Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 1.25 Billion |

| Market Size (2026) | USD 1.31 Billion |

| Market Size (2031) | USD 1.59 Billion |

| Growth Rate (2026 - 2031) | 3.95% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Spain Ceramic Tiles Market Analysis by Mordor Intelligence

The Spain ceramic tiles market size was USD 1.25 billion in 2025 and is projected to reach USD 1.59 billion by 2031, reflecting a 3.95% CAGR. Spain retained its premium-export positioning in 2025 as renovation-led demand in North America favored high-design, low-embodied-carbon tiles and verified slip performance, even as energy and compliance costs pressured margins. Factors contributing to this domestic demand included code-driven slip and air-quality mandates, along with an increased reliance on environmental product declarations in public tenders. From 2026 to 2030, the European Union emissions trading system plans a reduction in free allowances. This move is expected to elevate annual compliance costs for the sector, intensifying margin pressures on gas-heavy plants. While production metrics improved through 2025, pricing power remained limited. As a result, investment focus shifted towards thin-gauge porcelain, digital short-run lines, and modular façade systems, all designed to streamline logistics and reduce installation time.

Key Report Takeaways

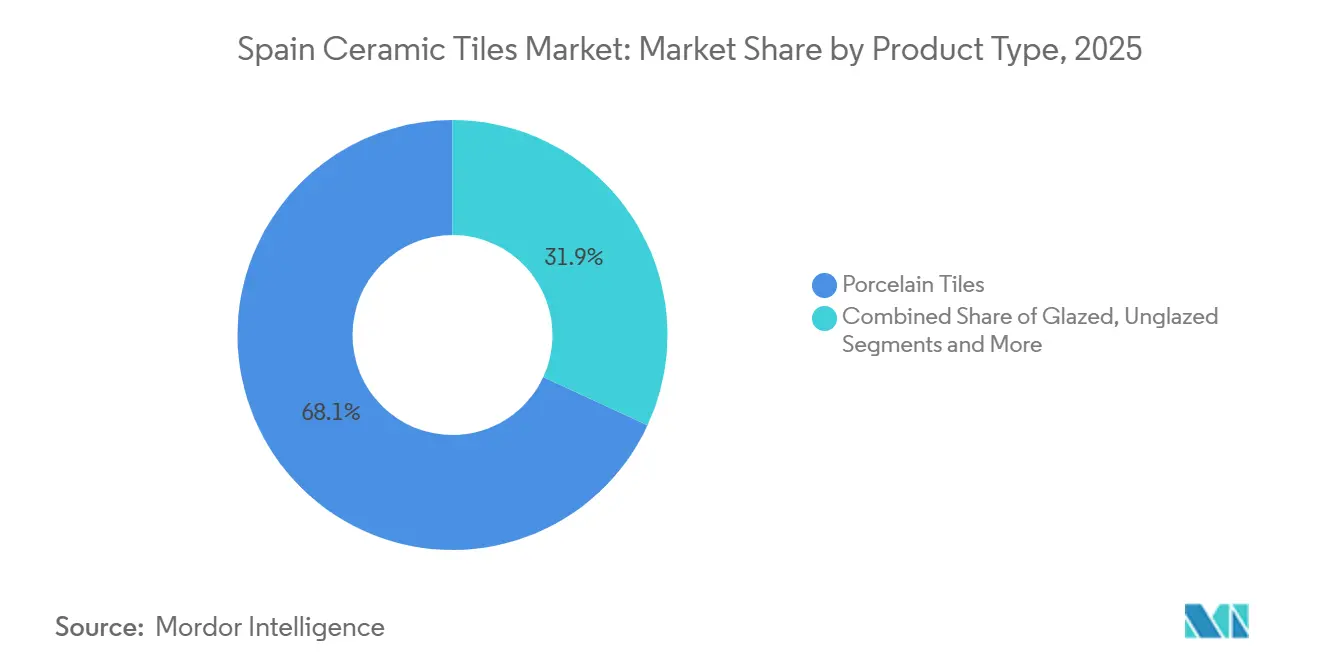

- By product type, porcelain led with 68.14% revenue share in 2025 in the Spain Ceramic Tiles Market, while porcelain is projected to grow at a 4.42% CAGR through 2031.

- By application, floor accounted for a 72.10% share in 2025 in the Spain Ceramic Tiles Market, while the wall is forecast to expand at a 4.31% CAGR to 2031.

- By end-user, residential captured 60.70% in 2025 in the Spain Ceramic Tiles Market, while residential is expected to lead growth at a 4.49% CAGR through 2031.

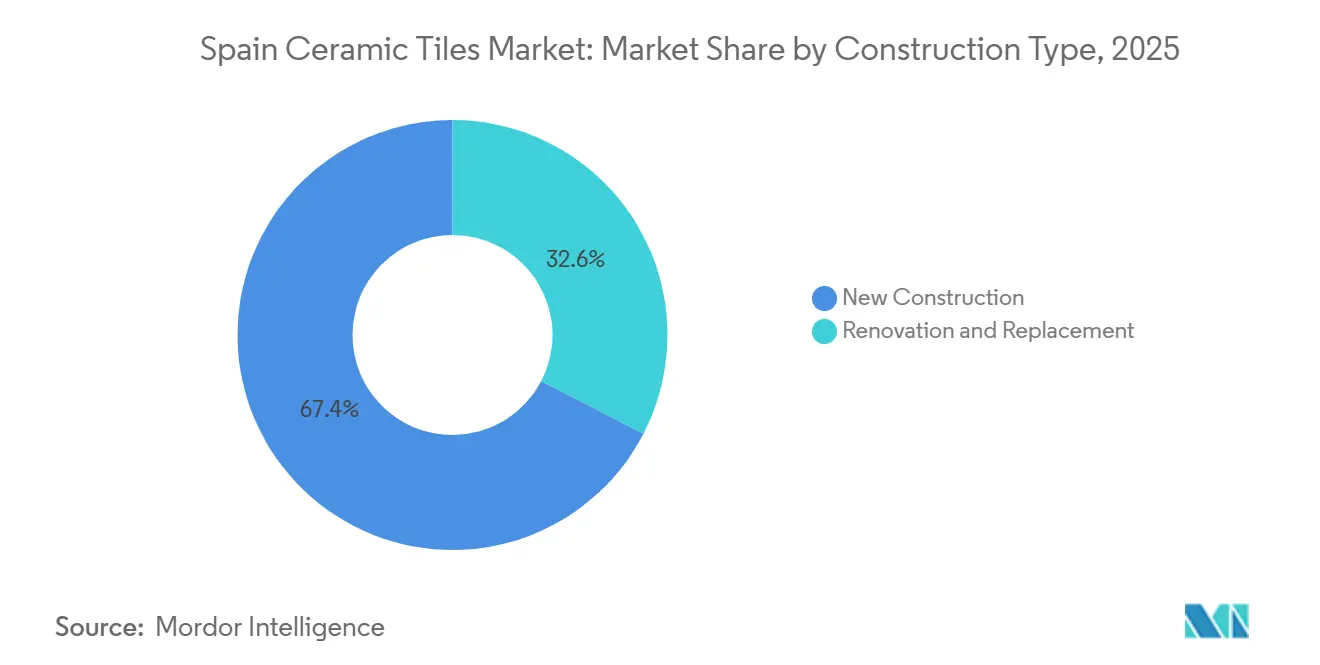

- By construction type, new construction held 67.40% in 2025 in the Spain Ceramic Tiles Market, while renovation is projected to advance at a 4.96% CAGR through 2031.

- By distribution channel, specialty tile and stone stores represented 23.53% in 2025 in the Spain Ceramic Tiles Market, while online retail is on track for a 5.34% CAGR through 2031.

- By geography, the Valencian Community held 25.12% in 2025 in the Spain Ceramic Tiles Market, while the Madrid Region is forecast to grow at a 4.74% CAGR to 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Spain Ceramic Tiles Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Renovation wave and energy-efficiency retrofits | +1.2% | National, early gains in Madrid, the Valencian Community, and Catalonia | Medium term (2-4 years) |

| Export recovery in premium sustainable design | +0.9% | Global, concentrated in the USA and core EU markets | Short term (≤ 2 years) |

| Preference for hygienic, low-VOC, easy-to-sanitize surfaces | +0.7% | National, strongest in healthcare, education, and transport hubs | Medium term (2-4 years) |

| Building code emphasis slip resistance and fire performance | +0.5% | National, especially Madrid, Barcelona, Valencia metros, and public institutions | Long term (≥ 4 years) |

| Public procurement favoring EPD-backed EU-made tiles | +0.4% | National, the highest in the Madrid Region, the Basque Country, and Catalonia | Medium term (2-4 years) |

| Adoption of porcelain pavers and ventilated facades | +0.6% | Urban cores including Madrid, Barcelona, Valencia, Seville | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Renovation Wave and Energy-Efficiency Retrofits Across Aging Housing Stock

Spain faces a housing deficit that has driven investment towards deep retrofits. Without sustained policy support for building upgrades, this shortfall could increase significantly over the decade. Ceramic tiles play an important role in these retrofitting initiatives. Their zero-VOC formulations and thermal mass properties enable projects to meet the Technical Building Code standards on indoor environmental quality and envelope performance. This trend is highlighted by a rise in housing permits, which increased in 2024. As labor shortages slow the pace of new constructions, a growing share of these permits is allocated to rehabilitation. These workforce limitations act as a bottleneck and drive the adoption of prefabricated tile systems. Such systems minimize on-site labor hours, supporting the use of modular facade solutions and large-format interior panels. Procurement rules raise the bar on slip resistance in shared areas under CTE DB-SUA Class 2 and Class 3 thresholds, and manufacturers have responded with structured finishes that meet these levels. Product-level decarbonization is visible in collections such as Porcelanosa’s ECOLOGIC, which embeds high recycled content and reports lower global-warming potential to qualify for EPD-linked scoring in tenders[1]Porcelanosa, “Butech Modular Facade Systems,” Porcelanosa, porcelanosa.com.

Export Recovery in Premium Design and Sustainable Collections Under EU Green Deal Alignment

Spanish exports were EUR 3.481 billion in 2024, with the United States rebounding in value terms as renovation budgets prioritized mid-to-premium looks and robust sustainability documentation[2]ASCER, “Spanish Ceramic Tile Industry Annual Report 2024,” ASCER, ascer.es. EU Green Deal targets are accelerating the adoption of tiles with lower embodied carbon, and Spanish producers report an average emissions intensity of close to 5.6 kilograms of CO₂ per square meter following sustained reductions. Scale and short-run customization converge in capital plans, including Pamesa’s investments in thin-gauge slab presses and high-bar digital printers to cut lead times for architecture projects. Pamesa's 2025 acquisition of Natucer, which generated EUR 32 million in 2024 revenues, consolidates production capacity while spreading the EUR 65 million investment in 24-bar digital printers and Supera continuous presses across a broader export base, enabling shorter lead times for North American specification projects.

Preference for Hygienic, Low-VOC, Easy-to-Sanitize Surfaces in Public Buildings

Post-pandemic facility standards elevate non-porous and bacteriostatic finishes in healthcare corridors, classrooms, and transit venues, and ceramic tiles provide Class 5 wear resistance and zero formaldehyde emissions to support life-cycle value[3]ISO, “Abrasion and Slip Resistance Testing,” ISO, iso.org. National code updates raised minimum slip-resistance thresholds in wet zones from Class 1 to Class 2, which narrows options to micro-textured porcelain in many public settings. Antibacterial ceramic surfaces validated under European projects, such as silver-ion systems tested to EN ISO 22196, are a strong fit for hospital procurement with documented microbial reduction. Designers also prefer large-format rectified tiles with tight joints to limit microbial lodging, and modular façade systems integrate these finishes into coordinated wall and floor specifications that streamline documentation for green building credits.

Building Code Emphasis on Slip Resistance and Fire Performance in High-Traffic Areas

Spain’s code framework prioritizes non-combustibility and verified friction values in public spaces, and porcelain tiles satisfy A1 fire classification while meeting Class 3 slip thresholds for external ramps and heavy-traffic corridors. Madrid Metro’s 2024 to 2025 upgrades specified UNE-ENV 12633 Class 3 slip performance for platforms, which condensed awards among manufacturers with pre-approved test certificates. The 2026 code update is expected to tighten façade fire-reaction criteria for systems covering significant surface area, which strengthens the role of ceramic ventilated facades that meet A2-s1,d0 performance or better. Industrial safety updates extend compartmentation and smoke control to additional facility types, and ceramic floor systems provide zero-smoke emissions without additive flame retardants. Public-sector landlords, hospitality operators, and airport authorities use these code baselines to minimize operational risk, and specified ceramic solutions align with insurance underwriting that favors non-combustible assemblies.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Elevated energy and carbon compliance costs | -0.8% | National, acute in the Castellón production hub | Short term (≤ 2 years) |

| Competitive pricing pressure from Turkish and Asian imports | -0.6% | National, stronger in Catalonia, Andalusia, and secondary markets | Medium term (2-4 years) |

| Rising penetration of LVT/SPC and engineered wood | -0.5% | National, price-sensitive segments in secondary cities | Medium term (2-4 years) |

| Drought-related construction constraints | -0.3% | Andalusia, Murcia, eastern Catalonia, episodic coastal impact | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Elevated Energy and Carbon Compliance Costs Inflating Domestic Tile Prices

The EU ETS will reduce free CO₂ allowances from 2026 to 2030, increasing compliance costs for gas-fired ceramics lines that run continuous kilns and dryers. Spanish industry analysts expect rising EU ETS outlays to absorb a large portion of sector profits unless producers accelerate electrification and fuel switching. Energy inflation since 2021 and limited pricing headroom in export markets have compressed margins, which have tested the resilience of smaller operators. Early electrification moves include the first fully electric tile kiln powered with renewable electricity, which eliminates Scope 1 emissions on specific lines and de-risks carbon costs. Large groups are piloting hydrogen and synthetic fuels that aim to cut gas dependence by mid-decade, and these projects illustrate the capex scale needed for decarbonization at volume.

Competitive Pricing Pressure from Turkish and Asian Imports in Mid-Range Product Lines

Imported mid-range porcelain from Turkey and Asia competes on landed cost, and currency effects and policy supports in origin markets translate into price ladders that challenge Spanish tiles in cost-sensitive channels. Builders in secondary cities weigh upfront price over life-cycle performance when budgets are tight, which shifts share toward imports in commodity ranges. Spanish manufacturers maintain an edge in documented slip resistance and EPD-backed sustainability that is required in many public and commercial projects[4]Boletín Oficial del Estado, “Código Técnico de la Edificación,” Government of Spain, boe.es. Larger-format imports are increasing, though compliance hurdles arise when polished finishes do not meet required friction classes under national codes for wet or external areas. Digital direct-sales channels intensify price comparisons, so domestic brands have responded with thin-gauge formats and service bundles that compress installation time and total cost of ownership.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Product Type: Porcelain Dominance Anchors Premium Positioning

Porcelain accounted for 68.14% of 2025 demand and is forecast to grow at a 4.42% CAGR through 2031, supported by EN 14411 Group Bia performance, freeze-thaw suitability, and large-format capability across floors and façades. Thin-gauge porcelain down to 6 millimeters reduces embodied carbon and freight cost per square meter, which supports export competitiveness in North America and lowers structural loads on retrofits. Advancing public procurement norms gives an advantage to porcelain collections with product-specific EPDs, and Spanish producers hold broad verification portfolios under accredited schemes. Glazed ceramic remains relevant in wall applications where decorative finishes and price targets dominate, while unglazed technical tiles focus on industrial and high-abrasion settings.

Modular systems enhance porcelain’s role as a complete solution since prefabricated façade panels integrate thermal, acoustic, and movement-control functions to cut site time. Structured surfaces and through-body coloration keep slip performance and aesthetics consistent over service life, which underpins specifications in high-traffic transit and retail corridors. Digital printing narrows the cost gap for photorealistic wood and stone looks on porcelain formats, which drives continued mix shift away from standard glazed wall tiles in higher-spec spaces. Price-sensitive segments still favor conventional glazed ceramic in selected regions, which sustains a multi-tier supply structure within the Spain ceramic tiles market.

By Application: Floor Remains Core, Wall Gains on Façade Innovation

Flooring held 72.10% of demand in 2025, anchored by code-mandated slip resistance in wet and high-traffic zones and the material’s abrasion resistance and durability in long-use facilities. CTE DB-SUA requires Class 2 for most indoor circulation areas and Class 3 for exterior ramps, which concentrates floor specifications on textured porcelain in public and commercial settings. Renovation programs in older residential stock lift floor replacement volumes, while transport hubs maintain strict friction and wear thresholds for liability and service continuity. Wall applications are growing at a 4.31% CAGR to 2031, helped by ventilated façades and photocatalytic coatings that contribute to air-quality goals and reduce maintenance frequency.

Large-format wall slabs reduce joints and water ingress risk, and this raises acceptance in high-rise residential towers and corporate headquarters projects with periodic façade cleaning cycles. Export-facing wall lines benefit from capacity additions and process intensification on thin slabs, which shorten lead times for specification-driven projects. Roofing remains a niche application in heritage sites where ceramic profiles align with protected aesthetics, while modern systems rely on membranes or metal for weight and assembly reasons. Documented EPDs and friction values increasingly appear as prerequisites in public tenders for both floor and wall packages, which favors domestic suppliers with ready-to-download technical files.

By End-User: Residential Leads, Commercial Diversifies

Residential accounted for 60.70% of demand in 2025 and is expected to expand at a 4.49% CAGR through 2031 as aging housing stock, hygiene preferences, and energy retrofit incentives increase kitchen and bathroom upgrade cycles. Indoor-air-quality provisions under national regulation reinforce zero-VOC and easy-to-sanitize surfaces in occupied spaces, and porcelain meets these requirements with minimal maintenance. Demographic and inheritance dynamics channel spending into refurbishment rather than relocation in many provinces, and tile durability and fire performance strengthen its role in long-term asset value. In commercial settings, hospitality and retail have resumed brand-driven renovation schedules that emphasize slip resistance and cleanability with coordinated floor-wall concepts.

Healthcare facilities require bacteriostatic finishes validated under EN ISO 22196, and antibacterial ceramic solutions offer documented performance for infection-control standards. Education and public buildings face budget ceilings yet must comply with non-combustible surface requirements, which supports ceramic wall cladding in circulation and assembly areas. Transport hubs specify high friction and wear classes and favor materials with reproducible performance across large areas, which keeps porcelain in the core palette. The Spain ceramic tiles market continues to benefit from the breadth of institutional applications where code compliance, EPD availability, and long service life outweigh initial price differentials.

By Construction Type: Renovation Surges Past New-Build

New construction represented 67.40% of demand in 2025, while renovation and replacement projects are projected to grow at a 4.96% CAGR, reflecting policy and demographic forces that favor upgrades to existing homes and buildings. Energy performance regulations and life-cycle accounting are shifting project scopes toward envelope improvements, bathroom reconfigurations, and accessibility upgrades where porcelain provides slip-resistant, non-porous surfaces. Public funding under the Recovery and Resilience Plan prioritizes urban regeneration and energy retrofits, which channels tenders into product categories with verifiable environmental performance. Renovation cycles also proceed with fewer permitting hurdles than new builds, which compresses lead time from award to installation and rewards suppliers with rapid sample-to-order processes.

New-build momentum persists in growth corridors like the Madrid Region and remains an anchor for distribution networks that combine direct contractor sales with specialized retail. Off-site construction and prefabricated façade systems deliver scheduling certainty, and ceramic modules enable repeatable assembly with integrated movement and drainage solutions. The Spain ceramic tiles market benefits from both streams since larger new-build projects adopt modular cladding while renovation projects use thin-gauge formats to avoid structural interventions. As code updates tighten thermal transmittance limits, ceramic rainscreens paired with mineral insulation will stay central to compliant façades, which underscores the value of EPD-documented assemblies.

By Distribution Channel: Online Disrupts, Specialty Adapts

Specialty tile and stone stores held 23.53% of distribution in 2025 and continue to serve as design consultation hubs with hybrid models that combine curated sampling and e-commerce fulfillment. Online retail posts the fastest growth at a 5.34% CAGR because manufacturers and distributors now offer full technical documentation, EPD downloads, and real-time availability through digital portals. Direct sales to contractors remain the largest single channel in project-based jobs since volume discounts and established credit terms align with builder cash-flow structures. Home improvement stores focus on DIY-friendly ceramic ranges yet face limits where waterproofing and substrate preparation require professionals from the Spain ceramic tiles industry.

B2B platforms and manufacturer portals accelerate selection through visualization and sample shipping, which shortens specification cycles in both residential and small commercial projects. Public tenders require ISO and EPD documentation that online channels can present instantly, which reduces time spent chasing paper certificates and test reports. Specialty stores retain a role in boutique hospitality and heritage projects where custom color and small-batch runs need hands-on technical guidance. The Spain ceramic tiles market is therefore multi-channel, with digital convenience improving access and physical consultative spaces preserving value in complex specifications.

Geography Analysis

The Valencian Community accounted for 25.12% of the 2025 volume, supported by Castellón’s dense cluster that integrates clay inputs, frits and glazes, kilns, and logistics within a compact radius for efficient supply. This concentration enables just-in-time workflows and supports export scale, while decarbonization investments and electrification pilots determine which facilities sustain high utilization. Public innovation grants in 2025 backed SME digitalization and hydrogen pilots, although the magnitude of sector capex needs means large groups advance faster on electrification and process changes. Regional demand benefits from coastal renovation programs that address corrosion and accessibility in older multifamily buildings, where slip resistance and water tolerance are critical.

The Madrid Region is forecast to grow at 4.74% through 2031 because new permits, office-to-residential conversions, and high-income demand in central districts pull premium tile specifications into core projects. Public procurement for Operación Campamento requires low-embodied-carbon materials with verified life-cycle data, so projects strengthen the advantages of domestic producers with accredited EPDs. Catalonia contributes a significant share and continues steady growth as hospitality renovations and urban retrofit policies expand the use of ventilated facades and slip-tested interior finishes. Andalusia faces episodic drought constraints that tighten construction schedules in coastal zones, so projects with water-saving site practices and prefabrication progress more predictably.

Other regions, including the Basque Country, Galicia, Castilla y León, and Murcia, add diversified demand with municipal retrofits, food-processing flooring upgrades, and public-building programs that mandate non-combustible, hygienic finishes. Logistics access, accreditation expectations, and code enforcement shape local mixes, and Madrid Metro’s slip standards for platforms exemplify how large public owners channel volume to pre-certified ceramic lines. Comparing major geographies shows interior regions gaining share as renovation intensity and institutional spending offset slower ground-up activity in saturated cores, which broadens the customer base for the Spain ceramic tiles market.

Competitive Landscape

The top five producers control nearly half of the domestic capacity, yet competition remains active across premium, mid-range, and commodity segments as EPD coverage, code compliance, and modular solutions become entry tickets. Strategic differentiation focuses on speed and sustainability, so short-run digital printing and thin-gauge slab lines reduce lead times while enabling custom looks for design-led projects. Electrification and alternative fuels define resilience to carbon costs, and the first fully electric kiln powered by renewable electricity demonstrates a path to zero Scope 1 on selected lines.

Vertical integration into façades and installation systems captures value beyond tiles, and modular units with integrated insulation and drainage compress site time and centralize documentation. Patent activity underscores material and process innovation, including hydrogen combustion and photocatalytic glazes that maintain surface cleanliness under UV exposure. Export performance depends on verified environmental credentials and slip performance that meet North American standards, which supports Spain’s premium positioning in renovation-focused channels.

Digital channels intensify price transparency for mid-range products, and domestic brands respond with service bundles, fast sampling, and clear EPD access to justify premiums. Utilization and capex discipline remain critical because energy costs and EU ETS exposure raise the hurdle rate for kiln refurbishments and process changes. The Spain ceramic tiles market continues to reward suppliers who combine verifiable sustainability, code-ready performance, and reliable lead times for both domestic tenders and export customers.

Spain Ceramic Tiles Industry Leaders

Pamesa Cerámica

Porcelanosa Grupo

Grupo STN

Baldocer

Keraben Grupo

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Pamesa Group reported a pre-tax profit of EUR 114 million for 2024, marking a fivefold increase from the previous year. This profit accounted for 10.1% of revenues.

- February 2025: Tile of Spain (ASCER) launched the ‘Time of Spain’ initiative to unify collective and individual manufacturer promotions under one brand, concentrating efforts from February to March 2026 to enhance global visibility during key calendar periods.

- February 2025: Cevisama 2025 rebranded with a strong Made in Europe focus, showcasing 403 exhibitors with 96% from Europe. The event shifted towards the contract sector, featuring a Hotel Cevisama installation.

Spain Ceramic Tiles Market Report Scope

A complete background analysis of the spanish ceramic tiles market, which includes an assessment of the parental market, emerging trends in the segments and regional markets, and significant changes in market dynamics and market overview, is covered in the report. The report also offers a qualitative and quantitative assessment by analyzing data gathered from industry analysts and market participants across various key points in the value chain.

The Spanish ceramic tiles market is segmented by product, application, construction type, and end-user. By product, the market is sub-segmented into glazed, porcelain, scratch-free, and other products. By application, the market is sub-segmented into floor tiles, wall tiles, and other applications, By construction type, the market is sub-segmented into new construction, replacement, and renovation. By end-user, the market is sub-segmented into residential and construction. The report offers market size and forecasts for the Spain ceramic tiles market in value (USD) for all the above segments.

By Product Type

| Porcelain Tiles |

| Glazed Ceramic Tiles |

| Unglazed Ceramic Tiles |

| Mosaic Tiles |

| Others (Decorative, Patterned, Handmade) |

By Application

| Floor |

| Wall |

| Roofing |

By End-User

| Residential | |

| Commercial | Hospitality (Hotels, Resorts) |

| Retail Spaces | |

| Offices & Institutions | |

| Healthcare | |

| Educational Facilities | |

| Transport Hubs (Airports, Metro, Bus Terminals) | |

| Other Commercial Users |

By Construction Type

| New Construction |

| Renovation and Replacement |

By Distribution Channel

| Specialty Tile & Stone Stores |

| Home Improvement & DIY Stores |

| Online Retail |

| Direct Sales to Contractors |

By Geography

| Valencian Community |

| Catalonia |

| Andalusia |

| Madrid Region |

| Other Regions |

| By Product Type | Porcelain Tiles | |

| Glazed Ceramic Tiles | ||

| Unglazed Ceramic Tiles | ||

| Mosaic Tiles | ||

| Others (Decorative, Patterned, Handmade) | ||

| By Application | Floor | |

| Wall | ||

| Roofing | ||

| By End-User | Residential | |

| Commercial | Hospitality (Hotels, Resorts) | |

| Retail Spaces | ||

| Offices & Institutions | ||

| Healthcare | ||

| Educational Facilities | ||

| Transport Hubs (Airports, Metro, Bus Terminals) | ||

| Other Commercial Users | ||

| By Construction Type | New Construction | |

| Renovation and Replacement | ||

| By Distribution Channel | Specialty Tile & Stone Stores | |

| Home Improvement & DIY Stores | ||

| Online Retail | ||

| Direct Sales to Contractors | ||

| By Geography | Valencian Community | |

| Catalonia | ||

| Andalusia | ||

| Madrid Region | ||

| Other Regions | ||

Key Questions Answered in the Report

What is the current size and growth outlook for the Spain ceramic tiles market?

The Spain ceramic tiles market size was USD 1.31 billion in 2026 and is projected to reach USD 1.59 billion by 2031 at a 3.95% CAGR.

Which product type leads demand in Spain?

Porcelain led with a 68.14% share in 2025, supported by thin-gauge formats, EPD availability, and strong slip and fire performance for code-driven projects.

Where is growth fastest by geography within Spain?

The Madrid Region is the fastest-growing major area with a 4.74% CAGR outlook to 2031, helped by conversions and public procurement that favors low-embodied-carbon tiles.

Which end-user segment drives volume today?

Residential accounted for 60.70% in 2025 and is expected to lead growth due to hygiene preferences and energy-efficiency retrofits in aging homes.

How are regulatory trends shaping product choices?

CTE DB-SUA slip thresholds, and A1 fire requirements push specifications toward structured porcelain and ventilated ceramic façades with published EPDs.

What strategies help Spanish brands compete against low-cost imports?

Verified EPDs, thin-gauge porcelain, short-run digital customization, and modular façade systems help defend value and compress total installed cost in the Spain ceramic tiles market.

Page last updated on: