API Contract Manufacturing Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

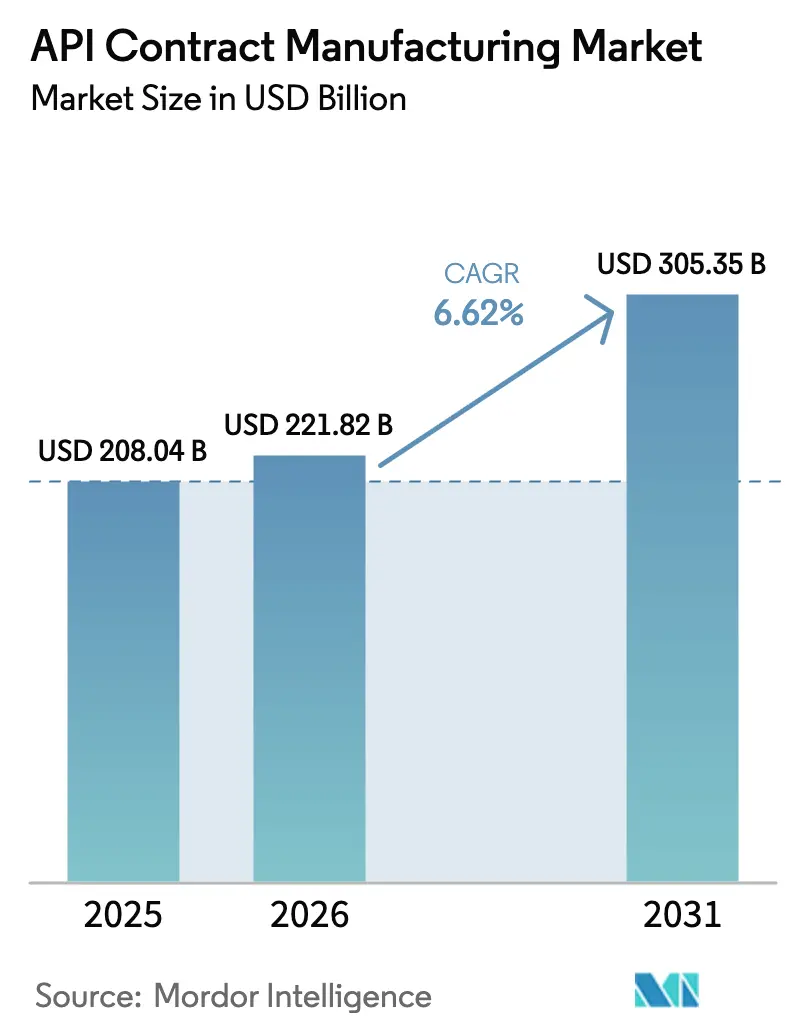

| Market Size (2026) | USD 221.82 Billion |

| Market Size (2031) | USD 305.35 Billion |

| Growth Rate (2026 - 2031) | 6.62% CAGR |

| Fastest Growing Market | North America |

| Largest Market | Asia Pacific |

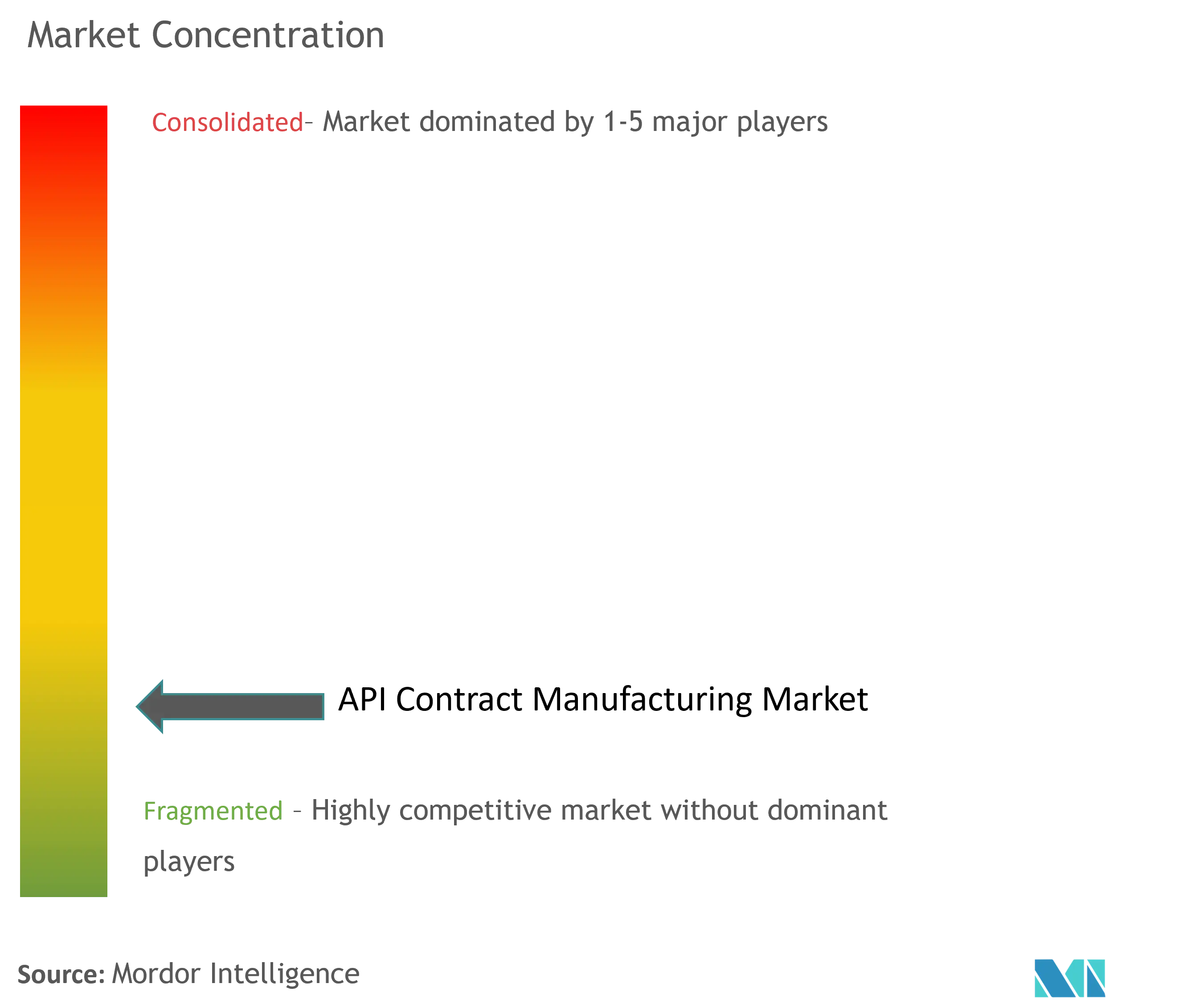

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

API Contract Manufacturing Market Analysis by Mordor Intelligence

The API contract manufacturing market size is expected to grow from USD 208.04 billion in 2025 to USD 221.82 billion in 2026 and is forecast to reach USD 305.35 billion by 2031 at 6.62% CAGR over 2026-2031. Strong momentum comes from the steep rise in outsourcing of complex molecules, escalating demand for high-potency APIs, and widespread adoption of continuous-flow processing, which together are reshaping pharmaceutical supply chains. More than 70% of active pharmaceutical ingredients are now sourced externally, enabling brand-owners to redirect capital toward R&D while leveraging CDMOs’ scale and regulatory know-how. Asia is projected to post a 9.7% CAGR thanks to capacity expansions in India and China, whereas North America preserved a 40.7% API contract manufacturing market share in 2024, anchored by a mature innovation ecosystem and stringent regulatory oversight. Biologics and HPAPIs remain the fastest-growing opportunity pockets, with HPAPI revenue advancing 8.3% annually as oncology pipelines expand. Continuous manufacturing continues to deliver 40-50% cost savings and sizeable ESG gains, reinforcing its strategic appeal to both innovators and contractors.

Key Report Takeaways

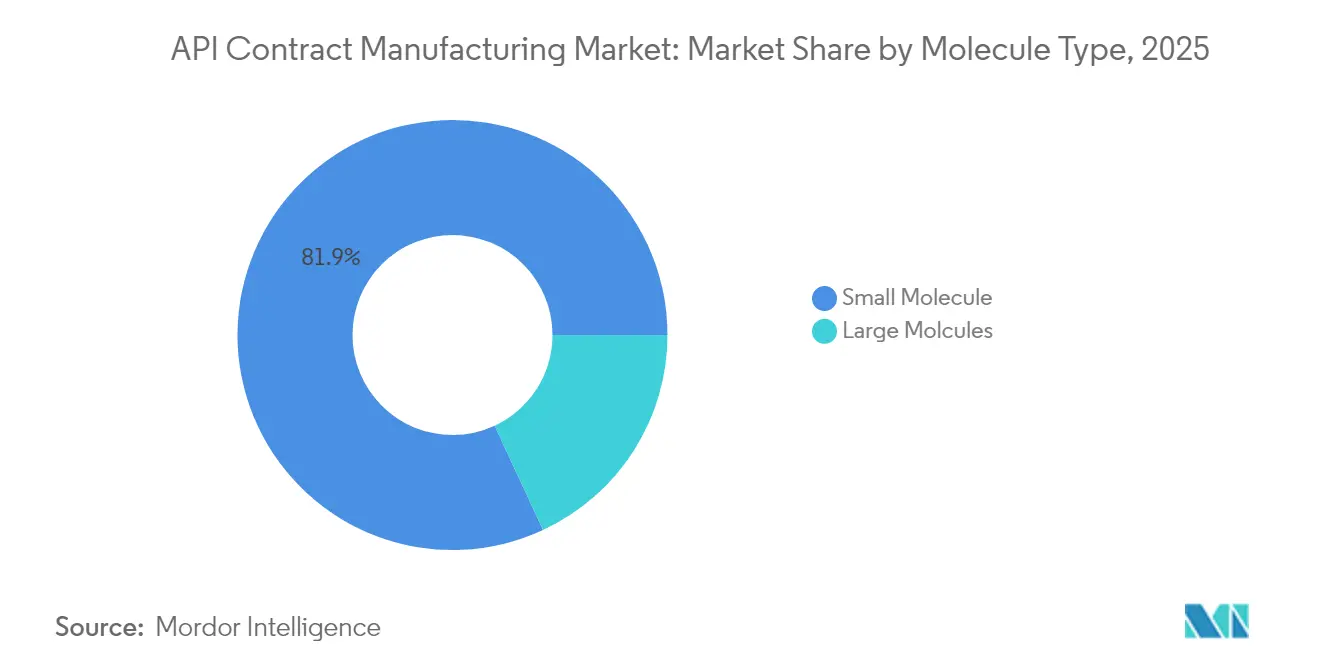

- By molecule type, small molecules dominated with 81.92% of the API contract manufacturing market share in 2025, while biologics are on track to grow at a 6.82% CAGR through 2031.

- By potency, standard-potency APIs held 89.18% of the API contract manufacturing market size in 2025; HPAPIs represent the fastest-growing slice at an 8.02% CAGR.

- By synthesis method, chemical routes captured 70.88% revenue in 2025, yet biotech/fermentation is projected to advance 7.32% per year to 2031.

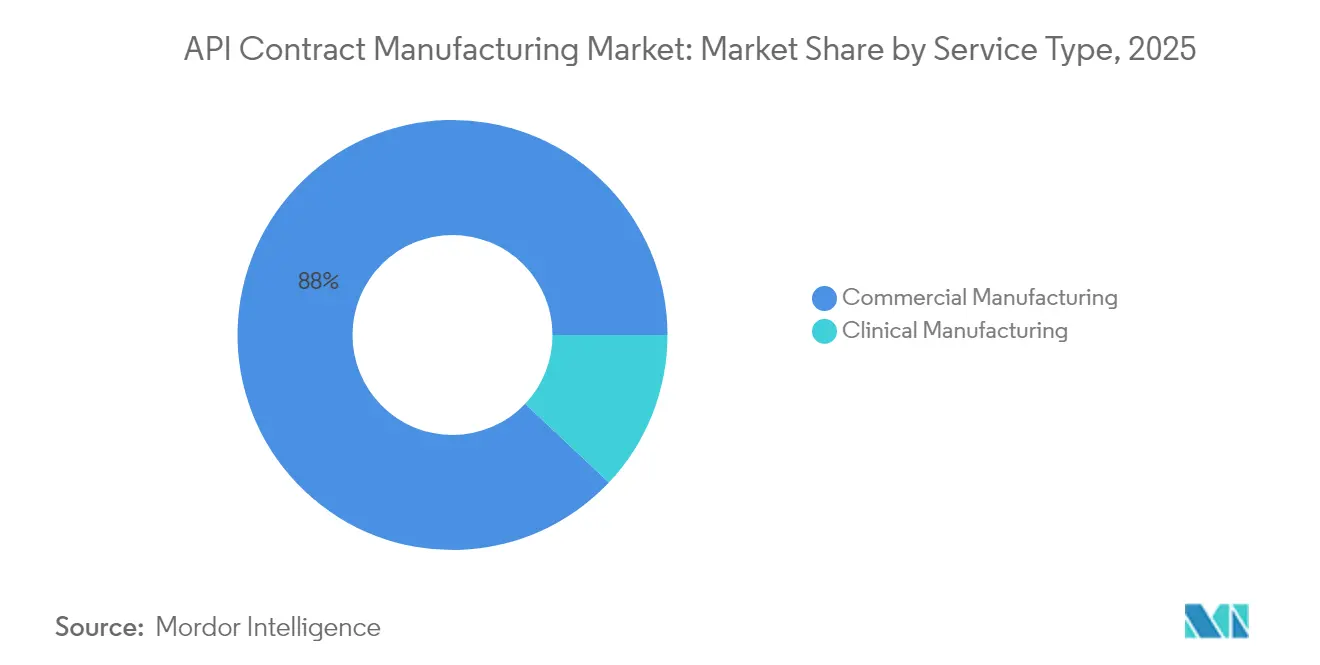

- By service, commercial manufacturing accounted for 87.96% revenue in 2025, whereas clinical manufacturing is set to post a 6.87% CAGR.

- By therapeutic area, oncology led with 42.15% revenue in 2025; endocrine & metabolic disorders are forecast to grow 6.9% annually to 2031.

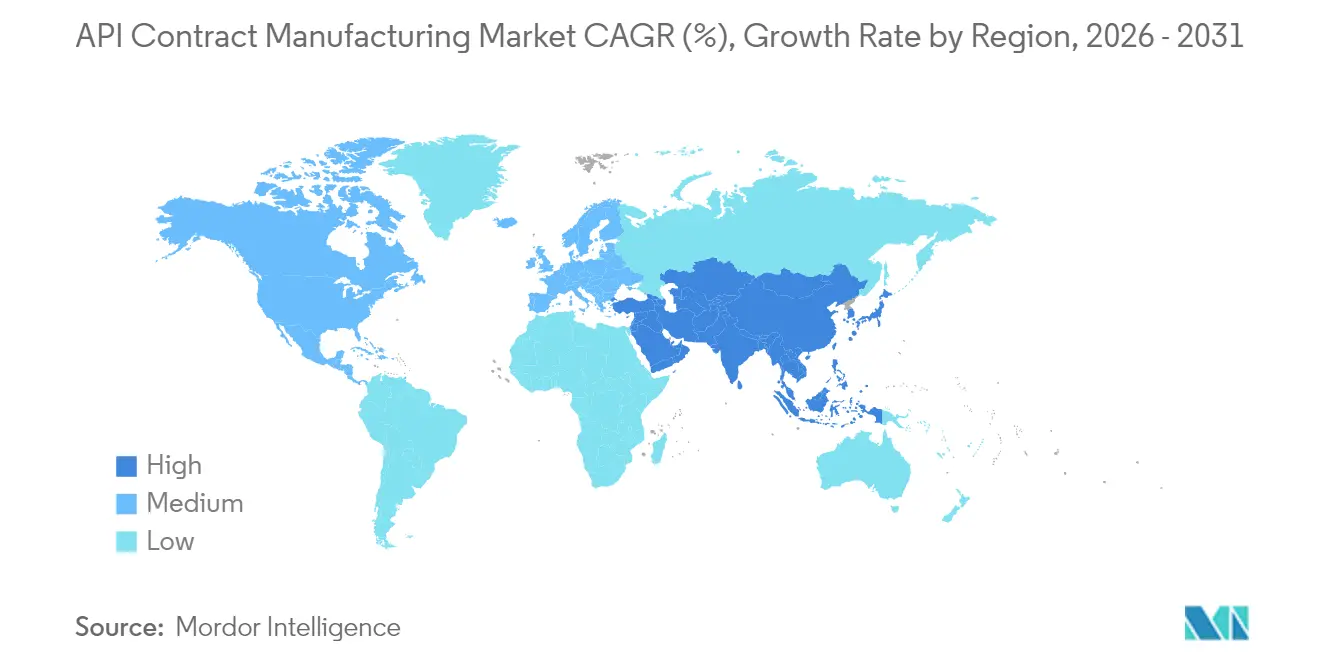

- By region, North America commanded 40.28% share in 2025, while Asia Pacific is the fastest-expanding region at 9.25% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global API Contract Manufacturing Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Complex small-molecule outsourcing | +1.8% | North America & Europe | Medium term (2-4 years) |

| Oncology pipeline fueling HPAPI demand | +1.2% | Global | Long term (≥ 4 years) |

| Biologics expansion | +1.5% | North America, Europe, Asia | Long term (≥ 4 years) |

| Faster FDA/EMA approvals | +1.0% | North America & Europe | Short term (≤ 2 years) |

| Continuous-flow manufacturing adoption | +1.3% | Global | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Rising Outsourcing of Complex Small-Molecule APIs

Outsourcing penetration for APIs rose to 74% in 2024, driven by innovators’ need to access advanced chemistries, reduce fixed costs, and hasten scale-up. Small biopharma firms outsource even more aggressively, relying on CDMOs for 85% of API synthesis as they lack internal plant infrastructure. CDMOs equipped with flow chemistry and high-containment suites report 30-35% lower unit costs than in-house networks, reinforcing the economic rationale for external manufacturing. This migration of volume underpins steady expansion of the API contract manufacturing market.

Surge in Oncology Pipeline Requiring HPAPI Containment Expertise

Oncology accounted for 42.71% revenue in 2024, and the segment’s premium compounds fuel an 8.34% annual rise in HPAPI demand. Strict occupational-exposure limits necessitate purpose-built suites with isolators and single-use technology, raising barriers to entry and cementing long contracts for CDMOs already certified to handle potent cytotoxics.

Biologics Expansion Driving Large-Molecule API Contracts

Large-molecule programs spanning monoclonal antibodies and bioconjugates are advancing at a 7.07% CAGR to 2030, supported by sustained FDA approval momentum for these modalities. CDMOs continue to pour capital into mammalian cell-culture lines and conjugation capacity as demand shifts toward complex biologics.

Accelerated FDA/EMA Approvals Expanding CDMO Throughput

The FDA cleared 59 new molecular entities in 2024, compressing timelines from Phase III to launch and intensifying the hunt for commercial capacity. CDMOs with integrated clinical-to-commercial suites are best placed to absorb this volume, translating regulatory speed into topline growth.

Regulatory Stringency on Cross-Contamination in HPAPI Facilities

The FDA and EMA now require dedicated air-handling, rigorous cleaning validation, and real-time monitoring in potent-compound blocks, inflating capital spend and lengthening qualification cycles. Smaller CDMOs struggle to fund upgrades, potentially slowing the overall API contract manufacturing market growth trajectory.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Regulatory Stringency on Cross-Contamination in HPAPI Facilities | ~-0.9% | Global, with highest impact in North America & Europe | Medium term |

| Generic Buyers' Price Pressure Compressing CDMO Margins | ~-1.2% | Global, most severe in Asia & emerging markets | Short term |

| Source: Mordor Intelligence | |||

Generic Buyers’ Price Pressure Compressing CDMO Margins

Escalating price erosion in generic finished-dose markets cascades upstream to API suppliers. Asian producers with low-cost structures intensify bidding wars, forcing contractors to adopt lean programs and invest in productivity tools just to preserve margins.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Molecule Type: Biologics Reshape Manufacturing Paradigms

Small-molecule pathways retained an 81.92% share of the API contract manufacturing market size in 2025, reflecting entrenched chemistries and high-volume therapies. Biologics, however, are the clear growth engine, expanding 6.82% annually as antibody and conjugate pipelines swell. The swing toward biologics compels CDMOs to couple cell-line development, upstream fermentation, and downstream purification within one campus, a capability only a minority presently command. Lonza’s multi-billion-dollar acquisitions and brownfield builds underscore the capital intensity required to stay ahead.

Biologics’ intricate processes and sterility demands create durable moats for established suppliers, contrasting with more commoditized small-molecule work. As regulatory confidence in biosimilar interchangeability improves, legacy Big Pharma increasingly outsources even late-stage biologic assets, enlarging the total API contract manufacturing market.

By Potency: HPAPIs Drive Specialized Containment Investments

Standard-potency compounds generated 89.18% revenue in 2025 and benefit from capacity abundance. Yet HPAPIs, catalyzed by targeted oncology regimens, are adding 8.02% per year. The API contract manufacturing market size for HPAPIs is forecast to exceed USD 35.66 billion by 2031 as customers seek partners with OEL ≤ 10 ng/m³ cleanrooms. Contractors submitting to repeated regulatory inspections quickly differentiate themselves, winning multi-year supply contracts at premium margins.

The cost of isolated suites, barrier technology, and advanced PPE continues to rise. Still, the higher value of HPAPI campaigns offsets these overheads and tempts mid-tier CDMOs to invest, intensifying competition within this lucrative corridor of the API contract manufacturing market.

By Synthesis Method: Biotech Processes Gain Momentum

Chemical synthesis captured 70.88% revenue in 2025 thanks to its scalability and familiarity. Fermentation and cell-free expression, however, are projected to grow 7.32% annually as precision fermentation enables production of peptides, oligos, and complex enzymes with lower waste. The API contract manufacturing market share of biotech routes will continue to rise, propelled by regulatory willingness to accept novel upstream technologies and the ESG edge of biological processes.

AI-driven strain engineering shortens development cycles, prompting CDMOs to integrate bioinformatics teams alongside classical process engineers. Those able to harmonize chemical and biological toolkits secure stickier relationships with innovator clients seeking dual-path feasibility studies.

By Service Type: Clinical Manufacturing Accelerates Development

Commercial supply still dominates with 87.96% of revenue in 2025. Nonetheless, clinical manufacturing is expanding 6.87% each year as small and mid-cap biotech firms funnel record venture capital into first-in-human programs. Integrating chemical route scouting, scale-up, and GMP supply under one roof allows CDMOs to move candidates from grams to multi-kilogram lots without tech transfer delays.

The early engagement model lowers failure risk and positions the contractor as the logical commercial partner, deepening wallet share and reinforcing API contract manufacturing market expansion.

By Therapeutic Area: Oncology Dominates Specialized Production

Oncology APIs led with 42.15% revenue in 2025 and anchor demand for both HPAPIs and complex bioconjugates. Endocrine and metabolic disorders show the sharpest growth at 6.9% CAGR, helped by surging demand for GLP-1 analogs. Novo Nordisk alone earmarked DKK 80 billion for new API capacity to meet incretin demand.

Cardiovascular, CNS, and infectious-disease categories remain sizable but mature. Venture investment into rare-disease modalities continues to trickle toward CDMOs with niche viral-vector and nucleic-acid capabilities, reinforcing the diversified nature of the API contract manufacturing industry.

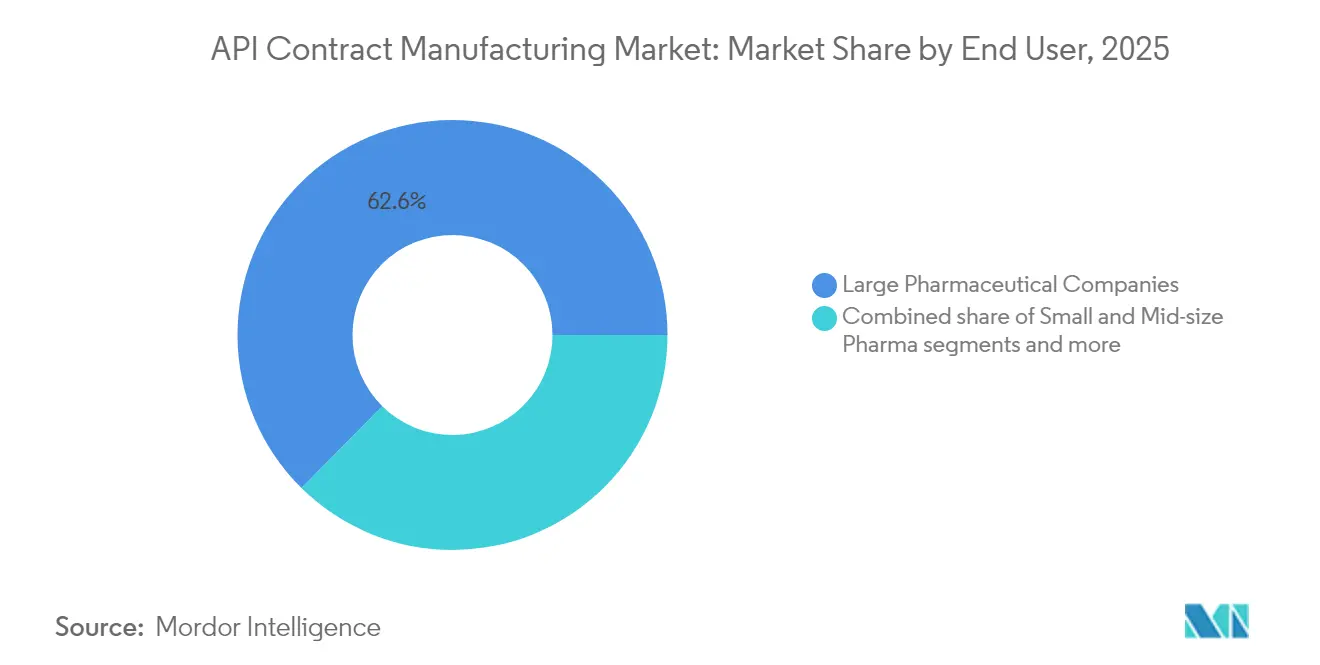

By End User: Biotechnology Companies Drive Innovation

Large pharmaceutical companies constituted 62.61% spend in 2025, yet the biotech community is the fastest mover, increasing outsourcing outlays at an 7.78% CAGR. Early-stage companies outsource 85% of API work because they lack capital-intensive plants and choose to preserve cash for clinical milestones. CDMOs offering flexible, small-volume reactors and integrated analytical support resonate most strongly with this constituency.

Academic centers and public-sector agencies occupy a niche but expanding role, particularly in pandemic preparedness and orphan-disease programs that gain funding through global health initiatives. The breadth of end-user needs underpins sustained growth of the API contract manufacturing market.

Geography Analysis

North America retained 40.28% of the API contract manufacturing market size in 2025, supported by high R&D intensity and FDA’s supportive stance toward advanced manufacturing. Recent mega-projects such as Eli Lilly’s USD 9 billion Indiana build-out add fresh domestic capacity for peptide and small-molecule APIs. A pending U.S. national-security probe into reliance on foreign APIs, however, could trigger import tariffs and reinforce reshoring themes, altering cost curves for buyers.

Asia Pacific remains the high-velocity node, expanding 9.25% annually. India and China are on track to supply more than half of global API output by mid-decade, buoyed by competitive operating costs and production-linked incentive schemes. Taiwan’s biotech revenue grew 8.1% year-on-year in 2023, illustrating regional diversification. Continual upgrades to GMP enforcement and environmental rules aim to boost export credibility but also elevate compliance costs, provoking consolidation among smaller domestic manufacturers.

Europe commands a major share of high-value and potent-compound work because of entrenched quality standards and a large biologics footprint. The European Medicines Agency’s Shortages Monitoring Platform, active from February 2025, pushes manufacturers to disclose API capacity constraints promptly, nudging brand owners to secure dual sourcing. Emerging hubs in the Middle East, Africa, and South America remain nascent but receive policy support aimed at enhancing local resilience and could serve as secondary supply points for multinational sponsors watching geopolitical flashpoints.

Competitive Landscape

The API contract manufacturing market displays moderate fragmentation: the top 10 contractors hold roughly one-third of revenue, with hundreds of niche players filling therapeutic or technological gaps. Strategic M&A persists—Novo Holdings’ acquisition of Catalent reflects the premium placed on GLP-1 capacity as demand far outstrips supply[1]Source: Bourne Partners, “Novo Holdings Acquires Catalent to Expand GLP-1 Manufacturing,” bourne-partners.com. Lonza, Thermo Fisher, and Catalent continue multibillion-dollar capex programs to secure end-to-end platforms that span early-stage development through fill-finish.

Specialization rather than low cost now defines differentiation. High-potency suites, mammalian cell-culture lines, bioconjugation, and continuous-flow reactors command premium pricing and long contracts. Digitalization is the new arms race: Lonza pilots AI route-scouting tools that cut process-development cycles by 30%. At the same time, green chemistry credentials increasingly influence RFP outcomes, evident in Siegfried’s pledge to shift to 100% renewable electricity within three years[2] Source: Siegfried Holding AG, “Sustainability Report 2024,” siegfried.ch .

White space still exists in advanced therapy medicinal products, integrated drug-substance/drug-product offerings, and low-carbon manufacturing. Start-ups born with continuous-flow DNA or specialized viral-vector platforms are courting venture funding, and larger CDMOs continue to evaluate bolt-on acquisitions to close capability gaps and reinforce their stance within the API contract manufacturing market.

API Contract Manufacturing Industry Leaders

Teva Pharmaceuticals Industries Ltd

Sun Pharmaceutical Industries

Boehringer Ingelheim GmbH

Piramal Pharma Solutions

AbbVie

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Teva Pharmaceutical Industries revealed plans to divest its API unit to focus on branded and biosimilar medicines.

- March 2025: Almac Pharma Services inaugurated a USD 84.2 million commercial solid-dose facility in Craigavon, UK, adding 35 million tablet capacity

Global API Contract Manufacturing Market Report Scope

API contract manufacturing market is segmented by type, form, molecules, manufacturing, end users, and geography. By type, the market is segmented as organic and inorganic. The market is segmented by form as solid, liquid, and semi-solids. The market is segmented by molecules as small molecules API and large molecules API. By manufacturing, the market is segmented into clinical and commercial manufacturing. The market is segmented by end users, such as pharmaceutical industries, research organizations, and other end users. By geography, the market is segmented as North America, Europe, Asia-Pacific, Middle East and Africa, and South America. The report also covers the estimated market sizes and trends for 17 countries across major regions globally. The report offers the value (in USD) for the above segments.

| Small Molecule APIs |

| Large Molecule / Biologic APIs |

| Standard Potency APIs |

| High-Potency APIs (HPAPIs) |

| Synthetic / Chemical |

| Biotech / Fermentation |

| Pre-clinical |

| Clinical Phase I |

| Clinical Phase II |

| Clinical Phase III |

| Commercial |

| Drug-Substance Development |

| Drug-Substance Manufacturing |

| Drug-Product Manufacturing |

| Analytical & Packaging |

| Oncology |

| Cardiovascular Diseases |

| Central Nervous System Disorders |

| Endocrine & Metabolic Disorders |

| Infectious Diseases |

| Others |

| Large Pharmaceutical Companies |

| Small & Mid-size Pharma |

| Biotechnology Firms |

| Generics Manufacturers |

| Academic & Research Institutes |

| North America | United States |

| Canada | |

| Mexico | |

| Rest of Asia-Pacific | China |

| Japan | |

| India | |

| South Korea | |

| Australia | |

| Rest of Asia-Pacific | |

| Europe | Germany |

| France | |

| United Kingdom | |

| Italy | |

| Spain | |

| Rest of Europe | |

| South America | Brazil |

| Argentina | |

| Rest of South America | |

| Middle East and Africa | GCC |

| South Africa | |

| Rest of Middle East | |

| Brazil | |

| Argentina | |

| Rest of South America |

| By Molecule Type | Small Molecule APIs | |

| Large Molecule / Biologic APIs | ||

| By Potency | Standard Potency APIs | |

| High-Potency APIs (HPAPIs) | ||

| By Synthesis Method | Synthetic / Chemical | |

| Biotech / Fermentation | ||

| By Manufacturing Stage | Pre-clinical | |

| Clinical Phase I | ||

| Clinical Phase II | ||

| Clinical Phase III | ||

| Commercial | ||

| By Service Type | Drug-Substance Development | |

| Drug-Substance Manufacturing | ||

| Drug-Product Manufacturing | ||

| Analytical & Packaging | ||

| By Therapeutic Area | Oncology | |

| Cardiovascular Diseases | ||

| Central Nervous System Disorders | ||

| Endocrine & Metabolic Disorders | ||

| Infectious Diseases | ||

| Others | ||

| By End User | Large Pharmaceutical Companies | |

| Small & Mid-size Pharma | ||

| Biotechnology Firms | ||

| Generics Manufacturers | ||

| Academic & Research Institutes | ||

| By Geography | North America | United States |

| Canada | ||

| Mexico | ||

| Rest of Asia-Pacific | China | |

| Japan | ||

| India | ||

| South Korea | ||

| Australia | ||

| Rest of Asia-Pacific | ||

| Europe | Germany | |

| France | ||

| United Kingdom | ||

| Italy | ||

| Spain | ||

| Rest of Europe | ||

| South America | Brazil | |

| Argentina | ||

| Rest of South America | ||

| Middle East and Africa | GCC | |

| South Africa | ||

| Rest of Middle East | ||

| Brazil | ||

| Argentina | ||

| Rest of South America | ||

Key Questions Answered in the Report

What is the current size of the API contract manufacturing market?

The API contract manufacturing market size is USD 221.82 billion in 2026 and is on track to reach USD 305.35 billion by 2031.

Which region is growing fastest in API contract manufacturing?

Asia Pacific posts the highest growth, clocking a projected 9.25% CAGR from 2026 to 2031 due to aggressive capacity expansions and supportive government policies.

Why are HPAPIs attracting investment?

High-potency APIs serve targeted oncology therapies, command premium pricing, and require dedicated containment, prompting CDMOs to build specialized suites and capture higher-margin contracts.

How does continuous-flow manufacturing benefit CDMOs?

Flow reactors lower production costs by up to 50%, cut waste, and enhance safety, allowing CDMOs to meet ESG targets while winning cost-sensitive bids.

Page last updated on: