud-based analytics solutions.

Mandatory National Health Insurance Boosting Imaging Volumes

Universal coverage, effective January 1, 2025, closed the last reimbursement gaps, prompting a 26.5% surge in patient throughput at Burjeel Medical City during H1 2024[1]Burjeel Holdings, “2024 Investor Presentation,” burjeelholdings.com. Unified fee schedules from Dubai Health Authority and the Department of Health Abu Dhabi cap scan tariffs and stabilize cash flows, encouraging providers to pursue volume expansion. American Hospital Dubai installed GE’s Revolution Apex 256-slice CT in February 2025 specifically to meet insured demand for cardiac CT angiography. Shorter appointment queues are now the primary competitive lever among private imaging centers.

Growing Inbound Medical-Tourism Flows (Dubai & Abu Dhabi)

Dubai and Abu Dhabi rank sixth and eighth globally on the Medical Tourism Index, respectively, and host 214 Joint Commission International-accredited facilities in 2026. International patients require same-day work-ups, spurring investments in rapid-turnaround MRI, CT, and PACS that slash report times to under 4 hours. Cleveland Clinic Abu Dhabi’s 25,000 annual cardiac procedures rely on advanced cardiac MRI and CT capabilities that mirror those of North American centers. High-spec hybrid suites, such as Siemens’ Nexaris Angio-CT, launched at American Hospital Dubai in January 2025, reinforce the Emirates’ destination-medicine positioning.

AI-Enabled Teleradiology Networks Easing Radiologist Shortage

With only 5.6 radiologists per 100,000 residents, the UAE leans on AI triage and tele-reading platforms. The Malaffi exchange now links 67 facilities and 4 million images, letting any licensed radiologist read exams from any site. Department of Health pilots show AI chest-X-ray tools trimming read times by 30%, equivalent to a virtual workforce gain. SEHA’s LEO360 tele-stroke robot cuts door-to-neurologist time to 10.7 minutes, proving remote workflows can match urgent-care demands. Vendors embedding auto-routing and structured reporting into PACS capture sticky software revenue while legacy archives risk obsolescence.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Capital & Lifecycle Cost of Advanced Modalities | -0.9% | National, acute in smaller emirates | Short term (≤ 2 years) |

| Limited Local Service Engineers → Extended Downtime | -0.6% | National, severe in northern emirates | Medium term (2-4 years) |

| Fragmented Procurement Slows Multi-Site Standardisation | -0.5% | National, across emirate lines | Long term (≥ 4 years) |

| Cyber-Security & Data-Residency Barriers for Cloud PACS | -0.4% | National, compliance focus | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High Capital & Lifecycle Cost of Advanced Modalities

A 3 Tesla MRI costs USD 2 million–3 million, and PET-CT exceeds USD 2.5 million, outlay levels that stretch budgets of community providers outside Dubai and Abu Dhabi. Add-on lifecycle expenses—helium refills, detector swaps, and annual software fees—run about 10%-15% of ticket price each year, dragging ROI when scanner utilization slips below 60%. Smaller clinics increasingly defer purchases, funneling complex cases to tertiary centers and concentrating capacity in the two largest emirates.

Limited Local Service Engineers → Extended Downtime

High expatriate turnover leaves a thin bench of certified MRI and PET-CT technicians. Parts often ship in from Europe or Saudi Arabia, prolonging outages up to 10 days. Siemens’ partnership model supplies on-site engineers to large hospitals, but independents cannot command similar terms, so unplanned downtime erodes patient trust and revenue.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Modality: CT Scanners Outpace Legacy X-Ray Growth

CT is forecast to grow 8.43% annually through 2031, the quickest pace among modalities in the UAE diagnostic imaging equipment market. X-ray retained a 28.12% share in 2025, yet faces slower growth as flat-panel detectors commoditize. The UAE diagnostic imaging equipment market size for CT systems is expected to reach USD 93 million by 2031, while CT’s accelerating uptake chips away at X-ray’s long-held volume leadership. Premium CT installations, such as GE’s Revolution Apex at American Hospital Dubai, underline demand for 256-slice spectral imaging that lowers radiation dose and delivers sub-millimeter resolution[2].

MRI, bolstered by Siemens’ MAGNETOM Flow.Neo launch at Adam Vital Hospital in 2026 accounts for a rising share of cross-sectional spending, though helium logistics and room build costs moderate penetration outside tertiary hubs. Ultrasound remains a high-volume staple, especially for obstetrics, vascular, and point-of-care exams. Nuclear imaging, hybrid modalities, and breast tomosynthesis make up smaller but strategically important segments as oncology screening rises. Vendors compete primarily on AI-driven workflow, low-dose algorithms, and interoperability rather than raw hardware specs, reflecting the market’s maturing preference for software differentiation.

By Portability: Mobile Units Gain Share in Underserved Settings

Fixed-room-based installations accounted for 72.54% of 2025 sales, anchoring the UAE diagnostic imaging equipment market share in tertiary hospitals. Mobile and portable platforms, however, are forecast to expand at a 7.43% CAGR, capturing incremental procedures in emergency tents, sporting events, and rural clinics. Handheld ultrasound penetration, led by Butterfly Network, already positions the UAE diagnostic imaging equipment market size for portable devices at more than USD 25 million in 2026. Hyperfine’s Swoop portable MRI trials aim to demonstrate that bedside neuro-imaging can eliminate inter-department transport delays.

Regulatory bodies still require the same image-quality benchmarks for mobile units, so battery life, rugged design, and AI enhancement remain critical differentiators. As reimbursement frameworks evolve to acknowledge scans performed outside standard radiology suites, the portability category stands to monetize use cases previously deemed non-billable.

By Application: Cardiology Imaging Accelerates on AI-Guided Protocols

Cardiology imaging is set to grow 8.78% per year to 2031, aided by AI-driven coronary CT angiography and cardiac MRI. Orthopedics and trauma retained 21.54% of the UAE diagnostic imaging equipment market share in 2025 thanks to high road-traffic-accident volumes. Oncology applications expand hand in hand with new cancer centers, while neurology benefits from telestroke networks that fast-track CT perfusion studies.

Women’s health imaging receives a policy push from nationwide breast cancer screening that now mandates annual tomosynthesis for women over 40. Advanced visualization software that automates ejection-fraction calculation or lesion segmentation is shortening report cycles, helping providers handle rising caseloads without proportional growth in radiologist headcount.

By End User: Diagnostic Centers Capture Medical-Tourism Demand

Hospitals consumed 62.54% of 2025 spending, yet will surrender an incremental share to standalone diagnostic centers growing at 7.54% annually. The latter market to expatriates and medical tourists who prize same-day slots and late-evening service windows. The UAE diagnostic imaging equipment industry sees specialty clinics—such as sports medicine, women’s health, and day surgery—leveraging dedicated modalities to deliver differentiated care. Mobile service providers, though still niche, address remote worksites and hospitality venues, hinting at future upside once reimbursement parity is achieved.

Large chains such as Burjeel Holdings aggregate procurement across multi-emirate networks, negotiating volume discounts that small independents cannot match, thereby widening cost advantages and reinforcing consolidation.

Regulatory Landscape

Diagnostic imaging equipment placement in the UAE is governed by a federal framework anchored by the Emirates Drug Establishment (EDE), which became the primary federal authority for regulating and registering medical products after the transfer of core services from the Ministry of Health and Prevention. Federal Decree-Law No. (38) of 2024 provides the legal basis for importation and circulation controls, and manufacturers typically operate through a UAE-based Marketing Authorization Holder registered on the EDE digital portal, with product risk classification (Class I to IV) influencing the registration pathway.

Technical compliance runs in parallel through the Ministry of Industry and Advanced Technology (MoIAT), which administers UAE standardization and conformity assessment for regulated products, including issuance of UAE Certificates of Conformity where applicable. For ionizing-radiation modalities (for example, X-ray and CT), import and commissioning are also tied to licensing and safety requirements under the Federal Authority for Nuclear Regulation (FANR), adding an additional compliance gate beyond medical device registration and reinforcing demand for locally compliant installation, shielding, and acceptance testing capabilities.

Value Chain Analysis

The UAE diagnostic imaging equipment value chain starts with predominantly imported systems (CT, MRI, ultrasound, X-ray, and hybrid modalities) from global OEMs, with product registration, classification, and local representation coordinated through the EDE portal. Market access then flows through licensed local distributors and agents concentrated around Dubai logistics and healthcare hubs (including Jebel Ali Free Zone and Dubai Healthcare City), which support import clearance, warehousing, and last-mile delivery to hospitals and imaging centers. Service delivery is a core part of the chain, as providers increasingly procure systems bundled with software, upgrades, and uptime commitments under long-term vendor-managed contracts.

Downstream, providers connect imaging workflows into enterprise IT and health information exchanges, which raises the importance of locally hosted PACS, cybersecurity controls, and interoperability support. Regulatory and supply resilience requirements are also reshaping channel strategy: Federal Decree-Law No. 38 of 2024 (effective January 2, 2025) introduced a multi-agent approach for import and distribution, pushing OEMs to reconsider exclusive arrangements and build redundancy across distribution and service partners. Ongoing constraints in certified field engineering capacity, particularly outside Dubai and Abu Dhabi, keep parts logistics, on-site maintenance, and training as key bottlenecks that influence vendor selection and total cost of ownership.

Competitive Landscape

The UAE diagnostic imaging equipment market is moderately concentrated, with GE HealthCare, Siemens Healthineers, and Philips collectively holding an estimated 55%-60% market share, driven by long-term value partnerships. Siemens has secured a 10-year agreement with American Hospital Dubai, offering a comprehensive package of supply, software, and service. GE counters with per-scan contracts featuring the SIGNA Hero 3 T MRI and Revolution Apex CT systems. Philips leverages its enterprise informatics capabilities to secure PACS upgrades integrated with Malaffi connectivity.

Canon Medical, Fujifilm, and Hologic are positioned in high-growth segments. Canon focuses on CT and ultrasound through its partnership with Aster, Fujifilm specializes in advanced visualization and PACS, and Hologic drives growth in breast tomosynthesis under the national screening program. Chinese OEMs, such as United Imaging, showcased competitively priced 3 Tesla MRI and spectral CT systems at Arab Health. However, they face challenges in penetrating Tier-1 hospital tenders due to limited service network depth and the need for stronger clinical evidence.

Emerging disruptors, including QT Imaging with its acoustic breast CT, Hyperfine's portable MRI, and Butterfly Network's handheld ultrasound, are addressing point-of-care gaps but collectively account for less than 5% of the market. Competitive strategies increasingly focus on AI-driven workflows, cloud-ready archives compliant with data-residency regulations, and financing models designed to shift capital expenditure burdens off provider balance sheets.

United Arab Emirates Diagnostic Imaging Equipment Industry Leaders

Fujifilm Holdings Corporation

Koninklijke Philips N.V.

Siemens Healthineers AG

GE HealthCare

Canon Medical System Corporation

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

A clear opportunity sits in AI-enabled enterprise imaging and locally compliant informatics stacks that improve throughput under constrained radiologist supply, while staying aligned with UAE data-residency and cybersecurity requirements. Providers are already deploying network-level imaging platforms, such as RAK Hospital adopting an AI-powered enterprise imaging platform from PaxeraHealth (June 2026), and payer-driven volume growth under the nationwide health-insurance mandate is reinforcing the business case for workflow automation, structured reporting, and auto-triage integrated into PACS and modality consoles.

Premium cross-sectional upgrades and new-site buildouts are also expanding procurement whitespace beyond routine replacement cycles. Examples include Al Zahra Hospital Dubai installing Siemens Healthineers NAEOTOM Alpha photon-counting CT (February 2026) for higher-acuity cardiac and neurovascular imaging, and Aster DM Healthcare announcing an AED 1 billion UAE expansion program that includes two new hospitals in Dubai and an annex at Aster Hospital, Al Qusais. As hospital groups and diagnostic centers scale, demand is shifting toward bundled solutions, including financing, multi-year service coverage, and AI-ready platforms that reduce downtime risk and accelerate time-to-report for medical tourism and insured populations.

Recent Industry Developments

- June 2026: RAK Hospital implemented an AI-powered enterprise imaging platform from PaxeraHealth to consolidate imaging workflows and data access across its network. The move supports faster clinical collaboration and strengthens the role of software-led enterprise imaging as a purchasing driver alongside new hardware.

- January 2026: QT Imaging signed a USD 24 million exclusive distribution agreement with Al Naghi Medical Co. for QTI Breast Acoustic CT scanners in the UAE, with a deployment plan of 43 units through 2028. The deal expands access to alternative breast imaging technology and increases competitive pressure in women’s health imaging where screening-driven volumes favor differentiated modalities.

- January 2025: Siemens Healthineers signed a 10-year value partnership with American Hospital Dubai that included installing the Nexaris Angio-CT hybrid suite. The agreement reinforces the UAE shift toward long-term, outcomes-oriented procurement models that bundle equipment, software, and service to manage technology obsolescence and uptime.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the market covers revenues generated from diagnostic imaging equipment sold and installed in the UAE for clinical imaging, across major modalities used by hospitals and imaging centers.

Scope exclusions: imaging services, radiology reading fees, service contracts, maintenance-only revenues, and consumables are excluded from this market size.

Segmentation Overview

- By Modality

- MRI

- Computed Tomography

- Ultrasound

- X-Ray (Digital, Analog)

- Nuclear Imaging

- Fluoroscopy & C-arm

- Mammography

- By Portability

- Fixed Room-based Systems

- Mobile / Portable Systems

- Hand-held & Wearable Imaging Devices

- By Application

- Cardiology

- Oncology

- Neurology

- Orthopedics & Trauma

- Gastroenterology & Hepatology

- Women’s Health (Ob/Gyn & Breast)

- Urology

- Emergency & Critical Care

- Sports Medicine & Rehabilitation

- Other Applications

- By End User

- Hospitals

- Diagnostic Imaging Centers

- Specialty Clinics & Day-Surgery Centers

- Mobile Imaging Service Providers

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the UAE healthcare context and to anchor demand signals that can be checked year over year. We reviewed public sources such as UAE Ministry of Health and Prevention releases, Dubai Health Authority updates, Abu Dhabi Department of Health information, and international datasets from the World Health Organization and World Bank for population, disease burden, and system capacity indicators.

To translate these signals into an equipment demand view, we also used import and trade references (where available) and scanned peer-reviewed clinical and radiology journals for modality adoption patterns and utilization drivers. Company annual reports, investor presentations, and reputable press were used to cross-check launch timelines and replacement-cycle commentary. Paid subscriptions supporting company financials and patent databases were used selectively to validate supplier exposure and technology direction. The sources listed above are illustrative only, and many other public references were also used for data collection, cross-checking, and clarification.

Primary Interviews and Surveys

Primary work focused on confirming what drives UAE equipment buying decisions and how procurement translates into annual demand. We spoke with a mix of hospital imaging heads, diagnostic center operators, biomedical engineering teams, distributors, and modality-focused experts to validate assumptions on installed-base replacement, portable versus fixed purchases, and tender and budget timing across the UAE.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 13% | |

| Mid tier: 46% | Functional/Unit leaders: 31% | |

| Smaller Players: 21% | Managers: 56% |

Market-Sizing & Forecasting

Sizing starts with a top-down reconstruction of the UAE demand pool by linking healthcare capacity and imaging activity signals to equipment needs, and then mapping those needs to modality-level spending. Because buying decisions are often tied to specific projects and replacement planning, the model also uses selective bottom-up approximations, where sampled ASP-by-modality and unit volumes from channel checks are used to validate and adjust totals.

Key inputs (illustrative) include modality mix shifts between X-ray, CT, MRI, ultrasound, and other systems, the split of portable versus fixed installations, replacement cycles tied to equipment age and uptime expectations, tender and procurement timing in large health systems, and expansion in diagnostic imaging centers. Forecasts use scenario analysis supported by expert views on capital budget direction, expected installation lead times, and the pace of portable adoption, and then the scenarios are blended into the final base case. When bottom-up volume signals are incomplete for smaller sites, we handle the gaps by applying conservative coverage factors that are rechecked through interviews and import and shipment context.

Data Validation & Update Cycle

Outputs are validated through multiple checks so totals remain consistent with the real-world buying pattern. We compare modeled results against independent signals such as healthcare spending direction, facility expansions, and modality adoption commentary, and then investigate large year-to-year jumps before sign-off.

A second analyst review is completed to recheck assumptions, units, and currency conversion timing, followed by targeted re-contacts when a variance cannot be explained by known drivers. The report is refreshed annually, and if a material event impacts procurement or pricing, interim updates are triggered. Before delivery, we run a final pass so clients receive the latest updated view rather than an older snapshot.

Mordor Intelligence's UAE Diagnostic Imaging Equipment Market Market Sizing Compared With Other Published Estimates

Published market sizes for UAE diagnostic imaging equipment can look far apart even when the topic sounds the same, since the market boundary and the year used for comparison are often not aligned. Differences also show up when one estimate leans more on shipment value assumptions, while another leans more on installed base and replacement expectations.

The key gap drivers here are usually scope and price logic, followed by how frequently assumptions are refreshed. Some sources may mix equipment with imaging services or include long-term service contracts, and others may use aggressive ASP progression without checking what is actually tendered in public and semi-public procurement.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 167.41 M (2025) | |

| Industry Publisher A | USD 283.12 M (2025) | This figure appears closer to a broader medical imaging definition where adjacent revenues can be counted, and modality totals may be built using higher assumed ASP levels and wider application coverage that can inflate equipment-only demand. |

| Market Publisher B | USD 1.50 B (2023) | The scale suggests a wider basket than annual equipment revenues in a single year, which can happen if multi-year project values, services, or a wider device scope is embedded, and if the base year is not aligned with current procurement cycles. |

The table shows a wide spread versus the 2025 value because the boundary is not treated the same across sources, and year alignment is also inconsistent. In Mordor Intelligence's model, the total is kept to equipment revenues in the UAE by modality, and it excludes imaging services and maintenance-only revenues, which is why broader medical imaging totals come out higher. With the scope kept consistent and the main inputs tied back to procurement and replacement signals, the output is easier to reproduce and to explain on a planning call.

Key Questions Answered in the Report

What is the current value of the UAE diagnostic imaging equipment market?

The market stood at USD 177.54 million in 2026 and is on track to reach USD 238.15 million by 2031.

How fast will CT adoption grow in the Emirates?

CT revenue is forecast to expand at an 8.43% CAGR through 2031, the quickest clip among all imaging modalities.

Why are diagnostic centers gaining ground on hospitals?

Centers offer shorter wait times and cater directly to expatriates and medical tourists, resulting in a projected 7.54% CAGR in spending through 2031.

What role does mandatory health insurance play in imaging demand?

Universal coverage introduced in 2025 eliminated upfront fees, producing double-digit volume spikes and de-risking capital investment in high-throughput scanners.

Which vendors dominate the UAE scanner landscape?

GE HealthCare, Siemens Healthineers, and Philips together command about 55%-60% of local revenue via multi-year value-partnership deals.

How do data-residency rules affect cloud PACS adoption?

Regulations require health data to stay inside the UAE, prompting providers to adopt locally hosted solutions like e& enterprise's sovereign cloud PACS rather than overseas archives.

Page last updated on: