Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

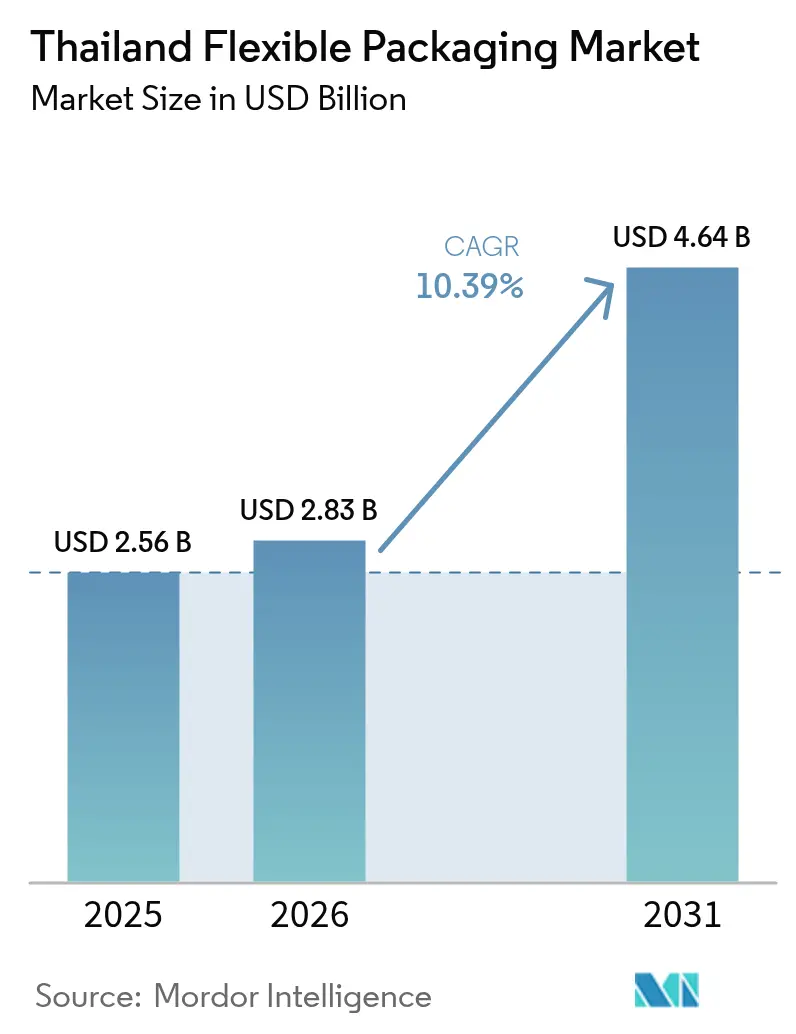

| Base Year Market Size (2025) | USD 2.56 Billion |

| Market Size (2026) | USD 2.83 Billion |

| Market Size (2031) | USD 4.64 Billion |

| Growth Rate (2026 - 2031) | 10.39% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Thailand Flexible Packaging Market Analysis by Mordor Intelligence

The Thailand flexible packaging market size was valued at USD 2.56 billion in 2025 and estimated to grow from USD 2.83 billion in 2026 to reach USD 4.64 billion by 2031, at a CAGR of 10.39% during the forecast period (2026-2031). Solid e-commerce logistics growth, government bioplastic subsidies, and a steady wave of China-plus-one manufacturing relocations are accelerating demand across pouch, sachet, and mailer formats. Brand-owner commitments to recyclability are nudging converters toward mono-material, machine-direction-oriented polyethylene (MDO-PE), even as high-barrier multilayer laminates retain their critical role for oxygen-sensitive foods. The Thailand flexible packaging market is also benefiting from rising halal ready-to-eat exports, a revitalized tourism sector that favors portion-controlled sachets, and policy-backed industrial investments in the Eastern Economic Corridor. Competitive intensity remains moderate, with multinational converters investing in chemical recycling and Industry 4.0 lines while more than 200 small and medium-sized enterprises (SMEs) retain leadership in short-run jobs.

Key Report Takeaways

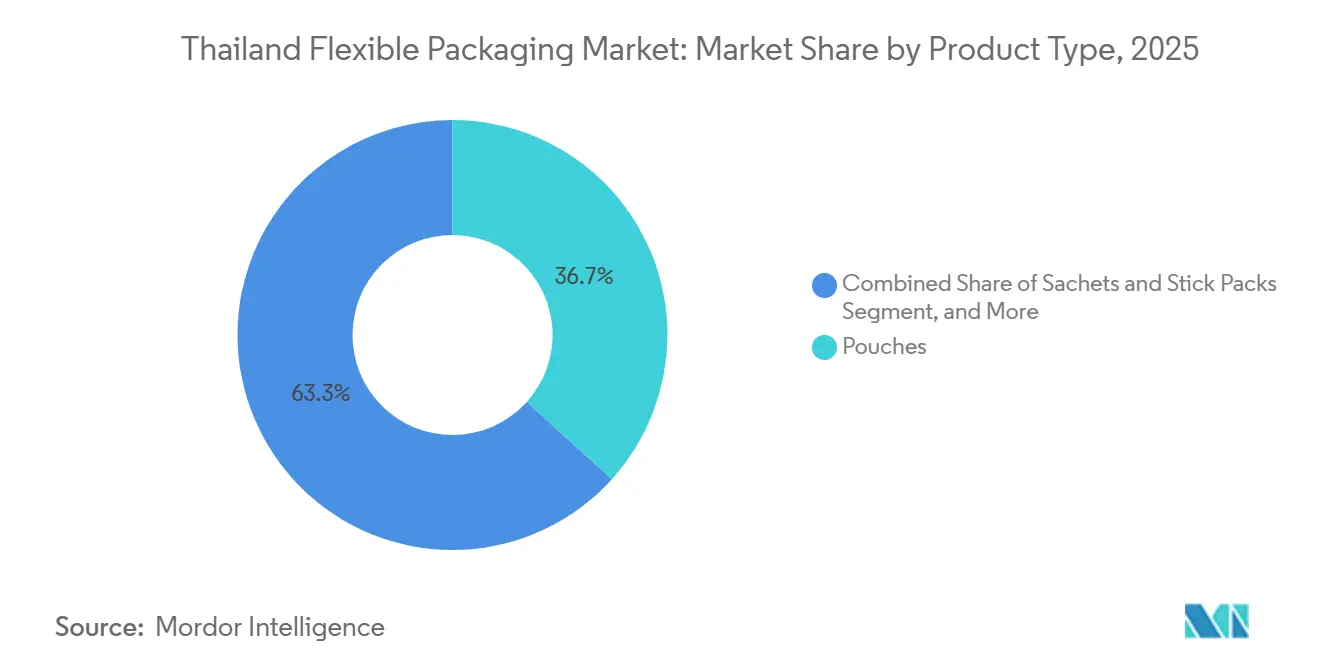

- By product type, pouches led with 36.71% of the Thailand flexible packaging market share in 2025, while sachets and stick packs are advancing at an 11.54% CAGR through 2031.

- By material, plastic captured 54.89% of the Thailand flexible packaging market in 2025, and bioplastics are projected to expand at an 11.36% CAGR through 2031.

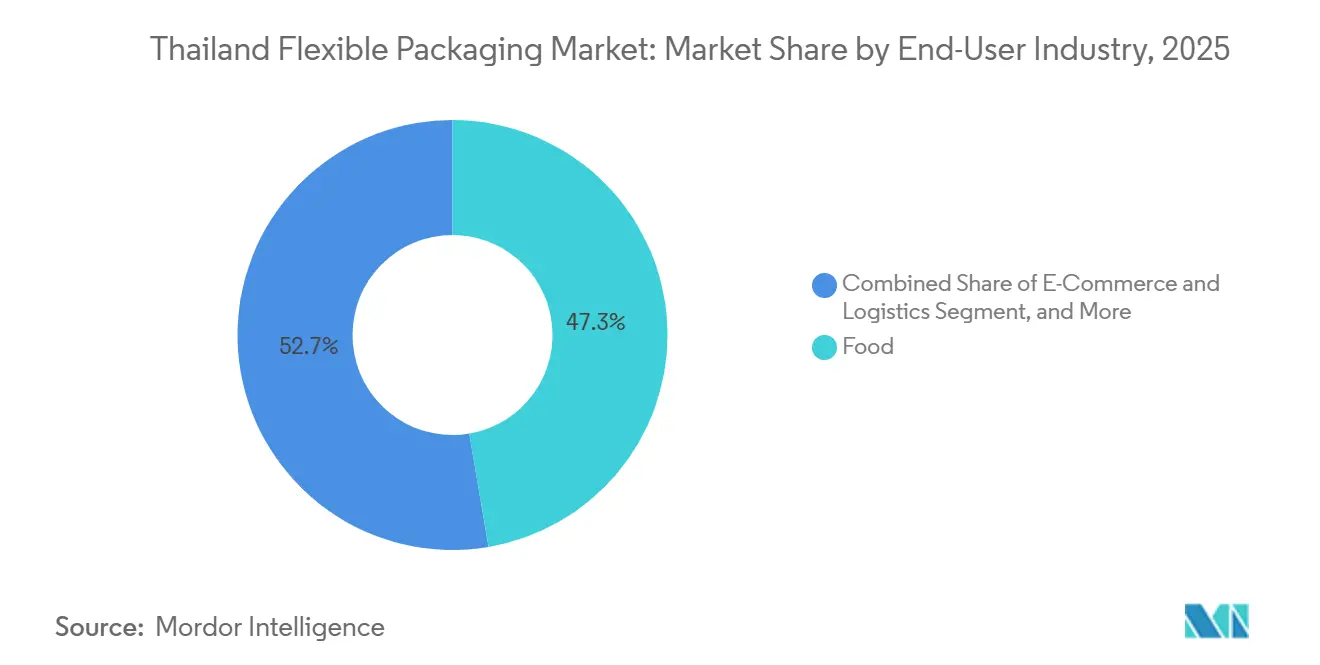

- By end-user industry, food accounted for 47.33% of 2025 demand in the Thailand flexible packaging market, whereas e-commerce and logistics are climbing fastest at an 11.74% CAGR during the forecast period.

- By layer structure, multilayer barrier laminates commanded 62.48% share in 2025, yet mono-material structures are poised to grow at a 10.77% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Flexible Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging E-commerce Parcel Volumes Accelerating Demand for Lightweight Mailing Packs | +2.8% | National, concentrated in Bangkok Metropolitan Region and Eastern Economic Corridor logistics hubs | Short term (≤ 2 years) |

| Boom in Thailand's Halal and Ready-to-Eat Food Exports Requiring High-Barrier Pouches | +2.1% | National, with early gains in Southern provinces and Central food-processing zones | Medium term (2-4 years) |

| Bio-Circular-Green Policy Subsidising Bioplastic Film Capacity Additions | +1.9% | National, led by Rayong and Map Ta Phut petrochemical clusters | Medium term (2-4 years) |

| Brand-Owner Shift to Mono-Material MDO-PE Film for Recyclability | +1.5% | Global, with spillover to Thailand via multinational fast-moving consumer goods mandates | Medium term (2-4 years) |

| Adoption of Industry 4.0 Flexo Presses Improving Short-Run Economics for SMEs | +1.2% | National, early adoption in Bangkok and Samut Prakan converter clusters | Long term (≥ 4 years) |

| International FMCG Near-Shoring to Thailand amid China+1 Strategy | +0.9% | Eastern Economic Corridor and Chonburi industrial estates | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surging E-Commerce Parcel Volumes Accelerating Demand for Lightweight Mailing Packs

Daily parcel throughput climbed to 7-8 million in 2025, a jump that converted corrugated shippers into lighter polyethylene mailers, enabling them to save 20-30% on last-mile freight costs. Private couriers installed automated sorters to handle peak loads of more than 12 million parcels per day, pulling in orders for peel-and-seal pouches, anti-static electronics sleeves, and insulated frozen-food bags. Converters trimmed mailer gauges to 40-60 microns, lowering resin usage without sacrificing drop resistance. Apparel and beauty brands, which dominate flash-sale events, are requesting custom graphics within one-week lead times, pressuring SMEs to adopt quick-change flexo presses. Despite the volume spike, Thailand has not imposed e-commerce packaging regulations, so voluntary take-back programs by marketplaces are the main nudge toward recyclable mono-material solutions.[1]Office of the National Economic and Social Development Council, “Thailand Digital Trade Outlook 2027,” NESDC.go.th

Boom in Thailand's Halal and Ready-to-Eat Food Exports Requiring High-Barrier Pouches

Halal-certified exports reached roughly USD 7.8 billion in 2025, anchored by shelf-stable curries and ready meals that demand retort pouches with aluminum-foil or silicon-oxide barriers capable of 18-24 month shelf life. Certification by the Halal Science Center and the Central Islamic Council creates documentation hurdles that favor large converters with traceable supply chains. Gulf Cooperation Council importers increasingly request high-barrier, transparent films to showcase product quality, spurring investment in aluminum oxide vapor deposition. Resealable zippers and spouts command a 30-40% price premium but deliver portion control sought by urban consumers abroad. Expected expansion of halal capacity in Southern provinces is set to lift local demand for retort-grade laminates through 2030.[2]Department of International Trade Promotion, “Gulfood 2026 Participation Report,” DITP.go.th

Bio-Circular-Green Policy Subsidising Bioplastic Film Capacity Additions

The Bio-Circular-Green model grants up to eight-year tax holidays plus 30-50% capital subsidies, propelling bioplastic capacity from 95,000 t/y in 2024 toward a 375,000-400,000 t/y goal by 2030. NatureWorks opened a 75,000 t/y polylactic acid plant in 2025, cutting regional PLA resin prices by 10-15% and making compostable produce bags and mailers cost-competitive with conventional polyethylene. Large retailers are now piloting PLA-based bakery wraps to comply with municipal park bans on single-use plastics. Converters are blending PLA with PBAT to bolster seal strength, addressing earlier puncture issues that limited adoption. Carbon credits issued by the Thailand Greenhouse Gas Management Organization add another incentive for brand owners who switch to certified bioplastic films.[3]Office of Industrial Economics, “Bioplastic Capacity Roadmap 2024,” OIE.go.th

Brand-Owner Shifts to Mono-Material MDO-PE Film for Recyclability

Global FMCG firms pledge 100% recyclable packaging by 2030, driving a pivot from polyethylene-polypropylene-ethylene vinyl alcohol laminates to mono-material MDO-PE that fits existing polyethylene waste streams. Newer metallocene-based PE grades deliver 60-70% of legacy moisture barrier while allowing 30-40 micron gauge reductions, trimming unit resin cost by 15-20%. Converters accept a 10-15% oxygen barrier trade-off in dry snacks and pet food to gain a marketing edge on recyclability. Sorting facilities report lower contamination when mono-material pouches replace mixed polymer laminates, boosting recovery yields. SMEs must still fund extrusion upgrades, with three-to-five-year paybacks delaying widespread change.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Ban on Imported Plastic Scrap Tightening Local rPET/rPE Availability | -1.8% | National, acute in Bangkok and Eastern Seaboard converter clusters | Short term (≤ 2 years) |

| Extended Producer Responsibility Draft Law Raising Compliance Costs | -1.4% | National, with higher impact on multinational fast-moving consumer goods firms | Medium term (2-4 years) |

| Skilled-Labour Shortage in Advanced Printing and Converting | -0.9% | National, concentrated in Bangkok Metropolitan Region and Samut Prakan | Long term (≥ 4 years) |

| Volatile Feedstock Prices Eroding Converter Margins | -0.7% | National, linked to global crude oil and naphtha markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Ban on Imported Plastic Scrap Tightening Local rPET/rPE Availability

The 2025 prohibition on imported plastic scrap removed 150,000-200,000 t/y of recycled PET and PE feedstock, inflating recycled PET prices by 25-30% and eroding the cost edge over virgin resin. Domestic collection accounts for only a third of available PET bottles, while flexible film recovery remains negligible due to manual sorting constraints. Food-grade rPET supply now meets less than half of converter demand, pushing exporters to pay premiums for certified imported pellets or risk failing recycled-content mandates in Europe. Chemical recycling pilots by SCG Packaging and TPBI promise relief but are unlikely to reach scale before 2027. Converters serving cosmetic sachets and detergent refill packs face the sharpest squeeze as recycled-content targets tighten.

Extended Producer Responsibility Draft Law Raising Compliance Costs

A draft Extended Producer Responsibility (EPR) bill, slated for enactment by 2027, proposes levies equal to 2-4% of annual packaging spend, tiered by recyclability. Brand owners have begun redesigning from metallized films to mono-material MDO-PE, yet SMEs lack the capital to swap tooling or fund design trials. Uncertainty over fee formulas has already delayed several extrusion upgrades because payback models cannot price future EPR costs. Producer responsibility organizations are expected to pool obligations, but governance rules remain vague, generating caution among domestic food brands. Industry groups lobby for longer phase-ins and export exemptions to avoid ceding share to nearby Vietnam, where EPR remains voluntary

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Pouches Stay Dominant While Sachets Accelerate

Pouches accounted for a commanding 36.71% of the Thai flexible packaging market in 2025, underscoring their versatility for beverages, pet food, and home-care refills. Brands prefer stand-up formats with spouts or zippers that lend billboard-like shelf presence and enable portion control at a lower total system cost than glass jars. In parallel, sachets and stick packs are growing at an 11.54% CAGR as on-the-go consumers snap up single-serve beverages, condiments, and nutraceutical powders delivered directly via e-commerce. The Thailand flexible packaging market size for sachets is forecast to reach USD xx billion by 2031, helped by hotel amenity refills and trial-size personal-care samples that ride tourism’s rebound. Pouch converters are adding digital print modules to serve seasonal promotions, whereas sachet makers invest in high-speed multilane form-fill-seal machines that can run 1,200 sticks per minute. Weight reduction is also a focal point; new linear low-density polyethylene films cut pouch gram weight by 8-10% without compromising drop resistance.

Down-gauging aside, pouches hold firm in value-added retort meals and pet food where oxygen and moisture barriers are non-negotiable. Sachets, on the other hand, are moving beyond powders into liquids such as single-dose shampoos using heat-resistant cast polypropylene layers. Multinational beverage brands are trialing perforated twin-stick formats that mix probiotic cultures with vitamins only when opened, placing extra sealing accuracy demands on equipment. Local SMEs that serve instant noodle condiments rely on flexo presses with 10,000-unit minimums, creating an opportunity for digital-only newcomers serving micro-batches for influencer-led product launches. Overall, the Thailand flexible packaging market continues to favor formats that balance consumer convenience, lightweight logistics, and evolving EPR cost structures.

By Material: Plastics Dominate As Bioplastics Build Momentum

Plastic retained a 54.89% share of the Thailand flexible packaging market in 2025, thanks to polyethylene, polypropylene, and PET winning on cost-performance metrics. Polyethylene’s broad toolkit, from low-density grades for bread bags to high-density grades for detergent pouches, anchors converter production volumes exceeding 3 million t/y. Yet the Thailand flexible packaging market size for bioplastics is expanding quickly and is forecast to grow at an 11.36% CAGR, catalyzed by the Bio-Circular-Green subsidy scheme and falling PLA resin prices. Brand owners in fresh produce and bakery lines have switched to PLA-based films that meet marine park compostability requirements while maintaining pack integrity throughout an eight-day supply chain.

Conventional plastic stalwarts now face dual pressures: volatile crude-linked feedstock costs and EPR fees that penalize difficult-to-recycle multilayer structures. Polypropylene’s clarity and heat resistance keep it relevant for boil-in-bag rice and microwave popcorn, but recycled PP streams remain underdeveloped, hurting circularity claims. PET stays critical for metallized snack films, yet shortages of food-grade rPET after the scrap-import ban mean converters often blend virgin and recycled content below the 25% thresholds specified by European customers. On the bioplastic front, early-stage PBAT blends enhance toughness, while GMO-free PLA grades answer export market labeling requirements. Converters that master coextrusion of bio-based outer layers with thin barrier tie layers are well positioned to capture premium positions as multinational FMCG buyers seek to decarbonize their regional portfolios.

By End-User Industry: Food Anchors Volume, E-Commerce Leads Growth

Food retained 47.33% of 2025 demand in the Thailand flexible packaging market, led by rice, seafood, and snack applications, where extended shelf life offsets the humid tropical distribution conditions. Modified-atmosphere pouches for durian chips and freeze-dried fruits are penetrating export niches, leveraging oxygen scavengers to achieve 12-month milestones. Meanwhile, e-commerce and logistics are on pace for the fastest trajectory, expanding at an 11.74% CAGR through 2031. Apparel mailers, bubble-wrap liners, and tamper-evident pouches now form a staple cost line for online sellers that prioritize cube efficiency over traditional corrugated boxes. The Thailand flexible packaging market share for logistics films is expected to double by 2031 as next-day delivery footprints stretch into secondary provinces.

Beverage converters deploy aseptic aluminum-free pouches for energy drinks and children’s juices, capturing refrigeration savings and portability advantages. Personal-care brands are introducing refill pouches with 80% less plastic than rigid pumps, although consumer acceptance of flexible packs for thick lotions remains uneven. The pharmaceutical sector relies on regulated blister and sachet lines certified to ISO 15378, boosting demand for high-barrier aluminum laminates. Pet food mirrors humanization trends, migrating from bulky polypropylene woven sacks into premium stand-up pouches with press-to-close sliders, a switch that boosts shelf appeal and reseal convenience. Collectively, these shifts underscore broad diversification beyond core food into lifestyle, health, and logistics verticals, which will sustain the Thailand flexible packaging market well past 2031.

By Layer Structure: Multilayer Laminates Hold Sway, Mono-Material Gains Pace

Multilayer laminates accounted for 62.48% of the 2025 value in the Thailand flexible packaging market, reflecting their unmatched gas, aroma, and moisture barriers for coffee, pharmaceuticals, and seafood. Typical seven-layer builds sandwich PE, PET, EVOH, and sometimes aluminum foil, providing oxygen transmission rates of <1 cc/m²/day, which are necessary for a 24-month shelf life. Yet mono-material structures are forecast to capture a growing slice, expanding at a 10.77% CAGR as EPR and corporate recycling agendas reshape design briefs. The Thailand flexible packaging market size attributable to mono-material solutions could top USD xx billion by 2031 if fee penalties on non-recyclable laminates become law.

Leading converters are installing MDO-PE lines that stretch film to improve stiffness, allowing the elimination of oriented polyamide or PET outer layers. Early adopters report 15-20% resin savings and faster cure times when switching to solvent-free adhesives, though capital intensity remains high at USD 5-7 million per line. Brands accept 10-15% shorter shelf life in dry-food categories, judging the trade-off acceptable for circularity messaging and fee relief. Research collaborations aim to achieve clear SiOx coatings on mono-PE that could close the barrier gap within 2 years. Despite momentum, barrier laminates will persist in pharmaceutical sachets and high-fat snacks until new chemistries or recycling-ready metallization scales economically across converter tiers.

Geography Analysis

Bangkok and its surrounding provinces accounted for about 48% of the 2025 Thailand flexible packaging market share, a dominance rooted in the heavy concentration of fast-moving consumer goods headquarters, dark-store fulfillment hubs, and high-turn retail outlets. Dense urban demand supports rapid artwork approval cycles, enabling converters near the capital to deliver printed pouches in less than 5 days. Ongoing same-day delivery programs by leading e-commerce platforms are also lifting order volumes for lightweight mailers and tamper-evident sachets. As a result, local extrusion and printing capacity continues to expand inside industrial estates in Samut Prakan, Pathum Thani, and Nonthaburi.

The Eastern Seaboard, covering Rayong, Chonburi, and Chachoengsao, accounted for roughly 27% of the 2025 value and is projected to grow at a 10.8% CAGR through 2031. Petrochemical feedstock plants supply low-cost polyethylene and polypropylene to nearby converters, while automotive and electronics assemblers consume stretch film, anti-static bags, and corrosion-inhibitor wraps. Government-backed double-track rail projects linking Laem Chabang port with inland depots are expected to trim freight costs by up to 20%, further reinforcing the region’s appeal to future investors. Foreign manufacturers relocating from China have already announced new food and device plants that will require high-barrier pouches, adding depth to the local demand base.

Outside the big two hubs, Central Thailand accounts for 16% of Thailand's flexible packaging market, thanks to rice-milling and sugar-processing clusters in Ayutthaya and Nakhon Pathom that rely on gusseted bags and bulk liners. Northern provinces such as Chiang Mai capture close to 9% of spending, supported by artisanal snack exporters and coffee roasters that favor small-batch digital printing. The South contributes 9% today and shows the fastest trajectory, rising at a 11.2% CAGR as halal food factories and seafood processors adopt retortable pouches and transparent, high-barrier films. New deepwater berths in Songkhla are improving container connectivity for seafood exports, while rubber plantations supply latex coatings for specialty barrier films. The sparsely industrialized Northeast remains below 7% but could see an uplift once planned agro-processing free zones come online.

Competitive Landscape

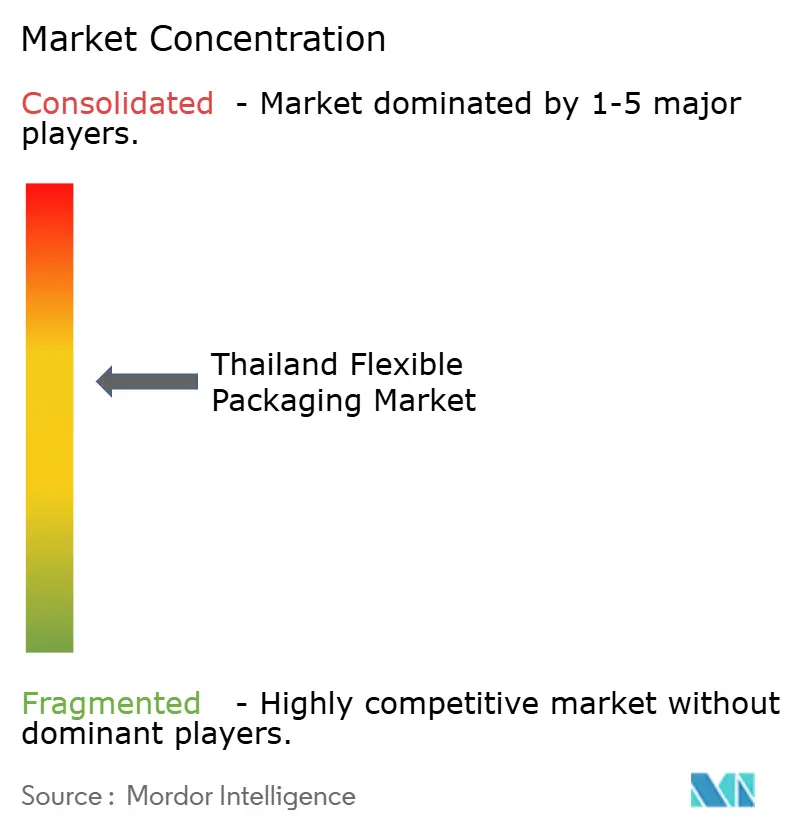

The five largest converters, Amcor, SCG Packaging, Huhtamaki, Thung Hua Sinn Group, and Sealed Air, collectively controlled roughly 37% of 2025 sales, leaving the remaining 63% to more than 200 small and medium-sized enterprises. Multinationals dominate in retort-grade pouches, pharmaceutical laminates, and machine-direction-oriented polyethylene films, segments that demand capital-intensive coextrusion lines and global certifications. Local players flourish in commodity bags and quick-turn runs where customer proximity and low overheads trump scale. Competition, therefore, varies sharply by end use, swinging from consolidated in high-barrier food exports to fragmented in plain rice and sugar sacks.

Strategic activity accelerated in 2025. SCG Packaging allocated fresh capital for mono-material PE lines in Rayong, positioning itself for the coming Extended Producer Responsibility fee structure that rewards recyclable films. Huhtamaki completed an 8,000-ton annual expansion featuring solvent-free lamination and high-speed MDO-PE extrusion, aimed at snack and pet food contracts that now insist on circular-ready structures. Amcor integrated the capabilities from its late-2024 Berry HHS acquisition, broadening its regional sterile-pack offering for medical devices assembled in the Eastern Economic Corridor. At the same time, Sealed Air began marketing bag-in-box solutions from its newly acquired Liquibox unit to Thai beverage fillers seeking aseptic flexibility.

Technology adoption is widening the performance gap. Top-tier plants run inline camera inspections, predictive maintenance software, and automated turret slitters, pushing scrap rates below 4%, while the majority of SMEs still rely on manual checks and record 8-12% waste. Digital-only newcomers such as FastPack serve influencer-led beauty brands with 1,000-unit minimums and 72-hour lead times, nibbling share from traditional flexo houses. Rising EPR costs, higher wage bills, and the need for traceable recycled inputs point to greater consolidation, as smaller converters may lack the balance-sheet strength to fund compliance and automation simultaneously.

Thailand Flexible Packaging Industry Leaders

Amcor plc

Thung Hua Sinn Group

Huhtamaki Oyj

Sealed Air Corporation

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: NatureWorks began commercial runs at its 75,000 t/y PLA plant in Rayong, a USD 600 million project that immediately expanded resin options for compostable films.

- September 2025: Huhtamaki reported 14% revenue growth from its Thai flexible packaging plants over the first three quarters, following the completion of an 8,000-ton-per-year expansion that added machine-direction-oriented polyethylene extrusion and solvent-free lamination for fully recyclable films.

- May 2025: Thailand’s Pollution Control Department released updated EPR guidelines, detailing tiered fees tied to recyclability that slash levies on mono-material PE and PET packs by 40-50% compared with multilayer structures, while outlining draft compliance timelines for brand owners.

- March 2025: SCG Packaging posted an 8% year-over-year revenue lift for the first quarter, fueled by e-commerce and food packaging demand, and confirmed new mono-material polyethylene extrusion lines in Rayong to supply recyclable film ahead of Thailand’s expected 2027 EPR rules.

Thailand Flexible Packaging Market Report Scope

The Thailand Flexible Packaging Market Report is Segmented by Product Type (Pouches, Bags, Films and Wraps, Sachets and Stick Packs, Labels and Sleeves, Flexitanks and Other Product Types), Material (Plastic, Paper, Aluminum Foil, Bioplastics, Multilayer Barrier Structures), End-User Industry (Food, Beverage, Personal Care and Cosmetics, Pharmaceuticals and Healthcare, Pet Food and Animal Feed, Home-Care and Industrial, E-Commerce and Logistics), Layer Structure (Mono-Material Structures, and Multilayer Barrier Laminates). The Market Forecasts are Provided in Terms of Value (USD).

By Product Type

| Pouches |

| Bags |

| Films and Wraps |

| Sachets and Stick Packs |

| Labels and Sleeves |

| Flexitanks and Other Product Types |

By Material

| Plastic | Polyethylene (PE) |

| Polypropylene (PP) | |

| Polyethylene Terephthalate (PET) | |

| Polyvinyl Chloride (PVC) | |

| Other Plastics | |

| Paper | |

| Aluminum Foil | |

| Bioplastics | |

| Multilayer Barrier Structures |

By End-User Industry

| Food |

| Beverage |

| Personal Care and Cosmetics |

| Pharmaceuticals and Healthcare |

| Pet Food and Animal Feed |

| Home-Care and Industrial |

| E-Commerce and Logistics |

By Layer Structure

| Mono-Material Structures |

| Multilayer Barrier Laminates |

| By Product Type | Pouches | |

| Bags | ||

| Films and Wraps | ||

| Sachets and Stick Packs | ||

| Labels and Sleeves | ||

| Flexitanks and Other Product Types | ||

| By Material | Plastic | Polyethylene (PE) |

| Polypropylene (PP) | ||

| Polyethylene Terephthalate (PET) | ||

| Polyvinyl Chloride (PVC) | ||

| Other Plastics | ||

| Paper | ||

| Aluminum Foil | ||

| Bioplastics | ||

| Multilayer Barrier Structures | ||

| By End-User Industry | Food | |

| Beverage | ||

| Personal Care and Cosmetics | ||

| Pharmaceuticals and Healthcare | ||

| Pet Food and Animal Feed | ||

| Home-Care and Industrial | ||

| E-Commerce and Logistics | ||

| By Layer Structure | Mono-Material Structures | |

| Multilayer Barrier Laminates | ||

Key Questions Answered in the Report

How large is the Thailand flexible packaging market in 2026?

It is estimated at USD 2.83 billion, on its way to USD 4.64 billion by 2031 at a 10.39% CAGR.

Which format dominates demand today?

Pouches top the mix, securing 36.71% share in 2025 due to their versatility in food, pet food, and home-care refills.

What is the fastest-growing end-use segment?

E-commerce and logistics packaging is advancing at an 11.74% CAGR, fueled by 7-8 million daily parcel volumes.

How will upcoming EPR rules affect converters?

Draft legislation could add 2-4% to packaging spend, pressuring non-recyclable multilayer films and favoring mono-material MDO-PE.

Are bioplastics viable in Thailand?

Yes, Bio-Circular-Green incentives and new PLA capacity have cut resin prices 10-15%, enabling double-digit growth in compostable films.

Which Thai region is posting the fastest consumption growth?

The Eastern Seaboard is projected to rise at a 10.8% CAGR through 2031, driven by near-shored electronics and consumer-goods factories.

Page last updated on: