France Data Center Physical Security Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

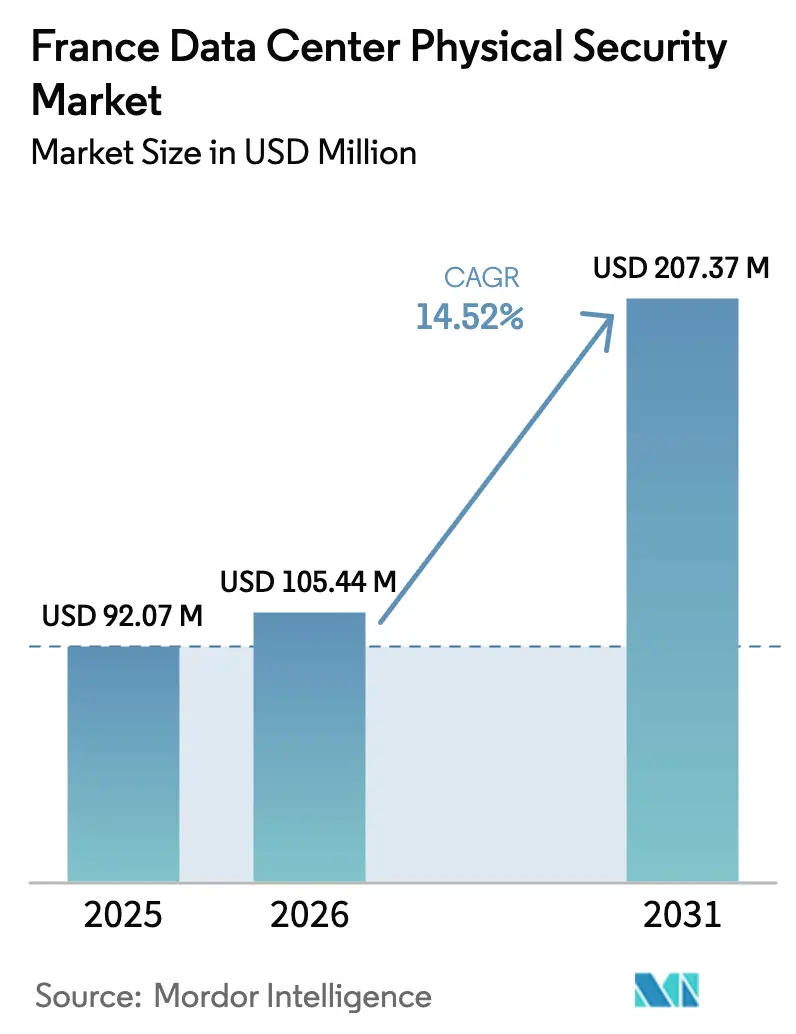

| Base Year Market Size (2025) | USD 92.07 Million |

| Market Size (2026) | USD 105.44 Million |

| Market Size (2031) | USD 207.37 Million |

| Growth Rate (2026 - 2031) | 14.52% CAGR |

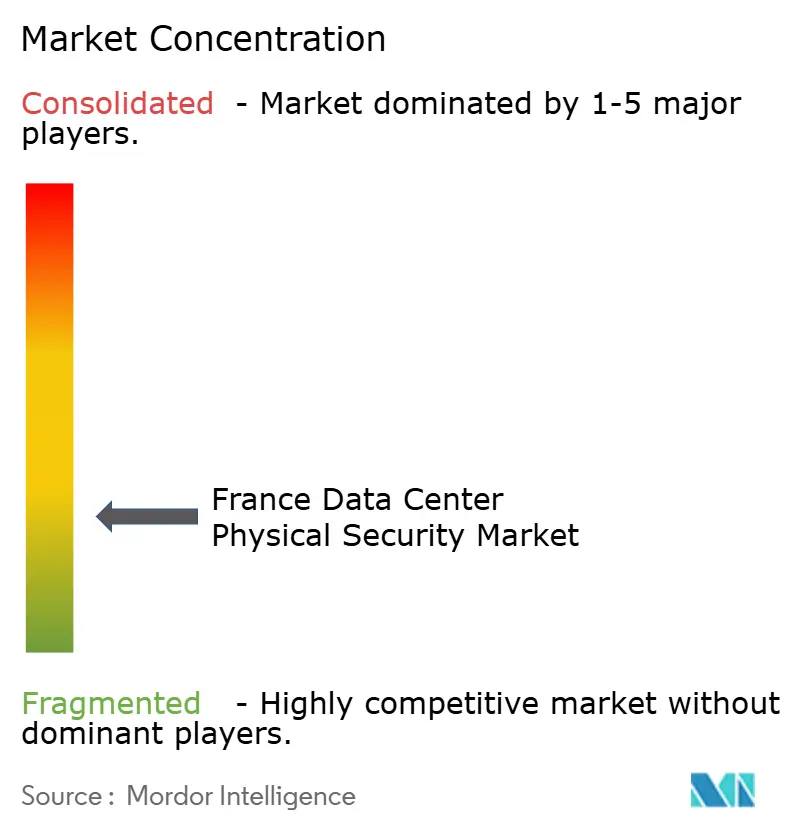

| Market Concentration | Low |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

France Data Center Physical Security Market Analysis by Mordor Intelligence

France data center physical security market size in 2026 is estimated at USD 105.44 million, growing from 2025 value of USD 92.07 million with 2031 projections showing USD 207.37 million, growing at 14.52% CAGR over 2026-2031. Growth is propelled by record hyperscale commitments, national digital-sovereignty mandates, and rigorous ANSSI and GDPR requirements that elevate physical protection from a cost center to a board-level priority. Capital inflows such as the UAE-France 1 GW AI campus and Microsoft’s €4 billion expansion fast-track demand for integrated perimeter, access-control, and AI-driven video-analytics systems. The shift toward autonomous surveillance robots, biometric access, and edge-aware micro-data centers further reshapes procurement strategies. Vendors able to combine local compliance expertise with scalable AI capabilities hold the strongest competitive advantage in the France data center physical security market.

Key Report Takeaways

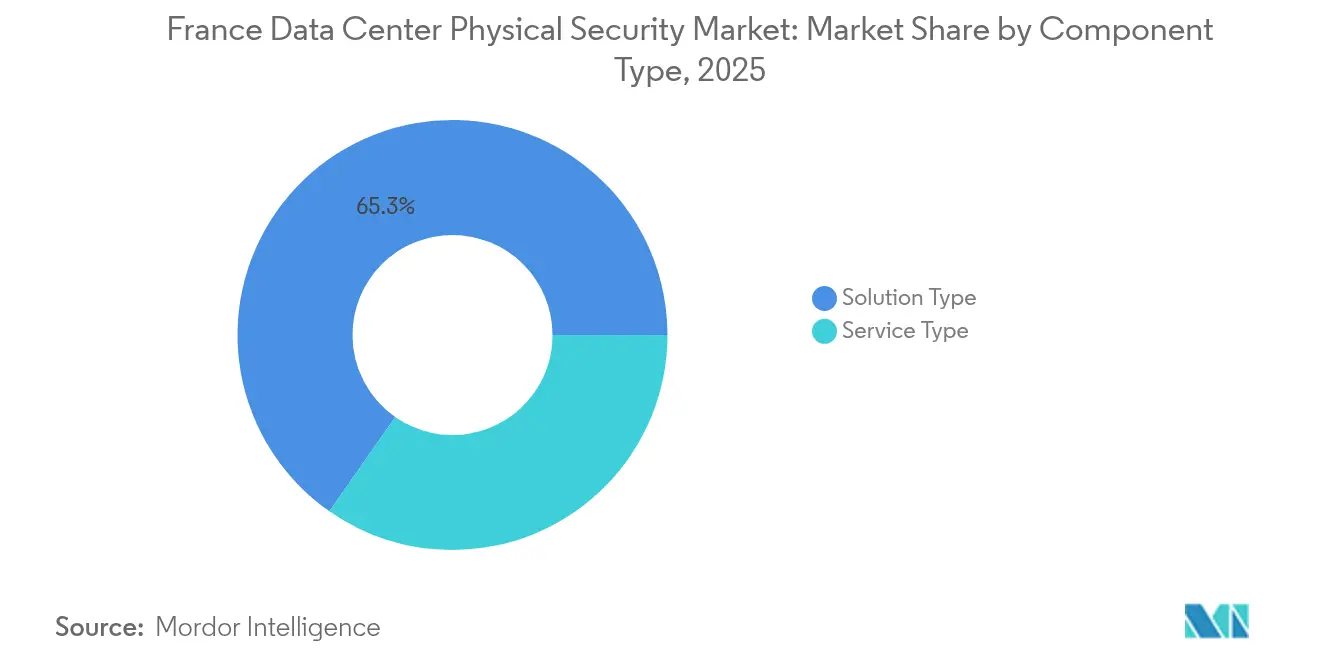

- By component, Solution Type led with 65.30% of the France data center physical security market share in 2025, while Services are poised for the fastest 15.55% CAGR to 2031.

- By data-center tier, Tier III facilities held 66.65% revenue share in 2025; Tier IV deployments are projected to expand at an 17.65% CAGR through 2031.

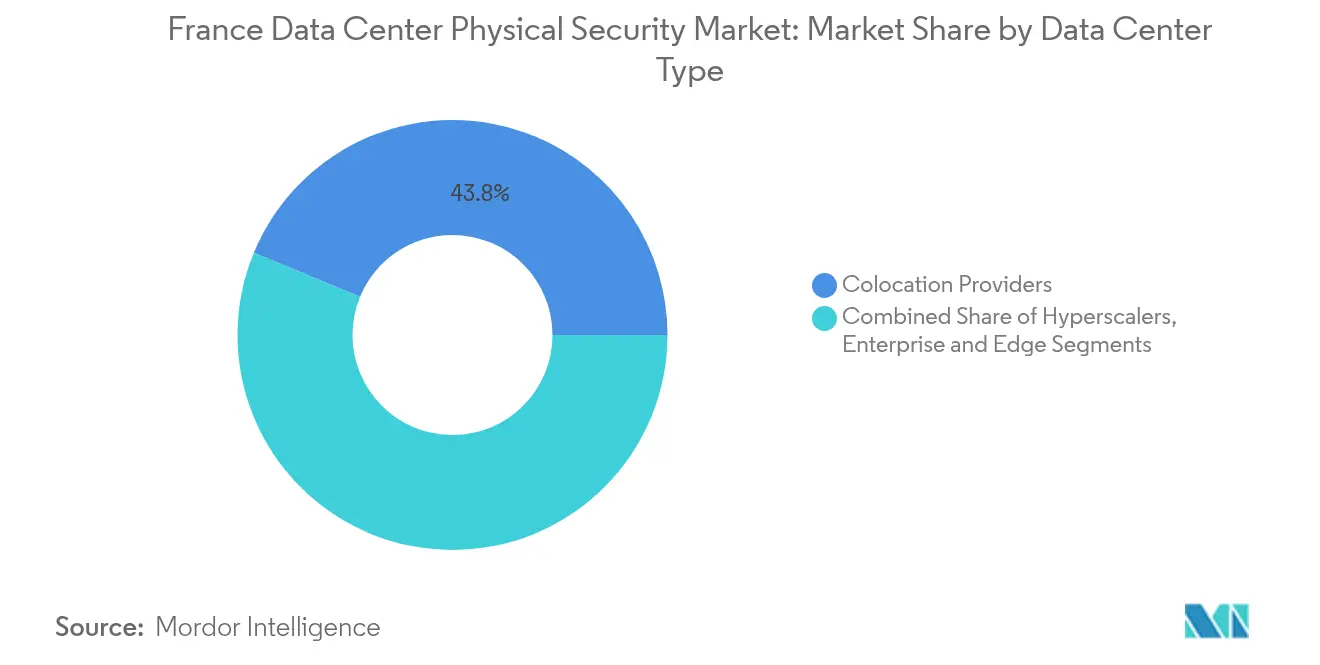

- By data-center type, Colocation Providers captured 43.75% of 2025 revenue, whereas the Hyperscaler/Cloud Service Providers segment is forecast to grow at 17.05% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Global valuation is built by aggregating outputs from multiple countries and regions, with France being one of the contributors. Our global data center physical security market size represents that cumulative total.

France Data Center Physical Security Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| AI-driven video analytics for proactive threat detection | +2.1% | France, with spillover to broader EU | Medium term (2-4 years) |

| Surge in hyperscale and colocation investments | +3.4% | National, concentrated in Paris region | Short term (≤ 2 years) |

| National digital-sovereignty projects driving local data-center builds | +2.8% | France, with policy influence across EU | Long term (≥ 4 years) |

| Stringent ANSSI and GDPR compliance requirements | +1.9% | France, with regulatory harmonization effects in EU | Medium term (2-4 years) |

| Adoption of edge micro data centers for 5G densification | +1.7% | France, urban centers leading deployment | Medium term (2-4 years) |

| Deployment of autonomous security robots and drones | +1.3% | France, pilot deployments expanding nationally | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

AI-Driven Video Analytics for Proactive Threat Detection

Real-time analytics platforms now flag anomalies in milliseconds, shrinking incident-response windows and trimming guard-staff costs. XXII’s migration to Axelera AI’s Metis accelerator cut power draw five-fold and saved €1.5 million in annual operating expense, underscoring the ROI that keeps the France data center physical security market moving toward edge-enhanced computer-vision stacks.[1]Axelera AI Press Office, “XXII migrates real-time analytics to Metis edge accelerator,” axelera.ai Integrators such as Sopra Steria embed these engines into multi-tenant facilities, ensuring compliance with privacy mandates while enriching forensic evidence trails.

Surge in Hyperscale and Colocation Investments

France’s standing as Europe’s emerging AI hub brings a multiplier effect on physical security. Microsoft’s three-site build, part of its €4 billion pledge, mandates layered defenses from fence to rack that map corporate baseline standards to local certification checklists.[2]Data Center Dynamics Editorial Team, “Microsoft invests €4 billion in French cloud and AI expansion,” datacenterdynamics.com Similarly, the 1.4 GW MGX-Bpifrance-Nvidia-Mistral campus represents the continent’s largest security scope, demanding biometric corridors, redundant surveillance clusters, and AI-orchestrated incident workflows that keep the France data center physical security market in high-capex mode.

National Digital-Sovereignty Projects

Paris frames sovereign data capacity as a strategic asset. Semiconductor partnerships with Thales, Radiall, and Foxconn aim to derisk hardware supply lines, locking in trusted physical-security chains from component fab to rack enclosure.[3]CNBC Staff, “France moves to cut semiconductor reliance through new alliances,” cnbc.com Fluidstack’s €10 billion nuclear-powered AI supercomputer showcases how sovereignty doctrines push operators to specify locally governed, autonomous security operations centers that reinforce the France data center physical security market’s long-run momentum.

Stringent ANSSI and GDPR Compliance Requirements

Updated ANSSI guidance for generative-AI hosting compels multilayer “defense-in-depth” architectures, while CNIL fines topping €55 million in 2024 make non-compliance financially untenable. Health-data storage rules (HDS framework) restrict third-country access, prompting dual-authentication gates, segregated equipment rooms, and exhaustive audit logging—all growth engines for the France data center physical security market.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital expenditure on advanced security layers | -2.3% | France, with broader EU market effects | Short term (≤ 2 years) |

| Complex privacy laws limiting biometric surveillance | -1.8% | France, with CNIL enforcement precedent | Medium term (2-4 years) |

| Semiconductor supply-chain constraints | -1.5% | Global, with specific impacts on French deployments | Medium term (2-4 years) |

| Scarcity of certified security-integration specialists | -1.1% | France, with skills shortage across EU | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital Expenditure on Advanced Security Layers

Energy inflation—professional tariffs rose 84% in 2023—squeezes opex budgets, forcing operators to stagger upgrades despite recognition that downtime risks outweigh costs. Schneider Electric’s USD 140 million factory expansion highlights the capital intensity of sensor, cabinet-lock, and analytics-hardware supply required to satisfy the France data center physical security market. Meanwhile, HID’s 20% revenue dip in physical access shows how budget gatekeepers curtail refresh cycles when ROI is unclear.

Complex Privacy Laws Limiting Biometric Surveillance

CNIL’s cautious stance on “augmented cameras” imposes legal friction on face-recognition and gait-analysis rollouts, prompting suppliers to pivot toward privacy-preserving alternatives such as tokenized mobile credentials. Multi-factor systems must achieve compliance without over-collecting personal data, slowing the rollout of some biometric modalities in the France data center physical security market even as threat actors grow more sophisticated.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Component: Services Gain Speed While Solutions Dominate

The France data center physical security market awarded Solution Type 65.30% revenue share in 2025, anchored by large-scale video-surveillance refreshes and perimeter-defense hardware orders. Video analytics engines, thermal imaging, and mobile-credential access points form the bulk of capital allocations. Axis Communications’ thermal-camera line, demonstrated at GSX 2024, exemplifies how higher pixel fidelity offsets visibility challenges in Paris’ fog-prone outskirts. In parallel, AI-enabled access controls-illustrated by Basic-Fit’s multi-country rollouts-enter colocation halls to lessen staffing levels while bolstering audit trails.

Services, though smaller at present, are on a 15.55% CAGR path to 2031 as operators externalize risk through managed SOCs, maintenance SLAs, and regulatory consulting. Tiered ANSSI certification keeps consulting benches busy, while Thales-Google Cloud’s 24/7 SOC co-delivery model typifies premium outsourcing demand. Integration specialists benefit from multi-vendor complexity, sustaining double-digit growth within the France data center physical security market as hybrid AI-edge architectures proliferate.

By Data-Center Tier: Tier IV Sets the Reliability Benchmark

Tier III sites controlled 66.65% of 2025 spend, balancing uptime and budget constraints, but Tier IV is scaling at 17.65% CAGR as hyperscalers insist on concurrent-maintainable designs. Thésée DataCenter’s Tier IV certification demonstrated the cost-plus security that 99.995% uptime demands, including dual-path access control and fully redundant surveillance clusters. Operators leverage modular pod layouts that isolate fire zones and restrict blast radius for hostile events, reinforcing the France data center physical security market’s shift toward higher-tier norms.

Lower-tier (I-II) facilities, particularly edge micro sites linked to 5G densification, prioritize rapid rollout over maximum redundancy. Here, cloud-managed cameras and software-defined locks yield enterprise-grade security without on-premise hardware overhead. Scaleway’s DC5 conversion of a Cold-War shelter illustrates how inherent fortification mixed with modern sensors delivers compliance on a compressed schedule. This tiered landscape ensures that every new capacity tranche injects incremental demand into the France data center physical security market.

By Data Center Type: Hyperscalers Redefine Standards

Colocation Providers retained the largest 43.75% share in 2025, serving diverse tenants with flexible, tenant-segmented security zones. Yet the Hyperscaler/Cloud Service Providers category is racing ahead at 17.05% CAGR, standardizing global security blueprints and automating incident response across estates. Microsoft applies a common AI-orchestrated perimeter posture to each new French facility, creating a replicable playbook that influences mid-market operators.

Edge and enterprise micro-centers gain relevance as latency-sensitive AI inference workloads proliferate. nLighten’s purchase and rebrand of Euclyde to nLighten France expands secure edge nodes that inherit hyperscale-grade policies while nesting inside regional metro rings. As these nodes multiply, the France data center physical security market size for edge solutions swells, with autonomous patrol robots and cloud-native management consoles becoming standard fare.

Geography Analysis

France anchors EU digital-sovereignty ambitions, positioning the France data center physical security market as a regional benchmark. The Paris metropolitan cluster absorbs the bulk of hyperscale expansions, including Microsoft’s three-site build and the USD 30-50 billion UAE-France AI campus, each demanding multilayered defenses tuned to ANSSI directives. High network density and inter-exchange connectivity fuel adoption of AI-enhanced video analytics that bridge physical and logical insights.

Northern France rises as a secondary hotspot owing to land availability, maritime fiber routes, and industrial talent pools. Microsoft’s planned facilities near Dunkirk illustrate how lower real-estate costs free capital for advanced perimeter-intrusion detection and redundant badge systems. Government incentives, coupled with fewer urban permitting hurdles, accelerate go-live timelines, thereby pumping incremental volumes into the France data center physical security market.

Southern France, favored for hydro and solar supply plus cooler ambient temperatures at altitude, lets operators reallocate saved cooling opex toward security automation. Facilities along the Grenoble-Lyon axis, such as BSO’s DataOne AI hub, layer electromagnetic shielding and high-density rack sensors to mitigate heat and interference risks posed by clustered GPUs. Robust road and rail logistics ease hardware replenishment, supporting tighter SLA windows and sustaining the France data center physical security market’s geographic diversification.

Coverage of the global data center physical security market by Mordor Intelligence spans a wide geographic footprint, with regional analysis available for Europe, Asia, and Africa, alongside detailed country-level intelligence for Belgium, Austria, India, South Africa, Hong Kong, and Vietnam, each shaped by local operating conditions.

Competitive Landscape

The France data center physical security market is moderately fragmented, with multinationals and homegrown specialists jousting for contracts that bundle compliance assurance with AI innovation. Axis Communications, Thales, and Schneider Electric leverage vast product portfolios and channel ecosystems, maintaining front-runner status. Thales’ €20.6 billion 2024 revenue underscores scale advantages, while its $3.6 billion Imperva buyout sharpens data-protection cross-selling angles.

Niche players carve value through autonomy and analytics. Econocom’s Captain DC robot patrols white-space aisles, measuring temperature, humidity, and audible anomalies while feeding alerts to cloud SOCs. Génération Robots supplies 130-kg perimeter sentries adaptable to rugged terrain, targeting defense-adjacent campuses that mirror hyperscale security postures. Integrators fuse physical and cyber telemetry, anticipating Cyber Resilience Act requirements that make holistic risk dashboards indispensable.

Supplier alliances expand reach. Thales pairs with CEA on trusted generative-AI frameworks for defense use, a spillover that enhances anomaly detection inside critical data halls. Schneider Electric collaborates with Intel to embed AI inference at UPS and PDU layers, enriching situational awareness without extra racking footprint. As competition sharpens, vendors capable of turnkey delivery—from fence-line LIDAR to SOC orchestration—will steer deal flow across the France data center physical security market.

France Data Center Physical Security Industry Leaders

Johnson Controls International plc

Schneider Electric SE

Axis Communications AB

Genetec Inc.

Thales Group

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- February 2025: MGX, Bpifrance, Nvidia, and Mistral AI unveiled plans for a 1.4 GW Paris data-center campus, one of Europe’s largest AI builds, mandating military-grade physical security across multiple zones

- February 2023: Vantage Data Centers committed €1.4 billion to its EMEA platform, earmarking funds for upgraded perimeter, credential, and surveillance systems within French sites

- February 2025: Eclairion secured €50 million to host the Mistral AI cluster, expanding a specialized footprint that requires hardened cages and biometric gates.

- February 2025: G42 and DataOne revealed an AI-focused facility in France, bolstering national capacity and related security outlays

France Data Center Physical Security Market Report Scope

The data center physical security market refers to the industry focused on providing products and services to safeguard data centers' physical infrastructure and assets. This includes measures to protect data centers from unauthorized access to premises, hardware theft, vandalism, sabotage, terrorist acts, and other physical threats. Data center physical security components may include video surveillance and monitoring, access control systems, physical barriers, biometric authentication, and environmental controls designed to ensure the safety and integrity of the data center environment.

The French data center physical security market is segmented by solution type, service type, and end user. By solution type, the market is segmented into video surveillance, access control solutions, and others. Service type is segmented into consulting services, professional services, and others. End user is segmented into IT & telecommunication, BFSI, government, media & entertainment, and other end users. The market sizes and forecasts are provided in terms of value (USD) for all the above segments.

| By Solution Type | Video Surveillance |

| Access Control | |

| Perimeter Security (Mantraps, Fences, Bollards) | |

| Intrusion Detection and Monitoring | |

| Environmental and Fire Safety Systems | |

| By Service Type | Consulting |

| Integration and Deployment | |

| Maintenance and Managed Services |

| Tier I and II |

| Tier III |

| Tier IV |

| Hyperscaler/Cloud Service Providers |

| Colocation Providers |

| Enterprise and Edge Data Center |

| By Component | By Solution Type | Video Surveillance |

| Access Control | ||

| Perimeter Security (Mantraps, Fences, Bollards) | ||

| Intrusion Detection and Monitoring | ||

| Environmental and Fire Safety Systems | ||

| By Service Type | Consulting | |

| Integration and Deployment | ||

| Maintenance and Managed Services | ||

| By Data-center Tier | Tier I and II | |

| Tier III | ||

| Tier IV | ||

| By Data Center Type | Hyperscaler/Cloud Service Providers | |

| Colocation Providers | ||

| Enterprise and Edge Data Center | ||

Key Questions Answered in the Report

What is the current size of the France data center physical security market?

The market stands at USD 105.44 million in 2026 with a forecast to hit USD 207.37 million by 2031.

Which component segment is growing fastest?

Managed and maintenance services are projected to expand at 15.55% CAGR as operators outsource complex security operations.

Why are Tier IV facilities gaining traction in France?

Hyperscale builds demand 99.995% uptime, driving redundant security architectures that align with Tier IV certification.

How do France’s privacy laws affect biometric security adoption?

CNIL’s strict GDPR interpretation requires privacy-preserving designs, slowing deployment of some facial-recognition systems.

Which geographic areas in France are seeing the most new data center security investment?

Paris leads, but Northern ports and the Grenoble-Lyon corridor are emerging hotspots due to fiber access and renewable energy.

What technology trend is redefining video surveillance in French data centers?

AI-driven real-time analytics running on edge accelerators are replacing manual monitoring, cutting energy use and response times.

Page last updated on: