Sports Composites Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

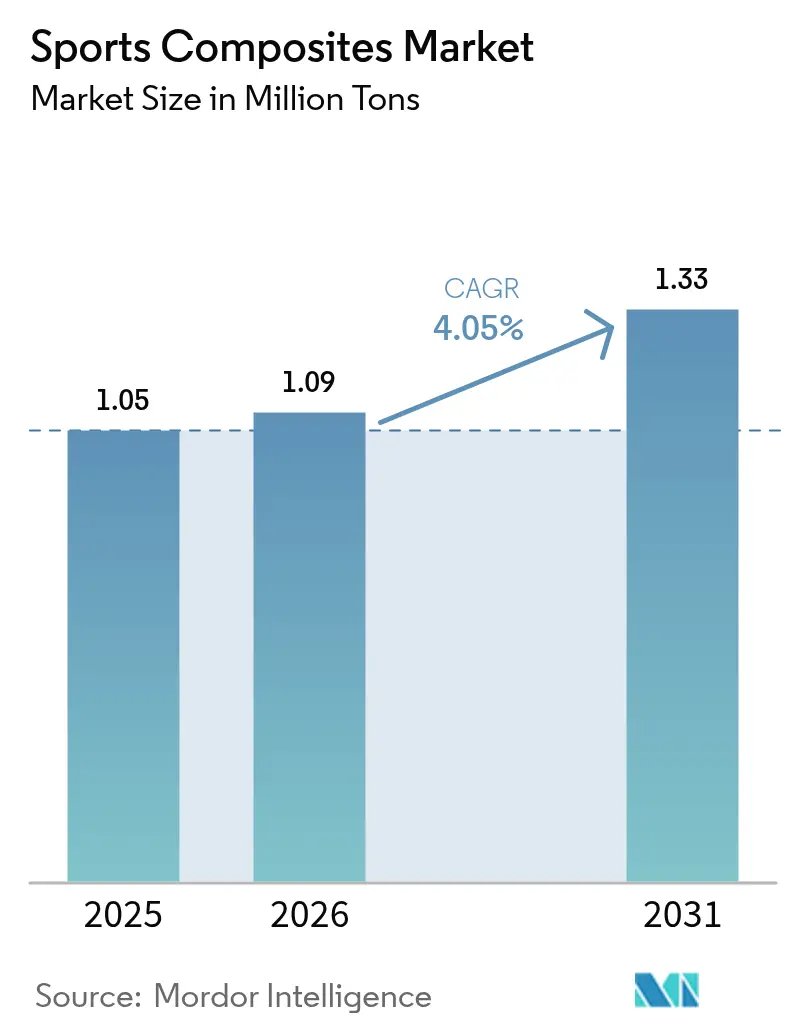

| Market Volume (2026) | 1.09 Million tons |

| Market Volume (2031) | 1.33 Million tons |

| Growth Rate (2026 - 2031) | 4.05% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | Asia-Pacific |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Sports Composites Market Analysis by Mordor Intelligence

The Sports Composites Market size is expected to grow from 1.05 Million tons in 2025 to 1.09 Million tons in 2026 and is forecast to reach 1.33 Million tons by 2031 at 4.05% CAGR over 2026-2031. Growth rests on the widening preference for lightweight, high-performance equipment that measurably enhances athletic output, a trend showcased by the broad carbon-fiber use at the 2024 Paris Olympics[1]NitPro Composites, “Carbon Fiber Sports Equipment in the 2024 Paris Olympics,” nitprocomposites.com. Rising manufacturing automation, sustained product innovation and a sharpening focus on sustainable materials are further solidifying demand. The Asia-Pacific region anchors volume growth through large-scale production capacity, government-backed cycling initiatives and steadily climbing domestic consumption. Carbon-fiber adoption is accelerating as microwave-assisted processing, automated fiber placement and thermoplastic routes narrow historical cost gaps. Ongoing supply turbulence in PAN feedstock and uneven recycling infrastructure pose near-term hurdles but are unlikely to derail the medium-term expansion pathway.

Key Report Takeaways

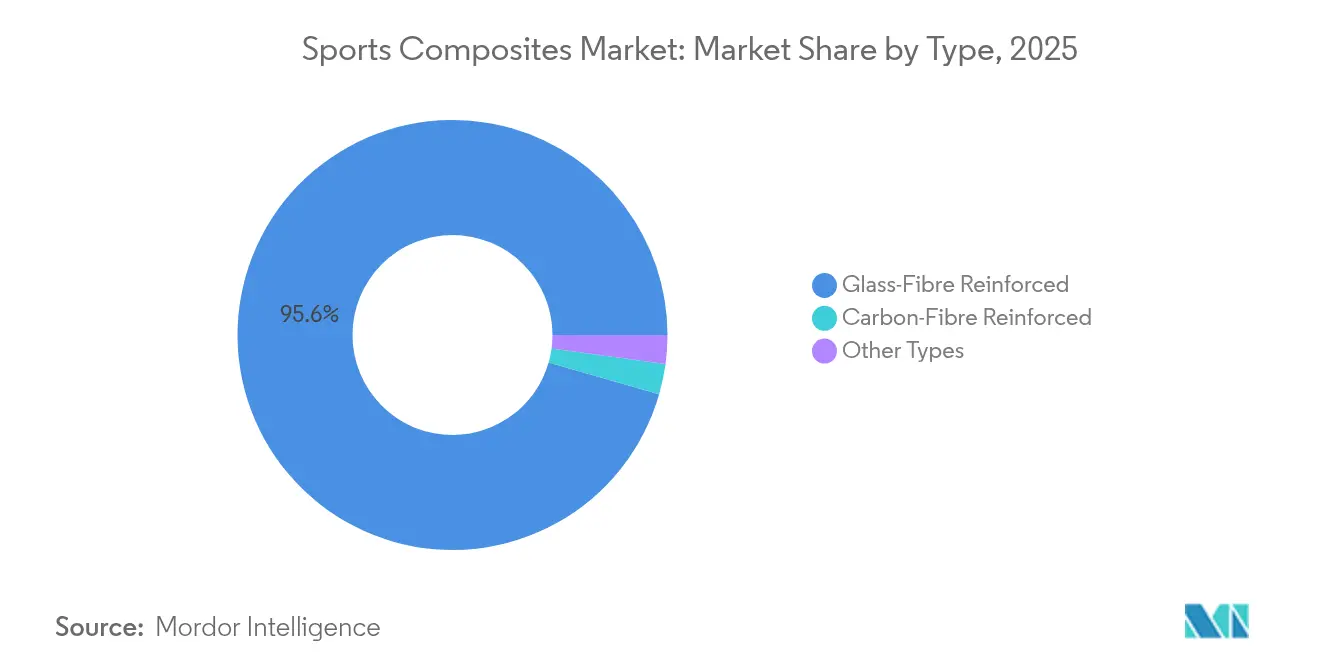

- By type, glass-fibre reinforced composites led with 95.55% of sports composites market share in 2025, while carbon-fibre reinforced products are projected to register the fastest 9.38% CAGR through 2031.

- By resin, epoxy accounted for 39.55% of the sports composites market size in 2025 and is set to advance at a 5.12% CAGR during 2026-2031.

- By manufacturing process, prepreg lay-up held 44.55% share in 2025; resin transfer molding is forecast to expand at a 7.72% CAGR to 2031.

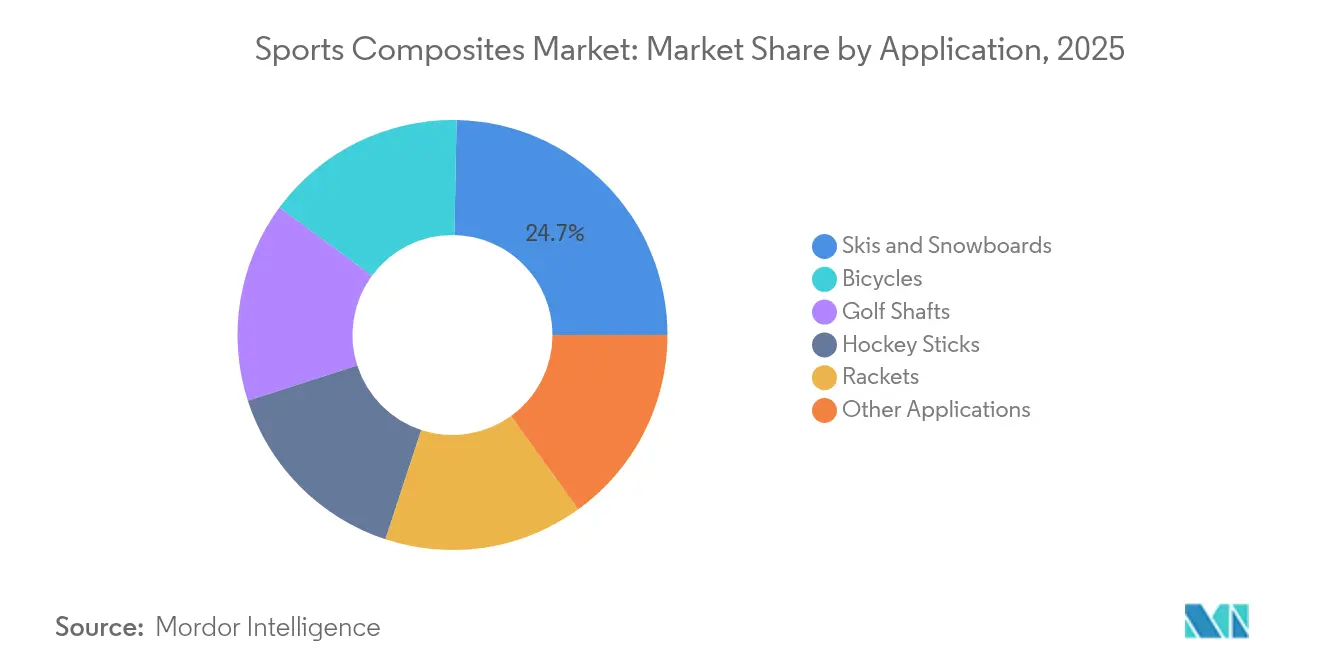

- By application, skis and snowboards commanded 24.70% of the sports composites market size in 2025, whereas bicycles are growing fastest at a 5.68% CAGR.

- By geography, Asia-Pacific captured 55.40% sports composites market share in 2025 and is slated to maintain the highest 4.64% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Sports Composites Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Market | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising Adoption of Automated Fiber-Placement for High-End Bicycles in Europe | +1.5% | Europe, with spillover to North America | Medium term (2-4 years) |

| Increasing Demand for Lightweight and High-Performance Sports Equipment | +0.9% | Global | Long term (≥ 4 years) |

| Government-Backed Cycling Infrastructure Boom in Asia Catalyzing Demand for Lightweight Frames | +0.7% | Asia-Pacific, primarily China, Japan, and South Korea | Medium term (2-4 years) |

| Growing Golf Industry | +0.5% | North America, Europe, Asia-Pacific | Medium term (2-4 years) |

| Growing Popularity of Recreational and Professional Sports | +0.3% | Global | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising adoption of automated fiber placement for high-end bicycles

Automated fiber placement systems are gaining traction among European frame builders as equipment prices fall and programming tools mature. The technology delivers precise tow placement, cuts scrap rates by 30% and trims lay-up time by roughly 40% compared with hand lay-up. Resulting frames weigh 15-20% less yet meet stringent stiffness benchmarks, allowing brands to tailor ride characteristics for professional racers and demanding enthusiasts. Production repeatability also opens the door to larger batch runs without compromising custom geometries, thereby supporting profitable mid-volume supply contracts across Europe and North America. Wider AFP integration is expected to ripple into other tubular products, including hockey sticks and golf shafts, as machine utilization rates rise and unit costs continue to decline.

Increasing demand for lightweight and high-performance equipment

Across disciplines, athletes now rely on composite gear to secure marginal gains that translate into podium finishes. Carbon-fiber tennis rackets generate up to 30% higher rebound power while dampening frame vibration by 10%, helping players maintain control during extended rallies. In cycling, carbon frames shave up to 40% weight relative to aluminum while preserving torsional rigidity—a combination that improves acceleration on climbs and sprints. Mainstream consumers are adopting these technologies as retail prices drop, widening the customer base for composite goods. Manufacturers are therefore scaling thermoplastic molding and integrating graphene or nanofillers to deliver lighter, tougher and more sustainable product lines without sacrificing profit margins.

Government-backed cycling infrastructure boom in Asia

National and municipal authorities in China, Japan and South Korea are allocating multi-billion-dollar budgets to bicycle lanes, rental schemes and velodromes. Improved infrastructure raises commuting and recreational cycling participation, stimulating demand for both entry-level and premium composite frames. Producers in Fujian and Guangdong have announced double-digit capacity expansions to meet fresh orders, while Japanese material suppliers are promoting locally designed carbon prepregs to capture value within the region. Suppliers anticipate spillover advantages in protective gear and components—such as helmets, handlebar stems and wheelsets—as consumers gravitate toward full composite systems to maximize ride performance.

Expanding golf participation

The global golf landscape is diversifying as younger players, women and emerging-market consumers take up the sport. These demographics demand lighter shafts with precise flex profiles that complement varied swing speeds. Carbon-fiber technology enables extreme wall-thickness control and micro-taper adjustments, supporting mass customization programs run by leading club makers. Producers also highlight vibration dampening and torque stability as key selling points, allowing amateurs to replicate professional shot consistency. As participation grows, shaft volumes rise, reinforcing economies of scale for prepreg production lines dedicated to sporting goods.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High Volatility in PAN-Based Carbon-Fiber Feedstock Prices | -1.2% | Global, with higher impact in regions with limited local production | Short term (≤ 2 years) |

| Limited End-of-Life Recycling Ecosystem for Multi-Material Sports Gear | -0.3% | Europe, North America | Medium term (2-4 years) |

| Tariff Barriers on Composite Bicycle Imports in the U.S. | -0.2% | North America, with impact on Asian exporters | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

High volatility in PAN-based carbon-fiber feedstock prices

PAN precursor accounts for roughly half of finished carbon-fiber cost, leaving processors exposed to price swings linked to acrylonitrile and energy inputs. Spot quotations surged during 2024 and early 2025, compressing margins for mid-range sporting goods and deterring some bicycle OEMs from all-carbon frame catalogs. Research at the University of Limerick indicates microwave-assisted stabilization and carbonization could cut energy use by 70%, laying groundwork for cost relief, yet commercial roll-out remains two to three years away. In the interim, producers explore lignin-based precursors and scale recycled fiber blends to hedge price risk, but qualification cycles slow uptake in performance-critical gear.

Limited end-of-life recycling ecosystem for multi-material sports gear

Nearly 90% of composite sporting goods disposed in the United Kingdom still reach landfill. Complex lay-ups that combine fiber, resin and metallic inserts hinder straightforward material separation, while geographically dispersed user bases inflate reverse-logistics costs. Recent initiatives like the Carbon Fibre Circular Alliance (CFCA) are beginning to address this gap by developing circularity solutions specifically for carbon fiber sports equipment, with participation from major manufacturers including Scott Sports and Wilson Sporting Goods. Ski recycling trials in Denmark likewise leverage wind-turbine blade shredding expertise to process winter-sport laminates. Until such schemes scale, major brands face mounting sustainability scrutiny and must foot higher eco-design and take-back program expenses.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Carbon-Fibre Gaining Despite Glass Dominance

Glass-fibre composites retained a dominant position, equal to 95.55% of the sports composites market in 2025. The material’s low cost and adequate mechanical profile suit entry-level skis, hockey sticks and protective shells, which depend on volume throughput and price competitiveness. Nevertheless, carbon-fibre output is projected to climb at a 9.38% CAGR, more than twice the overall sports composites market pace, as manufacturers exploit microwave stabilization, tow spreading and recycled fiber feeds to rein in cost. The sports composites market size tied to carbon-fibre goods is therefore set to rise sharply, propelled by bicycles, golf shafts and professional racket frames where weight savings justify premium pricing.

At application level, the sports composites market shows expanding dual-material architectures that blend carbon skins with glass core plies to balance cost and performance. Broader familiarity with carbon filament winding and automated tape placement shortens development cycles for new tubular products, enabling brands to unveil differentiated road and gravel bike line-ups each season. Niche fibers—aramid for impact resistance and bio-derived reinforcements such as algae-based carbon—remain experimental but attract research grants targeting reduced embodied carbon.

By Resin Type: Epoxy Leads Through Performance Advantages

Epoxy platforms comprised 39.55% of 2025 volume, reflecting their leading stiffness retention, low shrinkage and strong fiber bonding. The segment’s 5.12% projected CAGR keeps it ahead of polyurethane and polyester formulations due to growing demand for high-temperature-capable resins in thermoplastic fusion bonding. Developers are rolling out self-healing epoxy matrices and antibacterial additives for racket handles and helmet liners, broadening the property palette without major retooling. Polyurethane remains prominent in vibration-critical boards and pads, while vinyl ester holds share in marine-exposed surf and paddle gear where hydrolysis resistance is prized.

Future growth stems from fast-curing hot-melt epoxies compatible with high-speed compression presses. These chemistries slash cycle times, making automated short-run production financially viable for mid-market brands. Consequently, epoxy’s slice of the sports composites market size is expected to widen as processing productivity climbs and circularity initiatives repurpose manufacturing scrap into pre-preg stock.

By Manufacturing Process: Advanced Techniques Reshape Production

Prepreg lay-up delivered 44.55% of 2025 tonnage thanks to tight resin control and high fiber-volume fractions that underpin top-tier skis, frames and shafts. Autoclave cure, once the cost bottleneck, is being progressively replaced by out-of-autoclave ovens and rapid-pressure presses, shaving unit energy demand. Meanwhile, resin transfer molding is slated for a 7.72% CAGR because closed-mold tooling produces Class A finishes on both sides and entraps fewer volatiles, aligning with tightening plant emission norms. The sports composites market is also seeing filament winding expand into e-bike frames and trekking poles as multi-axis heads place varying moduli fibers along load paths.

Automated fiber placement is the showpiece innovation: multi-robot cells programmatically lay narrow tows to create variable-thickness laminates that cut inert mass from non-critical zones. Early adopters report 20% laminate weight reduction and rapid amortization of equipment on high-margin race products. As deposition speeds rise, AFP is expected to handle selected mid-volume items, reinforcing its role in future sports composites market growth.

By Application: Performance Demands Drive Diverse Adoption

Skis and snowboards accounted for 24.70% of the sports composites market size. Composite cores balance torsional stiffness with flex for edge grip, while strategic carbon and basalt stringers tune damping. Suppliers now experiment with recycled carbon and flax hybrids to meet resort sustainability targets. Bicycles, expanding at a 5.68% CAGR, rely on high-modulus carbon tubes, monocoque frames and structural rims to transfer rider wattage efficiently. Advanced thermoplastic over-molding merges dropouts and cable guides during cure, trimming secondary assembly labour.

Golf shafts, hockey sticks, and racket frames round out high-volume applications, each pushing lay-up science to fine-tune balance, vibration, and rebound. The sports composites market continues to diversify, with fishing rods, crash helmets and protective padding collectively absorbing meaningful tonnage. Emerging nanofiller-enhanced laminates for park-golf club faces, which demonstrated over 1,000% vibration-damping gains, illustrate the constant expansion of performance envelopes that composites unlock.

Geography Analysis

Asia-Pacific dominated 2025 with 55.40% of global volume. Producer scale, integrated fiber supply, and escalating domestic demand position the region as the key manufacturing and consumption hub. Chinese export data shows sporting goods shipments of CNY 7 billion (USD 992 million) in the first seven months of 2024, up 15.41% year-on-year. Regional policies that encourage urban cycling, winter-sport participation, and green material adoption underpin a forecast 4.64% CAGR to 2031. The sports composites market benefits from favorable trade terms under RCEP, helping Chinese, Japanese, and South Korean brands penetrate ASEAN and Oceania retail channels.

North America follows, supported by high discretionary spending on premium bicycles, golf sets, and winter gear. Domestic sustainability programs accelerate circular-economy pilots that recover carbon fiber from broken rackets and skis, positioning the region as a blueprint for end-of-life solutions. Yet tariff hikes on imported composite bicycles add cost pressures, encouraging some brands to onshore frame production or source from tariff-exempt partners to protect pricing.

Europe maintains a robust base of high-end ski, yacht, and cycling manufacturers who leverage precision AFP and RTM processes. Regional research clusters refine bio-based epoxy and recyclable thermoplastic composites, helping brands cut cradle-to-grave emissions. Development funding and stringent eco-design rules push firms to adopt closed-loop systems, giving European producers an early-mover advantage in circular product portfolios. South America, the Middle East, and Africa remain emerging but promising, with sports participation and infrastructure builds spawning new demand nodes for composite products.

Value Chain Analysis

The sports composites value chain starts with petrochemical and bio-based feedstocks that move into PAN precursor and glass fiber production. Carbonization for carbon fiber and resin synthesis for epoxy, polyurethane, polyester, vinyl ester, and emerging recyclable thermoplastics follow, before material suppliers such as Toray Industries, Mitsubishi Chemical, Hexcel, SGL Carbon, and Solvay convert inputs into prepregs, fabrics, tapes, and other semi-finished composite forms. Sporting-goods OEMs and tier suppliers then cut, lay up, and mold these materials into frames, shafts, sticks, rackets, boards, and protective gear using prepreg lay-up, RTM, filament winding, and compression molding. Finished goods reach brand-owned channels and specialized distributors, feeding both retail and aftermarket replacement demand, with warranty returns and breakage creating a secondary flow of scrap.

Bottlenecks cluster around high-modulus carbon fiber availability and conversion capacity, and the premium golf shaft ecosystem highlights single-source exposure where critical material supply is heavily concentrated among Japan-based producers. Cost and continuity risks also rise with PAN feedstock volatility and with the limited, geographically dispersed end-of-life collection network for multi-material sporting goods. In response, the chain is building circular pilots that connect resin innovators and recyclers with niche board and winter-sport brands, including Arkema’s eco-designed speed board prototype at JEC World 2026, which used Elium recyclable thermoplastic resin and recycled carbon fibers, and the Zephir Project consortium validating a circular windsurf board prototype through on-water testing in April 2026.

Competitive Landscape

The global playing field combines large resin and fiber conglomerates with specialized sporting goods manufacturers, resulting in a moderately fragmented environment. Hexcel, Toray, and SGL Carbon leverage material-science depth and scale to supply consistent prepregs and tow, while niche firms differentiate through tailored golf shafts and flexible structural textiles. Equipment brands ranging from HEAD to Wilson embed material breakthroughs into popular gear lines, creating vertical integration that secures supply and embeds proprietary know-how into end products.

Innovation remains the decisive competitive lever. Microwave-assisted carbonization, lignin-derived precursors, and graphene-seeded laminates are nearing pilot scale, promising lower cost and enhanced performance. Firms commercializing closed-loop recycling or high-throughput AFP will likely capture a premium share as regulators and consumers demand greener, lighter, and longer-lasting gear. Consequently, the sports composites market is expected to favor agile producers that couple formulation expertise with adaptable manufacturing footprints.

Sports Composites Industry Leaders

TORAY INDUSTRIES, INC

Mitsubishi Chemical Carbon Fiber and Composites, Inc.

Hexcel Corporation

SGL Carbon

Solvay

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated where performance requirements meet circularity, and brands are moving from sustainability messaging into structural validation of recyclable and bio-derived composite systems. Arkema’s March 2026 demonstration of a recyclable speed board prototype at JEC World 2026, using Elium liquid thermoplastic resin and recycled carbon fibers, points to a pathway for boards and similar high-surface-area products that can support depolymerization-enabled resin platforms, assuming collection and processing partners scale. Separately, recycling programs that target harder composite streams are expanding the materials loop for sports components, including surfboard fins produced from recycled wind-turbine blade fiberglass that gained competition visibility in 2026, supporting uptake of reclaimed reinforcement in non-safety-critical parts where consistent aesthetics and mechanical minimums can be maintained.

A second opportunity area is technology transfer from aerospace into sport-oriented prepregs, fiber architectures, and engineered subcomponents that reduce weight while keeping stiffness and durability in bicycles, golf shafts, and rackets. Teijin Carbon’s March 2026 expansion of Tenax NEXT prepreg systems for high-end bike frames reinforces ongoing productization of advanced resin and fiber solutions for sporting goods. Component-level innovation also supports differentiation for premium builds, with Sapim debuting the RC-1 composite spoke at the 2026 Sea Otter Classic and signaling continued substitution of metal with composites in rotating and fatigue-sensitive parts. In adjacent soft-goods inputs, bio-based polymer platforms are entering performance sportswear supply chains, including Avantium’s July 2026 collaboration on PEF-based textile prototypes and CovationBio’s July 2026 commercial launch of Sorona elasterell-p stretch fiber, which can feed into helmet-liner and padding ecosystems that pair textiles with composite shells.

Recent Industry Developments

- June 2026: Hexcel and Deutsche Aircraft announced a long-term composite partnership and supply agreement for the D328eco regional aircraft programme. While aerospace-led, it tightens downstream demand for advanced composite solutions and reinforces investment in composite materials, processing know-how, and qualified supply chains that also serve high-performance sporting goods.

- April 2025: HEAD commercialized the limited-edition BOOM RAW tennis racquet using 100% bio-circular carbon fibers supplied by Toray Carbon Fibers Europe under ISCC PLUS mass-balance certification. The launch moved a prototype sustainability concept into a retail product, encouraging broader OEM qualification of lower-footprint reinforcements in performance rackets and paddles.

- November 2024: Toray Advanced Composites completed the acquisition of Gordon Plastics assets in Englewood, Colorado, expanding capacity and capabilities for continuous fiber reinforced thermoplastic composite tapes. This supports faster-cycle manufacturing routes and helps broaden thermoplastic composite availability for sporting-goods components that prioritize repeatability, impact tolerance, and end-of-life recyclability.

Research Methodology Framework and Report Scope

Market Definition and Coverage

For this study, the sports composites market is defined as composite laminates, prepregs, and molded composite parts used to make sporting equipment, where the composite content is a functional material and not a small trim.

Scope exclusions: Excluded items include raw fibers, thermoplastic films, and prepregs that are primarily destined for aerospace, automotive, or marine uses instead of sports equipment.

Segmentation Overview

- By Type

- Carbon-Fibre Reinforced

- Glass-Fibre Reinforced

- Other Types

- By Resin Type

- Epoxy

- Polyurethane

- Other Resin types

- By Manufacturing Process

- Prepreg Lay-up

- Resin Transfer Molding

- Filament Winding

- Pultrusion

- Compression Molding

- Other Processes

- By Application

- Golf Shafts

- Hockey Sticks

- Rackets

- Bicycles

- Skis and Snowboards

- Other Applications

- By Geography

- Asia-Pacific

- China

- Japan

- India

- South Korea

- Rest of Asia-Pacific

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Rest of Europe

- South America

- Brazil

- Argentina

- Rest of South America

- Middle East and Africa

- Saudi Arabia

- South Africa

- Rest of Middle East and Africa

- Asia-Pacific

Data Sources, Market Sizing, and Validation

Desk Research

Desk research helped us set the outer limits of the market and keep volume assumptions realistic. We referenced public sources such as national customs statistics for import and export flows, USITC-style trade tables, and government industrial production releases where composite manufacturing is tracked.

To avoid relying on one signal, we also reviewed trade association pages and technical bodies related to reinforced plastics, along with peer-reviewed materials journals that discuss sports equipment composite use and processing trends. Company annual reports, investor presentations, and product brochures were used to understand where composite grades are positioned in sports categories. Paid subscriptions were used selectively for company financials and intelligence, patent databases, and shipment-level import and export records. These sources are illustrative only, and many other public references were also used to collect, validate, and clarify data points.

Primary Interviews and Surveys

Primary work focused on filling gaps that public sources do not explain well, such as the typical composite content per unit, scrap rates in fabrication, and how quickly a sport category shifts between carbon and glass reinforcements. We spoke with a mix of composite material suppliers, sporting goods manufacturers, converters, and distributors, and the discussions covered APAC, EMEA, and the Americas so regional mix and pricing could be checked in a consistent way.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 13% | APAC: 51% |

| Mid tier: 58% | Functional/Unit leaders: 39% | EMEA: 30% |

| Smaller Players: 14% | Managers: 48% | Americas: 19% |

Market-Sizing & Forecasting

The core sizing model uses a top-down build that reconstructs sports composite demand from sports equipment production and trade signals, and then converts that demand pool into composite volume using typical material intensity factors. Only after category totals were formed, selective bottom-up checks were applied, such as sample supplier roll ups, channel checks on large equipment categories, and sampled volume times average selling price cross-checks, which helped adjust outliers.

Key inputs used in the model include composite content per equipment unit (for example bicycle frames versus rackets), the mix shift between carbon and glass reinforcements, regional manufacturing concentration, import and export movement for sports goods, and processing yield and scrap assumptions. Where data was thin for niche sports, gaps were handled by using proxy categories with similar construction methods and then rechecked with interview feedback.

For forecasting, scenario analysis was used because adoption is sensitive to participation trends, pricing of reinforcement fibers, and substitution between material systems. The forward view was tied back to what interviewees expect on production planning, lead times, and price progression, so the forecast does not move only on a single growth rate assumption.

Data Validation & Update Cycle

Validation was done through multiple checks that compare the model output against independent signals, such as trade flows for sports goods, regional production shifts, and reported capacity additions for composite processing. When a country or sport category showed a sharp jump that did not match these signals, the assumptions were revisited and respondents were re-contacted to confirm what changed.

Before sign-off, the numbers go through step-by-step analyst review so unit conversions, pricing logic, and regional splits are consistent. Reports are refreshed annually, and interim updates are made when major events materially shift demand or supply. Right before delivery, a final pass is completed so clients receive the most current view available at that time.

Mordor Intelligence's Sports Composites Market Estimate Compared With Other Published Estimates

Published market sizes for sports composites can look far apart because each publisher measures a different thing, and the unit of measure is not always the same. Differences usually come from how far up the value chain the counting goes, whether adjacent sports goods are included, and how frequently assumptions are refreshed.

Protective gear foams and other non-structural padding often get bundled into some revenue totals, but those items sit outside Mordor Intelligence's scope because the model tracks composite laminates, prepregs, and molded parts used in sporting equipment shipments. The spread also reflects price build methods, where some estimates apply a broad CAGR to revenue and others rebuild demand using production and trade indicators, followed by currency timing and inflation handling that can change the stated USD value.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 4.22 B (2025) | |

| Industry Research House A | USD 4.00 B (2024) | Uses a revenue lens with broad segmentation and does not clearly separate composite structural parts from adjacent sports materials, which can compress or expand totals depending on the included bill of materials. |

| Market Analytics Group B | USD 3.78 B (2024) | Reports value-based totals over a different base year and forecast window, and it does not specify exclusions for non-sports composite end uses, which can shift the counted demand pool and the price progression applied. |

Reading the table together, most of the difference comes from scope and unit conversion, and not just from growth expectations. By keeping the counted universe tied to clearly defined sports equipment composite forms and then cross-checking volume and pricing with independent signals, the final figure stays traceable and easier to replicate.

Key Questions Answered in the Report

What is the current size of the sports composites market?

The sports composites market stands at 1.09 million tons in 2026 and is projected to reach 1.33 million tons by 2031.

Which material type is growing fastest within sports composites?

Carbon-fibre reinforced composites are expanding at a 9.38% CAGR, outpacing all other reinforcement types.

Why does Asia-Pacific dominate sports composites production?

The region benefits from integrated supply chains, government support for cycling and winter sports, and robust export demand that collectively deliver 55.40% of global volume.

How are manufacturers tackling carbon-fiber cost volatility?

Firms are piloting microwave-assisted carbonization, exploring lignin-based precursors and increasing recycled fiber content to reduce dependence on conventional PAN feedstock.

What role does automated fiber placement play in sports equipment manufacturing?

AFP enables precise tow deposition, cuts scrap, and produces lighter frames and shafts, driving wider adoption in high-end bicycles, hockey sticks and next-generation golf clubs.

Is recycling of composite sports gear commercially viable?

Pilot projects in Europe and North America show recycled fibers retain 60-70% of original strength, yet broader rollout awaits cost-effective collection networks and standardized processing lines.

Page last updated on: