Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.17 Billion |

| Market Size (2026) | USD 1.24 Billion |

| Market Size (2031) | USD 1.64 Billion |

| Growth Rate (2026 - 2031) | 5.82% CAGR |

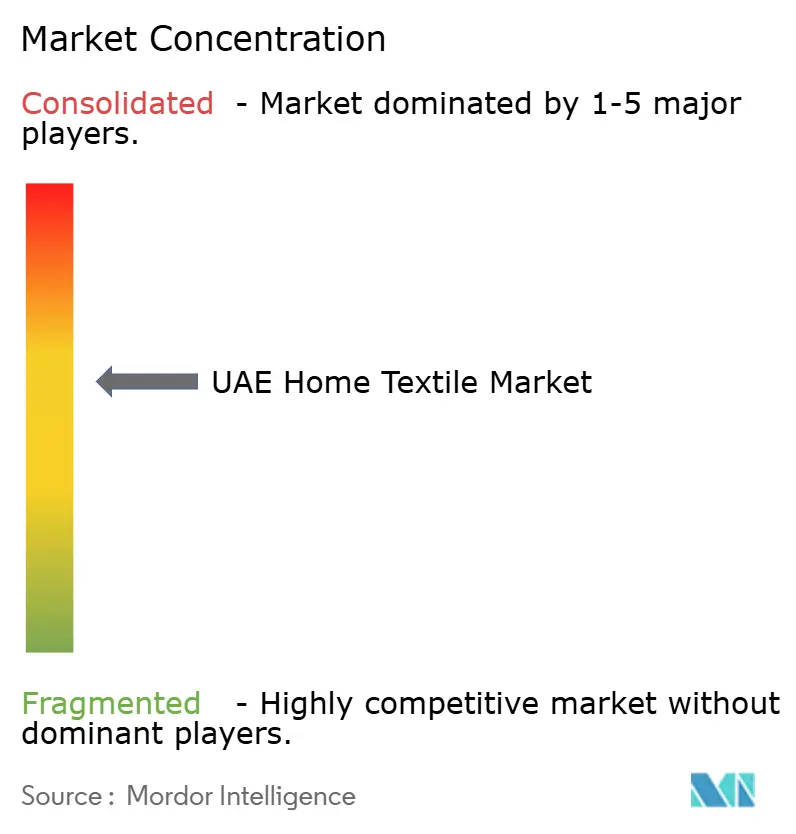

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

UAE Home Textile Market Analysis by Mordor Intelligence

The UAE home textile market size is expected to grow from USD 1.17 billion in 2025 to USD 1.24 billion in 2026 and is forecast to reach USD 1.64 billion by 2031 at 5.82% CAGR over 2026-2031. Demand is underpinned by the confluence of sustained expatriate household formation, a strong pipeline of hospitality openings linked to Tourism Vision 2030, and a rising consumer preference for certified-sustainable, premium fabrics. The UAE home textile market enjoys insulation from cyclical shocks because hotel operating standards require frequent linen rotation, while retail landlords intensify experiential merchandising to counter e-commerce competition. Digital transformation, highlighted by same-day delivery and buy-now-pay-later (BNPL) options, converts browsing into higher-value baskets that boost average order values by 25–50% across major chains. However, import-dependent raw-material costs and new customs-tariff granularity compel retailers to adopt agile sourcing and precision inventory planning.

Key Report Takeaways

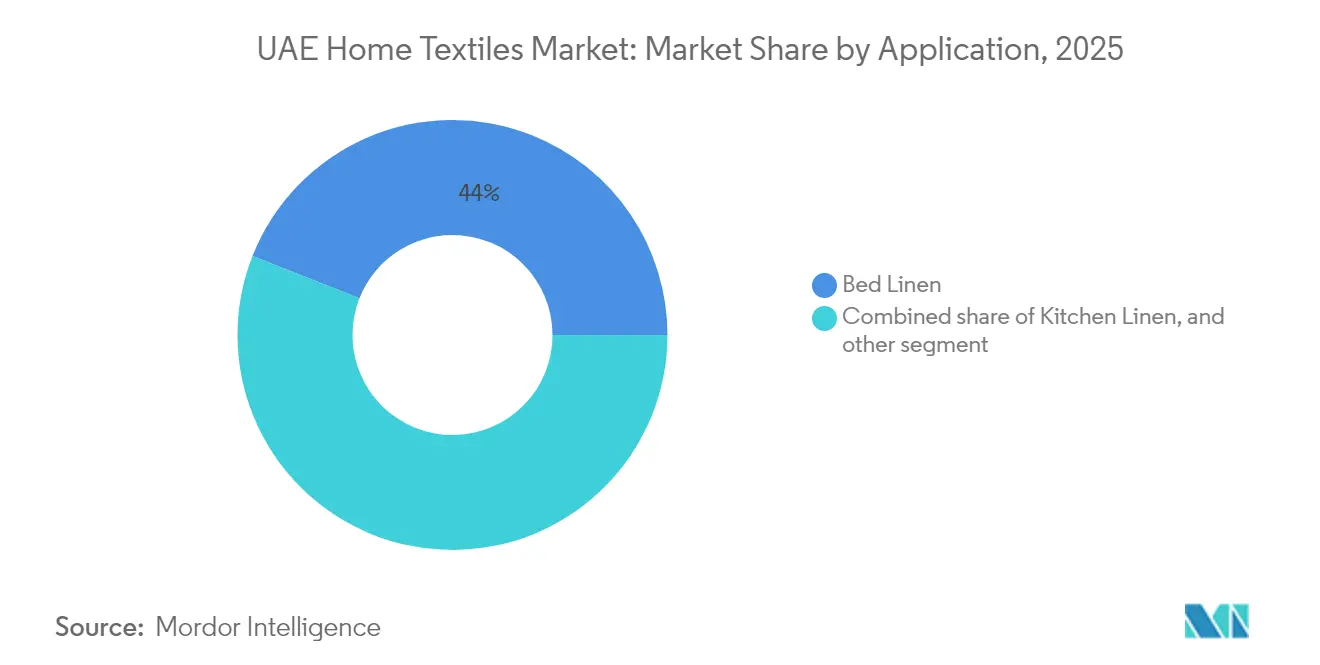

- By application, bed linen commanded 44.02% of the UAE home textile market size in 2025, while upholstery is accelerating at a 8.74% CAGR to 2031.

- By material, cotton retained a 55.92% share of the UAE home textile market in 2025; bamboo and other natural fibers are growing at a 10.24% CAGR across the same horizon.

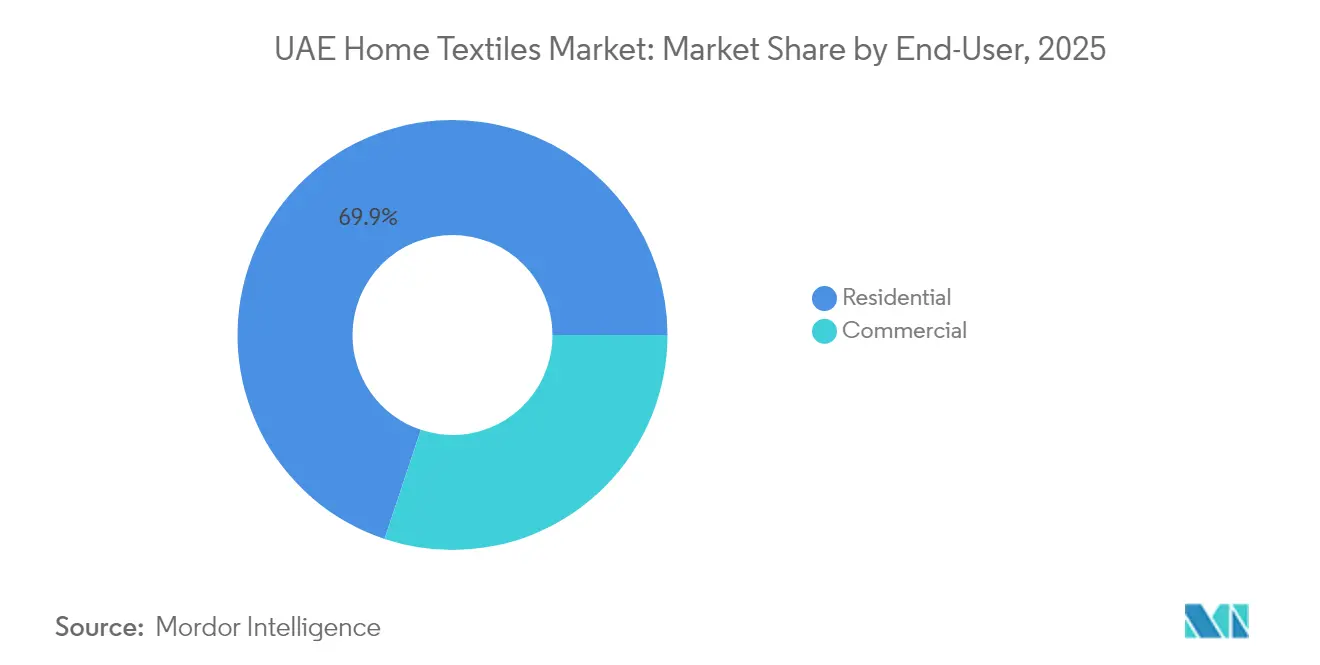

- By end-user, residential accounted for 69.88% of the UAE home textile market demand in 2025, while the commercial segment advances at an 7.95% CAGR through 2031.

- By distribution channel, offline outlets held an 80.74% share in 2025, but online revenue is scaling at a 13.21% CAGR through 2031 as BNPL adoption widens.

- By geography, Dubai captured 47.72% of the UAE home textile market share in 2025, whereas the Northern Emirates are expanding at a 10.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

UAE Home Textile Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising expatriate population fueling household formation | +1.2% | Dubai, Abu Dhabi, Sharjah | Medium term (2–4 years) |

| Rapid growth of e-commerce furnishing platforms | +0.9% | UAE-wide urban centers | Short term (≤ 2 years) |

| Government housing initiatives for Emiratis | +0.8% | Abu Dhabi, Northern Emirates | Long term (≥ 4 years) |

| Hospitality boom ahead of Tourism Vision 2030 | +1.4% | Dubai, Abu Dhabi, coastal emirates | Medium term (2–4 years) |

| Sustainability shift toward organic/bamboo textiles | +0.6% | Dubai, Abu Dhabi, premium segments | Long term (≥ 4 years) |

| Uptake of smart/functional home textiles | +0.4% | Dubai, Abu Dhabi, luxury hospitality | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Expatriate Population Fueling Household Formation

The UAE’s expatriate demographic—approximately 85% of the 9.8 million total shows no signs of contraction as Golden Visa reforms and virtual-work permits make long-term residency more attractive [1]U.S. Department of Commerce, “United Arab Emirates – Market Overview,” export.gov. Each new visa approval translates into an entire dwelling requiring bedding, bath linen, curtains, and décor, thereby injecting predictable baseline demand into the UAE home textile market. Corporate relocations in finance, tech, and professional services funnel highly paid talent into Dubai and Abu Dhabi, and these workers typically invest in premium 400-thread-count or higher cotton sheets rather than economy blends. Family reunifications further multiply household unit counts, particularly in suburban communities around Dubai Hills and Yas Island. Short-term rental operators, enabled by Dubai’s flexible licensing, cycle linens every few months to meet hospitality cleanliness standards, compounding fabric turnover. Altogether, population inflow adds a structural growth layer that cushions the UAE home textile market against global slowdowns.

Rapid Growth of E-Commerce Furnishing Platforms

Online penetration may still trail electronics or fashion, but home-textile e-tail is growing at a 13.88% CAGR—more than double offline expansion. Fast and free same-day delivery resolves the tactile-trust gap once associated with duvet cover purchases, while BNPL tools like Tabby and Tamara smooth ticket sizes exceeding AED 1,000 (USD 272) without interest charges. E-retailers deploy augmented-reality room simulators so shoppers can transpose color-accurate bedspreads onto existing décor, dropping return rates to low single digits at IKEA UAE [2]IKEA UAE, “Click & Collect,” ikea.com. Digital channels lend themselves to storytelling around sustainability credentials, a critical differentiator in bamboo and organic-cotton assortments. Emerging direct-to-consumer brands exploit social commerce on Instagram and TikTok, achieving near-real-time feedback loops that guide micro-collections. The result is a flywheel in which retailers and insurgent labels alike redirect marketing to digital, expanding the UAE home textile market’s reach well beyond traditional mall footfall.

Government Housing Initiatives for Emiratis

Federal and emirate-level housing programs—such as Abu Dhabi’s Dhiyafati initiatives—add institutional purchase volumes for standardized bed-and-bath kits. The “Made in the Emirates” mark incorporated via Cabinet Resolution 16-2023 obliges public agencies to favor locally manufactured textiles, unlocking guaranteed off-take for mills based in Ajman and Ras Al Khaimah. These government orders often include multi-year maintenance contracts that specify replacement cycles, anchoring predictable revenue streams inside the UAE home textile market. Suppliers benefit from payment-term security and lower marketing costs relative to retail operations. Moreover, public projects frequently adhere to sustainability thresholds laid out by the Ministry of Industry and Advanced Technology, encouraging OEKO-TEX-certified or recycled-polyester inputs. Over the long term, housing initiatives also cultivate a culture of home ownership among Emiratis, fostering discretionary upgrades from entry-level cotton to luxury linen as disposable income grows.

Hospitality Boom Ahead of Tourism Vision 2030

Tourism Vision 2030 targets 40 million hotel guests, a near-tripling from 2022’s 14.3 million figure, forcing hotel developers to accelerate room-key delivery. Newbuilds such as Ciel Tower (1,004 rooms) and Wynn Al Marjan (1,542 rooms) specify 300–400 gsm towel sets and 600-thread-count bedding to match international chain standards. Hotel operators typically stock four linen sets per bed to ensure constant rotation, thereby quadrupling initial purchase orders versus room count. Premium-branded residences adopt hotel specifications to satisfy service-apartment tenants, blending residential and hospitality procurement patterns. Suppliers that can demonstrate antimicrobial treatments or recycled-water wash durability acquire preferred-vendor status, an invaluable moat inside the UAE home textile market. The continuous inflow of business and leisure travelers thus exerts a sustained pull on high-turnover commercial-grade textiles.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising retail prices amid VAT & cost-of-living pressure | -0.8% | UAE-wide mid-market | Short term (≤ 2 years) |

| Supply-chain risk from import-dependent raw materials | -0.6% | UAE-wide | Medium term (2–4 years) |

| Fragmented traditional retail outside Tier-1 cities | -0.4% | Northern Emirates, Sharjah suburbs | Medium term (2–4 years) |

| Local-content rules elevate compliance costs | -0.3% | UAE-wide importers | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Retail Prices Amid VAT & Cost-of-Living Pressure

Effective VAT pass-through combined with elevated utility fees narrows discretionary budgets for middle-income households, the segment most likely to defer linen refreshes. Although a 13% net spending-intent lift is forecast for 2025, 38% of consumers have already trimmed luxury purchases, prompting retailers to re-engineer price-laddering strategies. Introduction of a 12-digit Integrated Customs Tariff expands HS codes from 7,800 to more than 13,400 lines, increasing administrative overhead at ports [3]PricewaterhouseCoopers, “UAE Customs & International Trade Update,” pwc.com. Retailers compensate by thinning SKU depth or renegotiating payment terms, potentially dampening the breadth of choice. Mid-market private-label programs help offset procurement inflation but struggle to market sustainability or smart-textile features effectively. Therefore, while affluent consumers remain resilient, growth in the UAE home textile market risks deceleration if mid-tier price elasticity intensifies.

Supply-Chain Risk from Import-Dependent Raw Materials

The UAE imports virtually all raw cotton and synthetic yarn, making the supply chain vulnerable to geopolitical tremors such as U.S. tariff hikes on Chinese goods or Red Sea shipping disruptions [4]Fibre2Fashion, “US Tariff Surge: Implications,” fibre2fashion.com. Weather-induced crop failures—from drought in Texas to floods in Pakistan—cause gyrations in global cotton prices; a 20% spike in 2024 forced some UAE wholesalers to absorb costs rather than pass them onto retailers. Egyptian extra-long-staple cotton supplies have tightened due to foreign-exchange curbs, driving hospitality buyers to alternative blends that may not meet brand specs. Small and medium retailers lacking hedging mechanisms end up over-stocked or out-of-stock, impairing service levels. Inventory buffering inflates working-capital requirements, and extended lead times complicate fresh-collection launches. Collectively, these frictions weigh on margin and agility within the UAE home textile market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Application: Bed Linen Dominance Drives Hospitality Expansion

Bed linen generated 44.02% of 2025 revenue, equivalent to roughly USD 0.52 billion of the UAE home textile market size, reflecting both residential upgrades and high-turnover hotel requirements. Luxury properties stock four sets per bed and replace them after 150 wash cycles, creating a recurrent demand loop that buffers cyclicality. Thread-count escalation remains a positioning tool: five-star hotels mandate 600-thread-count sateen sheeting to differentiate guest experience, while branded residences borrow the same playbook to command premium rents. Residential buyers influenced by hotel stays increasingly replicate high-GSM, OEKO-TEX-certified duvet covers at home, reinforcing the aspirational feedback loop. As a result, suppliers who master commercial-grade durability while maintaining soft hand-feel capture both institutional and retail clients, reinforcing bed linen’s weight inside the UAE home textile market.

Upholstery’s 8.74% CAGR stems from a residential mega-project pipeline exceeding 70,000 units, including Palm Jebel Ali and Azizi Venice, each flaunting interior packages reliant on sofa fabrics, cushions, and drapes . Architects specify performance chenille and velvet blends treated for stain resistance, stimulating incremental meterage per unit. Bath linen maintains steady mid-single-digit growth as spas and wellness centers expand; new facilities demand double-ply 800 gsm towels to withstand chlorine exposure. Kitchen linen sales rise with the post-pandemic cooking wave, benefiting manufacturers of Teflon-coated aprons and heat-resistant gloves. Carpets transition toward accent-rug sales as hard-surface flooring dominates new constructions, yet Berber and monochrome patterns still feature in premium villas. Collectively, application diversification injects resilience into the UAE home textile market and balances dependence on bed linen.

By Material: Cotton Leadership Challenged by Sustainable Alternatives

Cotton represents 55.92% of 2025 revenue—about USD 0.65 billion within the UAE home textile market size—thanks to its comfort properties and established supply chains. Egyptian long-staple varieties dominate luxury categories, while Indian compact-spun cotton finds favor in value-tier sheeting. OEKO-TEX STANDARD 100 verification secures hotel contracts, as chains fear guest complaints over chemical residue. High-GSM cotton also meets spa durability standards, where bleach cycles would degrade lesser fibers. Despite logistic costs, cotton’s familiarity sustains its hold in the UAE home textile market.

Bamboo viscose and flax linen scale at a 10.24% CAGR, attracting eco-conscious buyers seeking naturally antibacterial, breathable options for desert climates. Retailers highlight water-usage reductions of up to 50% in bamboo cultivation compared with conventional cotton, bolstering marketing narratives. Linen’s textured aesthetic aligns with interior-design trends favoring neutral palettes and artisanal finishes. Synthetic fibers, while facing green-washing scrutiny, remain indispensable for flame retardancy in hospitality curtains. Recycled polyester blends appear in cushion liners and mattress protectors, satisfying hotel chain sustainability pledges without sacrificing stain resistance. Material plurality thus secures supply-chain resilience within the UAE home textile market and widens consumer choice.

By End-User: Commercial Acceleration Outpaces Residential Growth

Residential buyers contributed 69.88% of 2025 sales, buoyed by an influx of long-term expatriates eligible for 10-year visas, who are more willing to invest in high-quality sheets rather than rental stopgaps. Villa owners in Dubai Hills and Al Raha Beach favor hotel-grade linen to mimic five-star experiences, and 77% of residents prioritize wellness features such as hypoallergenic pillows. Short-term rental operators, including Airbnb super-hosts, replace linens every quarter to protect star ratings, adding an institutional dimension to the residential category. Retailers target this segment with bulk-buy promotions and convenient bundle packs, ensuring the UAE home textile market continues to draw strength from the residential channel.

Commercial demand, though on a smaller base, is expanding faster at 7.95% CAGR, propelled by room-inventory growth and governmental housing tenders. Hotels often tie suppliers into three-year framework agreements that guarantee volume but require exacting quality audits. Healthcare facilities specify antimicrobial fabrics capable of withstanding autoclave sterilization, while educational dormitories seek value-engineered yet durable options. Corporate offices invest in acoustic drapes and ergonomic seat cushions as part of hybrid-workplace redesigns. Supplier agility—offering mixed pallets of towels, sheets, and drapery—wins contracts that span multiple commercial sub-sectors. The result is a diversified contract-sales ecosystem that adds depth to the UAE home textile market.

By Distribution Channel: Digital Transformation Accelerates Omnichannel Shift

Brick-and-mortar venues still account for 80.74% of 2025 revenue thanks to the tactile imperative of selecting fabrics and the mall-centric leisure culture. Landmark malls like Dubai Mall and the newly opened Nad Al Sheba Mall function as lifestyle destinations, where visitors explore curated room vignettes and collect swatches. Retailers integrate RFID tagging into showrooms so customers can scan and seamlessly transfer items into digital carts for home delivery. These stores double as micro-fulfillment centers, ensuring faster last-mile dispatch to nearby districts. Thus, offline keeps relevance by embracing experiential retail rather than pure shelf stocking.

Online channels, expanding at a 13.21% CAGR, flourish by solving pain points: same-day delivery eliminates waiting time, live-chat advisors mitigate sizing confusion, and BNPL increases cart conversion for premium bundles. Marketplaces segment search filters by fabric certification—OEKO-TEX, GOTS—simplifying ethical shopping journeys. Pure-plays such as HomeBox Digital roll out AR visualization to preview rug placement at scale, reducing returns. Quick-commerce units like Carrefour Now deliver emergency linen replacements within an hour, a boon for serviced apartments facing last-minute check-ins. Collectively, omnichannel fluidity expands the UAE home textile market’s addressable audience and equalizes access for consumers in secondary cities.

Geography Analysis

Dubai holds 47.72% of 2025 sales in the UAE home textile market, powered by 1,198 hotels generating AED 38 billion (USD 10.35 billion) in annual revenue and acting as high-frequency textile buyers. The emirate’s extensive mall ecosystem, from Mall of the Emirates to Dubai Hills Mall, fosters brand discovery for international labels, while advanced logistics infrastructure enables same-day delivery across all districts. Dubai residents also report the highest willingness to pay for sustainability credentials, translating into premium shelf space for bamboo and organic-cotton SKUs. However, rising rents and regulatory compliance costs incrementally erode retailer margins, encouraging diversification into Northern Emirates production hubs.

Abu Dhabi constitutes the second-largest geography, benefiting from steady government employment, mega cultural projects, and a maturing tourism strategy anchored by Saadiyat Island museums. Public-sector housing schemes create predictable institutional orders favoring “Made in the Emirates” textiles, while luxury resorts such as Jumeirah Saadiyat and the forthcoming Saadiyat Grove demand upscale linens conforming to eco-specifications. The emirate also serves as a springboard for western-region supply to Ruwais and Al Dhafra, broadening distribution footprints inside the UAE home textile market.

The Northern Emirates—Ajman, Ras Al Khaimah, Fujairah, and Umm Al Quwain—record the fastest 10.35% CAGR, leveraging lower industrial-land rents and free-zone incentives to attract spinning, weaving, and finishing units. Ajman’s manufacturing contributes 35% of the emirate's GDP, offering vertically integrated mills that shorten lead times for retailers. Ras Al Khaimah’s maritime ports streamline exports to Saudi Arabia, converting local plants into regional hubs. Though retail spend per capita trails Dubai, the rising population and improved transport links via Etihad Rail widen market access. Sharjah bridges the gap, mixing a manufacturing-heavy northern zone with retail-rich Al Majaz waterfront, making it an increasingly balanced contributor to the UAE home textile market’s geographic mosaic.

Competitive Landscape

Fragmentation remains moderate: the top five organized players secure the majority of sales, leaving meaningful white space for niche entrants. IKEA anchors the value-premium spectrum with branded Scandinavian designs and circular-economy buy-back schemes. Home Centre, backed by Landmark Group, plans a USD 1 billion investment that will add 400 stores and expand e-commerce capacity by 2028. Danube Home infuses private-label assortments that squeeze middle-income price points yet still carry OEKO-TEX tags to signal safety.

International consolidation is gathering pace, as illustrated by TJX Companies’ USD 360 million stake in off-price specialist Brands for Less, injecting global procurement muscle into fast-turnover discount channels. Technology is the new battleground: augmented-reality configurators, AI-driven demand forecasting, and BNPL integration differentiate scale retailers, while direct-to-consumer upstarts—such as Indo Count Global’s relaunched Wamsutta brand—use vertical integration to shorten design-to-shelf cycles.

Sustainability remains a non-negotiable qualifier for luxury hotels, pushing suppliers to invest in traceability apps and low-impact dyeing processes. Mills based in the Northern Emirates gain a competitive advantage because local production reduces transport emissions, supporting LEED point accrual for hotel developers. As import tariffs and localization rules tighten, multi-region sourcing strategies and in-house compliance teams become core competencies. Competition, therefore, pivots on omnichannel sophistication, eco-credential authenticity, and compliance agility, shaping the evolving structure of the UAE home textile market.

UAE Home Textile Industry Leaders

Home Centre (Landmark Group)

IKEA

Danube Hom

Pan Emirates Home Furnishings

JYSK

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- March 2025: Majid Al Futtaim posted full-year 2024 UAE revenue growth of 7% and reported 97% mall-leasing occupancy, signaling robust consumer footfall that underpins textile sales. Digital revenue reached AED 2.7 billion (USD 735.19 million), with quick commerce now accounting for 38% of that figure—a key channel for last-minute towel and pillow orders. Management highlighted BNPL as a catalyst for a 45% increase in purchase frequency, underscoring digital’s growing clout in the UAE home textile market.

- November 2024: Landmark Group unveiled a USD 1 billion capital plan to open 400 stores across the GCC, India, and Southeast Asia over three years. Roughly 25% of that outlay targets Home Centre and Lifestyle formats in the UAE, with a strong emphasis on omnichannel technology and local warehousing. The expansion is expected to add 2,000 new SKUs in bed and bath linens, catering to both middle-income and premium shoppers.

- August 2024: TJX Companies signed a definitive agreement to acquire a 35% stake in Dubai-based Brands for Less for approximately USD 360 million. The off-price model allows surplus European and U.S. bed-and-bath lines to enter the UAE home textile market at aggressive price points. Analysts expect accelerated store rollout in Sharjah and Ras Al Khaimah, intensifying price competition in the value segment.

- July 2025: Indo Count Global relaunched the historic American brand Wamsutta as a premium direct-to-consumer bedding line, supported by a new Dubai office for Middle East fulfilment. The vertical integration model promises 15-day design-to-delivery cycles and leverages blockchain-based traceability to verify organic-cotton origin, addressing a core consumer concern in the UAE home textile market.

UAE Home Textile Market Report Scope

A subset of textiles used for home furnishings is known as home textiles. It consists of clothing and textiles for the interior. They are sometimes employed for ornamental purposes rather than for practical ones. This report aims to provide a detailed analysis of the home textile market of the UAE. It focuses on market dynamics, technological trends, and insights into various materials, applications, and product types. Also, it analyses the major players and the competitive landscape in the home textile industry of the UAE. As in UAE after the oil industry textile is the largest market for expansion of its market globally distribution channel plays a major role. UAE Home Textile Market is Segmented By Product (Bed Linen, Bath Linen, Kitchen Linen, Upholstery and Floor Covering), and By Distribution Channel (Supermarkets & Hypermarkets, Specialty Stores, Online and Other Distribution Channels). The report offers market size and forecasts in value (USD million) for all the above segments.

By Application

| Bed Linen |

| Bath Linen |

| Kitchen Linen |

| Upholstery |

| Others (Carpets and Area Rugs) |

By Material

| Cotton |

| Linen |

| Synthetic Fibers |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo etc.) |

By End-User

| Residential |

| Commercial |

By Distribution Channel

| Offline |

| Online |

By Geography

| Dubai |

| Abu Dhabi |

| Sharjah |

| Northern Emirates (Ajman, RAK, Fujairah, UAQ) |

| By Application | Bed Linen |

| Bath Linen | |

| Kitchen Linen | |

| Upholstery | |

| Others (Carpets and Area Rugs) | |

| By Material | Cotton |

| Linen | |

| Synthetic Fibers | |

| Other Materials (Wool, Hemp, Silk, Jute, Bamboo etc.) | |

| By End-User | Residential |

| Commercial | |

| By Distribution Channel | Offline |

| Online | |

| By Geography | Dubai |

| Abu Dhabi | |

| Sharjah | |

| Northern Emirates (Ajman, RAK, Fujairah, UAQ) |

Key Questions Answered in the Report

How big is the UAE home textile market in 2026?

The UAE home textile market size is USD 1.24 billion in 2026 and is set to grow at a 5.82% CAGR to 2031.

Which product category sells the most?

Bed linen remains the largest, making up 44.02% of 2025 revenue, thanks to hotel and residential demand.

What materials are consumers favoring for sustainability?

Bamboo and linen are gaining momentum, growing at a 10.24% CAGR as 60% of shoppers value eco-friendly options.

Which region shows the highest growth rate?

The Northern Emirates post a 10.35% CAGR, benefiting from manufacturing incentives and lower overheads.

How fast are online channels expanding?

E-commerce revenue is scaling at a 13.21% CAGR, driven by BNPL adoption and same-day delivery.

What competitive moves are shaping the sector?

Landmark’s USD 1 billion store rollout, TJX’s stake in Brands for Less, and Wamsutta’s direct-to-consumer launch illustrate strategic expansion and consolidation.

Page last updated on: