Aquafeed Additives Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 3.03 Billion |

| Market Size (2031) | USD 3.79 Billion |

| Growth Rate (2026 - 2031) | 4.55% CAGR |

| Fastest Growing Market | Europe |

| Largest Market | Asia Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Aquafeed Additives Market Analysis by Mordor Intelligence

Aquafeed Additives Market size market size in 2026 is estimated at USD 3.03 billion, growing from 2025 value of USD 2.9 billion with 2031 projections showing USD 3.79 billion, growing at 4.55% CAGR over 2026-2031. Strong demand for functional nutrition, tighter antibiotic-use rules, and finite fishmeal supplies are steering feed formulators toward precision-engineered additives that raise feed conversion efficiency and protect fish health. Europe’s regulatory push for sustainable aquaculture and Asia-Pacific’s production scale jointly underpin volume growth, while emerging protein sources such as single-cell biomass widen the portfolio of compatible additives. Investments in AI-driven feeding systems that cut wastage by 10-20% further enhance uptake, especially among high-value salmon and shrimp operators. Volatile fishmeal prices and lengthy approval timelines temper progress, yet government incentive programs from the European Union's (EU’s) Horizon funds to Saudi Arabia’s Vision 2030 offset part of the risk.

Key Report Takeaways

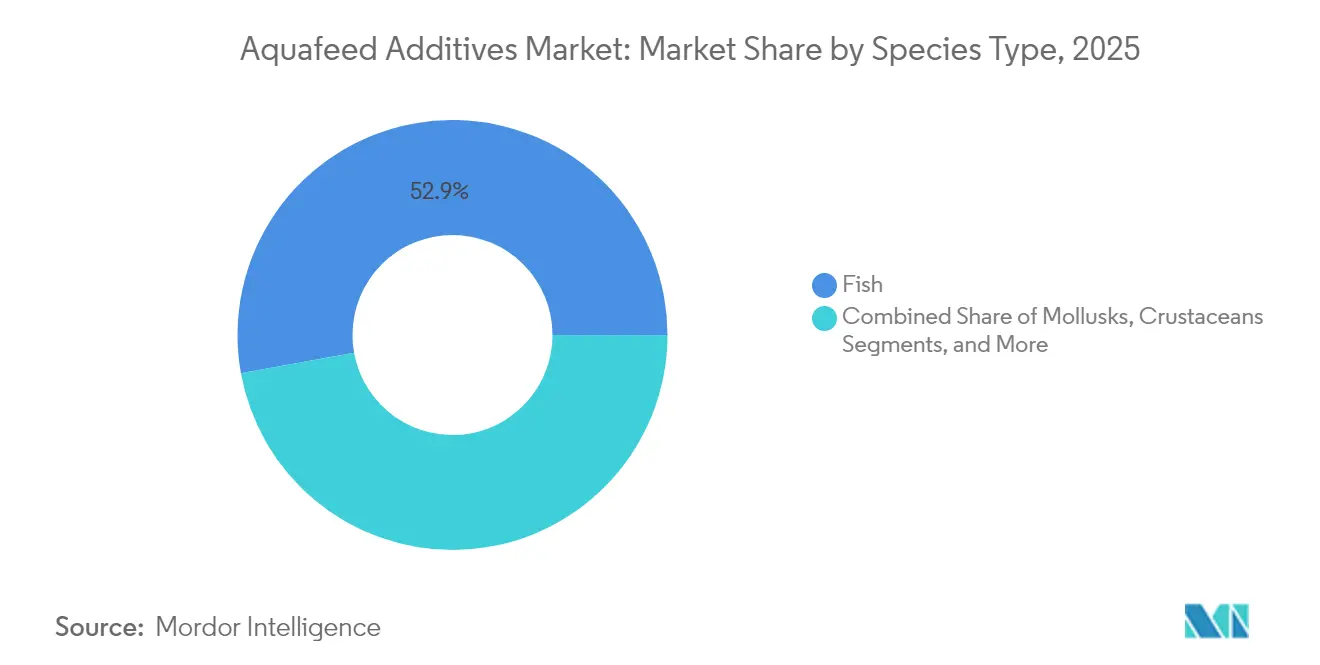

- By species type, fish held 52.85% of the aquafeed additives market share in 2025, while crustaceans are projected to rise at a 8.92% CAGR by 2031.

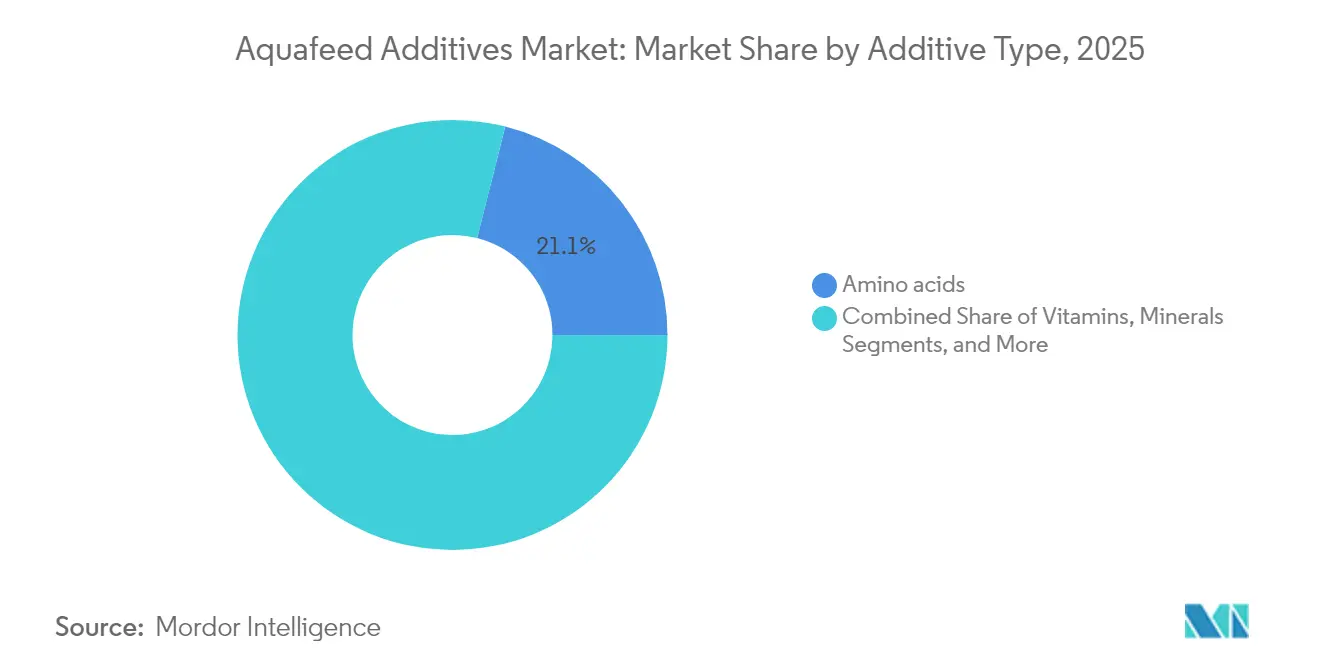

- By additive type, amino acids led with 21.05% of the aquafeed additives market size in 2025; probiotics and prebiotics post the fastest growth at 9.21% CAGR.

- By form, dry extruded pellets accounted for 67.05% of the aquafeed additives market size in 2025, and the micro-encapsulated powders are projected at an 10.78% CAGR.

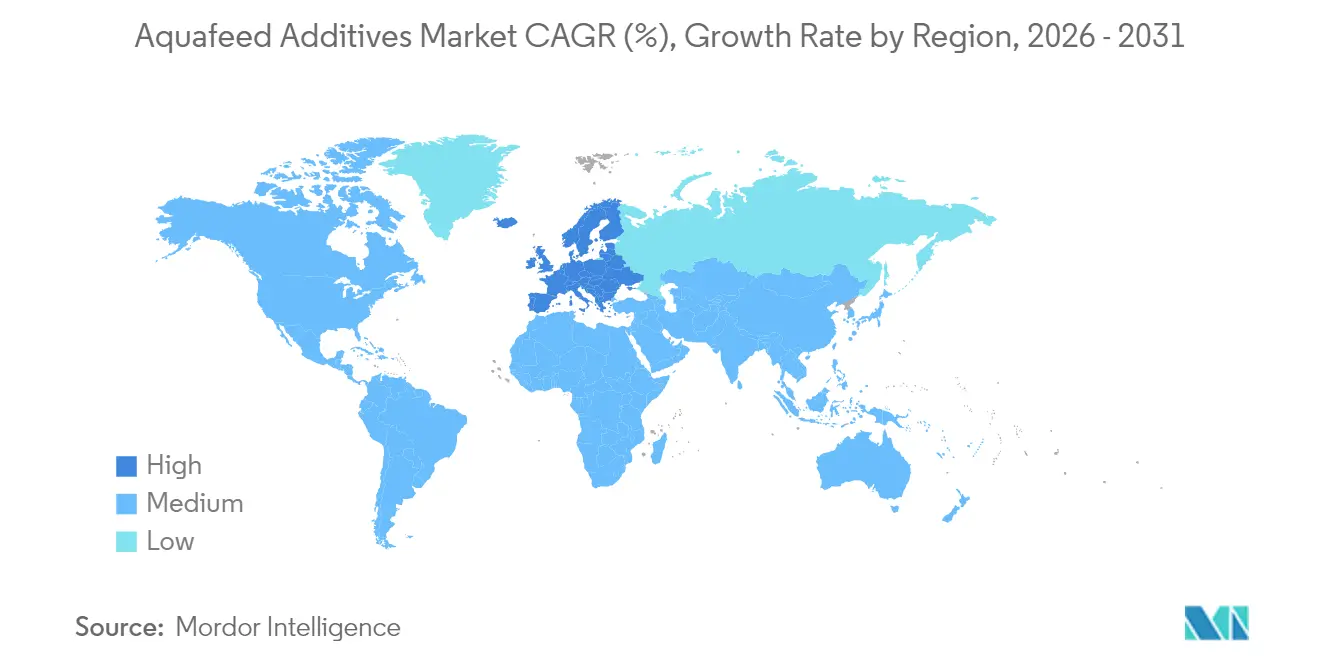

- By geography, Asia-Pacific captured 61.05% revenue share in 2025, but Europe registers the highest regional CAGR of 8.05% through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Aquafeed Additives Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising global seafood consumption and protein shift | +1.2% | Global, strongest in Asia-Pacific and Europe | Medium term (2-4 years) |

| Expansion of intensive aquaculture capacity | +0.9% | Asia-Pacific core, spill-over to Middle East and Africa | Long term (≥4 years) |

| Government subsidies and sustainability mandates in aquaculture | +0.7% | Europe and North America, rising in Middle East | Medium term (2-4 years) |

| Functional additives replacing in-feed antibiotics | +0.8% | Global, led by EU, adopted in Asia-Pacific | Short term (≤2 years) |

| Carbon-footprint labeling spurring micro-algae and single-cell additives | +0.5% | Europe and North America | Long term (≥4 years) |

| AI-driven precision feeding enabling higher specialty-additive inclusion | +0.4% | Europe, North America, select Asia-Pacific | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Global Seafood Consumption and Protein Shift

Global protein demand is moving toward aquatic sources. Africa alone is forecast to raise seafood intake from 10 million metric tons to 29 million metric tons by 2050,[1]NTU, “Future Fish Demand in Africa,” ntu.edu.sg a trajectory mirrored in Asia, where tilapia integrators are localizing feed mills to cut imports. FAO expects farm-raised fish prices to climb 24% by 2030, encouraging producers to adopt additives that deliver faster growth and shorten production cycles. Retailers such as Albert Heijn now stock shrimp fed on insect meal and algal oil, signaling buyer acceptance of alternative feed technologies. This demand pivot supports amino acid and enzyme use in plant-based diets that replace fishmeal while sustaining optimal amino-acid profiles for performance. Consequently, the aquafeed additives market gains resilience against fishmeal volatility.

Expansion of Intensive Aquaculture Capacity

Saudi firm NAQUA operates 500 ponds and targets 250,000 metric tons of annual output by 2030, highlighting the global shift toward high-density systems that rely on robust probiotic and water-quality programs. In China, intensive shrimp farms produced 2.09 million metric tons in 2022, yet faced germplasm depletion and disease risks that drive uptake of immune-boosting additives. Recirculating aquaculture systems and biofloc require precision nutrient packages to sustain microbial balance, creating premium demand pockets. The aquafeed additives market, therefore, benefits from clustered, technology-driven expansions across Asia, the Middle East, and South America.

Government Subsidies and Sustainability Mandates in Aquaculture

The EU-funded Care4Aqua project channels EUR 4.8 million (USD 5.05 million) into antibiotic-free feed solutions and selective breeding support, accelerating additive trials that target water quality and immunity. Updated European green-feed codes reward sustainable formulations, while the US Strategic Plan for Aquaculture advances infrastructure backing that welcomes novel additives.[2]USDA, “Strategic Plan for Aquaculture Economic Development,” usda.gov In Saudi Arabia, SALIC’s acquisition of a 42.4% stake in NAQUA aligns with state-driven scale-up goals, channeling funds into feed plants and additive partnerships. Nonetheless, fragmented subsidy reporting hampers full market transparency. Overall, policy incentives lower (Capital Expenditure) CAPEX risk and accelerate product validation across the aquafeed additives market.

Functional Additives Replacing In-Feed Antibiotics

European Union approval of juniper essential oil for all food-producing animals underscores the regulatory preference for phytogenic antimicrobials over antibiotics. Probiotic Bacillus licheniformis cultures have yielded superior growth and survivability in hybrid grouper trials. Studies indicate that digital monitoring platforms can effectively track probiotic performance in aquaculture, supporting integration with data-driven feeding systems. FDA (Food and Drug Administration) guidance has clarified petition routes, yet mandates exhaustive safety dossiers that lengthen lead times. Turmeric oil’s quorum-sensing disruption against Aeromonas hydrophila exemplifies dose-dependent pathogen control via botanicals. The aquafeed additives market thus pivots toward multi-functional blends that satisfy health, regulatory, and consumer criteria.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile fishmeal and fish-oil pricing impacting additive cost pass-through | -0.8% | Global, strongest in cost-sensitive Asian markets | Short term (≤ 2 years) |

| Stringent multi-region approval timelines for novel feed additives | -0.6% | Europe and North America regulatory markets, affecting global launches | Medium term (2-4 years) |

| Micro-plastics scrutiny on pellet binders and coating agents | -0.4% | Europe and North America, emerging concerns in Asia-Pacific | Medium term (2-4 years) |

| Climate-induced crop failures tightening phytobiotic supply | -0.5% | Global, especially Mediterranean and tropical regions | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile Fishmeal and Fish-Oil Pricing Impacting Additive Cost Pass-Through

Volatile fishmeal and fish-oil prices disrupt aquafeed additive manufacturers, complicating cost pass-through and profitability. Peru’s 300% surge in fishmeal output lifted global production by 75% in January 2025, yet price swings restrict manufacturers’ ability to price through additive premiums. Fish oil output climbed 34%, but suppliers leveraged compressed margins as feed makers struggled to absorb dual cost pressures. China’s aquafeed output fell 3.5% in 2024 amid flooding and farmer cost-cutting, illustrating how volatility curbs additive uptake. FAO foresees fishmeal prices rising 30% by 2030, quickening the search for insect meal or single-cell proteins that demand new additive calibrations. Supply-chain uncertainty, particularly the reliance on frozen fish inputs until September 2025, complicates inventory planning for the aquafeed additives market.

Stringent Multi-Region Approval Timelines for Novel Feed Additives

Lengthy evaluation processes, varying compliance requirements, and extensive safety trials delay market entry, increasing costs for innovators. EFSA (European Food Safety Authority) authorizations average 3-4 years, and the 2021 Transparency Regulation layers extra disclosure steps that can trigger resubmissions if data gaps appear. The Magni-PHI case for poultry shows that toxicology and environmental studies often extend beyond the initial scope before approval. In the US, Food Additive Petitions remain the most onerous path, prompting some developers to pursue (Generally Recognized as Safe) GRAS or AAFCO (Association of American Feed Control Officials) listing first. Divergent dossiers for EU and US regulators elevate legal and scientific costs, a drag on smaller innovators. Mealworm-powder authorization in January 2025 came two years after European Food Safety Authority (EFSA) safety clearance, illustrating typical pacing.[3]European Commission, “EU Strategic Guidelines for Sustainable Aquaculture,” ec.europa.eu Such lags defer revenue capture across the aquafeed additives market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Species Type: Fish Hold the Majority While Crustaceans Lead Growth

Fish represented 52.85% of the aquafeed additives market share in 2025, remaining the largest consumer group due to the extensive farming of salmon, tilapia, and carp globally. This dominance converted into an estimated USD 1.53 billion slice of the aquafeed additives market size in 2025, illustrating the purchasing power of operators that have standardized additive protocols to safeguard feed-conversion ratios. Salmon producers in Norway and Chile continue to layer functional amino acids and antioxidants that counteract stress during high-density grow-out and transport phases, the Asian carp farms emphasize cost-effective vitamin and enzyme packages to hit tight feed budgets. Established feed mills already integrate digital traceability, so any additive that demonstrates a measurable uplift in feed efficiency or fillet yield quickly scales through long-term supply contracts. Consequently, fish farming sets the baseline specification that most suppliers use when validating new ingredients.

Crustaceans, led by shrimp, display the fastest adoption curve with a 8.92% CAGR through 2031 as producers justify the higher additive spend to offset still-elevated disease risks and achieve premium coloration. Trials using 5% astaxanthin-rich krill oil have delivered 100% survival under salinity stress while raising market value through deeper pigmentation, reinforcing willingness to pay for specialty inputs. Chinese farmers continue turning to multi-phase functional diets that include immunostimulant probiotics, the South American growers focus on encapsulated phytogenics that resist leaching in brackish ponds. Mollusks and niche species such as sea cucumbers remain small but notable, with micronized mineral blends enhancing shell strength and texture attributes that fetch superior prices in gourmet channels. As demand diversifies, suppliers tailor species-specific additive bundles, positioning the aquafeed additives market for steady volume and value gains across distinct production segments.

By Form: Micro-Encapsulation Transforms Delivery Systems

Dry extruded pellets dominated with 67.05% of the aquafeed additives market share in 2025, translating into the largest slice of the aquafeed additives market size because most commercial ponds and cages already rely on automated feeders that dispense uniform pellets with predictable sink rates. High output lines in Asia and South America prefer this form since its hardness, moisture profile, and dust level can be adjusted quickly to suit species' needs while keeping production costs low. Feed mills now fine-tune pellet matrices with heat-stable enzymes and encapsulated vitamins to cut nutrient losses during extrusion and subsequent bulk handling. Operators also monitor pellet breakage because fines clog precision feeders and inflate wastage, prompting suppliers to refine binder ratios and introduce optical sorters for tighter quality control.

Micro-encapsulated powders post the fastest 10.78% CAGR through 2031 as coacervation and electrostatic spray drying shield sensitive bioactives from heat and humidity, extending shelf life to 18 months under warehouse conditions. Encapsulation efficiencies as high as 99% preserve omega-3 fatty acids, essential oils, and probiotics until they hit the gut, which improves efficacy and lets formulators lower inclusion rates without sacrificing performance. Uniform particle size supports homogeneous dispersion in mash or pellet coatings, reducing hotspot risks that can trigger palatability dips or off-flavors. As farms install AI-guided dispensers capable of dosing micron-scale supplements directly into water columns, demand for low-dust, free-flowing powders is set to accelerate. Together, these trends are reshaping formulation strategy, pushing suppliers to balance the cost advantages of traditional pellets with the performance edge that advanced encapsulation brings.

By Additive Type: Probiotics Surge Past Traditional Categories

Amino acids retain a 21.05% market share in 2025, anchoring protein synthesis in diets and pushing fishmeal replacement above 35%. Probiotics and prebiotics exhibit a 9.21% CAGR, reflecting broad regulatory endorsement and field efficacy. Multi-strain blends at 2 grams per kilogram have enhanced growth and antioxidant enzyme activity in Cirrhinus mrigala, reducing FCR by 0.1 points on average. The aquafeed additives market size for probiotics is projected to climb from USD 0.38 billion in 2026 to USD 0.59 billion in 2031.

Enzyme innovation is another lever. Protease inclusion raises amino-acid digestibility, while phytase unlocks bound phosphorus, curbing mineral leaching in ponds. Vitamins A and E in nano-emulsions see uptake during temperature stress events, supporting oxidative resilience. Meanwhile, microbial astaxanthin from Phaffia rhodozyma offers a scalable alternative to crustacean by-product extraction, freeing supplies for salmonids. Collectively, these shifts deepen product diversity across the aquafeed additives market.

Geography Analysis

Asia-Pacific contributed 61.05% of global revenue in 2025 and continues to anchor volume growth, led by China’s shrimp production surpassing 2 million metric tons. Disease outbreaks and protein-source shifts compel farms to layer immune-enhancing additives on top of core amino-acid packages. Vietnam and India are expanding export-oriented aquaculture, but price sensitivity shapes a two-tier market where premium additives coexist with cost-optimized blends.

Europe’s aquafeed additives market size is projected to expand from USD 0.56 billion in 2026 to USD 0.83 billion by 2031 on an 8.05% CAGR as EU directives elevate sustainability requirements. Norway’s salmon sector leads precision feeding adoption, catalyzing trials of AI-supported dosing systems that elevate functional additive use efficiency. Horizon Europe projects funnel more than EUR 6 million (USD 6.95 million) into green-feed research annually, accelerating the commercialization of algae-derived antioxidants and phytonutrients.

North America presents a mature but innovation-friendly landscape. The US Strategic Plan for Aquaculture backs public-private infrastructures where additive developers pilot novel proteins or bacteriophage solutions under controlled conditions. Canada’s engagement with indigenous rights adds ESG layers that reward eco-friendly formulations. Meanwhile, Mexico’s shrimp operators deepen cross-border supplier ties, boosting additive throughput.

Competitive Landscape

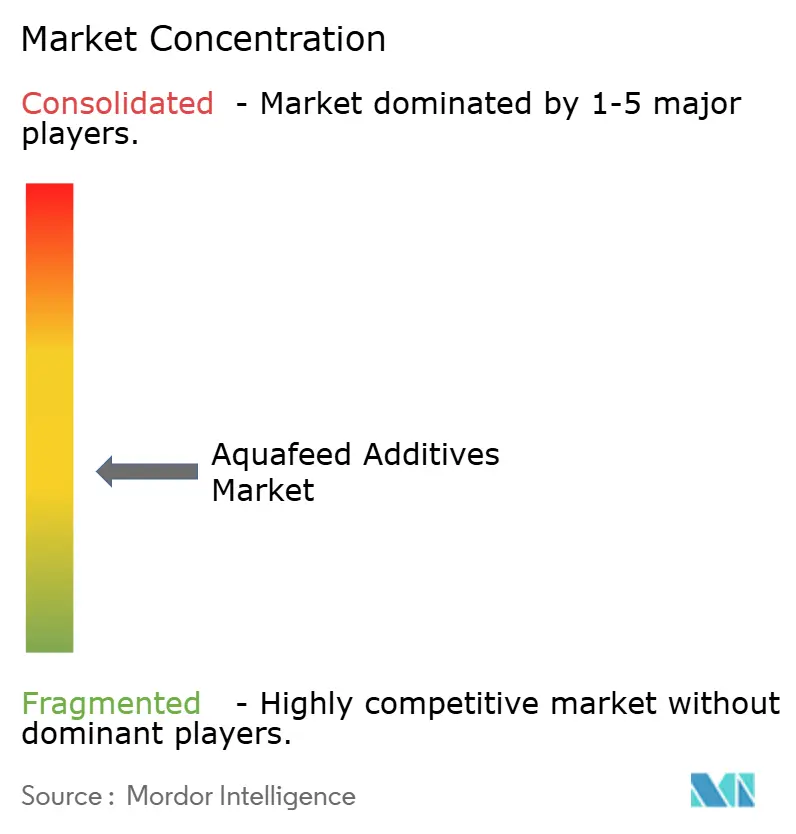

The aquafeed additives market shows moderate fragmentation. Companies like Nutreco N.V. (Skretting), Evonik Industries AG, and Cargill, Incorporated are leveraging integrated chemical and commodity footprints. Their Research and Development budgets exceed USD 200 million annually, funding enzyme and phytogenic platforms. Mid-tier firms like ADM, Alltech, and Nutreco broaden portfolios via acquisitions, exemplified by Alltech’s EUR 7 million (USD 7.57 million) purchase of Raisio’s feed facility to scale Nordic nutrition solutions.

Technology remains a key differentiator. AKVA’s GBP 13.7 million (USD 17.5 million) acquisition of Observe Technologies embeds AI analytics into integrated farm management, a move anticipated to lift feed conversion by 5–7% on early deployments. Venture funding of USD 808 million flowed into aquaculture in the past year, highlighted by eFishery’s USD 200 million round targeting smart-feeding adoption. Start-ups such as String Bio gain traction after securing GRAS (Generally Recognized as Safe) status for microbial proteins, enabling additive pairing with novel substrates.

Expertise in regulatory compliance serves as a competitive advantage, with firms proficient in EFSA (European Food Safety Authority) dossier submissions collaborating with smaller ingredient innovators to accelerate market entry in the EU. Sustainability accreditation carbon labeling, ASC (Aquaculture Stewardship Council) compliance, and traceability platforms now feature heavily in supplier pitches. These dynamics collectively keep the aquafeed additives market competitive yet open to disruption.

Aquafeed Additives Industry Leaders

Nutreco N.V. (Skretting)

BioMar Group

Alltech

Evonik Industries AG

Cargill, Incorporated

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: BioMar Norway has achieved ASC Feed Certification, ensuring its feed production meets sustainability and environmental responsibility standards and supporting Norwegian salmon farms ahead of upcoming certification requirements.

- June 2025: IFB Agro has approved to acquire Cargill India’s shrimp and freshwater fish feed business, including feed formulations, manufacturing facilities, and associated resources, to strengthen its position in the aquafeed sector.

- May 2025: Marfeed, a newly launched brand by MIAVIT GmbH and Arctic Feed Ingredients AS, introduces innovative feed additives designed to enhance aquaculture health, nutrition, and sustainability.

- June 2024: BP Ventures invested USD 30 million in Calysta to support the rollout of its FeedKind protein product aimed at the aquaculture sector, highlighting growing interest in alternative protein sources for aquafeed applications.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the aquafeed additive market as the value and volume of commercially manufactured ingredients, such as amino acids, enzymes, organic acids, probiotics, antioxidants, binders, and vitamins, deliberately blended into compound aquafeeds to improve growth, health, and feed conversion across finfish and crustacean species. According to Mordor Intelligence analysts, valuations cover first-time sales from additive formulators and premix blenders to feed mills or integrators, expressed in USD and metric tons.

Scope exclusion: home-mixed on-farm additives and pharmaceutical water treatments are left outside the market boundary.

Segmentation Overview

- By Species Type

- Fish

- Salmonids

- Tilapia

- Carp

- Catfish

- Mollusks

- Crustaceans

- Others

- Fish

- By Additive Type

- Vitamins

- Minerals

- Antioxidants

- Amino Acids

- Enzymes

- Acidifiers

- Probiotics and Prebiotics

- Phytogenics and Essential Oils

- Others (Carotenoids/Astaxanthin, Pellet Binders/Bentonite, etc.)

- By Form

- Dry Extruded Pellets

- Moist Pellets

- Micro-encapsulated Powders

- By Geography

- North America

- United States

- Canada

- Mexico

- Rest of North America

- Europe

- Germany

- United Kingdom

- France

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Vietnam

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East

- Turkey

- Saudi Arabia

- Rest of Middle East

- Africa

- South Africa

- Rest of Africa

- North America

Detailed Research Methodology and Data Validation

Primary Research

Structured calls with nutritionists at Asian and Latin American feed mills, procurement leads at additive blenders, and farm-level veterinarians allowed us to validate species-specific inclusion rates, emerging functional claims, and average selling prices. Regional panels ensured perspectives from high-growth tilapia and shrimp belts, as well as mature salmon clusters.

Desk Research

We began with national aquaculture production files from FAO FishStat, customs codes for HS 2309 additive preparations, and species-wise feed demand sheets released by China's Ministry of Agriculture. Trade association briefs from IFFO, the Global Aquaculture Alliance, and the European Feed Manufacturers Federation helped benchmark fishmeal substitution ratios. Company 10-Ks and investor decks were scanned through D&B Hoovers, while price trajectories for key amino acids and organic acids were pulled from Dow Jones Factiva. These publicly available sources frame baseline volumes, input costs, and regulatory shifts that shape additive uptake. The list cited here is illustrative; many additional open databases and industry periodicals were reviewed during desk work.

Market-Sizing & Forecasting

A top-down demand pool was built by matching 2024 aqua biomass outputs with species-level feed conversion ratios, then applying inclusion-rate ranges for each additive class. Selective bottom-up roll-ups of supplier revenues cross-checked totals. Key variables like global fishmeal prices, soybean protein concentrate share, disease-driven mortality events, shrimp pond intensification, and regulatory caps on in-feed antibiotics enter a multivariate regression that feeds an ARIMA overlay for the 2025-2030 outlook. Gaps in bottom-up lines, for opaque captive volumes, were bridged using normalized ASP bands agreed in expert interviews.

Data Validation & Update Cycle

Model outputs pass three-step variance tests against historical trade flows and listed-company segment sales, followed by peer review and a senior analyst sign-off. We refresh every twelve months, but interim updates trigger when policy shifts or commodity shocks materially alter assumptions.

Why Our Aquafeed Additives Baseline Commands Reliability

Published numbers often differ because each publisher chooses distinct additive baskets, base years, and price curves.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 2.9 B (2025) | Mordor Intelligence | - |

| USD 2.46 B (2025) | Regional Consultancy A | excludes probiotic blends sold via premix channels |

| USD 2.48 B (2025) | Trade Journal B | applies uniform ASPs without species weighting |

| USD 2.42 B (2025) | Industry Association C | uses 2023 feed volumes rolled forward at flat 3 % growth |

Differences stem mainly from narrower product scope, simplified price assumptions, and infrequent refresh cadences. By triangulating multi-source volumes with live ASP intelligence, Mordor delivers a balanced, transparent baseline that decision-makers can trace back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the aquafeed additives market size in 2026?

The aquafeed additives market size stands at USD 3.03 billion in 2026 and is forecast to climb to USD 3.79 billion by 2031 on a 4.55% CAGR.

Which region leads the aquafeed additives market?

Asia-Pacific leads with 61.05% of revenue share in 2025, backed by China’s high-volume aquaculture sector and growing demand for functional feed solutions.

Why are probiotics gaining traction in aquafeed?

Regulatory restrictions on antibiotics and proven immunity benefits push probiotics to a 9.21% CAGR, the highest among additive categories to 2031.

How do fishmeal price swings affect additive demand?

Fishmeal volatility raises overall feed costs, making performance additives crucial for feed-conversion gains but sometimes delaying adoption in cost-sensitive markets.

Which species segment is growing fastest?

Crustaceans exhibit a 8.92% CAGR due to premium shrimp prices and the need for health-enhancing additives in intensive pond and RAS systems.

What technologies are reshaping the aquafeed additives industry?

AI-driven precision feeding, micro-encapsulation for bioactive protection, and microbial protein ingredients are notable innovations driving competitive advantage.

Page last updated on: