Market Overview

| Study Period | 2019 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

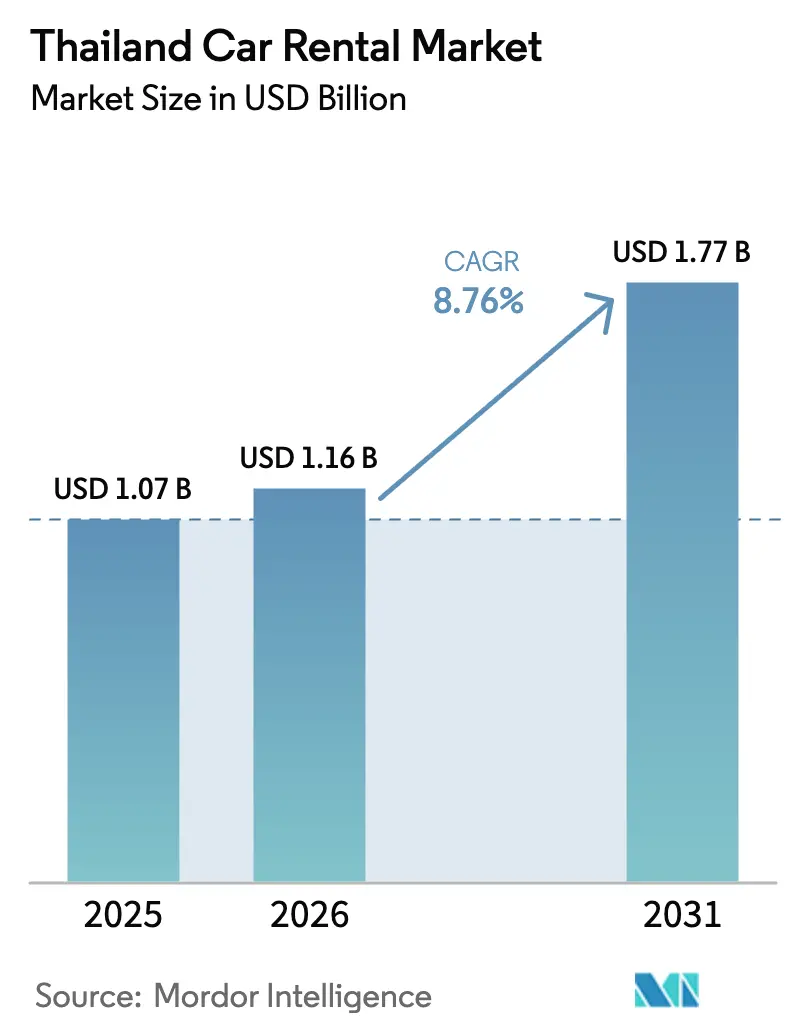

| Base Year Market Size (2025) | USD 1.07 Billion |

| Market Size (2026) | USD 1.16 Billion |

| Market Size (2031) | USD 1.77 Billion |

| Growth Rate (2026 - 2031) | 8.76% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Thailand Car Rental Market Analysis by Mordor Intelligence

The Thailand car rental market size was valued at USD 1.07 billion in 2025 and is estimated to grow from USD 1.16 billion in 2026 to reach USD 1.77 billion by 2031, at a CAGR of 8.76% during the forecast period (2026-2031). Sustained visa-free entry for major source markets, rapid expansion of low-cost carriers into secondary airports, and accelerated fleet electrification together underpin the long-run growth profile of the Thailand car rental market. At the same time, the sector faces near-term turbulence from a sharp fall in Chinese group tourism, tightening fleet-financing rules, and rising vehicle acquisition costs. Operators are therefore rebalancing toward domestic travelers and long-term corporate subscriptions, deploying digital booking platforms to capture price-sensitive demand, and adding battery electric vehicles (BEVs) to meet government sustainability incentives. Competitive intensity is rising as peer-to-peer platforms and ride-hailing-linked rental schemes squeeze traditional operators’ margins and force them to invest in differentiated service models.

Key Report Takeaways

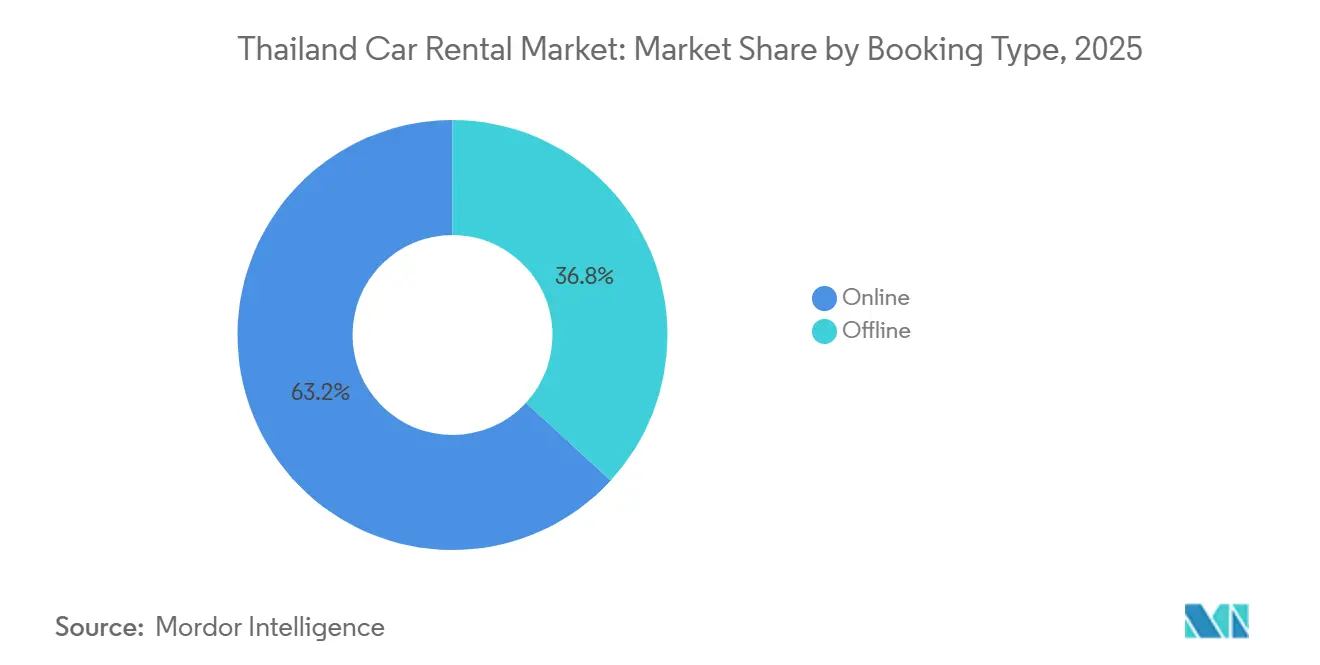

- By booking type, online channels held 63.16% of the Thailand car rental market share in 2025, and are advancing at a 9.28% CAGR through 2031.

- By rental duration, short-term agreements accounted for 71.26% of the Thailand car rental market share in 2025; long-term contracts are projected to expand at a 9.41% CAGR through 2031.

- By application, leisure and tourism accounted for 65.47% of the Thailand car rental market in 2025, whereas commuting and business rentals are the fastest-growing segment, with a 9.43% CAGR to 2031.

- By vehicle class, economy and mini cars led the Thailand car rental market with 48.72% share in 2025; SUVs and MPVs are forecast to grow at a 9.31% CAGR through 2031.

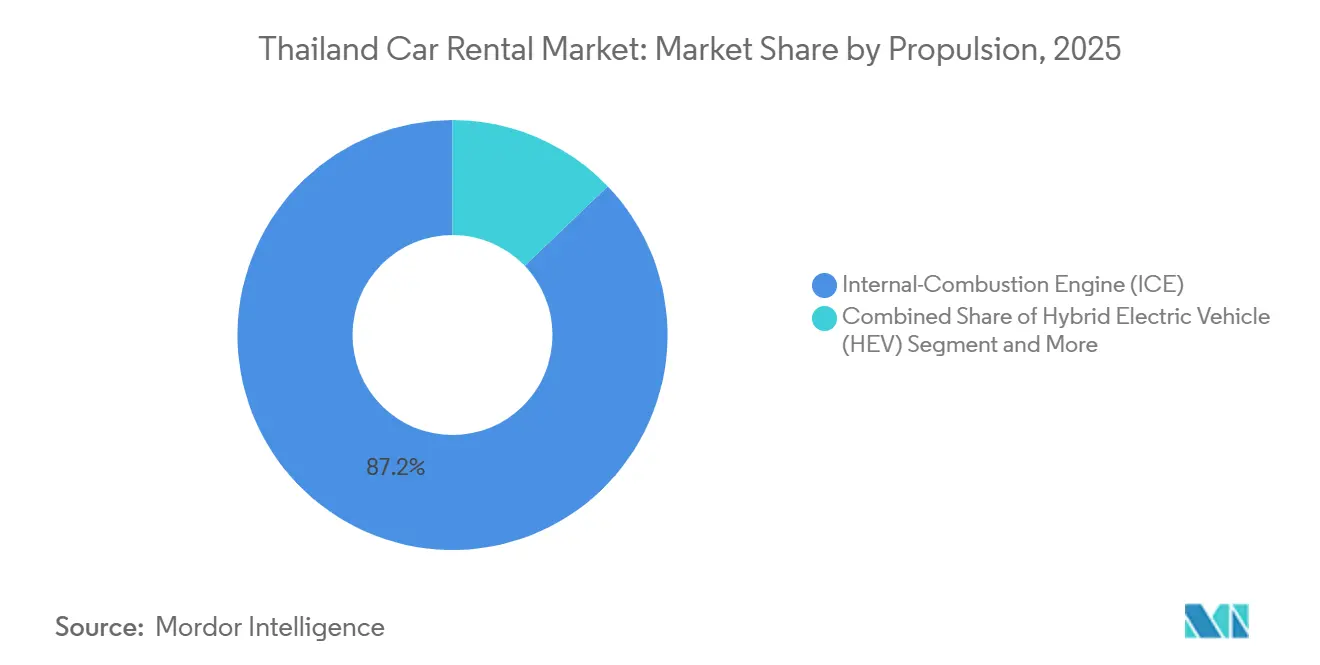

- By propulsion, internal-combustion engine (ICE) vehicles dominated the Thailand car rental market share with 87.15% in 2025, but BEVs are expanding at a 12.36% CAGR through 2031.

- By rental channel, airport counters commanded 68.31% of the Thailand car rental market in 2025, while downtown and off-airport outlets are growing at a 9.38% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Thailand Car Rental Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tourism Rebound | +2.5% | Bangkok, Phuket, Chiang Mai, Pattaya, Krabi, Surat Thani | Medium term (2-4 years) |

| Digital Booking & Price-Comparison Platforms | +1.8% | Bangkok, Phuket, Chiang Mai, Pattaya, Rayong | Short term (≤ 2 years) |

| Expansion of Low-Cost Carriers | +1.5% | Rayong (U-Tapao), Chiang Mai, Khon Kaen, Chiang Rai, Hat Yai, Surat Thani | Medium term (2-4 years) |

| Self-Drive Tourism Surge | +1.2% | Bangkok, Phuket, Chiang Mai, Pattaya | Short term (≤ 2 years) |

| EV-Rental Purchase Incentive Program | +1.0% | Bangkok, Phuket, Chiang Mai, Rayong | Long term (≥ 4 years) |

| Deposit & Damage-Tracking Systems | +0.3% | Bangkok, Phuket | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tourism Rebound & Visa-Free Schemes

Thailand’s permanent visa-waiver for China, India, and Russia, introduced in 2025, removed a long-standing friction that deterred short-stay travelers. Chinese independent visitors recovered to over 75% of pre-pandemic levels in 2025, boosting multi-day car-hire demand beyond coach-based itineraries. Indian and Russian tourists accounted for around 4.4 million arrivals in 2025 and gravitated toward multi-destination road trips across beach and cultural circuits[1]"Thailand welcomes 32.9 million foreign tourists in 2025", The Nation, nationthailand.com. The shift toward spontaneous, last-minute digital reservations rewards operators with real-time fleet visibility and flexible pick-up options.

Rise of Digital Booking & Price-Comparison Platforms

Digital booking apps such as Drivemate and Houpcar, along with aggregators embedded in super-apps like Grab and Traveloka, captured 63.16% of the Thailand car rental market transactions in 2025 and are growing at a 9.28% CAGR through 2031. Transparent price discovery pressures margins but vastly enlarges reach, prompting incumbents to integrate application programming interfaces (APIs) that feed real-time rates to multiple portals. Operators differentiate via doorstep delivery, bundled insurance, and loyalty perks, yet must streamline cost structures to remain competitive against asset-light digital platforms.

Expansion of Low-Cost Carriers to Secondary Airports

Airports of Thailand plans to increase Suvarnabhumi's capacity to 70 million passengers by 2031, and U-Tapao's to 16 million by 2026, distributing traveler flows away from Bangkok’s primary gateways[2]"AOT pushes Suvarnabhumi expansion worth 210bn baht", The Nation, nationthailand.com. New frequencies to Chiang Rai, Khon Kaen, and Hat Yai create fresh pockets of car-hire demand, but operators face upfront investments in counters, parking, and local fleets before passenger volumes fully materialize. Flexible branch scheduling and inter-city one-way rentals mitigate stranded-capacity risk.

Surge in Chinese Self-Drive Tourism

In recent years, there has been a noticeable increase in the number of free independent travelers from China. This group tends to spend more on their trips and shows a strong preference for self-drive itineraries, often supported by the convenience of Chinese-language GPS applications. While concerns about safety and the limited availability of right-hand-drive vehicles have posed challenges, growing confidence in peer-reviewed platforms like Zuzuche is helping travelers overcome these barriers. This shift reflects a broader trend of Chinese tourists seeking more personalized and flexible travel experiences.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Fleet Acquisition | -1.9% | Global, with an acute impact on the premium and EV segments | Short term (≤ 2 years) |

| Competition From Ride-Hailing Apps | -1.4% | National, concentrated in urban centers and tourist areas | Medium term (2-4 years) |

| Stricter Fleet-Financing | -1.1% | National, affecting both operators and consumers | Short term (≤ 2 years) |

| Sparse Charging Infrastructure | -0.8% | National, with rural and intercity gaps most affected | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Fleet Acquisition & Maintenance Costs

The 2026 excise-tax overhaul slashed BEV rates to 2% while lifting taxes on large ICE engines to 50%, inflating upfront prices for conventional cars and forcing rental firms to weigh accelerated electrification against capital constraints. Semiconductor shortages extend delivery lead times, prolonging fleet age and raising maintenance bills. New central-bank supervision of auto leasing since December 2025 has tightened credit standards, lifting borrowing costs for smaller operators. Balancing fiscal incentives with liquidity needs becomes critical for mid-tier companies.

Competition from Ride-Hailing and Super-Apps

Grab, commanding around 70% of Thailand's ride-hailing market, has innovatively integrated rental economics into its platform by leasing electric vehicles (EVs) directly to drivers through a revenue-based financing model. While on-demand mobility services have emerged as alternatives to traditional taxi rentals, they've inadvertently reduced the market size for airport transfers. Furthermore, super-apps, which seamlessly combine services like flights, hotels, and rides, have begun to overshadow traditional operators. This shift has compelled these operators to enhance their offerings, investing in value-added services and corporate subscriptions—areas where ride-hailing services struggle to compete.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Booking Type: Digital Channels Redefine Distribution

Online reservations accounted for 63.16% of the Thailand car rental market size in 2025 and are projected to grow at a 9.28% CAGR through 2031, driven by metasearch engines and peer-to-peer listings that expose live prices across dozens of operators. Apps embed seamless e-wallet payments, one-click insurance, and user ratings, raising expectations for transparency and convenience. Offline desks still capture last-minute walk-ins at major airports, but their growth lags as mobile-first travelers favor the immediacy of smartphone bookings. Operators experiment with dynamic pricing and loyalty partnerships to retain direct-channel traffic amid aggressive aggregator discounting.

Thairung Group’s acquisition of Drivemate and the immediate infusion of a BEV fleet validated the strategic pivot toward asset-light supply and digital discovery. Super-apps extend reach into food delivery and fintech ecosystems, converting everyday users into rental customers through cross-promotion. Elderly travelers and first-time visitors still value face-to-face service for complex insurance questions, sustaining a residual role for staffed counters. Nonetheless, digital share gains appear durable, underpinning automated check-out kiosks and contactless vehicle handovers in high-volume locations.

By Rental Duration: Corporate Subscriptions Gain Momentum

Short-term hires accounted for 71.26% of Thailand's car rental market share in 2025, driven by leisure-centric traffic at Bangkok, Phuket, and Chiang Mai airports. Daily rates remain the yield driver, yet seasonal volatility exposes cash flow to swings. In contrast, long-term rentals and monthly subscriptions bundled with maintenance and roadside support are set to grow at a 9.41% CAGR through 2031. Multinationals adopt pay-as-you-use fleets to hedge against ownership costs and align with sustainability mandates by swapping ICE units for BEVs.

Corporate accounts prize predictable budgeting and nationwide service coverage, pushing operators to offer fleet portals with usage analytics and centralized billing. Demand also stems from remote-work professionals choosing flexible car access over ownership. Subscription providers optimize asset utilization by redeploying idle corporate cars into weekend leisure pools, smoothing revenue seasonality. For traditional daily-rental players, entering long-term contracts requires re-engineering maintenance operations and credit-risk assessment frameworks.

By Application: Leisure Dominates, Business Segment Accelerates

Leisure travel delivered 65.47% of the Thailand car rental market size in 2025, anchored by inbound visitors and domestic holidaymakers exploiting Thailand’s dense long-weekend calendar. Visa-free policies and LCC route proliferation sustain baseline growth, yet leisure bookings remain vulnerable to exchange-rate shifts and geopolitical shocks such as the 2025 drop in Chinese group tours. Business and commuting rentals, while smaller, are emerging as the growth engine, with a 9.43% CAGR through 2031, as corporates pivot to fleet-as-a-service contracts and ride-hailing drivers lease cars through platform financing.

Enterprise clients spread bookings more evenly across the year, reducing seasonality risk. They also value electric models for corporate social responsibility targets, nudging operators toward BEV procurement. Leisure-focused fleets may diversify into chauffeur-drive and curated-itinerary packages to defend market share against ride-hailing. Creating cross-selling opportunities between leisure and business pools helps raise overall utilization and yields.

By Vehicle Class: Budget Cars Anchor, SUVs Lead Upside

Economy and mini cars accounted for 48.72% of the Thailand car rental market size in 2025, reflecting price sensitivity among tourists and domestic travelers. Compact sedans offer a balance of comfort and affordability, yet SUVs and MPVs are on a 9.31% CAGR trajectory, driven by multi-generation family trips and road-trip tourism. Rental companies leverage higher daily rates on SUVs to offset steeper acquisition and fuel costs, while end-users appreciate ride height and cargo capacity on provincial highways.

Hybrid and plug-in versions of sought-after SUV models are attracting corporate renters who prioritize a reduced carbon footprint but are wary of range limitations. To navigate potential tax increases on larger ICE engines and tap into the premium market segment, operators are curating mixed fleets. This diversification not only supports dynamic yield management but also directs demand toward more profitable models during peak times.

By Propulsion: ICE Predominates, BEV Adoption Accelerates

ICE cars accounted for 87.15% of the Thailand car rental market size in 2025, underpinned by established fuel infrastructure and lower sticker prices. Fleet-wide BEV share is climbing at 12.36% CAGR through 2031, accelerated by tax cuts to 2% and subsidies up to THB 100,000 per unit under the EV3.5 program. Operators such as Sixt and Hertz now deploy Nissan LEAF and BYD ATTO 3 units at major airports to serve environmentally mindful travelers and corporate accounts.

However, charging access remains patchy, with only Bangkok, Phuket, and Chiang Mai offering widespread availability, hindering a nationwide shift to electrification. The Provincial Electricity Authority has set its sights on adding 1,000 new chargers at tourist hotspots, and EGAT is on track to match that number by 2030. Until the charging network becomes denser, fleets are leaning towards mixed propulsion systems, with hybrids playing a crucial role in balancing cost and range considerations.

By Rental Channel: Airports Retain Scale, Downtown Networks Rise

Airport counters captured 68.31% of Thailand's car rental market size in 2025 as Suvarnabhumi, Don Mueang, Phuket, and Chiang Mai absorbed the bulk of tourist flows. Planned capacity upgrades through 2031 underpin continued relevance, yet downtown and off-airport branches are growing at a 9.38% CAGR through 2031. City outlets tap domestic weekend travelers, corporate users, and residents seeking doorstep delivery, while also avoiding hefty airport concession fees that erode margins.

Collaborations with hotel chains like ONYX Hospitality seamlessly integrate rental bookings into room reservations, broadening the market reach beyond just airport arrivals. Operators are leveraging mobile handover teams and smart lock boxes to facilitate keyless pickups at condo lobbies and office towers. This widespread network not only enhances service delivery but also shields operators from abrupt declines in tourist numbers, a challenge highlighted by the 2025 downturn in Chinese tourist arrivals.

Geography Analysis

Bangkok remains the nucleus of the Thailand car rental market, hosting the largest concentration of fleets, counters, and maintenance depots. Suvarnabhumi and Don Mueang funnel international and domestic passengers into the capital’s dense downtown network, while corporate headquarters in Sathorn and Sukhumvit generate steady long-term lease demand. Peer-to-peer handovers and ride-hailing driver rentals flourish in the city thanks to high smartphone penetration and abundant charging stations for nascent BEV fleets.

Phuket and Chiang Mai rank next in rental density, each benefiting from strong leisure pull, international air connectivity, and growing expatriate communities. Seasonal peaks tied to the northeast monsoon require agile fleet rotation, and both provinces serve as early test beds for BEV offerings due to supportive local charging grids. However, their dependence on inbound tourism exposes revenue to macro shocks, underscoring the need for diversified domestic marketing campaigns.

Emerging clusters include U-Tapao-linked Pattaya, Rayong’s industrial corridor, and northern cities such as Chiang Rai and Khon Kaen. Low-cost carrier route launches spread rental demand across these secondary hubs, prompting operators to deploy modular counters and shared parking to curb fixed costs. Sparse charging infrastructure and uncertain flight load factors elevate operational risk, yet first movers can lock in airport concession space before rents escalate. Southern gateways Krabi, Hat Yai, and Surat Thani cater to island-hopping tourists and see spike-driven rental usage that rewards advanced yield-management algorithms.

Competitive Landscape

In Thailand's car rental market, a handful of players hold sway. Dominating airport concessions, Thai Rent A Car, Sixt, Avis Budget Group, Hertz, and Europcar capitalize on their substantial brand equity and global reservation platforms. Online aggregator growth has compressed pricing power, compelling incumbents to pursue alliances, such as Thai Rent A Car’s 2024 partnership with Enterprise Mobility, which integrates cross-border bookings and corporate fleet solutions.

Domestic mid-tier players, Bizcar Rental, Chic Car Rent, and Drive Car Rental, capitalize on local knowledge and nimble decision-making to pilot doorstep delivery and smartphone self-check-ins. The Bizcar-Drivemate merger forged a hybrid peer-to-peer plus owned-fleet model, signaling convergence between sharing platforms and conventional operations. Ride-hailing giant Grab inserts itself into the rental value chain by leasing EVs to drivers, eroding short-distance hire volumes and forcing traditional operators to refine propositions around multi-day leisure, premium SUVs, and corporate subscriptions.

Global developments reverberate locally. Avis Budget Group’s USD 518 million impairment on U.S. EV inventories in 2026 prompted a renewed focus on disciplined fleet sizing[3]"Avis Budget Group Reports Fourth Quarter and Full Year Results", Avis Budget Group, avisbudgetgroup.com, which may slow its BEV rollout in Thailand and open room for local specialists to seize early-adopter corporate accounts. Meanwhile, VinFast’s 2024 dealer network launch introduces new BEV supply channels that proactive rental companies can tap to diversify electric offerings alongside Chinese marques BYD and Great Wall.

Thailand Car Rental Industry Leaders

-

Sixt SE

-

Avis Budget Group

-

Thai Rent A Car

-

Europcar Mobility Group

-

Hertz Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- December 2025: Chic Car Rent received 50 Nissan Almera units from Nissan Thailand, underscoring Nissan's commitment to bolstering Thailand's car rental sector.

- April 2025: Sixt Car Rental Thailand unveiled its commitment to elevate its premium car rental offerings. The company officially integrated the tech-savvy, premium electric vehicle, Xpeng X9, sourced from Xpeng Thailand.

Thailand Car Rental Market Report Scope

A car rental service is a business that temporarily uses vehicles for individuals or companies for a specified period, usually ranging from a few hours to several days. Customers can rent a car for various purposes, such as travel, leisure, or business, paying a fee that typically covers the rental period and mileage.

The Thailand Car Rental market is segmented by booking type, rental duration, application, vehicle class, propulsion, and rental channel. By Booking Type, the market is segmented into Online and Offline. By Rental Duration, the market is segmented into Short-term and Long-term. By Application, the market is segmented into Leisure / Tourism and Commuting. By Vehicle Class, the market is segmented into Economy & Budget, Compact & Mid-size, SUV & MPV, and Luxury & Premium. By Propulsion, the market is segmented into Internal-Combustion Engine (ICE), Hybrid Electric Vehicle (HEV), and Battery Electric Vehicle (BEV). By Rental Channel, the market is segmented into Airport and Downtown.

Market forecasts are provided in terms of Value (USD).

By Booking Type

| Online |

| Offline |

By Rental Duration

| Short-term |

| Long-term |

By Application

| Leisure / Tourism |

| Commuting / Business |

By Vehicle Class

| Economy & Mini |

| Compact & Mid-size |

| SUV & MPV |

| Luxury & Premium |

By Propulsion

| Internal-Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) |

| Battery Electric Vehicle (BEV) |

By Rental Channel

| Airport |

| Downtown / Off-airport |

| By Booking Type | Online |

| Offline | |

| By Rental Duration | Short-term |

| Long-term | |

| By Application | Leisure / Tourism |

| Commuting / Business | |

| By Vehicle Class | Economy & Mini |

| Compact & Mid-size | |

| SUV & MPV | |

| Luxury & Premium | |

| By Propulsion | Internal-Combustion Engine (ICE) |

| Hybrid Electric Vehicle (HEV) | |

| Battery Electric Vehicle (BEV) | |

| By Rental Channel | Airport |

| Downtown / Off-airport |

Key Questions Answered in the Report

What is the current size of the Thailand car rental market?

The Thailand car rental market size is valued at USD 1.16 billion in 2026, on track to reach USD 1.77 billion by 2031.

Which booking channel is growing fastest in Thailand’s car rental sector?

Online platforms, ranging from peer-to-peer apps to metasearch engines, are expanding at a 9.28% CAGR through 2031, outpacing traditional counters.

How are government policies influencing fleet electrification?

Tax rebates cutting BEV excise rates and subsidies under the EV3.5 scheme are accelerating BEV adoption among rental operators.

Why are long-term corporate subscriptions gaining traction?

Companies favor predictable monthly fees, bundled maintenance, and the ability to scale fleets without heavy capital outlays.

Which vehicle class offers the highest growth potential?

SUVs and MPVs are forecasted to grow at about 9.31% CAGR as multi-generation family travel and road-trip tourism drive demand for larger, more versatile vehicles.

Page last updated on: