Telerehabilitation Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

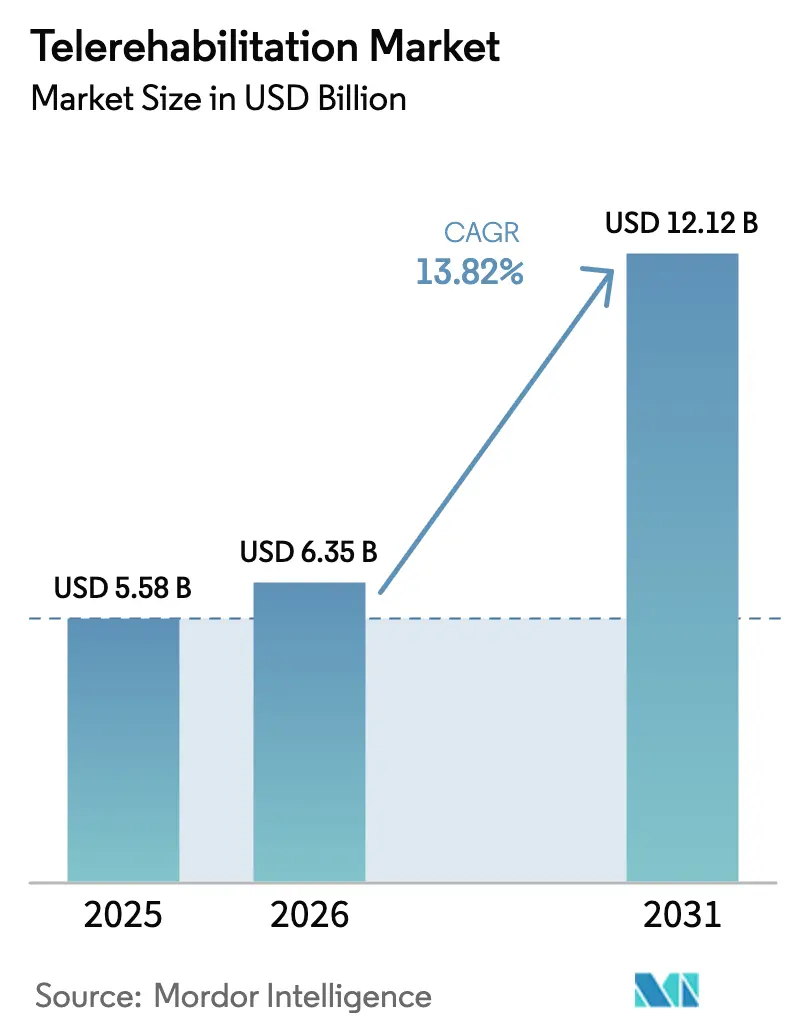

| Market Size (2026) | USD 6.35 Billion |

| Market Size (2031) | USD 12.12 Billion |

| Growth Rate (2026 - 2031) | 13.82% CAGR |

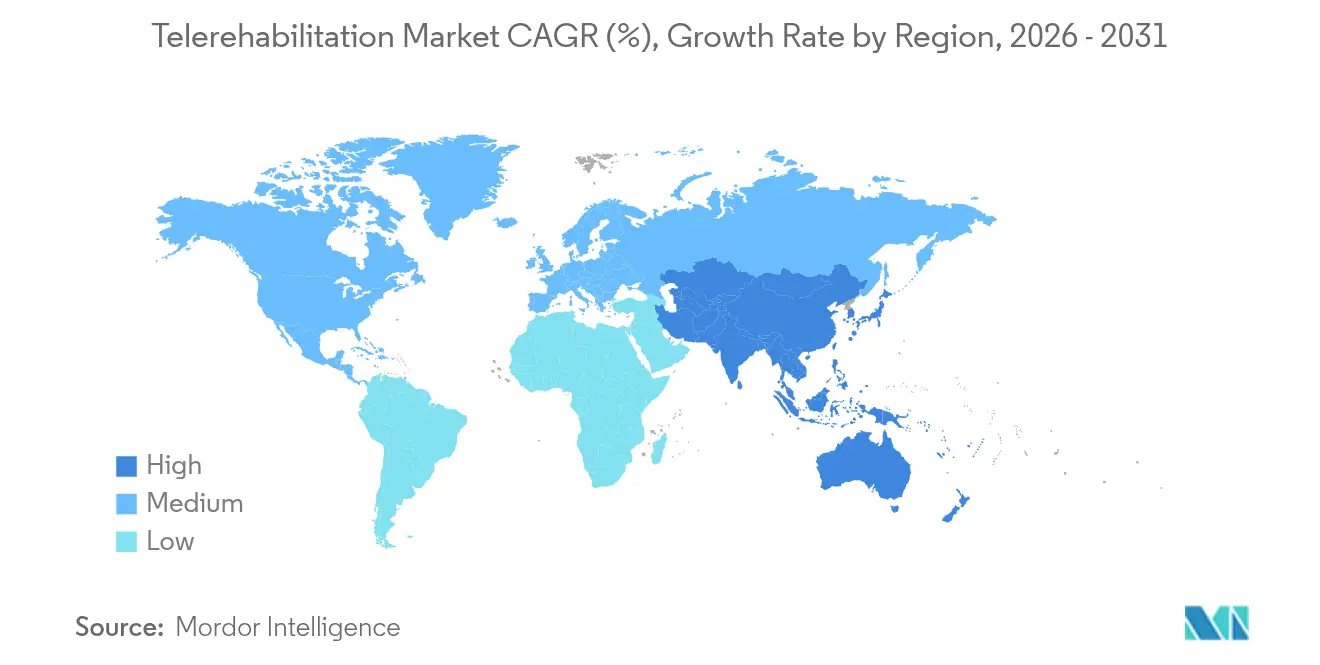

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

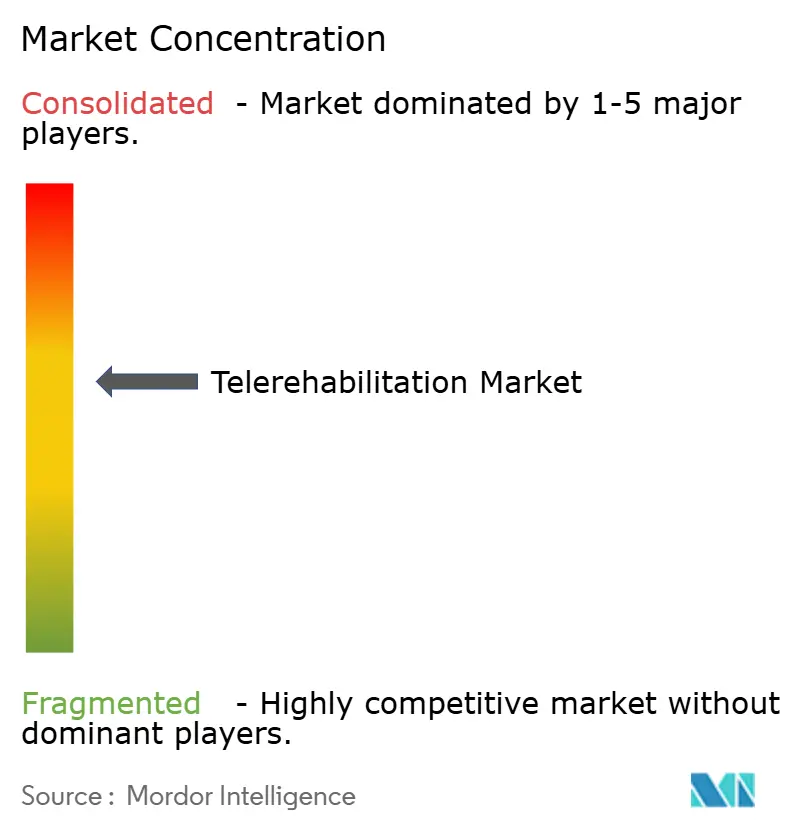

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Telerehabilitation Market Analysis by Mordor Intelligence

Telerehabilitation market size in 2026 is estimated at USD 6.35 billion, growing from 2025 value of USD 5.58 billion with 2031 projections showing USD 12.12 billion, growing at 13.82% CAGR over 2026-2031. Sustained regulatory support, rapid AI-driven platform enhancements, and a lasting shift toward decentralized care anchor this growth. Expanded Medicare telehealth flexibilities, Germany’s DiGA reimbursement model, and rising cardio-pulmonary recovery volumes collectively strengthen demand. Cloud deployment continues to outpace on-premise models, sensor fusion sharpens clinical accuracy, and real-time data integration moves telerehabilitation from reactive therapy to predictive intervention. Strategic acquisitions and IPO pipelines signal investor confidence while competitive intensity pushes vendors to bundle physical, cardiometabolic, and behavioral programs into unified virtual care suites.

Key Report Takeaways

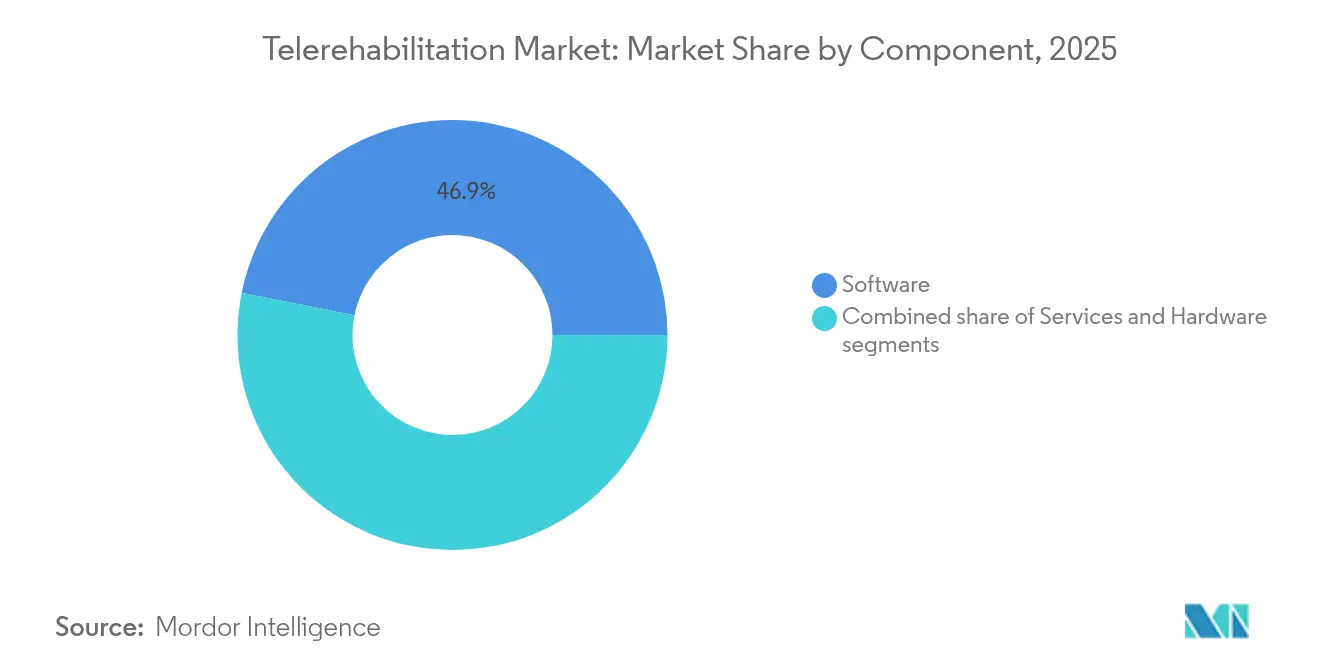

- By component, software held 46.85% revenue share in 2025, while services are projected to deliver the fastest 16.27% CAGR to 2031.

- By mode of delivery, cloud-based platforms led with 67.90% revenue and are poised to expand at a 16.68% CAGR through 2031.

- By application, cardiac rehabilitation led with 33.75% revenue share in 2025; respiratory rehabilitation is set to grow at a 17.19% CAGR to 2031.

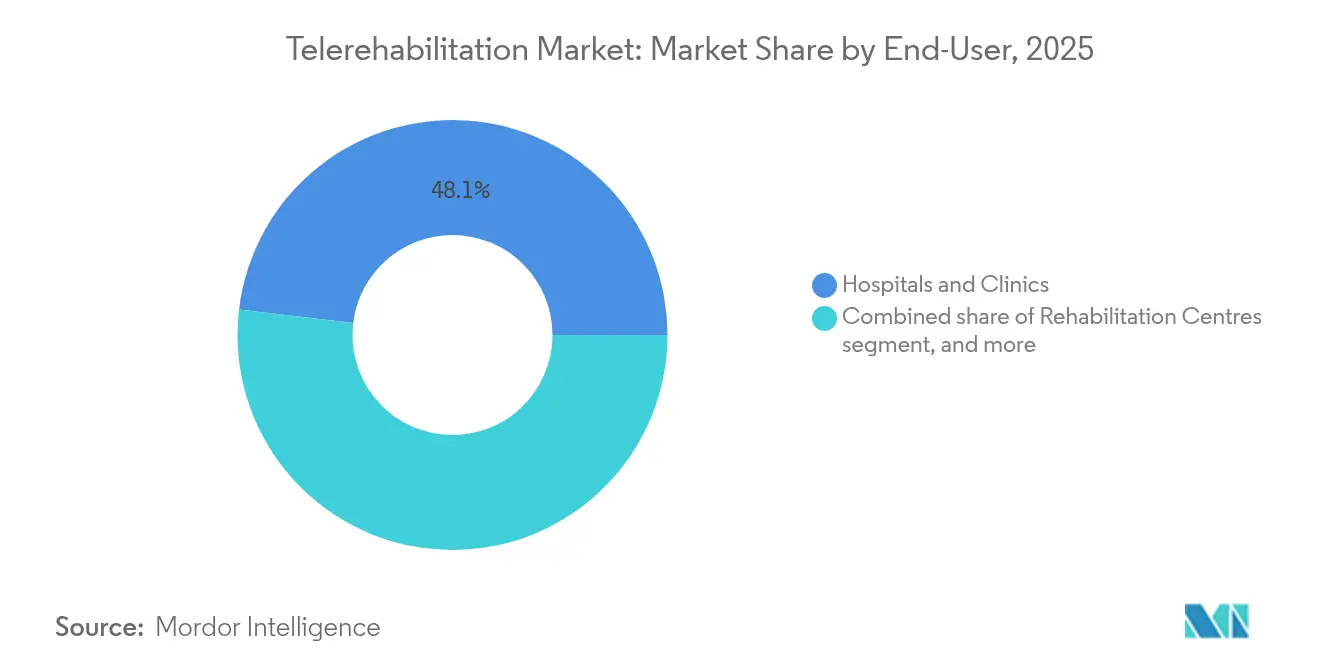

- By end-user, hospitals and clinics controlled 48.10% of spending in 2025, whereas home-care settings will advance at a 17.46% CAGR.

- By technology, sensor-based frameworks produced 37.10% of 2025 revenue, However, image-based telerehabilitation is forecast to climb at 15.96% CAGR.

- By geography, North America contributed 41.95% of 2025 revenue, yet Asia-Pacific is projected to record a 15.52% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Telerehabilitation Market Trends and Insights

Driver Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Growing Prevalence Of Chronic Diseases And Aging Population | +3.2% | Global, highest in APAC and North America | Long term (≥ 4 years) |

| Convenience And Cost Savings Of Remote Rehabilitation | +2.8% | Global, particularly rural and underserved areas | Medium term (2-4 years) |

| Continuous Technological Advancements In Telehealth Platforms | +2.5% | North America and Europe, expanding to APAC | Medium term (2-4 years) |

| Favorable Reimbursement And Policy Support For Digital Care | +2.1% | North America and Europe, emerging in APAC | Short term (≤ 2 years) |

| Rising Healthcare Provider Adoption Of Remote Patient Monitoring | +1.8% | Global, led by North America and Europe | Medium term (2-4 years) |

| Increasing Demand For Home-Based Care Amid Workforce Shortages | +1.6% | Global, more acute in developed markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Growing Prevalence Of Chronic Diseases And Aging Population

By 2030, adults aged 65+ will account for 22% of the global population, and 80% will manage multiple chronic conditions requiring long-term rehabilitation[1]World Health Organization, “World Population Ageing 2024 Highlights,” who.int. Stroke affects 15 million people every year, leaving 5 million with lasting disability that centers struggle to accommodate. Meta-analyses show virtual reality–enabled stroke programs match in-clinic gains while sustaining adherence above 90%. With chronic-care spending nearing USD 4 trillion, payers view scalable telerehabilitation as a cost-containment lever that protects functional status and curbs readmissions. These demographic and economic pressures make the telerehabilitation market central to future rehabilitation capacity planning.

Continuous Technological Advancements In Telehealth Platforms

Artificial intelligence now personalizes exercise progression, flags non-adherence, and predicts outcomes with 85% accuracy[2]Nature Digital Medicine, “Predictive models in telerehab,” nature.com. Conversational guidance tools, such as SWORD Health’s Phoenix AI, halve surgery rates and deliver a 3.2x return, demonstrating hard-dollar impact validated in more than 3 million sessions (company data). Markerless computer-vision engines power image-based motion capture through a standard camera, eliminating wearables while returning lab-grade kinematic data. Virtual reality immersion reduces chronic back-pain scores by 68% in controlled trials. These advances transform static video calls into continuous, data-rich rehabilitation ecosystems that adapt in real time to patient performance.

Favorable Reimbursement And Policy Support For Digital Care

The CY 2025 Physician Fee Schedule preserves telehealth flexibilities for Rural Health Centers and adds CPT codes for virtual caregiver training, solidifying a short-term reimbursement tailwind. Germany’s DiGA pathway has cleared 56 apps and generated more than 200,000 prescriptions annually, proving that fast-track reimbursement can accelerate adoption. In the United States, the FDA Digital Health Advisory Committee and Pre-Cert pilots aim to streamline approvals for evidence-backed digital therapeutics. These policy moves lower entry barriers, define quality guardrails, and give providers confidence to mainstream remote rehabilitation services.

Rising Healthcare Provider Adoption Of Remote Patient Monitoring

Eighty-four percent of rehabilitation physicians now use telehealth for follow-up care, reflecting a permanent shift in clinical workflows. Large systems such as Mass General Brigham integrate hospital telemetry, at-home sensors, and telerehabilitation sessions on a single cloud platform to cover 49 facilities (company data). New Remote Therapeutic Monitoring codes reimburse analysis of motion, respiration, and heart-rate data, embedding a durable revenue stream. Cardiac telerehabilitation programs consistently match the exercise-capacity gains of center-based therapy, regardless of age profile. This convergence of billing, workflow, and evidence cements remote programs as a workforce extender amid global clinician shortages.

Restraints Impact Analysis*

| Restraints Impact Analysis | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Digital Divide And Limited Broadband Penetration | –1.8% | Global, especially rural and developing regions | Long term (≥ 4 years) |

| Data Privacy, Security, And Compliance Risks | –1.2% | Global, stricter in Europe and North America | Medium term (2-4 years) |

| Variable Clinical Evidence And Lack Of Standardized Protocols | –0.9% | Global, with greater effect in emerging markets | Medium term (2-4 years) |

| Regulatory And Licensing Barriers Across Jurisdictions | –0.7% | Cross-border implementations, notably in APAC and Europe | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Digital Divide And Limited Broadband Penetration

Rural broadband adoption remains 10-15% lower than urban levels, and 21% of seniors still lack reliable internet for video-based therapy. Forty percent of older adults need hands-on technical support before independent platform use. Nigerian physiotherapists lifted telerehabilitation adoption from 18.7% pre-pandemic to only 34.4% during lockdowns, demonstrating persistent infrastructure barriers. Audio-only visits help, yet visual analysis is essential for gait and range-of-motion assessment. Closing connectivity gaps through 5G rollout and simple user interfaces is vital for equitable market expansion.

Data Privacy, Security, And Compliance Risks

Health-data breaches exposed 45 million U.S. records in 2024, making telehealth platforms prized targets. GDPR and HIPAA mandates raise development costs and slow multinational rollouts, while data-transfer restrictions complicate cloud deployments. Integration problems between telerehabilitation platforms and electronic health records create silos that hinder decision-making. Vendors must embed end-to-end encryption, role-based access, and audit trails to reassure providers and regulators, but these investments lengthen commercialization timelines and dampen early-stage margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Software Drives Innovation While Services Accelerate Growth

Software captured 46.85% of telerehabilitation market share in 2025 on the strength of AI engines, biometric analytics, and immersive content libraries. Platform vendors continually release feature upgrades that enhance precision and patient engagement without new hardware. As installations proliferate, services revenue is scaling even faster. Clinicians, health coaches, and technical specialists deliver remote supervision, device onboarding, and outcomes reporting, activities expected to climb at a 16.27% CAGR to 2031. Hospitals outsource these tasks to keep staff focused on complex cases, driving steady service uptake.

Service acceleration signals a pivot from pure-play software toward hybrid care models that align technology with human judgement. Employers frequently contract white-label offerings that combine cloud algorithms and coaching calls in one subscription. Hardware remains essential for select use cases such as force-plate gait analysis or neuromuscular stimulation, yet commodity sensors and computer vision shrink capital needs. This blended architecture reduces upfront spending while spreading recurring revenue across software licenses and clinical services, reinforcing sustained growth of the telerehabilitation market.

By Mode of Delivery: Cloud-Based Dominance Accelerates Through Scalability Advantages

Cloud platforms accounted for 67.90% of 2025 revenue and will keep expanding at 16.68% CAGR as providers seek rapid deployment without major IT upgrades. Subscription models convert capital expenditure into predictable operating outlays, a critical advantage for cash-constrained community hospitals. Automatic security patches and real-time analytics elevate compliance and performance levels beyond what most local data centers can maintain. As a result, several large systems committed to sunset on-premise instances within the planning cycle.

A minority of institutions still rely on on-premise solutions for ultra-high-security workflows, but hybrid strategies allow sensitive data to stay local while leveraging cloud algorithms for processing. Regulatory assurances such as extended Medicare telehealth coverage and EU Health Data Space rules further lower perceived risk. These dynamics ensure that the telerehabilitation market size tied to cloud deployment will continue to rise faster than any other delivery mode through 2031.

By Application: Cardiac Leadership Faces Respiratory Rehabilitation Surge

Cardiac programs retained a 33.75% revenue share in 2025, solidified by strong evidence, standardized protocols, and bundled reimbursement. Virtual cardiac rehab improves exercise tolerance and cuts readmissions, making it indispensable for value-based care contracts. Even so, respiratory telerehabilitation is projected to advance at 17.19% CAGR as long-COVID cases and COPD prevalence climb. Remote pulmonary coaching, pulse-oximetry monitoring, and breathing-exercise apps are drawing fresh payer attention as they reduce emergency visits and improve dyspnea.

Orthopedic and neurological pathways also gain momentum through AI-based gait analysis and VR stroke modules. A notable reference point is Mayo Clinic’s home-based COPD rehabilitation service, which combines phone coaching with wearables to lift quality-of-life scores and walking distance. This multi-clinical traction broadens addressable populations, reinforcing demand across every major segment of the telerehabilitation market.

By End-User: Hospital Dominance Challenged by Home-Care Acceleration

Hospitals and clinics held 48.10% of 2025 spending, using telerehabilitation to protect length-of-stay metrics and expand outpatient volumes. Yet home-care settings will outpace every other channel at a 17.46% CAGR through 2031. Patients prefer convenient sessions, caregivers appreciate reduced travel, and payers observe lower total spend. Large employers and pay-viders now contract directly with virtual therapy networks to keep musculoskeletal claims in check.

Rehabilitation centers still offer specialized expertise, but many license cloud platforms to serve post-discharge patients remotely. Partnerships such as Teladoc Health’s integration with Amazon’s Benefits Connector show how consumer platforms can funnel millions of members into structured cardiometabolic programs (company data). This decentralization positions the telerehabilitation market to align with broader home-health and hospital-at-home initiatives.

By Technology: Sensor-Based Leadership Faces Image-Based Innovation Pressure

Sensor-based frameworks produced 37.10% of 2025 revenue, leveraging wearables, IMUs, and pressure mats for objective measurement. However, image-based telerehabilitation is forecast to climb at 15.96% CAGR as AI computer vision achieves sub-degree accuracy from a laptop camera. Eliminating hardware lowers barrier to entry for patients and enables unlimited scale for providers. Vendors now blend sensors and camera analytics for redundancy, enhancing clinical confidence.

Robotics, VR/AR, and stimulation devices deepen therapeutic intensity for complex cases. For example, markerless motion capture added to open-platform software expanded the telerehabilitation market size for post-orthopedic surgery care by cutting per-patient device costs 45%. Emerging multi-modal systems that fuse vision, EMG, and force data promise even higher predictive power, keeping innovation cycles brisk.

Geography Analysis

North America generated 41.95% of global revenue in 2025 thanks to Medicare policy continuity, FDA guidance, and a dense network of digital-health investors. The region’s providers rapidly embed telerehabilitation inside integrated delivery networks, and multisite health systems now include virtual rehab metrics on enterprise scorecards. U.S. employers also drive volumes by offering no-cost remote therapy under self-insured plans, creating parallel demand beyond traditional provider settings.

Europe records steady adoption under a patchwork of national frameworks. Germany’s DiGA pathway, France’s LPPR reforms, and the United Kingdom’s NICE digital-health guidelines each enhance coverage visibility, while the forthcoming EU Health Data Space promises smoother cross-border data exchange. Nordic countries pilot 5G-enabled rural telerehabilitation pods, and Italy funds home-based COPD programs through regional health authorities. Collectively, these efforts expand the telerehabilitation market while preserving the continent’s stringent privacy standards.

Asia-Pacific is the fastest-growing territory with a 15.52% CAGR projected to 2031. Governments in China, Japan, and Australia earmark stimulus funds for remote care infrastructure to manage aging populations and workforce shortfalls. Indonesia’s collaboration between Philips and Siloam Hospitals showcases public-private models that bypass brick-and-mortar shortages. Mobile-first platforms meet diverse linguistic and cultural needs, accelerating adoption among middle-income populations. This momentum positions the region to materially narrow the telerehabilitation market share gap with North America before the end of the decade.

Competitive Landscape

The telerehabilitation industry features moderate consolidation as incumbents pursue scale and data breadth. The five largest vendors together hold roughly 55% of global revenue, leaving room for niche specialists. Teladoc Health widened its moat by acquiring Catapult Health in February 2025 for USD 65 million, adding preventive screenings that feed new rehabilitation referrals (company press release). Earlier, the firm bought UpLift Health Technologies for USD 30 million to bolster behavioral health, rounding out a whole-person portfolio.

Digital-first players focus on measurable outcomes. SWORD Health cited 3.2x customer ROI and 50% surgery avoidance when it secured USD 130 million in Series D capital in June 2024 (company statement). Hinge Health’s SEC filing for its pending IPO showed Q1 2025 revenue at USD 123.8 million, up 50% year over year. Such metrics attract payers seeking actuarial proof that virtual therapy lowers total episode costs.

Technology partnerships also shape competition. Medbridge’s purchase of Rehab Boost inserted markerless motion capture into its learning-management backbone, while Philips collaborates with Mass General Brigham on AI-driven cardiac event prediction. These moves tighten integration points and raise switching costs. Looking ahead, white-space opportunities lie in respiratory and oncology rehabilitation, where few vendors offer dedicated protocols, and in emerging markets that leapfrog straight to mobile-first solutions.

Telerehabilitation Industry Leaders

American Well

Koninklijke Philips N.V.

Tunstall Group

Teladoc Health, Inc.

Hinge Health, Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- April 2025: Teladoc Health acquired UpLift Health Technologies for USD 30 million to enhance virtual mental health services, demonstrating strategic expansion beyond physical rehabilitation into comprehensive behavioral health solutions Quiver Quantitative.

- March 2025: Hinge Health filed for initial public offering with the SEC, reporting 33% revenue growth to USD 390 million in 2024 and serving over 532,000 members across 2,250 organizations, marking a significant milestone in telerehabilitation market maturation CNBC.

- February 2025: Teladoc Health announced acquisition of Catapult Health for USD 65 million to enhance preventive care capabilities through at-home wellness exams and early health-condition detection, expanding beyond traditional telerehabilitation into comprehensive health management CNBC.

- January 2025: Teladoc Health partnered with Amazon to integrate cardiometabolic programs into Amazon's Health Benefits Connector, providing streamlined enrollment for diabetes, hypertension, and weight-management services for over 1 million active participants Teladoc Health.

- 2025: Avel eCare acquired Amwell Psychiatric Care to expand behavioral health services to 46 states, addressing increasing mental-health-care demand through integrated telemedicine solutions Fierce Healthcare.

Global Telerehabilitation Market Report Scope

As per the scope of the report, telerehabilitation tools refer to a range of technological solutions and tools designed to provide remote rehabilitation services and support to individuals recovering from injuries, surgeries, or medical conditions. The telerehabilitation market is segmented into components, mode of delivery, application, and geography. By component, the market is segmented into software and services and hardware. By mode of delivery, the market is segmented into cloud-based and on-premise. By application, the market is segmented into cardiac rehabilitation, neurological rehabilitation, physiotherapy rehabilitation (orthopedic), cancer, and other applications. The other segments include pediatric rehabilitation and others. By geography, the market is segmented into North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. For each segment, the market sizing and forecasts were made based on value (USD).

| Software |

| Services |

| Hardware |

| Cloud-Based |

| On-Premise |

| Hybrid |

| Cardiac Rehabilitation |

| Neurological Rehabilitation |

| Physiotherapy / Orthopaedic |

| Respiratory Rehabilitation |

| Other Applications |

| Hospitals & Clinics |

| Rehabilitation Centres |

| Home-Care Settings |

| Payers & Self-Insured Employers |

| Image-Based Telerehabilitation |

| Sensor-Based Telerehabilitation |

| VR/AR-Based Platforms |

| Robotics-Assisted Systems |

| AI-Enabled Motion-Capture Platforms |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| Japan | |

| India | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East & Africa | GCC |

| South Africa | |

| Rest of Middle East & Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Component | Software | |

| Services | ||

| Hardware | ||

| By Mode of Delivery | Cloud-Based | |

| On-Premise | ||

| Hybrid | ||

| By Application | Cardiac Rehabilitation | |

| Neurological Rehabilitation | ||

| Physiotherapy / Orthopaedic | ||

| Respiratory Rehabilitation | ||

| Other Applications | ||

| By End-User | Hospitals & Clinics | |

| Rehabilitation Centres | ||

| Home-Care Settings | ||

| Payers & Self-Insured Employers | ||

| By Technology | Image-Based Telerehabilitation | |

| Sensor-Based Telerehabilitation | ||

| VR/AR-Based Platforms | ||

| Robotics-Assisted Systems | ||

| AI-Enabled Motion-Capture Platforms | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| Japan | ||

| India | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | GCC | |

| South Africa | ||

| Rest of Middle East & Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the telerehabilitation market and its growth outlook?

The telerehabilitation market stood at USD 6.35 billion in 2026 and is projected to reach USD 12.12 billion by 2031, growing at a 13.82% CAGR.

Which delivery model is expanding the fastest?

Cloud-based deployment leads with 67.90% revenue share in 2025 and is forecast to advance at a 16.68% CAGR because providers favor scalable, low-maintenance solutions.

Why is respiratory telerehabilitation considered a high-growth segment?

Long-COVID recovery needs and rising COPD prevalence push respiratory programs to a 17.19% CAGR, outpacing traditional cardiac and orthopedic pathways.

How are reimbursement policies influencing adoption?

Extended Medicare telehealth flexibilities, new CPT codes, and Germany’s DiGA fast-track pathway provide stable payment mechanisms that encourage providers to integrate remote rehabilitation.

What are the main barriers to wider telerehabilitation uptake?

Uneven broadband access and heightened cybersecurity requirements limit deployment in rural areas and add compliance costs for vendors.

Which regions present the greatest future opportunity?

Asia-Pacific is projected to post a 15.52% CAGR as aging demographics, chronic disease burden, and government digital-health initiatives converge to accelerate demand.

Page last updated on: