Syndromic Multiplex Diagnostic Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Market Size (2026) | USD 3.10 Billion |

| Market Size (2031) | USD 3.98 Billion |

| Growth Rate (2026 - 2031) | 5.13% CAGR |

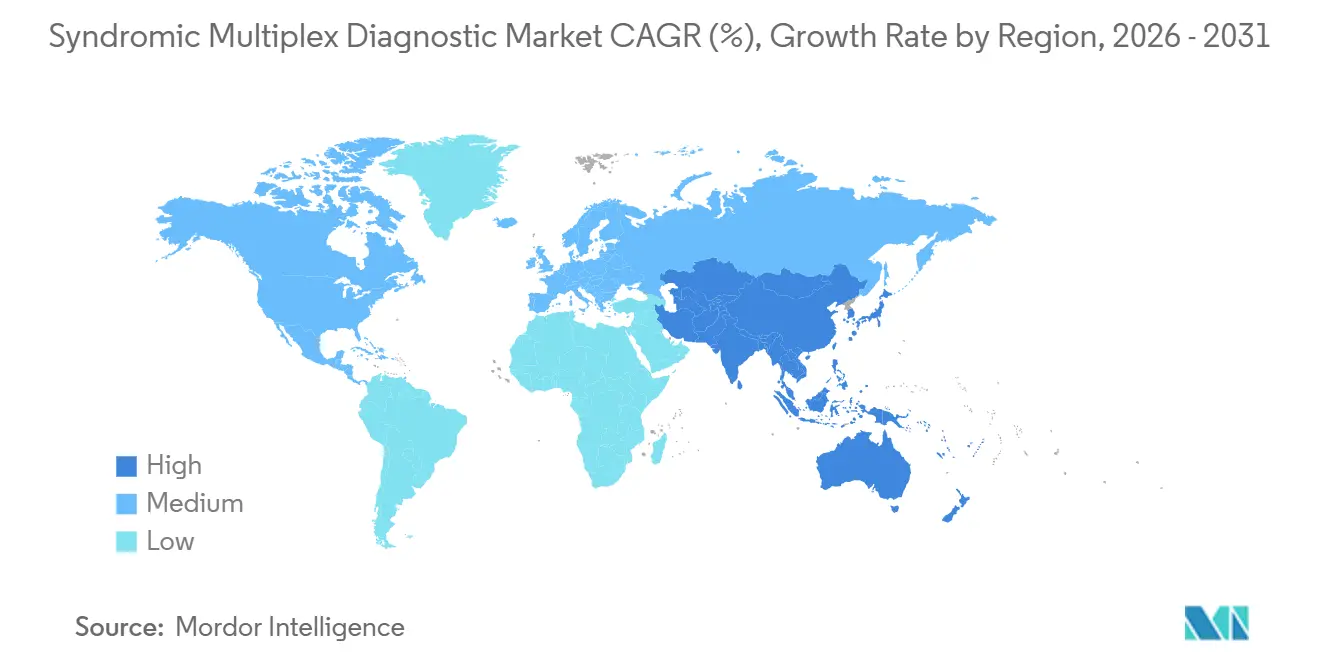

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

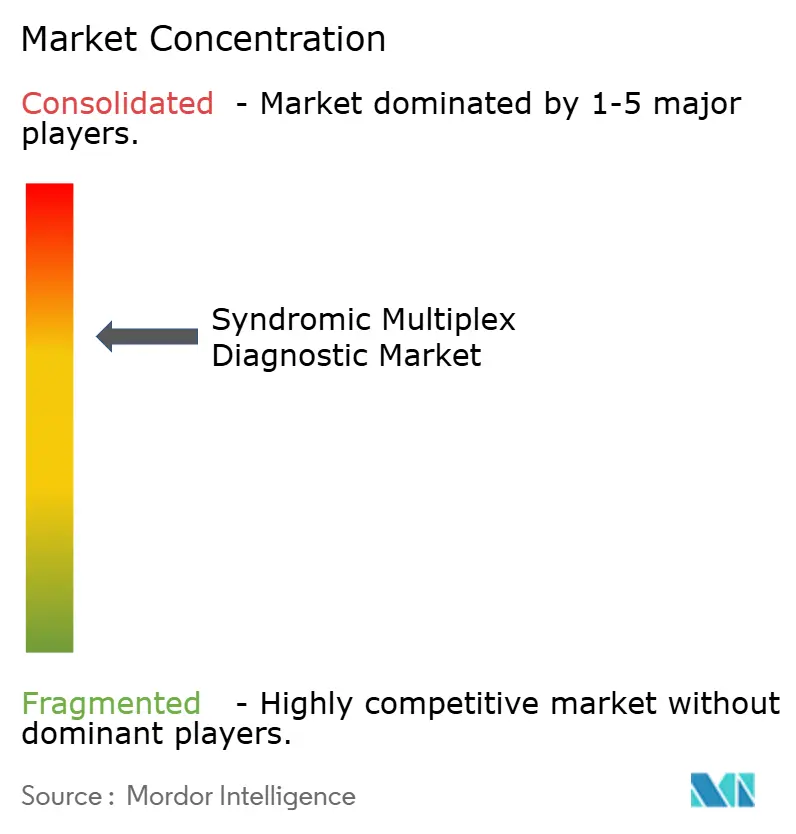

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Syndromic Multiplex Diagnostic Market Analysis by Mordor Intelligence

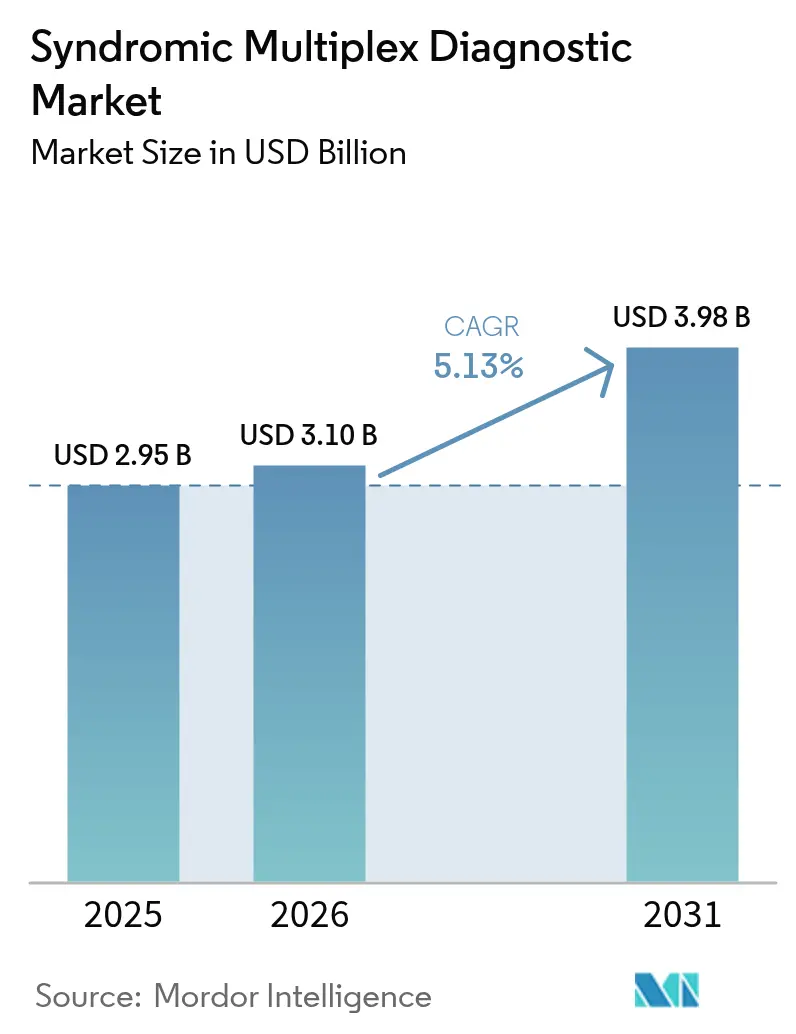

The syndromic multiplex diagnostic market size was valued at USD 2.95 billion in 2025 and was estimated to grow from USD 3.10 billion in 2026 to reach USD 3.98 billion by 2031, at a CAGR of 5.13% during the forecast period (2026-2031). Rising respiratory virus co-circulation, the move toward enteric pathogen surveillance, and reimbursement that favors multiplex testing are sustaining steady demand. Next-generation sequencing (NGS) assays are broadening the clinical toolkit by detecting unexpected pathogens that fixed-target panels miss, a capability that shortened confirmation time during the 2025 H5N1 spillover event. Retail pharmacy chains are deploying CLIA-waived systems in rural clinics, expanding access while intensifying price competition from Asia-Pacific suppliers that offer panels at 40-60% lower list prices. Regulatory scrutiny is increasing as the U.S. Food and Drug Administration (FDA) now requires 510(k) submissions for most laboratory-developed multiplex panels, stretching approval timelines by up to 18 months.

Key Report Takeaways

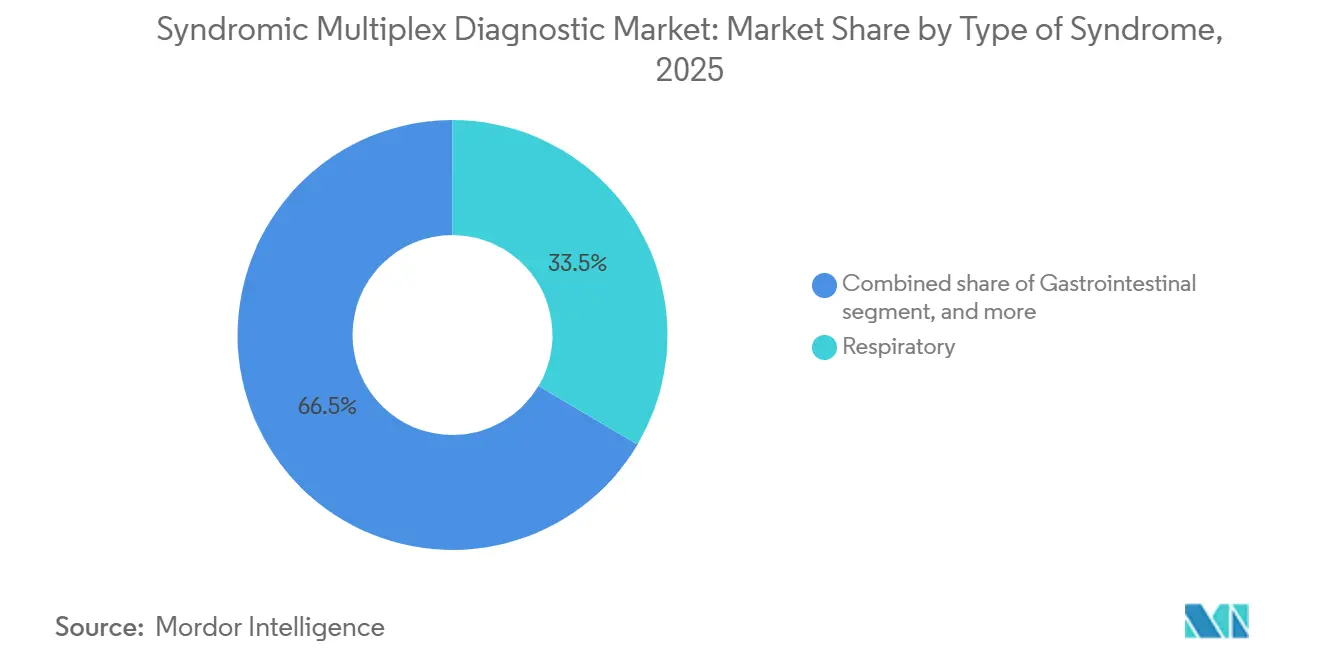

- By type of syndrome, respiratory panels led with 33.55% of syndromic multiplex diagnostic market share in 2025, while gastrointestinal panels are advancing at 9.25% CAGR through 2031.

- By technology, multiplex PCR platforms held 63.53% share of the syndromic multiplex diagnostic market size in 2025 and NGS-based assays are projected to expand at 10.75% CAGR to 2031.

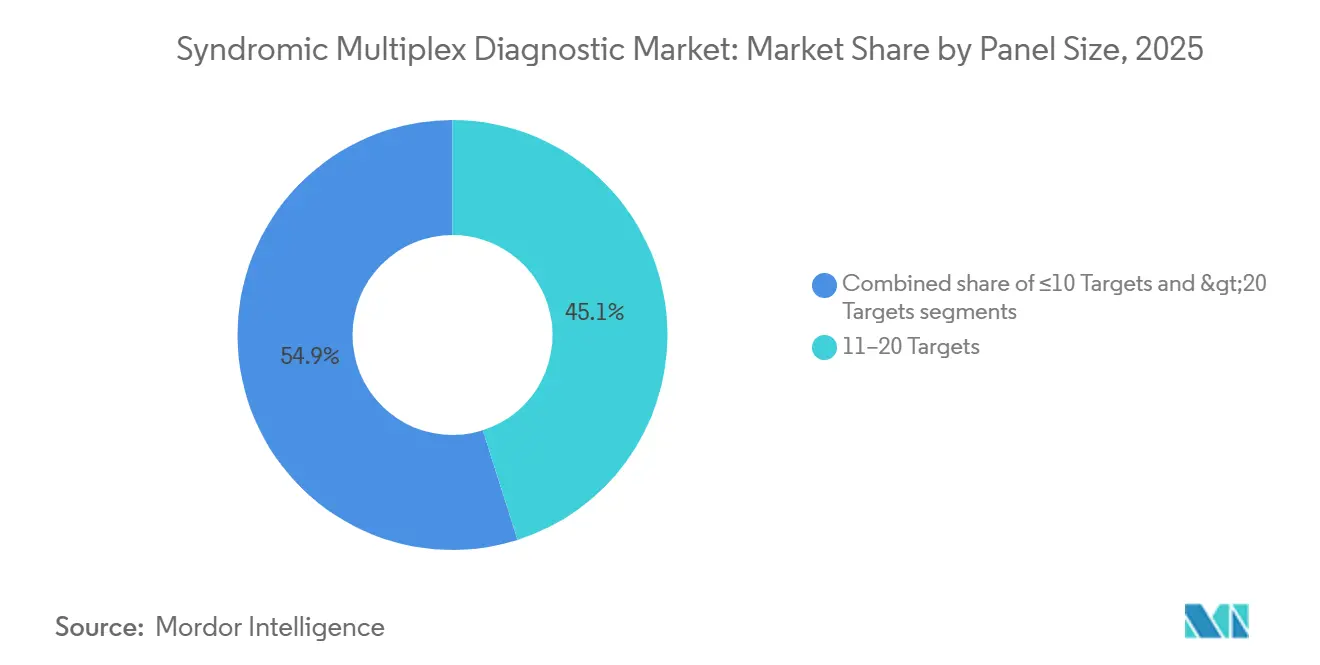

- By panel size, 11-20 target menus accounted for 45.15% of 2025 revenue, whereas panels exceeding 20 targets are growing at 9.82% CAGR.

- By end user, diagnostic laboratories captured 44.55% of 2025 demand, yet point-of-care clinics are the fastest-growing channel at 8.32% CAGR.

- By geography, North America generated 41.55% of 2025 revenue, but Asia-Pacific is the most dynamic region with 7.22% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Syndromic Multiplex Diagnostic Market Trends and Insights

Drivers Impact Analysis*

| Driver | % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising prevalence of infectious diseases | +1.2% | Global, highest in Asia-Pacific and Sub-Saharan Africa | Short term (≤ 2 years) |

| Growing adoption of molecular diagnostics | +1.5% | North America and Europe leading, Asia-Pacific accelerating | Medium term (2-4 years) |

| Expanding point-of-care testing infrastructure | +0.9% | North America rural areas, Asia-Pacific tier-2/3 cities, Latin America | Medium term (2-4 years) |

| Favorable reimbursement frameworks | +0.7% | North America, Western Europe | Long term (≥ 4 years) |

| AI-driven result interpretation | +0.5% | Global, concentrated in high-volume reference laboratories | Medium term (2-4 years) |

| Retail-pharmacy tele-diagnostic kiosks | +0.4% | North America, selected Asia-Pacific markets | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising Prevalence of Infectious Diseases

The co-circulation of influenza A/B, RSV, and SARS-CoV-2 compressed decision windows during the 2024-2025 season, prompting clinicians to favor multiplex respiratory panels that deliver results within 30-60 minutes. WHO laboratories logged 127 novel influenza reassortants in 2025, highlighting the risk that single-target PCR assays miss emerging strains[1]World Health Organization, “Global Influenza Surveillance and Response System,” who.int. Hospital emergency departments now initiate multiplex testing in 62% of U.S. cases versus 41% in 2023, reflecting antimicrobial stewardship goals that demand rapid rule-out of multiple pathogens. Enteric outbreaks are reinforcing this shift; the norovirus GII.4 Sydney wave caused 340 institutional clusters in Europe during early 2025, driving adoption of gastrointestinal panels that detect 22 pathogens. FDA granted nine Emergency Use Authorizations for new respiratory panels in 2025, accelerating market entry while maintaining clinical performance standards.

Growing Adoption of Molecular Diagnostics

Hospitals are replacing culture workflows with molecular panels to meet mandates that require pathogen identification within six hours of specimen collection. FDA clearance of Cepheid’s Xpert GI Panel in 2024 eliminated the 24-72 hour culture delay for gastrointestinal outbreaks. A 2025 Clinical Infectious Diseases study showed multiplex respiratory panels shortened hospital stays by 1.2 days and cut antibiotic use by 18%, saving USD 3,400 per patient despite the USD 150-200 test cost. Reference laboratories favor high-throughput systems such as Luminex NxTAG, which processes 96 samples in five hours. Regulatory harmonization in China accelerated adoption when the National Medical Products Administration fast-tracked 17 PCR assays in 2025.

Expanding Point-of-Care Testing Infrastructure

CLIA-waived instruments enable testing outside hospitals. bioMérieux’s BIOFIRE SPOTFIRE obtained waiver status in 2024 and is now installed at 450 CVS MinuteClinics, serving regions where patients previously traveled more than 25 miles for molecular testing. Walgreens began piloting 200 Cepheid Xpert Xpress systems in 2025, again targeting underserved counties. India’s Ministry of Health funded installations of 600 point-of-care molecular platforms across Uttar Pradesh and Bihar, prioritizing tuberculosis-burdened districts. FDA guidance issued in 2024 now requires 95% agreement with laboratory methods for panels seeking CLIA waiver, increasing validation rigor. Retail deployment is set to grow as reimbursement expands for pharmacy-originated diagnostics.

Favorable Reimbursement Frameworks for Multiplex Panels

Medicare boosted payment for CPT 87631-87633 by 4.2% in 2025 to acknowledge that syndromic panels cut downstream costs. Private payers mirrored this move; Anthem removed prior authorization for gastrointestinal panels in outpatient settings starting January 2025. In contrast, Germany reimburses respiratory panels at only EUR 35-45 (USD 38-49), slowing adoption in primary care. The reimbursement gap extends to emerging bloodstream infection assays, where 40% of U.S. commercial payers still deny coverage despite FDA clearance, forcing hospitals to absorb costs to meet sepsis protocols. FDA’s 2024 clinical-utility guidance now links reimbursement prospects to evidence of cost effectiveness, prompting vendors to include health-economic endpoints in pivotal trials.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High cost of syndromic test panels | -0.8% | Global, most acute in low- and middle-income countries | Short term (≤ 2 years) |

| Stringent regulatory approval processes | -0.6% | North America and Europe, tightening in Asia-Pacific | Medium term (2-4 years) |

| Supply-chain bottlenecks for mastermixes | -0.4% | Global, shortages in Asia-Pacific and Latin America | Short term (≤ 2 years) |

| Cybersecurity concerns around cloud platforms | -0.3% | Global, highest in regions with strict data-protection laws | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Cost of Syndromic Test Panels

U.S. list prices of USD 150-250 per respiratory panel remain a barrier in outpatient settings where reimbursement lags hospital rates by up to 40%. Affordability is even tougher in Asia-Pacific, where annual health spending per capita is USD 73 in India and USD 132 in Indonesia. Chinese manufacturers disrupt pricing by offering 15-target panels at USD 35-50, forcing multinationals to adopt tiered pricing that erodes margins. Multiplex instruments cost USD 15,000-75,000, challenging budgets at independent laboratories and rural hospitals. bioMérieux now leases SPOTFIRE units for USD 400 per month with five-year reagent commitments, yet such arrangements lock customers into single-vendor ecosystems.

Stringent Regulatory Approval Processes

FDA’s final rule ending enforcement discretion for laboratory-developed tests requires 300-500-specimen clinical studies for each syndromic panel, adding USD 0.5-1.2 million and 12-18 months to time-to-market. China’s revised 2025 guidelines demand validation against 50 clinical isolates per target, tripling workload relative to earlier rules. Europe’s In Vitro Diagnostic Regulation (IVDR) now mandates notified-body review for most multiplex assays, stretching approval queues even for established vendors[2]European Commission, “In Vitro Diagnostic Regulation,” ec.europa.eu . These requirements favor companies with large clinical-trial networks and squeeze smaller innovators toward partnership or acquisition.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type of Syndrome: Gastrointestinal Panels Gain Momentum

Respiratory panels captured 33.55% of syndromic multiplex diagnostic market share in 2025, underscoring entrenched seasonal demand. Gastrointestinal panels, however, are growing at 9.25% CAGR as infection-control budgets grapple with norovirus and Clostridioides difficile co-infections. The syndromic multiplex diagnostic market size allocated to bloodstream infection testing is smaller today but rising as hospitals aim to meet the one-hour sepsis bundle deadline. Central nervous system panels remain niche yet vital in meningitis workups, while urinary and sexually transmitted infection panels face reimbursement hurdles outside inpatient care.

Panel mix is shifting as enteric outbreaks highlight the risk of under-diagnosis. FDA clearance of the 14-target Cepheid Xpert GI panel in 2024 removed a bottleneck for rapid stool testing. Hospitals are adding bloodstream infection panels that identify 33 pathogens and resistance markers in under an hour, improving antimicrobial stewardship. CNS testing growth is capped by relatively low incidence but carries premium pricing that supports manufacturer margins. Vaginitis and complicated UTI panels may accelerate once payers expand coverage beyond symptomatic women in specialist clinics.

By Technology Platform: NGS Assays Challenge PCR Dominance

Multiplex PCR platforms produced 63.53% of 2025 revenue thanks to rapid 30-60 minute workflows. The syndromic multiplex diagnostic market size attributed to NGS is rising at 10.75% CAGR, reflecting its value in detecting novel pathogens such as the 2025 H5N1 spillover, confirmed 48 hours earlier by metagenomic sequencing than by PCR. Isothermal amplification is scaling in resource-constrained clinics due to low hardware complexity, while microarrays remain relevant in reference labs that value high sample throughput.

NGS adoption is accelerating as Oxford Nanopore streamlines six-hour runs that narrow the gap with PCR turnaround. Regulatory clarity came in 2024 when FDA issued analytical-sensitivity guidelines for metagenomic assays, reducing uncertainty for vendors. PCR leaders respond by adding broader target menus and AI-enabled readouts to defend share. Isothermal systems such as Abbott’s ID NOW deliver 13-minute flu results yet remain limited to three targets, reinforcing their role in focused point-of-care scenarios.

By Panel Size: Stewardship Programs Favor Larger Menus

Panels covering 11-20 targets dominated with 45.15% of 2025 revenue, balancing breadth and workflow simplicity. Panels exceeding 20 targets are expanding at 9.82% CAGR as hospitals seek simultaneous detection of resistance genes to guide therapy within the sepsis hour. Small panels with ≤10 targets continue to serve pharmacy clinics where cost and ease of use outweigh breadth.

Larger menus excel in critical care; a 33-target bloodstream panel cut time to appropriate therapy by 22 hours and lowered 30-day mortality by 14%. Mid-sized respiratory menus benefit from Medicare’s higher reimbursement code 87633, aligning economics with clinical value. FDA now asks manufacturers to justify each added target’s clinical utility, curbing the pursuit of kitchen-sink menus that inflate cost without proven benefit.

By End User: Point-of-Care Clinics Surge

Diagnostic laboratories retained 44.55% share in 2025 by processing high-volume panels during flu season. Point-of-care clinics, however, are growing at 8.32% CAGR as CLIA-waived platforms reach rural pharmacies. Hospitals remain pivotal for complex specimen types such as cerebrospinal fluid, while research institutes pilot metagenomic workflows that inform next-generation panel design.

Pharmacy adoption reshapes market logistics. CVS and Walgreens now compete with emergency departments for respiratory testing volume, capitalizing on 30-minute sample-to-result systems. Hospital labs counter by locating instruments directly in emergency departments, cutting 47 minutes in median turnaround relative to central labs. Research centers continue to evaluate customizable panels that link genomic surveillance with infection-control policy.

Geography Analysis

North America produced 41.55% of 2025 revenue, anchored by robust Medicare reimbursement and widespread CLIA-waived installations in retail settings. U.S. emergency departments reached 62% penetration for respiratory panels, though outpatient growth now leads incremental demand. Canada lags because provincial plans reimburse panels at roughly half U.S. rates, limiting usage to tertiary centers. Mexico’s IMSS allocated USD 50 million in 2025 for molecular infrastructure in 120 regional hospitals, signaling rising Latin American demand.

Asia-Pacific is the fastest-growing territory at 7.22% CAGR. China fast-tracked 17 multiplex assays in 2025, and domestic firms now supply 60-70% of provincial hospital demand at sharply lower prices. India earmarked USD 340 million to extend molecular diagnostics into tier-2 cities where hospital access is limited[3]Ministry of Health and Family Welfare, India, “National Health Programs,” mohfw.gov.in. Japan aligned PMDA rules with FDA 510(k) pathways, trimming duplication and accelerating foreign product launches. Australia’s Therapeutic Goods Administration granted provisional approvals for five CLIA-equivalent panels in 2025, improving rural healthcare access. South Korea leverages Seegene’s export strength to capture European share with cost-competitive respiratory menus.

Europe remains the second-largest region but grows slowly because reimbursement averages 60% below U.S. levels. France became the first EU country to reimburse gastrointestinal panels in early 2025, widening clinical adoption. The United Kingdom’s NHS Test and Trace program is piloting multiplex testing in 50 emergency departments with a target to reduce inappropriate antibiotic prescriptions by 20% by 2027. GCC countries fund hospital expansions that include molecular labs, while Brazil’s ANVISA approvals outpace reimbursement, leaving private hospitals as the main purchasers.

Competitive Landscape

Market concentration is moderate; the top five companies—bioMérieux, Danaher (Cepheid), DiaSorin (Luminex), Roche, and Abbott—account for a large share but face intensifying price pressure from Asia-Pacific entrants offering 40-60% cheaper panels. bioMérieux consolidated its position through the BioFire Diagnostics acquisition, while Roche integrated GenMark’s ePlex platform to deepen assay menus. Cepheid and Walgreens launched a retail testing pilot in 2025 that shifts volume away from hospital labs, forcing incumbents to match throughput and ease of use.

Technology drives competition. Seegene’s MuDT PCR detects 25 targets in one reaction and undercuts list prices by 30%, gaining European hospital contracts. QuantuMDx’s 15-minute Q-POC cartridge challenges existing CLIA-waived devices in urgent care settings. Midsize innovators gravitate toward bloodstream infection and resistance panels, where only three FDA-cleared assays exist and clinical need is acute. Patent cliffs loom; Luminex’s microarray portfolio begins to expire from 2027, opening space for new multiplex chemistries.

Strategic moves focus on vertical integration and manufacturing scale. SD Biosensor’s 2024 purchase of Meridian Bioscience added lyophilized mastermix capacity and a 90-country sales network. MiRXES is commercializing 40-target respiratory panels built on proprietary ID3EAL chemistry, aiming at Southeast Asian hospitals underserved by Western brands. Instrument bundling with multi-year reagent contracts helps incumbents fend off price competition but locks laboratories into single-supplier ecosystems.

Syndromic Multiplex Diagnostic Industry Leaders

bioMérieux

Danaher (Cepheid)

DiaSorin S.p.A (Luminex)

Abbott

F. Hoffmann-La Roche

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- November 2025: DiaSorin secured FDA 510(k) clearance for a new syndromic respiratory disease test.

- September 2025: QIAGEN launched QIAstat-Dx Rise, an automated syndromic platform with high throughput and simplified workflow.

Global Syndromic Multiplex Diagnostic Market Report Scope

As per the scope of this report, a syndromic multiplex diagnostic test employs testing of various pathogens in a single test reaction and helps healthcare providers to deliver efficient medications in proper time by minimizing uncertainty and mistakes that occur while testing for infection. The syndromic multiplex diagnostic test gives more accurate, realistic, and comprehensive results in critical care.

The syndromic multiplex diagnostic market is segmented by type of syndrome, technology platform, panel size, end-user, and geography. By type of syndrome, the market is categorized into respiratory, gastrointestinal, central nervous system, bloodstream/sepsis, and cUTI & STDs. By technology platform, it is divided into multiplex PCR, isothermal amplification, microarray-based, and NGS-based. Based on panel size, the segmentation includes ≤10 targets, 11–20 targets, and >20 targets. By end-user, the market is segmented into hospitals, diagnostic laboratories, point-of-care/retail clinics, and research institutes. Geographically, the market is analyzed across North America, Europe, Asia-Pacific, the Middle East and Africa, and South America. The market report also covers the estimated market sizes and trends for 17 different countries across major regions, globally. The report offers the value (in USD) for the above segments.

| Respiratory |

| Gastrointestinal |

| Central Nervous System |

| Bloodstream / Sepsis |

| cUTI & STDs |

| Multiplex PCR |

| Isothermal Amplification |

| Microarray-based |

| NGS-based |

| Less than 10 Targets |

| 11-20 Targets |

| Greater Than 20 Targets |

| Hospitals |

| Diagnostic Laboratories |

| Point-of-Care / Retail Clinics |

| Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| Australia | |

| South Korea | |

| Rest of Asia-Pacific | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East and Africa | |

| South America | Brazil |

| Argentina | |

| Rest of South America |

| By Type of Syndrome | Respiratory | |

| Gastrointestinal | ||

| Central Nervous System | ||

| Bloodstream / Sepsis | ||

| cUTI & STDs | ||

| By Technology Platform | Multiplex PCR | |

| Isothermal Amplification | ||

| Microarray-based | ||

| NGS-based | ||

| By Panel Size | Less than 10 Targets | |

| 11-20 Targets | ||

| Greater Than 20 Targets | ||

| By End-User | Hospitals | |

| Diagnostic Laboratories | ||

| Point-of-Care / Retail Clinics | ||

| Research Institutes | ||

| Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| Australia | ||

| South Korea | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East and Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What CAGR is forecast for the syndromic multiplex diagnostic market between 2026 and 2031?

The market is projected to grow at 5.13% CAGR over 2026-2031, rising from USD 3.10 billion in 2026 to USD 3.98 billion by 2031.

Which syndrome panel holds the largest share today?

Respiratory panels led with 33.55% of 2025 revenue due to routine flu and RSV screening in hospitals.

Why are gastrointestinal panels growing faster than other segments?

Hospitals are prioritizing enteric pathogen surveillance as norovirus and Clostridioides difficile co-infections strain infection-control budgets, driving a 9.25% CAGR through 2031.

How are point-of-care clinics affecting market dynamics?

Retail pharmacies and urgent-care centers are deploying CLIA-waived instruments, making point-of-care clinics the fastest-growing end-user segment at 8.32% CAGR.

Which technology is challenging PCR's dominance?

Next-generation sequencing-based assays, expanding at 10.75% CAGR, can identify novel or unexpected pathogens that fixed-target PCR panels may miss.

What is the biggest restraint on market growth?

High panel costs, especially in low- and middle-income countries, are subtracting an estimated 0.8 percentage point from the overall CAGR.

Page last updated on: