Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2021 - 2024 |

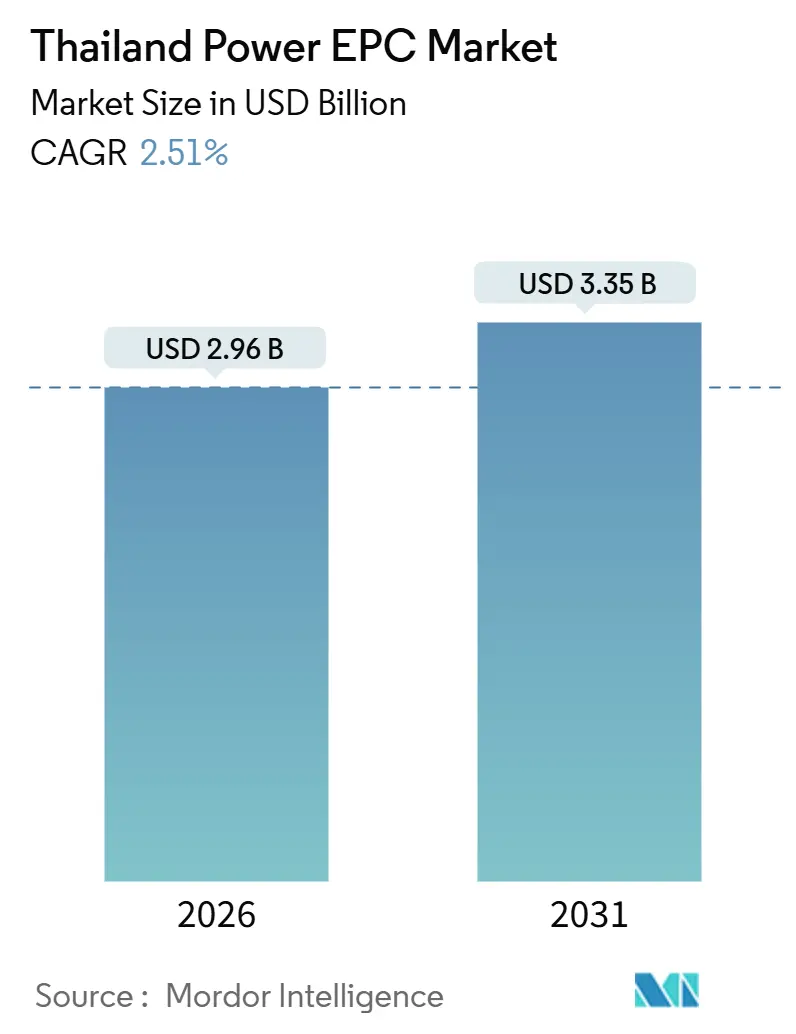

| Market Size (2026) | USD 2.96 Billion |

| Market Size (2031) | USD 3.35 Billion |

| Growth Rate (2026 - 2031) | 2.51% CAGR |

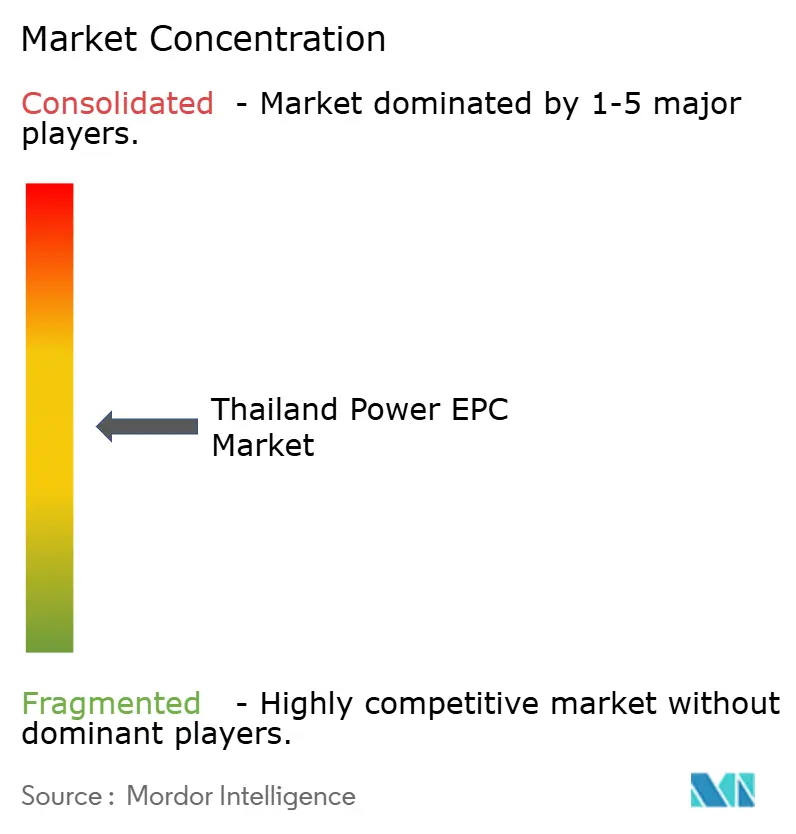

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Power EPC Market Analysis by Mordor Intelligence

The Thailand Power EPC Market size is estimated at USD 2.96 billion in 2026, and is expected to reach USD 3.35 billion by 2031, at a CAGR of 2.51% during the forecast period (2026-2031).

Modest topline growth conceals a structural realignment: capital is shifting from baseload thermal builds toward grid reinforcement, renewable integration, and digital substations as outlined in the Power Development Plan (PDP) 2022-2037.[1]Energy Policy and Planning Office, “Thailand Power Development Plan 2022-2037,” eppo.go.th Data-center electricity demand in the Eastern Economic Corridor (EEC) is accelerating direct-purchase agreements, prompting rapid solar-plus-BESS roll-outs and new 500 kV transmission corridors.[2]Board of Investment Thailand, “EEC Data-Center Investment Applications,” boi.go.th Combined-cycle gas turbines (CCGT) remain dominant, yet offshore-wind pilots, hydrogen co-firing mandates, and 3.2 million smart-meter deployments are reshaping EPC bid structures. Exchange-rate swings, elevated lending costs, and lengthy Environmental Impact Assessment (EIA) cycles temper near-term order books but also drive innovation in hedging, modular construction, and fast-track permitting pathways.

Key Report Takeaways

- The Thailand power EPC market is segmented into power generation EPC and power transmission and distribution (T&D) EPC. Power generation EPC accounted for 69.3% of the market in 2025, while power transmission and distribution (T&D) EPC is projected to grow at a 2.71% CAGR through 2031.

- By technology, thermal generation captured 63.8% of the Thailand power generation EPC market share in 2025; renewables are forecast to register the fastest 5.8% CAGR through 2031.

- By project size, the 100 MW-499 MW band held 61.5% share of the Thailand power generation EPC market size in 2025, while microgrids below 100 MW are expanding at a 6.1% CAGR to 2031.

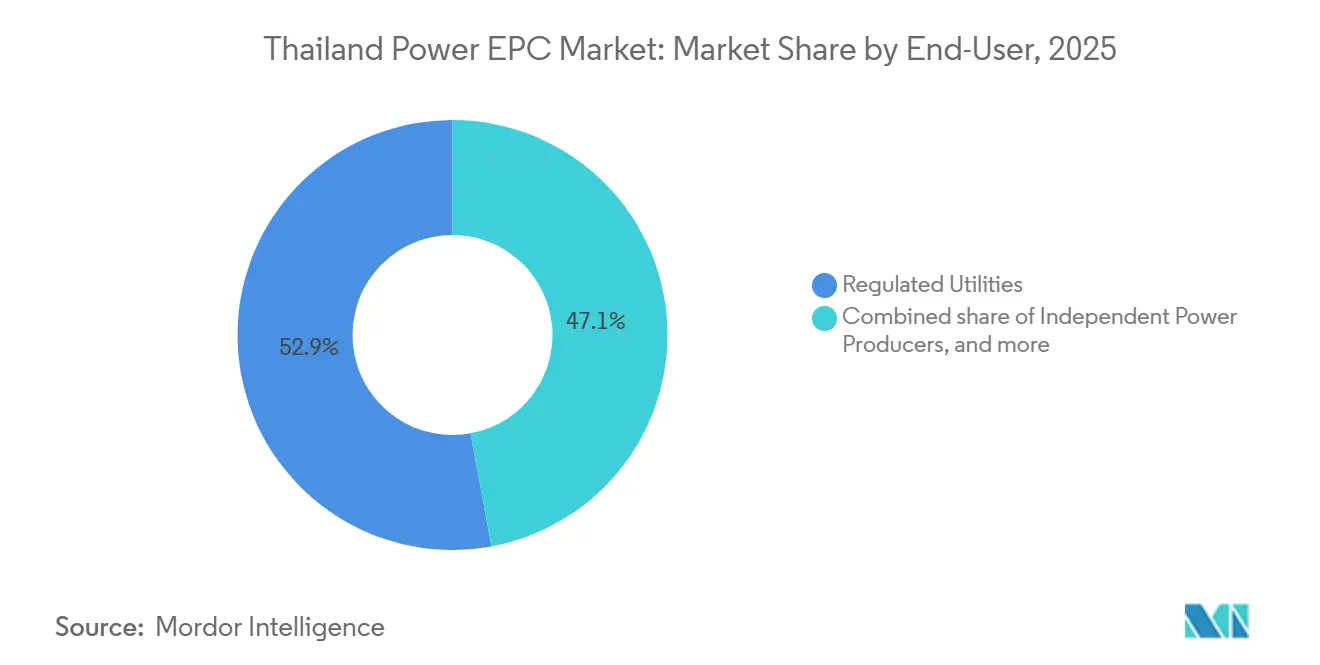

- By end user, regulated utilities commanded a 52.9% share of the Thailand power generation EPC market size in 2025; Independent Power Producers posted the highest 5.7% CAGR over 2026-2031.

- Mitsubishi Power, Marubeni, and Toshiba together supplied more than 40% of 2025 thermal capacity additions, underscoring moderate concentration in large-scale gas projects.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Thailand Power EPC Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government-backed PDP 2022-2037 capital-expenditure pipeline | +0.6% | National, concentrated in EEC and Gulf of Thailand | Long term (≥ 4 years) |

| Rapid growth in industrial and data-center electricity demand | +0.7% | EEC, Bangkok Metropolitan Region | Short term (≤ 2 years) |

| Renewable-energy targets under AEDP 2022 steering EPC uptake | +0.5% | Nation-wide, early gains in Northeast, South, Central | Medium term (2-4 years) |

| Grid-modernization incentives (smart substations, HVDC links) | +0.4% | National transmission backbone | Medium term (2-4 years) |

| Offshore-wind pilot zones unlocking multi-GW EPC contracts | +0.3% | Gulf of Thailand | Long term (≥ 4 years) |

| ASEAN Power Grid cross-border trading catalyzing T&D EPC | +0.2% | Borders with Laos, Malaysia, Myanmar | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government-Backed PDP 2022-2037 Capital-Expenditure Pipeline

The THB 2.9 trillion (USD 85 billion) PDP commits 51% renewable penetration by 2037 and phases out subcritical coal, anchoring steady demand for generation, transmission, and distribution packages. Hydrogen co-firing targets of 5% in 2026 and 20% in 2035 compel EPC bidders to pre-qualify combustors that can accept blended gas, as seen in Mitsubishi Power’s 5,300 MW Rayong–Chonburi modular complex commissioned in 2024.[3]Mitsubishi Power, “Rayong–Chonburi CCGT Complex Fact Sheet,” mitsubishi-power.com EGAT’s THB 21.9 billion backbone expansion shifts value toward 500 kV lines and digital substations that evacuate offshore-wind output to EEC load centers.[4]Electricity Generating Authority of Thailand, “Hydrogen Co-Firing Roadmap,” egat.co.th The long-run program flattens order volatility yet crystallizes fuel-mix risk because gas stays above 60% of installed capacity through 2030.

Rapid Growth in Industrial and Data-Center Electricity Demand

Forty-six data-center filings worth THB 168 billion (USD 4.9 billion) in 2024 clustered 90% of requests in the EEC, adding 2,000 MW of direct PPA capacity from January 2026. Amazon Web Services, Google, and TikTok alone plan hyperscale campuses exceeding 400 MW IT load, accelerating solar-plus-BESS and 500 kV line awards. Digital Edge and B.Grimm are building a 100 MW campus, while CtrlS activated 150 MW in 2025 at THB 15 billion spend. Industrial electricity in the corridor grew 4.2% year-on-year in 2024 versus 2.1% nationwide, pulling forward substation upgrades originally slated for 2028. The surge lifts microgrid EPC volumes as estates deploy 5-20 MW captive solar arrays to stabilize tariffs and uptime for semiconductor and EV-battery plants.

Renewable-Energy Targets Under AEDP 2022 Steering EPC Uptake

AEDP 2022 lifts renewables to 51% by 2037, requiring 32 GW of solar by 2030 and 74 GW by 2037 plus 11.8 GW of storage. Gulf Energy delivered 393 MW solar and 256 MW solar-plus-BESS during 2024-2025 using LONGi bifacial modules and Samsung SDI cells. BCPG’s 10 MW wind-plus-BESS site in the South features grid-forming inverters that provide synthetic inertia. Two offshore zones totaling 4.5 GW entered EIA in 2024, with commercial operation targeted in 2030; foreign developers must JV with local builders to meet 40% local-content rules. EPC headroom extends to foundation engineering, export cable laying, and onshore substations.

Grid-Modernization Incentives (Smart Substations, HVDC Links)

EGAT earmarked USD 5.67 billion for smart substations, HVDC studies, and meter digitalization to cut technical losses below 5% by 2030. MEA’s 3.2 million smart-meter rollout by 2027 enables time-of-use tariffs and demand response, creating new EPC scopes in communications, data analytics, and device installation. PowerChina’s 500 kV GIS yard in Thung Song, delivered in October 2024, showcases IEC 61850 digital relays and 3,000 MVA ratings. Gunkul’s June 2025 award for a 37 km 500 kV line to evacuate offshore-wind energy underscores momentum in backbone expansion. HVDC remains conceptual, yet Malaysia-Thailand feasibility work on a ±500 kV intertie progressed in 2024.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Lengthy EIA and permitting timelines | −0.4% | Nation-wide; acute in farm provinces and coastal zones | Short term (≤ 2 years) |

| High project-finance costs amid rising policy rates | −0.3% | National; heavier on IPP renewables | Short term (≤ 2 years) |

| Currency-exchange volatility on imported equipment | −0.2% | National; affects high-import content projects | Short term (≤ 2 years) |

| Local opposition to land acquisition for renewables | −0.2% | Northeast solar, South wind, Central biomass | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Lengthy EIA and Permitting Timelines

Thailand’s EIA regime requires ONEP, provincial offices, and public hearings, extending utility-scale solar and wind approvals to 12-24 months. Offshore-wind zones face permit decisions only by late 2026, pushing foundation and turbine contracts beyond initial schedules. Solar farms in Nakhon Ratchasima met farmer resistance over perceived soil impacts, stalling 200 MW in 2024. Southern wind developers ordered extra marine-biology studies to placate fisheries, adding nine months to timelines. A 2025 fast-track path for <50 MW projects exists but covers only a fraction of the Thailand power EPC market.

High Project-Finance Costs Amid Rising Policy Rates

Bank of Thailand reduced the policy rate to 2.25% in December 2024, yet power-project loans float at 5.5-6.5%, depressing IPP equity returns. Thai Baht swings between THB 33-36 per USD, inflating gas-turbine and PV import bills and eroding fixed-price EPC margins. Gulf Energy reported a 12% turbine-cost jump on Euro weakness, prompting tariff renegotiation with EGAT. Smaller developers face 0.3-0.5 percentage-point hedging premiums they can scarcely absorb, despite an Asian Development Bank USD 200 million concessional line established in 2025.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Technology: Thermal Resilience Amid Emerging Offshore Wind

Thermal generation accounted for 63.8% of the 2025 EPC value, anchored by domestic gas supply and LNG imports. The Thailand power EPC market size for thermal plants reached USD 2.01 billion in 2025. Mitsubishi Power’s 1,400 MW Hin Kong CCGT, commissioned in January 2025, illustrates next-generation 61%-efficiency turbines that already co-fire 5% hydrogen. Renewable capacity is poised for a 5.8% CAGR as AEDP mandates 32 GW of new solar by 2030. The Thailand power generation EPC market share held by renewables should rise steadily once offshore wind breaks ground, yet local foundation expertise and supply-chain gaps remain barriers.

Cost dynamics diverge across technologies. Turbine prices rose 10-12% on currency moves, squeezing thermal EPC spreads, while photovoltaic module oversupply shaved 15% off 2025 panel quotes, widening solar margins. Offshore wind developers must joint-venture to satisfy 40% local content, potentially lifting balance-of-plant costs but embedding knowledge transfer that benefits domestic yards. Hydrogen-ready retrofits represent a niche yet growing bid line as EGAT seeks 20% blending by 2035.

By Capacity Band: Mid-Scale Dominance, Microgrid Momentum

Projects sized 100-499 MW held 61.5% of installed capacity in 2025 and attracted the bulk of turnkey CCGT and utility-scale solar EPC awards. Hin Kong’s twin 700 MW blocks typify a modular design that trims per-MW civil costs. In contrast, the Thailand power generation EPC market size for microgrids under 100 MW is minor today but expanding 6.1% annually as data centers and industrial estates adopt rooftop solar, diesel-hybrid, and BESS networks.

DER economics improve as lithium-ion prices fall and direct-purchase PPAs bypass MEA and PEA retail tariffs. Southern islands, once reliant on USD 0.44 per kWh diesel, now procure hybrid power at USD 0.23 per kWh, illustrating the commercial appeal of sub-20 MW builds. Projects above 500 MW remain limited to CCGT and future offshore wind, the latter contingent on HVDC export cables and dedicated 500 kV substations that lengthen lead times.

By End-User: Utilities Lead but IPPs Accelerate

Utilities, EGAT, MEA, and PEA claimed 52.9% of 2025 outlays, reflecting statutory supply duties and grid-ownership rights. Still, IPPs logged a 5.7% CAGR outlook as Direct PPA rules unlock captive demand from hyperscalers and industrial zones. The Thailand power generation EPC market share for IPPs should exceed 47% by 2031 if current tender patterns persist.

Gulf Energy and BCPG collectively earmarked USD 2.5 billion for solar-plus-BESS and offshore wind before 2027, enhancing their bargaining leverage on module and inverter procurement. RATCH aims for 1,500 MW of renewable expansion linked to AWS and Google data-center loads. Utilities remain pivotal gatekeepers via grid-connection fees and curtailment clauses, though regulatory reform is narrowing their historic advantage.

Geography Analysis

The EEC captured 38-42% of incremental builds during 2024-2025, fueled by THB 168 billion in data-center filings and automotive electrification capex. EGAT fast-tracked 2,000 MW of direct-purchase solar allocations to feed these hyperscalers, and 500 kV circuits from Bang Lamung to Pluak Daeng are under construction. Combined with B.Grimm’s 100 MW campus and CtrlS’s 150 MW facility, the corridor anchors near-term EPC revenue.

The Bangkok Metropolitan Region accounts for roughly 30% of T&D spend, led by MEA’s smart-meter rollout and substation digitalization that accommodate 1,200 MW of rooftop solar. Northeastern provinces provide land-rich solar sites but face pushback from farmers worried about crop yields, delaying several 50-100 MW portfolios. Southern Thailand, home to 4.5 GW of planned offshore wind, waits on EIAs; substation groundwork and port-upgrade packages nonetheless appear in 2026 tender schedules.

Cross-border energy flows reinforce Thailand’s hub status. Imports of 7,000 MW from Laos and exports of 300 MW to Malaysia depend on future HVDC nodes under study. Northern provinces focus on biomass and small hydro tied to agro-industrial value chains, though feedstock price volatility hinders capacity-factor performance.

Regulatory Landscape

Thailand's electricity sector is governed primarily under the Energy Industry Act B.E. 2550 (2007). The Energy Regulatory Commission (ERC) administers licensing for generation, transmission, and distribution activities, while the Energy Policy and Planning Office (EPPO) steers national planning instruments such as the Power Development Plan (PDP) and Alternative Energy Development Plan (AEDP). Within the report scope, PDP 2022-2037 remains the core reference, and a Draft PDP 2024 has been discussed publicly as a longer-horizon update aligned with net-zero ambitions. This supports policy-led capex continuity alongside evolving reliability planning, including LOLE-based standards referenced in 2026 legal and policy analyses.

Market access and project structuring are also shaped by state-utility procurement and grid-connection requirements. Incremental liberalization is appearing through the direct PPA framework for large consumers such as data centers, including Third Party Access (TPA) concepts through the national grid. In the EEC, this direct-purchase channel functions as a key regulatory anchor for EPC contracting, while environmental approvals remain a gating factor. EIA processes routed through ONEP and related public-hearing steps can extend utility-scale renewable approvals to 12-24 months, and offshore wind zones face permit decisions only by late 2026 in the current evidence base.

Competitive Landscape

The Thailand power EPC market balances global OEMs and domestic contractors. Japanese groups, Mitsubishi Power, Marubeni, and Toshiba, dominate CCGT turnkey builds, leveraging decades-old EGAT alliances and hydrogen-ready turbine lines. Siemens Energy and GE Vernova focus on equipment-supply contracts, pairing with Thai civil firms to mitigate schedule and currency risks.

Chinese SOEs, PowerChina, CEEC, entered high-voltage transmission in 2024 with price points 12-15% below incumbents, completing a 500 kV GIS substation in Nakhon Si Thammarat. Local builders Sino-Thai, B.Grimm, Toyo-Thai, and Ital-Thai secure balance-of-plant and civil scopes thanks to intimate knowledge of Thai EIA and land-rights protocols. Offshore-wind foundations, BESS integration, and hydrogen retrofits remain open lanes; no Thai EPC owns a jacket-installation vessel, and hydrogen combustor lines are still absent.

Technology differentiation now hinges on digital twins, modular skid assemblies, and grid-forming inverter experience. EGAT’s 2023 pre-qualification roster lists 18 global contractors for 500 kV works, signaling harder bidding and thinner margins ahead. Despite moderate fragmentation, the top five players controlled roughly 45-50% of the 2025 value, indicating balanced competition without monopolistic dominance.

Thailand Power EPC Industry Leaders

Sino-Thai Engineering & Construction PCL

Mitsubishi Power

Siemens Energy AG

GE Vernova

AFRY (Pöyry PLC)

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace in Thailand power EPC is concentrated in grid and flexibility packages that sit between generation additions and the PDP and AEDP integration requirements, including 500 kV corridors, digital substations, and storage-enabled renewable interconnection. The evidence base indicates EPC scope is shifting toward renewable integration and system services. EGAT and metropolitan utilities have active digitalization programs, including MEA's 3.2 million smart-meter rollout by 2027, and grid-forming inverter deployments in hybrid renewable-plus-BESS projects are already creating demand for protection, communications, and control engineering beyond conventional balance-of-plant work.

Opportunities also extend to brownfield efficiency and replacement projects, alongside industrial and data-center driven captive and direct-supply builds. In July 2026, the Siemens-Marubeni consortium handed over the South Bangkok Power Plant Replacement Project Phase 1 for commercial operations, reflecting continued execution of large, schedule-critical EPC under EGAT oversight, while newer workstreams concentrate on upgrades and modular retrofits. Data-center investment filings clustered in the EEC, together with the 2,000 MW direct PPA allocation referenced in the report context, continue to pull forward solar-plus-BESS and substation upgrades. This favors EPC contractors with fast-track permitting capability, modular construction methods, and experience integrating storage, digital substations, and metering and communications layers into utility acceptance tests.

Recent Industry Developments

- July 2026: Siemens Energy and Marubeni, as a consortium, handed over South Bangkok Power Plant Replacement Project Phase 1 to EGAT for commercial operations. The milestone reinforces ongoing investment in high-efficiency thermal replacement and associated grid tie-in works, sustaining large-package EPC demand even as renewable integration expands.

- May 2026: B.Grimm Power collaborated with Siemens Energy to upgrade ten existing co-generation power plants in Thailand, lifting total capacity by 44 MW. The program highlights rising brownfield EPC scopes in controls, efficiency upgrades, and outage-managed execution, which broadens contractor demand beyond new-build projects.

- October 2024: Mitsubishi Power completed construction and commenced full commercial operations of a 5,300 MW natural gas-fired combined cycle power plant in Chonburi and Rayong provinces. The commissioning underscored continued reliance on large CCGT capacity and sets a reference point for hydrogen-ready and high-efficiency turbine requirements that increasingly shape EPC bid specifications.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the Thailand power EPC market is defined as the revenue earned from engineering, procurement, and construction work delivered for power generation plants and for transmission and distribution network projects within Thailand.

Scope exclusions: We exclude pure equipment manufacturing sales, routine operations and maintenance contracts, and consulting-only or design-only assignments that are not tied to an EPC delivery scope.

Segmentation Overview

- Power Generation EPC

- By Technology

- Thermal

- Nuclear

- Renewables

- By Capacity Band

- Up to 100 MW (DER, micro-grid)

- 100 to 499 MW

- Above 500 MW

- By End-User

- Regulated Utilities

- Independent Power Producers

- Industrial Captive Power

- Public Sector and SOE

- By Technology

- Power Transmission and Distribution (T&D) EPC

Data Sources, Market Sizing, and Validation

Desk Research

Desk research is used to frame the demand environment for power EPC work in Thailand, and then to gather reference data points that can be checked across multiple public records. We typically start with Thailand energy system plans and utility activity statistics, then connect them with project announcements and tender notes so the pipeline is not interpreted in isolation.

Sources used include public and official materials such as Thailand energy ministry and regulator releases, national utility planning documents, International Energy Agency (IEA) statistics, International Renewable Energy Agency (IRENA) capacity updates, and World Bank macro indicators that help explain the investment cycle. We also review company filings, investor presentations, association websites, and reputable press coverage, along with selective paid subscriptions for company financials and intelligence, patent databases, and import or export shipment-level databases where equipment flows can act as a cross-check. These examples are illustrative only, and many other sources are also referred to for data collection, validation, and clarification.

Primary Interviews and Surveys

Primary interviews and surveys are used to confirm what is moving from plans to awarded work, and to pressure test timing and pricing assumptions that desk research cannot fully lock down. We speak with EPC contractors, engineering firms, developers, key subcontractors, and project-linked stakeholders across generation and T and D to understand award patterns, typical contract scope splits, and local execution constraints.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 35% | CXOs: 18% | |

| Mid tier: 46% | Functional/Unit leaders: 27% | |

| Smaller Players: 19% | Managers: 55% |

Market-Sizing & Forecasting

Market sizing is built using a top-down and bottom-up blend, where the starting point is a demand pool reconstructed from Thailand project additions in generation and grid works, and then converted into EPC revenue using realistic EPC intensity factors. Once the demand pool is set, it is split across major technology types and capacity bands so that the mix reflects what is actually being built.

Key model inputs include announced and under-construction capacity (MW), grid expansion and upgrade activity, typical EPC cost per MW by technology, the share of projects awarded as full EPC versus split packages, and the timing of project milestones that shift revenue recognition. In places where public project values are missing, gaps are handled through proxy ranges (for example, technology-specific cost per MW and standard substation or line cost benchmarks) and then narrowed through primary feedback.

For forecasting, scenario analysis is used around the national build schedule and award delays, and then the final trajectory is cross-checked with a simple multivariate regression that relates EPC revenue to expected capacity additions, fuel mix shifts, and investment signals. The modeled outputs are subsequently corroborated with selective bottom-up approximations such as sampled project values, channel checks on procurement activity, and interview-based pricing sense checks, which helps us avoid overstating the addressable EPC work in any single year.

Data Validation & Update Cycle

Validation is done through several checks so that unusual jumps do not pass through unchallenged. Our team compares the modeled totals with independent signals like capacity additions, tender releases, and visible project execution progress, and then investigates variances by technology and by project size before sign-off.

Where the spread is driven by pricing, contract timing, or scope packaging, we re-contact relevant interviewees and then update the assumptions in the model, followed by another review pass. Reports are refreshed annually, with interim updates when major awards, cancellations, or policy shifts materially change the near-term pipeline, and then a final freshness pass is completed before delivery.

Mordor Intelligence's Thailand Power Epc Market Size Versus Other Published Estimates

Published estimates for Thailand power EPC often do not match because different authors are not counting the same work, and they also time the revenue differently across multi-year projects. Even when the same currency is used, the market year selected and the handling of price escalation can shift the final value.

The biggest gaps usually come from scope choices, especially whether transmission and distribution EPC is included alongside generation, and whether smaller grid upgrade packages are treated as EPC revenue or left out as maintenance-like work. Another driver is how aggressively early-stage projects are counted, since some estimates lean on announcements, while others require clearer award status and execution readiness before values are included.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 2.96 B (2026) | |

| Global Consultancy A | USD 3.99 B (2026) | This estimate appears to apply a broader project pool and faster revenue recognition, which can lift near-term totals when projects are still pre-award or have uncertain schedules. |

| Industry Publisher B | USD 1.70 B (2024) | This figure looks closer to power generation EPC only and uses an earlier year, which typically excludes T and D EPC and misses later-year grid and plant awards captured in newer tracking. |

The spread is largely explained by what is included and by how project timing is translated into yearly revenue. When T and D EPC is counted alongside generation, and project readiness filters are applied before pricing and escalation assumptions are finalized, the resulting 2026 value stays closer to visible award activity, which is aligned with the refresh cadence described by Mordor Intelligence in its Thailand EPC market write-up.

Key Questions Answered in the Report

How large is the Thailand power EPC market today?

The Thailand power EPC market size stood at USD 2.96 billion in 2026 and is projected to reach USD 3.35 billion by 2031.

Which EPC segment is growing faster, generation or transmission?

Transmission and distribution EPC is expanding at a 2.71% CAGR through 2031, outpacing generation construction as grid upgrades absorb offshore-wind and data-center demand.

What share of new projects comes from renewable energy?

Renewables accounted for 36.2% of 2025 EPC spending and are set to rise steadily, supported by a 5.8% CAGR under AEDP 2022 targets.

Why are microgrids gaining traction in Thailand?

Direct PPAs for data centers and industrial estates plus falling battery costs drive 6.1% CAGR growth for sub-100 MW microgrids that hedge grid-tariff exposure and improve reliability.

Which regions attract the most EPC investment?

The Eastern Economic Corridor leads with roughly 40% of incremental capacity additions, followed by the Bangkok Metropolitan Region and Southern offshore-wind zones.

Who are the leading EPC contractors in Thailand?

Mitsubishi Power, Marubeni, Toshiba, PowerChina, and local firms such as Sino-Thai and B.Grimm dominate project awards, especially in gas turbines, transmission lines, and solar-plus-BESS builds.

Page last updated on: