Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

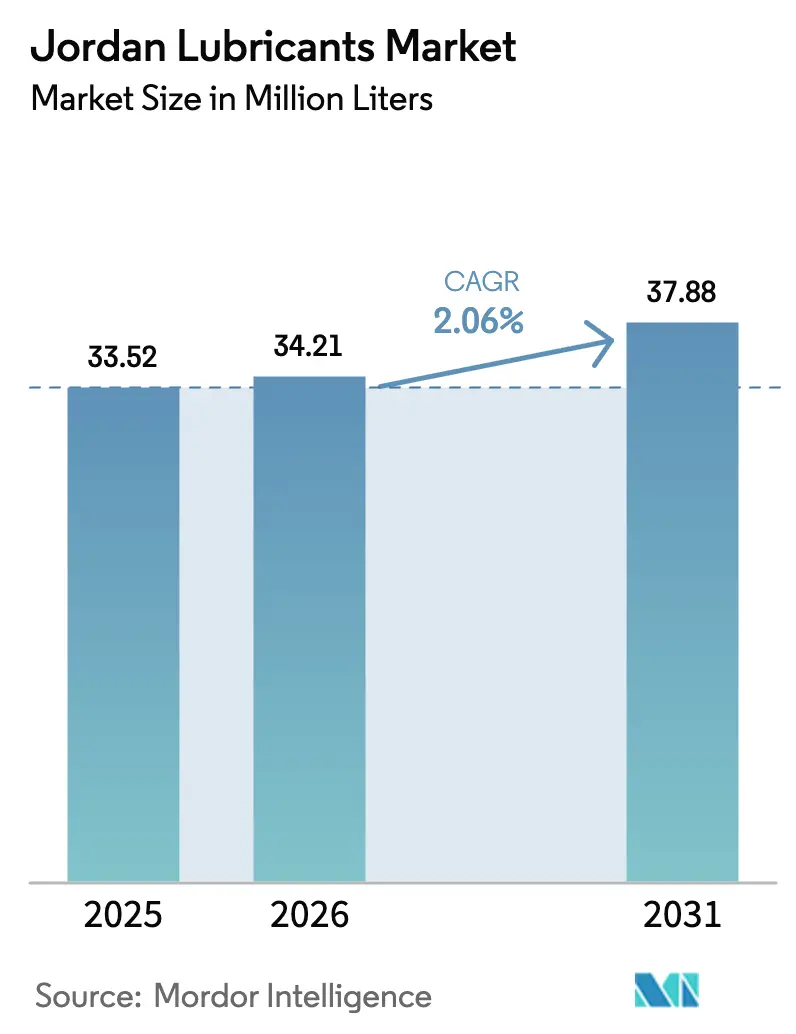

| Base Year Market Size (2025) | 33.52 Million liters |

| Market Volume (2026) | 34.21 Million liters |

| Market Volume (2031) | 37.88 Million liters |

| Growth Rate (2026 - 2031) | 2.06% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Jordan Lubricants Market Analysis by Mordor Intelligence

The Jordan Lubricants Market size is expected to increase from 33.52 Million liters in 2025 to 34.21 Million liters in 2026 and reach 37.88 Million liters by 2031, growing at a CAGR of 2.06% over 2026-2031. Expansion in passenger-car ownership, a steady pipeline of power-plant projects, and growing phosphate and potash output underpin demand, while faster adoption of electric and hybrid powertrains and longer drain intervals limit absolute volume growth. The cabinet’s 2025 tax cuts on gasoline, hybrid, and electric vehicles have rebalanced new-car mix toward fuel-efficient models that consume less oil, yet the shift simultaneously accelerates penetration of low-viscosity synthetic formulations that command higher margins. Industrial consumption benefits from the National Electric Power Company’s (NEPCO) 5,200 MW installed base and a planned 700 MW combined-cycle gas-turbine (CCGT) project, both of which require ISO 8068:2024-compliant turbine oils. Bio-based and re-refined lubricants gain policy tailwinds from the Ministry of Environment’s Energy Sector Green Growth National Action Plan 2021–2025, which prioritizes renewable feedstocks and tighter hazardous-waste controls.

Key Report Takeaways

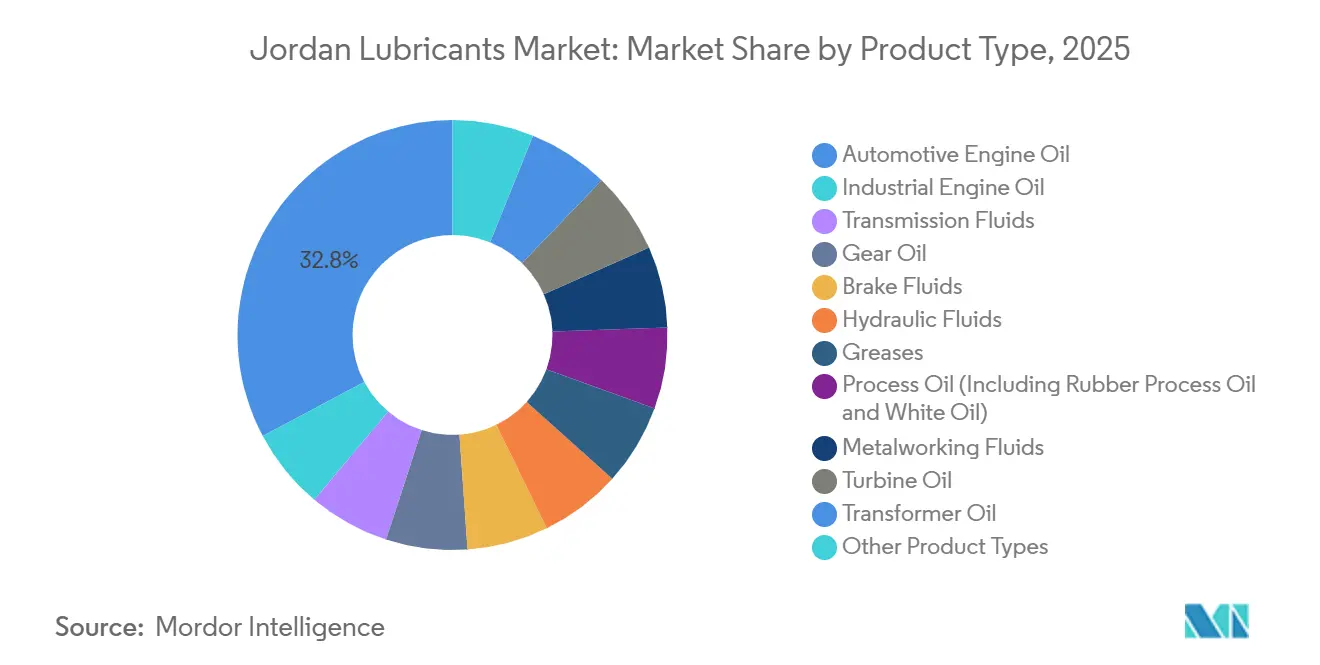

- By product type, automotive engine oil led with 32.78% Jordan lubricants market share in 2025, while industrial engine oil is set to expand at a 2.45% CAGR through 2031.

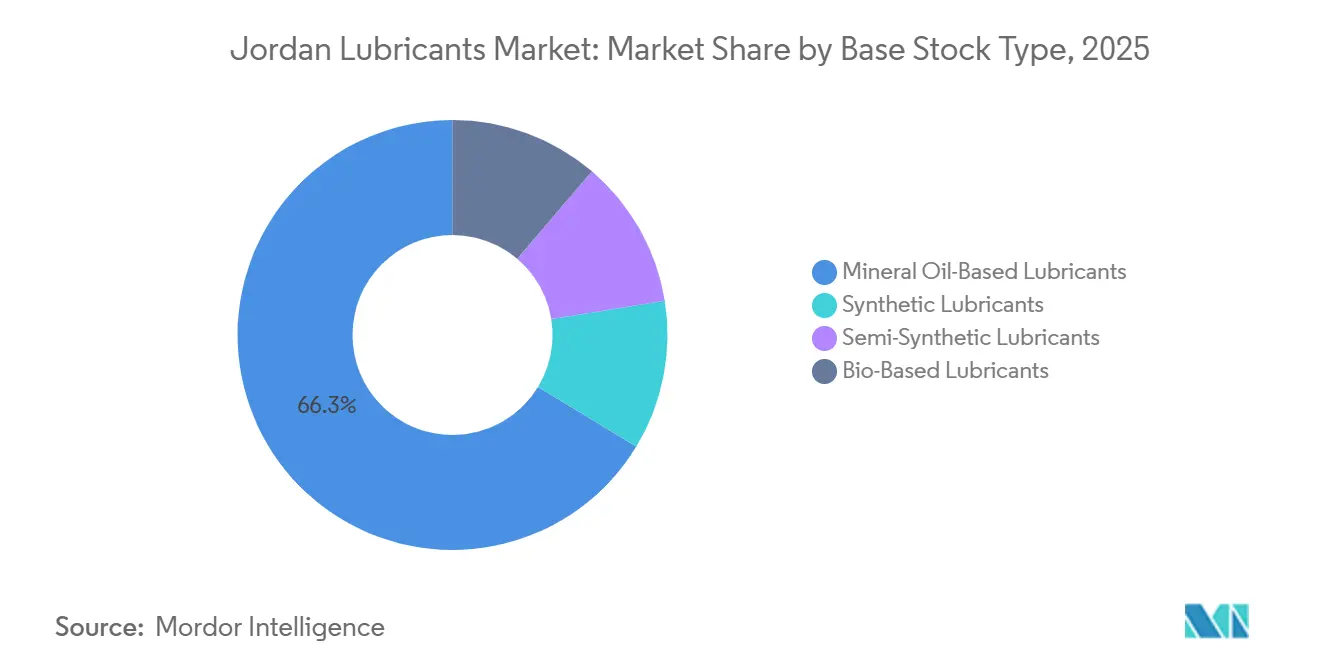

- By base stock type, mineral oil-based lubricants dominated with a 66.32% share in 2025, whereas bio-based lubricants are forecast to post a 2.89% CAGR to 2031.

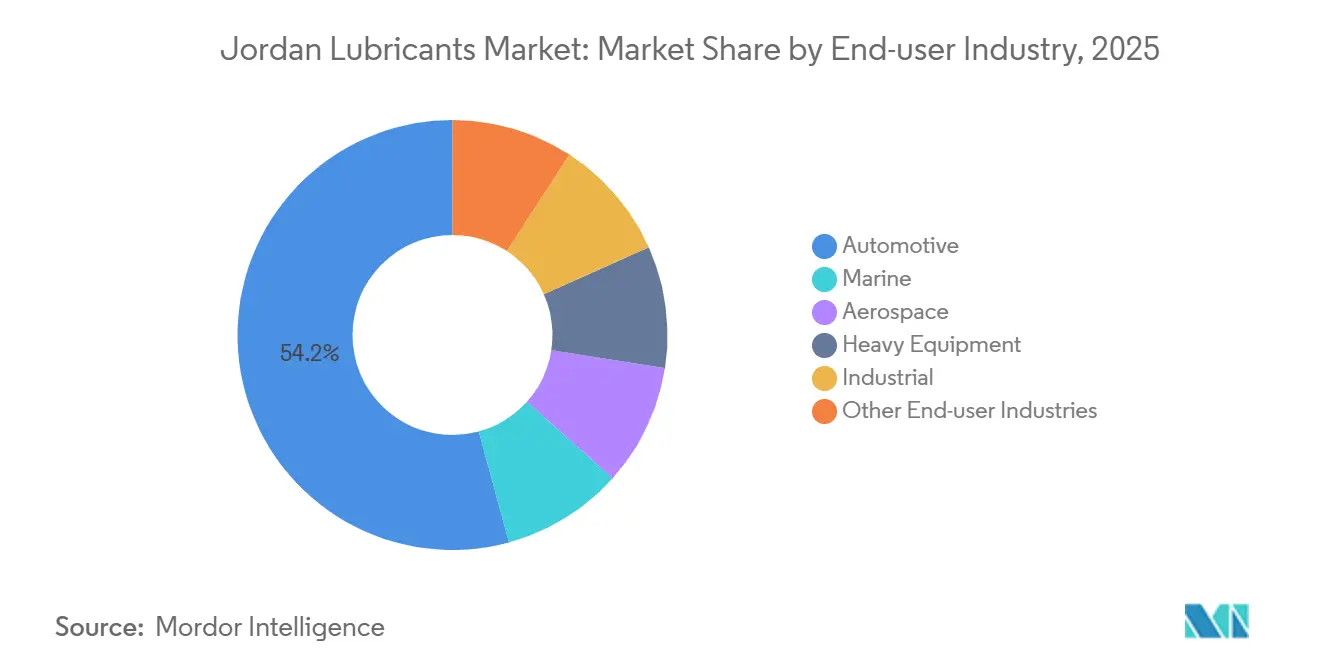

- By end-user industry, automotive accounted for 54.23% of volume in 2025; the industrial segment, however, is projected to grow at a 2.35% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Jordan Lubricants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surging Vehicle Population in Jordan | +0.6% | National, with concentration in Amman, Irbid, Zarqa governorates | Medium term (2–4 years) |

| Renewed Downstream Investments at Zarqa Refinery | +0.3% | National, supply-chain benefits for Amman industrial zone | Long term (≥ 4 years) |

| Accelerated Roll-Out of Combined-Cycle Gas-Turbine (CCGT) Plants | +0.4% | National, peak demand in Amman East, Samra, Al Qatrana power hubs | Medium term (2–4 years) |

| Mandatory Engine-Efficiency Standards from 2027 | +0.5% | National, early adoption in Greater Amman Municipality fleet procurement | Short term (≤ 2 years) |

| Rapid Growth of Ride-Hailing and Delivery Fleets | +0.2% | Urban centers: Amman, Irbid, Aqaba | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Surging Vehicle Population in Jordan

Vehicle registrations surpassed 2 million in 2024 and are on track to exceed 2.3 million by 2030, anchoring baseline demand for engine, transmission, and brake fluids. Hybrid clearances grew 27% year on year in 2025 following tax cuts, pushing SAE 0W-20 and 5W-30 synthetics deeper into the aftermarket. Private ownership climbed 6.4% during 2024, yet new import rules effective November 2025 restrict electric vehicles older than three years, lifting quality benchmarks that indirectly elevate lubricant performance requirements. The Jordan Standards and Metrology Organization (JSMO) tests every batch at its ISO/IEC 17025:2017-accredited lab, ensuring minimum viscosity, flash point, and base-number thresholds are met[1]JSMO, “Accredited Laboratories List,” jsmo.gov.jo .

Renewed Downstream Investments at Zarqa Refinery

Jordan Petroleum Refinery Company (JPRC) plans a USD 2.6 billion upgrade to lift crude capacity to 120,000 bpd, though talks with the Sinopec-Itochu consortium remain unresolved. Even during delay, JPRC’s 25,000 t/yr blending plant, certified to ISO 9001:2015 and approved by Mercedes-Benz and GE, supplies more than 100 grades locally. A successful expansion would unlock domestic Group II/III base oil streams, reducing import dependence and enabling premium synthetic blends.

Accelerated Roll-Out of CCGT Plants

NEPCO’s installed 5,200 MW fleet includes several CCGT units, and a 700 MW tender published in November 2025 signals more turbines to come. ISO 8068:2024 raises oxidative-stability and volatility bars for turbine oils, promoting Group III+ and ester chemistries that support extended drain intervals. Reliable baseload gas capacity remains essential as Jordan targets 31% renewable electricity by 2030.

Mandatory Engine-Efficiency Standards from 2027

Jordan intends to align with Euro 6 norms starting in 2027, driving demand for low-SAPS oils that protect diesel particulate filters. The Gulf Standards Organization’s GSO 1785-2:2023 already references ACEA sequences and provides a regional template. OEMs consequently specify thinner grades—SAE 0W-20 and below—that rely on Group III+ or PAO base stocks for cold-crank and volatility targets.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Political and Economic Instability | -0.4% | National, spillover from regional tensions (Gaza, Syria) | Medium term (2–4 years) |

| Premium-Grade Lubricant Price Inflation Vs. Regional Peers | -0.3% | National, competitive pressure from GCC imports (Saudi Arabia, UAE, Kuwait) | Short term (≤ 2 years) |

| Expansion of Electric-Bus Pilots in Amman Reducing Engine Oil Demand | -0.2% | Greater Amman Municipality, planned expansion to 4 additional BRT lines | Medium term (2–4 years) |

| Source: Mordor Intelligence | |||

Political and Economic Instability

Public debt stood at 112.5% of GDP in 2023, and the USD 1.2 billion IMF facility effective March 2024 obliges fiscal tightening, limiting public spending on fleet renewal. GDP grew only 2.6% in 2024 with similar expectations for 2025, slowing discretionary upgrades. Regional shocks from the Gaza crisis and the Syrian refugee burden dilute tourism receipts and remittances, reducing lubricant purchases. Environmental fines under the 2017 Protection Law reach JOD 10 million for severe contamination, adding compliance costs that smaller blenders struggle to absorb.

Premium-Grade Lubricant Price Inflation Vs. Regional Peers

Absence of integrated Group II/III refining inflates import bills; Saudi, UAE, and Kuwaiti suppliers land synthetics 10–15% cheaper, squeezing Jordanian distributors. Castrol’s MoreCircular initiative showcases lower-carbon, re-refined base oils, but Jordan lacks a robust used-oil collection network, limiting local circular supply. JSMO’s four-stage certification secures product quality, yet the process adds cost and time to market entry[2]U.S. Commercial Service, “Jordan Standards and Certification,” trade.gov .

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Industrial Engine Oil Outpaces Automotive Growth

Automotive engine oil held 32.78% of Jordan lubricants market share in 2025, yet industrial engine oil is forecast to register a 2.45% CAGR to 2031, outstripping every other category. Heavy-duty CK-4 and ACEA E9 oils serve haul trucks at Jordan Phosphate Mines Company and Arab Potash Company, while turbine oils meet ISO 8068:2024 standards in NEPCO’s CCGT fleet. Transmission, gear, and hydraulic fluids support the USD 2.5 billion Aqaba–Amman desalination build, with thousands of pumps and actuators coming online.

Castrol’s MoreCircular program validated re-refined base oils globally, but Jordan’s collection rate remains low, limiting near-term supply. JSMO’s ISO/IEC 17025 lab tests viscosity, density, flash point, pour point, and base number, underpinning product credibility. JPRC’s 25,000 t/yr plant offers 100-plus grades, positioning JoPetrol to win tenders once domestic base-oil supply materializes through the refinery upgrade.

By Base Stock Type: Bio-Based Gains Traction amid Mineral Dominance

Mineral oil-based lubricants captured 66.32% of volume in 2025, yet bio-based lubricants are projected to clock a 2.89% CAGR through 2031, the fastest across base-stock groups. The Energy Sector Green Growth plan encourages biodegradable fluids in forestry, agriculture, and open-system hydraulics. Scientific literature reports 60–80% biodegradability within 28 days for ester-based lubricants, well above mineral benchmarks.

Synthetic and semi-synthetic blends fulfill low-viscosity passenger-car requirements—SAE 0W-16 and below—that hinge on Group III+ or PAO chemistries. Jordan’s 2017 Environmental Protection Law sets stiff fines and even prison for hazardous-waste violations, nudging users toward lower-toxicity products. Shell’s local distributor already supplies biodegradable hydraulic fluids to Aqaba port, signaling early adoption.

By End-user Industry: Industrial Segment Accelerates on Power and Mining

Automotive represented 54.23% of volume in 2025; however, the industrial segment is on course for a 2.35% CAGR to 2031, lifted by power generation, mining, and infrastructure spending. The planned 700 MW CCGT facility and existing 5,200 MW portfolio sustain turbine-oil and transformer-oil demand.

Mining consumes large volumes of diesel engine oil, gear oil, and hydraulic fluid in phosphate and potash operations. The two-wheeler fleet expands after 2025 duty cuts, supporting small but rising volumes of motorcycle oils. Greater Amman’s electric-bus roll-out trims diesel demand yet opens a niche for e-driveline lubricants.

Geography Analysis

Amman, Irbid, and Zarqa anchor more than half of lubricant consumption, mirroring vehicle registrations and industrial load centers. Amman hosts the BRT Green Line, ride-hailing fleets, and premium-oil retailers, while Zarqa is home to JPRC’s blending facility and the prospective refinery upgrade. Aqaba port drives marine-oil demand and functions as the entry gate for imported base stocks from GCC refiners, although land transport costs erode price competitiveness.

The cabinet’s 2025 tax reforms and the November 2025 import-quality mandate improve fleet efficiency but tilt usage toward low-viscosity synthetics, primarily in urban zones. Rural governorates lag in charging infrastructure despite USD 15 million earmarked for Greater Amman chargers, creating an uneven transition to electric powertrains. Cross-border competition persists; GCC suppliers leverage economies of scale to land synthetics at double-digit discounts.

Environmental oversight remains strict, especially near Aqaba’s marine ecosystem and in mining districts. Fines that reach JOD 10 million for severe contamination push operators toward biodegradables and certified waste-oil collection programs. NEPCO’s grid-expansion plans sustain transformer-oil demand countrywide, while smart-meter roll-outs will enlarge the pool of dielectric fluids required in distribution assets.

Competitive Landscape

Global majors—Shell, TotalEnergies, ExxonMobil, Castrol, and Chevron—share shelves with JoPetrol and ADNOC Distribution in a moderately fragmented arena. Shell’s distributor, International Overseas Trading EST., supplies industrial and marine customers, leveraging Tellus hydraulics and Corena compressor oils. TotalEnergies managed roughly 180 filling stations until Vivo Energy agreed to acquire the business in November 2025, a move that will bring the Engen brand and may realign lubricant portfolios.

JoPetrol generated JOD 73 million net profit in fiscal 2024, backed by ISO 9001 quality systems and OEM seals from Mercedes-Benz and GE. The stalled refinery upgrade caps vertical integration, yet local blending still offers responsiveness and lower freight costs for domestic customers. Castrol relies on multiple third-party distributors and promotes re-refined MoreCircular lines to differentiate.

Barriers to entry remain high due to JSMO’s certification regime and capital requirements for blending plants. Strategy focus centers on technical support, OEM approvals, and specialty niches like low-SAPS or biodegradable fluids. Price pressure from GCC imports forces Jordanian suppliers to emphasize service, lab testing, and rapid delivery instead of discounts.

Jordan Lubricants Industry Leaders

TotalEnergies

Zaitak (Jordan National Lube Oil Company LLT)

Shell plc

Castrol Limited

Scope Lubricants

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: Vivo Energy signed an agreement to acquire TotalEnergies Marketing Jordan. This agreement included approximately 180 service stations and the company's fuels and lubricants business, representing Vivo Energy's initial entry into the Middle East market.

- June 2025: Arabian Petroleum Supply Company (Apsco) formed a strategic alliance with Exxon Mobil Corporation to expand the distribution and marketing of Mobil-branded lubricants in Jordan. This initiative built on Apsco's established role as the exclusive distributor for Mobil lubricants.

Jordan Lubricants Market Report Scope

A lubricant is a fluidic material that reduces friction between surfaces in contact and energy loss caused by friction. It can also be handy in cleaning, cooling, and protecting metal parts from corrosion, rust, and other challenges that a vehicle, machine, or equipment faces during operation.

The Jordan lubricants market is segmented by product type, base stock type, and end-user industry. By product type, the market is segmented into automotive engine oil, industrial engine oil, transmission fluids, gear oil, brake fluids, hydraulic fluids, greases, process oil (including rubber process oil and white oil), metalworking fluids, turbine oil, transformer oil, and other product types. By base stock type, the market is segmented into mineral oil-based lubricants, synthetic lubricants, semi-synthetic lubricants, and bio-based lubricants. By end-user industry, the market is segmented into automotive (passenger vehicles, commercial vehicles, and two-wheelers), marine, aerospace, heavy equipment (construction, mining, and agriculture), and industrial (power generation, metallurgy and metalworking, textiles, oil and gas, and other end-user industries). For each segment, the market sizing and forecasts have been done on the basis of volume (liters).

By Product Type

| Automotive Engine Oil |

| Industrial Engine Oil |

| Transmission Fluids |

| Gear Oil |

| Brake Fluids |

| Hydraulic Fluids |

| Greases |

| Process Oil (Including Rubber Process Oil and White Oil) |

| Metalworking Fluids |

| Turbine Oil |

| Transformer Oil |

| Other Product Types |

By Base Stock Type

| Mineral Oil-Based Lubricants |

| Synthetic Lubricants |

| Semi-Synthetic Lubricants |

| Bio-Based Lubricants |

By End-user Industry

| Automotive | Passenger Vehicles |

| Commercial Vehicles | |

| Two-Wheelers | |

| Marine | |

| Aerospace | |

| Heavy Equipment | Construction |

| Mining | |

| Agriculture | |

| Industrial | Power Generation |

| Metallurgy and Metalworking | |

| Textiles | |

| Oil and Gas | |

| Other End-user Industries |

| By Product Type | Automotive Engine Oil | |

| Industrial Engine Oil | ||

| Transmission Fluids | ||

| Gear Oil | ||

| Brake Fluids | ||

| Hydraulic Fluids | ||

| Greases | ||

| Process Oil (Including Rubber Process Oil and White Oil) | ||

| Metalworking Fluids | ||

| Turbine Oil | ||

| Transformer Oil | ||

| Other Product Types | ||

| By Base Stock Type | Mineral Oil-Based Lubricants | |

| Synthetic Lubricants | ||

| Semi-Synthetic Lubricants | ||

| Bio-Based Lubricants | ||

| By End-user Industry | Automotive | Passenger Vehicles |

| Commercial Vehicles | ||

| Two-Wheelers | ||

| Marine | ||

| Aerospace | ||

| Heavy Equipment | Construction | |

| Mining | ||

| Agriculture | ||

| Industrial | Power Generation | |

| Metallurgy and Metalworking | ||

| Textiles | ||

| Oil and Gas | ||

| Other End-user Industries | ||

Key Questions Answered in the Report

How large is the Jordan lubricants market in 2026?

The Jordan lubricants market size stands at 34.21 million liters in 2026 and is projected to reach 37.88 million liters by 2031.

What impact will electric-bus deployments have on lubricant consumption?

Electric buses reduce diesel-engine oil volumes but still require drivetrain fluids, greases, and coolants, slightly reshaping but not eliminating fleet lubricant needs.

Which lubricant product segment is expanding the fastest?

Industrial engine oil is projected to record the highest growth, at 2.45% CAGR through 2031.

How will upcoming emission standards affect lubricant specifications?

Planned Euro 6-aligned rules in 2027 will boost demand for low-SAPS, low-viscosity synthetic oils that protect after-treatment devices.

Page last updated on: