Thermoform Packaging Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

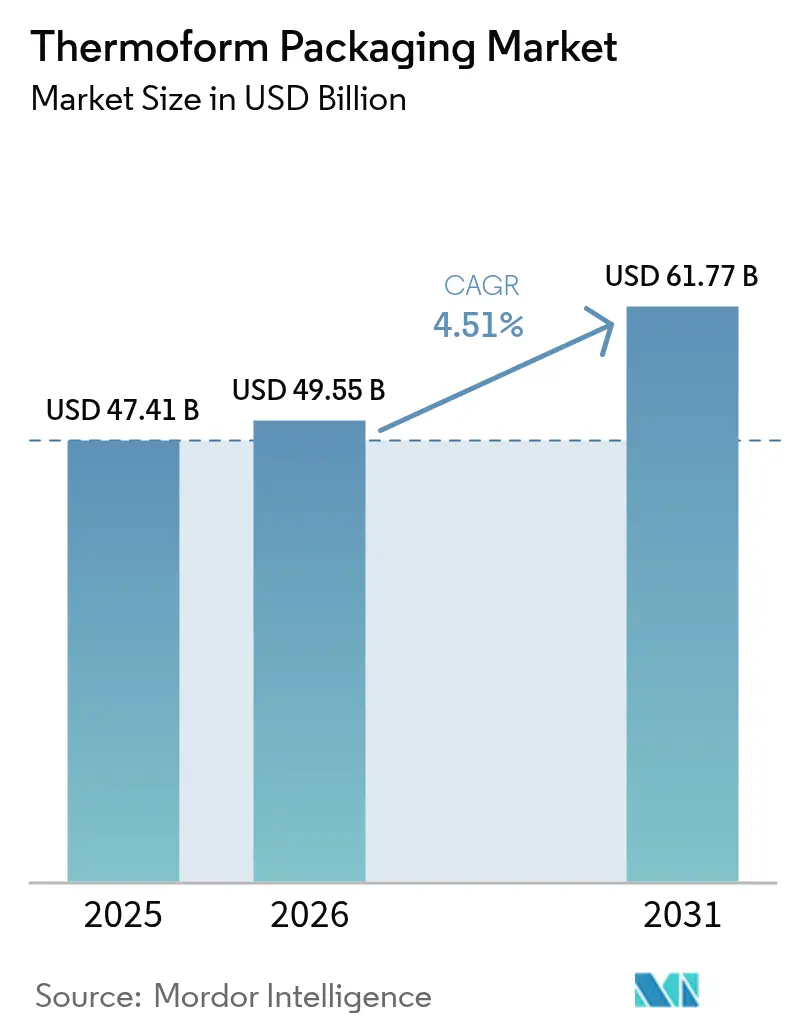

| Market Size (2026) | USD 49.55 Billion |

| Market Size (2031) | USD 61.77 Billion |

| Growth Rate (2026 - 2031) | 4.51% CAGR |

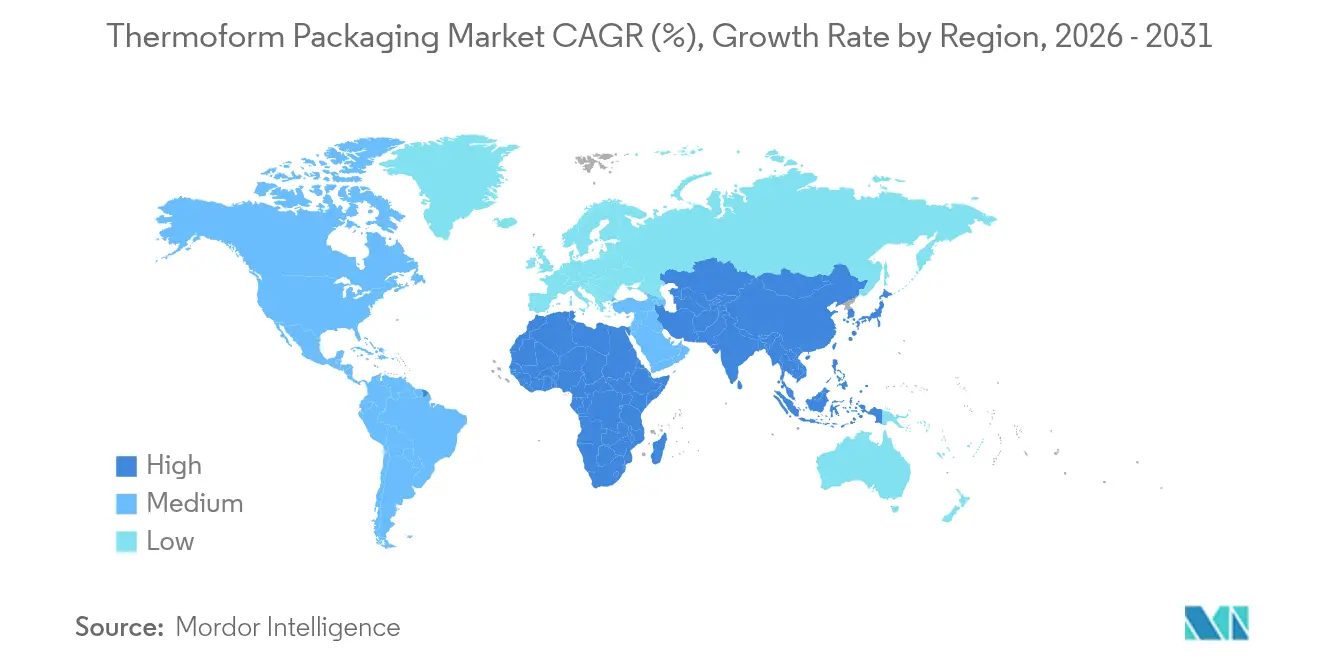

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia Pacific |

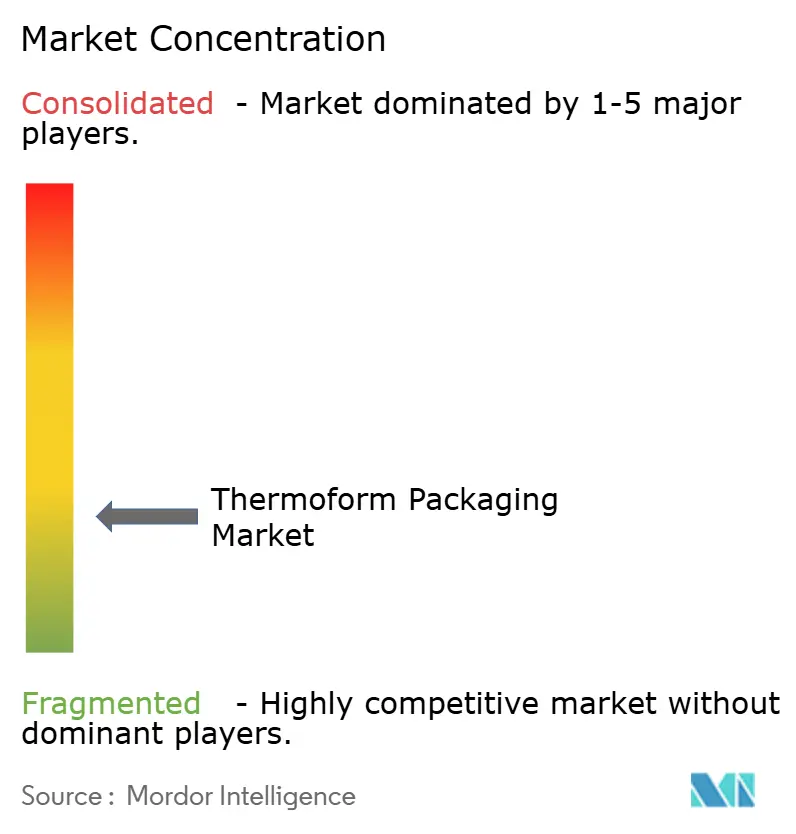

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thermoform Packaging Market Analysis by Mordor Intelligence

Thermoform packaging market size in 2026 is estimated at USD 49.55 billion, growing from 2025 value of USD 47.41 billion with 2031 projections showing USD 61.77 billion, growing at 4.51% CAGR over 2026-2031. Demand is underpinned by regulatory mandates for recyclable formats, steady penetration of Industry 4.0 production lines and sustained consumer preference for convenient, portion-controlled packs. Mono-material tray designs, meal-kit proliferation and the switch from glass vials to polymer blisters in injectables are reshaping product specifications, while automation‐enabled short runs are widening customer choice. Producers are balancing energy-intensive PET and polypropylene cycles with rPET and bio-resins, seeking cost offsets from eco-modulated fees. Strategic acquisitions—most notably Toppan’s purchase of Sonoco’s thermoforming assets and the Amcor–Berry merger—signal a race for scale, broader geographic reach and deeper material science capabilities.

Key Report Takeaways

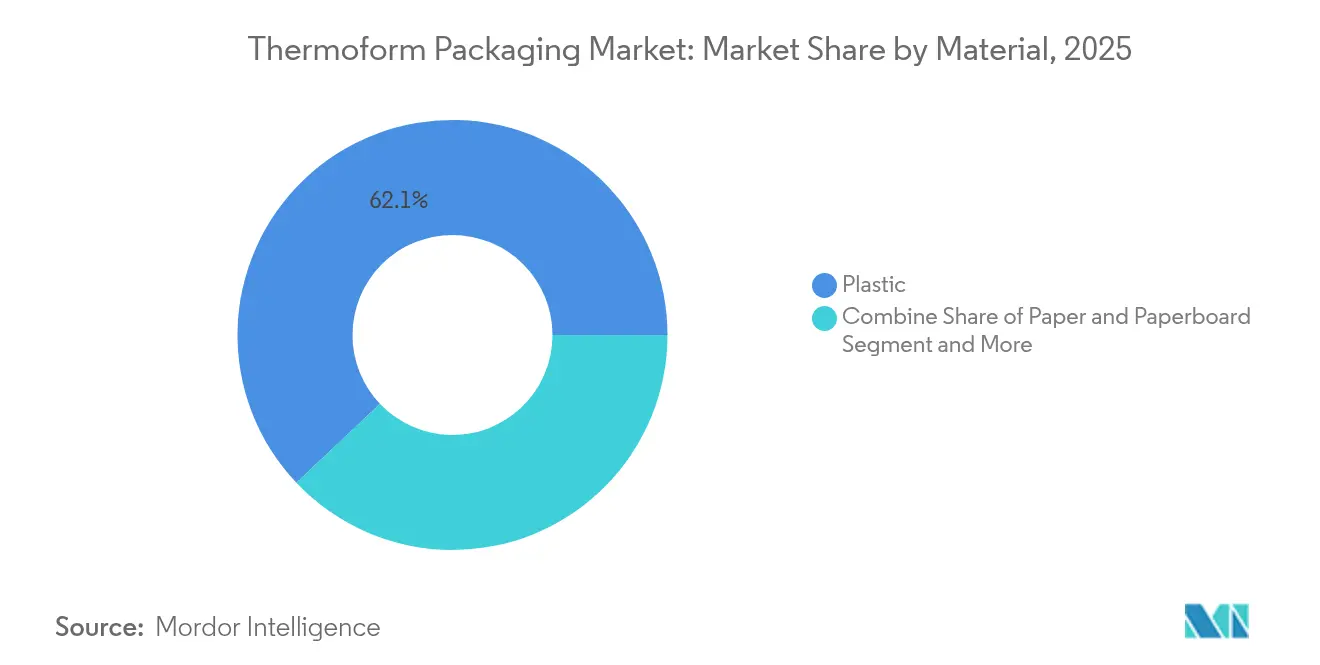

- By material, plastics retained 62.07% share of the thermoform packaging market size in 2025, while bio-based and biodegradable polymers are set to grow at an 8.21% CAGR to 2031.

- By product type, blisters led with 37.05% of revenue in 2025; trays and lids represent the fastest-growing segment at 7.6% CAGR.

- By packaging thickness, ≤200 µm held 59.85% share of the thermoform packaging market size in 2025, whereas the 200–500 µm band is advancing at an 7.95% CAGR.

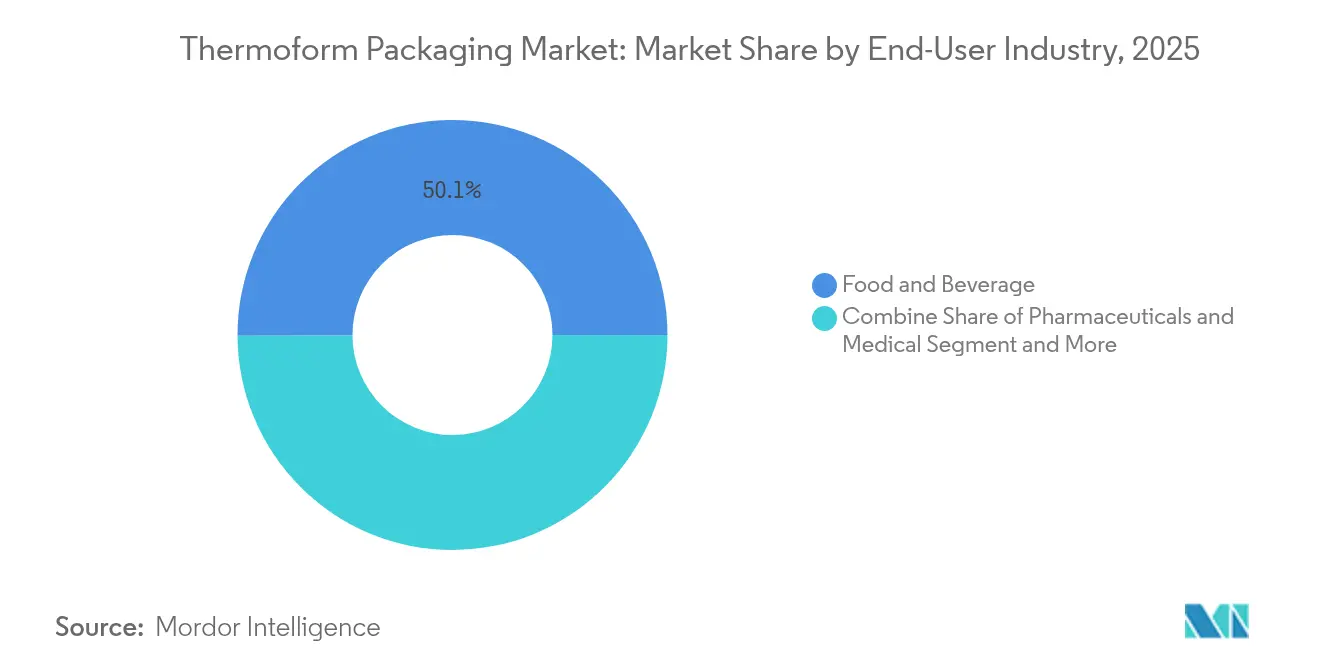

- By end-user industry, food and beverage contributed 50.06% of 2025 sales; pharmaceuticals and medical applications are growing the quickest at 9.04% CAGR.

- By technology, vacuum forming accounted for 44.8% of revenue in 2025, while pressure forming is expanding at 8.29% CAGR.

- By geography, Asia-Pacific commanded 39.76% of the thermoform packaging market share in 2025; the region is projected to expand at a 7.05% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Thermoform Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in demand for mono-material recyclable trays | +1.2% | Global, with EU and North America leading | Medium term (2-4 years) |

| Growth of fresh meal-kit delivery startups | +0.8% | North America & EU, expanding to APAC | Short term (≤ 2 years) |

| Per-capita rise in single-serve convenience foods | +0.9% | Global, particularly urban centers | Medium term (2-4 years) |

| Shift from glass vials to thermoform blister packs in injectables | +0.7% | Global, with APAC and North America core | Long term (≥ 4 years) |

| Automation lowering tooling-changeover cost (Industry 4.0 lines) | +0.6% | North America & EU, spill-over to APAC | Long term (≥ 4 years) |

| Government stimulus for on-shore pharmaceutical packaging | +0.5% | National, with early gains in US and EU | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Surge in demand for mono-material recyclable trays

Circular-economy rules are steering converters toward PET- or PE-only tray structures that pass curbside sortation tests. Graphic Packaging International’s Ecoflex™ PET line, for instance, meets the EU 2030 recyclability requirement while preserving top-seal integrity for chilled foods. Lower eco-modulated fees in Europe, coupled with brand owner commitments, boost the business case despite thicker walls needed to replicate multilayer barriers. ExxonMobil and Alpine jointly validated all-PE thermoforms that sustain oxygen barriers after nine recycling loops, underscoring material science advances.

Growth of fresh meal-kit delivery startups

HelloFresh and peer platforms have scaled to tens of millions of weekly servings, forcing packagers to optimize freshness over multiday transit, curb mass and hit carbon targets. Barrier-enhanced polypropylene trays paired with recyclable film lidding are proliferating, while vacuum-skin formats suppress drip loss and extend shelf life. Temperature sensors and QR-based provenance tags embedded into lids are emerging differentiators, fostering premium pricing.

Per-capita rise in single-serve convenience foods

Urban households prioritizing portion control translate into higher unit volumes per tonne of product. Berry Global’s 125 g PP dessert cups illustrate the shift, offering clarity and leak-proof seals for rail-commuter snacking. The dynamic also spills into over-the-counter pharmaceuticals, where unit-dose blisters support adherence.

Shift from glass vials to thermoform blister packs in injectables

Biologic therapies benefit from shatter-free polymer blisters that minimize particulate risk and lower cold-chain weight. US FDA fast-track pathways for advanced manufacturing further de-risk adoption. Brand owners report double-digit falls in breakage-related rejects after switching.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Accelerating plastic-use taxation in EU and North America | -0.9% | EU and North America, expanding globally | Short term (≤ 2 years) |

| Sporadic supply of medical-grade PP and PET sheets | -0.6% | Global, with APAC manufacturing hubs affected | Medium term (2-4 years) |

| High energy intensity vs. molded-fiber forming | -0.4% | Global, particularly energy-intensive regions | Medium term (2-4 years) |

| Limited barrier performance for oxygen-sensitive SKUs | -0.3% | Global, affecting food and pharmaceutical applications | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Accelerating plastic-use taxation in EU and North America

Italy’s levy of EUR 0.45/kg on virgin polymers joined the UK’s recycled-content tax in 2024, slicing converter margins unless material mixes exceed 30% recyclate. [1]EY, “Italy’s Plastic Tax Will Enter into Force on 1 July 2024,” ey.com Registered UK businesses remitted more than GBP 200 million in the first 18 months, highlighting fiscal bite.[2]MHA, “ESG & the Impact of Plastic Packaging Tax,” mha.co.uk

Sporadic supply of medical-grade PP and PET sheets

Resin rationing during 2024–2025 constrained healthcare converters. Kaysun’s database expansion and INVISTA’s MedSelect PP grades mitigated shortages but added qualification lead times.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Plastic dominance faces bio-based challenge

Plastics delivered 62.07% of 2025 sales, equating to the largest slice of the thermoform packaging market. rPET trays and PP cups stay competitive on barrier metrics and line efficiency, while price spikes in prime resin strengthen recyclate economics. Bio-based polymers, led by PLA blends, chart an 8.21% CAGR and benefit from policy carrots such as EU compostability labeling. The thermoform packaging market size for bio-based grades is projected to triple between 2025 and 2030 as high-volume food service chains lock in low-carbon packaging contracts. Scaling hurdles persist around feedstock supply continuity and heat-distortion thresholds beyond 60 °C.

In contrast, paperboard thermoforms carve niche demand in bakery and ready-meal lids where grease resistance can be engineered with plant-based coatings. Aluminum retains service in airline catering owing to lightweight-to-strength ratios but its share inches downward on cost volatility and recycling energy load. Cascades’ 100% rPET rolled-edge tray underlines how incumbent polymers evolve to satisfy rising recycled-content quotas.

By Product Type: Blisters lead while trays accelerate

Blister packs captured 37.05% of 2025 turnover, leveraging tamper evidence and unit-dose accuracy for OTC medicines and nutraceuticals. Volume growth aligns with ageing demographics and strict drug compliance rules. Trays and lids, however, are the fastest climber at 7.6% CAGR, with meal-kit firms standardizing portioned protein and produce cells. The thermoform packaging market size for trays surpassed USD 15.6 billion in 2026, supported by supermarket delis converting from EPS to clear PET. Pressure-formed dual-compartment inserts appeal to premium confectionery seeking elevated shelf presence without secondary cartons.

Blister innovators embed digital watermarking for authentication, while trays undergo design-for-recycling audits to shave EPR fees. Recloseable clip-on lids boost consumer convenience, encouraging reuse and aligning with brand waste-reduction pledges.

By Packaging Thickness: Thin-wall dominance drives efficiency

Thin-wall formats ≤200 µm secured 59.85% revenue in 2025, driven by cost avoidance and lightweighting mandates. They support high-speed fill-seal lines in yogurt and dessert operations. Yet the 200–500 µm bracket is pacing at 7.95% CAGR on strength needs in surgical kit blisters and returnable e-commerce inserts. Above 500 µm applications revolve around industrial dunnage where cycle durability overrides material spend. ALPLA’s rePETec containers prove 0.2 mm walls can survive hot-fill conditions, slashing polymer use 25% per unit.

By End-User Industry: Food leads, pharmaceuticals surge

Food and beverage delivered 50.06% of receipts in 2025, anchored by chilled ready meals and on-the-go snacks. However, pharma and medical packs are racing ahead at 9.04% CAGR. Single-dose biologics, self-administered injectables and diagnostics test cassettes all pivot toward form-fill-seal blistering that assures sterility. The thermoform packaging industry is also courting personal-care brands seeking Instagram-ready clamshells that protect fragile glass while amplifying shelf appeal.

By Thermoforming Technology: Vacuum forming dominates, pressure forming advances

Vacuum forming occupied 44.8% of 2025 value, prized for tooling economy and rapid prototyping. Enhanced ceramic heater arrays now tighten sheet temperature windows, cutting scrap below 3%. Pressure forming shows greatest upside at 8.29% CAGR, supplying finely grained fascia in automotive interiors and boutique electronics. AI-directed plug-assist systems modulate force vectors, yielding wall-thickness uniformity within ±3%, a leap from the 8% variance common five years ago.

Geography Analysis

Asia-Pacific’s 39.76% hold on the thermoform packaging market is fortified by vertically integrated resin hubs in China and India coupled with rising disposable incomes. Government-led pharma parks and e-commerce booms in tier-2 cities sustain a 7.05% regional CAGR. Indian converters leverage Extended Producer Responsibility credits to co-invest in PET flake plants, boosting rPET tray output for quick-service restaurants.

North America presents a mature but innovation-hungry landscape. Four US states have enacted EPR statutes compelling brand owners to bankroll end-of-life programs; converters thus pilot colorant-free PET and digital watermarks to ease sorting. FDA advanced manufacturing incentives accelerate domestic blister capacity, supporting on-shoring of critical drug packaging.

Europe enforces the strictest regime, with the 2030 recyclability rule and graduated recycled-content thresholds pushing rapid material reformulation. Plastic levies in Italy and Spain raise virgin-polymer costs by as much as USD 550/tonne equivalent, hastening adoption of recyclable PP and PET blends. Faerch’s pledge to incorporate 100,000 t/yr of post-consumer PET into food trays exemplifies region-specific circularity scale-ups.

Latin America and the Middle East & Africa trail in market size yet post stable mid-single-digit growth on back of urbanization and food retail modernization. Local players invest in rPET sheet extrusion capacity to circumvent import tariffs and adhere to emerging regional waste policies.

Competitive Landscape

The thermoform packaging market is fragmented. Scale plays dominate M&A headlines—Toppan’s USD 1.8 billion purchase of Sonoco’s thermoform assets deepens its North American footprint. Amcor’s all-stock merger with Berry Global forms a USD 24 billion revenue giant intent on extracting USD 650 million in annual synergies via resin pooling and shared R&D centers.

Technology differentiation is rising. Firms retrofit presses with vision-guided robotic stackers to cut labor cost per 1,000 packs by 25%. Investment in bio-resin compounding lines positions converters to meet retailer-imposed carbon ceilings. Disruptors such as Dart Container’s molded-fiber venture with PulPac claim 80% CO₂ savings, targeting quick-service clamshells.

Raw-material integration also shapes strategy. rPET sheet extruders partner with deposit-scheme operators to lock feedstock streams, insulating against pellet volatility. Patent filings on oxygen-scavenging mono-PET are climbing, signaling focus on barrier innovation that maintains recyclability without multilayer adhesives.

Thermoform Packaging Industry Leaders

Amcor PLC

Sonoco Products Company

Anchor Packaging, Inc.

Mondi Group

Smurfit WestRock

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Amcor and Berry Global completed their all-stock merger, forming a USD 24 billion packaging leader and targeting USD 650 million in annual synergies

- December 2024: Toppan Holdings acquired Sonoco’s Thermoformed & Flexible Packaging unit for USD 1.8 billion to expand sustainable offerings in the Americas

- September 2024: Sonoco announced a strategic review of its thermoformed and flexibles portfolio to streamline operations.

- September 2024: Dart Container partnered with PulPac to install dry molded fiber lines that curb CO₂ emissions by up to 80%.

Global Thermoform Packaging Market Report Scope

Thermoform packaging involves the heating of plasticuntil it reaches a pliable state, and then forming the plastic into various shapes. This report segments the market byMaterial(Plastic, Paperboard, Aluminium), by Product Type(Blisters, Clam-shell, Trays & Lids), End-user Industry(Pharmaceutical, Food & Beverage, Electronics) and Geography.

| Plastic |

| Paper and Paperboard |

| Aluminum |

| Bio-based/Biodegradable Polymers |

| Blisters |

| Clamshells |

| Trays and Lids |

| Cups and Bowls |

| Other Product Type |

| Up to 200 µm |

| 200–500 µm |

| Above 500 µm |

| Food and Beverage |

| Pharmaceuticals and Medical |

| Personal Care and Cosmetics |

| Consumer Electronics |

| Other End-user Industry |

| Vacuum Forming |

| Pressure Forming |

| Mechanical Forming |

| Plug-Assist Forming |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Material | Plastic | ||

| Paper and Paperboard | |||

| Aluminum | |||

| Bio-based/Biodegradable Polymers | |||

| By Product Type | Blisters | ||

| Clamshells | |||

| Trays and Lids | |||

| Cups and Bowls | |||

| Other Product Type | |||

| By Packaging Thickness | Up to 200 µm | ||

| 200–500 µm | |||

| Above 500 µm | |||

| By End-user Industry | Food and Beverage | ||

| Pharmaceuticals and Medical | |||

| Personal Care and Cosmetics | |||

| Consumer Electronics | |||

| Other End-user Industry | |||

| By Thermoforming Technology | Vacuum Forming | ||

| Pressure Forming | |||

| Mechanical Forming | |||

| Plug-Assist Forming | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the thermoform packaging market?

The thermoform packaging market size is USD 49.55 billion in 2026 and is projected to reach USD 61.77 billion by 2031 at a 4.51% CAGR.

Which region leads global demand?

Asia-Pacific holds 39.76% of 2025 revenue and remains the fastest-growing region at a 7.05% CAGR through 2031.

Which material segment is expanding the fastest?

Bio-based and biodegradable polymers are climbing at an 8.21% CAGR as regulations and brand sustainability targets intensify.

How are taxes affecting plastic thermoformers?

Plastic-use levies in the EU and North America inflate virgin polymer costs, pushing converters toward recycled and mono-material solutions to avoid penalties.

Why is pressure forming gaining popularity?

Pressure forming achieves finer surface detail and tighter tolerances than vacuum forming, supporting premium electronics and automotive parts, and is advancing at an 8.29% CAGR.

What impact will the Amcor–Berry merger have?

The combined entity commands USD 24 billion in revenue and targets USD 650 million in synergies, likely accelerating investment in sustainable materials and Industry 4.0 production assets.

Page last updated on: