Terahertz Components And Systems Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

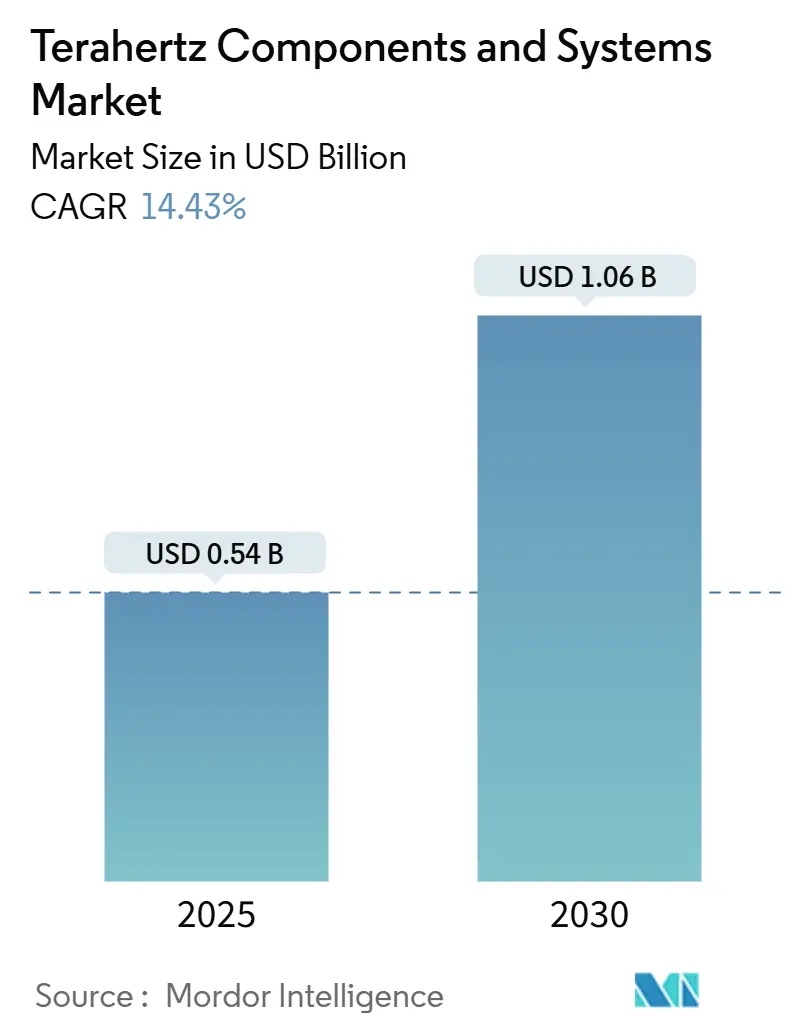

| Market Size (2025) | USD 0.54 Billion |

| Market Size (2030) | USD 1.06 Billion |

| Growth Rate (2025 - 2030) | 14.43% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Terahertz Components And Systems Market Analysis by Mordor Intelligence

The terahertz components and systems market size is USD 0.54 billion in 2025 and is forecast to reach USD 1.06 billion by 2030, translating into a robust 14.43% CAGR over the period. Solid demand stems from security screening deployments beyond airports, widening use in semiconductor non-destructive testing, and intensifying 6G research that validates use of sub-terahertz backhaul links. Room-temperature detector breakthroughs, quantum-cascade laser miniaturization, and spectrum liberalization across Asia-Pacific further accelerate adoption. Leading vendors emphasize vertical integration to control critical III-V compound supply chains, while buyers value smaller footprints, lower operating costs, and easy integration with factory automation systems. Inter-industry technology spillovers-from photonics, microwave, and semiconductor fields-sustain a continuous pipeline of performance enhancements that reinforce the long-term growth outlook.

Key Report Takeaways

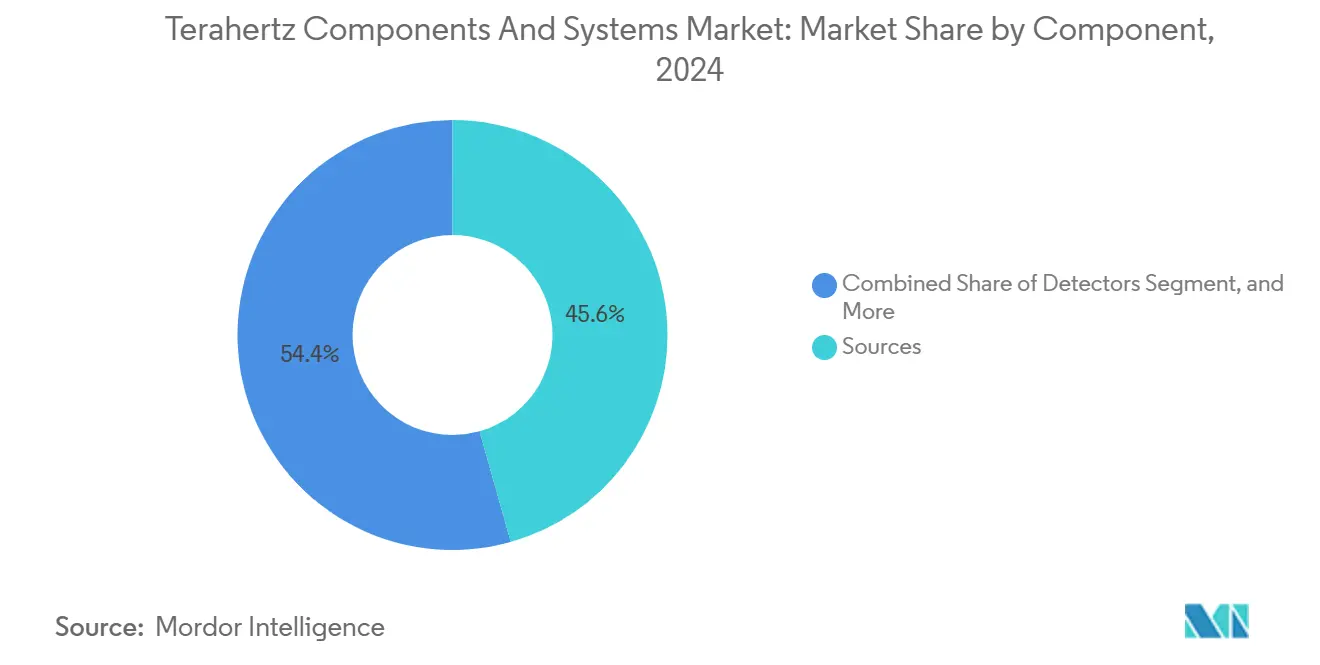

- By component, sources led with 45.63% of the terahertz components and systems market share in 2024; detectors are projected to expand at a 15.12% CAGR to 2030.

- By system type, imaging systems accounted for 53.83% of the terahertz components and systems market share in 2024, while communication systems record the highest projected CAGR at 15.34% through 2030.

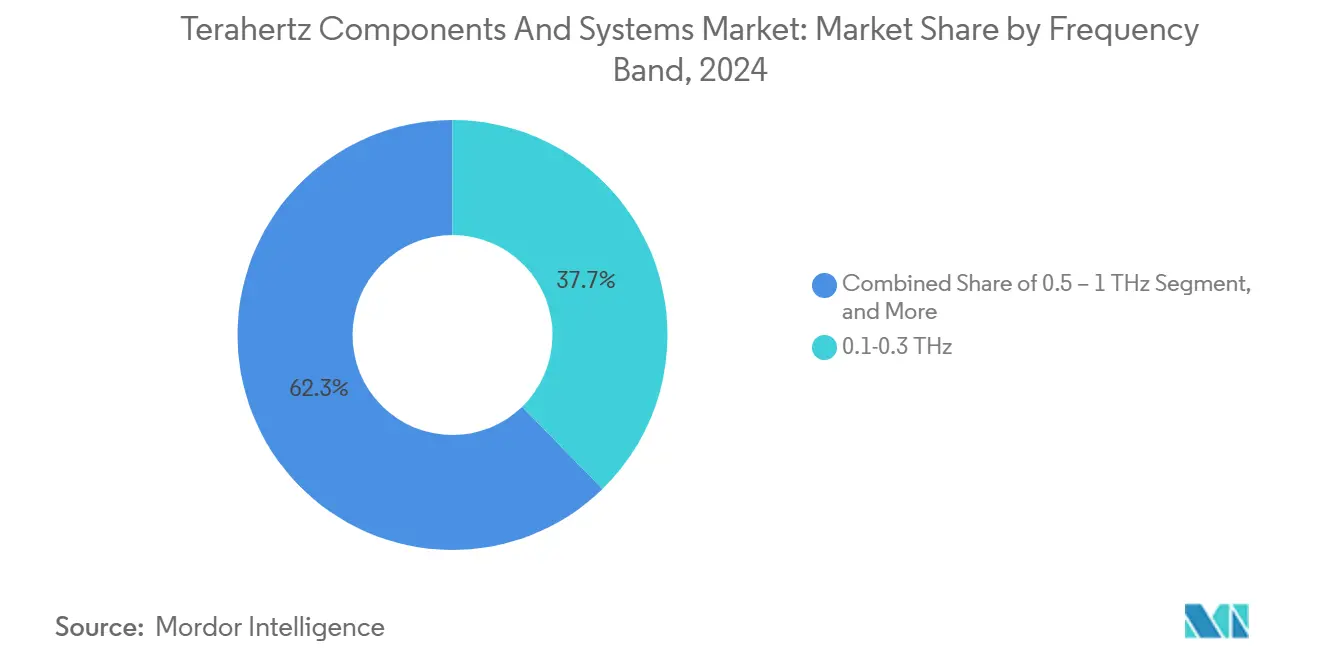

- By frequency band, the 0.1-0.3 THz range captured 37.72% of the terahertz components and systems market share in 2024; the 0.5-1 THz band is forecast to grow at 15.26% CAGR in the same horizon.

- By end-use industry, aerospace and security held 29.97% of the terahertz components and systems market share in 2024, whereas telecommunications is advancing at a 15.19% CAGR to 2030.

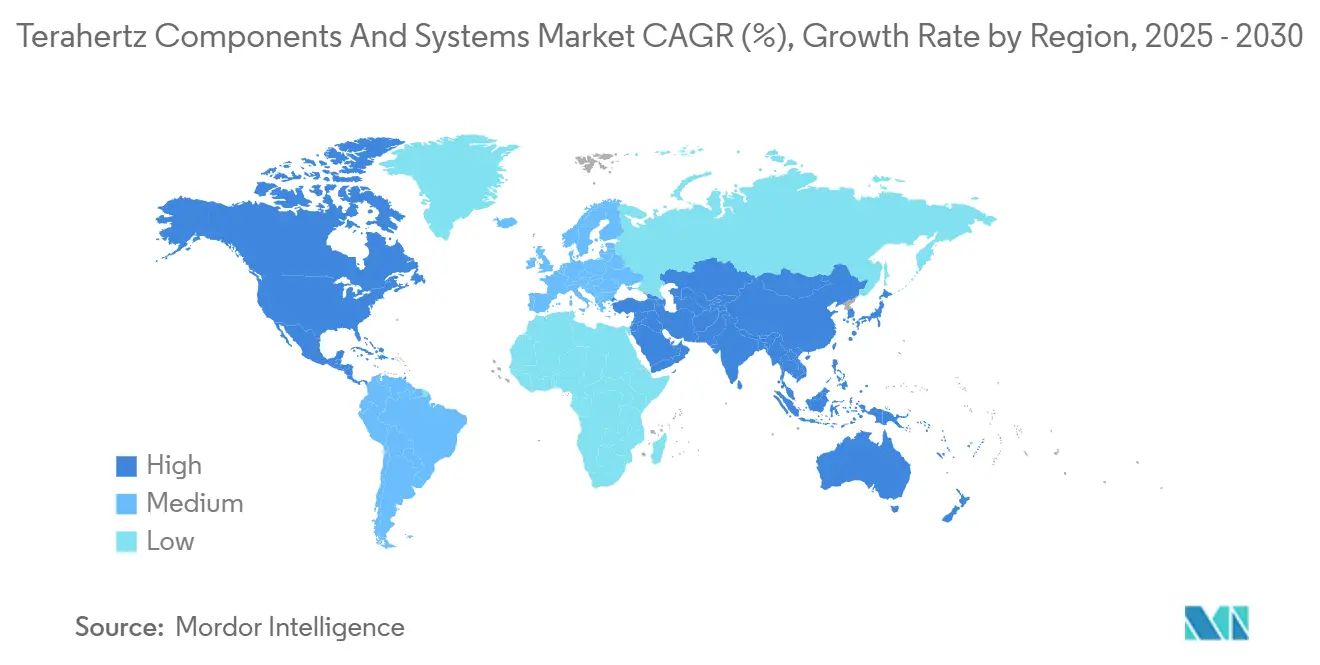

- By geography, North America commanded 34.53% of the terahertz components and systems market share in 2024, while Asia-Pacific is the fastest-growing region with a 14.96% CAGR through 2030.

Global Terahertz Components And Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Adoption in airport and border security | +2.5% | North America, Europe, Global rollout | Medium term (2–4 years) |

| Non-destructive semiconductor inspection | +2.8% | Asia-Pacific core, spillover to North America | Short term (≤2 years) |

| 6G sub-THz wireless backhaul R&D | +2.1% | Asia-Pacific, North America | Long term (≥4 years) |

| Miniaturization of quantum-cascade lasers | +1.9% | Europe, North America, Global manufacturing | Medium term (2–4 years) |

| 220-330 GHz spectrum liberalization | +1.4% | Asia-Pacific, global spillover | Short term (≤2 years) |

| Room-temperature detector breakthroughs | +1.2% | North America, Europe, Global R&D hubs | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Rising adoption in airport and border security screening

Transportation authorities expand terahertz imaging beyond metal detectors because the technology reliably identifies non-metallic threats at a distance while preserving passenger privacy. By 2024, the U.S. Transportation Security Administration will have deployed passive systems at more than 200 airports, and European border agencies will have outfitted major transit hubs with comparable solutions.[1]IEEE Staff, “Passive Terahertz Imaging for Security Applications,” IEEE Transactions on Terahertz Science and Technology, ieeexplore.ieee.org Funding momentum continues: the U.S. Department of Homeland Security directed USD 150 million toward next-generation screening, with terahertz platforms attracting roughly 30% of the allocation. Because terahertz waves are non-ionizing and can penetrate common clothing fabrics, adoption extends to critical-infrastructure perimeter protection and event-venue security. Vendor focus on modular, low-maintenance designs further accelerates procurement cycles, while global air-traffic recovery amplifies installation backlogs.

Expanding non-destructive inspection of semiconductor packages

Advanced packaging architectures-flip-chip, fan-out, and chiplet designs-create inspection challenges that terahertz imaging resolves by detecting voids, delamination, and wire-bond failures without damaging samples. Leading foundries in Taiwan and South Korea realized 40% higher defect-detection sensitivity versus legacy X-ray systems after integrating inline terahertz scanners. As 3D-stacked devices move into volume production, fab owners embed terahertz tools in automated material-handling lines, enabling near-real-time yield feedback. The direct link between high-value logic devices and time-to-market pressures ensures steady budget allocation despite macroeconomic fluctuations. Component vendors support the trend with turnkey modules calibrated for standard JEDEC-size packages, reinforcing scale efficiencies that lower the cost of ownership.

Accelerating R&D toward 6G sub-THz wireless backhaul

Telecom equipment makers target data rates above 1 Tbps for ultra-dense networks and see 140-320 GHz channels as practical short-haul links. Samsung and UC Santa Barbara achieved 6.2 Gbps over 15 m using a 140 GHz prototype in 2024. Meanwhile, Ericsson committed EUR 200 million to terahertz beamforming and atmospheric-compensation research, citing the need to relieve fiber-congestion bottlenecks. The International Telecommunication Union drafted preliminary 6G guidelines that reference sub-terahertz bands for backhaul, catalyzing multinational consortia. Field trials now run in Tokyo, Seoul, and Austin, measuring link performance under rain-fade and multipath conditions. Outcomes inform chipset roadmaps that, in turn, enlarge the addressable base for transceiver, antenna, and filter suppliers.

Mainstream miniaturization of quantum-cascade THz lasers

Compact quantum-cascade laser (QCL) modules surpassed the 10 mW power threshold at room temperature in 2024, with TOPTICA’s newest line shrinking footprint by 50%. Eliminating bulky cryogenic coolers slashes system weight and power draw, facilitating battery-powered handheld analyzers for pharmaceutical field audits and explosives detection. Manufacturing cost per QCL dropped 35% on average thanks to optimized epitaxial growth and wafer-bonding techniques. Ecosystem partners quickly adapted: enclosure makers offer hermetically sealed micro-optics mounts, and software vendors integrate driver electronics in plug-and-play boards. The convergence of portability, price decline, and stable output across wide frequency tuning ranges broadens use cases, from process monitoring on factory floors to museum conservation diagnostics.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of ultrafast photonic components | −1.8% | Global, particularly emerging markets | Medium term (2–4 years) |

| Limited penetration depth in water-rich media | −1.5% | Global, healthcare and food industries | Long term (≥4 years) |

| Lack of harmonized THz test standards | −1.2% | Global, regulatory fragmentation | Short term (≤2 years) |

| Integration complexity with legacy lines | −0.9% | North America, Europe | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

High cost of ultrafast photonic components

Time-domain spectroscopy platforms depend on femtosecond lasers and high-speed detectors that rely on scarce III-V substrates. Prices for indium phosphide climbed 25% in 2024, with 3-inch wafers selling for USD 800, squeezing vendor margins.[2]Shanghai Metals Market Analysts, “III-V Substrate Pricing 2024,” Shanghai Metal Market, metal.com A full terahertz TDS rig still lists between USD 150,000 and USD 300,000, exceeding capital-expenditure thresholds for many midsize enterprises. Supply-chain risk, exacerbated by geopolitical frictions, keeps inventory buffers high and economies of scale elusive. Although vertically integrated manufacturers invest in in-house crystal growth to secure feedstock, smaller players contend with volatile procurement cycles that hinder aggressive price cuts.

Limited penetration depth in water-rich materials

Terahertz absorption coefficients exceed 100 cm⁻¹ in tissues with high water content, restricting imaging depth to superficial layers.[3]Editorial Board, “Terahertz Imaging of Biological Tissues,” Nature Photonics, nature.com Consequently, medical diagnostics such as skin-cancer evaluation deliver only 1-2 mm penetration, curbing their comparative advantage against ultrasound or MRI. Industrial settings face analogous hurdles-high-humidity food-processing lines attenuate terahertz signals, limiting defect detection inside packaged products. Researchers explore lower-frequency operation and advanced signal-processing algorithms, yet underlying molecular-absorption physics caps achievable gains. The constraint dampens enthusiasm in life sciences investors, directing near-term funding toward less moisture-sensitive inspection domains.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Sources Drive Market Foundation

Sources generated 45.63% of revenue in 2024, underscoring their pivotal influence on overall system performance and cost. Quantum-cascade lasers register the fastest growth trajectory on the strength of room-temperature milestones that remove bulky cryogenic subsystems. Photomixer sources remain favored for broadband time-domain spectroscopy, whereas backward-wave oscillators oppose niche industrial-processing needs requiring high continuous-wave power. Detector demand accelerates at a 15.12% CAGR through 2030 as Schottky-diode and bolometer arrays unlock room-temperature responsivity levels once reserved for cooled devices. Waveguides and antennas benefit from 3D-printed silicon micromachining that yields 90% coupling efficiency across 220–330 GHz channels.

Growing volume shipments in the detectors and passive-component categories signal deeper market democratization, shifting the cost stack away from generation subsystems alone. Suppliers now bundle fully matched source-detector pairs calibrated for specific frequency windows, minimizing integration friction for system OEMs. Advanced filter and modulator designs incorporate metamaterial structures that compress physical footprints while sharpening spectral roll-off. The terahertz components and systems market sees parallel investment in automated alignment robotics and precision dicing to uphold sub-10 µm assembly tolerances. Sustained R&D in silicon photonics platforms seeks eventually to hybrid-integrate terahertz front ends with CMOS, promising step-change cost reductions once production matures.

By System Type: Communication Systems Accelerate Growth

Imaging solutions dominated revenue at 53.83% in 2024, buoyed by longstanding airport screening and industrial QA installations. They retain scale advantages thanks to progressive standardization and falling lens-array costs. Conversely, communication systems showcase the steepest 15.34% CAGR to 2030, reflecting operator trials of terabit-class backhaul for 6G cells. Pioneering demos, such as Samsung’s 6.2 Gbps sub-THz link, validate outdoor feasibility and trigger chipset roadmaps for 2027–2028 pilot rollouts. Spectroscopy instruments continue steady uptake in pharmaceutical polymorph detection and industrial polymer characterization, supported by easier-to-use software that demystifies spectral-feature interpretation.

The terahertz components and systems market aligns its engineering roadmaps with diverging system priorities: security buyers demand passive, wide-field imagers; telecom OEMs require beam-steered phased-arrays; lab spectroscopists want ultrabroad bandwidth over 0.1–3 THz. Component vendors, therefore, specialize in application-tuned form factors: vacuum-sealed camera cores, flip-chip-mounted up-converters for handset testbeds, and rack-mount spectroscopy engines that slot into existing FTIR benches. As communication prototypes near commercialization, economies of scale are expected to push per-gigahertz hardware costs down, indirectly benefiting imaging and spectroscopy buyers seeking greater affordability.

By Frequency Band: Mid-Range Spectrum Retains Lead

The 0.1–0.3 THz window supplied 37.72% of 2024 revenue, balancing manageable atmospheric absorption with relatively mature component availability. Regulatory clarity around D-band allocations enables early wireless backhaul pilots, while imaging and spectroscopy users appreciate lower attenuation through clothing and plastics. Market pull in higher-resolution use cases propels the 0.5–1 THz range to a 15.26% CAGR, aided by advances in photoconductive-switch drivers and lithography capable of sub-micron waveguide features. Pharmaceutical manufacturers favor frequencies above 0.5 THz for polymorph discrimination, and cultural-heritage researchers tap the window to differentiate layered pigments without destructive sampling.

Component designers counter higher-frequency fabrication challenges by adopting silicon micromachined waveguides and additive-manufactured horn antennas that sustain low loss beyond 750 GHz. Filters deploy multi-pole inductive-capacitive cavities etched via deep reactive-ion processes, keeping insertion loss below 0.5 dB. Alignment automation tightens to sub-5 µm tolerances, essential for maintaining signal integrity when wavelengths shrink. As measurement campaigns refine atmospheric-absorption models, network planners can better optimize link-budget calculations, emboldening telcos to book early component orders for 2028–2029 deployment phases.

By End-Use Industry: Telecommunications Emerges as Growth Leader

Aerospace and security users retained 29.97% of 2024 sales, as terahertz imaging reached full-production maturity in airport, border, and defense facilities. Nevertheless, telecommunications exhibits the fastest 15.19% CAGR amid global 6G initiatives seeking multi-gigabit backhaul in dense urban grids. Ericsson’s EUR 200 million commitment to terahertz R&D rallies suppliers to align product roadmaps with base-station volume timelines. Semiconductor fabs accelerate orders for inline terahertz inspection to catch sub-micron voids in system-in-package products, pushing industrial automation integrators to certify vibration-hardened scanner enclosures.

Healthcare and life-sciences activity remains exploratory; yet room-temperature detector progress enables portable instruments for tablet coating inspection and burn-depth assessment. Academic and research institutes sustain foundational physics inquiries, ensuring a pipeline of trained personnel for industry hiring. Industrial nondestructive-testing users-especially in aerospace composites-value terahertz’s ability to highlight moisture ingress and delamination where ultrasound sensitivity drops. End-use diversification stabilizes revenue flows, cushioning the terahertz components and systems market against budget swings in any single vertical.

Geography Analysis

North America held 34.53% of global revenue in 2024 on the strength of DHS and TSA procurement programs that integrated passive terahertz portals across major U.S. airports. Semiconductor manufacturers such as Intel and TSMC Arizona embed terahertz inline scanners to validate advanced-packaging output, broadening domestic demand. Canada’s National Research Council contributes world-class QCL and detector science, while Mexican contract manufacturers assemble waveguide sub-modules, leveraging USMCA trade provisions. The Federal Communications Commission’s conditional licensing in the 95 GHz–3 THz regime promotes early wireless link trials that feed component design iterations. Capital inflows from the U.S. CHIPS Act further anchor substrate and epitaxy investments that shorten domestic supply chains and enhance security posture.

Asia-Pacific is the fastest-growing region at a 14.96% CAGR through 2030, propelled by spectrum liberalization across 220–330 GHz ranges and ambitious 6G roadmaps in South Korea, Japan, and China. Samsung funnels sustained R&D into phased-array chipsets, while NTT pilots point-to-point links across dense Tokyo streetscapes. Chinese fabs in Jiangsu and Sichuan buy terahertz wafer-probe stations to accelerate yield ramp in 2.5D and 3D IC packaging. India’s nascent fab ecosystem eyes terahertz inspection for silicon photonics packaging, and Australia’s mining sector explores hand-held terahertz scanners to grade ore slurry moisture in real time. Regional cooperation bodies, such as ASEAN Digital Ministers, evaluate cross-border spectrum harmonization to simplify equipment certification.

Europe leverages a deep photonics supply chain to maintain technology leadership despite modest overall growth. Germany’s TOPTICA and Menlo Systems continue to pioneer compact QCL and fiber-coupled TDS modules, while France’s ONERA tests terahertz sensors for composite wing inspection. The European Telecommunications Standards Institute orchestrates common test protocols, expediting multi-country pilot deployments. Horizon Europe grants allocate over EUR 50 million for terahertz research, uniting universities and SMEs. The United Kingdom advances polarization-sensitive terahertz imaging for counter-UAV systems, and Italy’s fashion industry trials terahertz scanners to authenticate luxury fabrics. Eastern European contract manufacturers compete on cost for passive-component machining, bolstering regional cost competitiveness.

Competitive Landscape

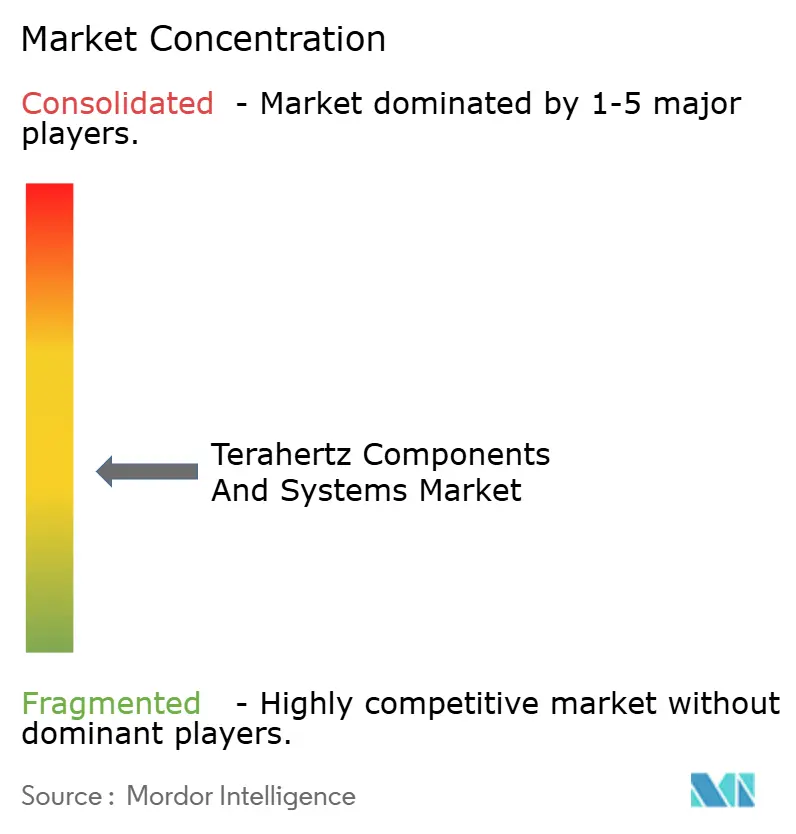

The terahertz components and systems market displays moderate fragmentation. The top five vendors account for roughly 45% of global revenue thanks to long-term patent portfolios, specialized clean-room assets, and multi-sector reference projects. TeraView excels in turnkey imaging systems and recently partnered with Sanyo Trading to localize support in Japan. TOPTICA’s QCL product line expansion raises entry barriers in power-density benchmarks. Virginia Diodes dominates in Schottky-diode mixers and frequency multipliers and secured a USD 5 million U.S. DoD contract in 2024 for sub-millimeter-wave component R&D.

Emerging challengers attract venture financing by exploiting white-space niches. Tihive’s USD 9.7 million Series A funds automated inline scanners for automotive composite parts, while Israeli start-ups harness metamaterial antennas that collapse array thickness to a few millimeters. Apple’s 2024 spectroscopy patent hints at future smartphone integration, signaling potential consumer-scale volumes that could reorder supply-chain economics. Strategic playbooks converge on three differentiation pillars: room-temperature operation, miniaturization conducive to handheld form factors, and cost-optimized manufacturing pipelines underpinned by silicon-compatible processes. Cross-licensing trends emerge as incumbents seek access to novel material stacks and device architectures perfected by smaller innovators, reinforcing a collaborative yet competitive ecosystem.

Terahertz Components And Systems Industry Leaders

TeraView Limited

HÜBNER GmbH & Co. KG

TOPTICA Photonics AG

Menlo Systems GmbH

Virginia Diodes, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: TeraView formed a distribution alliance with Sanyo Trading to drive terahertz sales in Japan’s pharma and semiconductor sectors, targeting USD 20 million incremental revenue over three years.

- March 2025: Coherent won USD 33 million CHIPS Act funding to enlarge 150 mm indium phosphide substrate output, mitigating U.S. reliance on Asian suppliers.

- February 2025: Tihive raised EUR 8.6 million (USD 9.7 million) to scale automated terahertz quality-control systems for aerospace and automotive manufacturing.

- January 2025: Samsung validated 6.2 Gbps data throughput over 15 m at 140 GHz, reinforcing commercial timelines for 6G backhaul deployments.

Global Terahertz Components And Systems Market Report Scope

| Sources (Photomixers, Quantum-cascade lasers, etc.) |

| Detectors (Schottky diode, Bolometer, etc.) |

| Waveguides and Antennas |

| Other Component |

| Imaging Systems |

| Spectroscopy Systems |

| Communication Systems |

| Other System Type |

| 0.1 – 0.3 THz (D-band) |

| 0.3 – 0.5 THz |

| 0.5 – 1 THz |

| greater than 1 THz |

| Aerospace and Security |

| Semiconductor and Electronics |

| Healthcare and Life Sciences |

| Academic and Research |

| Industrial NDT and Process Control |

| Telecommunications |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | Saudi Arabia |

| United Arab Emirates | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Component | Sources (Photomixers, Quantum-cascade lasers, etc.) | ||

| Detectors (Schottky diode, Bolometer, etc.) | |||

| Waveguides and Antennas | |||

| Other Component | |||

| By System Type | Imaging Systems | ||

| Spectroscopy Systems | |||

| Communication Systems | |||

| Other System Type | |||

| By Frequency Band | 0.1 – 0.3 THz (D-band) | ||

| 0.3 – 0.5 THz | |||

| 0.5 – 1 THz | |||

| greater than 1 THz | |||

| By End-Use Industry | Aerospace and Security | ||

| Semiconductor and Electronics | |||

| Healthcare and Life Sciences | |||

| Academic and Research | |||

| Industrial NDT and Process Control | |||

| Telecommunications | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| Japan | |||

| India | |||

| South Korea | |||

| Australia | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | Saudi Arabia | |

| United Arab Emirates | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current value of the terahertz components market?

It stands at USD 0.54 billion in 2025 and is projected to double to USD 1.06 billion by 2030.

Which segment is growing fastest within terahertz components?

Communication systems post the quickest expansion, clocking a 15.34% CAGR driven by 6G backhaul trials.

Why are terahertz components relevant to semiconductor manufacturing?

They enable non-destructive inspection of advanced packages, detecting voids and delamination that X-ray tools can miss, improving yield and reducing scrap.

Which region leads in market share today?

North America tops with 34.53% share, powered by DHS and TSA security deployments and domestic semiconductor investment.

What technological breakthrough is lowering system cost?

Room-temperature quantum-cascade lasers have removed the need for cryogenic cooling, shrinking size and trimming bill of material outlays by roughly 35%.

What limits terahertz use in medical imaging?

Strong absorption in water-rich tissues caps penetration depth to a few millimeters, diminishing effectiveness for deep-tissue diagnostics.

Page last updated on: