Market Overview

| Study Period | 2020 - 2030 |

|---|---|

| Forecast Data Period | 2025 - 2030 |

| Historical Data Period | 2020 - 2023 |

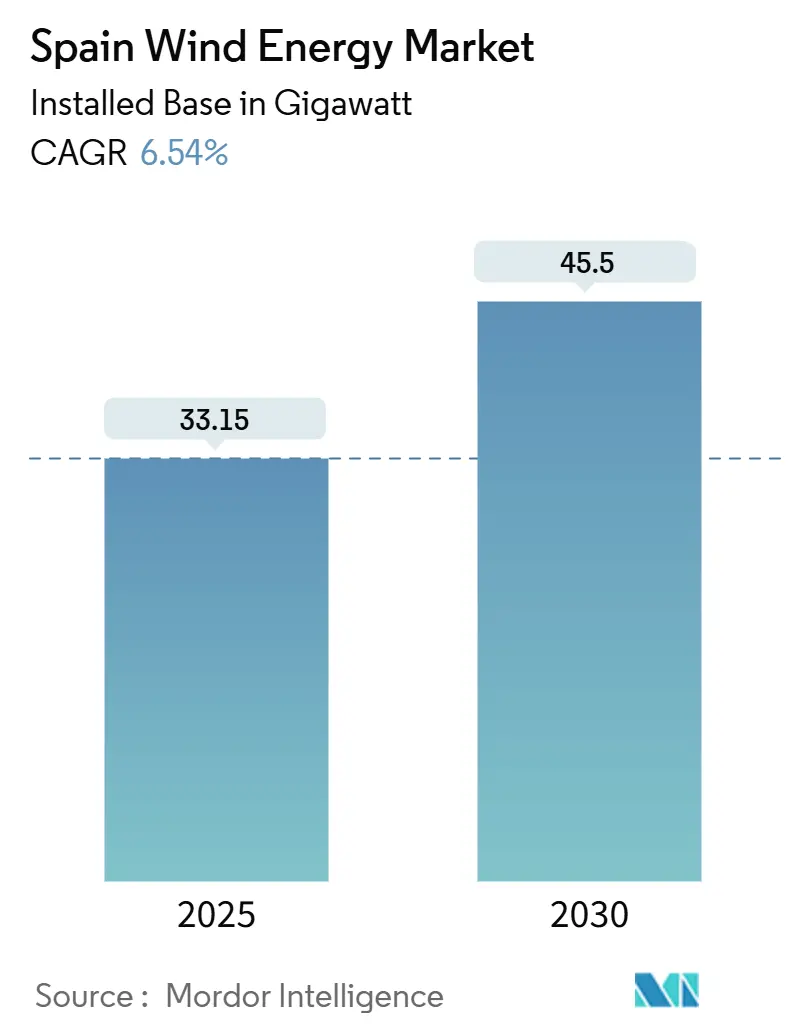

| Market Volume (2025) | 33.15 gigawatt |

| Market Volume (2030) | 45.5 gigawatt |

| Growth Rate (2025 - 2030) | 6.54% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Wind Energy Market Analysis by Mordor Intelligence

The Spain Wind Energy Market size in terms of installed base is expected to grow from 33.15 gigawatt in 2025 to 45.5 gigawatt by 2030, at a CAGR of 6.54% during the forecast period (2025-2030).

National electricity data confirm that wind already contributes 23.2% of Spain’s power mix. Growth is propelled by the Integrated National Energy and Climate Plan (PNIEC), which anchors the 62 GW target and mandates sustained annual additions of about 4.2 GW. Investors view the Spain wind energy market as a hedge against geopolitical volatility, while regulators frame it as a pillar of energy sovereignty. Policy certainty, an accelerating corporate PPA pipeline, and active repowering of aging fleets converge to create a sizeable runway for capacity expansion despite grid congestion and permitting bottlenecks.

Key Report Takeaways

- By location, onshore accounted for 100.0% of installed capacity in 2024, whereas offshore is forecast to expand at a 139.4% CAGR through 2030, reshaping the Spain wind energy market share.

- By turbine capacity, the 3-6 MW class captured 58.7% of the Spain wind energy market size in 2024, but turbines above 6 MW are expected to post a 12.8% CAGR to 2030.

- By application, utility-scale plants held 91.3% of installed capacity in 2024; community projects show the fastest growth outlook at a 16.2% CAGR through 2030.

- By component, blades represented the cost focus in 2024, and recyclable designs are projected to command 70% of repowering demand by 2030.

Spain Wind Energy Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| EU 2030 Renewable-Energy Mandate | +1.80% | National, aligned with EU decarbonization goals | Long term (≥ 4 years) |

| Repowering of Ageing Spanish Fleets | +1.20% | Castilla y León, Galicia, Aragón | Medium term (2-4 years) |

| Grid-connected Corporate PPA Boom | +1.00% | Madrid and Barcelona industrial corridors | Medium term (2-4 years) |

| Hybrid Wind-Solar Project Economics | +0.60% | Andalucía, Extremadura | Medium term (2-4 years) |

| Floating-Offshore Pilot Successes | +0.80% | Canary Islands, Galicia, Basque Country | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

EU 2030 Renewable-Energy Mandate

Spain aligns its PNIEC with the EU directive requiring 42.5% renewable energy in final energy consumption by 2030, dedicating EUR 27.6 billion from its Recovery and Resilience Plan to climate measures.[1]European Commission, “Spain Recovery and Resilience Plan,” ec.europa.eu Nearly 300 approved wind and solar projects, representing 28 GW, now queue for construction permits, and Iberdrola has partnered with Norway’s sovereign fund on 2.6 GW of joint capacity that will feed both the domestic grid and future green-hydrogen exports.[2]Iberdrola, “Iberdrola and Norway’s Sovereign Fund Sign 2.6 GW Agreement,” iberdrola.com

Repowering of Aging Spanish Fleets

Roughly half of the installed turbines are over 20 years old, prompting Galicia’s decree that 20 legacy farms must complete repowering within 18 months. Iberdrola’s first four projects replace 200 turbines with 82 modern units while raising annual output by 30%. EDP’s Galician upgrade cut the fleet from 80 to 10 turbines yet doubled generation to 100 GWh, underscoring the productivity gains available through modernization. Blade-recycling centres opened by ACCIONA and Iberdrola now process about 6,000 t of composites per year and create a circular-economy service niche.

Grid-Connected Corporate PPA Boom

Long-term renewable contracts underpin 10–15-year cash flows and are displacing subsidy schemes. Iberdrola alone signed 900 MW of PPAs during 2024, including a 35 MW deal with Google for the Cascante wind farm. Capital Energy’s 80 GWh arrangement with Cementos Portland Valderrivas demonstrates that Spain wind energy market developers now scout industrial corridors as eagerly as windy ridges.

Hybrid Wind-Solar Project Economics

ACCIONA Energía’s Cuenca hybrid couples 36 MW of wind with 29.4 MW of PV and generates 105,670 MWh yearly, illustrating how complementary profiles lift grid utilization. Enlight Renewable Energy’s 554 MW Gecama hybrid attracted USD 310 million of financing, signalling investor belief that multi-technology plants reduce curtailment risk.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Sub-station Bottlenecks in Rural Spain | −0.9% | Castilla-La Mancha, Aragón, Galicia | Short term (≤ 2 years) |

| Slow Environmental Permitting Cycle | −0.5% | Regions with protected bird habitats | Medium term (2-4 years) |

| Turbine-Blade Waste Management Gap | −0.2% | National | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Slow Environmental Permitting Cycle

EU regulators urged Spain to accelerate review timelines after only one-third of PNIEC-aligned renewable projects secured construction permits by 2024.[3]PV-Magazine, “EU Urges Spain to Accelerate Permits,” pv-magazine.comCourt interventions, such as the suspension of the La Espina farm to protect capercaillie habitat, highlight legal risks. Regional disparities in processing speed create a patchwork landscape in which developers sometimes select sub-optimal wind sites simply to avoid protracted litigation.

Turbine-Blade Waste Management Gap

First-generation turbines are reaching end-of-life, and Galicia alone forecasts over 6,000 t of composite waste each year by 2028. Iberdrola and ACCIONA have opened Spain’s first dedicated blade-recycling plants using mechanical and pyrolysis treatments, yet nationwide standards remain pending, and costs remain above landfill disposal.[4]ACCIONA, “Blade Recycling Facility Launch,” acciona.com

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Location: Offshore Emerges from Onshore’s Shadow

Onshore wind dominated the Spain wind energy market share at 100.0% in 2024, the legacy of two decades of feed-in tariffs that filled prime corridors across Castilla y León, Galicia, and Aragón. Capacity growth now leans on repowering, hybridization, and distribution-level projects, as greenfield options shrink under land-use and permitting constraints. Offshore capacity was negligible in 2024, but the first seabed auction in 2025 is set to propel offshore to an estimated 3 GW by 2030, translating into a 139.4% CAGR and introducing marine supply-chain clusters along Galicia and the Canary Islands.

Floating platforms unlock deep-water wind regimes where capacity factors exceed 50%, narrowing the cost gap with onshore assets to about 20% when local-content credits are included. Iberdrola’s 300 MW Windanker project will use tension-leg platforms that reduce steel by 35% and cut installation cycles under 48 hours. The ROFF decree’s 60% domestic sourcing rule is catalyzing investments in Galician blade plants and Basque tower yards, embedding industrial value inside Spain even before commercial offshore turbines spin. Onshore remains relevant through hybrid wind-solar-storage schemes that exploit existing interconnections, but offshore’s rise will diversify generation geography and revenue streams across the Spain wind energy market.

By Turbine Capacity: Scaling Up to Extract More from Less

Turbines rated 3-6 MW captured 58.7% of the Spain wind energy market in 2024, mirroring grid design limits and road logistics that historically favored midsize machines. Direct-drive 6 MW units like the SG 6.6-170 deliver 120-m hub heights and 85-m blades, lifting site yields by 15-20% without imposing outsized transport costs. Above-6 MW turbines are projected to grow at a 12.8% CAGR to 2030 as repowering projects condense three 2 MW legacies into one 7-8 MW giant, slashing O&M tasks by 40% and improving project IRRs.

Iberdrola’s 431 MW Castilla y León upgrade showed a 38% capacity factor, six points above the national average, by exploiting higher wind layers and improved generator efficiencies. Winter icing remains a risk in mountainous sites; Nordex’s N163 blade-heating feature extends generation hours by 8%, a niche still within the 6-7 MW range. Sub-3 MW units have shifted to specialized roles where tower height caps or community acceptance dictate smaller envelopes. As blades stretch beyond 90 m, port infrastructure and highway clearance upgrades become critical, favoring vertically integrated suppliers that can coordinate end-to-end logistics throughout the Spain wind energy market.

By Application: Utility-Scale Dominance with Community Upside

Utility-scale parks held 91.3% of installed capacity in 2024 and continue to anchor the Spain wind energy market, offering EUR 30 per MWh LCOE when built at scale. Corporate PPAs influenced 40% of 2024 additions, shifting investor focus toward profile-matched hybrid layouts that command 15% above-market tariffs yet reduce balancing costs for tech and industrial off-takers.

Community projects, though modest today, are set for a 16.2% CAGR through 2030 following a policy that guarantees EUR 50 per MWh for sub-5 MW cooperative assets connecting at the distribution level. By cutting interconnection fees by 60% and compressing permitting to under 12 months, these schemes unlock participation by municipalities and citizen groups. The 3 MW Valdepeñas wind cooperative already covers 40% of local load and pays annual dividends to 200 shareholders, exemplifying community alignment. C&I self-consumption remains capped at 1 MW per site; raising the threshold to 5 MW under a pending decree could unleash 500 MW of incremental demand by 2027 and further segment growth across the Spain wind energy market.

Geography Analysis

Castile-La Mancha anchors the Spain wind energy market with 1,737.5 MW spread across 56 Iberdrola farms that benefit from flat topography and favorable wind regimes. The regional government has fast-tracked hybrid wind-solar permits, enabling developers to maximize scarce grid connection points and trim curtailment. Investment programs exceeding EUR 17 billion are in the queue, including storage projects that complement variable generation profiles.

Galicia is the laboratory for large-scale repowering. Regional rules compel owners of 25-year-old farms to submit upgrade plans within 18 months, and pilot projects already raise average output from 1,300 to 1,700 full-load hours per year. The Atlantic coastline also supplies Spain’s top sites for pilot floating turbines, giving Galicia an early-mover edge in offshore supply-chain formation.

Andalusia, whose dual coastlines face both the Atlantic and Mediterranean, is earmarked for nearly half of the EUR 700 million national storage incentive package, allowing existing onshore arrays to shift output into evening peaks. La Pinta, a 50 MW floating concept off Granada-Almería, heads a project queue preparing for upcoming marine auctions. Catalonia’s PLEMCAT, a 30 MW experimental marine platform, conducts trial runs of sensor networks and maintenance robotics that could reduce OPEX across the Spain wind energy market. Meanwhile, Aragon and Valencia leverage high-voltage links into industrial belts, prompting developers to structure PPA-anchored projects that feed direct to factories, and the Canary Islands await the nation’s inaugural offshore auction, buoyed by premium local power prices that shorten payback periods for floating foundations.

Competitive Landscape

Iberdrola remains the reference player in the Spain wind energy market, operating 6,469 MW onshore and channeling a EUR 2 billion joint venture with Norway’s sovereign wealth fund into 2.6 GW of forthcoming capacity. It deploys a Generative AI Center of Excellence and over 100 digital applications to shave OPEX and boost availability, underscoring how data fluency is now strategic.

ACCIONA positions itself at the nexus of hybrid plants and blade recycling, opening Spain’s first industrial-scale composite recovery facility and floating offshore-developing Cuenca’s flagship wind-solar hybrid. Vestas and Siemens Gamesa vie for the repowering market, each tailoring 4–6 MW machines to Spain’s medium-wind classes; Siemens Gamesa adds recyclable blades to its pitch.

Disruptors such as Capital Energy and Exus Renewables focus on long-term PPAs with energy-intensive clients. Their agile commercial models allow rapid execution where incumbents face utility-scale approval cycles. International players RWE, Statkraft, and Ørsted establish R&D and supply-chain partnerships with Spanish engineering firms to capitalize on floating offshore expertise.[5]Financial Times, “Oil Majors Enter Spanish Wind,” ft.com

Spain Wind Energy Industry Leaders

Siemens Gamesa Renewable Energy, S.A.

Vestas Wind Systems A/S

Acciona SA

Iberdrola SA

Naturgy Energy Group SA

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Naturgy Energy Group SA is upgrading its 49.6-MW Somozas wind farm in Galicia, Spain, replacing 81 turbines with nine Vestas machines to boost output and reduce visual impact. Backed by a EUR 67 million investment from the EU’s NextGenerationEU recovery funds via Spain’s Circular Repowering programme, the farm’s capacity will slightly decrease to 46.4 MW but generate 168 GWh annually, powering 48,000 households. Vestas will supply seven V150-6.0 MW and two V110-2.2 MW turbines, along with a ten-year AOM 4000 service agreement. Commissioning is planned for Q2 2026.

- June 2025: Enlight Renewable Energy Ltd has secured approximately USD 310 million in financing to support the transformation of its 329MW Gecama wind farm into the largest hybrid power complex in Spain.

- March 2025: In March 2025, Exus Renewables inked a decade-long Power Purchase Agreement (PPA) with tech giant Google. Under this deal, Exus will provide 35 MW of renewable electricity sourced from the Cascante wind farm located in Navarra, Spain. This renewable energy commitment not only fuels Google's operations in Spain but also bolsters the company's ambition of reaching net-zero emissions. The 51 MW Cascante wind farm, with its annual output projected at over 136 GWh, has the capacity to energize more than 41,000 households.

Spain Wind Energy Market Report Scope

Wind energy is a form of renewable energy that harnesses the power of the wind to generate electricity. It involves using wind turbines to convert the turning motion of blades, pushed by moving air (kinetic energy) into electrical energy (electricity). The Spanish Wind Energy Market is segmented by location, application, and component. By location, the market is segmented into onshore and offshore. By turbine capacity, the market is segmented into up to 3 MW, 3 to 6 MW, and above 6 MW. By application, the market is segmented into utility-scale, commercial, and industrial, community Projects. The report also covers the market size and forecasts for Spain.

For each segment, the market sizing and forecasts have been done based on the installed capacity (GW).

By Location

| Onshore |

| Offshore |

By Turbine Capacity

| Up to 3 MW |

| 3 to 6 MW |

| Above 6 MW |

By Application

| Utility-scale |

| Commercial and Industrial |

| Community Projects |

By Component (Qualitative Analysis)

| Nacelle/Turbine |

| Blade |

| Tower |

| Generator and Gearbox |

| Balance-of-System |

| By Location | Onshore |

| Offshore | |

| By Turbine Capacity | Up to 3 MW |

| 3 to 6 MW | |

| Above 6 MW | |

| By Application | Utility-scale |

| Commercial and Industrial | |

| Community Projects | |

| By Component (Qualitative Analysis) | Nacelle/Turbine |

| Blade | |

| Tower | |

| Generator and Gearbox | |

| Balance-of-System |

Key Questions Answered in the Report

What is Spain’s installed wind capacity forecast for 2030?

The Spain wind energy market is projected to reach 45.50 GW of installed capacity by 2030, up from 33.15 GW in 2025.

How fast will offshore wind grow in Spain?

Offshore installations are expected to grow at a 139.4% CAGR through 2030 once the first seabed auction concludes in 2025.

Which turbine class leads current deployments?

Turbines rated 3-6 MW hold 58.7% of installed capacity, but units above 6 MW are the fastest-growing segment due to repowering.

Why are corporate PPAs critical for Spanish developers?

Corporate PPAs secure 10-15-year revenue streams, reduce merchant risk, and already back 40% of utility-scale additions.

What policy measure most affects future capacity?

The EU-mandated target for 81% renewable electricity by 2030 drives Spain’s commitment to 62 GW of total wind capacity, including 3 GW offshore.

How is Spain addressing turbine-blade waste?

Siemens Gamesa’s commercial RecyclableBlade and cement co-processing pilots aim to recycle legacy blades and cut landfill costs.

Page last updated on: