Sustainable Packaging Market Size and Share

Market Overview

| Study Period | 2019 - 2030 |

|---|---|

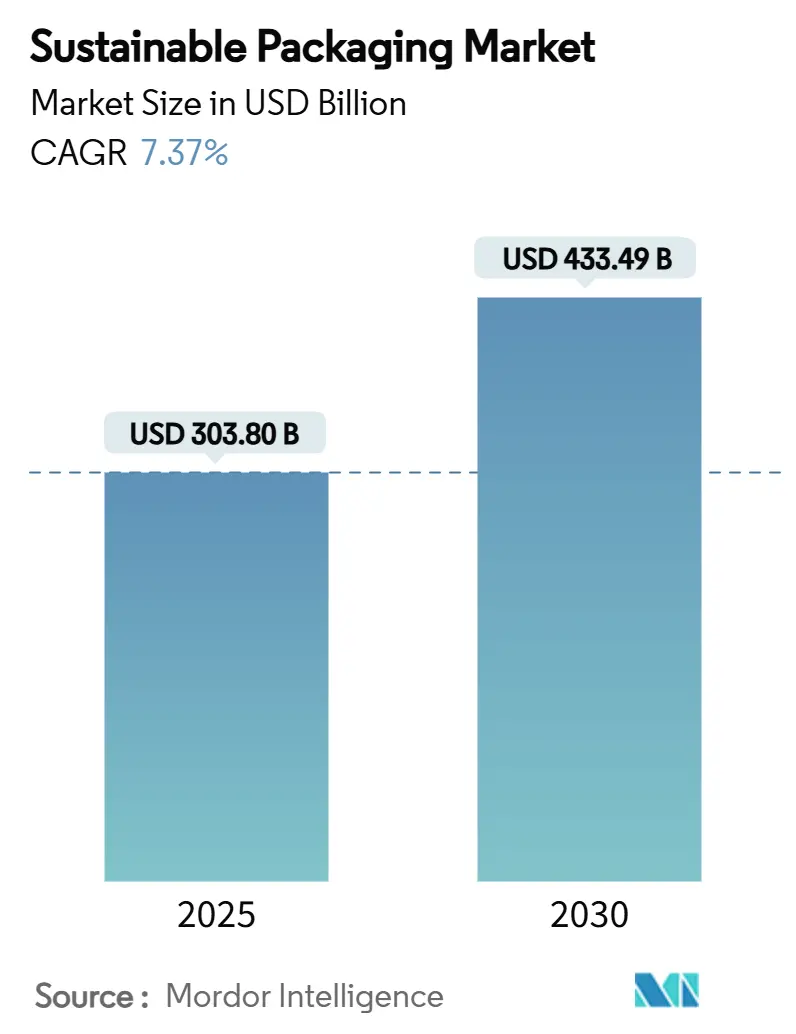

| Market Size (2025) | USD 303.80 Billion |

| Market Size (2030) | USD 433.49 Billion |

| Growth Rate (2025 - 2030) | 7.37% CAGR |

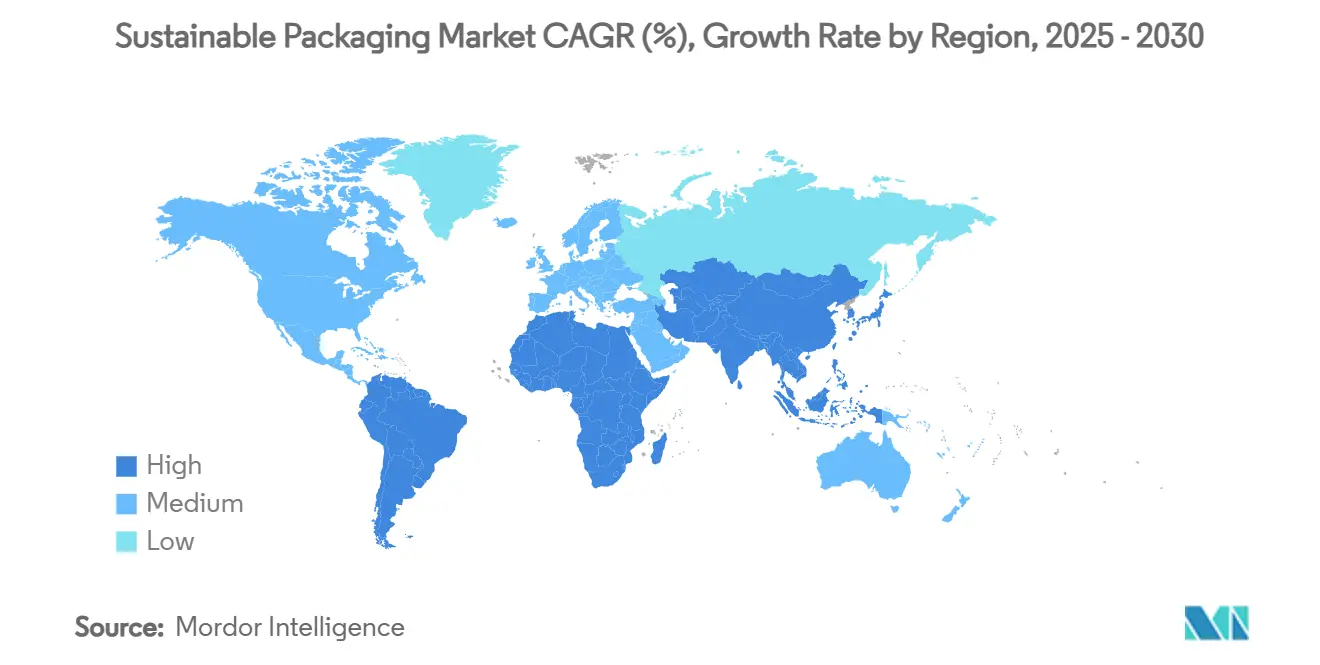

| Fastest Growing Market | Asia Pacific |

| Largest Market | Europe |

| Market Concentration | Low |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Sustainable Packaging Market Analysis by Mordor Intelligence

The sustainable packaging market size stood at a value of USD 303.80 billion in 2025 and is projected to reach USD 433.49 billion by 2030, reflecting a CAGR of 7.37%. Momentum is anchored in converging Extended Producer Responsibility (EPR) regulations that now span 63 countries, eliminating regulatory arbitrage and unlocking cross-border scale efficiencies. Brand commitments to minimum recycled-content thresholds, rapid progress in chemical recycling technologies, and rising e-commerce volumes that demand packaging right-sizing are accelerating capital deployment toward circular solutions. Venture funding into mycelium and seaweed-based substrates, coupled with AI-enabled sortation that improves material yields, is narrowing the cost gap between recycled and virgin feedstocks. Simultaneously, strategic mergers—such as the Amcor–Berry Global tie-up—are consolidating research and development resources to speed commercialization of next-generation formats.

Key Report Takeaways

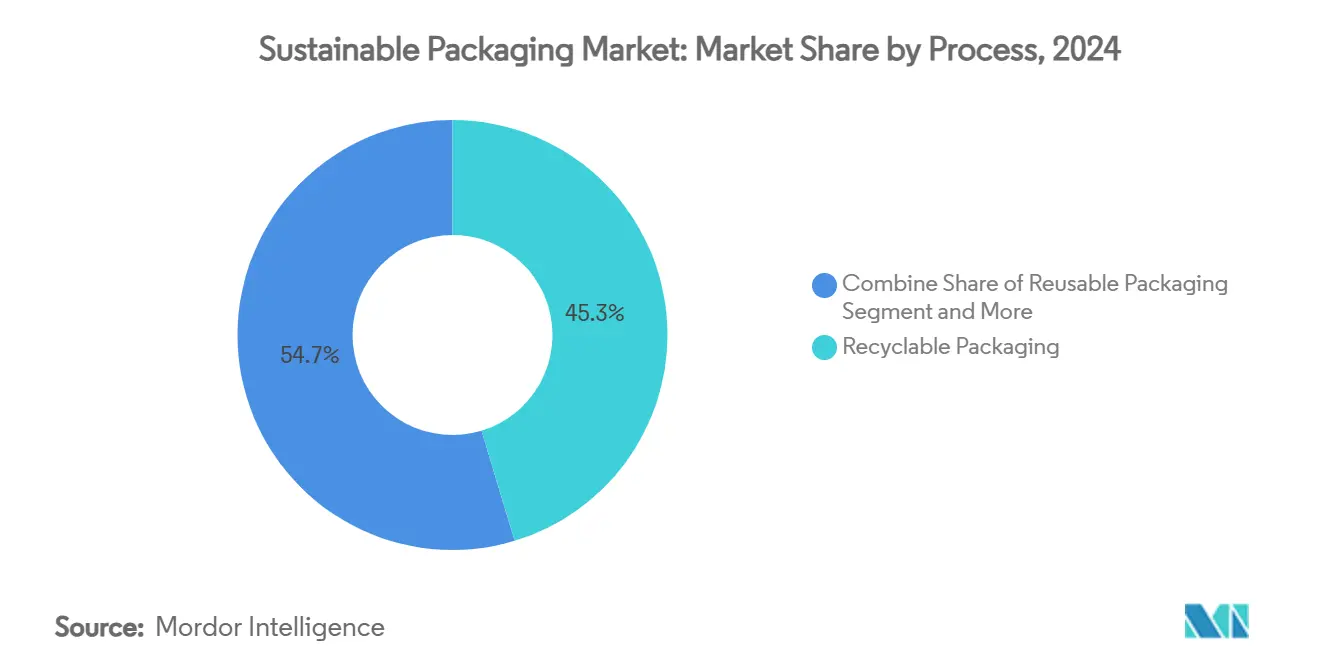

- By process, recyclable solutions maintained a 45.32% revenue share in 2024, while compostable and biodegradable formats are expanding at a 12.54% CAGR to 2030.

- By material, paper and paperboard led with 40.43% of the sustainable packaging market share in 2024; plant-based materials are forecast to grow at 11.43% CAGR through 2030.

- By packaging format, rigid solutions held 55.23% share in 2024, whereas flexible packaging is projected to advance at 8.43% CAGR through 2030.

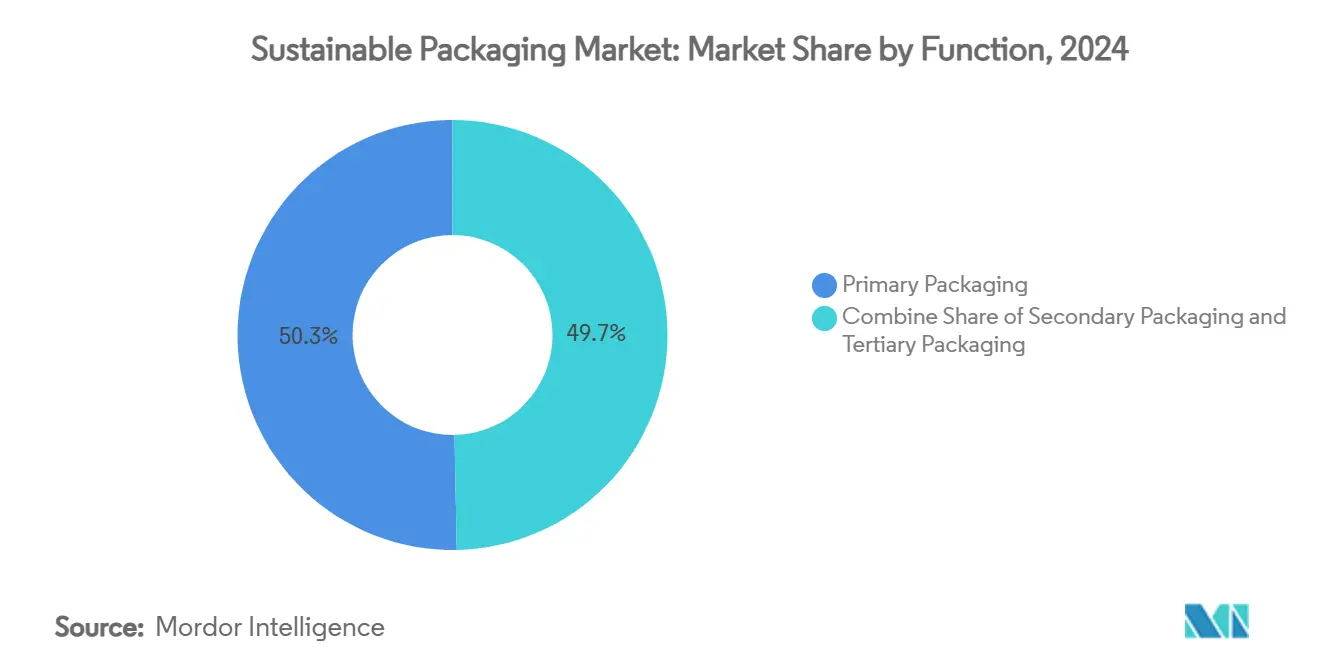

- By function, primary formats captured 50.32% of the sustainable packaging market size in 2024, while secondary packaging is growing fastest at 9.53% CAGR to 2030.

- By end user, food and beverage accounted for 38.32% of the sustainable packaging market size in 2024, yet e-commerce and retail are accelerating at a 12.89% CAGR toward 2030.

- By geography, Europe led with 34.57% market share in 2024; Asia-Pacific is expected to post the highest 11.21% CAGR through 2030.

Global Sustainable Packaging Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EPR laws surge in OECD and BRICS markets | +1.8% | Global, early rollout in EU & North America | Medium term (2-4 years) |

| Brand pledges for ≥25% PCR content | +1.2% | North America & EU | Short term (≤ 2 years) |

| Retail take-back & reuse pilots | +0.9% | North America, EU, expanding to APAC | Medium term (2-4 years) |

| AI-enabled sortation boosts recycling yields | +0.7% | Developed markets worldwide | Long term (≥ 4 years) |

| Food-grade chemical recycling for polyolefins | +0.6% | North America & EU | Long term (≥ 4 years) |

| Mycelium & seaweed packaging innovation | +0.4% | EU & North America | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Extended Producer-Responsibility Laws Create Compliance Convergence

Converging EPR mandates in 63 jurisdictions are dismantling regulatory fragmentation. The European Union’s Packaging and Packaging Waste Regulation, effective February 2025, sets 30% recycled-content targets for PET food packaging and bans PFAS, prompting similar frameworks across OECD and BRICS economies. [1]O’Keeffe, Hazel, “The New EU Packaging and Packaging Waste Regulation – Highlights and Challenges Ahead,” PackagingLaw.com, packaginglaw.com New Kenyan statutes mirror EU fee structures, while Oregon and Colorado require brand-funded Producer Responsibility Organizations from July 2025. Harmonized timelines let global brands deploy single-design solutions at scale, lowering compliance costs and accelerating adoption across the sustainable packaging market.

Brand Commitments Drive PCR Content Standardization Beyond Regulatory Minimums

Major consumer-goods firms now exceed legislation by pledging 25–50% post-consumer recycled (PCR) content portfolio-wide by 2030. Unilever’s 2025 goal for all packaging to be recyclable, reusable, or compostable and Amcor’s supply of 1,000 tons of recycled plastic for Cadbury wrappers exemplify voluntary targets setting de facto industry baselines. Standardized PCR measurement toolkits from the U.S. Plastics Pact streamline verification, catalyzing procurement clarity and fueling growth in the sustainable packaging market.

E-commerce Logistics Pilots Scale Reusable Packaging Systems

Amazon replaced 95% of North American plastic air pillows with curbside-recyclable paper and Walmart eliminated 2,000 tons of single-use plastic mailers, illustrating how shipping-volume leverage translates sustainability into lower unit costs. Retail take-back schemes integrate reverse logistics, giving rise to reusable packaging pools that circulate across e-commerce networks. Machine-learning-driven right-sizing further curtails material consumption, underpinning double-digit expansion of the sustainable packaging market.

AI-Enhanced Sortation Technologies Improve Recycling Economics

Machine-vision systems paired with NIR spectroscopy in European and U.S. materials-recovery facilities lift plastic identification accuracy and unlock 12 material streams, as seen at Sweden’s Site Zero and Ohio’s AMP ONE plants. California’s statute mandating 65% recycling of single-use packaging by 2032 incentivizes adoption, cutting contamination costs and narrowing price spreads between virgin and recycled resins. Higher yields widen PCR availability and reinforce the sustainable packaging market growth trajectory.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Limited supply of food-grade PCR resins | -1.4% | North America & EU | Short term (≤ 2 years) |

| Inflation-driven cost premiums vs. virgin feedstocks | -0.8% | Global | Medium term (2-4 years) |

| Fragmented composting infrastructure | -0.6% | North America & APAC | Medium term (2-4 years) |

| Greenwashing litigation risk | -0.4% | Developed markets | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

PCR Resin Supply Constraints Create Strategic Bottlenecks

Brand pledges now outstrip supply of clear, food-grade PCR. Declining milk volumes shrink the natural HDPE stream, inflating premiums and forcing import reliance that undercuts domestic reclaimers. This imbalance threatens timely fulfillment of regulatory quotas, slowing mass-market expansion of the sustainable packaging market.

Cost Premium Persistence Challenges Mass-Market Adoption

Recycled and bio-based substrates still trade at premiums to virgin polymers because of additional collection and processing costs, exacerbated by energy-price inflation.[2]Ecoplashk, “What is Post Consumer Resin (PCR) Plastic?” ecoplashk.com Volatile PCR prices complicate long-term procurement contracts, particularly for low-margin applications, tempering uptake within the sustainable packaging industry.

Segment Analysis

By Process: Compostable Solutions Gain Momentum Amid Infrastructure Gaps

Recyclable formats retained a 45.32% share in 2024, yet compostable and biodegradable offerings are growing at a 12.54% CAGR, reflecting investor faith in biomaterials such as B’Zeos’ seaweed films. The sustainable packaging market size for compostables is riding demand from food-service and personal-care brands seeking solutions free from microplastic fragmentation. However, only 30% of U.S. municipalities have access to industrial composting sites, curbing near-term penetration. In response, the U.S. COMPOST Act proposes USD 2 billion in grants to expand capacity, which would directly lift diversion rates and long-run growth prospects.

Consumer confusion over end-of-life handling still triggers contamination in organic-waste streams, calling for clearer labeling and public-education campaigns. Anaerobic digestion has emerged as an alternate pathway, generating biogas revenue that improves project economics and partially offsets infrastructure shortfalls. With policy and processing gaps gradually closing, compostable formats are set to capture an expanding slice of the sustainable packaging market.

Note: Segment shares of all individual segments available upon report purchase

By Material Type: Plant-Based Innovation Challenges Traditional Dominance

Paper and paperboard represented 40.43% of 2024 revenue owing to mature recycling systems and consumer trust. Plant-based substrates, however, are advancing at 11.43% CAGR, propelled by Stora Enso’s dry-forming fiber lines that cut water use by 75% and energy by 30%, boosting circularity credentials. The sustainable packaging market share of polyolefins is expected to contract gradually as PFAS bans and recycled-content rules intensify.

Advanced recycling breakthroughs, including Berkeley’s 260 °C vaporization process that converts polyethylene into feedstock with 98% recovery, enable food-grade loops and mitigate downcycling. Mycelium foams and wood-based PET replacements are expanding addressable use cases beyond niche segments, signaling a broader materials transition within the sustainable packaging market.

By Packaging Format: Flexible Solutions Drive Efficiency Gains

Rigid structures held 55.23% of 2024 revenue. Yet flexible formats, posting an 8.43% CAGR, are eroding that lead as mono-material pouches and films combine barrier performance with recyclability. Amcor’s recyclable retort pouch eliminates aluminum layers and cuts lifecycle carbon by up to 60%. Such innovations reduce weight and emissions, amplifying total cost-of-ownership advantages.

Huhtamaki’s 2024 launch of three mono-material solutions indicates accelerating pipeline depth. Meanwhile, rigid glass and metal remain entrenched in premium or refill channels where infinite recyclability and consumer perception of quality prevail. Overall, format substitution trends continue to shape the sustainable packaging market trajectory toward lighter, lower-carbon footprints.

By Function: Secondary Packaging Emerges as Growth Driver

Primary packaging generated 50.32% of 2024 turnover. Secondary formats, expanding at 9.53% CAGR, are benefiting from e-commerce volume that rewards right-sized cartons and cushioning alternatives. Amazon’s algorithmic box-sizing slashed corrugate use and eliminated 95% of plastic pillows, lifting efficiency and reinforcing demand within the sustainable packaging market.

Vacuum bag maker Moda, acquired by Amcor, deploys AI to meter film length precisely, trimming waste during poultry and cheese packing operations. Regulatory focus on transport-packaging emissions further drives investment toward lighter yet robust secondary and tertiary solutions.

Note: Segment shares of all individual segments available upon report purchase

By End User: E-commerce Transformation Accelerates Adoption

Food and beverage retained 38.32% of 2024 revenue but faces the fastest competitive encroachment from online retail, advancing 12.89% CAGR. The sustainable packaging market size for e-commerce formats benefits from high order volumes, enabling payback on machinery upgrades like paper mailer automation and reusable tote trials.

Luxury cosmetics house Estée Lauder reports 71% of packaging already meets “5 R” criteria and targets 100% by 2025, illustrating premium-segment pull through circular innovations. Pharmaceutical adoption of wood-based PET further diversifies the sustainable packaging industry customer base.

Geography Analysis

Europe’s 34.57% revenue share in 2024 reflects its first-mover regulatory stance that has birthed mature recycling infrastructure and eco-design norms. EPR fee modulation by circularity performance incentivizes high-recycled-content packaging, reinforcing supplier innovation cycles. Harmonized deposit-return schemes streamline collection, making Europe the reference market for both advanced recycling pilots and bio-based material commercialization. Multinational brand headquarters located in the region further amplify demand density, ensuring the sustainable packaging market continues to test and scale breakthroughs locally.

Asia-Pacific is on track for the fastest 11.21% CAGR thanks to tightening rules in Japan, South Korea, Australia, and pilot EPR frameworks in China and India. Japan’s recycled-plastic mandate effective 2024 and its positive list for food-contact recycled resins entering force in June 2025 unlock high-margin applications and spur domestic resin reprocessing investments. China’s evolving supervision policy for recycled plastics coupled with strong e-commerce growth accelerates volume uptake. Vietnam’s paper-packaging sector, projected at USD 3.5 billion by 2026, exemplifies regional expansion anchored in export-oriented manufacturing.

North America benefits from state-level EPR adoption and aggressive voluntary commitments by consumer-goods leaders. Oregon, Colorado, and California programs fund curbside upgrades, boosting PCR feedstock availability and narrowing cost spreads. Greenwashing litigation—exemplified by Australia’s recent Clorox action—raises disclosure rigor, bolstering consumer trust and driving transparent supply chains. Middle East & Africa and South America remain nascent but show rapid policy convergence, opening white-space opportunities for early technology entrants as infrastructure scales.

Competitive Landscape

Innovation and Sustainability Drive Future Success

Success in the sustainable packaging market increasingly depends on companies' ability to innovate while maintaining cost competitiveness and meeting stringent environmental standards. Market leaders are investing heavily in developing new materials and technologies that can replace traditional packaging solutions while maintaining or improving functionality. Companies are also focusing on building strong relationships with end-users through collaborative development projects and customized solutions. The ability to scale up sustainable solutions while maintaining price competitiveness remains crucial, as does the capacity to adapt to evolving regulatory requirements and changing consumer preferences.

For new entrants and smaller players, success lies in identifying and exploiting specific market niches where they can offer unique value propositions. This includes developing specialized sustainable packaging solutions for specific industries or applications, or focusing on particular geographical markets where they can build a strong local presence. Companies must also carefully navigate the increasing regulatory pressure around packaging sustainability and recycling requirements, which can create both challenges and opportunities. The risk of substitution from alternative packaging solutions remains a constant consideration, driving the need for continuous innovation and improvement in sustainable packaging offerings. Building strong relationships with key stakeholders across the value chain, from raw material suppliers to end-users, is becoming increasingly important for long-term success in the market. Eco-friendly packaging companies and green packaging companies are at the forefront of these efforts, continuously innovating to meet consumer and regulatory demands.

Sustainable Packaging Industry Leaders

-

Amcor plc

-

Smurfit WestRock

-

Sonoco Products Company

-

Sealed Air Corporation

-

Mondi plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2025: Amcor and Berry Global announced an all-stock merger, forming the world’s largest consumer-packaging company and allocating USD 180 million annually to sustainability-focused R&D.

- January 2025: Amcor launched Lift-Off Sprints and Lift-Off Connect, offering USD 3 million annually to startups working on AI-driven waste recognition and reusable systems.

- January 2025: Amcor secured a European patent for AmFiber Performance Paper, a recyclable high-barrier solution for food and healthcare packaging

- November 2024: B’Zeos raised EUR 5 million to scale seaweed-based compostable films, partnering with Nestlé on pilot applications

Global Sustainable Packaging Market Report Scope

Sustainable packaging is the development and use of packaging, resulting in improved sustainability. The study aims to analyze and understand the sustainable packaging market's current growth, opportunities, and challenges. The sustainable packaging market is segmented by process (reusable packaging, degradable packaging, and recycled packaging), material type (glass, plastic, metal, and paper), end user (pharmaceutical and healthcare, cosmetics and personal care, food and beverage, and other end users), and geography (North America, Europe, Asia-Pacific, Latin America, and Middle East and Africa). The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| Reusable Packaging |

| Recyclable Packaging |

| Compostable / Biodegradable Packaging |

| Edible Packaging |

| Paper and Paperboard |

| Plastics |

| Glass |

| Metal (Aluminum, Steel) |

| Plant-based Materials (Bagasse, Mushroom, etc.) |

| Rigid |

| Flexible |

| Primary Packaging |

| Secondary Packaging |

| Tertiary / Transport Packaging |

| Food and Beverage |

| Pharmaceutical and Healthcare |

| Cosmetics and Personal Care |

| E-commerce and Retail |

| Consumer Electronics |

| Other End User |

| North America | United States | |

| Canada | ||

| Mexico | ||

| Europe | Germany | |

| United Kingdom | ||

| France | ||

| Italy | ||

| Spain | ||

| Russia | ||

| Rest of Europe | ||

| Asia-Pacific | China | |

| India | ||

| Japan | ||

| South Korea | ||

| Australia and New Zealand | ||

| Rest of Asia-Pacific | ||

| Middle East and Africa | Middle East | United Arab Emirates |

| Saudi Arabia | ||

| Turkey | ||

| Rest of Middle East | ||

| Africa | South Africa | |

| Nigeria | ||

| Egypt | ||

| Rest of Africa | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| By Process | Reusable Packaging | ||

| Recyclable Packaging | |||

| Compostable / Biodegradable Packaging | |||

| Edible Packaging | |||

| By Material Type | Paper and Paperboard | ||

| Plastics | |||

| Glass | |||

| Metal (Aluminum, Steel) | |||

| Plant-based Materials (Bagasse, Mushroom, etc.) | |||

| By Packaging Format | Rigid | ||

| Flexible | |||

| By Function | Primary Packaging | ||

| Secondary Packaging | |||

| Tertiary / Transport Packaging | |||

| By End User | Food and Beverage | ||

| Pharmaceutical and Healthcare | |||

| Cosmetics and Personal Care | |||

| E-commerce and Retail | |||

| Consumer Electronics | |||

| Other End User | |||

| By Geography | North America | United States | |

| Canada | |||

| Mexico | |||

| Europe | Germany | ||

| United Kingdom | |||

| France | |||

| Italy | |||

| Spain | |||

| Russia | |||

| Rest of Europe | |||

| Asia-Pacific | China | ||

| India | |||

| Japan | |||

| South Korea | |||

| Australia and New Zealand | |||

| Rest of Asia-Pacific | |||

| Middle East and Africa | Middle East | United Arab Emirates | |

| Saudi Arabia | |||

| Turkey | |||

| Rest of Middle East | |||

| Africa | South Africa | ||

| Nigeria | |||

| Egypt | |||

| Rest of Africa | |||

| South America | Brazil | ||

| Argentina | |||

| Rest of South America | |||

Key Questions Answered in the Report

What is the current size of the sustainable packaging market?

The sustainable packaging market size is valued at USD 303.80 billion in 2025 and is projected to reach USD 433.49 billion by 2030.

Which region leads in market share today?

Europe holds the largest regional share at 34.57% thanks to early adoption of circular-economy regulations.

What segment is growing fastest by process?

Compostable and biodegradable packaging is expanding at a 12.54% CAGR through 2030, outpacing other process categories.

Why does flexible packaging gain traction?

Mono-material pouches cut material weight and improve recyclability, driving an 8.43% CAGR that exceeds rigid-format growth.

How are EPR laws influencing market growth?

Harmonized EPR frameworks across 63 countries standardize compliance requirements, enabling brands to scale a single package design globally and adding an estimated 1.8 percentage points to forecast CAGR.

What are the main bottlenecks hindering faster adoption?

Limited supplies of food-grade PCR resins and persistent cost premiums over virgin plastics remain key constraints, dampening near-term expansion.

Page last updated on: