Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

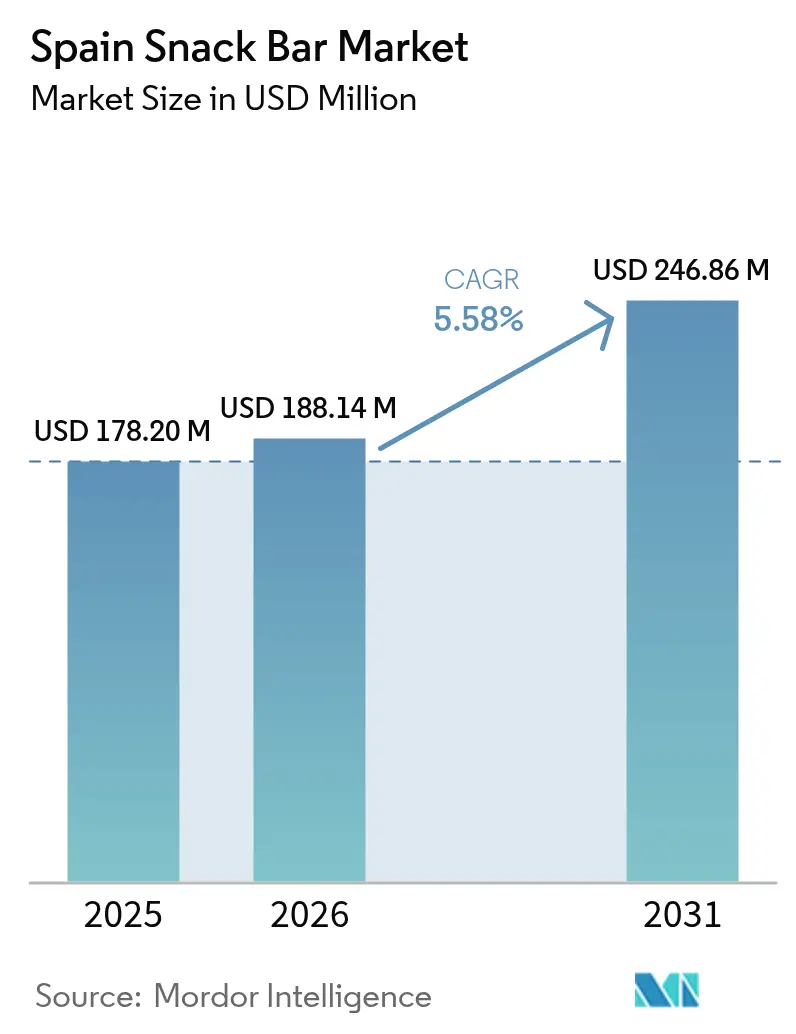

| Base Year Market Size (2025) | USD 178.20 Million |

| Market Size (2026) | USD 188.14 Million |

| Market Size (2031) | USD 246.86 Million |

| Growth Rate (2026 - 2031) | 5.58% CAGR |

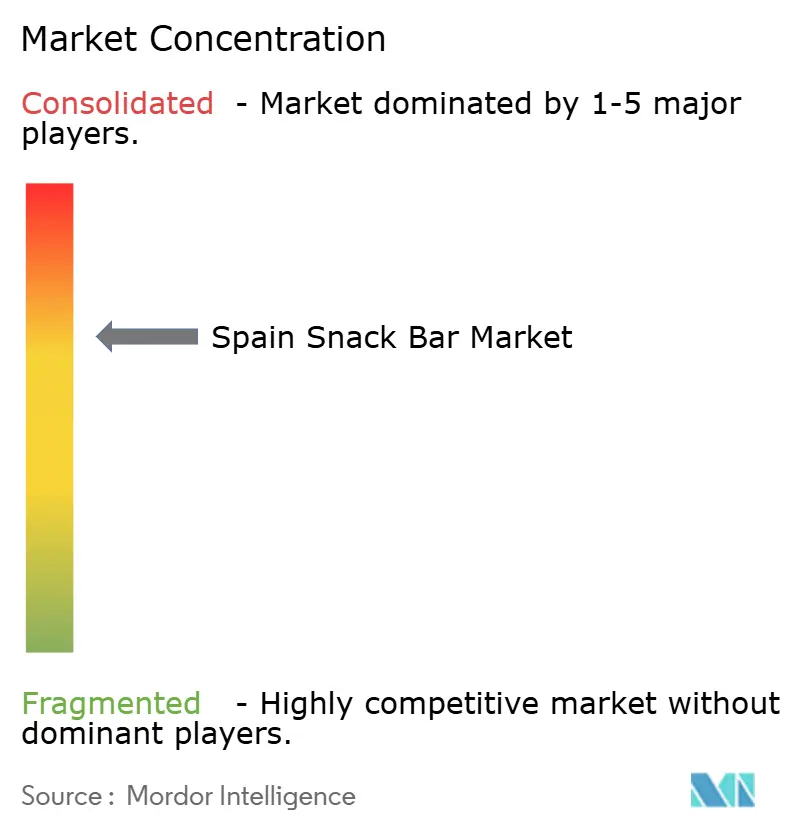

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Snack Bar Market Analysis by Mordor Intelligence

The Spain snack bar market size was valued at USD 178.20 million in 2025 and estimated to grow from USD 188.14 million in 2026 to reach USD 246.86 million by 2031, at a CAGR of 5.58% during the forecast period (2026-2031). Spain is actively driving the evolution of this market, fueled by shifting consumer preferences and lifestyle changes. The increasing focus on health and wellness, coupled with a growing demand for convenient on-the-go snacks, has positioned the country as a key player in shaping market trends. The expanding fitness and sports culture in urban areas further accelerates this growth. Spanish consumers are increasingly prioritizing functional, nutrient-dense, and clean-label products, pushing manufacturers to innovate with protein-rich, nut-based, and granola/oat formulations. Additionally, advancements in flavors, textures, and functional benefits are being introduced to meet the evolving demands of this dynamic market.

Key Report Takeaways

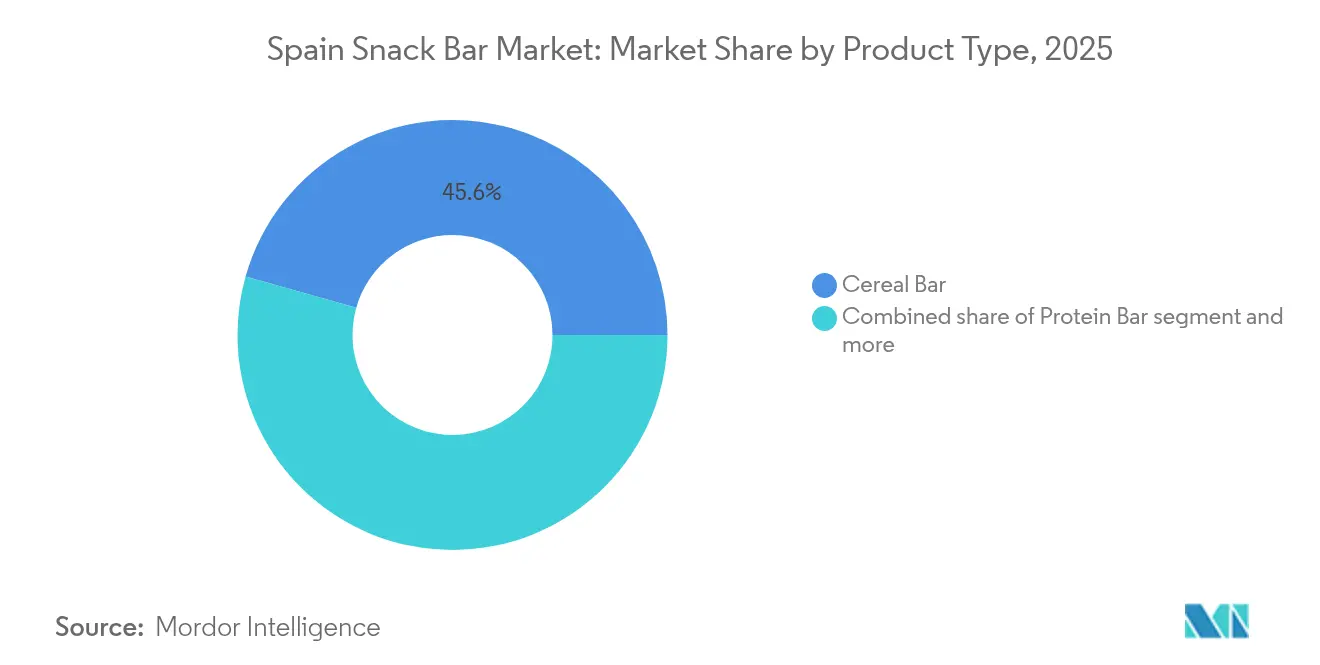

- By product type, cereal bars led with 45.62% of Spain snack bar market share in 2025, while protein bars are advancing at a 6.15% CAGR through 2031.

- By ingredient base, nut-driven formulations captured 29.44% of the Spain snack bar market size in 2025, whereas granola and oat bars are forecast to expand at a 6.29% CAGR.

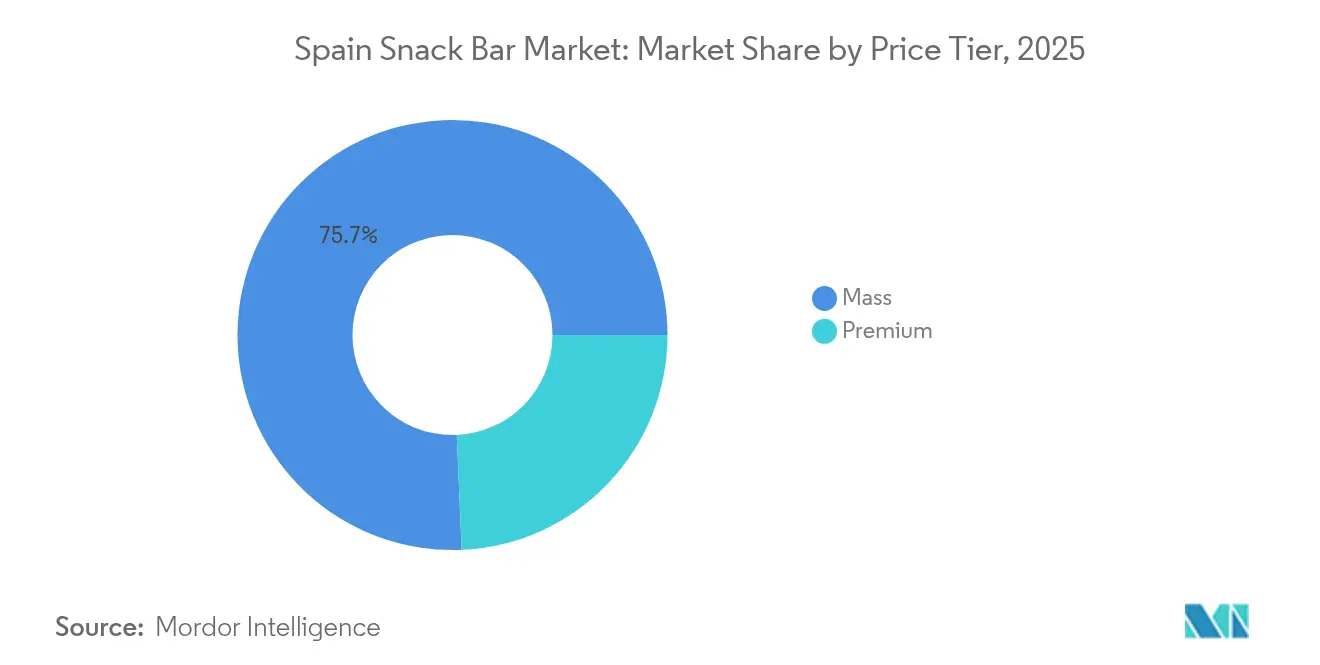

- By price tier, the mass segment held 75.68% revenue share in 2025, yet premium bars record the highest projected CAGR at 7.01% through 2031.

- By distribution channel, supermarkets and hypermarkets controlled 51.74% of sales in 2025, but online retail is climbing at an 7.62% CAGR to the end of the decade.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Snack Bar Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rising health and wellness awareness | +1.0% | National, strongest in Madrid, Barcelona, Valencia urban centers | Medium term (2-4 years) |

| Rise in on-the-go lifestyles | +0.9% | National, accelerated in metropolitan areas and commuter corridors | Short term (≤ 2 years) |

| Growth in fitness and sports culture | +0.8% | National, concentrated in Catalonia, Madrid, Andalusia | Medium term (2-4 years) |

| Innovation in flavors and textures | +0.7% | National, with premium-tier early adoption in urban markets | Long term (≥ 4 years) |

| Plant-based and vegan movement | +0.6% | National, strongest in Barcelona, Madrid, Valencia progressive urban centers | Medium term (2-4 years) |

| Clean label and natural ingredient preference | +0.5% | National, with heightened demand in health-conscious demographics | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Rising health and wellness awareness

A significant driver of the Spain snack bar market is the increasing consumer emphasis on health, wellness, and functional nutrition, mirroring a global trend toward mindful eating and preventive lifestyle choices. Spanish consumers are progressively seeking snacks that deliver nutritional benefits without sacrificing taste. These preferences include products high in protein, fiber, and natural ingredients, while avoiding artificial additives, preservatives, and excessive sugar. This trend is particularly evident among urban professionals and fitness-focused individuals who value convenient yet nutritious snack options to support their active lifestyles. For example, brands like Be-Kind Snacks offer Nut Protein Bars that are gluten-free, high in fiber, and free from artificial colors, flavors, or preservatives, catering directly to the preferences of health-conscious consumers. Such products highlight the growing demand for clean-label, nutrient-rich, and functionally designed snacks that not only address hunger but also align with dietary goals, weight management, and overall wellness.

Rise in on-the-go lifestyles

The Spain snack bar market is primarily driven by the increasing prevalence of busy, on-the-go lifestyles. Consumers are seeking quick, convenient, and portable nutrition options that align with demanding work schedules, travel routines, and active daily activities. Urban professionals, students, and fitness enthusiasts often prefer snacks that are easy to consume without requiring preparation or refrigeration, making snack bars a suitable choice. This shift in lifestyle has led manufacturers to emphasize single-serve packaging, compact formats, and multipacks, while also focusing on products that offer nutritional benefits such as protein, fiber, or functional ingredients. Additionally, the demand for multi-functional bars that serve as meal replacements, energy boosters, or wellness supplements is growing, allowing consumers to combine health and convenience effortlessly. As urbanization and commuting patterns in Spain continue to rise, on-the-go consumption habits are solidifying snack bars as a regular part of daily routines, driving innovation, market penetration, and overall growth.

Growth in fitness and sports culture

The growing fitness and sports culture in Spain is a key factor driving the snack bar market. As more consumers adopt exercise routines, gym activities, and active lifestyles, the demand for functional snack bars offering energy, protein, and recovery benefits has increased. These products appeal to both casual fitness enthusiasts and dedicated athletes. Functional snack bars, including protein, energy, and sports nutrition varieties, are increasingly viewed as integral components of fitness-oriented diets, supporting muscle recovery, endurance, and overall wellness. For example, data from The Association for Media Research (AIMC) in 2023 indicates that approximately 16.5% of the surveyed population in Spain had visited a gym, reflecting a growing segment of health-conscious and physically active individuals [1]Source: The Association for Media Research (AIMC), "Share of respondents who went to a fitness studio", aimc.es. This consumer group seeks nutrient-rich, convenient snacks that align with their fitness objectives, prompting manufacturers to create specialized formulations, introduce high-protein or low-sugar options, and market products with a focus on performance benefits.

Innovation in flavours and textures

Innovation in flavors and textures is a significant driver of the Spain snack bar market, as consumers increasingly seek diverse sensory experiences alongside nutritional benefits. Modern snack bar consumers are moving beyond standard cereal or nut flavors, actively exploring unique taste combinations, indulgent textures, and functional ingredient blends that enhance product differentiation and enjoyment. Manufacturers are addressing this demand by offering products with varied textures, such as crunchy, chewy, or layered formats, paired with inventive flavor profiles to attract consumer interest and encourage repeat purchases. For example, Nature Valley in Spain offers the Nature Valley Protein Bar with Salted Caramel, combining a popular indulgent flavor with a high-protein formulation, demonstrating how taste innovation can meet both sensory and functional expectations. By consistently experimenting with flavor pairings, textures, and ingredient formats, brands can appeal to adventurous consumers, drive engagement, and support market growth, making innovation a critical factor in the development of Spain’s snack bar market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High competition from alternative snacks | -0.6% | National, intensified in urban retail channels and e-commerce | Short term (≤ 2 years) |

| Sugar reduction regulations and labeling scrutiny | -0.5% | National, EU-wide regulatory pressure from AESAN and EFSA | Medium term (2-4 years) |

| Taste fatigue and limited differentiation | -0.4% | National, most acute in mass-tier cereal bar segment | Short term (≤ 2 years) |

| Supply chain and input volatility | -0.5% | National, with global commodity exposure for nuts, oats, cocoa | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

High competition from alternative snacks

The Spain snack bar market encounters notable challenges due to intense competition from alternative snacks and the risk of consumer taste fatigue. A wide range of snack options, such as nuts, dried fruits, ready-to-eat meals, yogurt-based snacks, and savory packaged products, directly competes with snack bars for consumer attention and spending. This variety of alternatives can hinder market growth, particularly among consumers seeking diverse or novel experiences, as repeated consumption of similar bar flavors and textures may result in taste fatigue. Within the snack bar segment itself, products that lack innovation in flavor, texture, or nutritional value may find it difficult to retain consumer loyalty. Consequently, manufacturers must consistently update product offerings, develop new formulations, and strike a balance between indulgence and functionality to sustain consumer interest. Without ongoing innovation, the combined impact of alternative snack options and taste fatigue may limit market penetration and slow the adoption of traditional or mass-market snack bars in Spain.

Sugar reduction regulations and labelling scrutiny

The Spain snack bar market is experiencing increasing regulatory pressure regarding sugar content and labeling transparency, which poses significant challenges to product development and market growth. Health authorities and consumer advocacy groups are demanding more accurate nutritional labeling, clear ingredient disclosures, and adherence to sugar reduction targets. These stringent requirements compel manufacturers to reformulate products to comply with stricter standards. While these regulations aim to improve public health outcomes, they can lead to higher production costs, restrict the use of widely preferred sweeteners, and alter taste profiles, potentially diminishing consumer appeal if not managed effectively. Furthermore, companies must address complex labeling requirements to highlight health benefits without making unverified claims. Non-compliance or misleading packaging can result in financial penalties, legal repercussions, and long-term damage to brand credibility, emphasizing the need for careful navigation of these regulatory landscapes.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Protein Bars Outpace Traditional Cereal Formats

Cereal bars accounted for 45.62% of the Spain Snack Bar Market in 2025, maintaining their leading position due to their alignment with Spanish consumers' preference for simple, familiar, and naturally wholesome ingredients, such as oats, grains, and seeds. Their popularity is further supported by their association with healthy convenience, offering a balance of energy, fiber, and satiety. Manufacturers are innovating with ancient grains, superfood inclusions, gluten-free options, and plant-based recipes to align with wellness and sustainability trends. These efforts ensure cereal bars remain relevant and modern, despite being a traditional category. This growth is bolstered by Spain's strong integration into grain-based food value chains. For example, according to the Observatory of Economic Complexity (OEC), Spain imported EUR 4.69 billion worth of cereals in 2024, highlighting the country's significant reliance on and availability of cereal-based raw materials . This supports continued growth, product diversification, and supply stability for the cereal bar segment.

Protein bars are projected to grow at a 6.15% CAGR from 2026 to 2031, solidifying their position in the Spain Snack Bar Market as consumers increasingly prioritize performance-oriented and functional nutrition. This segment is driven by a rising interest in fitness culture, increased participation in sports, gym activities, and outdoor recreation, as well as growing awareness of the benefits of protein intake for muscle recovery, satiety, and overall health. Unlike traditional snack bars, protein bars are recognized as nutritionally purposeful snacks, offering benefits such as high protein content, low sugar formulations, and targeted functionalities like energy balance or recovery support. The segment is evolving through cleaner-label formulations, increased use of plant-based proteins (e.g., pea, rice, and blended sources), reductions in artificial sweeteners, and improvements in texture and taste to address consumer concerns about chalkiness or hardness.

By Ingredient Base: Granola and Oats Gain on Clean-Label Momentum

Nut-based bars accounted for 29.44% of the Spain Snack Bar Market in 2025, dominating the ingredient-based segment due to their perceived health benefits, high satiety value, and natural nutrient density. Spanish consumers increasingly associate nuts like almonds, hazelnuts, and walnuts with heart health, protein content, and sustained energy, making these bars a preferred choice for everyday snacking and functional nutrition. The segment is advancing through innovative combinations with wholesome ingredients such as dried fruits, seeds, and whole grains, enhancing both flavor and nutritional value while aligning with clean-label and minimally processed preferences. Manufacturers are also introducing plant-based protein blends and allergen-conscious formulations, such as nut mixes with oats or seeds, to attract a broader health-conscious audience while maintaining a premium market position.

Granola and oat-based bars are expected to grow at a 6.29% CAGR through 2031, driven by their increasing popularity as a healthy, convenient, and versatile snack option in Spain. Consumers recognize oats and whole grains as heart-healthy, fiber-rich, and naturally sustaining, making these bars appealing for daily energy, weight management, and overall wellness. The segment is evolving with innovative flavor combinations, functional enhancements, and clean-label formulations, including the incorporation of superfoods, seeds, dried fruits, and plant-based proteins to boost nutritional value without compromising taste. Reformulations aimed at reducing sugar content and using natural sweeteners like honey or dates are further increasing consumer acceptance and encouraging repeat purchases.

By Price Tier: Premium Segment Surges on Functional Claims

The mass-tier segment accounted for 75.68% of the Spain Snack Bar Market in 2025 and continues to lead due to its accessibility, affordability, and broad appeal across diverse consumer groups. This segment primarily targets everyday consumers who value convenience, familiar flavors, and consistent quality over premium or niche offerings. Mass-tier bars are the default choice for most households, supported by ongoing innovations in taste, texture, and ingredient quality. These include healthier formulations with reduced sugar, the inclusion of whole grains, and fortification with nuts or dried fruits, enabling the segment to align with evolving health-conscious preferences without significant price increases.

Premium-tier snack bars are projected to grow at a 7.01% CAGR from 2026 to 2031, driven by increasing consumer demand for high-quality, functional, and indulgent snacking options. Unlike mass-tier bars, premium bars cater to health-conscious and lifestyle-oriented consumers willing to pay a premium for natural, clean-label ingredients, plant-based proteins, superfoods, and innovative flavor profiles. The segment is advancing through the inclusion of functional benefits such as enhanced protein content, probiotics, vitamins, and adaptogens, positioning premium bars as wellness-oriented lifestyle products rather than just snacks.

By Distribution Channel: E-Commerce Accelerates as Omnichannel Becomes Table Stakes

Supermarkets and hypermarkets accounted for a significant 51.74% share of the Spain Snack Bar Market in 2025, underscoring their pivotal role in influencing consumer snack preferences and driving market growth. Their dominance stems from their ability to provide a diverse range of products across various price points, flavors, and ingredient types. This makes them a preferred destination for both everyday cereal bars and emerging functional options, such as protein or nut-based bars. The segment is adapting to shifting consumer preferences, with an increasing focus on healthier, clean-label, and premium products to cater to the rising demand for wellness-oriented snacks. Additionally, the growth of private-label snack bars, which offer a balance of affordability and quality, further enhances the appeal of this segment.

Online retail for snack bars in Spain is anticipated to grow at a strong CAGR of 7.62% through 2031, driven by the rising adoption of digital shopping, convenience-oriented lifestyles, and the demand for product variety. This channel is evolving as consumers, particularly those aged 35 to 54, seek the convenience of comparing products, accessing niche or premium offerings, and purchasing functional snacks such as protein, nut-based, and clean-label bars from home. According to the Spanish Statistical Office, in 2024, approximately 5.9 million individuals aged 45 to 54 purchased products or services online in Spain, followed closely by 5.51 million people aged 35 to 44 . This highlights the expanding digital consumer base for snack bars. Manufacturers are increasingly addressing this trend by introducing subscription models, online-exclusive flavors, and convenient multipacks, while also prioritizing transparency regarding ingredients and nutritional benefits.

Geography Analysis

Spain's snack bar market demonstrates significant regional variation influenced by urbanization, lifestyle habits, and dietary traditions. Major urban centers such as Madrid, Barcelona, and Valencia drive overall demand due to their high population density, fast-paced lifestyles, and heightened awareness of health and wellness trends. These cities account for a substantial share of premium and protein bar consumption, as urban professionals increasingly seek convenient, nutritionally functional, and balanced snacking options that align with their busy routines.

Regions like Catalonia and Madrid stand out for their strong fitness culture, characterized by widespread gym memberships, active running communities, and participation in outdoor activities. This environment supports demand for sports nutrition-focused snack bars, including protein and energy bars, mirroring broader Western European trends where urban and active populations drive the adoption of functional food products. The combination of health-conscious consumers and openness to innovative formulations makes these regions particularly appealing for new product developments.

Spain’s coastal regions, such as the Costa del Sol and Costa Brava, experience seasonal demand spikes driven by tourism and outdoor recreational activities. The influx of domestic and international visitors during peak travel seasons boosts the consumption of portable, on-the-go snack formats. This trend encourages manufacturers to develop single-serve bars featuring diverse flavors, functional benefits, and natural ingredients. These seasonal consumption patterns provide opportunities for brands to optimize product offerings and tailor marketing strategies to cater to both local residents and transient tourists, supporting growth across Spain’s varied geographic landscape.

Competitive Landscape

The Spain snack bar market is highly fragmented, with a combination of global corporations and smaller niche players influencing its competitive dynamics. Leading multinational companies such as Nestlé S.A., PepsiCo Inc., Mars, Incorporated, and General Mills, Inc. utilize their scale, extensive distribution networks, and significant marketing resources to maintain strong positions in the cereal bar and mass-tier segments. These companies benefit from brand recognition, consistent product quality, and the ability to cater to broad consumer demands. However, their size often limits their agility, making it challenging to quickly adapt to emerging trends in functional and personalized nutrition.

This market dynamic has created opportunities in highly specific functional sub-segments. Products addressing specialized needs, such as hormonal-balance bars for women, cognitive-support bars featuring lion’s mane mushroom, or beauty-focused collagen bars, remain largely underserved by traditional players. Smaller startups and direct-to-consumer brands are capitalizing on these gaps, building loyal customer bases through social media engagement, influencer collaborations, and targeted community marketing. These strategies enable them to compete effectively despite their limited scale.

Technology adoption is another factor shaping the competitive landscape. Some brands are experimenting with AI-driven flavor development, blockchain-based traceability, and personalized subscription services. However, the adoption of these technologies varies across the market. Companies that successfully integrate these innovations gain advantages in product differentiation, consumer trust, and personalized nutrition offerings. This positions them to attract both functional snack enthusiasts and digitally savvy, health-conscious consumers.

Spain Snack Bar Industry Leaders

-

Nestlé S.A.

-

PepsiCo Inc.

-

Mars, Incorporated

-

General Mills, Inc.,

-

Associated British Foods PLC

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2024: Nestlé Fitness introduced three new products in Europe, including Spain, featuring no-added-sugar cereals as well as cocoa and honey bars, offering a versatile and protein-rich breakfast option.

- November 2023: Enervit SpA has entered into a binding agreement to acquire the remaining 50% stake in Enervit Nutrition SL from Laboratorios Farmacéuticos ROVI, securing full ownership of its Spanish branch for a total cash consideration of EUR 1.8 million.

Spain Snack Bar Market Report Scope

A snack bar is a ready-to-eat, baked product made of various ingredients, including granola, oats, chocolate, dried fruits, nuts, coconut oil, honey, peanut butter, raisins, and other dried fruit and nut ingredients.

The Spanish snack bar market is segmented by product type and distribution channel. The snack bar market offers a range of product types, including cereal, energy, and other snack bars, distributed through supermarkets/hypermarkets, convenience stores, specialty stores, online stores, and other distribution channels. For each segment, the market sizing and forecasts have been done based on value (USD).

By Product type

| Cereal Bar |

| Protein Bar |

| Fruit and Nut Bar |

By Ingredient Base

| Nut-based bars |

| Granola/Oat-based |

| Date-based |

| Dairy/Protein-based |

| Hybrid blends |

| Other |

By Price Tier

| Mass |

| Premium |

By Distribution Channel

| Supermarket/Hypermarket |

| Online Retail Store |

| Convenience Store |

| Other Distribution Channels |

| By Product type | Cereal Bar |

| Protein Bar | |

| Fruit and Nut Bar | |

| By Ingredient Base | Nut-based bars |

| Granola/Oat-based | |

| Date-based | |

| Dairy/Protein-based | |

| Hybrid blends | |

| Other | |

| By Price Tier | Mass |

| Premium | |

| By Distribution Channel | Supermarket/Hypermarket |

| Online Retail Store | |

| Convenience Store | |

| Other Distribution Channels |

Key Questions Answered in the Report

What is the revenue forecast for snack bars in Spain by 2031?

The Spain snack bar market is projected to reach USD 246.86 million by 2031, growing at a 5.58% CAGR.

Which product type is expanding the fastest?

Protein bars are advancing at a 6.15% CAGR through 2031, outpacing cereal and fruit-and-nut formats.

Why are granola and oat bars gaining traction?

Whole-grain credentials, compliance with EU Nutri-Score rules, and stable input costs underpin a 6.29% CAGR for oat-based bars.

How important is e-commerce for future growth?

Online retail is the fastest channel at an 7.62% CAGR, propelled by quick-commerce apps and subscription models.

Page last updated on: