Market Overview

| Study Period | 2019 - 2030 |

|---|---|

| Base Year For Estimation | 2024 |

| Forecast Data Period | 2025 - 2030 |

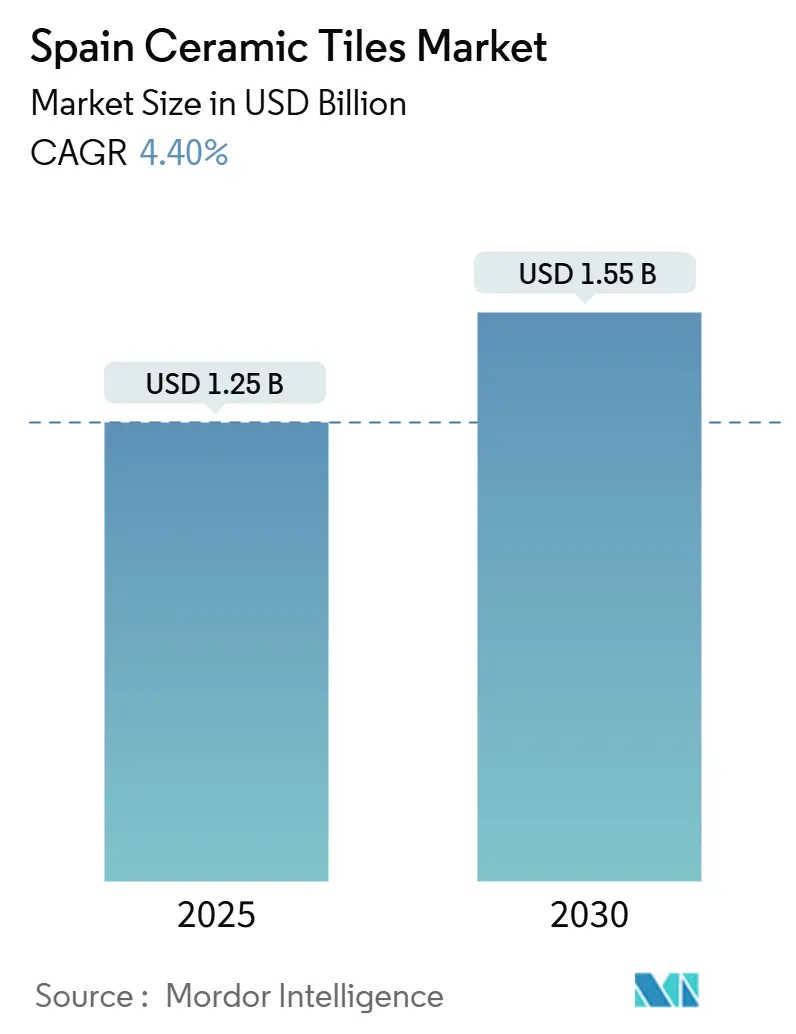

| Market Size (2025) | USD 1.25 Billion |

| Market Size (2030) | USD 1.55 Billion |

| Growth Rate (2025 - 2030) | 4.40% CAGR |

| Market Concentration | Medium |

Major Players

*Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. |

|

Spain Ceramic Tiles Market Analysis by Mordor Intelligence

The Spain ceramic tiles market size stood at USD 1.25 billion in 2025 and is forecast to climb to USD 1.55 billion by 2030, reflecting a 4.40% CAGR despite an 18% contraction in overall EU ceramic output during 2023. Growth hinges on Spain’s tourism rebound—85 million international arrivals in 2023 that spent EUR 108.66 billion (USD 117.12 billion)—which is driving hotel and resort refurbishments across Catalonia, the Balearics, and Valencia. Premium porcelain tiles, known for sub-0.5% water absorption and high mechanical strength, meet the durability demands of these hospitality projects while supporting energy-efficient envelopes in residential retrofits financed by Next Generation EU grants. Online DIY platforms, empowered by augmented-reality visualization and streamlined click-and-collect logistics, are eroding traditional store footfall yet broadening nationwide access to specialty formats. Environmental regulations—from silica-dust exposure limits to looming carbon-pricing schemes—continue reshaping capital-spending priorities and cement manufacturers’ shift toward green-hydrogen kiln conversions.

Key Report Takeaways

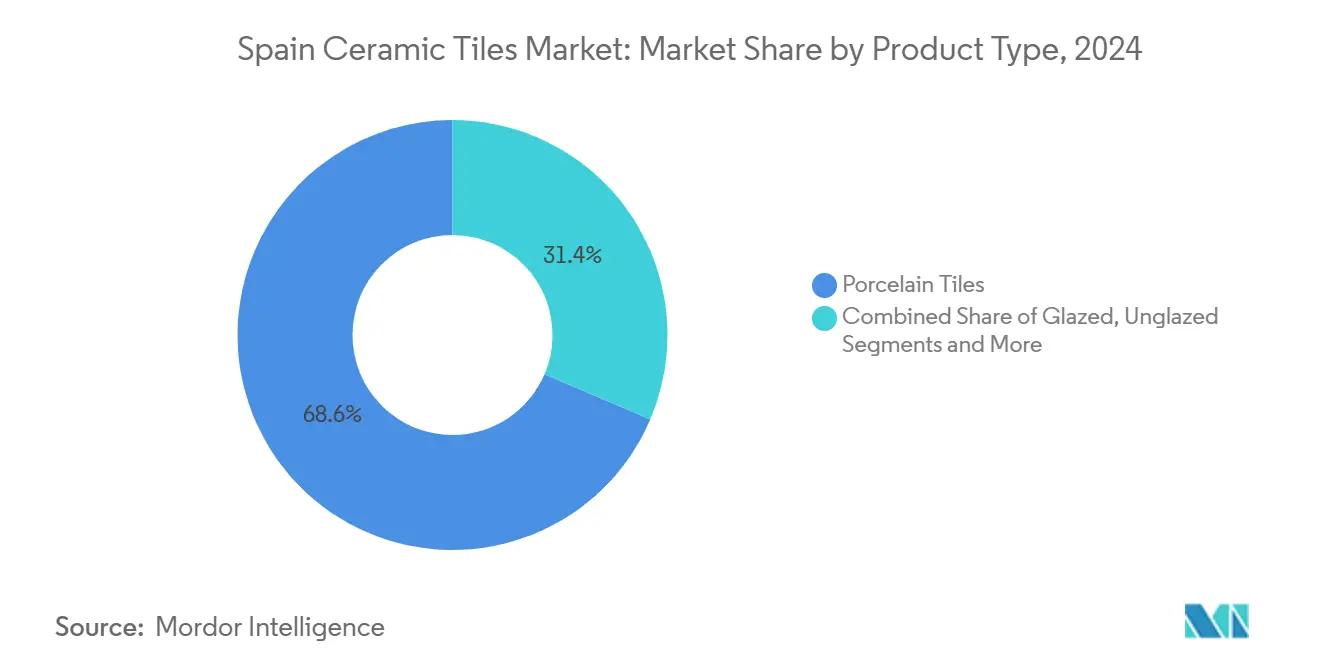

- By product type, porcelain captured 68.6% of Spain ceramic tiles market share in 2024, and it is advancing at a 4.71% CAGR through 2030.

- By application, floors accounted for 72.5% of the Spain ceramic tiles market size in 2024, whereas wall tiles are expanding faster at a 4.62% CAGR to 2030.

- By end-user, the residential segment held 61.2% revenue share of the Spain ceramic tiles market size in 2024 and is set to grow at 4.84% CAGR through 2030.

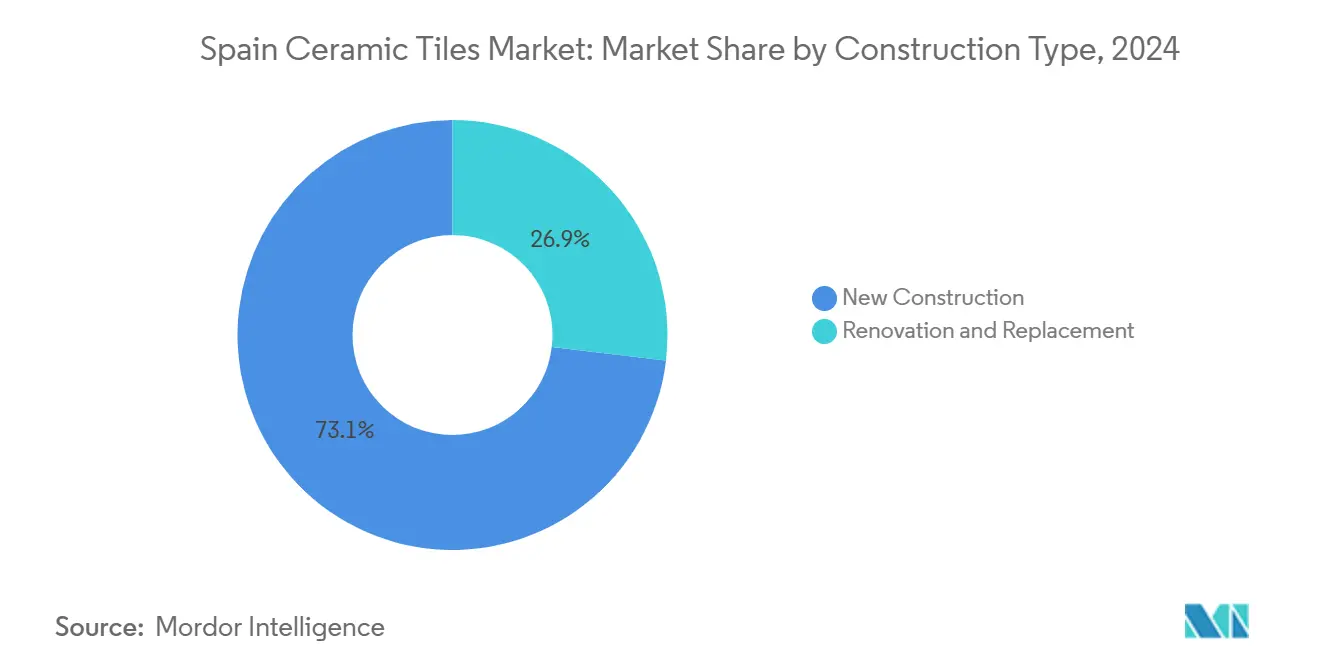

- By construction type, renovation and replacement projects represented 26.9% of Spain ceramic tiles market share in 2024 yet lead growth at a 5.37% CAGR.

- By distribution channel, online retail owned 12.8% of Spain ceramic tiles market size in 2024 and is projected to post a 5.80% CAGR, outpacing all other channels.

Spain Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in renovation & refurbishment of Spain's ageing housing stock | +1.2% | National, with concentration in Madrid, Catalonia, Valencia | Medium term (2-4 years) |

| Recovery of tourism-led hospitality refurbishments | +0.9% | Balearic Islands, Catalonia, Andalusia, Valencia coastal areas | Short term (≤ 2 years) |

| Government incentives for energy-efficient building envelopes | +0.8% | National, with higher uptake in Madrid, Catalonia | Medium term (2-4 years) |

| Expansion of online DIY channels and click-&-collect models | +0.6% | National, with early adoption in urban centers | Short term (≤ 2 years) |

| Adoption of antibacterial glazed surfaces in healthcare & transport hubs | +0.4% | Madrid, Barcelona, Valencia metropolitan areas | Long term (≥ 4 years) |

| Spain's green-hydrogen kiln conversions lowering energy bills post-2027 | +0.5% | Valencian Community, Catalonia manufacturing clusters | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in renovation & refurbishment of Spain's aging housing stock

The comprehensive retrofits to meet EU Green Deal performance thresholds, and the EUR 3.42 billion Next Generation EU allocation is earmarked for remediating 355,000 dwellings by 2030. Provincial programs such as Andalusia’s Plan Eco Vivienda offer 40% subsidies that cap direct homeowner outlays at EUR 3,000, spurring demand for long-life ceramic façades with low thermal conductivity[1]Source: Junta de Andalucía, “Subvenciones Plan Eco Vivienda,” Junta de Andalucía, juntadeandalucia.es. Because the national renovation rate remains 1% annually—well below the EU-mandated 3%—developers are accelerating permit applications, creating predictability for tile orders that favor porcelain due to its insulation value and durability. Third-party financing under the IDAE PAREER mechanism is easing upfront cash needs, broadening homeowner participation and further anchoring future orders for energy-compliant surfaces. This driver ties directly to the Spain ceramic tiles market by supplying a multi-year project pipeline that cushions manufacturers from cyclical new-build fluctuations.

Recovery of tourism-led hospitality refurbishments

International tourist spending surged 24.7% year-over-year in 2023, yielding EUR 108.66 billion that coastal hotels are deploying to refresh guestrooms, spas, and terraces with high-specification porcelain slabs. Average spend per visitor rose to EUR 1,278, signaling a shift toward higher quality experiences that require visually striking yet low-maintenance finishes. Renovation windows now extend across the calendar because reduced seasonality allows continuous works, smoothing demand for tiles in both peak and off-peak quarters. Operators increasingly choose antibacterial glazes that eliminate 99.9% of microbes, fulfilling hygiene expectations of post-pandemic travelers. CaixaBank Research forecasts tourism GDP will grow 2.5% annually through 2026, guaranteeing continued refurbishment cycles that elevate the Spain ceramic tiles market.

Government incentives for energy-efficient building envelopes

The National Energy Efficiency Fund disburses EUR 350 million each year to building-envelope retrofits, contingent on demonstrating 30% primary-energy reductions, prompting architects to specify ventilated ceramic façades with high R-values. Spain’s Integrated National Energy and Climate Plan targets a 23% greenhouse-gas cut from 1990 levels by 2030, adding legislative urgency that speeds specification of tiles complying with ISO 14001 environmental standards. Madrid and Catalonia municipalities, which process permits faster than rural regions, are consuming disproportionate volumes of smart-ventilated ceramic systems. The ERESEE 2020 long-term plan envisions 36.6% lower building energy use by 2050, giving manufacturers a four-decade runway to innovate low-emissivity glazes and lightweight, large-format composites. Collectively, these incentives expand the Spain ceramic tiles market by redirecting public subsidies toward technically advanced, higher-margin products.

Expansion of online DIY channels and click-&-collect models

E-commerce’s 12.8% share of Spain ceramic tiles market in 2024 is small but expanding because homeowners now rely on augmented-reality apps that preview colorways and grout lines in live spaces. Click-and-collect offerings allow bulky pallets to be staged locally, slashing freight surcharges and breakage rates that once deterred online tile purchases. Pandemic-era DIY habits linger, with Google searches for “azulejo baño” remaining 40% above 2019 levels; retailers translate this traffic into bundled kits that pair tiles with adhesives and sealants. Professional installers increasingly order through contractor portals that sync directly with warehouse inventory, guaranteeing just-in-time delivery to jobsites. These digital workflows improve SKU visibility for manufacturers, ultimately accelerating sales velocity across the Spain ceramic tiles market.

Restraints Impact Analysis

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile natural-gas prices inflating manufacturing costs | -0.8% | Valencian Community, Catalonia manufacturing hubs | Short term (≤ 2 years) |

| Rising inflow of low-cost imports (Turkey, India) in budget segment | -0.6% | National, with higher impact in price-sensitive segments | Medium term (2-4 years) |

| Tightening EU silica-dust limits driving compliance capex | -0.4% | National, affecting all manufacturing facilities | Medium term (2-4 years) |

| Scarcity of skilled tile installers delaying project timelines | -0.5% | National, with acute shortages in Madrid, Barcelona | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Volatile natural-gas prices inflating manufacturing costs

Spot gas soared above EUR 120 per MWh in 2023, forcing factories in Castellón’s ceramic corridor to sign short tenors or suspend kilns intermittently. Pamesa mitigated exposure by switching from Endesa to Naturgy, a move that saved EUR 85-90 million and nearly doubled EBITDA from EUR 106 million to EUR 192 million in one fiscal cycle. Such volatility complicates budgeting for glaze formulation and kiln scheduling, sometimes prompting price surcharges that erode customer loyalty. Manufacturers hedge with financial derivatives, but margin calls strain liquidity when price spikes outpace credit lines. Until green hydrogen scales economically, fuel swings will continue to compress profits and temper growth expectations for the Spain ceramic tiles market.

Rising inflow of low-cost imports (Turkey, India) in budget segment

Although the EU renewed anti-dumping duties on Chinese tiles, Turkish and Indian firms still leverage cheaper energy and labor to undercut domestic price points by up to 20% FOB, reshaping tender dynamics[2]Source: Cerame-Unie, “EU Renews Anti-Dumping Duties on Ceramic Tiles,” Cerame-Unie, cerameunie.eu. Spain saw its U.S. export volume slide 19.4% in 2024 as Indian supply displaced higher-cost Iberian shipments, exposing domestic producers to under-utilization risk. Local factories counter by pivoting toward large-format, rectified slabs and bespoke digital prints that command premium margins. However, budget renovation jobs—especially in secondary cities—remain vulnerable to imported alternatives, pressuring the Spain ceramic tiles market’s low-end tiers. Trade bodies lobby for broader safeguard clauses, but WTO compliance limits tariff expansions.

Segment Analysis

By Product Type: Porcelain Dominance Drives Premium Positioning

Porcelain retained 68.6% Spain ceramic tiles market share in 2024 and is forecast to record a 4.71% CAGR through 2030, underscoring its technical supremacy in high-traffic environments. Water absorption below 0.5% allows seamless indoor-to-outdoor transitions, satisfying hospitality designers who need continuity across lobbies and pool decks. KERAjet’s inkjet systems now print 1,000 dpi textures on 20 mm-thick slabs, enabling hyper-real stone looks without quarrying environmental costs[3]Source: Ceramic World Web, “KERAjet Celebrates 25 Years of Inkjet Innovation,” Tile Edizioni, ceramicworldweb.it. Glazed ceramic, holding 18.2%, continues attracting price-conscious renovators seeking color variety, while unglazed technical bodies serve factories and transit hubs requiring slip resistance.

Porcelain’s market leadership stems equally from manufacturing efficiency: continuous milling and spray-drying innovations let producers shorten kilning cycles by 15%, shaving energy use and supporting ESG compliance. Supply risk is minimal because Iberian clay seams near Teruel provide abundant low-iron feedstock ideal for white-body formulations. Export prospects remain bright; although U.S. volumes dipped, Latin American architects increasingly specify Spanish porcelain for upscale malls, diversifying revenue streams. Digital glazing lines with water-based inks cut volatile-organic compounds, enabling plants to meet ISO 50001 energy-management audits. As premium positioning intensifies, porcelain is likely to widen its margin gap over entry-level alternatives, reinforcing its anchor role within the Spain ceramic tiles market.

Note: Segment shares of all individual segments available upon report purchase

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Application: Floor Dominance Meets Wall Innovation

Flooring accounted for 72.5% of Spain ceramic tiles market size in 2024, reflecting the historical importance of durable pavements in Mediterranean architecture. Commercial malls in Seville and Valencia now request 1200 × 600 mm rectified planks, which minimize grout lines and streamline nightly cleaning. Yet wall applications grow 4.62% annually because open-plan kitchens favor seamless backsplashes extending into dining zones, a design motif amplified by social-media influencers. Large-format wall slabs over 3 m tall reduce vertical joints, accelerating installation and cutting labor hours—a key consideration given installer shortages. Roofing tiles, though a smaller slice, receive a boost from Spain’s updated Technical Building Code that rewards high-albedo surfaces for summer heat mitigation.

Hybrid SKUs marketed as “floor-and-wall interchangeables” simplify inventory for distributors and appeal to DIY shoppers navigating online catalogs. Digital-printing multi-pass heads now reproduce terrazzo speckles and terrazzo’s chip-aggregate randomness convincingly, aligning with the retro design trend sweeping Barcelona cafés. Manufacturers integrate recycled glass frit into glazes, helping projects earn LEED credits and cementing tile’s reputation as a circular-economy material. The segment’s evolution demonstrates how product innovation fills aesthetic niches while sustaining the Spain ceramic tiles market’s core revenue engine.

By End-User: Residential Resilience Amid Commercial Recovery

Residential projects held 61.2% Spain ceramic tiles market share in 2024 and are advancing at a 4.84% CAGR through 2030 as homeowners chase energy-saving grants and aesthetic upgrades. Madrid’s municipal rebate covering 40% of façade insulation costs catalyzes demand for ventilated porcelain skins that raise thermal mass without thickening walls. In commercial arenas, hotel refurbishments dominate because operators seek antibacterial surfaces and large-slab statement walls that differentiate guest experiences. Retail stores pivot toward omnichannel layouts, specifying dense-body tiles that stand up to roller-rack loads while matching corporate color palettes via digital glazing. Healthcare facilities, invigorated by EU resilience funds, require antimicrobial floor-wall cove systems that withstand aggressive cleaning regimes, sustaining specialized production runs for the Spain ceramic tiles industry.

Office tenants now favor biophilic designs, prompting architects to mix earthy, matte-finish tiles with living-wall inserts and daylighting strategies. Transport-hub investments—ranging from Zaragoza’s tram extension to Málaga Airport’s Terminal 4 planning—call for slip-resistant, low-maintenance tiles certified to DIN 51130 standards. Educational campuses upgrade cafeterias and dormitories with graffiti-resistant glazes, an emerging niche for Spanish factories experimenting with nanoparticle topcoats. Multifamily build-to-rent schemes adopt thin-tile panels that minimize dead load and accelerate floor-plate turnover, creating new SKU categories. This multi-sector demand blend stabilizes volumes and diversifies risk across the Spain ceramic tiles market.

By Construction Type: Renovation Surge Outpaces New-Build

New construction maintains 73.1% market share in 2024, reflecting Spain's ongoing urban development and infrastructure projects. However, renovation and replacement activities demonstrate superior growth at 5.37% CAGR through 2030, driven by the urgent need to modernize Spain's aging building stock and capture government energy efficiency incentives. The Valencia flooding of 2024 triggered fast-track reconstruction approvals that prioritize resilient flooring materials capable of withstanding future inundations. Next Generation EU funding mandates at least 30% energy-use cuts, nudging contractors toward high-performance porcelain that pairs thermal benefits with aesthetic upgrades. Manufacturers now package façade tiles with mounting substructures, reducing onsite craftsman hours and easing adoption among mid-rise renovators.

Circular-economy mandates encourage demolition crews to segregate old tiles for mechanical recycling, feeding raw material into Cosentino’s Cantera Tecnológica project, which converts 100,000 tons of waste into 240,000 tons of new aggregates. Builders in Bilbao and Oviedo increasingly choose tile overlays instead of full tear-outs, leveraging slim 6 mm panels that preserve ceiling heights while refreshing interiors. Municipalities offer fee rebates for renovations that deploy locally sourced ceramics, reinforcing regional supply chains and supporting employment. All told, renovation’s acceleration gives the Spain ceramic tiles market a countercyclical hedge against new-build lulls.

Get Detailed Market Forecasts at the Most Granular Levels

Download PDF

By Distribution Channel: Digital Disruption Challenges Traditional Retail

Specialty tile houses kept 43.2% Spain ceramic tiles market share in 2024, anchored by in-showroom design labs that guide clients through grout selection and slip-rating codes. Home-improvement chains such as Leroy Merlin leverage scale to bundle tiles with underfloor heating kits, capturing 28.4% share while serving both DIYers and small contractors. Online platforms, however, posted a blistering 5.80% CAGR, aided by AI-powered room renderings that let shoppers visualize grout color shifts in real time. Direct builder procurement, at 15.6%, remains vital for large hotel and airport tenders where manufacturers supply cut-to-size pieces pre-palletized for site cranes.

Brick-and-click hybrids now allow customers to reserve SKUs online, inspect them physically, and finalize electronically, compressing the decision cycle from weeks to days. Warehouses streamline pallet picking with AGV forklifts integrated into MES software, ensuring 24-hour dispatch—a decisive advantage for schedule-driven renovations. Drop-ship agreements between factories and e-retailers bypass intermediaries, letting consumers track containers from kiln exit to curbside delivery. Returns fall as augmented-reality apps improve color accuracy, further enhancing e-commerce margins. This omnichannel mosaic broadens buyer reach, ultimately magnifying revenue capture for the Spain ceramic tiles market.

Geography Analysis

The Valencian Community supplied 25.5% of Spain ceramic tiles market share in 2024, benefitting from dense industrial clusters around Castellón that house Porcelanosa, Pamesa, and Keraben. Abundant kaolin seams and port access lower raw-material and shipping costs, while the region’s Hydrogen Valley initiative underpins pioneering kiln trials planned for 2026[4]Source: Fuel Cells Works, “Hydrogen Valley Valencia Advances H₂frit Pilot,” Fuel Cells Works, fuelcellsworks.com. Provincial grants reimburse up to 50% of hydrogen retrofit expenses, accelerating the shift toward low-carbon manufacturing. Reconstruction of flood-damaged municipal buildings adds near-term volume, with special urban-planning rules fast-tracking permits and boosting tile demand. Valencian R&D hubs collaborate with university labs to perfect inkjet glaze rheology, cementing the region’s innovation edge within the Spain ceramic tiles market.

Catalonia commanded 22.8% share due to Barcelona’s steady pipeline of hotel revamps and luxury condos that favor large-format porcelain for seamless open-plan interiors. The Port of Barcelona’s streamlined customs accelerate raw-material imports and finished-goods exports, reinforcing supply chain agility. Coastal resorts in Costa Brava and Costa Daurada funneled EUR 20.88 billion in tourist spend into property upgrades during 2023, sustaining a premium-tile pull. Catalonia’s climate legislation, which caps building operational energy, further elevates demand for ventilated ceramic façades. Regional design councils promote circular construction, pushing architects toward recycled-content glazes that align with EU taxonomy rules and expand technical breadth across the Spain ceramic tiles market.

The Madrid Region delivered the fastest CAGR at 5.13% through 2030, supported by mixed-use megaprojects like Madrid Nuevo Norte and consistent office-tower retrofits. The capital’s 18.7% share understates future potential, as corporate relocations trigger facility upgrades requiring antibacterial tiles in lobbies and restrooms. Metro Madrid’s station-modernization plan specifies graffiti-resistant porcelain panels that fulfill anti-vandalism mandates, adding steady public-sector volume. Labor bottlenecks slightly temper installation speed, but higher wages attract cross-border artisans who offset the shortage. Government-backed mortgage incentives encourage apartment renovations, increasing per-capita tile consumption and injecting durable tailwinds into the Spain ceramic tiles market.

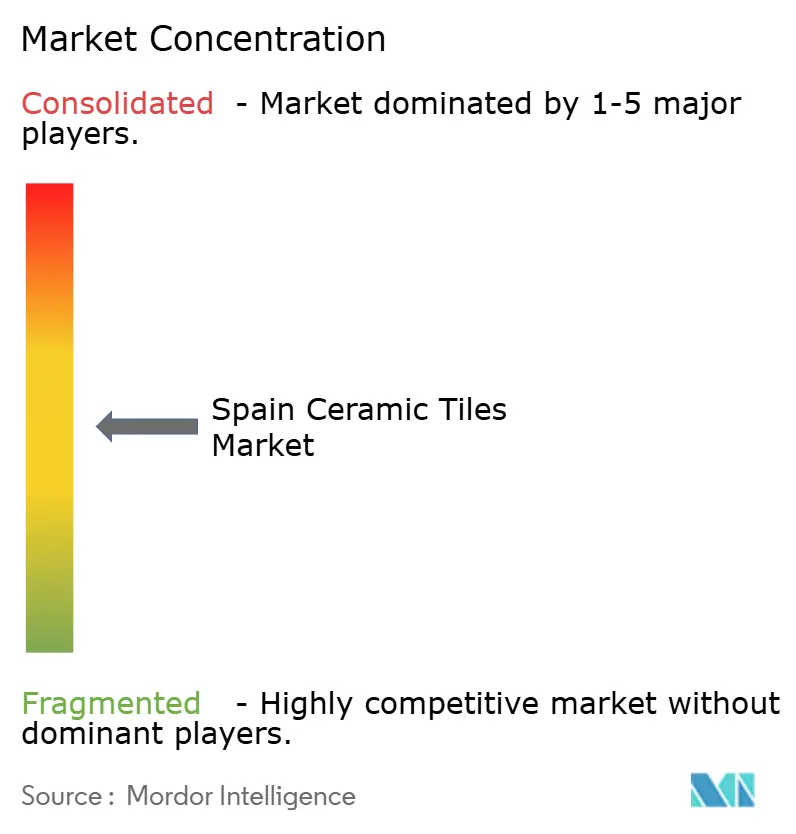

Competitive Landscape

Spain’s ceramic-tile sector shows moderate consolidation, with legacy brands leveraging continuous-kiln retrofits and digital-printing patents to defend margins against Asian importers. Pamesa’s 2024 energy-procurement overhaul lifted EBITDA fivefold, highlighting the outsized influence of fuel strategy on competitiveness. Porcelanosa’s automated high-bay warehouses deploy 120 AGVs that pick 300 pallets per hour, shrinking order-to-ship windows to 24 hours and elevating customer satisfaction. Roca Tile expands global reach via joint ventures in the United States, offsetting domestic cyclicality and boosting brand prestige abroad.

Innovation remains the main battleground: KERAjet’s fifth-generation printheads apply metallic lusters in a single pass, opening luxury-segment volumes while reducing ink waste by 15%. Smaller boutique players survive by channeling Spain’s artisanal heritage into hand-painted collections that command triple the square-meter price of mass-produced stock. Compliance costs, however, disproportionately burden SMEs; silica-dust extraction-system upgrades consume capex that could otherwise fund marketing. Collaboration across value-chain actors—glaze formulators, machinery builders, clay miners—is tightening, yielding process breakthroughs that the Spain ceramic tiles market can deploy at scale.

Rising ESG scrutiny influences investor sentiment; manufacturers publishing third-party-verified carbon footprints secure favorable loan terms under EU taxonomy rules. Corporate PPAs with renewable-energy farms cap power expenses while burnishing sustainability credentials, critical when courting LEED-focused developers. Import threats from Turkey and India persist, but Spain’s premium-quality positioning coupled with technological sophistication sustains a price floor. Antimicrobial, IoT-embedded, and recycled-content tiles constitute future growth vectors, with early adopters likely to consolidate share as building codes evolve.

Spain Ceramic Tiles Industry Leaders

-

Pamesa Cerámica

-

Porcelanosa Grupo

-

Grupo STN

-

Roca Tile

-

Keraben Grupo

- *Disclaimer: Major Players sorted in no particular order

Need More Details on Market Players and Competitors?

Download PDF

Recent Industry Developments

- November 2024: Cosentino committed EUR 90 million to its Cantera Tecnológica plant, aiming to convert 100,000 tons of waste into 240,000 tons of new ceramic-grade aggregates, cutting 1 million tons of CO₂ over a decade.

- September 2024: BP and Iberdrola reached final investment decision on a 25 MW green-hydrogen plant at BP’s Castellón refinery, slated to generate 2,800 tons of renewable hydrogen yearly for nearby ceramic kilns.

- August 2024: The H2frit project installed hydrogen-ready oxy-fuel burners at Esmalglass, commencing pilot tests to replace natural gas in frit production and cut kiln emissions materially.

Spain Ceramic Tiles Market Report Scope

A complete background analysis of the spanish ceramic tiles market, which includes an assessment of the parental market, emerging trends in the segments and regional markets, and significant changes in market dynamics and market overview, is covered in the report. The report also offers a qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across various key points in the value chain.

The Spanish ceramic tiles market is segmented by product, application, construction type, and end-user. By product, the market is sub-segmented into glazed, porcelain, scratch-free, and other products. By application, the market is sub-segmented into floor tiles, wall tiles, and other applications, By construction type, the market is sub-segmented into new construction, replacement, and renovation. By end-user, the market is sub-segmented into residential and construction. The report offers market size and forecasts for the Spain ceramic tiles market in value (USD) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Valencian Community |

| Catalonia |

| Andalusia |

| Madrid Region |

| Other Regions |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Valencian Community | |

| Catalonia | ||

| Andalusia | ||

| Madrid Region | ||

| Other Regions | ||

Need A Different Region or Segment?

Customize Now

Key Questions Answered in the Report

How large is Spain’s ceramic-tile demand in 2025?

The market is valued at USD 1.25 billion in 2025 and is projected to reach USD 1.55 billion by 2030.

Which product category holds the biggest share of tile sales?

Porcelain accounts for 68.6% of national volume and is also the fastest-growing category.

What is driving the surge in residential tile renovations?

EU-funded energy-efficiency grants worth EUR 3.42 billion subsidize upgrades for 355,000 homes, lifting residential demand.

Why are online tile sales expanding quickly?

Augmented-reality visualization, click-and-collect logistics, and pandemic-era DIY habits propel a 5.80% CAGR for e-commerce channels.

How are energy costs being tackled by Spanish manufacturers?

Leading plants are piloting green-hydrogen kilns and renegotiating gas contracts to curb fuel volatility and lower CO₂ emissions.

Page last updated on: