Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

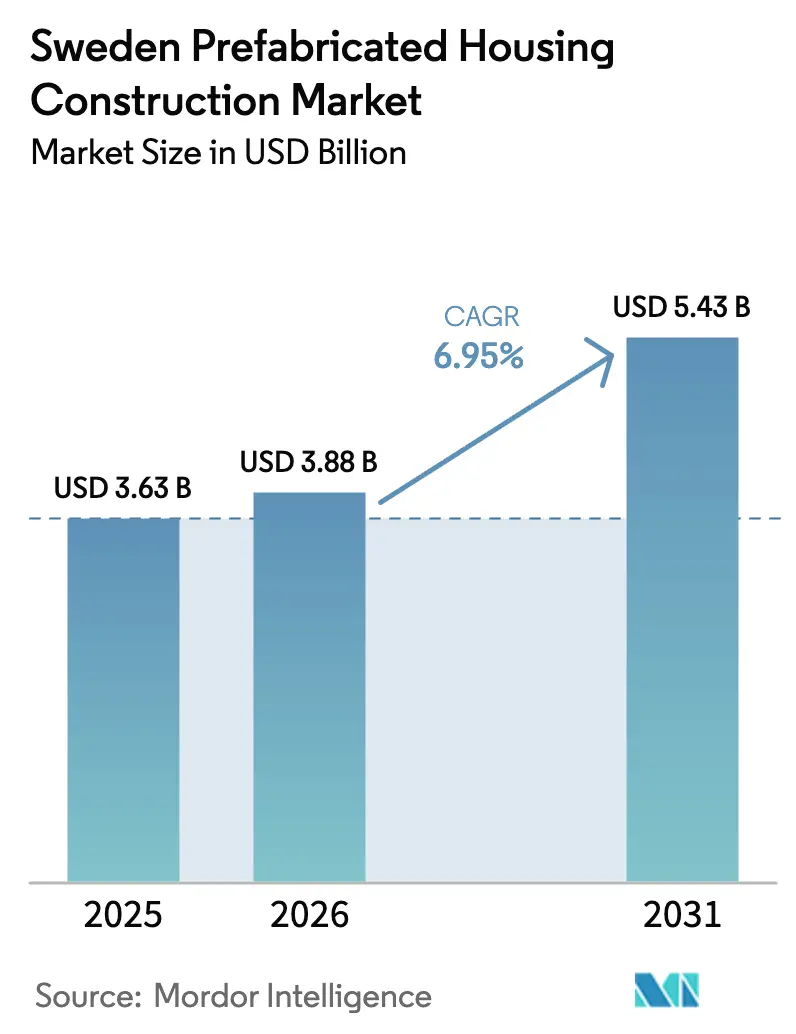

| Base Year Market Size (2025) | USD 3.63 Billion |

| Market Size (2026) | USD 3.88 Billion |

| Market Size (2031) | USD 5.43 Billion |

| Growth Rate (2026 - 2031) | 6.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sweden Prefabricated Housing Construction Market Analysis by Mordor Intelligence

The Sweden Prefabricated Housing Construction Market size is projected to expand from USD 3.63 billion in 2025 and USD 3.88 billion in 2026 to USD 5.43 billion by 2031, registering a CAGR of 6.95% between 2026 to 2031.

Accelerated adoption of factory-controlled production—driven by tight labor markets, stricter energy codes, and municipal fast-track housing targets—anchors sustained expansion despite the financing headwinds that slowed conventional site-built projects in 2024 and 2025. Timber retains an overwhelming lead because Sweden’s vertically integrated forestry chain secures stable raw-material pricing, while cross-laminated timber (CLT) volumetric systems satisfy embodied-carbon caps embedded in Boverket’s climate-declaration regime[1]Boverket, “Building Regulations (BBR),” boverket.se. Modular delivery compresses permit-to-occupancy schedules by 25–40%, a decisive advantage in Stockholm, Gothenburg, and Malmö, where rental unit wait lists exceed 9 years. Digitalization remains uneven, yet early movers connecting BIM models directly to CNC lines report double-digit reductions in rework, cementing an innovation wedge that late adopters will struggle to close over the forecast horizon.

Key Report Takeaways

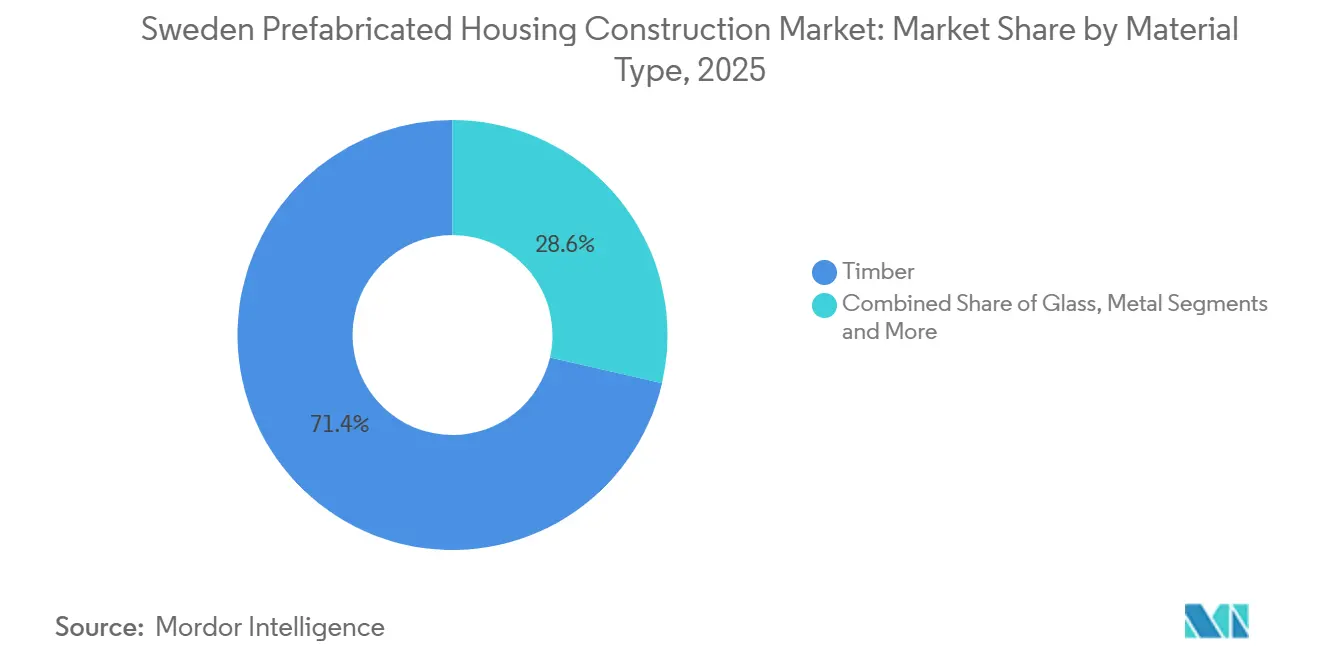

- By material, timber captured 71.4% of the Sweden prefabricated housing construction market share in 2025, while glass is forecast to post the fastest 7.81% CAGR to 2031.

- By housing type, single-family accounted for 76.9% of volume in 2025, whereas multi-family is projected to expand at an 8.09% CAGR through 2031.

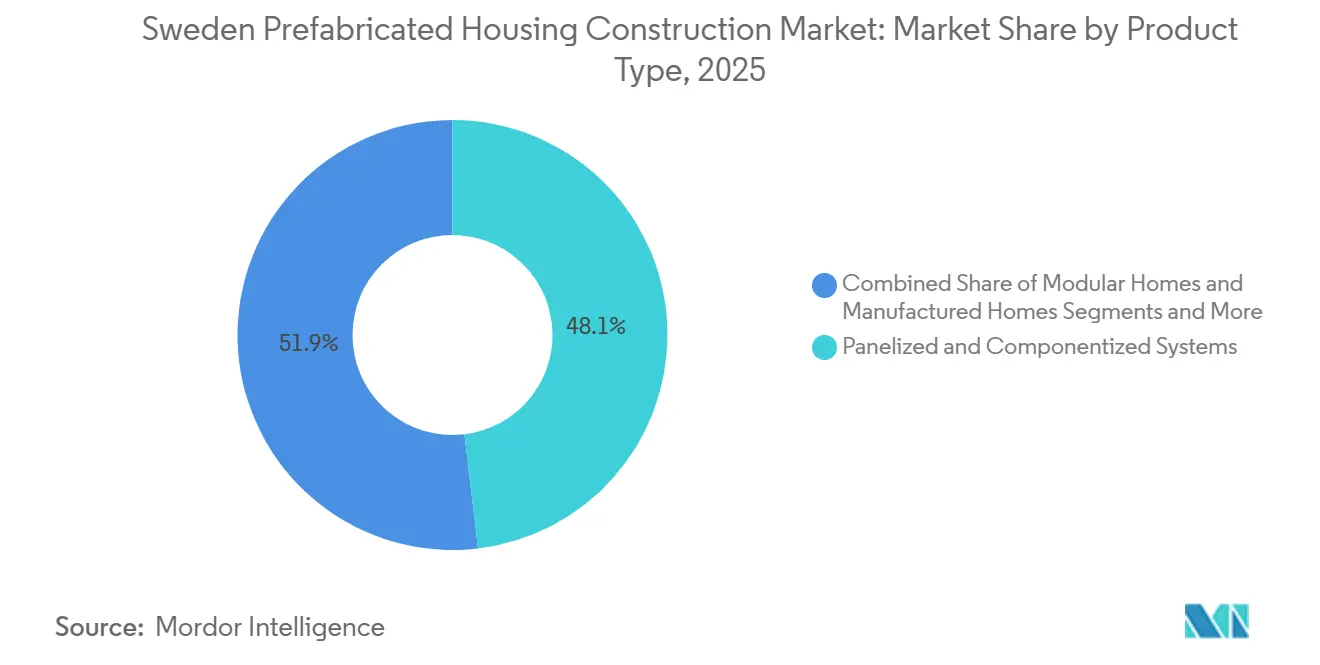

- By product type, panelized and componentized systems led the Sweden prefabricated housing construction market with 48.1% of the market share in 2025; modular homes will grow the fastest at an 8.31% CAGR to 2031.

- By city, Stockholm accounted for 33.7% of the 2025 volume, and Malmö has the highest 8.64% CAGR outlook to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Sweden Prefabricated Housing Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Industrialized timber tradition | +1.8% | Västra Götaland, Norrbotten, Västerbotten | Long term (≥ 4 years) |

| Tight energy codes & net-zero goals | +1.5% | Stockholm, Gothenburg, Malmö | Medium term (2–4 years) |

| Labor shortages & high on-site wages | +1.4% | Nationwide, acute in Stockholm and Gothenburg | Short term (≤ 2 years) |

| Urban-infill municipal pipelines | +1.2% | Stockholm, Malmö, Gothenburg, Uppsala, Linköping, Örebro | Medium term (2–4 years) |

| Digital design and DfMA standardization | +1.0% | National, led by Peab, NCC, Skanska, Randek | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Strong Tradition in Industrialized Timber Housing Enabling Scale and Quality

Swedish sawmills processed 74 million m³ of roundwood in 2024, with half converted to construction-grade timber, ensuring predictable input costs for volumetric plants that weathered the 2021-2022 steel and concrete price spikes. CLT capacity rose roughly 15% between 2023 and 2025, giving domestic producers a structural cost edge over import-dependent rivals exposed to spot-log volatility that saw prices jump from USD 47.0 per m³ in 2020 to USD 94.5 per m³ by Q4 2024. Factory-controlled moisture regimes and CNC precision minimize on-site remedial work, lowering warranty claims and life-cycle costs prized by municipal buyers. Timber modules also sequester 200-300 kg of CO₂ per m³, supporting climate-declaration compliance that became mandatory for buildings over 1,000 m² in 2022. These combined cost, quality, and regulatory advantages ensure timber remains the anchor material powering the Sweden prefabricated housing construction market.

Tight Energy Codes and Net-Zero Goals Favor High-Performance Factory-Built Envelopes

Boverket’s Building Regulations cap specific energy use at 65–85 kWh/m²-year, with Stockholm and other major municipalities enforcing thresholds up to 20% tougher in land-allocation tenders. Factory environments enable airtightness checks and thermal-bridge inspections that are nearly impossible outdoors in Sweden’s variable climate. Heimstaden Bostad’s 2024 deliveries cut dwelling footprints by 20% through standardized bathroom-pods, assisting Miljöbyggnad Silver certification that outperforms legal energy minimums by 20%[2]Heimstaden Bostad, “Annual, Governance, and Sustainability Report 2024,” heimstadenbostad.com. Integrating PV arrays and heat pumps during production trims retrofit costs later and aligns developments with EU Taxonomy green-building criteria. As Sweden targets a fossil-fuel-free status by 2040, factory-built shells offer the clearest path to comply, directly accelerating the Sweden prefabricated housing construction market.

Labor Shortages and High Site Wages Push Builders Toward Offsite Productivity Gains

Carpenter, electrician, and plumber vacancies surpassed 8% in Sweden’s big-city labor markets during 2024–2025, while site wages rose 4–5% each year, squeezing contractor margins. Prefabrication transfers up to 80% of labor hours into controlled plants where productivity per worker is 20–30% higher, thanks to ergonomic stations and parallel tasking. Lindbäcks Bygg shed roughly 100 positions during its 2022 turnaround, then pivoted to higher-margin municipal contracts that depend on its volumetric edge. Municipalities now weigh total life-cycle outlays instead of headline bid prices, tilting awards toward bidders who demonstrate cost certainty through factory labor smoothing. This wage arbitrage reinforces the economic rationale for the Sweden prefabricated housing construction market even as financing conditions fluctuate.

Urban Infill and Municipal Pipelines Suited to Rapid Modular Delivery

Stockholm’s City Plan earmarks 140,000 new homes over 2010–2030, with the Stockholmshusen program standardizing block designs to trim planning cycles[3]City of Stockholm, “Stockholm City Plan,” City of Stockholm, uitp.org. Snabba hus temporary housing targets 18–30-year-olds, explicitly favoring modular units that can be redeployed post-permit expiry. Starts in Stockholm County fell 46% year-over-year in Q1 2025, tightening supply and rewarding firms that can deliver within 18 months. Malmö and Gothenburg issue tenders with fixed schedule clauses that only prefab suppliers can satisfy, strengthening their role in de-risking municipal pipelines. The Sweden prefabricated housing construction market thus becomes a critical lever for cities battling housing shortages without stretching public budgets.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated financing & material costs | -0.9% | Nationwide, sharpest in cost-sensitive single-family segments | Short term (≤ 2 years) |

| Planning/heritage constraints | -0.6% | Stockholm inner city, Gothenburg Haga, Malmö Gamla Staden | Medium term (2–4 years) |

| Capacity bottlenecks & northern logistics | -0.4% | Norrbotten, Västerbotten, Jämtland | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Elevated Financing and Material Costs Challenging Price Parity in Some Segments

The Riksbank lifted its policy rate from 0% in 2022 to 4.0% by mid-2023, before easing to 2.5% in late 2025, yet new-build mortgage rates still hover at 4.5-5.5%, stalling starts in cost-sensitive single-family subdivisions. Prefab’s capital intensity magnifies interest-expense exposure relative to incremental site-built workflows. Material spikes compounded the strain, with timber and reinforcement-steel prices rising 76-83% and 64%, respectively, during 2021-2024. Skanska’s BoKlok factory logged a USD 57.1 million loss in 2024, prompting its USD 9.5 million sale to Surewood in February 2025. Unless input costs stabilize, some buyers revert to lowest-price conventional bids, slowing near-term uptake in the Sweden prefabricated housing construction market.

Planning and Heritage Constraints Slowing Approvals in Dense Areas

Sweden’s Planning and Building Act devolves detailed plans to 290 municipalities, leading to inconsistent façade, height, and material rules that complicate standardized module designs. Heritage districts like Stockholm’s Gamla Stan and Gothenburg’s Haga impose façade color and window-grid mandates that force bespoke engineering, eroding prefab economies of scale. Appeals can stretch building-permit decisions to 12 months, adding carrying costs for factories holding finished modules. Atrium Ljungberg’s Stockholm Wood City required multi-year negotiations to reconcile timber high-rise ambitions with fire-safety and aesthetic codes. Such procedural drag tempers the urban-core potential of the Sweden prefabricated housing construction market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Timber Secures Long-Term Cost and Carbon Advantage

Timber controlled 71.4% of the 2025 volume, anchoring the Sweden prefabricated housing construction market thanks to local forest resources and deep-rooted engineering know-how. Martinsons, with annual sales near USD 92 million, operates Sweden’s largest CLT press line, feeding domestic plants and exports to Germany and the United Kingdom. Timber’s locked-in pricing and embodied-carbon benefits dovetail with climate-declaration rules that became binding in 2022, pushing municipalities to favor carbon-storing assemblies.

Glass, the fastest-growing segment, will expand at a 7.81% CAGR by 2031 as dense urban infill seeks daylight-rich façades compatible with Boverket’s low-energy envelopes. Hybrid timber-concrete floors retain relevance in mid-rise apartment blocks where acoustic and fire-code demands peak, but concrete’s share remains in the mid-teens. Metals such as galvanized steel frame coastal builds yet occupy single-digit volume. Given these dynamics, timber’s dominance in the Sweden prefabricated housing construction market looks durable, reinforced by ongoing investments like Derome’s WEINMANN line capable of 1,500 units per year.

By Housing Type: Multi-Family Rises as Municipalities Target Rental Gaps

Single-family modules represented 76.9% of 2025 deliveries, upheld by owner-occupier preferences and municipal land-release policies that still favor detached homes around Sweden’s commuter belts. However, multi-family projects will log the segment-leading 8.09% CAGR through 2031 as public landlords confront record rental wait-lists exceeding nine years in Greater Stockholm.

Peab’s 2025-2026 pipeline in Uppsala, Lund, and Gothenburg showcases volumetric apartment blocks that cut onsite person-hours by one-third and realize earlier rental cash flows. NCC Complete echoed demand yet flagged financing delays that dampened Q3 2025 bookings. This bifurcation yields a Sweden prefabricated housing construction market split: capital-rich developers commit to build-to-rent ventures, while cash-tight players retreat to low-risk single-family lots until interest rates normalize.

By Product Type: Modular Homes Capture Schedule-Driven Orders

Panelized systems accounted for 48.1% of the Sweden prefabricated housing construction market size in 2025 since wall and roof cassettes fit seamlessly within established site logistics. Modular homes, delivered 80–95% complete, now lead growth at an 8.31% CAGR thanks to their 30–40% program-time compression.

Heimstaden’s standardized bathroom-pod roll-out illustrates hybridization: panelized envelopes paired with volumetric service cores achieve the best trade-off between transport efficiency and quality assurance. Manufactured park homes remain niche, serving seasonal cabin buyers. As digital design proliferates, module geometry standardization will intensify, nudging the Sweden prefabricated housing construction market toward higher volumetric penetration without abandoning flat-pack flexibility.

Geography Analysis

The south-central triangle of Stockholm, Gothenburg, and Malmö generated roughly 60% of Sweden’s prefabricated housing deliveries in 2025, reflecting acute urban shortages and municipal procurement rules that privilege speed, embodied-carbon cuts, and standardized designs. Stockholm’s 33.7% share stems from its 140,000-home target and programs like Snabba hus that mandate rapid modular builds for young adults, yet permit backlogs trimmed 2025 starts, opening share for rival regions.

Malmö enjoys the forecast high-water 8.64% CAGR to 2031 as lower land costs and the Øresund-region labor mobility foster modular social-housing deals. Gothenburg’s mid-teens slice grows steadily, fueled by West Link rail access and university campus expansions. Secondary cities - Uppsala, Linköping, Örebro, Västerås - together approach 20% share, driven by student-housing demand and municipal land allocations that welcome repeatable prefab clusters.

In the north, timber-rich counties like Norrbotten wrestle with logistic surcharges that raise delivered costs by up to 15%. Lindab’s 2024 plant consolidation from Luleå to Piteå epitomizes network redesigns to serve sparse markets more efficiently. Despite these hurdles, local authorities value prefab’s winter-proof production when site work freezes. Overall, geographic diversification cushions the Sweden prefabricated housing construction market against Stockholm’s cyclical permitting swings, spreading growth across university towns and cross-border labor corridors.

Competitive Landscape

Sweden’s prefabricated housing construction market is moderately fragmented, featuring integrated timber giants such as Derome, Martinsons, and Lindbäcks alongside contractor-affiliated modular units at Peab, NCC, and Veidekke. The 2022–2024 rate shock forced a pivot from capacity additions to margin defense, exemplified by Skanska’s USD 9.5 million divestiture of its BoKlok factory after a USD 57.1 million 2024 loss. Players now prioritize design-for-manufacture-and-assembly templates, bathroom-pod standardization, and selective municipal tenders to protect profitability.

Digital maturity separates leaders from laggards. Large contractors integrate BIM data straight into CNC lines, shaving weeks off delivery and minimizing rework. Smaller family-owned firms still rely on 2D shop drawings, limiting scale and exposing them to quality-assurance penalties in energy-tight projects. Randek and other equipment vendors capitalize by offering turnkey automation packages that let regional manufacturers upgrade without greenfield costs.

Regulatory barriers raise entry costs: since 2022, Boverket requires lifecycle-carbon disclosures for buildings over 1,000 m², advantaging timber experts armed with third-party environmental product declarations. Concrete-oriented rivals scramble to blend hybrid systems or risk procurement exclusion. Ongoing consolidation is expected as interest-rate normalization and energy-code tightening reward the financially and technologically prepared, reinforcing a flight-to-quality within the Sweden prefabricated housing construction market.

Sweden Prefabricated Housing Construction Industry Leaders

Derome AB

Martinson Group AB

Lindbacks

Trivselhus AB

Gotenehus AB

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: Skanska sold its BoKlok modular factory to Surewood Housing for USD 9.5 million after reporting a USD 57.1 million loss in 2024.

- October 2024: Atrium Ljungberg began building Brf Kulturarvet, the first residential block in Stockholm Wood City, a multi-story CLT landmark.

- April 2024: Heimstaden Bostad delivered 800 prefab units featuring factory-built bathroom pods, cutting unit footprints by 20% and achieving Miljöbyggnad Silver.

Sweden Prefabricated Housing Construction Market Report Scope

Prefabricated homes, often referred to as prefab homes, are primarily manufactured in advance offsite, then delivered and assembled on-site.

This report covers market insights, such as market dynamics, drivers, restraints, opportunities, technological innovation, its impact, Porter's five forces analysis, and the impact of COVID-19 on the market. In addition, the report provides company profiles to understand the competitive landscape of the market.

Sweden's prefabricated housing market is segmented by material and by sector. By material, the market is segmented by concrete, glass, metal, timber, and other materials types. By application, the market is segmented by residential, commercial, and other applications ( industrial, institutional, and infrastructure).

The report offers the market sizes and forecasts for Sweden's prefabricated housing market in value (USD) for all the above segments.

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Housing Type

| Single-Family |

| Multi-Family |

By Product Type

| Modular Homes |

| Panelized & Componentized Systems |

| Manufactured Homes |

| Other Prefab Types |

By City

| Stockholm |

| Gothenburg |

| Malmö |

| Uppsala |

| Other Cities |

| By Material Type | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Housing Type | Single-Family |

| Multi-Family | |

| By Product Type | Modular Homes |

| Panelized & Componentized Systems | |

| Manufactured Homes | |

| Other Prefab Types | |

| By City | Stockholm |

| Gothenburg | |

| Malmö | |

| Uppsala | |

| Other Cities |

Key Questions Answered in the Report

What is the current value of the Sweden prefabricated housing construction market?

The market was valued at USD 3.88 billion in 2026.

How fast is Sweden’s prefabricated housing sector expected to grow?

It is forecast to register a 6.95% CAGR between 2026 and 2031.

Which material dominates Swedish prefab housing?

Timber commands 71.4% share in 2025 thanks to abundant local forestry and favourable carbon regulations.

Why are modular homes gaining traction in Sweden?

Fully volumetric units can cut permit-to-occupancy schedules by up to 40%, helping cities address housing shortages quickly.

Which Swedish city shows the fastest prefab housing growth?

Malmö is projected to post an 8.64% CAGR through 2031 due to cross-border labor flows and modular social-housing demand.

What recent strategic move did Skanska make in this space?

Skanska sold its loss-making BoKlok modular factory to Surewood Housing for USD 9.5 million in February 2025.

Page last updated on: