Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

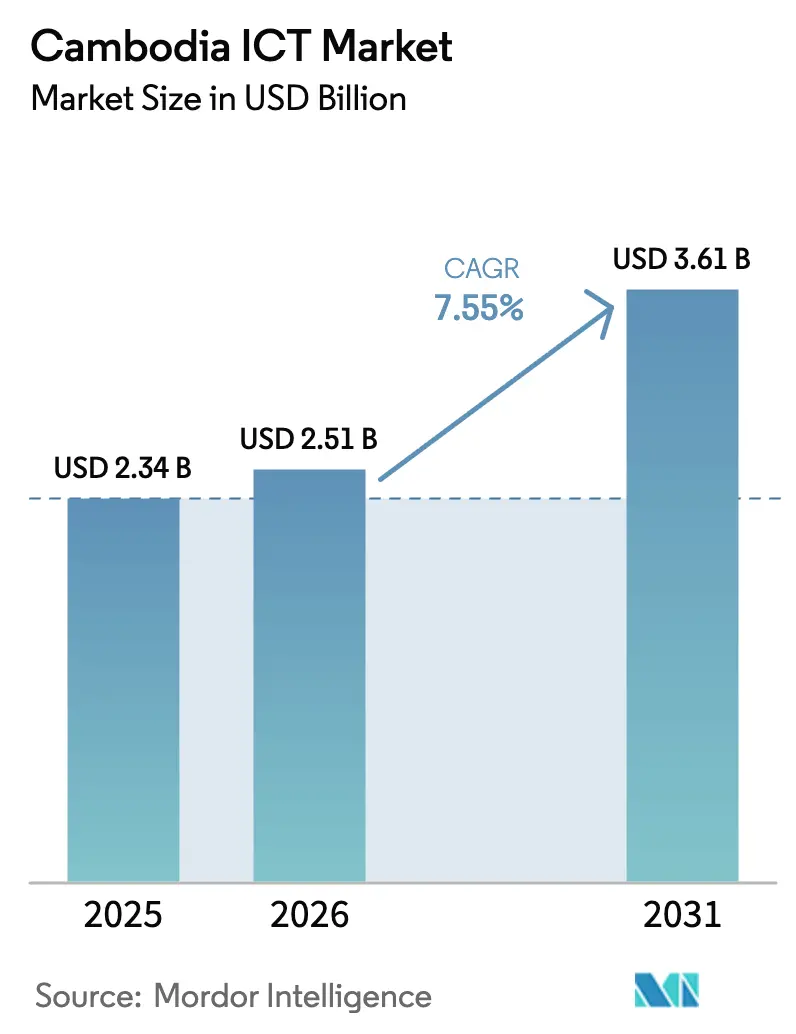

| Base Year Market Size (2025) | USD 2.34 Billion |

| Market Size (2026) | USD 2.51 Billion |

| Market Size (2031) | USD 3.61 Billion |

| Growth Rate (2026 - 2031) | 7.55% CAGR |

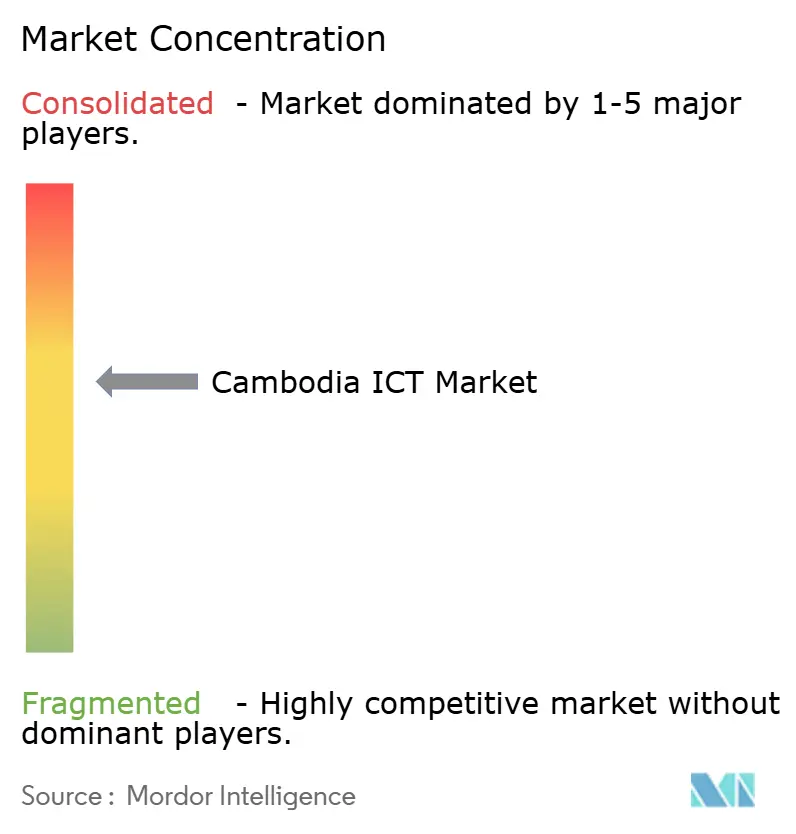

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Cambodia ICT Market Analysis by Mordor Intelligence

The Cambodia ICT market size is expected to increase from USD 2.34 billion in 2025 to USD 2.51 billion in 2026 and reach USD 3.61 billion by 2031, growing at a CAGR of 7.55% over 2026-2031. Policy-driven digitization, nationwide commercial 5G service launched on 1 January 2026, and surging demand for cloud-native and mobile-first enterprise solutions are expanding the addressable base of both consumers and businesses. Telecom operators are upgrading radio access networks, while hyperscale and local data-center investors are adding capacity, narrowing latency gaps that once limited enterprise workloads. Small and medium enterprises (SMEs) are embracing software-as-a-service and QR-code payments, reshaping distribution channels and compressing cash cycles. Meanwhile, draft data-protection rules and rural power constraints remain headwinds, tempering the otherwise robust growth trajectory of the Cambodia ICT market.

Key Report Takeaways

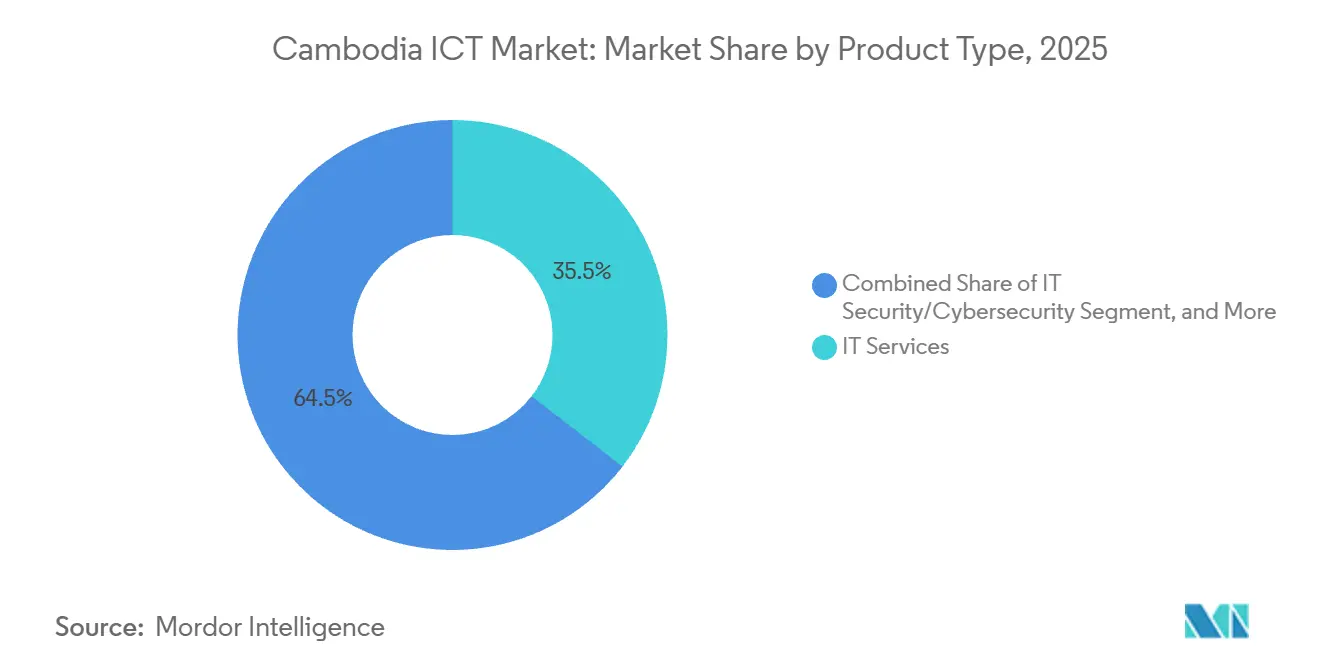

- By product category, IT services led with 35.48% revenue share in 2025, while cyber-security is forecast to advance at an 8.24% CAGR to 2031.

- By enterprise size, large enterprises accounted for 52.21% of the Cambodia ICT market share in 2025, whereas SMEs are projected to expand at an 8.72% CAGR through 2031.

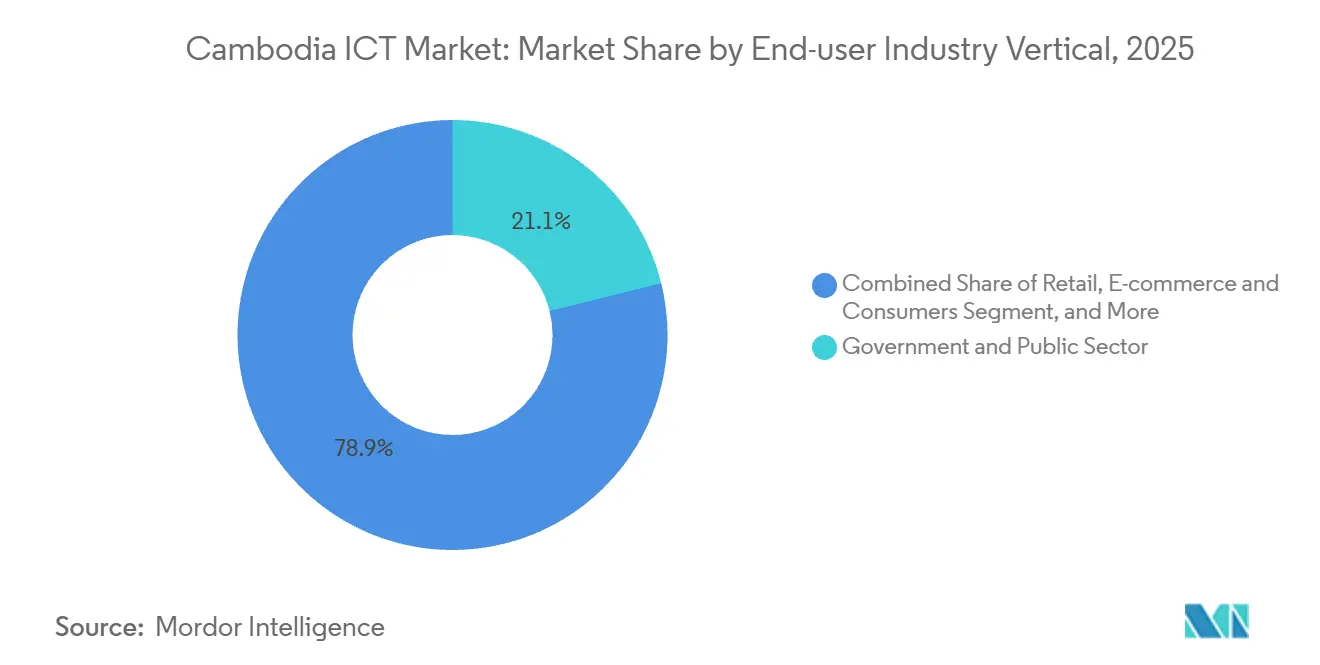

- By end-user vertical, government and public sector held 21.14% of spending in 2025, but retail and e-commerce is the fastest-growing vertical at an 8.91% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Cambodia ICT Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government Digital Economy and Society Policy 2021-2035 | +1.8% | National, strongest in Phnom Penh and provincial capitals | Long term (≥ 4 years) |

| Rapid Expansion of Mobile Internet Subscriptions | +1.5% | National, urban-led with rural catch-up | Medium term (2-4 years) |

| Accelerating Cloud and Data Center Investments | +1.2% | Phnom Penh and Siem Reap hubs | Medium term (2-4 years) |

| CamDX Adoption Catalyzing Seamless B2B e-KYC APIs | +0.9% | National, banking and fintech sectors | Short term (≤ 2 years) |

| Rising Smartphone Penetration and Affordable Data Prices | +0.8% | Nationwide | Short term (≤ 2 years) |

| Regional 5G Infrastructure-Sharing Mandates Lowering Capex | +0.7% | Operator networks countrywide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Government Digital Economy and Society Policy 2021-2035

The policy framework mandates end-to-end digitization of public services, standardizes interoperability for ministries, and funds a Tier IV National Data Center that will provide sovereign cloud for sensitive workloads. Rollouts such as the DG SuperApp, SARIKA text-to-speech, and verify.gov.kh have cut document-processing times for citizens and enterprises. Cross-border validation was demonstrated when the Philippines integrated the Khmer digital-identity stack, underscoring export potential. Public procurement under the policy is catalyzing demand for enterprise software, cybersecurity, and platform-as-a-service offerings. Standardized APIs embedded in the framework lower integration costs for start-ups and incumbents alike, encouraging fintech, e-commerce, and health-tech scale-ups.

Rapid Expansion of Mobile Internet Subscriptions

Mobile subscriptions hit about 19.6 million in 2025, equivalent to 117.38 subscriptions per 100 people, creating a mobile-first customer base. The nationwide 5G launch supports peak speeds of up to 20 Gbps, enabling latency-sensitive applications such as autonomous logistics and real-time quality control. Operators added hundreds of base stations and secured fresh bank financing ahead of the launch, driving wider coverage and better service quality. Ubiquitous connectivity underpins subscription video, cloud gaming, and mobile payments, opening new revenue streams for telecoms and content providers. SaaS vendors also benefit as reliable bandwidth reaches rural districts.

Accelerating Cloud and Data Center Investments

Huawei Cloud opened the first in-country cloud region in late 2024, ensuring data-residency compliance for regulated industries and lowering latency for domestic users. Four local colocation operators plus new greenfield projects are boosting rack supply in Phnom Penh, while hyperscalers serve overflow demand from regional hubs. Public-sector and development-finance programs subsidize cloud-migration roadmaps for SMEs, especially in tourism and retail. Converging local and regional capacity is prompting banks, retailers, and logistics firms to adopt hybrid-cloud architectures that were once considered risky because of latency and power constraints. As electricity reliability improves in urban centers, the cost-benefit equation tilts further in favor of cloud deployments.

CamDX Adoption Catalyzing Seamless B2B e-KYC APIs

CamDX processed more than 21.7 million e-KYC transactions by end-2024, linking 60 financial institutions through OAuth 2.0 and mobile deep-link authentication. The CamDigiKey app combines AI-based facial recognition, optical character recognition, and liveness checks to validate identity in minutes. Banks integrating the platform have slashed onboarding times and expanded reach to unbanked rural users. The system’s tie-in with the Interior Ministry’s ID database provides authoritative data feeds, reducing fraud. This infrastructure lowers compliance costs for fintech entrants and creates network effects that accelerate the usage of digital payments and micro-lending products. [1]CamDX Secretariat, “Cambodia Data Exchange Usage Statistics,” CamDX, camdx.gov.kh

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rural Connectivity and Digital Literacy Gaps | -0.6% | Northeastern and mountainous provinces | Long term (≥ 4 years) |

| Pending Personal Data Protection Law Creating Compliance Uncertainty | -0.4% | Nationwide | Short term (≤ 2 years) |

| Low Fixed-Broadband Affordability | -0.3% | Rural and low-income urban households | Medium term (2-4 years) |

| Electricity Reliability Constraints for Edge Data Centers | -0.2% | Rural and peri-urban districts | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rural Connectivity and Digital Literacy Gaps

Urban internet penetration surpassed 90%, yet fixed-broadband access remains scarce in rural areas, where penetration is 3.5% and speeds lag regional peers. Operators hesitate to invest in sparsely populated zones with low average revenue per user despite subsidies from the Universal Service Obligation Fund. NGOs and the Ministry of Education promote digital-skills programs, but research shows persistent competency gaps among teachers and graduates. Limited bandwidth and skills curb the adoption of cloud ERP, telemedicine, and e-learning outside major cities, constraining inclusive growth. This divide slows nationwide adoption of advanced ICT applications in the Cambodian market. [2]Open Development Cambodia Analysts, “Connectivity and Digital Literacy Gaps,” OpenDevelopment Cambodia, opendevelopmentcambodia.net

Pending Personal Data Protection Law Creating Compliance Uncertainty

Draft data-protection and cybersecurity bills are still under review, leaving enterprises without clear rules on cross-border transfer, breach notification, or localization. Multinationals hesitate to commit long-term capital to in-country infrastructure, while local fintech firms must plan for potential retroactive compliance costs. Development lenders are funding capacity-building, yet enforcement frameworks remain nascent, as reflected in Cambodia’s Tier 4 ranking on the Global Cybersecurity Index. Financial institutions and healthcare providers handling sensitive data, therefore, delay certain cloud migrations, dampening short-term momentum in the Cambodia ICT market. [3]ITU Experts, “Global Cybersecurity Index 2024,” International Telecommunication Union, itu.int

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type - Managed Services Anchor IT Services Dominance

IT services held 35.48% of 2025 revenue, giving the segment the largest Cambodia ICT market share among product lines. Managed security and cloud migration projects top the order books as government APIs and bank modernization accelerate. The Cambodia ICT market size associated with cyber-security solutions is set to climb at an 8.24% CAGR after Japan’s USD 5 million equipment grant and the July 2025 cyber-crime crackdown. Application, cloud, and identity security tools therefore post the fastest spend growth. Hardware demand remains steady, driven by Smart Axiata’s 475 additional BTS sites in 2024 and continued radio densification. In software, ERP, CRM, and core-banking overhauls dominate, with ABA Bank’s SUSE-based stack providing 99.999% uptime and 15% cost savings. The Cambodia ICT market benefits further from infrastructure outlays for the Tier IV National Data Centre and Telcotech’s campus. Finally, telecom operators are shifting toward value-added services, using e-money wallets and digital identity to diversify beyond pure connectivity.

The Cambodia ICT market is therefore evolving from asset-intensive build-outs to service-centric monetization, positioning managed service providers as pivotal orchestrators. Growth potential hinges on tight integration between sovereign data centers, operator edge nodes, and public-cloud APIs, a configuration that de-risks latency-sensitive workloads without violating anticipated data-localization clauses. Vendors able to pair compliance expertise with scalable automation will capture outsized share as ministries mandatorily expose micro-services through CamDX.

By Enterprise Size - SME Cloud Adoption Outpaces Large-Enterprise Spending

Large enterprises generated 52.21% of 2025 spend, but SMEs are pacing the Cambodia ICT market at an 8.72% CAGR to 2031. Grants under the Cambodia Jobs and Enterprise Transformation program helped subsidize cloud inventory and CRM platforms, lowering total cost of ownership for firms with fewer than 100 employees. Online Business Registration and CamDigiKey have streamlined licensing and banking, cutting onboarding time and encouraging micro-enterprises to formalize. Consequently, the Cambodia ICT market size attributed to SMEs is forecast to swell materially over the outlook period.

The large-enterprise segment remains vital, funding sophisticated 5G, AI, and API-monetization projects. Metfone’s pivot to a techco model, bundling eMoney, CamID, and school-information systems, exemplifies revenue-diversification plays. Smart Axiata’s USD 50 million debt facility and Huawei EasyAAU roll-out underscore the capital requirements for maintaining network leadership. Even so, the democratization of SaaS levels digital capabilities, enabling SMEs to deliver near-par service quality without matching the absolute spend of incumbents. This widening user base underpins secular expansion in the Cambodia ICT market.

By End-User Vertical - Retail and E-Commerce Lead Digital Acceleration

Retail and e-commerce recorded the highest 8.91% CAGR outlook on the back of social-commerce uptake among 21.61 million Facebook and TikTok users. Bakong processed USD 54.8 billion in the first half of 2024, and QR codes already power nearly half of digital payments, aligning payment rail maturity with merchant onboarding needs. Cloud POS, inventory analytics, and logistics tech therefore dominate procurement pipelines across large retailers and MSMEs alike. The Cambodia ICT market size allocated to retail tech will rise proportionately as cross-border KHQR acceptance spreads to Vietnam and Laos.

Government and public sector kept 21.14% share in 2025, driven by DG SuperApp contracts and the National Data Centre. BFSI continues modernizing core systems to reach the unbanked, with ABA Bank’s platform upgrade improving deployment times by 50%. Healthcare, manufacturing, and telecom also deepen IoT and analytics adoption, but their growth trails retail due to regulatory and infrastructure frictions. As verticals converge on API-based ecosystems, the Cambodia ICT market will see horizontal demand for managed security and analytics regardless of industry silos.

Geography Analysis

Phnom Penh anchors Cambodia ICT market demand thanks to dense fiber networks, multiple tier-III colocation sites, and the bulk of the nation’s ICT talent. Siem Reap, Battambang, and Sihanoukville follow, benefiting from tourism-driven service clusters and special-economic-zone incentives. Mobile broadband coverage exceeds 93% of the population, yet average speeds and reliability decline outside urban cores, limiting cloud and video-conferencing quality for rural enterprises. The Universal Service Obligation Fund subsidizes tower builds in remote provinces, but challenging terrain and low average revenue per user impede rapid rollout.

Cross-border cooperation shapes the geography of investment. China-Cambodia free-trade provisions streamline ICT equipment imports, while Australia’s Partnerships for Infrastructure injects telecommunications funding with governance conditionalities. ASEAN digital-economy talks aim to harmonize data-flow rules, giving Cambodian start-ups wider regional market access once technical standards align. Phnom Penh’s concentration of data centers yields agglomeration benefits, prompting hyperscalers to consider edge nodes in nearby provinces to manage overflow and support disaster recovery.

Rural provinces lag in fixed-broadband affordability, compelling reliance on cellular data for business applications. Power reliability issues constrain edge-computing deployments outside core grids, though solarized base stations show promise as micro-edge hosts. Government policy targets inclusive growth by mandating digital-literacy programs and smart-village pilots, but capacity gaps persist. Over the forecast horizon, gradual 5G expansion and targeted infrastructure grants will chip away at geographic disparities, pulling new user cohorts into the mainstream Cambodia ICT market.

Competitive Landscape

The market is moderately concentrated. Smart Axiata, Metfone, and Cellcard serve virtually all mobile subscribers and leverage scale advantages to invest in 5G, fiber backhaul, and fintech platforms. To offset pricing pressure, operators bundle content streaming, cloud back-up, and micro-insurance, moving beyond traditional airtime revenue. In contrast, IT Services, software, and colocation remain fragmented, with local integrators, Vietnamese data-center operators, and regional hyperscalers vying for enterprise contracts.

Strategic alliances reshape competition. Smart Axiata’s pact with TrueMoney merges telecom distribution and fintech rails, unlocking cross-sell efficiencies and boosting rural customer reach. Metfone’s partnership with Cisco elevates its enterprise portfolio, letting it offer certified lifecycle support across the provinces. All three operators joined the GSMA Open Gateway initiative, exposing network APIs for fraud prevention and identity verification, a move that levels the playing field for over-the-top service innovators.

White-space innovation emerges in AI localization for the Khmer language, edge-computing nodes powered by solar arrays, and cybersecurity solutions tailored to the country’s evolving regulatory landscape. Start-ups leverage CamDX’s standardized APIs to embed finance in ride-hailing and e-commerce apps, while blockchain pilots in land registry attract developer ecosystems aligned with the National Blockchain Roadmap. Competitive intensity will therefore remain moderate to high as incumbents guard scale advantages and disruptors exploit policy-driven digital public infrastructure openings.

Cambodia ICT Industry Leaders

Amazon Inc

IBM Corporation

Huawei Technologies Co., Ltd.

Google LLC

Microsoft Corporation

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Smart Axiata, Metfone, and Cellcard launched commercial 5G services nationwide.

- December 2025: Metfone and Cisco announced a strategic cooperation to distribute and support Cisco’s enterprise portfolio across Cambodia.

- December 2025: Verify.gov.kh digital-identity technology was adopted by the Philippines for its national ID system.

- November 2025: Phillip Bank Cambodia partnered with Liquid Group to introduce RoamQR for cross-border payments to Singapore.

Cambodia ICT Market Report Scope

Information and communications technology (ICT) is an extended term for information technology (IT) that encompasses a wide range of hardware, software, internet- and telecommunications-based services, social networking, media applications, and so on. The technology allows users to access, retrieve, store, send, and manipulate information in digital form. With the growing demand for multiple advanced solutions, such as IoT, cloud computing, big data, content management, and so on, ICT has gained popularity.

The Cambodia ICT Market Report is Segmented by Product Type (IT Hardware, IT Software, IT Services, IT Infrastructure, IT Security/Cybersecurity, and Communication Services), Enterprise Size (Small and Medium-sized Enterprises, and Large Enterprises), End-user Industry Vertical (BFSI, Government and Public Sector, Oil and Gas, IT and Telecom, Retail E-commerce and Consumers, Manufacturing and Industrial, Energy and Utilities, Healthcare, Other End-user Industry Verticals). The Market Forecasts are Provided in Terms of Value USD.

By Product Type

| IT Hardware | Computer Hardware |

| Networking Equipment | |

| Peripherals | |

| IT Software | |

| IT Services | IT Consulting and Implementation |

| IT Outsourcing (ITO) | |

| Business Process Outsourcing (BPO) | |

| Managed Security Services | |

| Cloud and Platform Services | |

| IT Infrastructure | |

| IT Security/Cybersecurity | Application Security |

| Cloud Security | |

| Data Security | |

| Network Security | |

| Endpoint Security | |

| Infrastructure Protection | |

| Integrated Risk Management | |

| Identity and Access Management (IAM) | |

| Communication Services |

By Enterprise Size

| Small and Medium-sized Enterprises |

| Large Enterprises |

By End-user Industry Vertical

| BFSI |

| Government and Public Sector |

| Oil and Gas |

| IT and Telecom |

| Retail, E-commerce and consumers |

| Manufacturing and Industrial |

| Energy and Utilities |

| Healthcare |

| Other End-user Industry Verticals (Includes Transportation, Logistics, Education, Hospitality etc.) |

| By Product Type | IT Hardware | Computer Hardware |

| Networking Equipment | ||

| Peripherals | ||

| IT Software | ||

| IT Services | IT Consulting and Implementation | |

| IT Outsourcing (ITO) | ||

| Business Process Outsourcing (BPO) | ||

| Managed Security Services | ||

| Cloud and Platform Services | ||

| IT Infrastructure | ||

| IT Security/Cybersecurity | Application Security | |

| Cloud Security | ||

| Data Security | ||

| Network Security | ||

| Endpoint Security | ||

| Infrastructure Protection | ||

| Integrated Risk Management | ||

| Identity and Access Management (IAM) | ||

| Communication Services | ||

| By Enterprise Size | Small and Medium-sized Enterprises | |

| Large Enterprises | ||

| By End-user Industry Vertical | BFSI | |

| Government and Public Sector | ||

| Oil and Gas | ||

| IT and Telecom | ||

| Retail, E-commerce and consumers | ||

| Manufacturing and Industrial | ||

| Energy and Utilities | ||

| Healthcare | ||

| Other End-user Industry Verticals (Includes Transportation, Logistics, Education, Hospitality etc.) | ||

Key Questions Answered in the Report

How large is the Cambodia ICT market in 2026?

The Cambodia ICT market size reached USD 2.51 billion in 2026 and is forecast to expand to USD 3.61 billion by 2031.

What is driving the fastest growth within Cambodia’s ICT spend?

Cyber-security services are expanding at an 8.24% CAGR through 2031 thanks to government mandates and Japan's USD 5 million equipment grant.

Which customer segment is accelerating ICT adoption most quickly?

SMEs are pacing spend at an 8.72% CAGR as cloud ERP and digital-payment subsidies lower adoption barriers.

Which vertical offers the strongest growth opportunity?

Retail and e-commerce show the fastest 8.91% CAGR on the back of social commerce and Bakong QR-code payment uptake.

Why are hyperscalers not yet present in Cambodia?

Pending data-protection rules and limited in-country demand have kept AWS, Google Cloud, and Microsoft Azure from building local regions, creating room for domestic data-center operators.

What challenges could slow ICT growth over the next five years?

Rural broadband gaps, delayed data-protection legislation, and provincial power reliability issues may curb adoption outside major cities.

Page last updated on: