Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

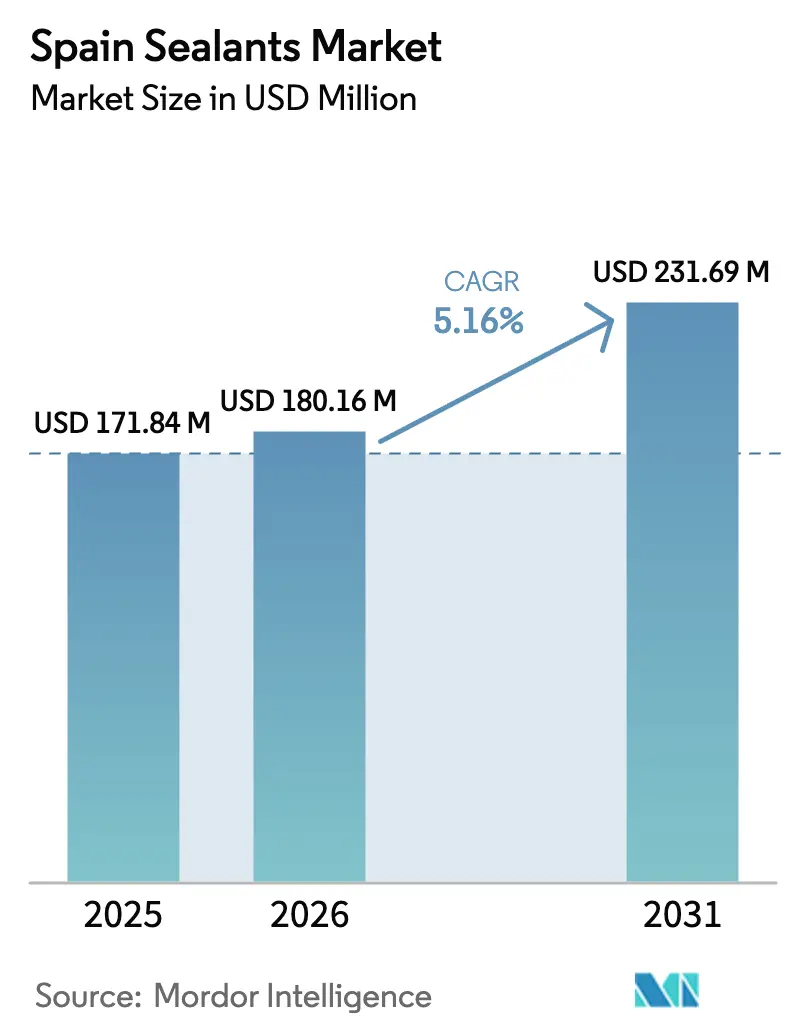

| Base Year Market Size (2025) | USD 171.84 Million |

| Market Size (2026) | USD 180.16 Million |

| Market Size (2031) | USD 231.69 Million |

| Growth Rate (2026 - 2031) | 5.16% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Sealants Market Analysis by Mordor Intelligence

The Spain Sealants Market size is projected to be USD 171.84 million in 2025, USD 180.16 million in 2026, and reach USD 231.69 million by 2031, growing at a CAGR of 5.16% from 2026 to 2031. A historic surge in deep residential rehabilitation, coupled with phased European energy-performance mandates, is anchoring steady demand for façade, window, and thermal-envelope sealants. Rapid expansion of electric-vehicle (EV) battery capacity, on-shore wind-blade refurbishments, and stricter indoor-air-quality rules are further broadening the application base for high-performance chemistries. At the same time, volatility in isocyanate and ethylene feedstocks, plus compliance costs under REACH and the Construction Products Regulation (CPR 2024), are compressing margins for undifferentiated products. Suppliers that deliver ultra-low-VOC, bio-based, or digitally traceable formulations are best placed to secure above-market growth in the Spain Sealants market.

Key Report Takeaways

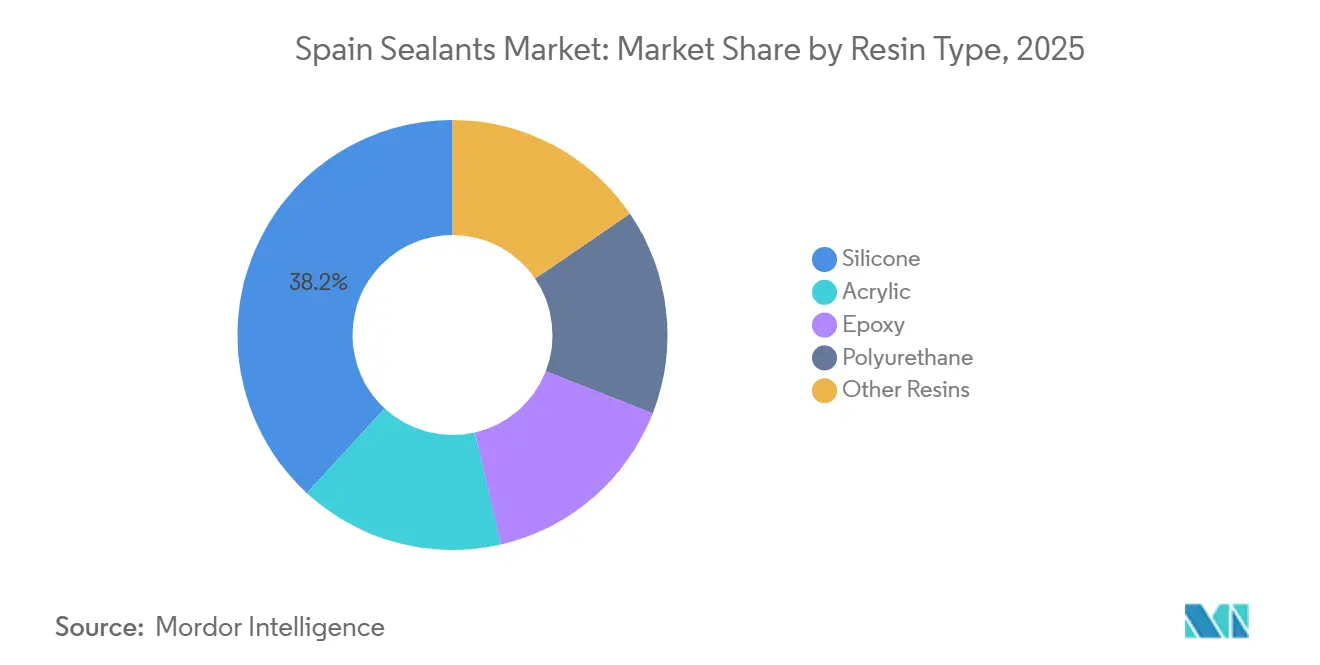

- By resin type, silicone captured 38.15% of Spain Sealants market share in 2025; polyurethane is projected to expand at a 6.96% CAGR between 2026-2031.

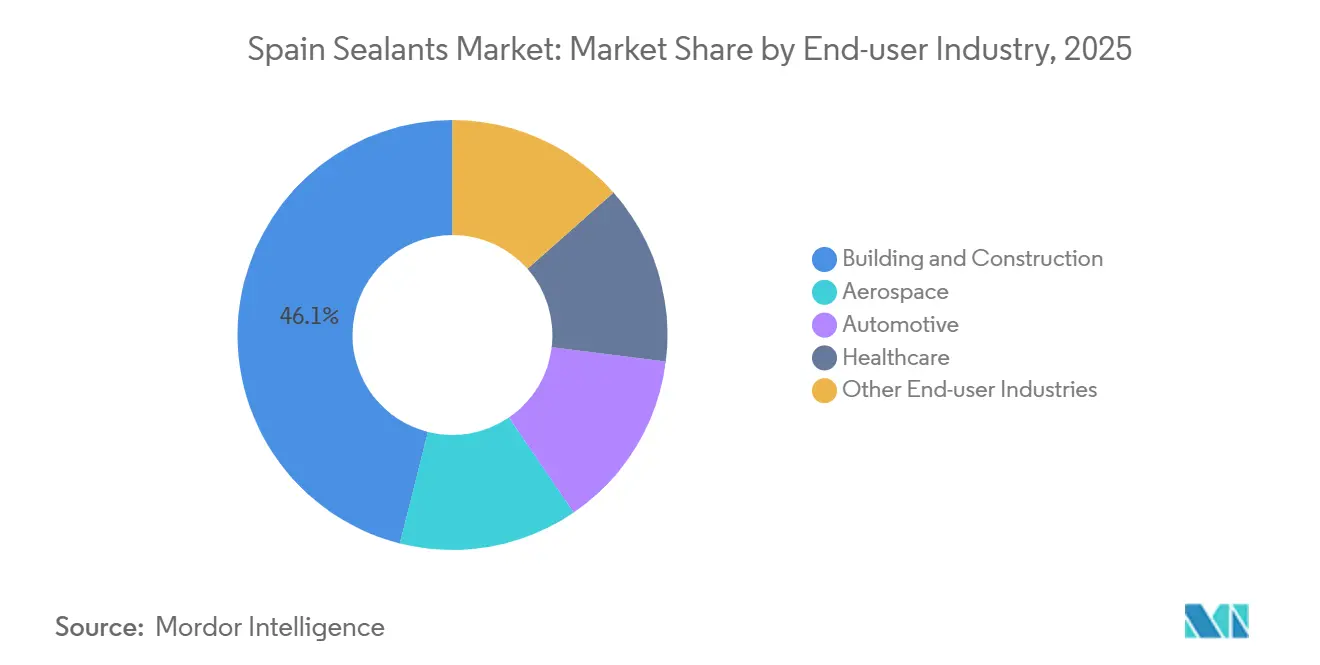

- By end-user industry, building and construction accounted for a 46.05% share of the Spain Sealants market size in 2025, while healthcare is advancing at a 7.12% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain Sealants Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation-driven demand surge in aged housing stock | +1.8% | Madrid, Catalonia, Andalusia | Medium term (2-4 years) |

| Automotive lightweighting mandates | +0.9% | Aragon, Catalonia | Medium term (2-4 years) |

| EU Fit-for-55 low-VOC requirements | +1.2% | Nationwide | Long term (≥4 years) |

| On-shore wind-blade refurbishments | +0.4% | Galicia, Castilla y León, Aragón | Short term (≤2 years) |

| Niche EV gigafactory demand | +0.3% | Aragón, Valencia | Medium term (2-4 years) |

| Catalan self-healing polymer R&D | +0.2% | Catalonia | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Renovation-Driven Demand Surge in Spain's Aged Housing Stock

Spain completed 1.85 million home renovations in 2025, and licenses for deep rehabilitation climbed 12.9% year on year[1]ConstruiBLE, “Balance de la rehabilitación energética en 2025,” construible.es. Roughly 80% of dwellings carry poor energy ratings, so fiscal incentives covering up to 100% of retrofit costs are channeling steady volumes toward window-perimeter, expansion-joint, and airtightness sealants. Minimum Energy Performance Standards under the PNRE 2026 require non-residential buildings to outperform the worst 16% of 2020 stock by 2030, creating a predictable multi-year order pipeline. Madrid, Barcelona, and Seville concentrate most subsidy beneficiaries, while a 700,000-worker shortfall in Spanish construction is steering contractors toward factory-applied sealant systems compatible with prefabricated façades. The resulting uplift cements a strong base trajectory for the Spain Sealants market.

Automotive Lightweighting Mandates Boosting Structural Sealant Usage

European End-of-Life Vehicle rules push automakers toward mixed-material bodies that depend on structural adhesives for weight savings. Spain’s EV transition is centered on the EUR 4.1 billion CATL-Stellantis battery plant in Aragón, due to supply 50 GWh annually by end-2026[2]Euronews, “Stellantis and CATL break ground in Spain,” euronews.com. The project elevates local demand for flame-retardant polyurethane and silicone chemistries meeting UL 94 V-0 and IEC 62368-1. High-elongation sealants that debond on command to enable recycling are emerging as preferred solutions, positioning technology leaders to capture premium margins in the Spain Sealants market.

EU Fit-for-55 Energy-Efficiency Rules Raising Demand for Low-VOC Sealants

The revised Energy Performance of Buildings Directive mandates zero-emission new buildings by 2030 and tightens solar-roof obligations starting 2027. Forthcoming EU limits on adhesive VOCs, effective mid-2026, require EPD-style transparency, accelerating Spain’s pivot to waterborne or hybrid systems. Suppliers that certify to Finnish M1 or French A+ standards gain preferential access to public bids under CPR 2024. Sika’s Purform and Wacker’s ELASTOSIL eco 7770 P already meet these thresholds, underscoring the regulatory-driven upgrade cycle fueling the Spain Sealants market.

Rapid Growth of On-Shore Wind-Blade Refurbishments

Aging turbines in Galicia and Castilla y León need leading-edge repair and composite-bond reinforcement. Specialized polyurethane and epoxy sealants with UV and salt-fog resistance shorten turbine downtime and command margin premiums. Utilities’ 100% renewable-energy pledges, including the new battery plant’s sourcing strategy, sustain this maintenance niche, strengthening regional pockets of demand inside the Spain Sealants market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile isocyanate prices | -0.7% | EU-wide, import-dependent | Short term (≤2 years) |

| Mechanical-fastener substitution in low-rise construction | -0.3% | Nationwide residential | Medium term (2-4 years) |

| Strict REACH limits on tin-catalyzed silicones | -0.4% | EU-wide | Short term (≤2 years) |

| Limited domestic feedstock base | -0.5% | National | Long term (≥4 years) |

| Source: Mordor Intelligence | |||

Volatile Isocyanate Prices Squeezing Polyurethane Sealant Margins

European ethylene costs average USD 800 per tons, double United States and quadruple Middle-East benchmarks, exposing up to 40% of regional capacity to closure risk. Spain imports all MDI (methylene diphenyl diisocyanate) and TDI (toluene diisocyanate), so 20-30% quarterly price swings erode margins for small formulators on 30-day terms. Absent domestic crackers, raw-material volatility remains a structural drag on polyurethane sales inside the Spain Sealants market.

Rising Substitution by Mechanical Fasteners in Low-Rise Construction

Industrialized building methods now cover about 2% of Spanish output and are trending toward 10% by 2030. Dry-joint façade panels use clips and brackets, trimming interior acrylic or polyurethane sealant volumes. Although high-performance hybrids still seal interfaces, commodity demand in single-family housing softens, moderating overall growth for the Spain Sealants market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Resin Type: Silicone Dominates, Polyurethane Accelerates on EV and Wind Demand

Silicone sealants held 38.15% of Spain Sealants market share in 2025, anchored by façade and sanitary applications that benefit from UV stability and mildew resistance. Wacker’s ELASTOSIL eco 7770 P adds biomass-offset content and EC1 plus certification, illustrating the premium end of this category. Polyurethane volumes are smaller today yet forecast to climb at 6.96% CAGR, propelled by EV battery sealing at the new Aragón gigafactory and high-elongation joints in wind-blade repairs. Sika’s Purform series, already REACH-compliant and low-monomer, positions the firm to capture this uplift.

Epoxy chemistries remain niche, serving aerospace and industrial flooring, while acrylics face price pressure and partial substitution from mechanical fasteners. Hybrid silyl-modified polymers (SMP) and emerging bio-based blends, such as Bostik’s 46% bio-carbon formulation, are carving out opportunities in public projects that weigh environmental classes under CPR 2024. Overall, commodity silicones and acrylics will track or trail the Spain Sealants market, whereas specialty polyurethane and certified hybrid systems are primed for above-trend gains.

By End-User Industry: Building and Construction Leads, Healthcare Surges on Regulatory Tailwinds

Building and construction consumed 46.05% of Spain Sealants market size in 2025, underpinned by 1.85 million home renovations and energy-retrofit subsidies covering up to 100% of eligible costs. Sika España’s CIMA+ applicator network and its “Revolución Industrializada” initiative are expanding technical-service ecosystems to lock in share across façades, roofs, and prefabricated panels. Automotive ranks second but carries outsized innovation weight as battery, thermal, and acoustic requirements intensify.

Healthcare is the breakout segment, projected to grow at 7.12% CAGR through 2031. August 2026 PFAS limits, less than or equal to 25 ppb individual, less than or equal to 250 ppb total, are spurring wholesale reformulation of sterile-barrier and hemostatic sealants. A single Madrid hospital tender worth USD 931,000 in 2025 underscores the purchasing power of Spain’s public health sector. Aerospace and marine activities supply a niche but stable epoxy and polysulfide demand, rounding out a profile in which regulatory stringency and high-value engineering uses steer growth into specialized corners of the Spain Sealants market.

Geography Analysis

Spain Sealants market demand clusters around Madrid, Catalonia, and Andalusia, which together generate more than half of the national consumption. Madrid alone accounted for 27.7% of tax-deduction beneficiaries for energy upgrades in 2025, reflecting its dense, aging housing stock and proactive municipal incentives. Catalonia combines sizeable retrofit needs with Spain’s largest auto plant at Martorell and active participation in EU polymer research and development, reinforcing dual residential and industrial pull.

Aragón has vaulted into the spotlight since the CATL-Stellantis ground-breaking, with 4,000 anticipated jobs and an ecosystem of component suppliers rallying around the 50 GWh battery plant. Galicia and Castilla y León contribute episodic spikes tied to wind-blade maintenance, whereas Valencia’s yacht-building and Balearic tourism infrastructure sustain marine sealant niches. Smaller autonomous communities such as La Rioja and Murcia register high retrofit ratios but low absolute volumes, making localized distributors critical for market coverage.

Regional regulatory heterogeneity compounds the challenge: while CPR 2024 and EPBD targets apply nationwide, autonomous communities retain latitude on subsidy design and building-code enforcement. Suppliers succeeding in the Spain sealants market deploy centralized EPD and Digital Product Passport (DPP) repositories yet tailor marketing, logistics, and technical services to the unique labor pools, climate zones, and procurement cultures of each region.

Competitive Landscape

The Spain Sealants market is moderately consolidated. Whitespace growth is gravitating to bio-based, PFAS-free, and battery-grade chemistries. Wacker’s biomass-offset silicones and Bostik’s EN 16640-certified hybrids qualify for top-tier environmental classes under CPR eco-modulated fees, while Dow and Henkel are scaling thermally conductive gap fillers for battery modules. Industry consolidation is likely as smaller players struggle to amortize testing, DPP creation, and REACH compliance across thin product lines, reinforcing a moderately concentrated Spain Sealants market.

Spain Sealants Industry Leaders

Dow

Henkel AG & Co. KGaA

MAPEI S.p.A.

Sika AG

Arkema

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: The FEICA 2025 European Adhesive and Sealant Conference and Expo was announced to be held from 10 to 12 September 2025 at the Kursaal Congress Centre in San Sebastian, Spain. This city will host the adhesive and sealant community for an opportunity to network and collaborate.

- February 2025: Master Builders Solutions announced its product line expansion for tail sealants for TBM (tunnel boring machines) operations for Spain and other countries to serve the growing population and urbanization.

Spain Sealants Market Report Scope

Sealants, flexible and paste-like, fill gaps, joints, and cracks between surfaces, effectively blocking air, water, moisture, and dust. Widely utilized in aerospace, construction, automotive, and healthcare, sealants protect joints. Unlike adhesives, sealants focus on providing water resistance and sealing, rather than structural bonding.

The Spain Sealants market report is segmented by resin and end-user industry. By resin, the market is segmented into acrylic, epoxy, polyurethane, silicone, and other resins. By end-user industry, the market is segmented into aerospace, automotive, building and construction, healthcare, and other end-user industries. The market size and forecasts are provided in terms of value (USD).

By Resin Type

| Acrylic |

| Epoxy |

| Polyurethane |

| Silicone |

| Other Resins |

By End-user Industry

| Aerospace |

| Automotive |

| Building and Construction |

| Healthcare |

| Other End-user Industries |

| By Resin Type | Acrylic |

| Epoxy | |

| Polyurethane | |

| Silicone | |

| Other Resins | |

| By End-user Industry | Aerospace |

| Automotive | |

| Building and Construction | |

| Healthcare | |

| Other End-user Industries |

Market Definition

- End-user Industry - Building & Construction, Automotive, Aerospace, Healthcare, and Others are the end-user industries considered under the sealants market.

- Product - All sealant products are considered in the market studied

- Resin - Under the scope of the study, resins like Polyurethane, Epoxy, Acrylic, Silicone, and Others are considered

- Technology - For the purpose of this study, One component and Two component sealant technologies are taken into consideration.

| Keyword | Definition |

|---|---|

| Hot-melt Adhesive | Hot melt adhesives are generally 100% solid formulations, based on thermoplastic polymers. They are solid at room temperature and are activated upon heating above their softening point, at which stage they are liquid, and hence, can be processed. |

| Reactive Adhesive | A reactive adhesive is made up of monomers that react in the adhesive curing process and do not evaporate from the film during use. Instead, these volatile components become chemically incorporated into the adhesive. |

| Solvent-borne Adhesive | Solvent-borne adhesives are mixtures of solvents and thermoplastic, or slightly cross-linked polymers, such as polychloroprene, polyurethane, acrylic, silicone, and natural and synthetic rubbers (elastomers). |

| Water-borne Adhesive | Water-borne adhesives use water as a carrier or diluting medium to disperse a resin. They are set by allowing the water to evaporate or be absorbed by the substrate. These adhesives are compounded with water as a diluent, rather than a volatile organic solvent. |

| UV Cured Adhesive | UV curing adhesives induce curing and create a permanent bond without heating by using ultraviolet (UV) light or other radiation sources. An aggregation of monomers and oligomers is cured or polymerized by ultraviolet (UV) or visible light in a UV adhesive. Because UV is a radiating energy source, UV adhesives are often referred to as radiation curing or rad-cure adhesives. |

| Heat-resistant Adhesive | Heat-resistant Adhesives refer to those that do not break down under high temperatures. One aspect of a complicated system of circumstances is the adhesive's capacity to withstand disintegration brought on by high temperatures. As the temperature rises, adhesives may liquefy. They can withstand stresses resulting from differing coefficients of expansion and contraction, which might be an additional advantage. |

| Reshoring | Reshoring is the practice of moving commodity production and manufacturing back to the nation where the business was founded. Onshoring, inshoring, and back shoring are further terms used. Offshoring, the practice of producing items abroad to lower labor and manufacturing costs, is the opposite of this. |

| Oleochemicals | Oleochemicals are compounds produced from biological oils or fats. They resemble petrochemicals, which are substances made from petroleum. The oleochemical business is built on the hydrolysis of oils or fats. |

| Nonporous Materials | Nonporous materials are substances that do not permit the passage of liquid or air. Nonporous materials are those that are not porous, such as glass, plastic, metal, and varnished wood. Since no air can get through, less airflow is required to raise these materials, negating the requirement for high airflow. |

| EU-Vietnam Free Trade Agreement | A trade agreement and an investment protection agreement were concluded between the European Union and Vietnam on June 30, 2019. |

| VOC content | Compounds with limited solubility in water and high vapor pressure are known as Volatile Organic Compounds (VOCs). Many VOCs are human-made chemicals that are used and produced in the manufacture of paints, pharmaceuticals, and refrigerants. |

| Emulsion Polymerization | Emulsion polymerization is a method of producing polymers or connected groups of smaller chemical chains known as monomers, in a water solution. The method is often used to make water-based paints, adhesives, and varnishes, in which the water stays with the polymer and is marketed as a liquid product. |

| 2025 National Packaging Targets | In 2018, the Australian Environment Ministry set the following 2025 National Packaging Targets: 100% of the packaging must be reusable, recyclable, or compostable by 2025, 70% of plastic packaging must be recycled or composted by 2025, 50% of average recycled content must be included in packaging by 2025, and problematic and unnecessary single-use plastic packaging must be phased out by 2025. |

| Russian Government’s Import Substitution Policy | The Western sanctions suspended the distribution of several high-tech items to Russia, including those required by the raw material export sectors and the military-industrial complex. In response, the government launched an "import substitution" scheme, appointing a special commission to oversee its implementation in early 2015. |

| Paper Substrate | Paper substrates are paper sheets, reels, or boards with a base weight of up to 400 g/m2 that has not been converted, printed or otherwise altered. |

| Insulation Material | A material that inhibits or blocks heat, sound, or electrical transmission is known as Insulation Material. The variety of insulation materials includes thick fibers like fiberglass, rock and slag wool, cellulose, and natural fibers as well as stiff foam boards and sleek foils. |

| Thermal Shock | A temperature change known as thermal shock generates stress in a material. It commonly results in material breakdown and is especially prevalent in brittle materials like ceramics. When there is a quick temperature change, either from hot to cold or vice versa, this process occurs abruptly. It occurs more frequently in materials with poor heat conductivity and insufficient structural integrity. |

Research Methodology

Mordor Intelligence follows a four-step methodology in all our reports.

- Step-1: Identify Key Variables: The quantifiable key variables (industry and extraneous) pertaining to the specific product segment and country are selected from a group of relevant variables & factors based on desk research & literature review; along with primary expert inputs. These variables are further confirmed through regression modeling (wherever required).

- Step-2: Build a Market Model: In order to build a robust forecasting methodology, the variables and factors identified in Step-1 are tested against available historical market numbers. Through an iterative process, the variables required for market forecast are set and the model is built on the basis of these variables.

- Step-3: Validate and Finalize: In this important step, all market numbers, variables and analyst calls are validated through an extensive network of primary research experts from the market studied. The respondents are selected across levels and functions to generate a holistic picture of the market studied.

- Step-4: Research Outputs: Syndicated Reports, Custom Consulting Assignments, Databases & Subscription Platforms