Market Overview

| Study Period | 2020 - 2031 |

|---|---|

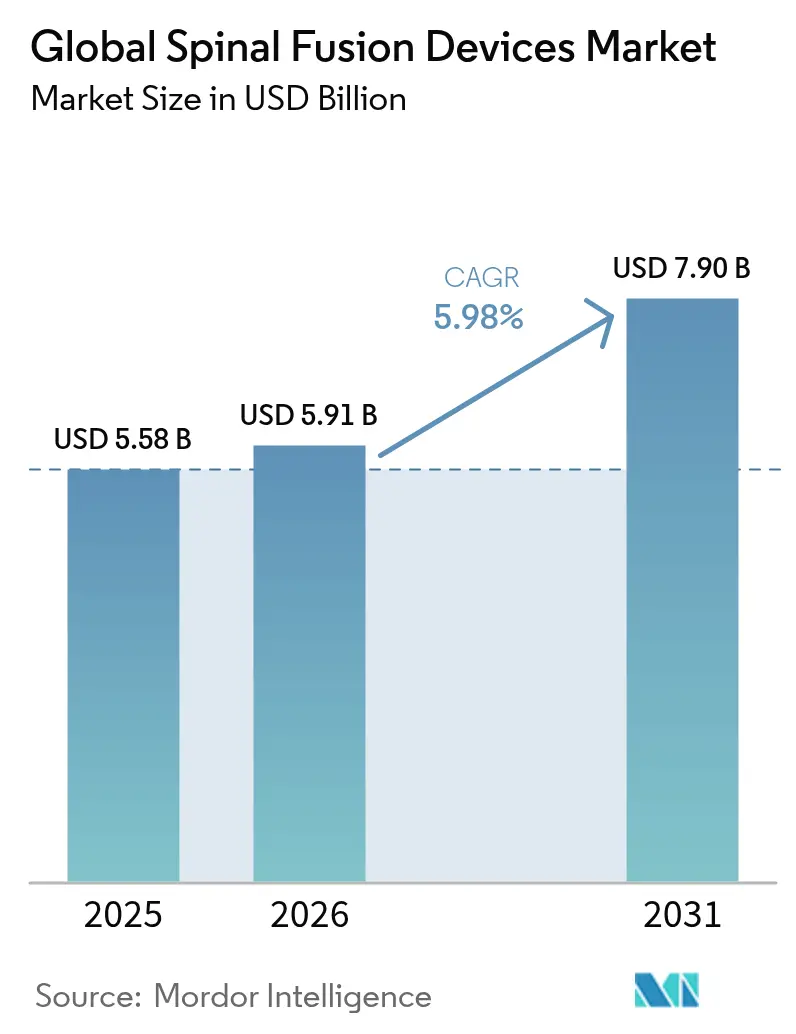

| Market Size (2026) | USD 5.91 Billion |

| Market Size (2031) | USD 7.9 Billion |

| Growth Rate (2026 - 2031) | 5.98% CAGR |

| Fastest Growing Market | Asia Pacific |

| Largest Market | North America |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Global Spinal Fusion Devices Market Analysis by Mordor Intelligence

The spinal fusion devices market size in 2026 is estimated at USD 5.91 billion, growing from 2025 value of USD 5.58 billion with 2031 projections showing USD 7.9 billion, growing at 5.98% CAGR over 2026-2031. Robust demand stems from demographic aging, rising degenerative spine disorders, and accelerating adoption of minimally invasive and AI-enabled surgical platforms. Hospitals and ambulatory surgery centers (ASCs) are scaling procedure volumes as Medicare has more than quadrupled the number of fusion procedures reimbursed in outpatient settings, reinforcing steady case-mix migration. Rapid FDA clearances for 3-D-printed patient-specific cages and the 96.99% screw-placement accuracy achieved by contemporary robotic systems are intensifying competitive differentiation. In parallel, payers’ shift toward bundled payments is pressuring pricing but is also catalyzing the development of value-driven implants, stimulating technological innovation across every product class.

Key Report Takeaways

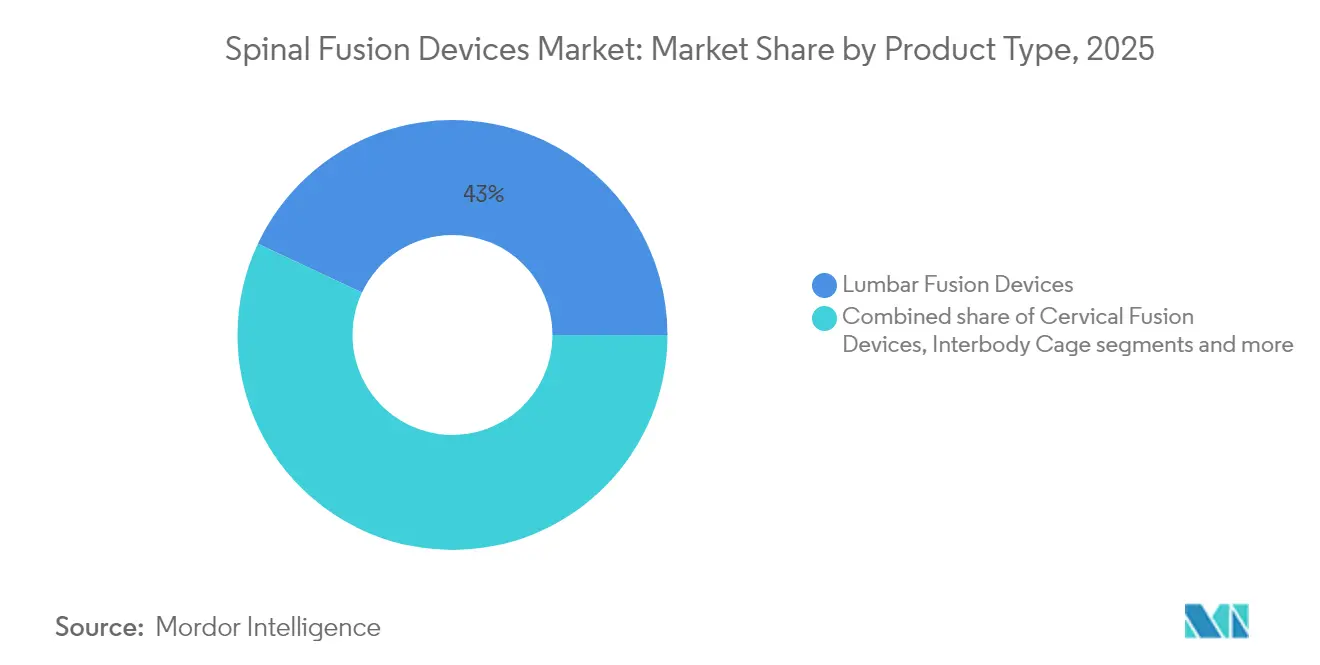

- By product type, lumbar fusion devices led with 43.02% of spinal fusion devices market share in 2025, while interbody cages are on track for a 6.79% CAGR through 2031.

- By surgery type, minimally invasive procedures captured 62.05% revenue in 2025; open surgery is trailing but remains essential for complex deformities. The minimally invasive segment is expanding at 6.12% CAGR to 2031.

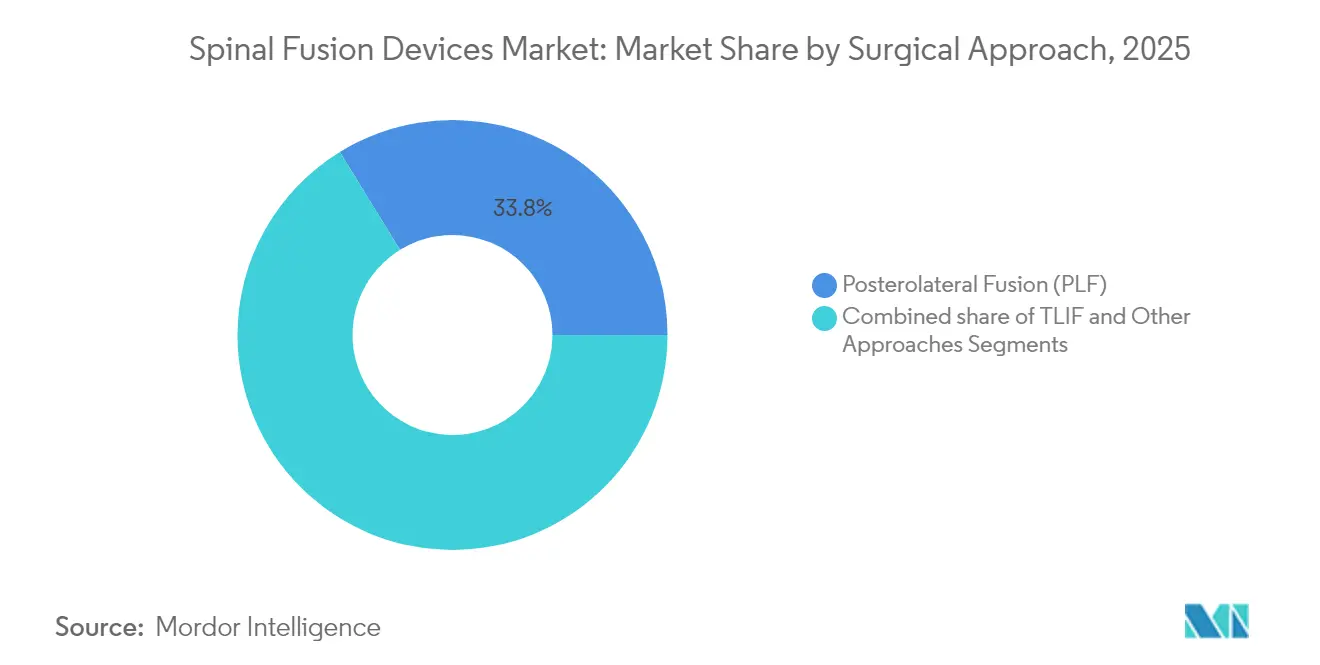

- By surgical approach, transforaminal lumbar interbody fusion (TLIF) recorded the fastest growth at 6.42% CAGR, whereas posterolateral fusion still held 33.78% revenue in 2025.

- By end-user, hospitals accounted for a 62.10% share of the spinal fusion devices market size in 2025, yet ASCs are set to accelerate at 6.57% CAGR to 2031.

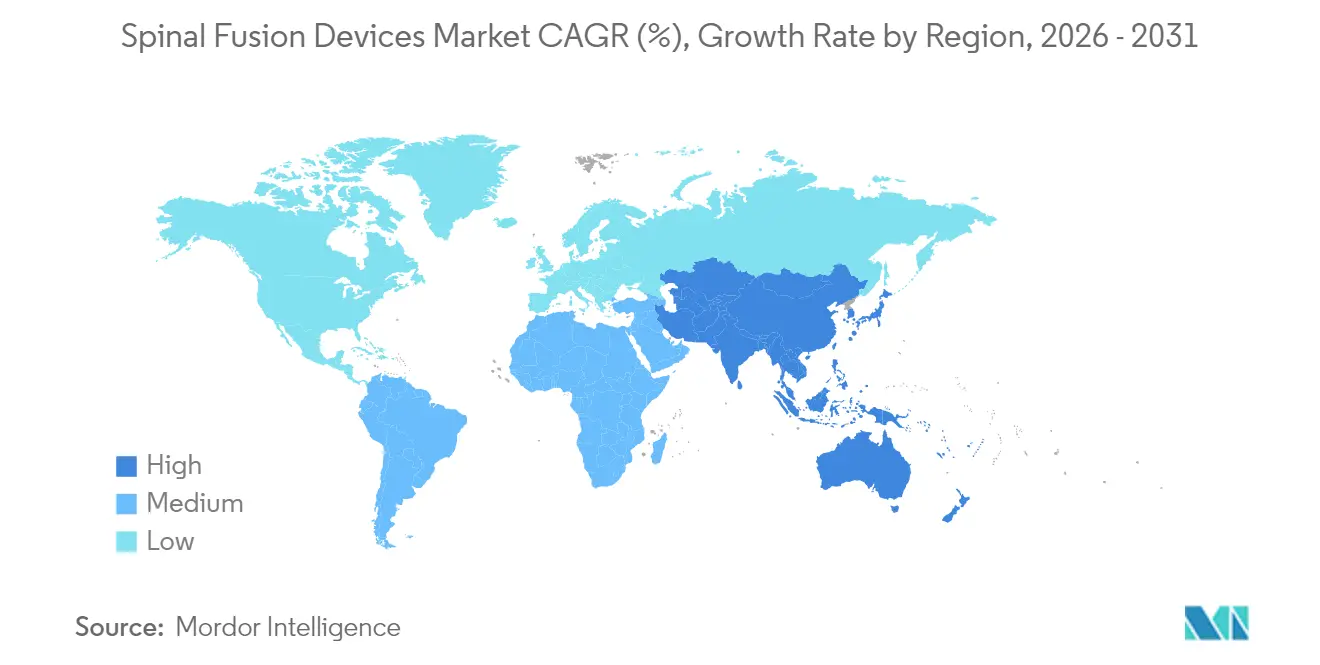

- By region, North America retained 45.88% of the global total in 2025; Asia–Pacific is the fastest-growing geography at a 6.72% CAGR.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global Spinal Fusion Devices Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Minimally invasive fusion techniques | +1.8% | North America & Europe leading, Asia-Pacific following | Medium term (2–4 years) |

| Prevalence of degenerative spine disorders | +1.5% | Global, concentrated in developed markets | Medium term (2–4 years) |

| Expanding geriatric population | +1.2% | Global, highest in North America & Europe | Long term (≥ 4 years) |

| Wider outpatient reimbursement | +0.9% | North America primary, expanding to Europe | Short term (≤ 2 years) |

| AI-guided robotic navigation | +0.7% | North America & Europe early, Asia-Pacific emerging | Medium term (2–4 years) |

| 3-D-printed patient-specific cages | +0.5% | Global, innovation led by North America & Europe | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Shift toward minimally invasive fusion techniques

Minimally invasive spine surgery is overturning long-standing open procedures by delivering shorter hospital stays[1]Zhaojun Song, “Short-term and mid-term evaluation of three types of minimally invasive lumbar fusion surgery for treatment of L4/L5 degenerative spondylolisthesis,” Scientific Reports, nature.com , smaller incisions, and lower complication rates while maintaining equal fusion success. Meta-analyses of transforaminal lumbar interbody fusion confirm fewer transfusions and a 4.83% complication rate versus 14.97% for open surgery. Robotic navigation drives screw accuracy beyond 96%, prompting device manufacturers to bundle implants, navigation, and intra-operative imaging. Fellowship programs now prioritize these techniques, ensuring a pipeline of surgeons fluent in robot-assisted workflows. Hospitals also leverage the faster patient recovery to improve bed turnover, directly aligning clinical performance with value-based purchasing.

Escalating prevalence of degenerative spine disorders

Sedentary lifestyles, obesity, and greater diagnostic scrutiny have raised lumbar disc degeneration incidence to more than 90% in individuals past 60 years. Earlier imaging enables timely surgical referral, averting progression to multilevel disease. Health-economic analyses prove that early fusion lowers chronic pain expenditure, and payers are expanding coverage accordingly. Clinical registries confirm that early single-level lumbar fusion reduces re-operation frequency and boosts quality-adjusted life years. Device makers respond by broadening portfolios of expandable cages and biologics optimized for single-level pathology.

Growing geriatric population & life-expectancy gains

By 2050, the global 65+ cohort will double, fostering steady fusion demand. Medicare reports a 193% growth in spine procedures from 2010–2021, including a 15.7% annual jump at ASCs. Older recipients experience similar fusion rates when minimally invasive techniques limit blood loss. Implant suppliers increasingly tailor instrumentation to osteoporotic bone, while biologic developers explore osteo-enhancing grafts. The demographic tide guarantees a durable patient base even if reimbursement pressure tightens.

Increasing reimbursement coverage for outpatient spine procedures

Medicare’s outpatient list now covers 58 fusion-related codes versus 12 in 2010, saving USD 140 million annually on anterior cervical fusions. Complication rates average below 2% in ASC settings, convincing private payers to roll out bundled payments that reward efficient care. Device vendors specifically design single-use, sterile-packed kits to fit ASC economics. Ambulatory centers reciprocate by installing compact CT scanners and image-guided towers, further propelling the spinal fusion devices market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High implant costs vs. value-based care | –1.1% | North America & Europe primary, emerging in Asia-Pac | Short term (≤ 2 years) |

| Adjacent-segment disease scrutiny | –0.9% | Global, highest in developed markets | Medium term (2–4 years) |

| Stringent FDA & MDR approval timelines | –0.8% | North America & Europe | Medium term (2–4 years) |

| Surgeon shortage in emerging economies | –0.6% | Asia-Pacific, Latin America, MEA | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High implant costs vs. value-based-care payment models

Bundled-payment pilots cap total episode cost, forcing providers to weigh implant performance against price. Cervical fusion intra-operative expenses reach USD 7,574, with 69% tied to hardware. Hospitals renegotiate volume contracts, favoring platforms that minimize re-operation liability. Manufacturers now issue evidence dossiers[2]Timothy J. Yee, “Cost-Effectiveness of Posterior or Transforaminal Lumbar Interbody Fusion for Grade 1 Lumbar Spondylolisthesis: A 5-Year Quality Outcomes Database Study,” Journal of Neurosurgery: Spine, thejns.org showing cost per quality-adjusted life year below USD 100,000 to defend premium tags. Firms unable to articulate value risk share erosion in the spinal fusion devices market.

Rising scrutiny on adjacent-segment disease outcomes

Long-term follow-ups reveal 23.6% revision rates at 10 years, spurring interest in motion-preserving alternatives. Surgeons incorporate prophylactic alignment strategies and hybrid constructs to blunt adjacent-segment loading. Device makers invest in dynamic stabilization and nucleus augmentation technologies. Persistent payer inquiries into lifetime effectiveness could temper uptake of certain rigid constructs.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Lumbar Devices Drive Volume Growth

Lumbar fusion devices generated 43.02% of the 2025 spinal fusion devices market share, cementing their role as workhorse solutions for spondylolisthesis and disc degeneration. The spinal fusion devices market size for lumbar instrumentation is projected to expand at a 5.6% CAGR as demand persists across both inpatient and outpatient channels. Interbody cages stand out with a 6.79% growth rate thanks to 3-D-printed titanium lattices that secure 97% fusion success. Surgeons favor expandable cages that restore disc height and sagittal balance without excessive nerve retraction. Cervical plates and screws maintain consistent uptake for anterior cervical discectomy and fusion, underscored by their long safety record. Thoracic systems meet niche trauma and deformity needs but are turning to modular constructs for inventory efficiency. Pedicle screw innovation now focuses on navigated insertion and torque-limiting drivers, reducing mal-position. Biologic graft substitutes, including cellular bone allografts, realize 98.5% fusion, narrowing reliance on iliac crest autografts.

Continued material science advances exploit porous PEEK and magnesium alloys that encourage osteointegration while dampening stress shielding. Patient-specific implants, produced in days, personalize endplate coverage and load-sharing characteristics. Vendors increasingly package cage-graft bundles, simplifying logistics for ASCs. Still, value-analysis committees scrutinize unit price, steering hospitals toward platforms demonstrating both clinical superiority and cost-effectiveness, a balance that will define winners across the spinal fusion devices market.

By Type of Surgery: Minimally Invasive Techniques Reshape Practice

Minimally invasive procedures held 62.05% spinal fusion devices market size in 2025, posting a 6.12% CAGR through 2031 as imaging, navigation, and tubular retractors converge to curtail tissue disruption. Open surgery retains a role in severe deformity corrections yet faces shrinking share as robotic guidance abbreviates learning curves. Real-time 3-D imaging permits percutaneous pedicle screw trajectories with sub-2 mm deviation, lessening neurologic risk. Meanwhile, single-position spine techniques limit patient flips, shaving anesthesia time. Hospitals harness these efficiencies to qualify more cases for outpatient discharge, buoying ASC adoption and reshaping reimbursement dynamics.

The spinal fusion devices market responds with compact instrument suites, sterile-packed implants, and disposable navigation arrays tailored to ASC throughput. Training centers augment cadaveric labs with mixed-reality simulators, accelerating surgeon competency. Payers reward minimally invasive pathways via bundled reimbursement uplift for low complication incidence. As evidence matures, regulators may green-light shorter clearance paths for kits demonstrably improving safety, further embedding minimally invasive approaches into mainstream spine care.

By Surgical Approach: TLIF Emerges as Preferred Technique

Posterolateral fusion accounted for 33.78% of spinal fusion devices market share in 2025 but cedes momentum to TLIF, which is rising at a 6.42% CAGR as biomechanical advantages gain clinical validation. TLIF enables circumferential fusion from a unilateral corridor, preserving contralateral musculature and cutting intra-operative blood loss by up to 50% versus traditional bilateral facetectomy. Robot-assisted, minimally invasive TLIF enhances cage placement accuracy, promoting superior lordosis restoration and disc height maintenance. The spinal fusion devices market size for TLIF-compatible cages and screws is forecast to outpace legacy posterior systems through 2031.

Alternative routes such as anterior lumbar interbody fusion (ALIF) thrive in cases demanding maximal sagittal correction, while lateral approaches minimize dorsal muscle trauma. Surgeons increasingly rely on patient-specific planning to decide between TLIF, ALIF, or lateral strategies. Finite-element models published in 2024 detail stress profiles for each approach, informing implant geometry that mitigates adjacent-segment overload. Ongoing refinement will likely harmonize approach selection with personalized risk assessment.

By End-User: ASCs Capture Growing Market Share

Hospitals preserved 62.10% of the spinal fusion devices market size in 2025 as they manage polytrauma and complex revisions, yet the ASC channel is expanding at 6.57% CAGR, fueled by Medicare’s outpatient coverage expansion. ASCs operate lean staffing ratios and rely on fast-turnover implants, compelling suppliers to streamline tray counts and offer consignment options. Clinical series report sub-2% complication rates for one- to two-level lumbar fusions in ASC environments. Payers leverage that safety record to contract bundled payments featuring gain-sharing clauses.

Hospitals respond with hospital-outpatient departments that mimic ASC efficiency while retaining access to critical care back-up. Specialty orthopedic clinics, though not primary surgical sites, influence implant selection through pre-operative planning and long-term follow-up data. The spinal fusion devices market will see sustained channel diversification as technology further reduces length of stay and enables same-day discharge for multi-level constructs.

Geography Analysis

North America contributed 45.88% to global revenue in 2025 and should grow at 5.21% CAGR through 2031 as premium robotics and 3-D-printed implants penetrate both inpatient and outpatient settings. Medicare’s 58 ASC-eligible spine codes have catalyzed a 15.7% annual procedure rise in ambulatory centers, underpinning the spinal fusion devices market trend toward lower-cost sites of care. FDA breakthrough designations expedite commercialization, reinforcing the region’s innovation leadership.

Asia–Pacific is the swiftest climber with a 6.72% CAGR to 2031, leveraging hospital infrastructure upgrades, rising disposable incomes, and an expanding base of fellowship-trained spine surgeons. China’s Class III registration requirements are lengthy, yet local partnerships ease market access, and provincial tenders often favor cost-effective, yet technologically advanced, domestically produced implants. Japan and South Korea add volume through aging demographics, while India’s private hospital chains import navigated systems to capture medical tourism.

Europe’s 5.64% CAGR reflects balanced growth moderated by MDR compliance costs that slightly slow new-product launches. National health services encourage outpatient migration, particularly in the Nordics and Germany, but pricing controls challenge premium device margins. South America advances at 5.97% CAGR as Brazil and Argentina upgrade tertiary centers and adopt minimally invasive techniques. Middle East and Africa post 6.29% CAGR on the back of Gulf States’ specialist hospital investments, although surgeon shortages restrain broader regional uptake. Overall, the spinal fusion devices market is expanding worldwide, yet growth vectors differ markedly by reimbursement climate, surgeon density, and regulatory velocity.

Regulatory Landscape

Spinal fusion implants are regulated as medical devices in the United States and as implantables under the EU MDR. In the United States, market access typically follows FDA 510(k) clearance for intervertebral fusion devices under Class II special controls, with the FDA IDE framework used to generate clinical evidence for new indications or higher-risk adjuncts. In Europe, compliance is driven by EU MDR 2017/745, which tightens clinical evaluation and post-market surveillance; in March 2026 the European Commission adopted delegated regulations expanding the MDR Well-Established Technologies list to include certain spinal fixation systems, enabling sampling-based conformity assessment where criteria are met and documentation is robust. Biocompatibility expectations tighten as ISO 10993-1:2025 updates flow into device biological safety programs, influencing materials validation for cages, coatings, and instrumentation that contact tissue and bone.

Value Chain Analysis

The spinal fusion devices value chain spans upstream materials and components, in-house or contract manufacturing, sterilization and packaging, and downstream distribution aligned to hospital and ASC case logistics. Key inputs include titanium (including plasma-atomized powder for additive manufacturing), cobalt-chrome alloys, and PEEK, with supply concentration in established industrial bases such as the United States and Germany. Midstream operations increasingly combine conventional machining with additive manufacturing for porous or patient-matched interbodies, followed by validated cleaning, packaging, and sterilization steps that are tightly coupled to regulatory technical documentation demands across FDA and EU MDR. Downstream, commercial execution relies on direct sales forces and procedure support, with instrument-tray management, consignment models, and sterile, single-use kits becoming more important as outpatient sites of care expand. Trade and tariff-related cost pressure in 2025 pushed manufacturers to reassess sourcing and consider near-shoring, and companies highlighted differing exposure profiles (for example, vertically integrated models with predominantly US-based manufacturing versus firms relocating supply away from China). Structural shifts in the channel are also evident as OEMs rebalance portfolios and routes to market, including Stryker's transfer of its spinal implants business into VB Spine, while enabling-technology ecosystems (navigation, imaging, robotics) raise the service intensity of distribution beyond logistics alone.

Competitive Landscape

The spinal fusion devices market is moderately consolidated: the top five suppliers control an estimated 62% of global sales, while a vibrant cadre of start-ups targets performance niches. Globus Medical’s USD 250 million purchase of Nevro augments motion-preservation and pain-management synergies, signaling convergence between hardware and neuromodulation. Stryker’s divestiture of legacy spinal implants, while retaining its Mako Spine robot, highlights a pivot toward software-driven ecosystems. Medtronic’s AiBLE platform integrates navigation, imaging, and analytics, contributing high single-digit segment growth and locking surgeons into proprietary workflows.

Emerging players exploit additive manufacturing to deliver patient-specific cages; Curiteva logged 2,000 implants without revision in its first post-approval year. Premia Spine’s TOPS motion-preservation implant demonstrated superior functional outcomes versus fusion in a 24-month randomized study, pressuring traditional rigid construct. Imaging vendors such as Siemens Healthineers partner with implant companies to co-develop AI-enabled planning suites, further blurring hardware-software borders. Supply-chain resilience also shapes competition, with firms localizing manufacture to avoid tariff exposure and MDR bottlenecks.

Price pressure intensifies as hospitals deploy gain-sharing contracts that reward lower implant costs and high patient-reported outcome scores. Vendors respond by unbundling navigation from implant purchase or offering subscription models that spread capital expense. Simultaneously, surgeons’ rising data literacy encourages evidence-based procurement, favoring firms that furnish real-world performance dashboards. Competitive differentiation is thus transitioning from raw implant design to holistic workflow optimization, clinical proof, and economic transparency across the spinal fusion devices market.

Global Spinal Fusion Devices Industry Leaders

Globus Medical

Johnson & Johnson Services, Inc.

Medtronic plc

Stryker Corporation

Zimmer Biomet Holdings

- *Disclaimer: Major Players sorted in no particular order

Market Opportunities and Future Outlook

Near-term whitespace is concentrated in solutions that make fusion workflows more predictable in outpatient settings while fitting bundled-payment economics: simplified instrument sets, sterile-packed kits, and implants that reduce reoperation risk. The reimbursement tailwind for outpatient spine is tangible, with Medicare's outpatient list covering 58 fusion-related codes versus 12 in 2010, and this care-site migration pulls demand toward minimally invasive-compatible interbodies, percutaneous fixation, and compact enabling technologies that suit ASC footprints. A second opportunity area is fusion biology and combination products that broaden surgeon choice across approaches, supported by recent regulatory actions rather than generic technology claims. In January 2026, Cerapedics received FDA approval for an expanded indication for PearlMatrix P-15 Peptide Enhanced Bone Graft across multiple lumbar interbody approaches (ALIF, PLIF, OLIF, LLIF) in addition to TLIF, reinforcing investment in biologic adjuncts that accelerate fusion. In parallel, the cadence of FDA clearances in 2026 for enabling platforms and new implant systems (for example, Medtronic's Stealth AXiS clearance and multiple 510(k) clearances tied to Globus Medical systems) underscores an active product refresh cycle where integration of planning, navigation, and robotics is increasingly packaged alongside implant portfolios to support surgeon standardization and procurement value.

Recent Industry Developments

- April 2026: Theradaptive received FDA approval to advance its OASIS trial for OsteoAdapt SP in spinal fusion into a pivotal study. The move expands the pipeline of biologic adjuncts targeting fusion outcomes and raises competitive pressure on graft and biologics positioning alongside implant systems.

- April 2025: Viscogliosi Brothers completed the acquisition of Stryker's US spine business, creating VB Spine. The transaction reshaped competitive dynamics in spinal implants by moving an established portfolio into a dedicated spine-focused entity while Stryker retained its Mako Spine robotics focus.

- August 2024: DePuy Synthes launched the VELYS Active Robotic-Assisted System (VELYS SPINE) following FDA 510(k) clearance. The launch strengthened competition around integrated robotics and navigation, encouraging bundled offerings that pair procedural enabling technology with spinal fusion implant pull-through.

Research Methodology Framework and Report Scope

Market Definition and Coverage

This market covers the revenues generated from spinal fusion devices used to permanently join two or more vertebrae in the cervical, thoracic, or lumbar spine, including key implant systems and related fusion hardware used in clinical care settings.

Scope exclusions: Devices used only for vertebral compression augmentation, electrical stimulation, or motion preservation are not counted in this market.

Segmentation Overview

- By Product Type

- Cervical Fusion Devices

- Thoracic Fusion Devices

- Lumbar Fusion Devices

- Interbody Cages

- Pedicle Screw Systems

- Bone Graft Substitutes and Others

- By Type of Surgery

- Open Spine Surgery

- Minimally Invasive Spine Surgery

- By Surgical Approach

- Transforaminal Lumbar Interbody Fusion (TLIF)

- Posterolateral Fusion (PLF)

- Other Approaches

- By End-User

- Hospitals

- Ambulatory Surgery Centers (ASCs)

- Specialty & Orthopedic Clinics

- By Geography

- North America

- United States

- Canada

- Mexico

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- GCC

- South Africa

- Rest of Middle East and Africa

- South America

- Brazil

- Argentina

- Rest of South America

- North America

Data Sources, Market Sizing, and Validation

Desk Research

Desk research was used to set the market boundaries, understand procedure and patient demand signals, and establish starting assumptions before interviews. We referred to public sources such as the US FDA device databases, US CDC and National Center for Health Statistics tables, CMS utilization and payment files, and OECD health statistics for surgery and population indicators.

To add context on clinical practice and device use, we also reviewed sources such as peer reviewed spine journals, conference proceedings, and guidelines published by spine and orthopedic associations. Company annual reports, investor presentations, and credible press were used to cross check product mix changes and geographic exposure. In a few places, paid subscriptions were used for company financials and patent databases to confirm innovation focus and approximate segment weightings. The sources listed here are illustrative, and many other public and paid references were used for data collection, cross checks, and clarification.

Primary Interviews and Surveys

Primary work focused on validating the link between fusion procedure demand and device revenue, and then stress testing the assumptions used in the model. We spoke with a mix of manufacturers, distributors, and care delivery stakeholders such as surgeons and procurement teams, covering major demand pools across APAC, EMEA, and the Americas to avoid overgeneralizing regional practice patterns.

Distribution of primary research fieldwork respondents

| Company type | Respondent position | Region |

|---|---|---|

| Top tier: 28% | CXOs: 12% | APAC: 44% |

| Mid tier: 58% | Functional/Unit leaders: 41% | EMEA: 29% |

| Smaller Players: 14% | Managers: 47% | Americas: 27% |

Market-Sizing & Forecasting

Sizing starts from a top-down build where procedure volumes and treated patient pools are reconstructed using hospital activity signals, aging demographics, and spine disorder prevalence, and then converted into device demand using fusion adoption by indication and average implants used per case. To keep the estimate grounded, the model also tracks variables such as minimally invasive penetration, cervical versus lumbar case mix, reimbursement stability, and average selling price movement by implant category.

Results are then corroborated using selective bottom-up approximations, such as sample supplier revenue splits, distributor channel checks, and ASP times volume sanity tests for key countries where data is clearer. When public visibility is limited, we fill gaps using proxy indicators like comparable procedure rates, healthcare spending intensity, and import patterns, followed by expert review before the value is rolled into the total.

For forecasting, scenario analysis is used to reflect different paths for procedure recovery, pricing pressure, and adoption of newer implant designs. The scenario weights are adjusted using what respondents expect for their order books and tender activity, so the forward view stays practical and does not rely on overly detailed inputs that are not consistently observable year to year.

Data Validation & Update Cycle

Validation is done through several passes so the final numbers are not driven by one data stream. We compare model outputs against independent signals such as procedure trends, healthcare spending direction, and reported revenue exposures, and then investigate any large variances at the country and region level.

Before sign off, the model is reviewed by another analyst to recheck units, currency conversions, and the treatment of one time anomalies like supply disruptions or policy changes. If a key assumption shifts, respondents are recontacted and the affected parts of the model are rebuilt, followed by a final consistency check. The report is refreshed annually, and interim updates are made when material events meaningfully change demand, pricing, or the product mix.

Mordor Intelligence's Spinal Fusion Devices Market Size Compared With Other Published Estimates

Published market sizes for spinal fusion devices do not always match because each publisher draws the market boundary in its own way, chooses different base years, and applies different pricing and volume assumptions. Differences also show up when some models rely more heavily on company mix disclosures, while others lean on procedure counts without fully converting them into device revenues.

Procedure volume signals, implant usage patterns per case, and revenue exposure checks by region are the evidence points that tie Mordor Intelligence to USD 5.91 B (2026) for this market. Key gap drivers still remain, since some estimates fold adjacent spine categories into the total, extend the scope of biologics differently, or push faster ASP growth without consistent checks against reimbursement and tender pricing. Currency timing choices can also shift the reported USD figure.

Benchmark comparison

| Source | Market Size | Gaps in Research Methodology |

|---|---|---|

| Mordor Intelligence | USD 5.91 B (2026) | |

| Global Consultancy A | USD 5.98 B (2025) | Uses a different base year and a longer forecast window, and the disclosed scope does not clearly separate fusion-only revenues from nearby spine implant categories, which can lift the starting value. |

| Industry Research Group B | USD 8.90 B (2024) | Appears to apply broader device coverage and a higher implied ASP level for the base year, and the country aggregation approach is not fully explained, which can widen the total when summed globally. |

Looking across the figures, most of the spread is explained by scope boundaries, base year choices, and how procedure demand gets translated into priced device volumes. Our approach stays repeatable because each step is linked to observable signals and then pressure tested through interviews, which helps keep the market size balanced rather than pushed by optimistic pricing or expanded product definitions.

Key Questions Answered in the Report

Which surgical technique is gaining the quickest traction among spine surgeons?

Transforaminal lumbar interbody fusion (TLIF) is being adopted rapidly because it restores disc height through a single posterior corridor while preserving muscle integrity and lowering complication risk.

How are 3-D-printed cages changing spinal fusion practice?

Patient-specific, additively manufactured cages improve endplate contact and promote faster osseointegration, translating to higher fusion reliability and fewer revision procedures.

Why are ambulatory surgery centers viewed as attractive venues for fusion procedures?

ASCs combine shorter turnover times with proven safety records, allowing payers and providers to realize substantial cost savings without sacrificing clinical outcomes.

What impact do bundled payment models have on implant selection?

Hospitals now choose devices based on total episode value, favoring systems that pair strong clinical evidence with lower long-term complication expenses.

How is artificial intelligence influencing intra-operative decision-making?

AI-guided navigation platforms overlay anatomical data in real time, helping surgeons optimize screw trajectories and reduce radiation exposure for both staff and patients.

What is the primary clinical concern limiting unlimited use of rigid fusion constructs?

Long-term studies highlight adjacent-segment disease as a meaningful risk, prompting interest in motion-preserving solutions and hybrid stabilization techniques.

Page last updated on: