Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

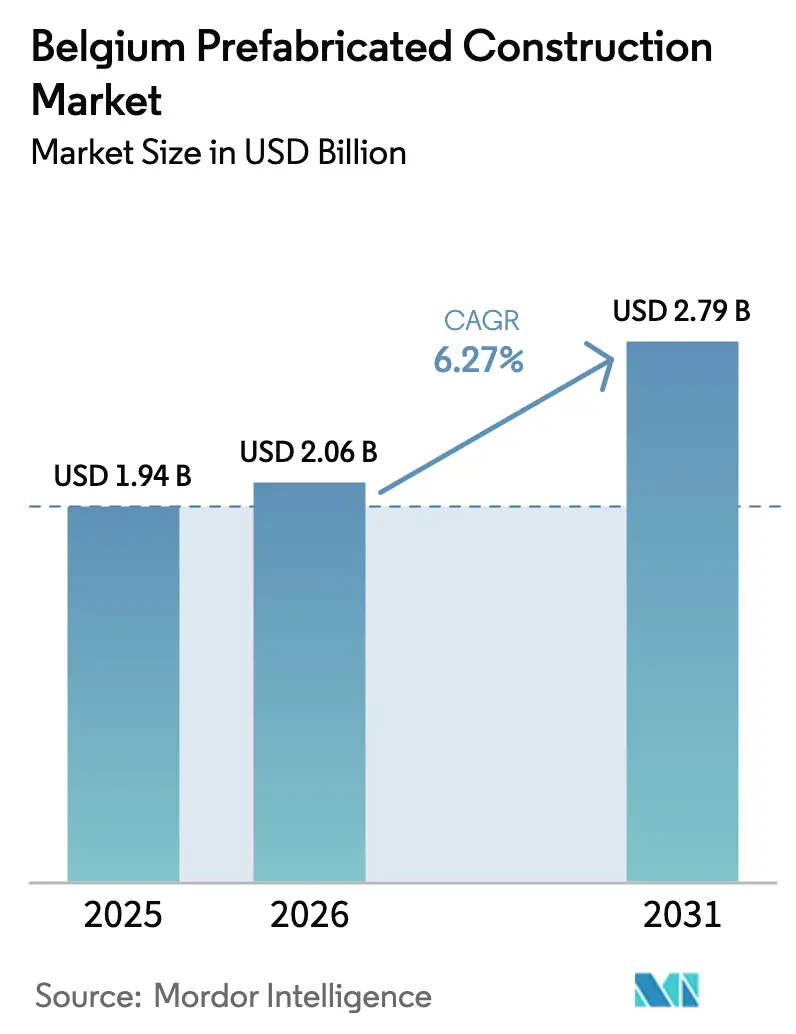

| Base Year Market Size (2025) | USD 1.94 Billion |

| Market Size (2026) | USD 2.06 Billion |

| Market Size (2031) | USD 2.79 Billion |

| Growth Rate (2026 - 2031) | 6.27% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Belgium Prefabricated Construction Market Analysis by Mordor Intelligence

Belgium Prefabricated Construction market size in 2026 is estimated at USD 2.06 billion, growing from 2025 value of USD 1.94 billion with 2031 projections showing USD 2.79 billion, growing at 6.27% CAGR over 2026-2031. Belgium Prefabricated Construction Market has reportedly been growing steadily, attributed to urbanization and the increasing demand for efficient construction solutions. Industry reports suggest that the residential sector has been leading this growth, with a rise in single-family prefabricated homes. Analysts have highlighted steel as the dominant material in the market, valued for its strength and recyclability. The market is said to feature a mix of domestic and international players, which is believed to drive innovation and competition. Observers have noted that the industry's focus on sustainability and rapid construction methods has been a key factor in its expansion.

Key Report Takeaways

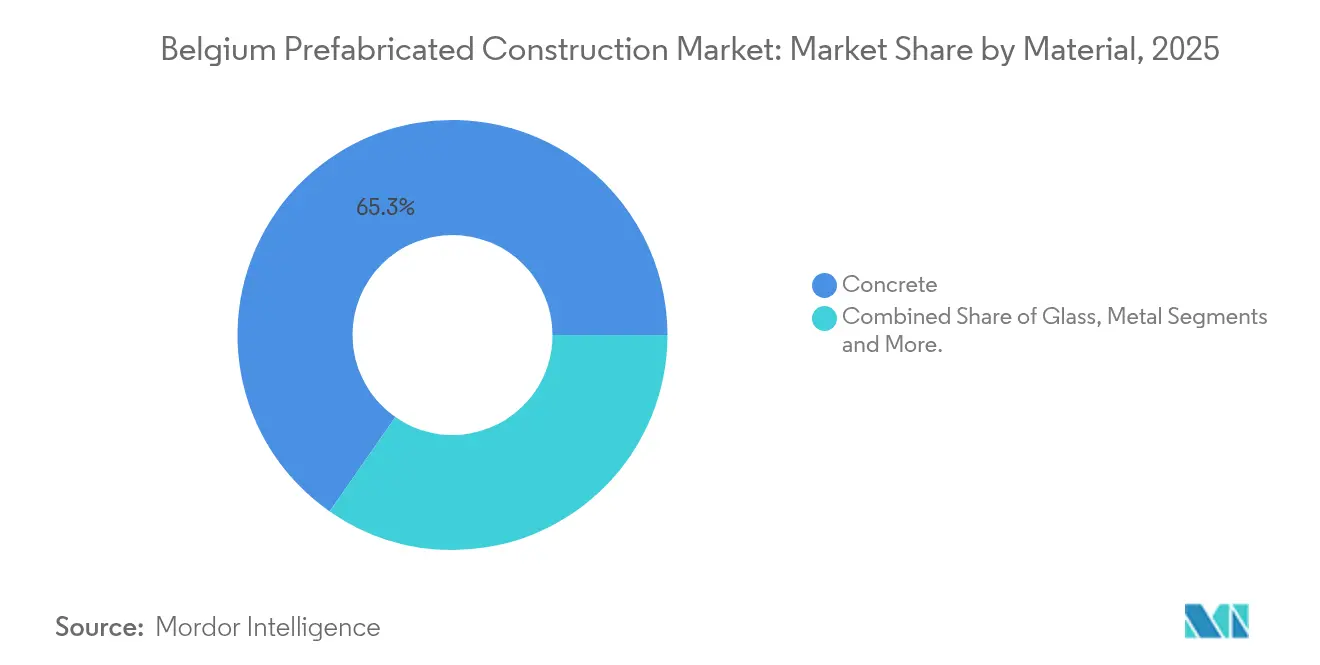

- By material, concrete captured 65.32% of the Belgium prefabricated construction market share in 2025, whereas timber is forecast to expand at a 6.71% CAGR through 2031.

- By application, residential accounted for 52.15% of the Belgium prefabricated construction market size in 2025, while commercial projects are advancing at a 7.12% CAGR to 2031.

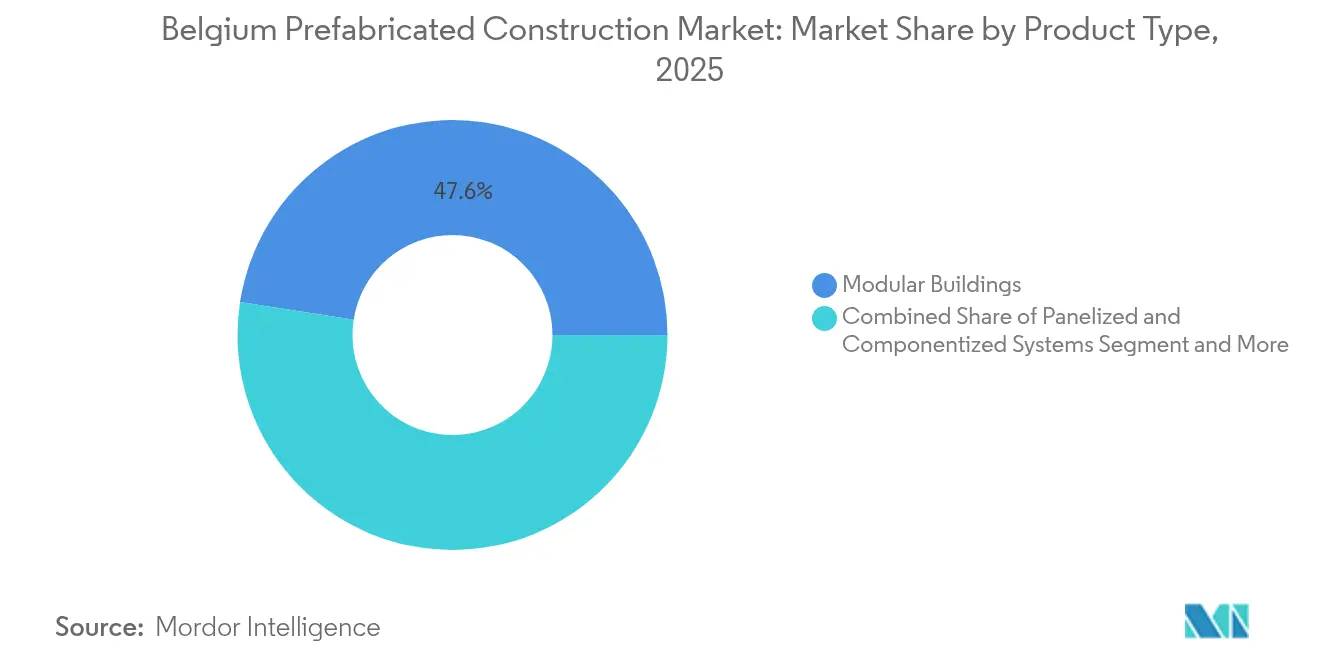

- By product type, modular buildings led with 47.55% revenue share in 2025, and volumetric modular units are projected to grow at 7.58% CAGR through 2031.

- By geography, Antwerp Province held a 30.22% share of the Belgium prefabricated buildings market in 2025; East Flanders is the fastest-growing area with an 7.74% CAGR forecast to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Belgium Prefabricated Construction Market Trends and Insights

Drivers Impact Analysis*

| Drivers | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Tight labor market and productivity needs | +1.2% | National, acute in Flanders | Short term (≤ 2 years) |

| EU energy-performance and circularity goals | +1.4% | National, driven by EPBD transposition | Medium term (2-4 years) |

| Public-sector adoption in education/health | +1.3% | Flanders and Brussels | Medium term (2-4 years) |

| Logistics and light-industrial demand | +0.9% | Antwerp Province, West Flanders | Long term (≥ 4 years) |

| Urban infill and brownfield redevelopment | +0.8% | Brussels Capital Region, Ghent, Antwerp | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Tight Labor Market And Productivity Imperatives

Belgian contractors face a chronic shortage of skilled trades, pushing builders toward factory automation and rapid on-site assembly. Alpha Beton’s 2024 investment in Progress Group's shuttering robots trimmed manual steps and kept output stable despite workforce gaps. Pauli Beton followed suit in 2025 with automated hollow-core lines from Elematic, citing labour scarcity as the prime motivator.[1]“Family Tradition and Innovation at Alpha Beton,” BFT International, bft-international.com Dry-assembly façades, such as Facadeclick, install three times faster than brickwork, directly easing the bricklayer shortage. The MW2023 modular-housing framework further institutionalizes offsite delivery to compress schedules. Collectively, this driver lifts the Belgium prefabricated buildings market growth by 1.2 percentage points and is likely to peak within two years as automation matures..

EU Energy-Performance and Circularity Mandates

The 2024 revision of the Energy Performance of Buildings Directive compels near-zero-energy performance, making factory-built high-efficiency envelopes the path of least resistance. Recticel’s USD 659 million 2024 revenue underscores demand for polyurethane panels that hit U-values below 0.15 W/m²K. IsoHemp’s hempcrete blocks surpass 1 million units a year, aligning with bio-based procurement preferences. Holcim’s USD 540 million GO4ZERO project will supply decarbonized cement for precast elements by 2029.[2]Miljan Gutovic, “GO4ZERO Project,” Holcim, holcim.comThese mandates lift the market CAGR by 1.4 percentage points, with compliance deadlines clustered between 2026 and 2028.

Public-Sector Modular Procurement

Long-term design-build-finance-maintain deals in education and healthcare are standardizing modular delivery. The Scholen van Morgen PPP covers 250 schools and 710,000 m², locking in panelised classrooms to meet strict handover milestones. HELORA’s five-hospital network applies “highly modular prisms” to enable phased additions. The European School Brussels V adopts volumetric units to limit disruption on a dense urban site. These contracts add 1.3 percentage points to growth, with impact cresting mid-decade as multi-year frameworks ramp up.

Logistics And Light-Industrial Demand In Port Corridors

E-commerce hubs and cold-chain players along the Antwerp–Bruges corridor prize fast, flexible structures. Nexus Logistics, launched in 2024 by Imtech and Cordeel, markets modular steel warehouses designed for disassembly. NYK’s automated car park in Zeebrugge, approved September 2025, relies on prefabricated framing to cut schedule risk. The EUR 335 million Europa Terminal upgrade embeds modular elements to keep port operations running. This driver contributes 0.9 percentage points to CAGR and extends through 2030 as cargo volumes climb.

Restraints Impact Analysis*

| Restraints | (~) % IMPACT ON CAGR FORECAST | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Strict permitting and heritage rules | -0.7% | Brussels, Antwerp heritage zones, Walloon municipalities | Short term (≤ 2 years) |

| High transport and cranage costs for oversized modules | -0.5% | Brussels, Antwerp, Ghent urban cores | Medium term (2-4 years) |

| Elevated material and financing costs | -0.6% | National, acute in Wallonia and Limburg | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Permitting Complexity and Heritage Constraints

Layered approvals elongate project timelines, especially where façades must match historic streetscapes. Antwerp’s quality-chamber reviews often stretch permits to 135 days and restrict panel dimensions. Brussels adds its own Plan Régional d’Urbanisme rules, while Wallonia enforces CODT zoning nuances. Modular suppliers must tweak designs municipality by municipality, undercutting standardization benefits. Facadeclick launched a training academy to quell approval hesitancy. This friction subtracts 0.7 percentage points from market CAGR but should ease as digital permitting portals mature.

Transport and Last-Mile Logistics Costs

Oversize modules incur police escorts, night-time drops, and special cranes, adding up to 25% to delivery budgets in the Brussels core. The Europa Terminal upgrade highlighted the need for phased scheduling to route gigantic elements through active docks. Skilpod’s pricing includes free haulage only inside a 100 km radius, underscoring distance sensitivity. Betca’s heavy-lift precast pits weigh up to 75 tonnes, demanding 500-tonne cranes on tight city blocks. These constraints shave 0.5 percentage points off growth, likely persisting until urban logistics hubs proliferate.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material: Concrete Strength, Timber Momentum

Concrete systems controlled 65.32% of the Belgium prefabricated construction market in 2025, sustained by Benor-certified precast slabs, beams, and double walls that dominate structural floors and parking decks. CRH’s Ergon and Prefaco divisions, together with D-Concrete and VB Beton, leverage mature batching plants and integrated transport fleets to keep per-square-meter costs competitive. Large-format elements up to 45 meters long and 64 tonnes heavy enable wide-span industrial halls without interior columns, a decisive advantage for logistics clients in Antwerp Port. As solar-ready roof loads and seismic robustness gain importance, engineered concrete remains the default choice for multi-story residential towers and data centers within the Belgium prefabricated construction market.

Timber, however, is the fastest-growing material, set to post a 6.71% CAGR through 2031 as public buyers embrace low-carbon procurement. Stabilame’s fully automated CLT line, showcased to PEFC auditors in 2025, feeds school and hospital tenders requiring certified chain-of-custody wood. IsoHemp’s bio-based hempcrete blocks serve retrofit façades that target circularity scores under EU taxonomy rules. Hybrid steel-timber frames such as those used at the Gare Maritime project shorten assembly times and store biogenic carbon, resonating with Belgium’s Renovation Pact targets. Metal sandwich panels, though a smaller slice, unlock fast-track cold-chain warehouses with 1.2 mm light-gauge C-sections made from ArcelorMittal’s XCarb steel. Niche bio-composites, from grass-fiber boards to recycled plastics, round out a diversifying material mix that responds to client decarbonization goals.

By Application: Housing Leads, Commerce Accelerates

Residential construction retained 52.15% of the Belgium prefabricated construction market share in 2025 as municipalities expanded affordable-housing pipelines. Modular home specialist Skilpod sells turnkey CLT units starting at USD 70,000, offering first-time buyers a controlled price point and 90-day delivery. Multi-family panelized systems—exemplified by Unilin’s Hydroflam boards at the OPZ Geel hospital residences—cut site MEP installation by 30%. Yet the commercial segment is pulling ahead in growth, on track for a 7.12% CAGR to 2031 as Brussels office conversions and logistics sheds demand flexible layouts. Cityforward’s district-wide retrofits hinge on panelized partitions and prefabricated façade cassettes, while Nexus Logistics’ circular warehouses meet e-retailers’ speed-to-market needs.

Education and healthcare sit in the “Others” category but yield landmark volume through long PPP concessions. The Scholen van Morgen program alone totals 710,000 m² of learning space delivered under modular envelopes that meet near-zero-energy standards. HELORA’s hospital cluster specifies volumetric patient rooms to phase expansions without shutting down wings. Algeco’s 345,000-unit rental fleet services temporary classrooms and site offices, mitigating demand peaks. These institutional avenues smooth out private-cycle volatility and deepen the resilience of the Belgium prefabricated construction market.

By Product Type: Modular Core, Volumetric Upswing

Modular buildings represented 47.55% of 2025 revenue, anchored by fully outfitted volumetric units craned into place in a single day. Volumetric is slated for 7.58% CAGR, the briskest among product families, as hospitals and municipalities chase repeatable room layouts and minimal site disturbance. Skilpod’s houses arrive painted and wired, while hsbcad’s BIM-to-CNC workflow lets timber fabricators cut components within 0.5 mm tolerances. Panelised systems maintain relevance where narrow streets cap module width; Facadeclick’s dry-brick panels retrofit façades without wet trades and meet heritage looks in Flemish towns. Prefabricated MEP cores, such as LITO’s plug-and-play HVAC blocks, slot into apartment risers and shorten commissioning cycles. Hybrid approaches blending flat-pack panels with volumetric bathrooms are gaining traction on constrained city plots, underscoring the adaptive fabric of product strategies across the Belgium prefabricated construction market.

Geography Analysis

Antwerp Province dominated with a 30.22% share of the Belgium prefabricated construction market in 2025, fuelled by port-centric industrial expansions and public-private megaprojects. The USD 364 million Europa Terminal upgrade embeds precast modules to keep quays operational, while INEOS’s Project ONE ethane cracker relies on 22,000 m³ of precast concrete supplied by Vanhout and Franki Foundations. Municipal design codes require contextual façades, yet the province’s robust logistics spine absorbs higher upfront engineering costs.

East Flanders is the pacesetter, projected at an 7.74% CAGR to 2031 on the back of Ghent’s brownfield conversions and a surge in school tenders. Stabilame’s CLT line caters to timber-first designs that meet embodied-carbon thresholds. The Green Energy Park near Asse applies Magnelis-coated light-gauge steel to research pavilions, highlighting cross-provincial supply chains. Anchored by the University of Ghent and a cluster of circular-construction start-ups, the region is becoming Belgium’s test bed for hybrid systems.

Brussels Capital Region, though smaller in land mass, commands premium office-to-residential conversions that favor high-spec façade panels and volumetric wet rooms. Cityforward’s USD 950 million portfolio retrofit will double housing density in the European district by 2028, driving sustained module demand. Wallonia’s growth lags as purchasing power trails Flanders, yet Alpha Beton’s upgrades in Sankt Vith signal a commitment to automated capacity. Limburg sees steady residential infill, supported by LITO’s prefabricated HVAC risers in Zolder and Hasselt. Collectively, regional nuances underscore why national averages mask divergent local trajectories within the Belgium prefabricated buildings market.

Competitive Landscape

The market sits at a moderate concentration level where legacy precast giants intersect with agile modular upstarts. CRH’s Ergon and Prefaco divisions, Recticel (USD 659 million revenue), and IsoHemp anchor concrete and insulation supply chains, leveraging decade-long Benor certification and entrenched contractor loyalty. Holcim’s July 2024 purchase of recycler Mark Desmedt broadens its circular material loop, while Recticel’s Rex buyout secures feedstock for high-performance PIR boards.

Digitalization is reshaping rivalry. Maguar Capital’s majority stake in HSBCAD injects capital to push BIM-to-CNC software deeper into Benelux timber fabricators, raising entry barriers for manual shops. Alpha Beton and Pauli Beton automate shuttering and hollow-core extrusion to offset labour gaps, signalling that robotics is now table stakes. Lemahieu Group’s triple acquisition spree—LDCwood, Lambrechts Hout, and Accoya distribution rights—locks down certified timber supply and enhances price control in the fast-growing bio-based segment.

Niche disruptors are closing financing rounds to scale. Facadeclick, eyeing “50 million clicks” annual output, positions its dry-assembly brick for heritage districts once regulatory familiarity grows. Nexus Logistics targets circular warehouses that can be disassembled and redeployed, a value proposition resonating with e-commerce operators that prize flexibility. Skilpod and Leko Labs remain volume-constrained but benefit from municipal procurement rules favouring local content. As demand fragments across materials and end uses, ecosystem partnerships—rather than outright vertical integration—are shaping competitive strategies across the Belgium prefabricated buildings market.

Belgium Prefabricated Construction Industry Leaders

CRH (Ergon, Prefaco, Schelfhout-Beton)

Recticel Group

Stabilame

D-Concrete

VB Beton

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- July 2025: Lemahieu Group acquired Lambrechts Hout, a Belgian timber supplier, to strengthen its position in the prefabricated timber-frame market and secure supply-chain continuity amid elevated wood-product pricing. The acquisition follows Lemahieu's September 2024 move to full control of LDCwood, which operates six ThermoWood kilns in Ostend, and its April 2025 appointment as Accoya distributor, collectively positioning the group as a vertically integrated timber-products supplier for modular and panelized construction.

- June 2025: Belgian healthcare REITs Aedifica and Cofinimmo agreed to merge, creating a combined portfolio valued at EUR 12.1 billion (USD 13.1 billion) and Europe's largest healthcare real estate company. The transaction, subject to shareholder and regulatory approvals, is expected to accelerate modular construction in senior housing and care facilities across Belgium and more than 12 European countries, leveraging economies of scale in procurement and standardized prefabricated patient rooms.

- June 2025: Belgian sovereign fund SFPIM and insurer Ethias, through their Cityforward vehicle, acquired 21 European-district office buildings in Brussels for approximately EUR 880 million (USD 950 million) from the European Commission. Cityforward plans to convert the portfolio to 70 percent sustainable offices and 30 percent residential units, targeting first occupancy from 2028 and effectively doubling residential density in the European district. The scale of the conversion is expected to drive demand for modular bathroom pods, panelized partitions, and prefabricated façade upgrades.

- May 2025: Stabilame, a Belgian CLT manufacturer, hosted a PEFC field trip to showcase its high-automation production facility, emphasizing certified sustainable forestry and chain-of-custody documentation. The event underscored timber suppliers' efforts to meet public-sector tender requirements for PEFC or FSC certification, particularly in education and healthcare projects under the Scholen van Morgen and HELORA frameworks.

Belgium Prefabricated Construction Market Report Scope

The Prefabricated Buildings Market refers to the industry focused on designing, manufacturing, and assembling building components off-site, which are then transported and installed at their final location. It includes modular, panelized, and pre-engineered structures utilized in residential, commercial, and industrial sectors. The market's growth is driven by the demand for cost-effective, time-efficient, and sustainable construction solutions. Key players include construction firms, material suppliers, and modular housing manufacturers. Trends in this market include the adoption of eco-friendly materials, advancements in 3D printing, and the integration of smart building technologies.

Belgiums prefabricated buildings industry is segmented by application (residential, commercial, and industrial). The report offers market size and market forecasts for Belgium prefabricated buildings market in value (USD).

By Material

| Concrete |

| Glass |

| Metal |

| Timber |

| Other Materials |

By Application

| Residential |

| Commercial |

| Others |

By Product Type

| Modular Buildings |

| Panelized & Componentized Systems |

| Other Prefab Types |

By Province

| Antwerp Province |

| East Flanders |

| West Flanders |

| Limburg |

| Rest of Belgium |

| By Material | Concrete |

| Glass | |

| Metal | |

| Timber | |

| Other Materials | |

| By Application | Residential |

| Commercial | |

| Others | |

| By Product Type | Modular Buildings |

| Panelized & Componentized Systems | |

| Other Prefab Types | |

| By Province | Antwerp Province |

| East Flanders | |

| West Flanders | |

| Limburg | |

| Rest of Belgium |

Key Questions Answered in the Report

What is the 2026 value of the Belgium prefabricated buildings market?

It is valued at USD 2.06 billion in 2026.

How fast is the prefabricated sector expected to grow in Belgium?

The market is forecast to post a 6.27% CAGR between 2026 and 2031.

Which material currently dominates Belgian offsite construction?

Precast concrete leads with a 65.32% share as of 2025.

Which province offers the highest growth potential?

East Flanders is projected to expand at an 7.74% CAGR through 2031.

Why are Belgian schools choosing modular buildings?

Public frameworks like Scholen van Morgen favor modular delivery for rapid schedules, consistent quality, and low on-site disruption.

What limits the wider use of large volumetric modules in city centers?

High cranage and escort costs, narrow streets, and heritage regulations constrain oversized deliveries in Brussels and Antwerp.

Page last updated on: