Subsea Systems Market Size and Share

Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Market Size (2026) | USD 19.75 Billion |

| Market Size (2031) | USD 25.03 Billion |

| Growth Rate (2026 - 2031) | 4.85% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

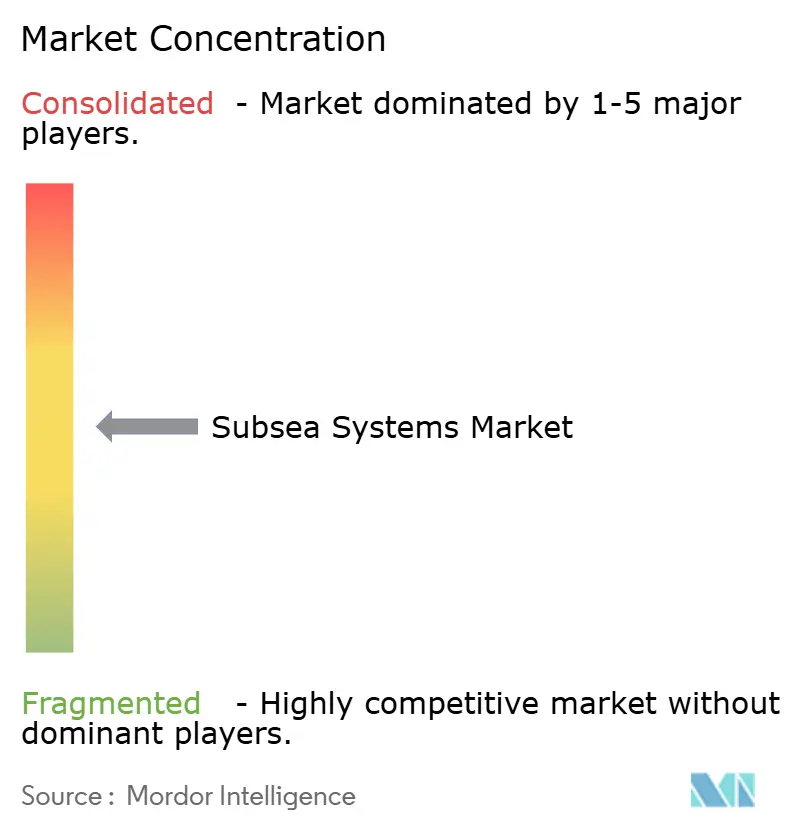

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Subsea Systems Market Analysis by Mordor Intelligence

The Subsea Systems Market size is projected to expand from USD 17.83 billion in 2025 and USD 19.75 billion in 2026 to USD 25.03 billion by 2031, registering a CAGR of 4.85% between 2026 to 2031.

Operators are steering capital toward cost-efficient tie-backs that link new wells to existing floating production, storage, and offloading vessels, cutting unit costs by as much as 40% in deepwater basins.[1]TechnipFMC, “Investor Relations – Projects and Contracts,” technipfmc.com A 23% jump in deepwater project sanctions during 2025, combined with subsea processing advances that pull breakeven prices below USD 40 per barrel, is broadening investment headroom.[2]Rystad Energy, “Offshore Field Sanctions and Investment Trends,” rystadenergy.com Growth is strongest in ultra-deepwater fields, niche high-pressure equipment, and digital technologies that lower inspection, maintenance, and repair outlays. Competitive differentiation revolves around integrated engineering-procurement-construction-installation (EPCI) models, modular standardized hardware, and early moves into carbon-capture and offshore wind subsea infrastructure. Supply-chain tightness in titanium alloys and semiconductors and policy shifts such as the 2024 Gulf of Mexico leasing moratorium temper momentum, yet the medium-term outlook remains positive.

Key Report Takeaways

- By system type, subsea production systems held 66.1% of the subsea system market share in 2025, while subsea processing systems are forecast to expand at a 5.8% CAGR through 2031.

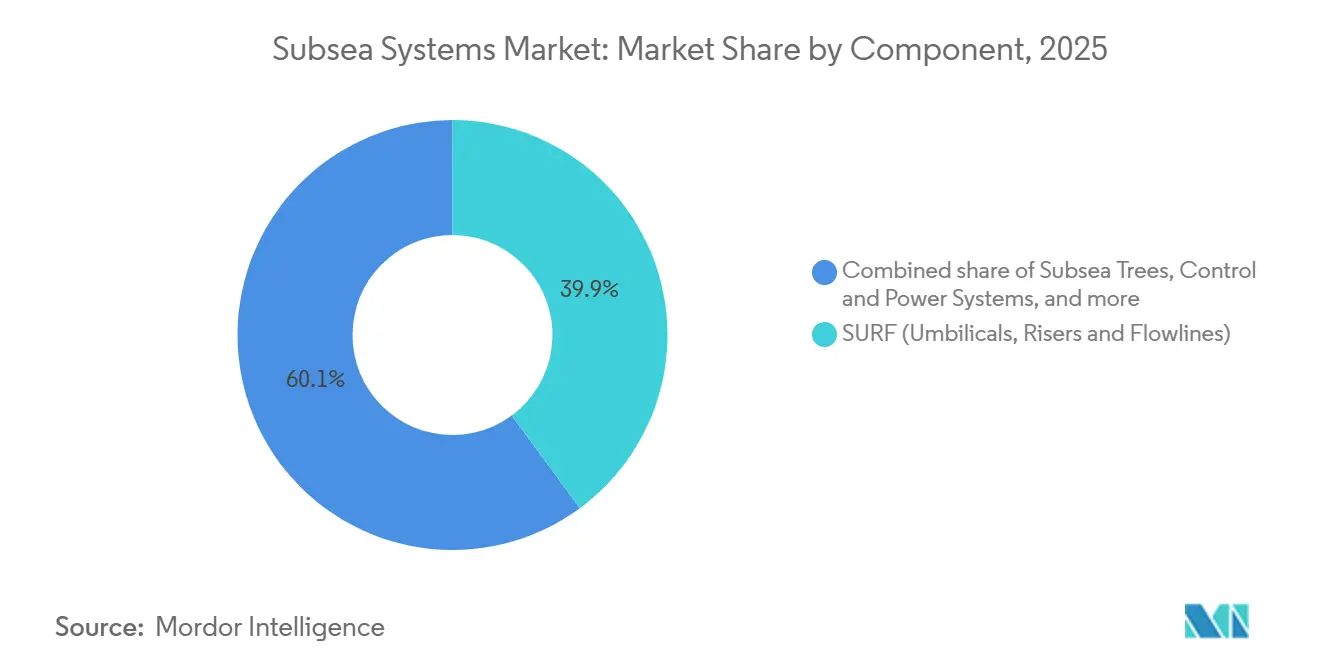

- By component, SURF captured 39.9% of the subsea system market size in 2025 and is projected to grow at a 6.5% CAGR to 2031.

- By water depth, shallow-water projects accounted for 61.5% of the subsea system market share in 2025; ultra-deepwater is advancing at a 7.7% CAGR to 2031.

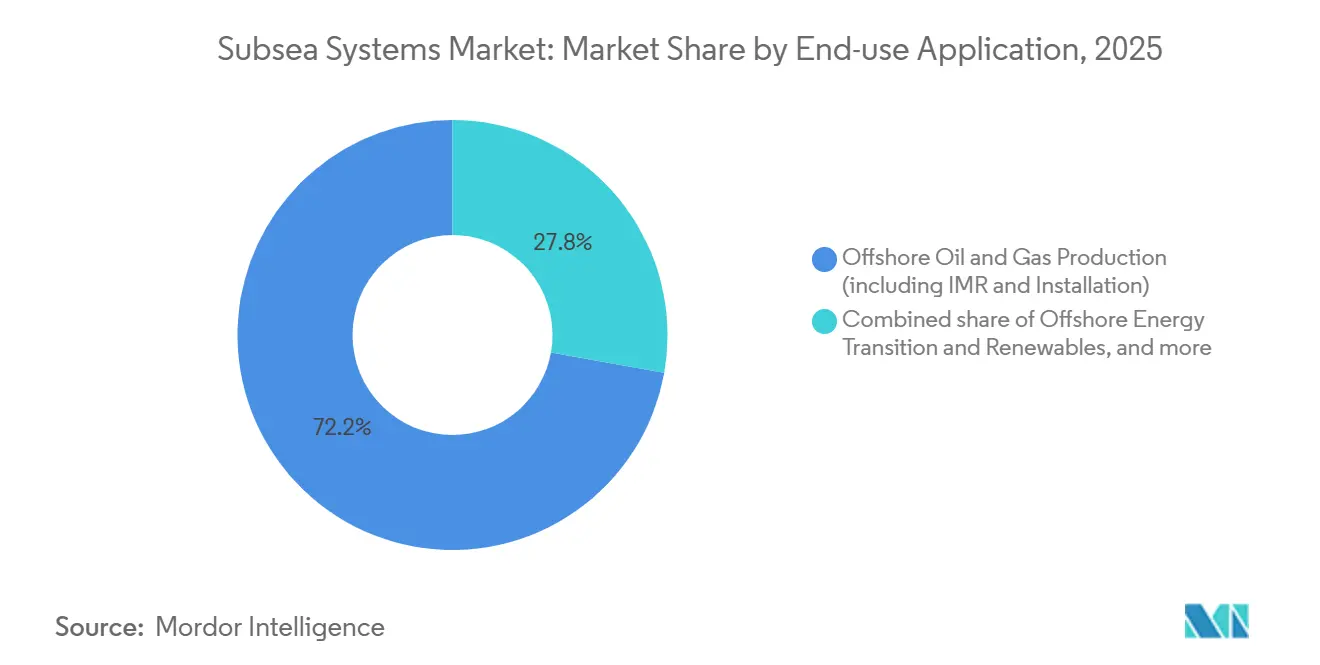

- By end-use application, offshore oil and gas production dominated with 72.2% revenue share in 2025, whereas offshore energy transition and renewables are set to expand at a 14.2% CAGR through 2031.

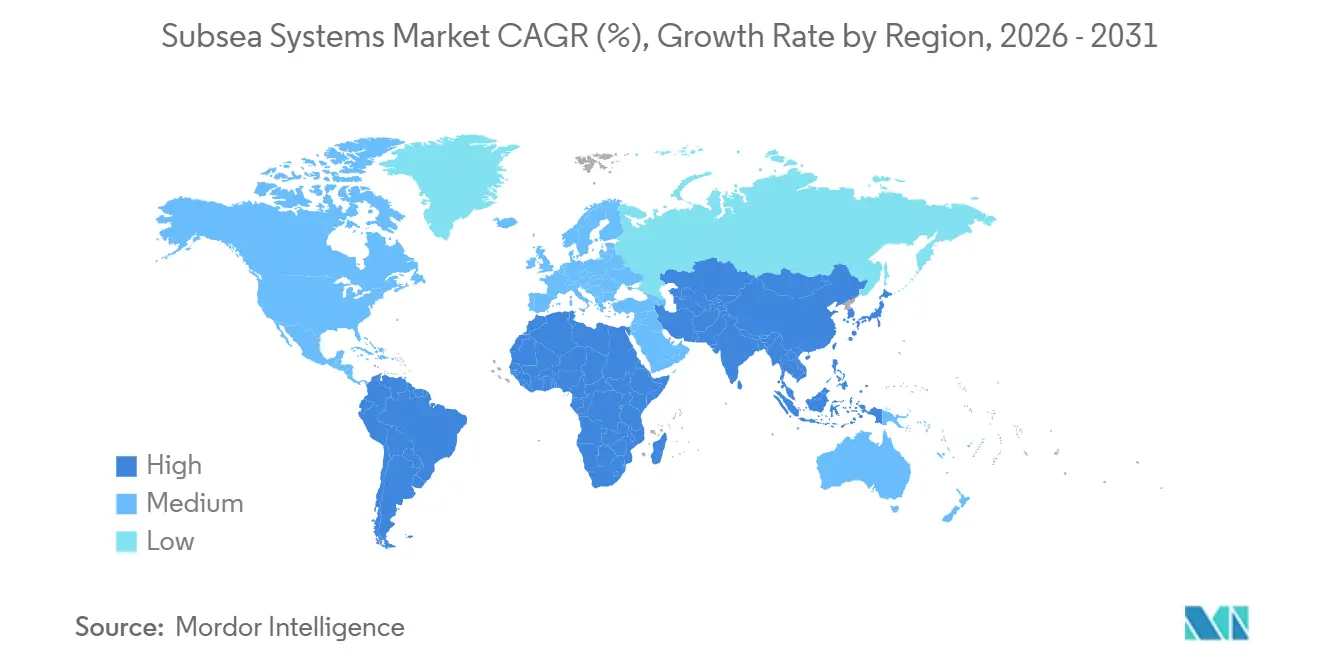

- By geography, North America led with 34.7% subsea system market share in 2025, while Asia-Pacific is projected to post an 11.9% CAGR up to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Global Subsea Systems Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Improved project economics via FPSO tie-backs | +1.2% | Brazil, Guyana, West Africa | Medium term (2-4 years) |

| Surge in deep-/ultra-deepwater field sanctions | +1.5% | South America, Gulf of Mexico, West Africa | Short term (≤ 2 years) |

| Technology advances in boosting and high-pressure equipment | +0.9% | North Sea, Gulf of Mexico, Brazil | Long term (≥ 4 years) |

| Brownfield life-extension and IMR uptrend | +0.7% | North Sea, Gulf of Mexico | Medium term (2-4 years) |

| Early adoption of subsea CO₂-injection infrastructure | +0.4% | Norway, United Kingdom, Australia | Long term (≥ 4 years) |

| Digital-twin and AI-driven predictive maintenance | +0.3% | Norway, United Kingdom, Gulf of Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Improved Project Economics via FPSO Tie-Backs

Eliminating fixed platforms and export pipelines in water depths beyond 1,000 m trims upfront spending by up to 45%.[3]Petrobras, “Pre-Salt Development and Investment Plans 2025-2029,” petrobras.com.br The Búzios field links 24 wells to four FPSOs over a 180 km network and operates at a USD 35 per barrel breakeven compared with USD 55 for fixed-platform layouts. Replicable well templates at ExxonMobil’s Yellowtail project decreased engineering hours by 40% and allowed phased investment that aligns with proven reservoir performance.[4]ExxonMobil, “Guyana Operations – Stabroek Block,” corporate.exxonmobil.com Modularity at Azule Energy’s Caminho FPSO supports future well tie-ins without topside changes, justifying a 15% premium in initial equipment cost.

Surge in Deep-/Ultra-Deepwater Field Sanctions

Forty-seven projects reached final investment decision in 2025, up from thirty-eight in 2024. Petrobras plans 180 new wells and 12 FPSOs in its pre-salt assets to maintain 2.3 million b/d output by 2030. Guyana’s Stabroek Block added three approvals requiring seventy-two trees and 420 km of flowlines in 1,600 m of water. West Africa’s Kaminho and Greater Tortue Ahmeyim phases integrate subsea compression to boost recovery 18% in maturing reservoirs. Chevron’s Anchor, the world’s deepest 20,000 psi field, validated a design unlocking four billion barrels in similar Gulf of Mexico prospects.

Technology Advances in Boosting & High-Pressure Equipment

Fourteen subsea compression stations installed by SLB’s OneSubsea division had added 1.2 billion barrels of recoverable reserves by 2025. Baker Hughes increased Ormen Lange throughput by 280 MMcf/d, deferring a USD 1.8 billion topside expansion. Aker Solutions’ 20,000 psi tree cuts wellhead footprint 30% and supports single-trip installs, saving five vessel days per well. TechnipFMC’s downhole water separation reduced topside load 40% at Mero, shrinking FPSO size and cost.

Brownfield Life-Extension & IMR Spend Uptrend

IMR and brownfield work now capture 38% of subsea capital in mature basins. Equinor invested USD 1.1 billion in Gullfaks to swap twenty-two trees and corrosion-resistant flowlines, adding 150 million barrels of reserves. Oceaneering logged a 34% rise in IMR contracts in 2025, using ROVs that cut diver reliance. Tie-ins cost USD 8-12 million per well with an 18-month payback at oil above USD 60. Digital twins at Aker BP lowered unplanned downtime 22% and extended inspection intervals to five years.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Offshore drilling bans and moratoria | -0.8% | United States, parts of Europe | Short term (≤ 2 years) |

| Oil-price volatility | -0.6% | Global | Short term (≤ 2 years) |

| Supply-chain bottlenecks in alloys and electronics | -0.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Talent shortage in ROV and robotics workforce | -0.3% | North America, Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Offshore Drilling Bans & Moratoria

The 2024 U.S. moratorium withdrew 12 million acres, eliminating demand in areas that once produced 18% of domestic offshore output. Denmark’s plan to halt new North Sea licenses by 2050 stranded USD 3.2 billion in subsea projects. A 78% UK windfall tax deterred four developments needing forty-eight trees. Capital is rerouting to Brazil, Guyana, and the Middle East, which captured 64% of subsea spending in 2025. Shorter investment cycles favor small tie-backs, reducing equipment intensity per field.

Supply-Chain Bottlenecks in Specialty Alloys & Electronics

Titanium Grade 5 sponge shortages raised lead times to 18 months in 2025. Japan and Russia supply 62% of output, prompting requalification at 25-30% higher cost. Indonesia’s nickel ore export ban cut global refined nickel 8%. Advanced logic chips for subsea control modules face 14-month delays under export restrictions, leading some operators to revert to hydraulic systems that offer 15% lower data bandwidth. The IEA projects 35% higher mineral intensity by 2030, amplifying risk.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By System Type: Processing Gains as Production Matures

Subsea processing systems are expected to widen at a 5.8% CAGR to 2031, outpacing the overall subsea system market. Equinor’s Åsgard compression added 306 million boe of reserves in 2024. Baker Hughes’ boosting modules at Ormen Lange increased export by 280 MMcf/d without topside changes. Subsea support and intervention demand is growing 4.2% annually as IMR contracts rise across the North Sea and Gulf of Mexico. Standardized API 17G and ISO 13628 interfaces now cut manufacturing lead times by 20%.

Continued dominance of production systems reflects the 66.1% subsea system market share recorded in 2025, yet growth moderates as greenfield approvals plateau. Integrated EPCI packages reduce delivery schedules, but saturation in conventional trees redirects budget toward compression, boosting, and digital control upgrades. In mature basins, retrofit interventions underpin stable order flow for workover systems.

By Component: SURF Dominates Amid Tie-Back Elongation

SURF captured 39.9% of the subsea system market size in 2025 and will climb at a 6.5% CAGR as tie-backs stretch beyond 150 km in Namibia’s Orange Basin. Steel lazy-wave risers at Mero cut installation time by 40%. Hybrid electro-hydraulic umbilicals with fiber-optic sensing detect thermal anomalies 72 hours sooner than pressure gauges. Subsea trees hold 18.2% share, with 20,000 psi designs enabling deep, high-pressure plays.

Control and power systems are shifting to all-electric architectures that reduce umbilical weight by 40% and double maintenance intervals. ABB’s subsea variable-speed drive at Johan Sverdrup powers pumps directly via an 8 MW link, removing hydraulic units. Manifolds, pumps, and boosting modules represent 17.3% share, with boosting growing 7.1% annually as enhanced recovery programs spread.

By Water Depth: Ultra-Deepwater Accelerates Despite Shallow Dominance

Shallow-water assets still accounted for 61.5% subsea system market share in 2025, benefiting from brownfield tie-backs that cost USD 8-12 million per well. Ultra-deepwater projects in Brazil, Guyana, and new West African plays support a 7.7% CAGR, driven by resource concentration and advanced 20,000 psi hardware. Chevron’s Big Foot uses shallow-water-proven tree designs adapted for ultra-deep pressures, proving cross-depth technology transfer.

Deepwater (500-1,500 m) held a 23.8% share, with TotalEnergies’ Ikike installing eighteen trees between 1,200 m and 1,400 m. Standardized modular systems under TechnipFMC’s Subsea 2.0 lower costs by 30%, narrowing the economic gap between depth classes.

By End-Use Application: Energy Transition Disrupts Oil & Gas Hegemony

Offshore oil and gas production secured 72.2% subsea system market share in 2025. Capital discipline focuses on high-spec pre-salt assets, such as Petrobras’ USD 64 billion plan through 2029. Saudi Aramco’s Marjan increment adds thirty-six wells in 90 m water, highlighting cost advantages in low-tax regions.

Offshore energy transition and renewables advance at a 14.2% CAGR. Northern Lights and Bifrost CCS projects reuse existing subsea infrastructure, cutting capital costs by more than half. Offshore wind cables for Dogger Bank and Empire Wind create a USD 8.2 billion cable market by 2030. Subsea power and communications grow 8.3% annually, while deep-sea mining remains on hold pending 2027 regulations.

Geography Analysis

North America retained 34.7% subsea system market share in 2025. The Gulf of Mexico drives high-pressure hardware demand, evidenced by Anchor’s seven trees rated for 20,000 psi. Canada’s approval of 5 GW of floating wind off Nova Scotia positions cable suppliers for multi-year contracts. Mexico farm-outs invite low-cost shallow-water tie-backs.

Asia-Pacific is projected to post an 11.9% CAGR through 2031. CNOOC plans to plant 120 trees for Bohai Bay by 2030. ONGC’s KG-DWN-98/2 will place eighteen trees in water deeper than 1,800 m. Petronas sanctioned twenty-four wells for Limbayong and Jerun in 2024. Stricter Chinese environmental assessments add six months to permits but enhance transparency.

Europe stabilizes as operators pivot to life-extension and CCS. Sleipner now injects 1.7 million t/y CO₂ with thirty-year equipment ratings. Twelve UK CCS licenses will need forty injection wells and 200 km of pipelines. South America maintains high-spec tree demand as Petrobras ordered seventy-two units during 2024-2025. Argentina studies a 2 GW floating wind site off Buenos Aires.

Middle East and Africa emerge as swing regions. Marjan will drill thirty-six subsea wells, while ADNOC’s Hail and Ghasha employ our gas manifolds built for 22% H₂S. West Africa’s Kaminho ties fifteen wells via a 12-slot manifold installed by Subsea 7.

Regulatory Landscape

Subsea systems are shaped by offshore safety, environmental permitting, and technical standards that affect equipment qualification and installation schedules. In the United States, the Bureau of Safety and Environmental Enforcement (BSEE) administers offshore oil and gas requirements under 30 CFR Part 250, including expectations around documentation and technology submissions for complex subsea developments such as HPHT and tiebacks.

Standards convergence continues to influence global specifications and supplier qualification. ISO 13628-1:2025 updated requirements for the design and operation of subsea production systems (including low-carbon energy applications), while ISO 14723:2025 sets specifications for subsea pipeline valves that complement API-based practices. In the United Kingdom, project-specific pipeline screening directions issued in 2026, including screening directions for Rosebank Phase 1 SURF installation and other pipeline works, highlight how pre-construction environmental screening and Pipeline Works Authorisation processes gate subsea SURF and related infrastructure activity.

Competitive Landscape

The top five providers, TechnipFMC, Subsea 7, Aker Solutions, Baker Hughes, and SLB OneSubsea, collectively held 58% of global EPCI value in 2025, indicating moderate consolidation. TechnipFMC’s iEPCI model cut Mero-3 schedules by 18 months and trimmed the installed cost by 22%. Subsea Integration Alliance between Aker and Subsea 7 targets 20% cost savings by merging equipment factories with installation fleets.

Technology leadership centers on digital twins, subsea processing, and all-electric control. Aker BP lowered downtime 22% via Cognite-powered models. SLB’s fourteen compression units secure multi-year service revenue. Mid-tiers pivot: Dril-Quip exited commodity trees to focus on harsh-environment risers. Cable makers Prysmian and Nexans diversify into offshore wind, expanding subsea scope. Patent filings, led by TechnipFMC’s twenty-three in 2024, emphasize processing and digital control.

Subsea Systems Industry Leaders

Subsea 7 SA

TechnipFMC PLC

Akastor ASA

National-Oilwell Varco Inc

Baker Hughes Co.

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Short-cycle tiebacks and brownfield programs are supporting repeatable demand for standardized subsea hardware and installation spreads, which benefits suppliers that can package trees, manifolds, control systems, and SURF under integrated delivery models. Contracting evidence shows this pattern continuing in 2026, including Equinor awarding about EUR 536 million for a first wave of subsea tieback projects on the Norwegian Continental Shelf (TWIN, Omega Sor, Tyrihans Nord, and Brime), and Petrobras awarding Subsea7 a supermajor SURF contract (more than USD 1.25 billion) for Sepia 2 in Brazils Santos basin.

Another focus area is electrification and data-rich subsea operations, where operators and contractors are moving away from hydraulic complexity toward all-electric architectures and real-time monitoring to reduce intervention burden and environmental exposure. In Asia-Pacific, subsea scope tied to gas developments and export infrastructure is also opening up demand, reflected in 2026 SLB OneSubsea contracts for a 94.6 km steel tube umbilical for the Kutei North Hub development in Indonesia, plus multi-well subsea packages such as Eni-led Baleine Phase 3 offshore Cote dIvoire. In Europe, CCS-related subsea transport and storage build-outs add an adjacent stream for pipeline, control, and integrity solutions that align with cross-border design and assurance expectations.

Recent Industry Developments

- July 2026: TechnipFMC won multiple subsea contracts from Equinor for tie-back developments offshore Norway (Omega Sor, Brime, Tyrihans Nord, and TWIN). The awards reinforce portfolio-based contracting around standardized tieback templates and integrated delivery, supporting faster execution across several small to mid-sized projects.

- September 2025: Petrobras awarded TechnipFMC a contract for subsea production systems spanning greenfield, brownfield, and revitalization projects, including installation support and life-of-field services. The structure points to continued preference for framework-style subsea procurement that bundles equipment with long-duration service scope.

- August 2024: A VLCC conversion program advanced toward becoming TotalEnergies seventh FPSO in Angola, with a SURF package including about 30 km of subsea flowlines, risers, and umbilicals to connect to a subsea production network. The development highlights ongoing FPSO-led subsea build-outs where SURF content and installation capability drive a significant share of project value.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this report, the subsea systems market is defined as the revenue earned from equipment and integrated systems that operate on the seabed or underwater to enable offshore field development, production support, and subsea connectivity.

Scope exclusions: Onshore oil and gas equipment and general offshore surface platform hardware are excluded unless they are sold as part of a subsea system package.

Segmentation Overview

- By System Type

- Subsea Production Systems

- Subsea Processing Systems

- Subsea Support and Intervention

- By Component

- SURF (Umbilicals, Risers & Flowlines)

- Subsea Trees

- Wellheads

- Manifolds

- Control and Power Systems

- Subsea Pumps and Compressors

- Subsea Boosting Modules

- Other Components (Buoyancy, Valves, Trenchers)

- By Water Depth

- Shallow Water (Up to 500 m)

- Deepwater (500 to 1,500 m)

- Ultra-Deepwater (Above 1,500 m)

- By End-Use Application

- Offshore Oil and Gas Production (including IMR and Installation)

- Offshore Energy Transition and Renewables

- Subsea Power and Communications

- Subsea Mining

- Others (Defense and Security, Subsea Storage, Academic and Research)

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Norway

- United Kingdom

- France

- Italy

- Germany

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- ASEAN Countries

- Rest of Asia-Pacific

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- United Arab Emirates

- Saudi Arabia

- Qatar

- South Africa

- Nigeria

- Algeria

- Rest of Middle East and Africa

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundary, map the value chain, and collect baseline indicators that explain subsea activity levels. We relied on public sources such as energy statistics and outlooks from agencies like the US EIA and IEA, offshore and marine releases from bodies such as the International Maritime Organization, and macro trade indicators from sources such as UN Comtrade.

We also reviewed regulator updates, project award announcements, annual reports, and investor presentations from companies active in subsea equipment and services to understand how demand timing shows up in procurement and common contract structures. In parallel, we used paid subscriptions for company financials and intelligence, patent databases, and an import and export shipment-level database to cross-check whether growth direction matches observed activity signals. The sources listed above are illustrative and not exhaustive, and many other public references were reviewed to support data collection, validation, and clarification.

Primary Interviews and Surveys

Primary work focused on validating what is being bought and installed in subsea developments, and how pricing and lead times shifted across core equipment groups. We spoke with a mix of contractors, component suppliers, and offshore operators across APAC, EMEA, and the Americas so that regional project pipelines and procurement behavior could be reflected in the final assumptions.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 33% | CXOs: 21% | APAC: 45% |

| Mid tier: 45% | Functional/Unit leaders: 20% | EMEA: 35% |

| Smaller Players: 22% | Managers: 59% | Americas: 20% |

Market-Sizing & Forecasting

Sizing started with a top-down build that reconstructs demand from offshore activity signals, then converted that demand into subsea system spending by applying typical equipment intensity by water depth and project type. After the demand pool was set, totals were corroborated using selective bottom-up approximations, including sampled contract values, supplier revenue exposure to subsea, and simple ASP times volume checks on common units like trees, manifolds, and umbilical lengths.

Several practical inputs guided the model, including deepwater and ultra-deepwater project sanctioning pace, subsea tieback intensity versus new developments, installation and intervention cadence, and observed pricing movement tied to steel, fabrication capacity, and vessel availability. For forecasting, scenario analysis was used so the base case reflects the most consistent view from interviews on project timing, inflation pass-through, and schedule slippage risk. Where bottom-up information was incomplete for smaller geographies or niche components, gaps were handled through proxy ratios anchored to comparable basins and then rechecked with expert feedback.

Data Validation & Update Cycle

Outputs were validated through several checks, including comparing implied subsea spending against offshore capex direction, project award momentum, and installed-base related maintenance activity. When large variances showed up at region or system level, assumptions were reviewed again and adjusted only when the supporting signals remained consistent.

Before sign-off, the model and narratives go through a multi-step analyst review so inconsistencies and outliers are flagged and corrected. Reports are refreshed annually, and interim updates are triggered when major project delays, large awards, or policy and price shocks materially change the outlook. Right before delivery, we do a final pass so clients receive the most current view available.

Mordor Intelligence's Subsea Systems Market Size Versus Other Published Estimates

Published values for subsea systems often do not match because authors apply different scope boundaries, year anchors, and rules for counting lumpy project revenue. Another source of difference is how pricing is treated, since subsea equipment orders can shift quickly with steel costs, vessel rates, and lead-time swings.

Subsea tree and SURF award momentum, deepwater project sanctioning cadence, and offshore capex direction are evidence points that keep Mordor Intelligence's estimate tied to near-term purchasing signals rather than only long-range pipelines. Differences still appear when some publishers broaden coverage into wider offshore services, pick an earlier base year that smooths the cycle, or assume faster ASP escalation without checking it against current contract and delivery conditions.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 19.75 B (2026) | |

| Industry Publisher A | USD 22.50 B (2025) | Uses a different base year and appears to count a wider set of subsea functions such as boosting, separation, injection, and compression, which can raise the stated total beyond core system packages in a single-year view. |

| Research Platform B | USD 20.89 B (2024) | Anchors the series earlier and likely smooths project timing, which can shift the reported size in years when awards and installations are uneven across basins and water depths. |

Overall, the spread is mainly explained by base-year choice, how broadly adjacent subsea items are included, and how strongly timing and pricing are smoothed across years. By keeping the market build traceable to clear activity indicators and then checking totals with simple supplier and contract sanity checks, the final number remains easier to reproduce with the same inputs.

Key Questions Answered in the Report

What is the current value of the subsea system market?

The subsea system market size stood at USD 19.75 billion in 2026 and is forecast to reach USD 25.03 billion by 2031.

Which segment grows fastest in the forecast period?

Offshore energy transition and renewables subsea applications are projected to expand at a 14.2% CAGR through 2031.

How significant is SURF in overall spending?

SURF accounted for 39.9% of global subsea system market size in 2025 and is expected to post a 6.5% CAGR up to 2031.

Which region leads demand today?

North America led with 34.7% subsea system market share in 2025, buoyed by deepwater Gulf of Mexico activity.

What role do FPSO tie-backs play in project economics?

Tie-backs to existing FPSOs can cut capital costs up to 40%, lowering breakeven prices to near USD 35 per barrel in deepwater settings.

How does supply-chain risk affect the market outlook?

Long lead times for titanium alloys and semiconductors can add costs and delays, trimming the global CAGR by an estimated 0.5%.

Page last updated on: