Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

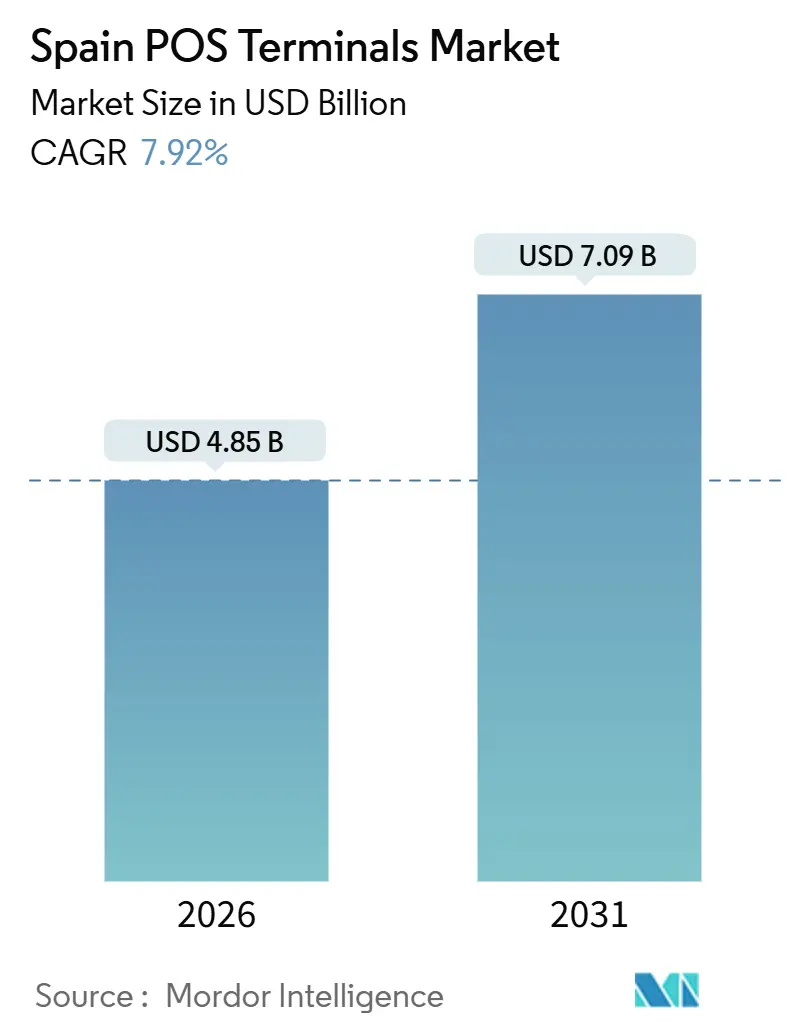

| Market Size (2026) | USD 4.85 Billion |

| Market Size (2031) | USD 7.09 Billion |

| Growth Rate (2026 - 2031) | 7.92% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain POS Terminals Market Analysis by Mordor Intelligence

The Spain POS terminals market size stood at USD 4.85 billion in 2026 and is projected to reach USD 7.09 billion by 2031, reflecting a 7.92% CAGR over the period. The trajectory is shaped by stricter cash-use limits, vibrant tourism flows, and near-universal contactless readiness among issuers and merchants. Regulatory mandates obligate even micro-businesses to digitize takings, while Bizum wallet integration and SoftPOS solutions are lowering entry costs for small hospitality and service operators. High smartphone penetration is nurturing mobile-originated tap-to-pay habits, and terminal refresh cycles are accelerating as retailers seek cloud analytics and omnichannel orchestration to compete with e-commerce giants. Meanwhile, interchange-fee caps are compressing margins for acquirers, nudging the ecosystem toward software-led recurring-revenue models rather than hardware subsidies.

Key Report Takeaways

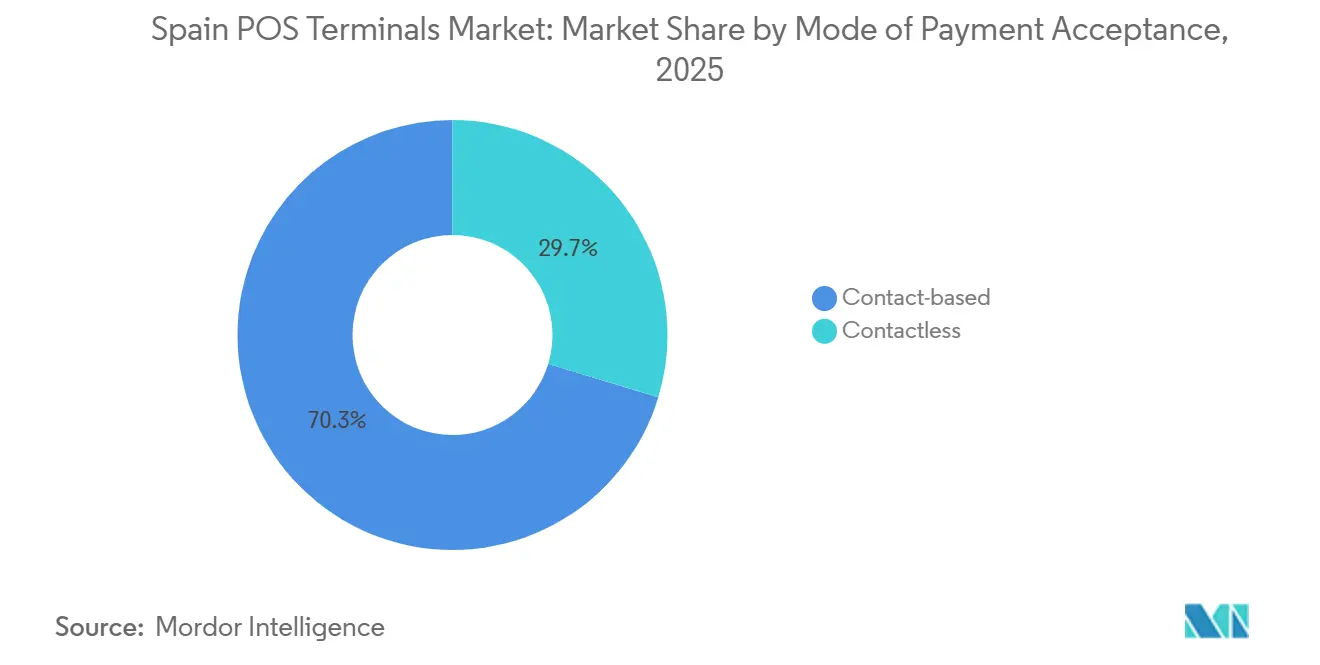

- By mode of payment acceptance, contactless methods captured 70.32% of transaction value in 2025; contactless payments are advancing at an 8.13% CAGR through 2031.

- By POS type, mobile and portable units held 46.58% of the Spain POS terminals market share in 2025, while mobile solutions are forecast to expand at an 8.67% CAGR between 2026-2031.

- By component, hardware commanded 62.14% of the Spain POS terminals market size in 2025, yet software is scaling at an 8.78% CAGR through 2031.

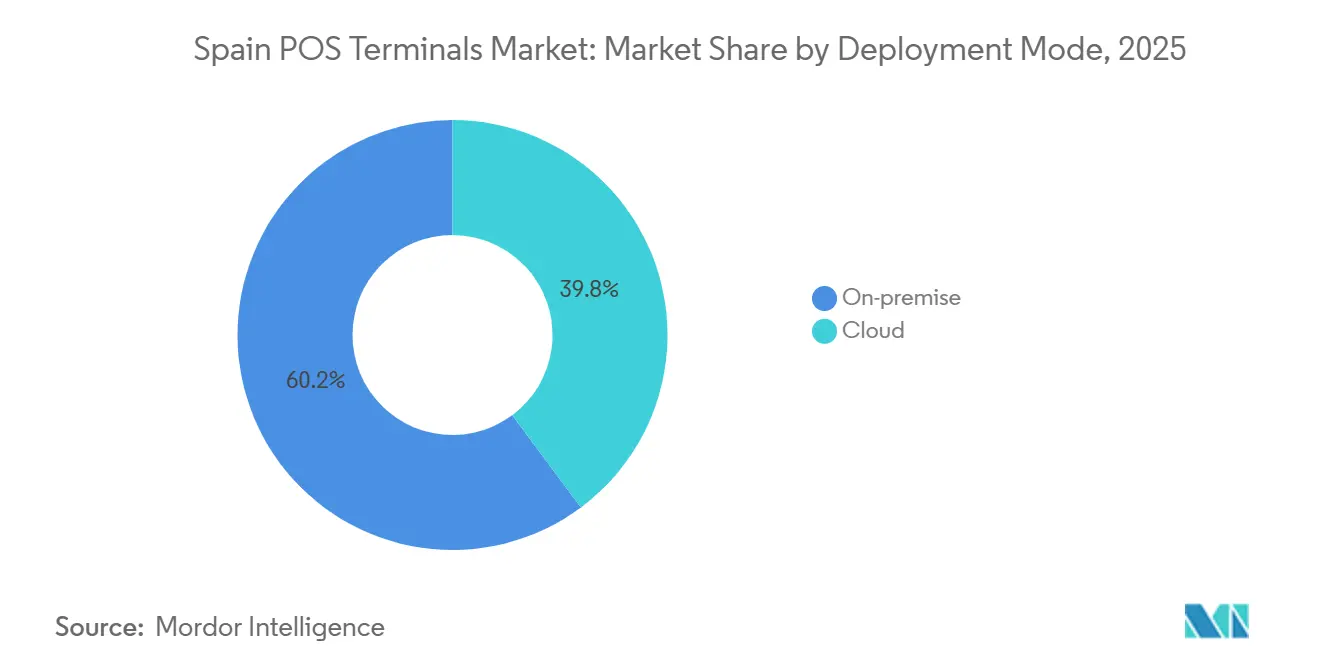

- By deployment mode, cloud platforms accounted for 39.81% revenue in 2025 and are growing at an 8.48% CAGR to 2031.

- By end-user industry, retail led with 35.28% revenue share in 2025; healthcare is the fastest-growing vertical, registering an 8.92% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

Spain POS Terminals Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in Contactless Card Issuance Driven by Spanish Banks | +2.1% | National, with concentration in Madrid, Barcelona, Valencia, Seville | Short term (≤ 2 years) |

| Government Cash-Transaction Limits and Fiscal Digitalization Law | +1.8% | National, particularly affecting micro-merchants in Andalusia, Castile and León, Galicia | Medium term (2-4 years) |

| Tourist Spending Rebound Boosting POS Volumes in Coastal Regions | +1.5% | Coastal tourism zones: Balearic Islands, Canary Islands, Costa del Sol, Costa Brava | Short term (≤ 2 years) |

| SME Adoption of Integrated Cloud POS for Omnichannel Commerce | +1.2% | National, early gains in urban centers Madrid, Barcelona, Bilbao | Medium term (2-4 years) |

| Instant Payments Integration via Bizum and SoftPOS Enablement | +1.0% | National, with higher penetration in digitally mature regions Catalonia, Madrid, Basque Country | Medium term (2-4 years) |

| Digital Euro Readiness Accelerating Early Terminal Upgrades | +0.6% | National, pilot programs concentrated in Madrid and Barcelona | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in Contactless Card Issuance Driven by Spanish Banks

Spanish issuers are saturating the market with NFC-enabled plastics and wallets, evidenced by CaixaBank’s 100.7 million mobile and contactless transactions in June 2025, up 34.4% year-on-year.[1]CaixaBank, “CaixaBank Processes 100.7 Million Mobile and Contactless Transactions in June 2025,” CAIXABANK.COM Banco de España counted 5.562 billion card operations in the first half of 2024, 93.7% of which were contactless. Across the euro area, 92% of terminals accepted contactless by late 2024. Mastercard research shows 50.4% of Spanish tap-to-pay transactions now originate from phones rather than cards. Acquirers are therefore bundling NFC readers with loyalty and analytics apps, positioning the Spain POS terminals market as a springboard for data-driven engagement rather than a simple payments endpoint.

Government Cash-Transaction Limits and Fiscal Digitalization Law

Law 11/2021 capped cash dealings at EUR 1,000, while Royal Decree 253/2025 imposes monthly card-payment reporting from January 2026.[2]Boletín Oficial del Estado, “Royal Decree 253/2025 on Fiscal Reporting Requirements,” BOE.ES Merchants in hospitality, automotive repair, and construction materials can no longer rely on opaque cash records without risking penalties. Upcoming B2B e-invoicing mandates under Law 18/2022 and EU VAT-in-the-Digital-Age reforms further propagate electronic rails. Consequently, SMEs - about 3.4 million firms - are fast-tracking Spain POS terminals market deployments to ensure compliance, spurring demand for cloud suites that auto-generate fiscal receipts and transmit them to tax platforms in real time.

Tourist Spending Rebound Boosting POS Volumes in Coastal Regions

International visitors spent EUR 76 billion between January-July 2025, 7.2% more than a year earlier. The Balearic Islands installed 1,652 validators and 611 dual EMV desks in partnership with Redsys and Banco Santander. Barcelona’s TMB fitted 1,070 buses with EMV readers, exceeding 500,000 transactions in early rollout. Such infrastructure slashes payment friction for tourists and fuels seasonal transaction spikes, reinforcing the Spain POS terminals market’s reliance on travel and leisure corridors.

SME Adoption of Integrated Cloud POS for Omnichannel Commerce

Spain ranks 11th on the EU Digital Economy and Society Index, yet only 60% of SMEs hold basic digital skills. The Digital Kit subsidy, worth EUR 2,000-12,000 per applicant, is nudging merchants toward cloud-based suites. BBVA’s Virtual POS, free for a year under the voucher, supports Bizum, Apple Pay, and Google Pay, lowering the barrier for micro-merchants. Stripe noted 4.2 million active terminals in early 2023, up 9.7% on-year, with contactless volumes jumping 18% in H1 2024. Cloud dashboards also optimize inventory across online and brick-and-mortar channels, critical during tourist peaks, anchoring future growth of the Spain POS terminals market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Interchange-Fee Caps Squeezing Acquirer Margins and Subsidies | -1.4% | National, with heightened pressure on acquirers serving low-ticket merchants in hospitality and retail | Medium term (2-4 years) |

| Fragmented SME Digital Literacy Hindering Advanced POS Uptake | -1.0% | National, concentrated in rural areas and among older merchant demographics in Castile-La Mancha, Extremadura, Aragon | Medium term (2-4 years) |

| GDPR-Related Compliance Costs for Cloud POS Vendors | -0.5% | National, affecting cloud-based SaaS providers and multi-country acquirers | Short term (≤ 2 years) |

| Dependence on Imported Chipsets Amid Geopolitical Supply Risks | -0.4% | National, with exposure to Asia-Pacific semiconductor supply chains | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Interchange-Fee Caps Squeezing Acquirer Margins and Subsidies

EU Regulation 2015/751 cut debit and credit interchange to 0.2% and 0.3% respectively, enacted locally via Royal Decree 150/2020.[3]European Commission, “EU Regulation 2015/751 on Interchange Fees,” EC.EUROPA.EU The reduced economics have curtailed free-terminal campaigns, pushing acquisition costs onto merchants. Low-ticket venues such as quick-service restaurants struggle to absorb higher rental fees, slowing Spain POS terminals market penetration in some rural pockets. Smaller acquirers lacking scale are withdrawing from unprofitable niches or consolidating, although SoftPOS is abating the hardware burden by enabling bring-your-own-device acceptance.

Fragmented SME Digital Literacy Hindering Advanced POS Uptake

Despite financial incentives, older proprietors in Castile-La Mancha, Extremadura, and Aragon often avoid cloud dashboards, fearing hidden costs and complexity. Limited local tech support aggravates hesitation, leaving merchants on legacy keypad devices that offer only payment capture. Vendors are responding with simplified user interfaces and on-site training, yet adoption of analytics, loyalty, and real-time inventory tools remains patchy, tempering near-term gains for the Spain POS terminals market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Mode of Payment Acceptance: Contactless Expands as the Default Choice

Contactless channels represented 70.32% of value in 2025, while they are growing at an 8.13% CAGR, gradually displacing chip-and-PIN. Contact-based terminals still serve high-value or offline-risk environments, but Banco de España indicates 93.7% of card operations were tap-to-pay by late 2024, underscoring consumer preference. The Spain POS terminals market size for contactless flows is widening as PSD2 low-value exemptions maintain frictionless taps and Bizum wallet integration offers domestic instant-payment alternatives.

Bizum’s addition to BBVA’s POS fleet in March 2025 merges wallet transfers with card workflows, cutting costs for small tickets. Ingenico and BBVA SoftPOS apps convert Android phones into terminals, boosting penetration in gig-economy services. The Spain POS terminals industry therefore sees dual-interface devices becoming minimum specs, ensuring continued but shrinking relevance for contact-based acceptance.

By POS Type: Mobility Redefines Checkout

Fixed lanes retained 53.42% share in 2025, yet portable systems rose 8.67% annually as eateries adopted tableside payments and festivals favored pop-up stalls. Barcelona’s TMB bus network and Balearic transport validators exemplify how transit deployments lean on mobile readers. Madrid Metro’s EUR 5.9 million upgrade across 302 stations further illustrates the capital intensity of fixed infrastructure.

SoftPOS is blurring lines between hardware categories. Ingenico estimated 350,000 Android-based devices live in Spain by January 2023, forecasting smartphones could handle 25% of acceptance within a few years. BBVA’s NFC app needs only Android 11, enabling same-day onboarding. High-volume grocery chains still rely on tethered scanners and cash drawers, but flexible mobility is redefining the customer journey across the Spain POS terminals market.

By Component: Software Leads Value Creation

Hardware comprised 62.14% revenue in 2025, yet software is expanding 8.78% annually as merchants demand real-time dashboards and omnichannel orchestration. Redsys processed 19.7 billion transactions worth EUR 505 billion in 2024, highlighting the service layer’s scale. Worldline’s exit from terminal manufacturing in 2022 and Adyen’s Android launches in 2025 both illustrate a pivot toward software ecosystems.

Digital Kit vouchers accelerate adoption, with BBVA offering a fee-free year for its virtual suite. PCI DSS and PSD2 rules necessitate continual firmware patches, locking merchants into subscription contracts and enlarging the Spain POS terminals market size for SaaS.

By Deployment Mode: Cloud Gains Momentum

On-premise solutions still hold 60.19% share, but cloud platforms are growing 8.48% yearly as SMEs appreciate subscription pricing. GDPR responsibilities cost vendors up to EUR 1.3 million, yet multi-tenant architecture amortizes these outlays. Stripe observed 18% growth in contactless usage in H1 2024, tied to the rise of cloud-connected models.

CaixaBank and BBVA’s 2025 Request-to-Pay trial via Iberpay proved cloud orchestration can support real-time invoices outside card rails. As 5G and satellite connectivity mature, offline justifications for local databases will erode, accelerating cloud penetration in the Spain POS terminals market.

By End-User Industry: Healthcare Surges Ahead

Retail controlled 35.28% share in 2025, but healthcare is pacing at an 8.92% CAGR thanks to Redsys Salud integrations with insurers like Adeslas SegurCaixa and Sanitas. Secure e-prescription terminals supplied by the National Mint also propel uptake. Hospitality thrives on revived tourism spend, hitting EUR 76 billion in the first seven months of 2025. Transportation investments, such as Madrid Metro’s rollout, extend acceptance to turnstiles.

Automotive repair, professional services, and government counters are adopting devices to comply with Law 11/2021 limits. The forthcoming national transport pass will widen scope further, reinforcing sector diversity within the Spain POS terminals market.

Geography Analysis

Spain’s POS penetration varies sharply by region. Coastal hotspots Balearic Islands, Canary Islands, Costa del Sol, and Costa Brava record seasonal peaks tied to international arrivals that rose 7.2% year-on-year in mid-2025. Transport upgrades, such as 1,652 validators in the Balearics and 1,070 EMV-enabled buses in Barcelona, have normalized tap-to-pay for visitors. Madrid Metro’s EUR 5.9 million project anchors acceptance in the capital.

Inland rural zones lag due to limited digital literacy among SMEs, although Digital Kit grants ease financial hurdles. Catalonia, Madrid, and the Basque Country lead Bizum and SoftPOS usage, reflecting higher smartphone adoption. CaixaBank’s contactless volumes skew toward its base in Catalonia and the Balearics, echoing tourism patterns. Redsys’ nationwide reach across 1.5 million merchants bridges gaps, while the planned 2026 national transport pass will harmonize acceptance across provinces, narrowing disparities in the Spain POS terminals market.

Coastal tourism zones, the Balearic and Canary Islands, Costa del Sol, and Costa Brava, generate seasonal transaction spikes, while Madrid, Barcelona, Valencia, and Seville anchor year-round volumes. Municipal upgrades such as 1,652 transit validators in the Balearics, 1,070 EMV-enabled buses in Barcelona, and a EUR 5.9 million contactless rollout across Madrid Metro underscore public investment in cashless mobility. Rural provinces lag because SME digital skills remain patchy, although Digital Kit grants of up to EUR 12,000 are nudging adoption. Bizum’s 28.8 million users and CaixaBank’s 100.7 million contactless transactions in June 2025 highlight higher wallet and SoftPOS penetration in Catalonia, Madrid, and the Basque Country. A planned 2026 national transport pass is expected to harmonize acceptance, narrowing the regional divide in the Spain POS terminals market.

Competitive Landscape

Worldline and Ingenico jointly held roughly 37% of global terminal shipments in 2025. Worldline’s 2022 divestiture of the Ingenico hardware arm to Apollo, plus 2025 sales of MeTS and PaymentIQ, signal a strategic shift toward acquiring and value-added services. Redsys dominates domestic processing, handling EUR 505 billion in 2024 and operating Spain’s PSD2 hub for 80 banks.

Adyen’s S1E4 Pro and S1F4 Pro terminals, launched in November 2025, emphasize Android ecosystems with app marketplaces. SoftPOS is emerging as white space; Ingenico forecasts smartphones could capture 25% of acceptance in a few years, and BBVA’s Android-based solution underscores bank-led momentum. SumUp, Square, and MONEI court micro-merchants with transparent pricing, unsettling incumbents reliant on bundled contracts.

NCR leverages Verifone, Equinox, and Ingenico readers to anchor its restaurant suite. PAX Technology has shipped more than 80 million devices globally and promotes the MAXSTORE management layer, deepening its foothold in the Spain POS terminals market. Margin compression from interchange caps is steering acquirers toward software subscriptions rather than hardware subsidies, reshaping competitive playbooks.

Spain POS Terminals Industry Leaders

NCR Corporation

Worldline SA

PayPal Holdings, Inc. (Zettle)

VeriFone, Inc.

NEC Ibérica, S.L.

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- January 2026: Adyen began a Europe-wide rollout of its S1E4 Pro and S1F4 Pro Android terminals, enabling third-party app downloads on-device.

- December 2025: Worldline divests PaymentIQ to Nuvei for EUR 160 million.

- November 2025: Adyen globally launches S1E4 Pro and S1F4 Pro terminals with third-party app support.

- October 2025: BBVA introduces BBVA Pay with Visa, enabling NFC payments on iOS devices.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Spanish point-of-sale (POS) terminals market as the annual value generated by fixed countertop workstations, self-checkout kiosks, tablets, and handheld card readers that process in-store card or wallet payments and ship new into Spain. Both bundled payment software and essential peripherals that ship with the terminal are counted, while recurring acquiring fees are not.

Scope Exclusions: ATM kiosks, smartphone-only SoftPOS apps that need no external reader, and purely e-commerce gateways sit outside our lens.

Segmentation Overview

- By Mode of Payment Acceptance

- Contact-based

- Contactless

- By POS Type

- Fixed Point-of-Sale Systems

- Mobile / Portable Point-of-Sale Systems

- By Component

- Hardware

- Software

- Services

- By Deployment Mode

- Cloud-based

- On-Premise

- By End-User Industry

- Retail

- Hospitality

- Healthcare

- Transportation and Logistics

- Other End-User Industries

Detailed Research Methodology and Data Validation

Primary Research

Multiple touchpoints with terminal makers, acquirers, fintech bodies, and SME merchants in Madrid, Barcelona, Andalusia, and Valencia let us cross-check shipment tallies, replacement cycles, and subsidy pass-through. These conversations filled gray areas left by desk work and anchored assumption ranges before model lock-in.

Desk Research

Our analysts first mapped the demand pool using open datasets, Banco de Espana's card-payment dashboards, European Central Bank Blue Book tables on active terminals, the National Institute of Statistics retail turnover index, and customs codes 847050/847090 that trace hardware inflows. Trade releases from the Spanish Confederation of Small and Medium Enterprises, press coverage in Dow Jones Factiva, and company filings collated via D&B Hoovers supplied channel margins and average selling prices.

Sector associations such as ANFAC (retail tech), AECE (hospitality), and policy notes from the Ministry of Economic Affairs clarified regulatory triggers and subsidy uptake. The sources above illustrate our breadth; many additional references supported data validation and narrative framing.

Market-Sizing & Forecasting

A top-down build starts from the ECB-reported installed base, adjusts for active-inactive churn, and multiplies net additions by blended hardware-software ASPs we derived from import pricing and supplier call-outs. Selective bottom-up roll-ups on three leading vendors confirmed variance under ±6 percent. Key drivers injected into our multivariate forecast include: (1) contactless share of card payments, (2) retail sales volume, (3) SME digital-kit subsidy disbursements, (4) average terminal life, and (5) card spend per capita. An ARIMA overlay captures seasonality from tourism peaks, and scenario logic tests currency or subsidy shocks. Where bottom-up gaps emerged, micro-merchant adoption, for instance, we interpolated using regional cash-to-card shift ratios endorsed by interviewees.

Data Validation & Update Cycle

Model outputs pass a two-layer analyst review, variance checks against Statista terminal counts and payment network volume, and peer sign-off. We refresh every twelve months, triggering interim revisions for material events such as subsidy rule changes or chipset shortages. A final analyst sweep occurs just before report release to guarantee clients receive the freshest baseline.

Why Mordor's Spain POS Terminals Baseline Remain the Trusted Baseline

Published estimates often diverge; different firms bundle services, convert currencies at varied dates, or project from aging datasets.

Key gap drivers include: some tally acquirer fee revenue, others strip software, many use static exchange rates, and several refresh on three-year cycles, whereas our annual cadence and dual-path validation restrain drift.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 1.47 B (2025) | Mordor Intelligence | |

| USD 3.25 B (2024) | Global Consultancy A | Adds acquiring & service revenue, vendor roll-ups, infrequent updates |

| USD 1.37 B (2024) | Industry Analyst B | Hardware only; relies on installed-base x ASP, limited primary checks |

| USD 0.50 B (2024) | Regional Consultancy C | Focus on retail checkouts; excludes mPOS, small sample scope |

In short, our disciplined scope selection, yearly refresh, and blend of open statistics with on-ground voices give decision-makers a balanced, reproducible baseline they can trust.

Key Questions Answered in the Report

What is the forecast value of the Spain POS terminals market by 2031?

The market is expected to reach USD 7.09 billion, expanding at a 7.92% CAGR.

Which payment method is growing fastest at Spanish points of sale?

Contactless transactions, covering 70.32% of value in 2025, are advancing at an 8.13% CAGR through 2031.

Why are cloud POS platforms gaining popularity in Spain?

Cloud models offer subscription pricing, remote updates, and real-time analytics, aligning with Digital Kit subsidies that cut upfront costs for SMEs.

Which end-user sector shows the highest growth potential?

Healthcare is projected to grow at an 8.92% CAGR thanks to insurer integrations and e-prescription workflows.

How are interchange-fee caps affecting acquirers?

Caps at 0.2% for debit and 0.3% for credit are compressing margins, prompting a shift away from hardware subsidies toward software-driven revenue.

What role does Bizum play at the physical point of sale?

Bizum wallet acceptance on BBVA and other terminals enables instant payments, offering merchants a low-cost domestic alternative to card networks.

Page last updated on: