Southeast Asia Postal Service Market Size and Share

Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

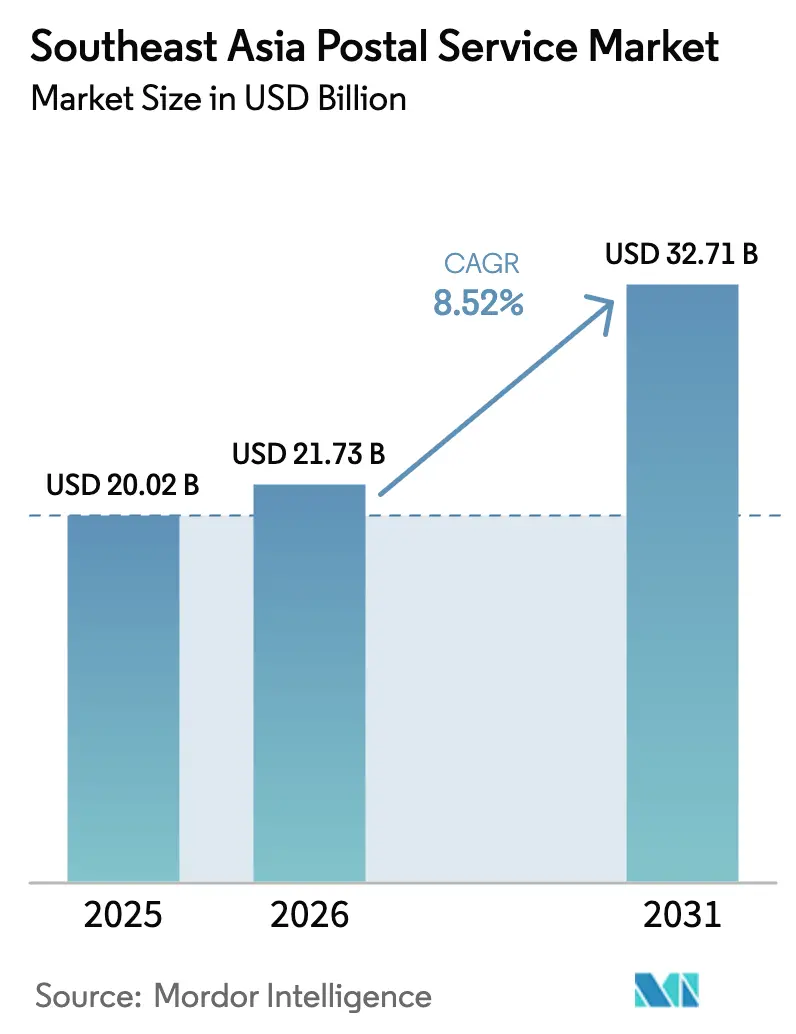

| Base Year Market Size (2025) | USD 20.02 Billion |

| Market Size (2026) | USD 21.73 Billion |

| Market Size (2031) | USD 32.71 Billion |

| Growth Rate (2026 - 2031) | 8.52% CAGR |

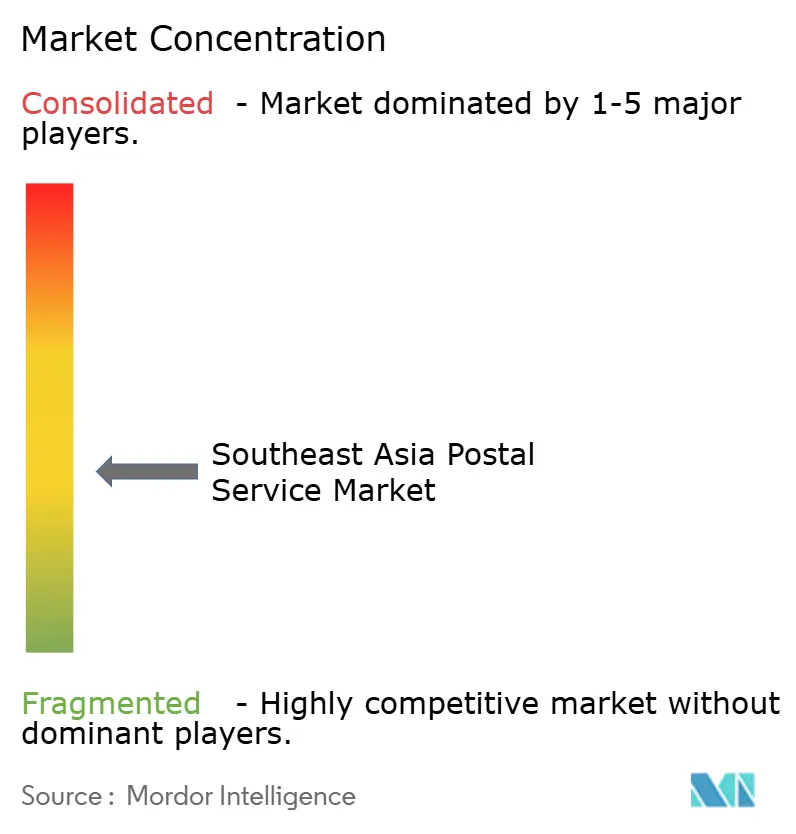

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Postal Service Market Analysis by Mordor Intelligence

The Southeast Asia Postal Service Market size market is expected to grow from USD 20.02 billion in 2025 to USD 21.73 billion in 2026 and is forecast to reach USD 32.71 billion by 2031 at 8.52% CAGR over 2026-2031.

Surging e-commerce volumes are propelling parcel demand and nudging operators toward faster, technology-enabled delivery models. Digital-payment uptake is trimming cash-on-delivery frictions, freeing cash flow and reducing costly return trips. Venture-backed express specialists are pressuring prices, prompting incumbents to automate sortation hubs and form strategic alliances to protect margins. Government-led modernization programs and improved customs processes are unlocking cross-border opportunities, yet archipelagic infrastructure gaps in Indonesia and the Philippines continue to inflate last-mile costs.

Key Report Takeaways

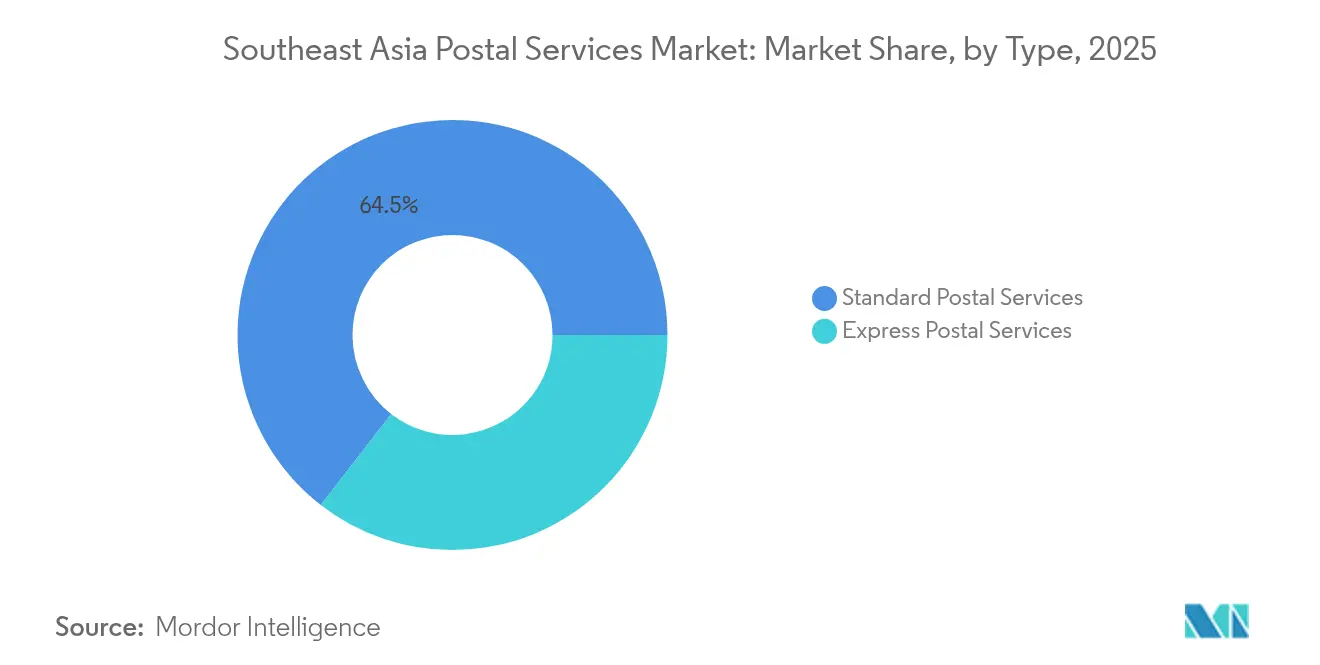

- By service type, express postal services captured 35.50% revenue share in 2025, while traditional mail remained dominant; express is forecast to expand at an 7.03% CAGR through 2031.

- By item, parcels accounted for 56.20% of the Southeast Asia postal service market size in 2025 and are advancing at a 8.27% CAGR to 2031.

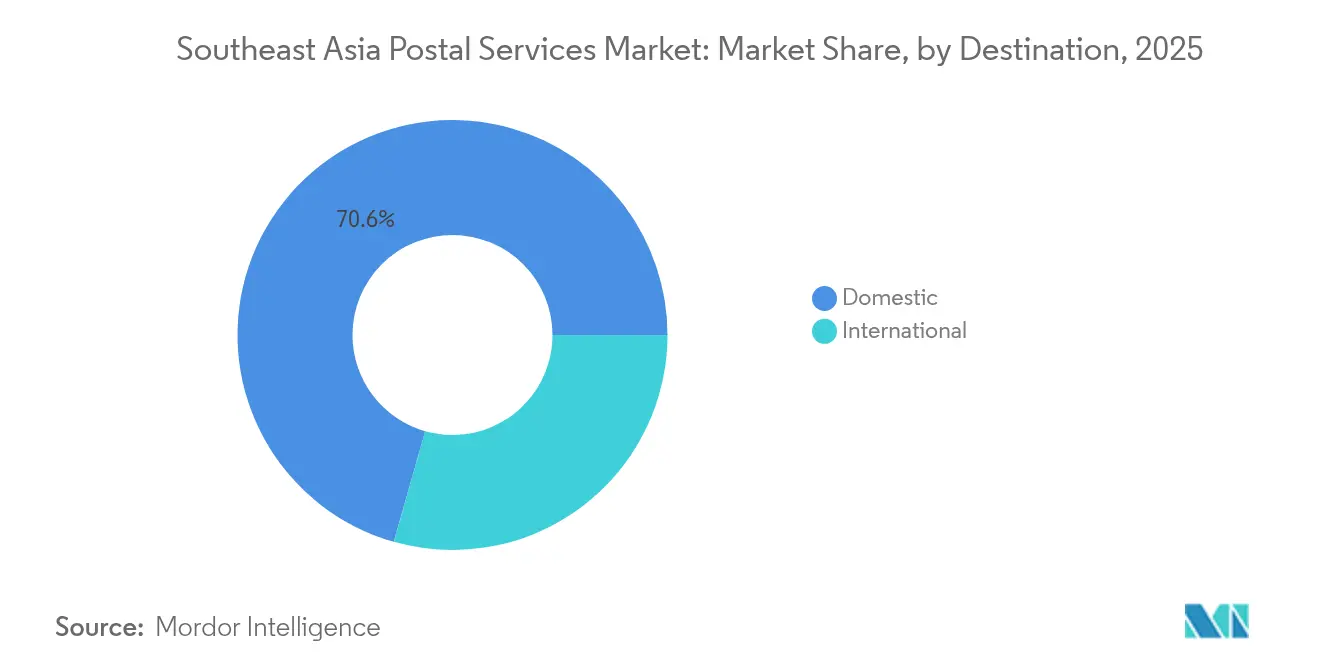

- By destination, domestic services held 70.60% revenue share in 2025, whereas international services are set to post the fastest 7.66% CAGR between 2026 and 2031.

- By end-user, the B2C segment led with 50.40% of 2025 revenue; the C2C segment shows the strongest outlook with a 9.36% CAGR through 2031.

- By delivery mode, road transport commanded 55.30% share in 2025, while air freight is projected to grow at a 8.74% CAGR over the forecast period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Postal Service Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Exploding e-commerce parcel volumes | +2.3% | Indonesia, Vietnam | Medium term (2-4 years) |

| Government logistics-modernization programs | +1.8% | ASEAN core markets | Long term (≥ 4 years) |

| Same- and next-day delivery expectations | +1.5% | Tier-1 cities | Short term (≤ 2 years) |

| Digital payment and BNPL expansion | +1.2% | Regional | Medium term (2-4 years) |

| Social-commerce micro-parcels | +0.9% | Rural Indonesia & Philippines | Medium term (2-4 years) |

| Automation & sorting-hub upgrades | +1.1% | Singapore, Malaysia, Vietnam | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Exploding E-commerce Parcel Volumes in Indonesia & Vietnam

E-commerce marketplaces, digital-first SMEs, and social-commerce sellers are generating record parcel throughput, compelling postal operators to expand line-haul capacity, deploy micro-fulfillment centers, and introduce predictive delivery tools. Indonesia’s population scale and Vietnam’s double-digit online-retail growth underpin recurring surges in parcel pickups that frequently exceed seasonal peaks. Operators such as Viettel Post have responded by nearly doubling sortation capacity and adding flexible line-haul schedules that match flash-sale spikes. Collaborative programs with leading platforms further integrate order-management data into postal routing engines, trimming failed deliveries and raising first-attempt success rates.

Government Logistics-Modernization Programs Across ASEAN

Cross-government initiatives—most notably the ASEAN Digital Masterplan 2025—are harmonizing customs protocols, piloting blockchain-based track-and-trace, and standardizing data interfaces across national postal gateways[1]ASEAN, “Master Plan on ASEAN Connectivity 2025,” asean.org. Vietnam’s postal development strategy targets 30% revenue growth for e-commerce delivery, while Indonesia’s national logistics ecosystem blueprint emphasizes public-private investment in multimodal corridors. These frameworks accelerate capital deployment into automated hubs and cross-border transit systems, reducing clearance times and creating predictable service-level standards.

Surge in Same- & Next-Day Delivery Expectations in Tier-1 Cities

Urban consumers in Singapore, Kuala Lumpur, Bangkok, and Jakarta increasingly treat next-day delivery and real-time visibility as default requirements. Start-ups deploy AI-driven route optimization, predictive traffic analytics, and urban micro-hubs to achieve sub-24-hour targets, prompting national posts to partner with food-delivery fleets during off-peak hours for parcel drop-offs. Service premiums enable operators to offset higher urban labor and property costs while sustaining higher revenue per parcel.

Digital Payment & BNPL Uptake Reducing COD Friction

Regional e-wallet penetration is shrinking the portion of cash-on-delivery orders, lowering reverse-logistics volumes and cutting cash-handling expenses. Payment ecosystems backed by leading banks now embed one-click checkout and escrow release on delivery confirmation, enabling postal operators to integrate payment status into dynamic routing. Pos Indonesia’s partnership with AWS leverages cloud architectures to reconcile digital payments instantly and automate COD reconciliation. As e-wallet adoption widens in rural provinces, operators expect a material improvement in cashflow predictability.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Archipelagic last-mile infrastructure gaps | -1.7% | Indonesia, Philippines | Long term (≥ 4 years) |

| SOE-centric regulations | -1.2% | Indonesia, Vietnam, Thailand | Medium term (2-4 years) |

| High cash-on-delivery share | -0.9% | Vietnam, Indonesia | Short term (≤ 2 years) |

| Margin compression from venture-backed entrants | -1.3% | Region-wide | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Archipelagic Last-Mile Infrastructure Gaps Inflating Costs

Multiple trans-shipment legs, limited roll-on-roll-off capacity, and inconsistent port schedules raise handling fees and extend delivery lead-times to outlying islands. Indonesia’s logistics costs equal 27% of GDP—far above continental peers—forcing operators to price a premium for remote destinations. Postal fleets mitigate by using coastal shipping, community agents, and drone pilots on sparsely populated islands, yet throughput variability still depresses network utilization and overall profit margins.

SOE-Centric Regulations Limiting Private Investment

Preferential route allocations, exclusive mailbox access, and differentiated licensing fees reinforce incumbent state-owned operator positions and dissuade capital inflows. The OECD’s competition review of Indonesian small-package delivery identified 19 regulatory obstacles that shield Pos Indonesia from full competition. Vietnam has begun loosening ownership caps, but procedural hurdles in customs and last-mile franchising still slow private entrant expansion.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Express Services Outpace Traditional Mail

Express services equating to 35.50% of overall revenue and rising at a 7.03% CAGR toward 2031, powered by marketplace flash-sales and merchant demand for speed guarantees. The Southeast Asia postal service market has high-frequency shoppers accept incremental premiums for next-day fulfillment. Automation investments, track-and-trace APIs, and cross-docking hubs position express specialists to scale sustainably while maintaining sub-48-hour regional coverage.

Traditional mail yet faces secular volume erosion as digital billing and e-government portals gain traction. Operators preserve relevance by bundling hybrid mail digital letter generation with physical confirmation and by leveraging extensive post-office networks for identity services, bill payment, and micro-finance. Cost restructuring programs shift daylight resources to parcels while nighttime sorting windows accommodate residual letter flow, preserving universal-service obligations without compromising speed expectations of the broader Southeast Asia postal service market.

By Item: Parcels Dominate Amid E-commerce Boom

Parcels commanded 56.20% of 2025 revenue and are expanding at 8.27% CAGR, reflecting the core engine of the Southeast Asia postal service market. E-commerce holiday events such as 11.11 and Ramadan sales funnel millions of parcels daily into the cross-border network, prompting operators to stagger pickup windows, enforce volumetric weight billing, and deploy predictive hub re-routing. Letters and printed matter continue to decline but remain essential for regulated financial statements and exam papers, guaranteeing baseline network utilization for the Southeast Asia postal service market.

Smaller micro-parcel formats generated by social-commerce transactions require high-density aggregation to remain profitable. J&T Express’ small-parcel optimization program demonstrated a 31% volume surge after introducing flexible pouch packaging thresholds, indicating latent demand in underserved rural clusters.

By Destination: Cross-Border Commerce Accelerates Growth

International services are tracking an 7.66% CAGR through 2031 as MSME exporters leverage online storefronts. The Southeast Asia postal service market size attributed to cross-border flows is approaching USD 5.93 billion, supported by the ASEAN Customs Transit System’s single-declaration model. Duty-paid upfront services and landed-cost calculators embedded into checkout reduce final-mile delays.

Domestic deliveries remain crucial, driven by cash-cycle dynamics and localized on-demand grocery platforms. Tier-two provincial capitals benefit from hub-and-spoke expansions, yet the Southeast Asia postal service market share of domestic volume is gradually ceded to international shipments as regional trade barriers fall.

By End-User: C2C Emerges as Growth Leader

B2C retained a 50.40% share of 2025 revenue, underpinned by mega-marketplaces that anchor predictable daily parcel waves. The Southeast Asia postal service market increasingly segments B2C pricing by weight bands and delivery-speed tiers to manage capacity. C2C volumes are accelerating at a 9.36% CAGR as social-commerce sellers distribute beauty, fashion, and thrift goods nationwide. Community drop-points, simplified onboarding apps, and instant payout options incentivize casual sellers to remain loyal to postal networks.

B2B deliveries—insurance policies, pharmaceuticals, and bank cheques—provide steady contract revenue, albeit at lower growth. Viettel Post’s dedicated B2B solutions for financial clients achieved 2.4 × market average growth, demonstrating potential for niche-specific products.

Geography Analysis

Indonesia led the Southeast Asia postal service market with 34.05% share in 2025. Pos Indonesia’s modern-cloud rollout with AWS is digitizing 4,800 post offices, enabling API-based service extensions for fintech partners. Regulatory liberalization remains gradual; the OECD highlighted 19 hurdles curbing private competition, yet foreign entrants partnering under asset-light models continue to penetrate high-density urban corridors. High logistics-to-GDP ratios underscore an urgent need for multimodal corridor upgrades if Indonesia is to sustain parcel-volume growth.

Vietnam is the fastest-growing market, forecast at a 11.84% CAGR. Postal service revenue topped 71 trillion VND in 2024, up 21% year-on-year, reflecting successful digital-first service rollouts and rapid SME onboarding. Viettel Post and Vietnam Post are scaling automated hubs and augmenting rural pickup networks to capture surging C2C transactions. The national 2IPD rank leap from 46th to 31st signals tangible improvements in service quality.

Thailand, Malaysia, and the Philippines post mid-single-digit growth. Thailand’s easing macro backdrop and Lazada’s USD 200 million sortation mega-hub are raising throughput readiness, while Malaysia harnesses Kuala Lumpur’s free-trade zone status for regional transshipment. The Philippines contends with archipelagic cost drag yet benefits from lifting foreign-equity caps in logistics, encouraging platform entrants to invest in automated coastal distribution nodes.

Singapore serves as the region’s innovation testbed; SingPost’s portfolio of 14 markets and its Regional eCommerce Logistics Hub anchor API-driven cross-border products. Emerging markets—Cambodia, Laos, Myanmar, and Brunei—remain small but attractive for future growth, supported by ASEAN-funded digital-trade facilitation grants.

Competitive Landscape

Competition spans state-owned incumbents, venture-funded express specialists, and integrated airline-led logistics platforms. J&T Express retained 25.4% regional parcel share in 2024, leveraging scale economies and sub-USD 0.70 unit costs. Ninja Van’s USD 50 million automation program targets 50% productivity gains to defend second position. Viettel Post is accelerating B2B vertical penetration, while SingPost positions as the cross-border orchestrator leveraging Singapore’s bonded warehousing.

Strategic collaboration shapes the market: Pos Indonesia bundles cloud analytics via AWS; Teleport aligns with 30 airlines for belly-hold capacity; and Cainiao’s robotic hub offers plug-in fulfillment to third-party sellers. White-space opportunities persist in cold-chain logistics and returns-management platforms, while high compliance costs and cash-cycle risks deter pure-play newcomers. Consolidation trends point toward joint ventures between national posts and express upstarts, balancing network reach with technology agility within the Southeast Asia postal service market.

Southeast Asia Postal Service Industry Leaders

DHL Express

UPS

FedEx

Singapore Post Limited

Ninja Van

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: Vietnam Post and Hoàng Hà Mobile formed a distribution partnership to extend device availability nationwide and bolster online sales

- April 2025: Viettel Post reported delivery-segment growth 2.4 × the market average and unveiled plans for sector-specific B2B solutions.

- April 2025: Teleport set a goal to deliver 2 million parcels daily via a hybrid mid-mile belly network.

- March 2025: Cainiao opened southern Vietnam’s largest automated sorting center, achieving 99% accuracy through robotics.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Mordor Intelligence defines the Southeast Asia postal service market as the total revenue earned by designated national postal operators and licensed private couriers from the collection, transport, and delivery of addressed letters, documents, and parcels weighing up to 70 kg across Indonesia, Thailand, Vietnam, the Philippines, Malaysia, Singapore, Cambodia, Myanmar, Laos, and Brunei.

Scope exclusion: bulk freight forwarding, 3PL warehousing, and shipments above 70 kg are not counted.

Segmentation Overview

- By Type

- Standard Postal Services

- Express Postal Services

- By Item

- Letters

- Parcels

- By Destination

- Domestic

- International

- By End-User

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Consumer-to-Consumer (C2C)

- By Delivery Mode

- Road

- Air

- Sea

- Rail

- By Country

- Indonesia

- Thailand

- Vietnam

- Philippines

- Malaysia

- Singapore

- Cambodia

- Myanmar

- Laos

- Brunei Darussalam

Detailed Research Methodology and Data Validation

Primary Research

Structured interviews with executives from postal authorities, private courier managers, large e-retailers, and last-mile tech vendors across Jakarta, Bangkok, Ho Chi Minh City, Manila, and Kuala Lumpur allow us to confirm service mix shares, price resets, and cross-border traffic ratios. Targeted surveys of frequent online shoppers and SME shippers further test adoption and satisfaction assumptions.

Desk Research

Our analysts first assemble macro and industry data from public sources such as the Universal Postal Union, ASEANstats, each country's postal regulator, customs trade dashboards, and e-commerce association releases. Company filings, investor presentations, and reputed business press help us benchmark operator revenues and capital spend. Paid datasets from D&B Hoovers and Volza provide cross-checks on firm-level sales and shipment flows. These publicly listed references illustrate the breadth of inputs; several additional sources are reviewed to validate numbers and clarify assumptions.

A second pass harvests granular indicators, parcel volumes, average revenue per item, delivery success rates, and urban population shifts from national statistical agencies, World Bank LPI tables, and Patent databases like Questel for automation roll-outs, thereby sharpening growth drivers.

Market-Sizing & Forecasting

A top-down model starts with reported operator revenues, adjusts for unreported private courier turnover using parcel volume multipliers, and re-casts figures into constant currency. Select bottom-up checks, sampled average selling price times parcel counts for leading carriers, are layered in to reconcile gaps. Key variables modeled include e-commerce GMV growth, average parcels per online order, domestic-international shipment mix, fuel cost pass-through, and regulatory tariff caps. Multivariate regression links these drivers to historic revenue, while scenario analysis covers fuel price and cross-border policy swings. Where operator disclosures are partial, conservative imputation guided by primary interviews fills the void before final triangulation.

Data Validation & Update Cycle

Draft outputs pass anomaly screens, peer review, and senior analyst sign-off. Models refresh annually; material events, new postal acts, large M&A, or double-digit fuel spikes trigger interim updates. A last validation lap is run just prior to client delivery so users receive the latest view.

Why Mordor's Southeast Asia Postal Service Baseline Remains Dependable

Published estimates often diverge because firms choose different service baskets, base years, and currency treatments.

Key gap drivers in this market include whether private couriers are counted, if cross-border parcel revenues are allocated to origin or destination, and the cadence of exchange rate resets. Mordor reports the full 10-country region, applies constant currency conversion at the mid-year IMF rate, and refreshes annually, whereas some publications extrapolate from single-country samples or roll forward older exchange rates.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| USD 20.02 B (2025) | Mordor Intelligence | - |

| USD 18.43 B (2024) | Global Consultancy A | Omits Cambodia, Laos, Brunei; uses mixed 2023 FX rates |

| USD 4.20 B (2025) | Trade Journal B | Counts only letter mail; excludes private couriers and e-commerce parcels |

The comparison shows that methodological scope and currency handling explain most discrepancies. By grounding its baseline in transparent variables and repeatable steps, Mordor Intelligence delivers a balanced, decision-ready figure that clients can track with confidence.

Key Questions Answered in the Report

What is the current size of the Southeast Asia postal service market?

The market is valued at USD 21.73 billion in 2026 and is projected to reach USD 32.71 billion by 2031.

Which country holds the largest share of the Southeast Asia postal service market?

Indonesia leads with 34.05% revenue share in 2025, supported by its large consumer base and expanding digital economy.

What segment is growing fastest within the market?

The C2C segment is forecast to expand at a 9.36% CAGR from 2026 to 2031, driven by social-commerce activity.

How are postal operators addressing high cash-on-delivery rates?

Operators integrate e-wallet payments, pre-delivery confirmations, and partial upfront deposits to reduce COD-related return costs.

Why is air freight important for the region’s postal services?

Air freight supports expedited cross-border deliveries, growing at a 8.74% CAGR as retailers increasingly promise two-day regional shipping.

What role do government programs play in the market’s outlook?

Initiatives under the ASEAN Digital Masterplan 2025 and national logistics strategies modernize infrastructure, streamline customs, and attract private investment, adding up to 1.8% to forecast CAGR growth.

Page last updated on: