Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

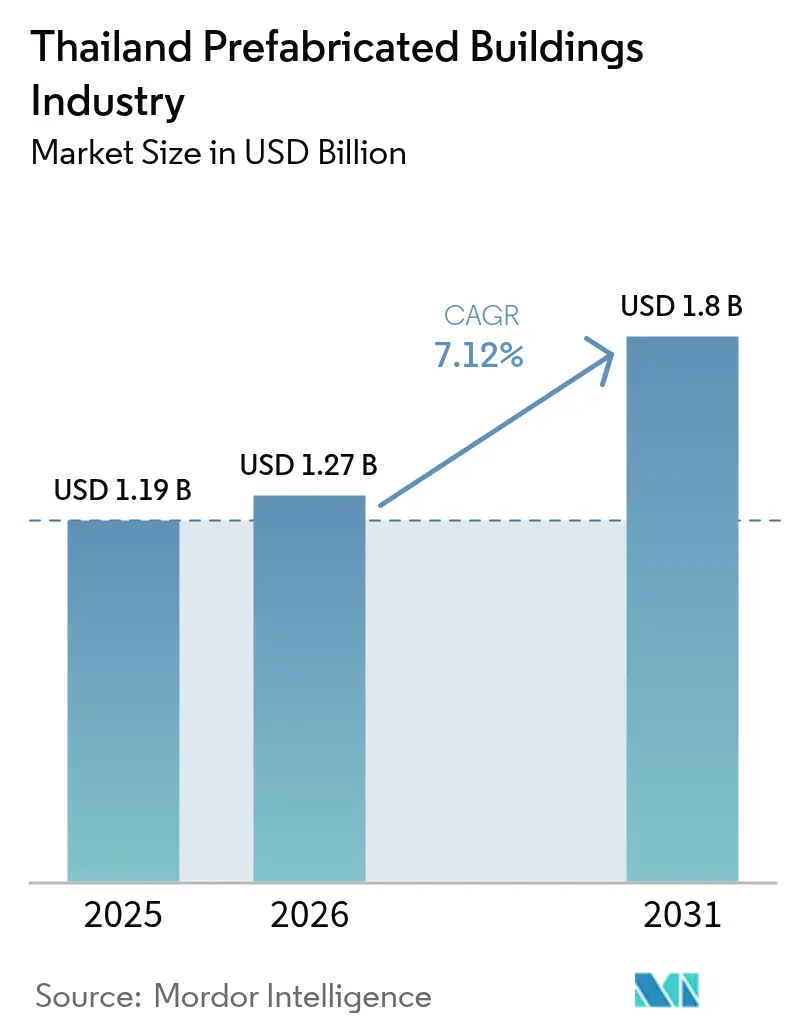

| Base Year Market Size (2025) | USD 1.19 Billion |

| Market Size (2026) | USD 1.27 Billion |

| Market Size (2031) | USD 1.8 Billion |

| Growth Rate (2026 - 2031) | 7.12% CAGR |

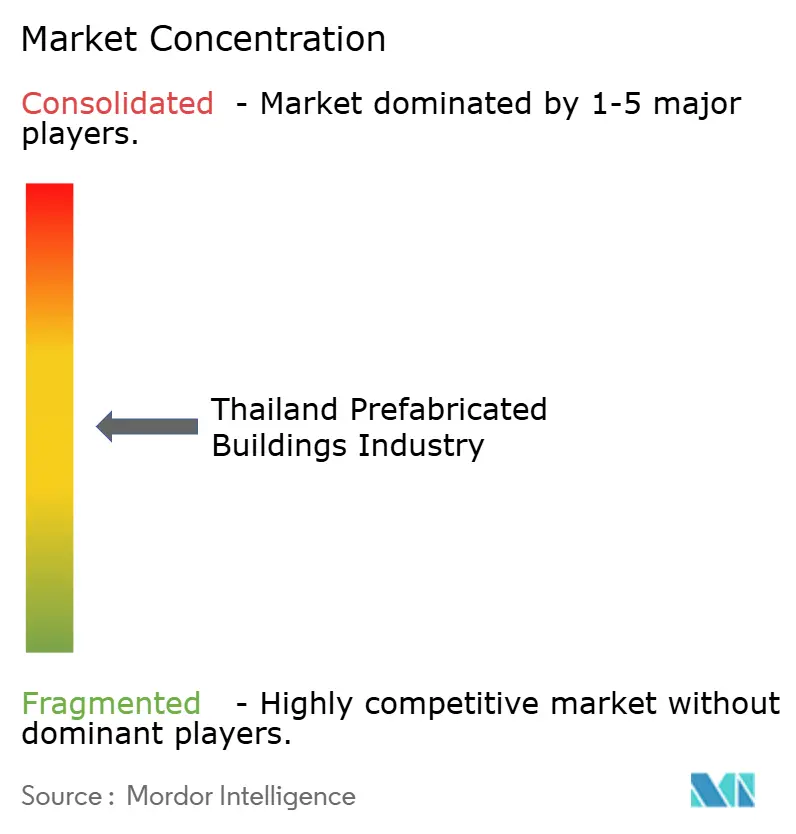

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Prefabricated Buildings Industry Analysis by Mordor Intelligence

Thailand prefabricated buildings market size in 2026 is estimated at USD 1.27 billion, growing from 2025 value of USD 1.19 billion with 2031 projections showing USD 1.8 billion, growing at 7.12% CAGR over 2026-2031. Thailand's prefabricated buildings market growth is propelled by a USD 76.6 billion national transport pipeline that favors modular execution, rising demand for flood-resilient housing, and post-pandemic hospital modernization. Accelerating urban labor costs in Bangkok, Board of Investment (BOI) incentives for low-waste materials, and the Eastern Economic Corridor (EEC) smart-city build-out further amplify adoption. Competition is fragmenting as integrated conglomerates fight nimble timber specialists while developers pivot toward factory-controlled quality. Near-term opportunities cluster around worker dormitories, resort pods, and elevated homes that mitigate chronic flood risk.

Key Report Takeaways

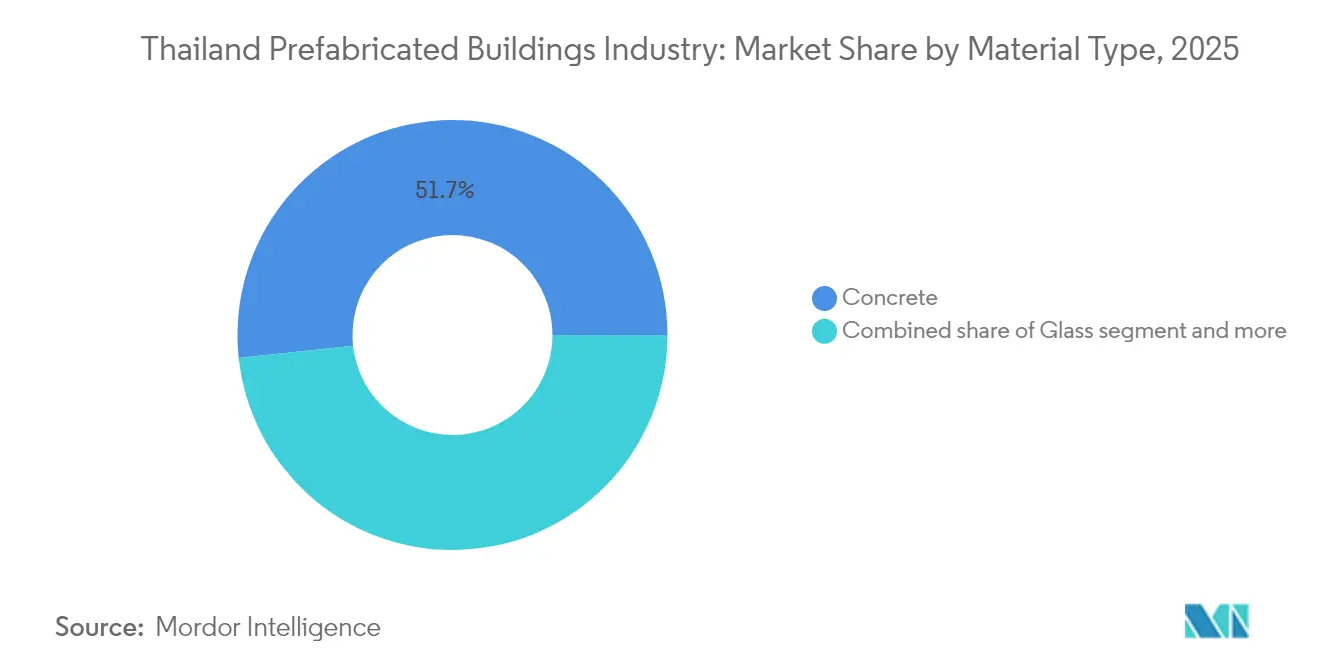

- By material, concrete accounted for 51.70% of the Thailand prefabricated buildings market size in 2025; timber is set to compound at an 8.05% CAGR to 2031.

- By application, residential captured 47.20% revenue share in 2025, and commercial use cases are expanding at a 7.65% CAGR to 2031.

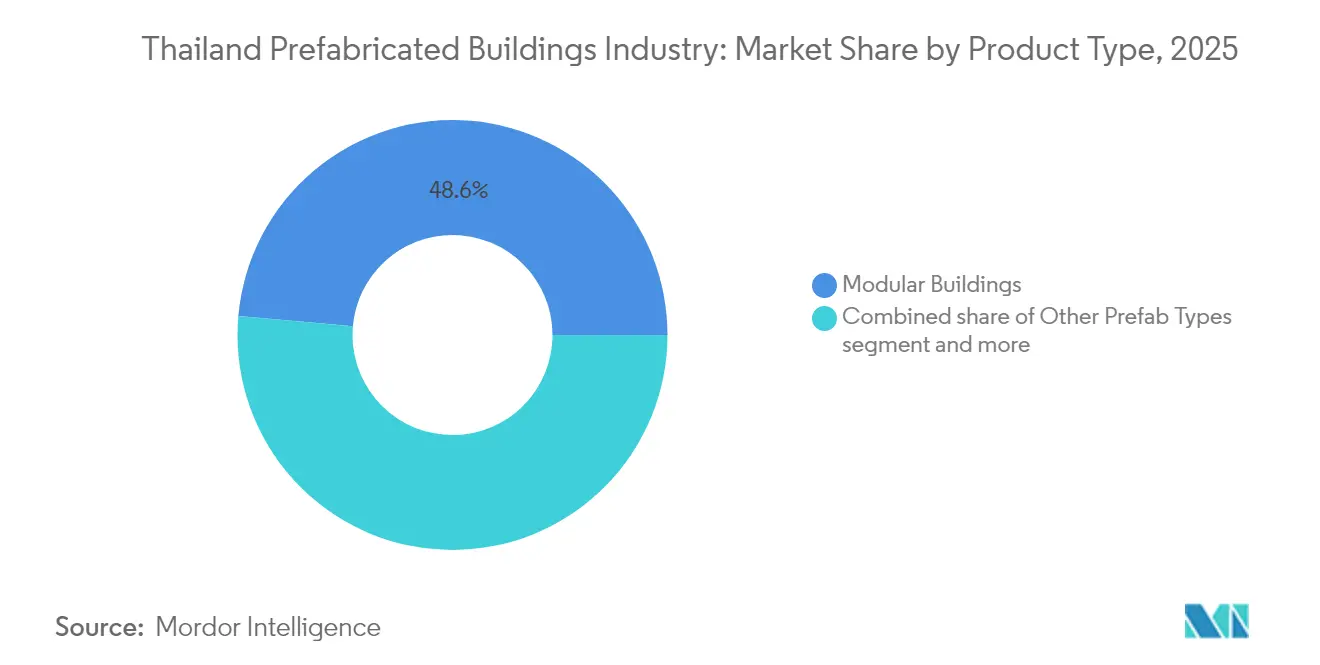

- By product, modular buildings commanded 48.60% of the Thailand prefabricated buildings market size in 2025 and are advancing at an 7.96% CAGR through 2031.

- By geography, Central Thailand led with 37.60% of Thailand's prefabricated buildings market share in 2025, while the Rest of Thailand regions are progressing at an 8.10% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Prefabricated Buildings Industry Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Eastern Economic Corridor turnkey industrial parks driving dormitory modules | + 1.8% | Eastern Thailand (Chonburi, Rayong, Chachoengsao) | Medium term (2-4 years) |

| Urban labour-cost inflation catalysing factory-built components | + 1.5% | Central Thailand, Greater Bangkok Metropolitan Area | Short term (≤ 2 years) |

| BOI tax incentives rewarding low-waste green construction materials | + 1.2% | National, with concentration in EEC and SEZ zones | Long term (≥ 4 years) |

| Post-COVID hospital upgrades leaning on modular wards | + 0.9% | National, with priority in secondary cities | Medium term (2-4 years) |

| Tourism-reopening surge in resort pods across islands | + 0.8% | Southern Thailand (Phuket, Koh Samui, Krabi) | Short term (≤ 2 years) |

| Flood-resilient elevated modular homes in Chao Phraya basin | + 0.6% | Central Thailand, Chao Phraya River basin provinces | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Eastern Economic Corridor Turnkey Industrial Parks Driving Dormitory Modules

The EEC is attracting hundreds of foreign manufacturers, creating immediate pressure for 200,000 worker beds that conventional construction cannot supply on schedule. Prefabricated dormitories shorten delivery cycles by up to 70%, aligning with the USD 38.3 billion Huai Yai smart-city timeline. Developers favor modular systems with integrated utilities to comply with higher living-standard mandates for advanced-manufacturing staff. Land-sale momentum at WHA industrial estates confirms robust demand for fast-track accommodation, while the new 10-year EEC visa deepens the need for semi-permanent modular housing[1]Chula Sukmanop, “Smart City Master Plan for Huai Yai,” Eastern Economic Corridor Office, eec.go.th.

Urban Labor-Cost Inflation Catalyzing Factory-Built Components

Bangkok builders face wage escalation and skilled-worker shortages that erode on-site productivity. Factory fabrication shifts repetitive tasks to controlled environments, lowering rework and minimizing site congestion. SCG’s merger with JWD created an ASEAN-wide logistics backbone that slashes last-mile costs, making factory-to-site delivery of precast frames and panels more economical than traditional formwork. Logistics now represents 13.7% of national GDP, so time-compressed deliveries reinforce the cost-benefit of modular production.

BOI Tax Incentives Rewarding Low-Waste Green Construction Materials

The BOI grants up to 13-year corporate tax holidays and import-duty waivers for projects that verify waste reduction and carbon savings. Prefabricated manufacturers deploying cross-laminated timber (CLT) and low-carbon cement qualify for maximum incentives. SCG lifted low-carbon cement to 63% of output in 2023, demonstrating how material innovation aligns with fiscal rewards. Importantly, the subsidy package extends to production machinery, catalyzing investment in automated panel lines and digital twin verification systems[2]Narit Therdsteerasukdi, “Investment Promotion Measures 2025,” Thailand Board of Investment, boi.go.th.

Post-COVID Hospital Upgrades Leaning on Modular Wards

COVID-19 exposed ICU shortages and infection-control gaps in secondary cities. Health-care groups are now specifying plug-and-play ward blocks that can be added without shutting down core services. Modular units built under clean-factory conditions integrate standardized HVAC and negative-pressure compartments, curtailing airborne transmission risk. Projects by Bangkok Dusit Medical Services in Rayong and Chonburi demonstrate 40% schedule cuts versus masonry builds, aligning with World Bank funding conditions for agile health-care capacity[3]Prasert Prasarttong-Osoth, “Network Expansion Update 2025,” Bangkok Dusit Medical Services, bdms.co.th.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Fragmented municipal permitting and prefab standards | -1.1% | National, with acute challenges in Bangkok and secondary cities | Medium term (2-4 years) |

| Conservative developer perception of quality risk | -0.8% | Central Thailand, premium residential segments | Long term (≥ 4 years) |

| Shortage of local CLT supply chain | -0.6% | National, with supply constraints from neighboring countries | Long term (≥ 4 years) |

| High logistics cost for oversize modules in narrow urban streets | -0.5% | Bangkok Metropolitan Area, historic city centers | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Fragmented Municipal Permitting and Prefab Standards

Thailand’s decentralized approval regime forces developers to navigate varying municipal rules, prolonging lead-times for factory-built components. Additional inspections are often required because local officials lack familiar templates for certifying off-site fabrication. The recent revocation of a high-rise permit over access-road disputes underscored regulatory unpredictability and heightened caution among investors. Harmonized prefab codes remain a work in progress, tempering short-term uptake despite national interest.

Conservative Developer Perception of Quality Risk

The collapse of a conventionally built government complex in 2024 intensified scrutiny of construction quality and, by extension, fostered skepticism toward unfamiliar techniques. Luxury condominium promoters worry that buyers equate prefabrication with standardized aesthetics and resale discounts. Although the incident involved traditional methods, reputational spillover slows innovation in premium segments until demonstrable quality benchmarks and third-party audit systems gain wider acceptance.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Concrete Dominance Amid Timber Innovation

Concrete retained 51.70% of Thailand's prefabricated buildings market share in 2025, buoyed by entrenched cement supply and design familiarity. The Thailand prefabricated buildings market size for concrete solutions is projected to rise alongside low-carbon cement substitution that meets BOI sustainability thresholds. Timber, led by CLT panels, is sprinting ahead at an 8.05% CAGR as developers chase embodied-carbon cuts and accelerated erection times. Supply bottlenecks from Thailand’s logging moratorium spur imports of plantation rubberwood and engineered bamboo, nudging manufacturers to localize processing capacity under the BOI’s green-material stimulus. Composite and metal sub-segments orbit niche industrial enclosures and façade retrofits, whereas glass modules underpin premium façade upgrades that demand precision glazing.

The concrete value chain is modernizing to defend its lead: Siam City Cement reported 36% EBITDA growth in H1 2024 after launching cement variants that claim 20% lower CO₂ per ton. Timber’s climb forms a counter-balance, unlocking architectural expressions aligned with eco-resort branding and flood-resilient stilts. Research into laminated bamboo shows strength‐to-weight ratios comparable with tropical hardwood, foreshadowing future material turnover as supply chains mature. Overall, shifting material preferences highlight Thailand's prefabricated buildings industry orientation toward cost-plus-sustainability metrics rather than lowest-cost-first criteria.

By Application: Residential Foundation with Commercial Acceleration

Residential accounted for 47.20% of the Thailand prefabricated buildings market size in 2025, driven by urban population growth and a chronic housing deficit. Elevated modular homes address recurrent inundation in the Chao Phraya basin, translating flood resilience into tangible homeowner value. Commercial assets, though smaller today, will chart a 7.65% CAGR as tourism reopens and EEC campuses spawn ancillary malls, hotels, and labs. Fast-track delivery is paramount: each month a resort opening slips can forfeit millions in peak-season revenue, compelling hospitality groups to pivot to factory-assembled pods.

The residential volume remains anchored by repeatable two-to-five-story schemes that optimize panelized walls and precast slabs. Commercial schemes increasingly integrate mixed-use precincts where modular guest rooms sit atop retail podiums. Developers such as Centara and Dusit demonstrate confidence, contracting modular superstructures that meet international brand standards without schedule overruns. The “others” category, health-care, education, and emergency shelters, keeps momentum via BOI funding that rewards social infrastructure. Collectively, application dynamics validate that Thailand's prefabricated buildings market continues its shift from cost-driven shelter provision to speed-and-quality-led asset creation.

By Product Type: Modular Buildings Lead Dual Dominance

Modular buildings held 48.60% of Thailand's prefabricated buildings market share in 2025 and are projected to capture the most incremental dollars as they grow at an 7.96% CAGR through 2031. Their closed-box format unites structure, MEP, and interior finishes under a single quality envelope, compressing on-site assembly to days. Panelized systems trail in share yet remain indispensable for vertical infill sites where transport-height limits apply. Container-based and hybrid systems populate mining camps, retail kiosks, and rapid-response classrooms.

Dual dominance stems from modular’s versatility across worker dorms, resort suites, and flood-lifted villas. Factory repeatability ensures tight tolerances that assuage conservative buyers, while building information modeling (BIM) integration expedites authority submissions. Thai Obayashi and Italian-Thai Development now integrate modular packages into public-transport stations to meet aggressive handover dates. Logistics gains, underscored by a new Inland Container Depot near Laem Chabang, further streamline oversized module routing and reinforce modular momentum.

Geography Analysis

Central Thailand commanded 37.60% of Thailand's prefabricated buildings market in 2025 as Bangkok’s mega-projects, dense contractor ecosystem, and superior logistics infrastructure concentrated demand. Urban labor costs and land constraints drive a pivot to factory-finished elements that can be installed during narrow night shifts, minimizing traffic disruption. The region’s high-density corridors accommodate innovative schemes such as “train-through-building” towers aligned to the Red Line, pushing modular engineering boundaries. Flood risk remains acute, so elevated prefab podiums gain favor in waterfront precincts. However, road widths hamper the movement of 3D boxes, local innovators engineer foldable modules and on-site stacking cranes to navigate tight inner-city grids.

The Rest of Thailand cohort posts the fastest 8.10% CAGR as infrastructure disperses. The EEC alone will deploy USD 38.3 billion through 2030 on smart cities, ports, and digital parks, each specifying modular dormitories and labs to compress build durations. Southern resort islands record brisk villa and pod installations as operators replace aging bungalows with sustainable units that meet global brand guidelines. Northern and Northeastern provinces, benefitting from World Bank secondary-city programs, adopt prefab classrooms and clinics to leapfrog skilled-labor shortages. Lower regulatory friction outside Bangkok also streamlines factory permitting and site approvals, nurturing regional manufacturing hubs.

Geographic momentum hints at a rebalanced Thai construction economy. While Bangkok remains the command center, provincial demand is scaling on the back of infrastructure, tourism, and climate-resilience spending. This decentralization aligns with government efforts to broaden income distribution and promote green-growth corridors, ensuring that the Thailand prefabricated buildings market expands across diverse topographies and risk profiles.

Competitive Landscape

Competition is moderately fragmented: conglomerates such as SCG Group deploy end-to-end supply chains covering cement, logistics, and modular assembly, while specialist players target niche eco-resort or CLT verticals. SCG Heim leverages in-house low-carbon cement to court BOI-incentivized projects, whereas CPAC Modular focuses on mid-rise residential towers with proprietary precast cores. Italian-Thai Development’s joint venture for the Thai–Chinese high-speed rail illustrates how infrastructure contractors are incorporating prefab viaducts and service buildings to meet stiff deadlines and budget ceilings.

White-space opportunities coalesce around CLT, flood-proof elevated pods, and hospital ward kits. Small firms with proprietary bamboo-laminate panels are courting resorts seeking authentic aesthetics and carbon credentials. Yet supply-chain gaps, especially kiln capacity and resin technology, temper scale. High-profile quality lapses in conventional builds have paradoxically raised the bar for prefab, encouraging firms to adopt ISO 19650 BIM protocols and off-site QA audits to win skeptical developers.

Strategic moves since 2024 show a tilt toward alliances: SCG partnered with a Japanese robotics integrator to automate final-finish lines, while WHA Corporation digitized its industrial-estate portfolio to feed just-in-time dormitory dispatch. Price pressures remain contained because labor scarcity pushes traditional costs higher, preserving prefab margins even as material costs rise. Overall, rivalry is intensifying, but product differentiation around sustainability, flood resilience, and digital integration sustains a wide playing field within the Thailand prefabricated buildings industry.

Thailand Prefabricated Buildings Market Leaders

SCG Heim Co., Ltd.

Pruksa Precast Co., Ltd.

CPAC Modular (Siam Cement Group)

Sino-Thai Engineering & Construction PCL

Thai Obayashi Corp., Ltd.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Thailand earmarked USD 38.3 billion for the Huai Yai smart city in the EEC, mandating modular construction for 5,795 rai of mixed-use assets. The scale and scheduling pressure of the smart-city program will translate into multi-year, high-volume orders for modular dormitories, mid-rise residential blocks, and public-service buildings, directly expanding the addressable market for turnkey prefab producers while anchoring new factory investments close to Chonburi and Rayong

- March 2025: An Italian-Thai / China Railway JV inked a USD 0.27 billion contract for 30 km of high-speed rail track and nine prefab service buildings. The project demonstrates large-scale infrastructure adoption of prefabricated construction techniques for rapid deployment.

- October 2024: Mitsubishi Power completed a 5,300 MW natural gas-fired power plant through joint venture with Gulf Energy Development and Mitsui & Co., utilizing advanced modular construction techniques for power-generation facility components.

- June 2024: Dusit Layan Verde Resort: Dusit International partnered with VillaCarte Group to manage dual-branded luxury resort and residences in Phuket, featuring 15 mid-rise buildings with 398 hotel rooms and 388 residential units utilizing sustainable modular construction techniques, set for 2027 completion.

Thailand Prefabricated Buildings Industry Report Scope

Prefabricated buildings (also known as prefabs) are manufactured offsite and transported to the location for on-site assembly. This report covers market insights, such as market dynamics, drivers, restraints, opportunities, technological innovation, and its impact, porter's five forces analysis, and the impact of COVID-19 on the market. Additionally, the report provides company profiles to understand the competitive landscape of the market.

The Thailand Prefabricated Buildings Industry is Segmented by Application (Residential, Commercial, and Other Applications (Infrastructure and Industrial)). The report offers market sizes and forecast for Thailand Prefabricated Buildings Industry in value (USD Billion) for all the above segments.

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By Key Regions

| Central |

| Eastern |

| Northeastern |

| Northern |

| Southern |

| Rest of Thailand |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By Key Regions | Central |

| Eastern | |

| Northeastern | |

| Northern | |

| Southern | |

| Rest of Thailand |

Key Questions Answered in the Report

How large is the Thailand prefabricated buildings market in 2026?

It stands at USD 1.27 billion in 2026 and is set to USD 1.8 billion by 2031 under a 7.12% CAGR.

Which product type leads prefab adoption in Thailand?

Modular buildings hold 48.60% share and are growing fastest at an 7.96% CAGR due to speed and integrated quality.

What role does the EEC play in prefab demand?

The USD 38.3 billion Huai Yai smart-city and linked industrial parks in the EEC require rapid dormitories, labs, and housing, making prefab indispensable.

Why is timber gaining traction against concrete?

BOI tax holidays and low-carbon mandates push developers toward CLT and engineered timber, driving an 8.05% CAGR for wood solutions.

Page last updated on: