Market Overview

| Study Period | 2020 - 2031 |

|---|---|

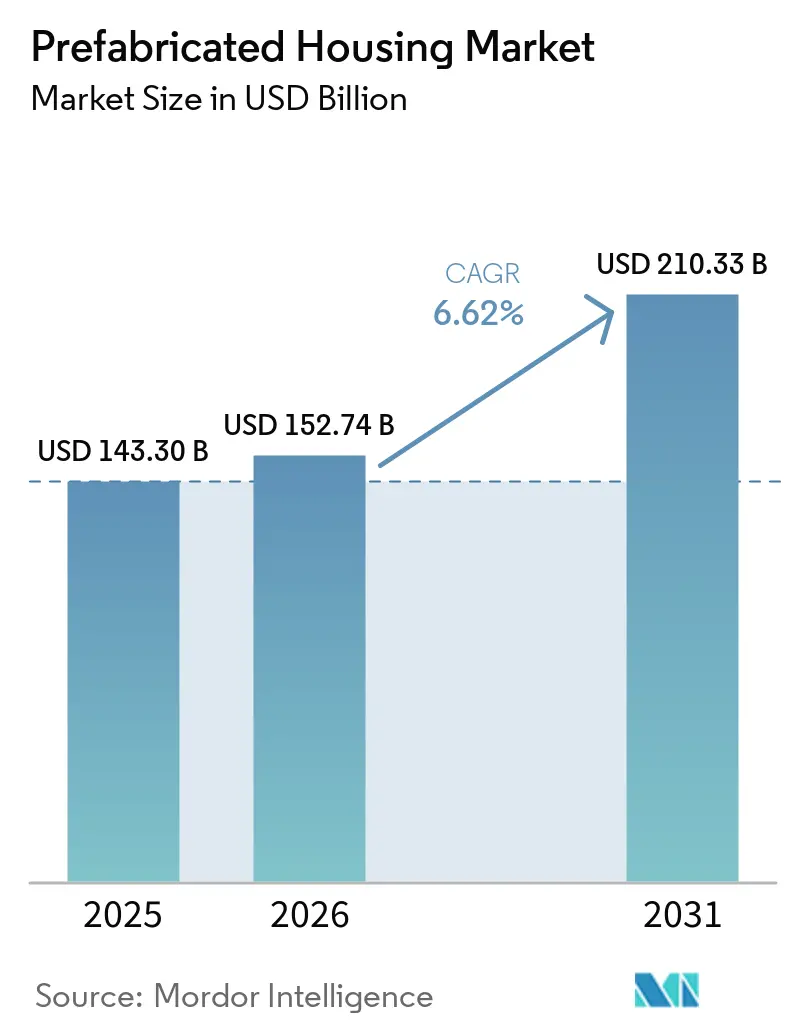

| Market Size (2026) | USD 152.74 Billion |

| Market Size (2031) | USD 210.33 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Fastest Growing Market | Middle East and Africa |

| Largest Market | Asia Pacific |

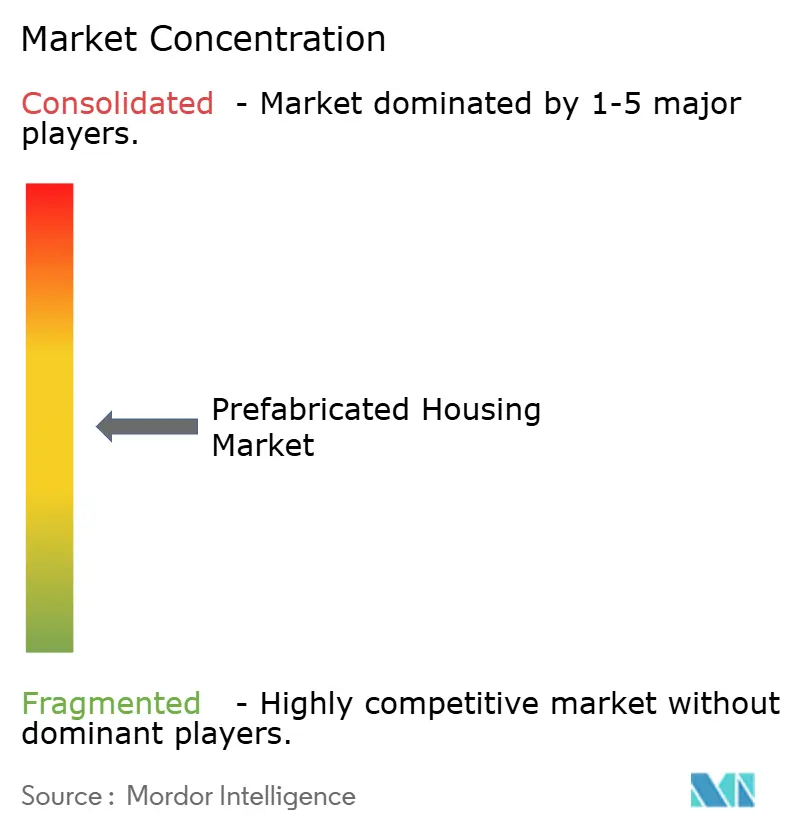

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Prefabricated Housing Market Analysis by Mordor Intelligence

The prefabricated housing market size in 2026 is estimated at USD 152.74 billion, growing from 2025 value of USD 143.3 billion with 2031 projections showing USD 210.33 billion, growing at 6.62% CAGR over 2026-2031. Rapid adoption of off-site manufacturing, policy incentives that shorten approval cycles, and steady material innovation are expanding the prefabricated housing market across income bands and geographies. Governments in Canada, Australia, and the United States are channeling public funds and code updates toward standardized factory-built homes that trim build times and cut life-cycle energy use. Labor shortages, estimated to affect 68% of construction firms, and higher interest in net-zero structures continue to shift demand from site-built to plant-assembled units. Technology adoption—from Building Information Modeling (BIM) through LiDAR-guided inspection—further solidifies quality control and cost predictability, reinforcing the competitive edge of the prefabricated housing market[1]Government of Canada, “Housing Design Catalogue,” canada.ca.

Key Report Takeaways

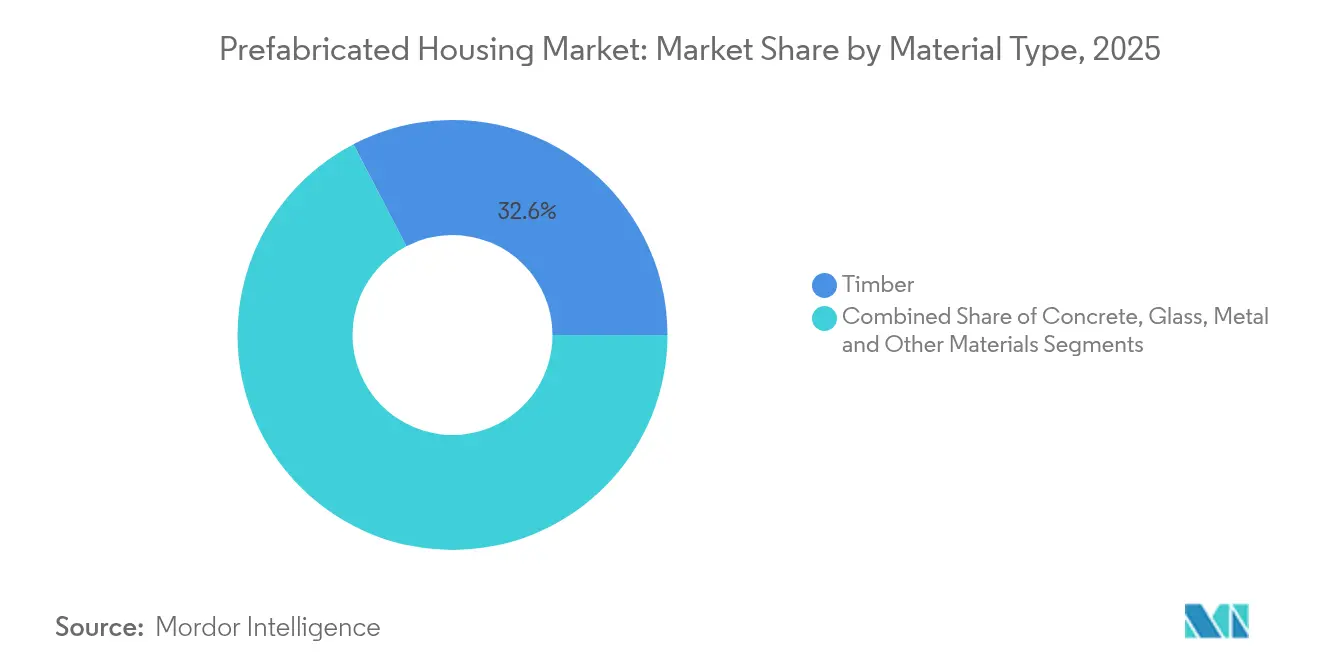

- By material type, timber captured 32.62% of prefabricated housing market share in 2025, and the same segment is advancing at a 7.18% CAGR through 2031.

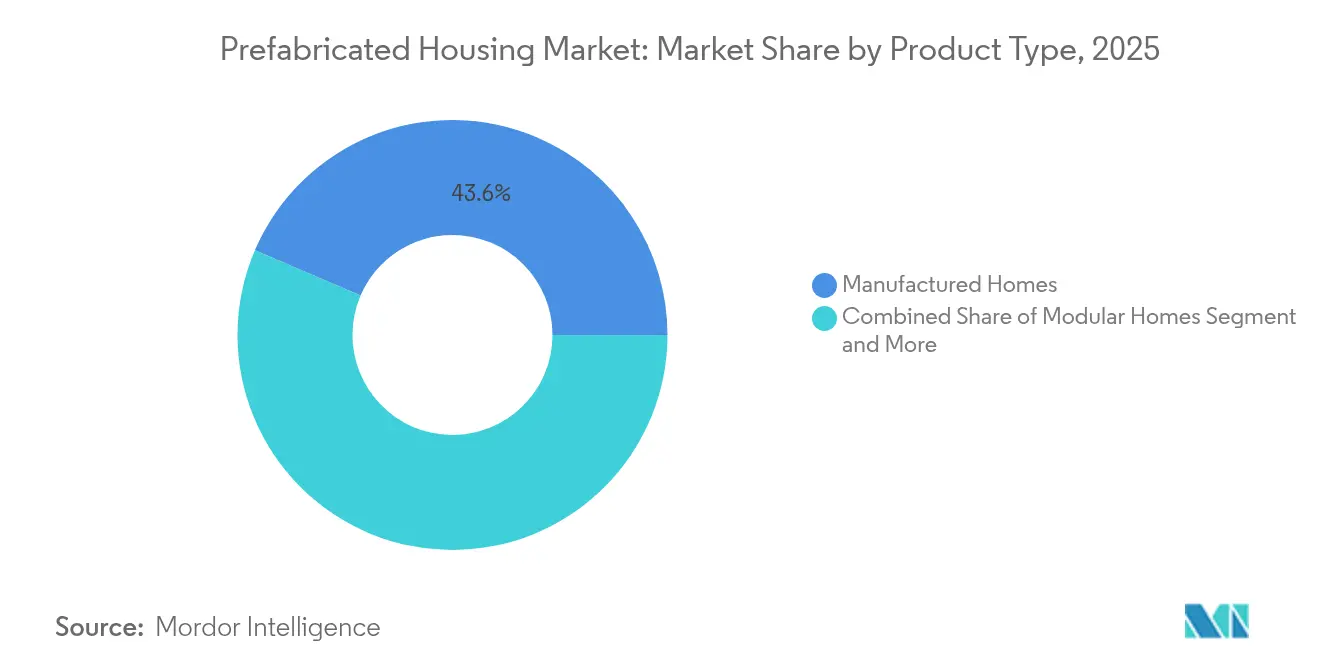

- By product type, manufactured homes held 43.55% share of the prefabricated housing market size in 2025, while modular homes are projected to expand at a 7.05% CAGR to 2031.

- By application, single-family construction accounted for 57.64% share of the prefabricated housing market size in 2025; multi-family projects are growing at a 6.88% CAGR through 2031.

- By geography, Asia-Pacific led with 35.88% revenue share in 2025, whereas the Middle East & Africa region is on track for the fastest 7.29% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Prefabricated Housing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Government push for affordable & sustainable housing | +1.8% | North America & Europe | Medium term (2-4 years) |

| Accelerating urbanization & housing shortfall | +1.5% | Asia-Pacific, MEA, Latin America | Long term (≥ 4 years) |

| Cost-efficient off-site manufacturing | +1.2% | Global | Short term (≤ 2 years) |

| Tech leap: BIM, 3-D printing & automated factories | +0.9% | North America & EU | Medium term (2-4 years) |

| ESG-linked green-building mandates | +0.8% | Europe & North America | Long term (≥ 4 years) |

| Disaster-rebuild & remote-work micro-units | +0.6% | North America & Australia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Government Push for Affordable & Sustainable Housing

Targeted public funding is reshaping market adoption, shifting prefab from a cost-driven option to a policy-backed priority. Canada’s Build Canada Homes program earmarks USD 25 billion in loans and USD 1 billion in equity, leveraging bulk orders that lower unit costs by 20%. The United States now ties Federal Housing Administration financing to the 2021 International Energy Conservation Code, adding USD 7,229 per unit in upfront costs yet saving USD 963 annually on energy. Australia committed USD 54 million to close a 62,000-home gap while standardizing certification, accelerating plant output. Sweden’s 84% prefab penetration shows how incentives and capacity building can synchronize supply and demand. Together these measures illustrate a durable shift toward factory-assembled units that meet strict sustainability targets.

Accelerating Urbanization & Housing Shortfall

Rapid urban growth compresses project timelines, intensifying demand for factory-assembled homes that can be erected in half the time of site-built equivalents. Vermont’s requirement for up to 36,000 new homes by 2029 mirrors wider North American shortages and positions modular solutions as a scalable fix that cuts construction costs by 20%. At the production level, Onx Homes’ Florida plant delivers components for 1,000 dwellings a year, shrinking site schedules from eight months to 30 days. In disaster-hit Los Angeles, modular micro-units helped wildfire victims return faster than conventional rebuilds. Hong Kong’s Transitional Housing Programme, with more than 21,000 units built via Modular Integrated Construction, underscores prefab’s advantage where land is scarce. These examples reveal how urban density and urgency are reinforcing demand for the prefabricated housing market.

Cost-Efficient Off-Site Manufacturing vs. Conventional Build

Plant production lowers labor reliance, curbs waste, and locks in repeatable quality even though front-loaded capital costs can be high. McKinsey studies show up to 20% cost savings and 50% schedule gains, amounting to potential annual savings of USD 20 billion across the United States and Europe by 2030. In high-labor-cost markets, general contractors report tangible benefits in safety, logistics, and waste reduction. Chinese case studies find greater upfront spending is offset by lifetime savings as faster turnarounds free capital for new projects. Hybrid systems like Plant Prefab’s blend of panels and modules strike a balance between cost and design flexibility. The aggregate effect sustains the prefabricated housing market on a strong cost-competitiveness footing.

Tech Leap: BIM, 3-D Printing & Automated Factories

Digital tools and robotics are transforming prefab from standardized boxes into customizable, high-precision dwellings. BIM enables seamless data flow from design to assembly, reducing errors while trimming lifecycle costs. 3-D printers can complete a 185 m² house in five workdays with fewer crew members, cutting up to 45% of expenses. LiDAR-based inspection offers 0.7 mm accuracy for structure and 0.9 mm for MEP, replacing labor-intensive checks. IoT-linked autonomous robots map foundations within ±15 mm tolerances, slashing layout errors. Decentralized “micro-factory” concepts such as Cuby’s mobile plants lower logistics expense by bringing production closer to the jobsite. These upgrades consolidate the technology moat that propels the prefabricated housing market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High logistics cost for oversized modules | -1.4% | Global, particularly affecting cross-border trade | Short term (≤ 2 years) |

| Scarcity of skilled prefab fabricators & installers | -0.9% | North America & Europe, expanding to APAC | Medium term (2-4 years) |

| Fragmented cross-border building codes slow approvals | -0.7% | Global, with acute impact on international trade corridors | Medium term (2-4 years) |

| Seismic- & cyclone-resilience perception gaps | -0.5% | Seismic zones (APAC, Americas West Coast) & hurricane-prone regions (North America, Caribbean) | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Logistics Cost for Oversized Modules

Transporting large modules adds 15-25% to project budgets when shipping dimensions exceed standard limits. Specialized trailers, permits, and escort requirements raise costs, particularly across borders where divergent road standards complicate routing. Australia’s dependence on Chinese imports shows supply risks; 70% of prefab inflow faces extra handling and compliance checks that slow delivery. Infrastructure gaps, such as low bridge clearances or weight restrictions in emerging regions, force manufacturers to down-size modules, eroding economies of scale. For remote areas, freight expenses can outstrip manufacturing savings, making localized micro-factories or panelized systems more viable. Unless route optimization and regional fabrication expand, logistics will restrain the prefabricated housing market’s full potential.

Scarcity of Skilled Prefab Fabricators & Installers

More than one-fifth of the construction workforce is approaching retirement, while 68% of firms cite skill deficits in precision assembly and digital tool use. Factory processes demand competencies in automated equipment, BIM workflows, and stringent quality-control regimes distinct from traditional carpentry. Community colleges and apprenticeship programs are emerging, yet the training pipeline lags near-term market needs. Geographic mismatch between manufacturing hubs and labor pools further complicates staffing, prompting employers to boost wages or relocate plants. Persistent talent shortages may temper growth even as demand accelerates, nudging firms to deploy robotics and standardized interfaces to reduce human error and lift productivity in the prefabricated housing market[2]World Bank, “Border Management and Logistics,” worldbank.org.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Timber Dominance Accelerates Sustainability Transition

Timber held a 32.62% share of the prefabricated housing market in 2025, outpacing all other materials and expanding at a 7.18% CAGR through 2031. Mass-timber panels show high seismic resilience, proven in laboratory shake-table tests that kept rocking frames intact under major earthquake loads. Regulatory roadmaps such as the United Kingdom’s Timber in Construction 2025 plan reinforce adoption by linking carbon targets to wood-based systems. Concrete retains a solid position through precast innovation that slashes curing times, while steel benefits from robotic welding that enhances dimensional accuracy. Glass and composite panels cater to specialized use-cases like hurricane-rated façades that must satisfy FEMA debris-impact guidelines.

Growth in the timber segment aligns with green-building certificates that reward low-embodied carbon, prompting developers to embrace Design for Manufacturing and Assembly principles that optimize panel sizing for factory output. The Nordic Swan Ecolabel extends this push by stipulating non-toxic ingredients across the building life cycle, strengthening consumer confidence. Continuous R&D in hybrid systems that pair timber with light-gauge steel or recycled composites illustrates how manufacturers can meet structural, fire, and acoustic codes without handicapping speed or cost. These synchronous advances ensure that wood remains the benchmark for sustainable solutions in the prefabricated housing industry.

By Application Type: Single-Family Leadership Faces Multi-Family Acceleration

Single-family units commanded 57.64% of the prefabricated housing market in 2025, yet multi-family projects are on a faster 6.88% CAGR trajectory to 2031. Firms like Clayton Homes shipped roughly 51,000 single-family dwellings in 2024, with 95% meeting Department of Energy Zero Energy Ready Home standards. Urban land scarcity and affordability pressures are shifting investor focus toward stacked modular blocks that compress construction windows and trim carrying costs. Los Angeles, New York, and London have each fast-tracked mid-rise modular projects to reduce neighborhood disruption.

Rising interest in disaster-recovery housing and flexible micro-units for remote workers further broadens application diversity. Hong Kong’s Modular Integrated Construction program delivered over 21,000 transitional units at record speed, showcasing how vertical stacking can answer density constraints. Zoning reforms in U.S. states—allowing accessory dwelling units by right—encourage small-scale prefab extensions. Collectively these dynamics enable multi-family formats to narrow the volume gap, driving portfolio diversification for builders active in the prefabricated housing market.

By Product Type: Manufactured Homes Lead While Modular Innovation Accelerates

Manufactured homes accounted for 43.55% of the prefabricated housing market in 2025, but modular homes are gaining ground with a 7.05% CAGR through 2031. The manufactured segment benefits from HUD standards that mandate wind-resistance up to 110 mph, offering nationwide code uniformity. Clayton, Skyline Champion, and Cavco leverage integrated financing arms to streamline consumer access, buttressing volume consistency. Modular builders, meanwhile, iterate quickly on seismic safety—utilizing slider devices and bonded rubber isolators that dissipate earthquake energy without compromising structural integrity.

Hybrid approaches that pair panelized walls with volumetric wet-core pods pull design flexibility into urban infill projects. Companies like Plant Prefab harness this model to cut onsite labor while allowing façade customization that meets architectural review boards. Steel-frame high-rise modules adopt advanced bolted connections tested under cyclic loading, securing approvals in Japan and Singapore. Emergent 3-D printed shells complement panel systems for accessory units, reflecting an innovation cadence that keeps the prefabricated housing market adaptive to diverse code environments and buyer preferences.

Geography Analysis

Asia-Pacific led with 35.88% share in 2025, underpinned by China’s large-scale factories and Japan’s mature consumer acceptance. Compliance barriers—for instance, aligning Chinese imports with Australian standards—spark investments in local certification labs that smooth cross-border trade. India’s incentive packages, which rank government financing as the most potent driver of prefab uptake, add long-term volume by encouraging domestic resource manufacture. Australia’s USD 54 million federal stimulus, coupled with a new national approval framework, streamlines pipeline visibility and lifts builder confidence.

Middle East & Africa is poised for the fastest 7.29% CAGR thanks to disaster recovery, youth-heavy demographics, and mega-infrastructure corridors that favor quick-turn developments. Post-earthquake Turkey illustrates scale economics, as centrally procured modular villages delivered communal services at lower per-unit costs than site-built shelters. Gulf Cooperation Council states embrace prefab labor-saving advantages amidst tighter visa quotas, integrating smart cooling skins to meet stringent thermal codes.

North America and Europe remain innovation hubs. Sweden maintains 84% prefab adoption in detached homes, and the United Kingdom is embedding off-site solutions into housing-supply targets via parliamentary advocacy. In the United States, state-level modern-methods-of-construction standards—enacted in Virginia and on deck in California—accelerate convergence. South America, led by Brazil, tests modular pilot projects in social-housing programs but contends with fragmented regulation. Across all regions, policy alignment and local fabrication capacity prove decisive for continued prefabricated housing market expansion.

Competitive Landscape

The global prefabricated housing market is fragmented, yet technology consolidation is raising the performance bar across the prefabricated housing market. Clayton Homes generated USD 12.4 billion revenue in 2024 through 46 plants, using vertical integration to buffer supply volatility. Skyline Champion acquired Regional Homes to add 1,400 annual shipments and broaden retail footprints. Such moves illustrate a volume-driven strategy that pools procurement and distribution.

Disruptors favor capital-light or technology-heavy models. Boxabl’s USD 3.5 billion SPAC merger underscores investor appetite for fold-out micro-units that compress shipping costs. Plant Prefab raises venture funding to commercialize hybrid panel-modular workflows, promising urban infill throughput at premium margins. Cuby’s mobile micro-factories show a regionalized production thesis that minimizes oversize freight expense while enabling design localization.

Standardization bodies increase interoperability, giving smaller entrants a pathway to scale. ISO 21723:2019 and ISO 2848:1984 codify horizontal and vertical module increments, while ICC’s 2024 modular appendix clarifies U.S. compliance. As warranty expectations rise, firms invest in LiDAR-enabled inspection and digital twins, deepening the technology moat. Although the top five players control less than 30% of volume, ongoing mergers hint at gradual concentration of know-how and capital, keeping competitive pressure high but opportunities open for niche specialists within the prefabricated housing market[4]ICC, “2024 International Building Code Appendix,” iccsafe.org.

Prefabricated Housing Industry Leaders

Clayton Homes (Berkshire Hathaway)

Skyline Champion Corporation

Cavco Industries Inc.

Sekisui House Ltd (North America arm)

Boxabl Inc.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- August 2025: Boxabl Inc. announced plans to go public through a USD 3.5 billion SPAC merger with FG Merger II Corp., representing one of the largest prefabricated housing market capitalizations.

- May 2025: Canada's federal government launched the Build Canada Homes program with USD 25 billion in loans and USD 1 billion in equity specifically for prefabricated housing projects.

- April 2025: Onx Homes launched an automated prefab factory in Pompano Beach, Florida, designed to produce components for 1,000 homes annually.

- July 2024: Skyline Champion Corporation announced acquisition of Regional Homes to enhance market position in the prefabricated housing sector.

Global Prefabricated Housing Market Report Scope

Prefabrication is assembling components of a structure in a factory or other manufacturing site and transporting complete assemblies or sub-assemblies to the construction site. A comprehensive background analysis of the global prefabricated house market, including the assessment of the economy and contribution of sectors in the economy, market overview, market size estimation for key segments, and emerging trends in the market segments, market dynamics, and geographical trends, and COVID-19 impact, is covered in the report.

The global prefabricated house market is segmented by type (single-family and multi-family) and geography (North America, Asia-Pacific, Europe, GCC, and the Rest of the World). The report offers market size and forecasts for all the above segments in value (USD).

By Material Type

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Type

| Single-Family |

| Multi-Family |

By Product Type

| Modular Homes |

| Panelised & Componentised Systems |

| Manufactured Homes |

| Other Prefab Types |

By Region

| North America | United States |

| Canada | |

| Mexico | |

| South America | Brazil |

| Argentina | |

| Chile | |

| Rest of South America | |

| Europe | Germany |

| United Kingdom | |

| France | |

| Italy | |

| Spain | |

| Rest of Europe | |

| Asia-Pacific | China |

| India | |

| Japan | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Middle East & Africa | United Arab Emirates |

| Saudi Arabia | |

| South Africa | |

| Nigeria | |

| Rest of Middle East & Africa |

| By Material Type | Concrete | |

| Glass | ||

| Metal | ||

| Timber | ||

| Other Materials | ||

| By Type | Single-Family | |

| Multi-Family | ||

| By Product Type | Modular Homes | |

| Panelised & Componentised Systems | ||

| Manufactured Homes | ||

| Other Prefab Types | ||

| By Region | North America | United States |

| Canada | ||

| Mexico | ||

| South America | Brazil | |

| Argentina | ||

| Chile | ||

| Rest of South America | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Middle East & Africa | United Arab Emirates | |

| Saudi Arabia | ||

| South Africa | ||

| Nigeria | ||

| Rest of Middle East & Africa | ||

Key Questions Answered in the Report

How big is the Prefabricated Housing Market?

The Prefabricated Housing Market size is expected to reach USD 152.74 billion in 2026 and grow at a CAGR of 6.62% to reach USD 210.33 billion by 2031.

What is the current Prefabricated Housing Market size?

In 2026, the Prefabricated Housing Market size is expected to reach USD 152.74 billion.

Who are the key players in Prefabricated Housing Market?

Daiwa House Industry, Sekisui House, Asahi Kasei Corporation, Skanska AB and Peab AB are the major companies operating in the Prefabricated Housing Market.

Which is the fastest growing region in Prefabricated Housing Market?

Middle East & Africa is estimated to grow at the highest CAGR over the forecast period (2026-2031).

Which region has the biggest share in Prefabricated Housing Market?

In 2026, the Asia Pacific accounts for the largest market share in Prefabricated Housing Market.

What years does this Prefabricated Housing Market cover, and what was the market size in 2025?

In 2025, the Prefabricated Housing Market size was estimated at USD 152.74 billion. The report covers the Prefabricated Housing Market historical market size for years: 2020, 2021, 2022, 2023 and 2024. The report also forecasts the Prefabricated Housing Market size for years: 2026, 2027, 2028, 2029, 2030 and 2031.

Page last updated on: