Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Base Year Market Size (2025) | USD 87.88 Billion |

| Market Size (2026) | USD 88.8 Billion |

| Market Size (2031) | USD 93.56 Billion |

| Growth Rate (2026 - 2031) | 1.05% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

North America Postal Services Market Analysis by Mordor Intelligence

North America Postal Services Market size market size in 2026 is estimated at USD 88.8 billion, growing from 2025 value of USD 87.88 billion with 2031 projections showing USD 93.56 billion, growing at 1.05% CAGR over 2026-2031.

Growth appears modest, yet the numbers hide sweeping structural change. Traditional First-Class Mail volumes continue to fall, while parcels have become the revenue engine as e-commerce deepens its hold on consumer behaviour. Major operators are modernising processing assets, electrifying fleets, and integrating digital APIs to improve service reliability and cost control. Competition is intensifying because Amazon Logistics has leap-frogged UPS in parcel volume, regional couriers are widening geographic reach, and crowdsourced delivery networks are moving into niche routes. These forces are encouraging postal incumbents to rework pricing, route density, and partner ecosystems to defend share. At the same time, near-shoring in Mexico, sustainability mandates in several U.S. states, and targeted capacity additions at Canadian hubs are reshaping the profit map across the region.

Key Report Takeaways

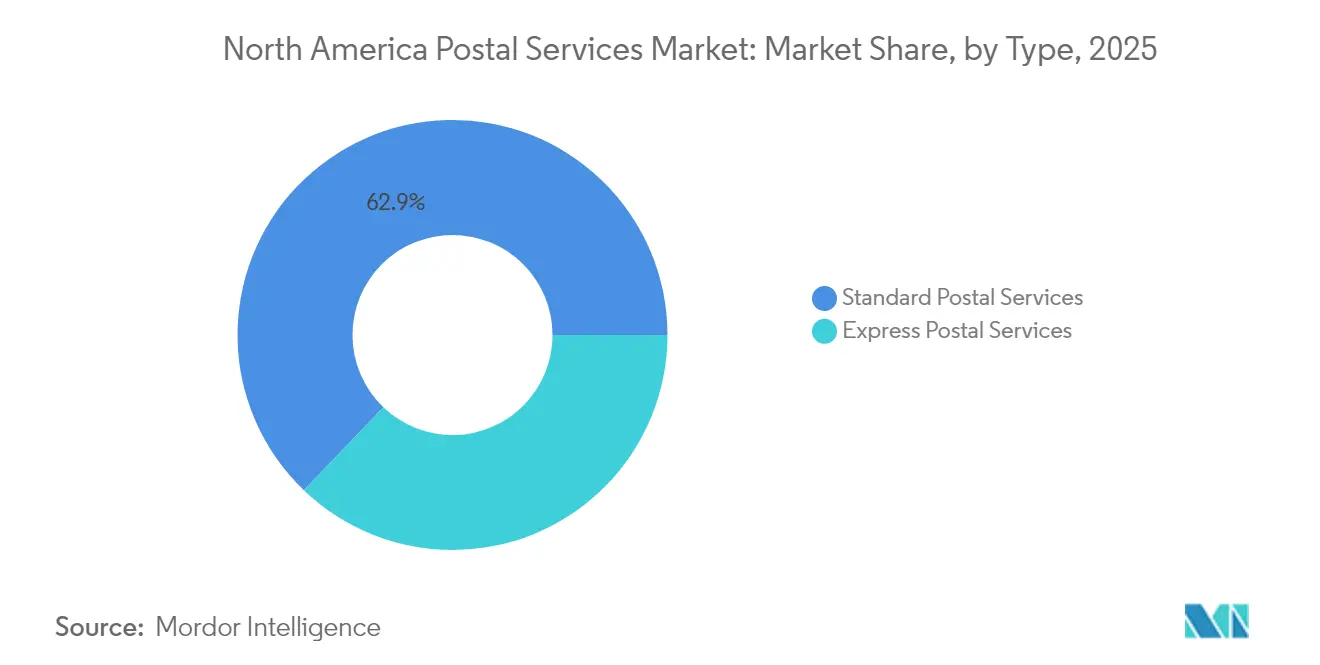

- By type, standard postal services claimed 62.85% of the North America postal services market share in 2025, while express services are forecast to grow the fastest at a 3.55% CAGR through 2031.

- By item, parcels led with 58.05% of the North America postal services market size in 2025; letter mail continues to contract, but parcels are projected to expand at a 3.65% CAGR to 2031.

- By destination, domestic services accounted for 80.65% share of the North America postal services market size in 2025, whereas international services are set to rise at a 3.55% CAGR during 2026-2031.

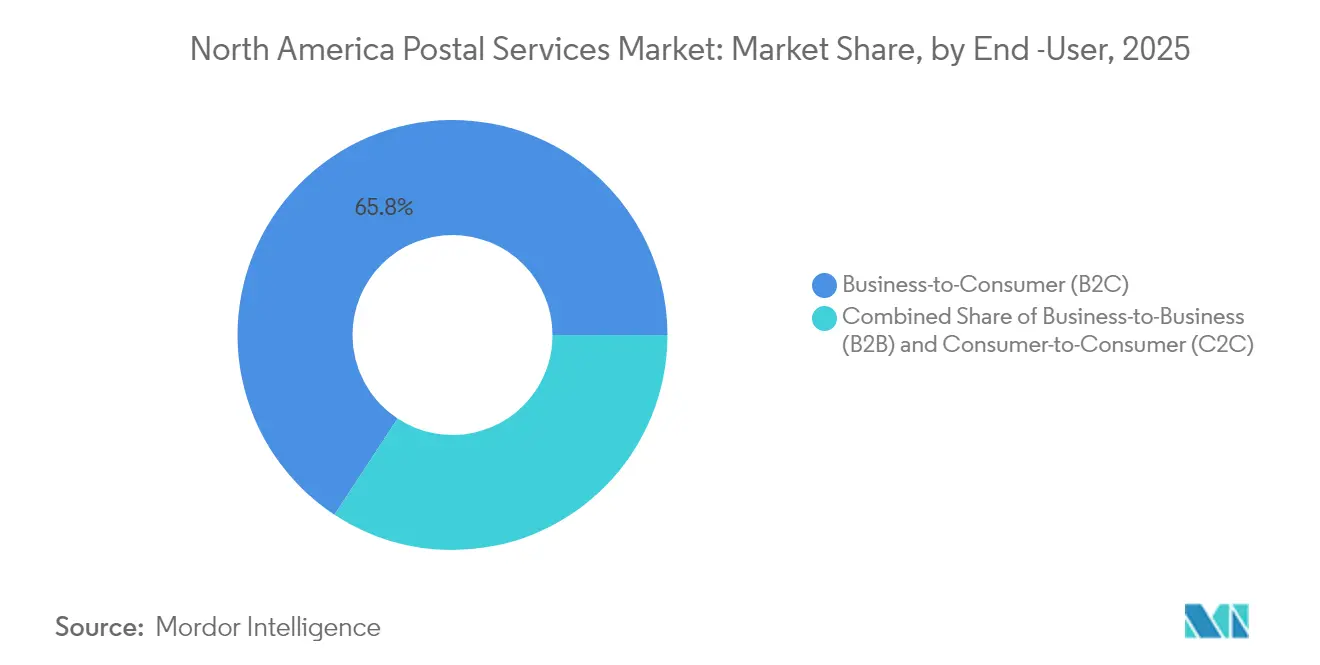

- By end-user, the B2C segment held 65.75% revenue share in 2025, while the C2C segment exhibits the highest projected CAGR at 4.1% to 2031.

- By delivery mode, road transport dominated with 72.05% share of the North America postal services market size in 2025; air transport shows the quickest expansion at a 2.95% CAGR over the forecast window.

- By geography, the United States represented 85.80% of the North America postal services market share in 2025, whereas Mexico is expected to post the fastest regional CAGR of 3.05% between 2026 and 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

North America Postal Services Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| E-commerce parcel volume boom driven by same-day delivery demands | +0.6% | United States, Canada, Mexico | Medium term (2-4 years) |

| SMB adoption of hybrid mail & fulfilment APIs | +0.3% | United States, spillover to Canada | Medium term (2-4 years) |

| U.S. Postal Service network modernization | +0.4% | United States | Long term (≥ 4 years) |

| Canada Post parcel expansion hubs | +0.2% | Canada, U.S. border regions | Medium term (2-4 years) |

| Mexico logistics-park near-shoring surge | +0.3% | Mexico, U.S. border states | Long term (≥ 4 years) |

| State-level sustainability mandates accelerating fleet electrification | +0.1% | California, New York, Massachusetts | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

E-commerce Parcel Volume Boom Driven by Same-Day Delivery Demands

Parcel traffic reached 21.7 billion pieces in the United States during 2023 and is projected to climb toward 29 billion by 2029, adding pressure on postal operators to prioritise parcel capacity over letter routes. Operators are now favouring predictable two-to-three-day windows over ultra-fast promises because reliability has become the key buying criterion for online shoppers. USPS upgraded seasonal processing to about 60 million parcels per day for the 2024 holiday peak, reflecting a permanent shift toward parcel-centric networks.

SMB Adoption of Hybrid Mail & Fulfilment APIs in the United States

Small and midsize businesses now contribute 28.9% of total U.S. postal volume, catalysed by easy-to-integrate shipping APIs offered by USPS and private carriers. Web Tools updates released during 2024 add end-to-end tracking and harmonised customs data, enabling even micro-merchants to print compliant labels directly from e-commerce dashboards. This digital bridge is democratising enterprise-grade logistics capabilities and sustaining higher-margin traffic across the network.

U.S. Postal Service's Network Modernization Increasing Processing Capacity

The USD 40 billion “Delivering for America” roadmap earmarks USD 17.3 billion for replacing legacy plants with regional processing and distribution centres and over 60 sorting and delivery centres[1]United States Postal Service, “Delivering for America Plan,” usps.com. By consolidating mail flow, the plan should lift daily parcel handling capacity from 47 million to 77 million by 2030. Despite regulatory concerns about service downgrades for rural areas, USPS expects annual cost savings of roughly USD 3.6-3.7 billion and improved on-time scores[2]Postal Regulatory Commission, “Advisory Opinion on Network Consolidation,” prc.gov.

Canada Post's Parcel Expansion Hubs Enhancing Cross-Border Reach

Canada Post opened the Albert Jackson Processing Centre in Toronto with 1 million-parcel daily throughput and is enlarging the Pacific Processing Centre at Vancouver International Airport to reinforce service to Asia-Pacific lanes. Both sites meet the Canada Green Building Council’s Zero-Carbon standard, signalling a dual focus on capacity and sustainability. The move is vital as the operator’s market share slid to 29% in 2024 after a prolonged strike.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| First-Class Mail volume decline from digital substitution in U.S. government agencies | -0.5% | United States | Long term (≥ 4 years) |

| Chronic labor shortages & rising union wage pressures | -0.3% | United States, Canada | Medium term (2-4 years) |

| Airport & border capacity bottlenecks | -0.2% | U.S.-Canada & U.S.-Mexico borders | Short term (≤ 2 years) |

| Mexican rural addressing gaps increasing last-mile costs | -0.1% | Mexico | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

First-Class Mail Volume Decline from Digital Substitution in U.S. Government Agencies

First-Class Mail fell by 50% between FY 2008 and FY 2023, eroding one of USPS’s most profitable revenue streams. Government bodies that once mailed tax notices and benefits statements are now defaulting to digital delivery, deepening revenue pressure. Even with higher parcel income, USPS posted a USD 6.5 billion net loss in FY 2023, and further declines in physical correspondence threaten funding for universal-service mandates.

Chronic Labor Shortages & Rising Union Wage Pressures at National Posts

A 32-day Canada Post strike in late 2024 snarled holiday deliveries and pushed several retailers to switch carriers, magnifying the corporation’s quarterly loss to USD 315 million before tax. Contract talks remain tense, with another walkout possible in 2025. In the United States, letter carrier wage discussions are also proving complex, underscoring workforce fragility in a tight labour market

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Express Services Outpace Standard Mail

Express services recorded a 3.55% CAGR for 2026-2031, surpassing overall market momentum. The benefits from premium pricing as businesses pay for predictable arrival windows. Continuous Producer Price Index gains for couriers confirm sustained demand, and major operators bolster time-definite lanes with later cut-offs and earlier clearances.

Standard services, although covering the broadest addressable base, wrestle with secular mail decline. Yet they still commanded 62.85% of the North America postal services market share in 2025 due to universal-service obligations that entrench nationwide delivery networks. USPS is recalibrating standards so 75% of First-Class Mail maintains a 1-5-day window and 14% gains faster service, aligning commitments with real-world transport flows.

By Item: Parcels Dominate Amid Letter Decline

Parcels held 58.05% share in 2025, generating the lion’s share of revenue for the North America postal services market. Operators expanded mechanised sortation and shifted labour from letter plants to parcel lanes, enabling single-piece handling rates as low as 20 seconds per unit during peak periods. The North America postal services market size tied to parcel business is forecast to grow at 3.65% CAGR on the back of expanding e-commerce categories such as oversized home goods and temperature-controlled groceries.

Letter volumes, in contrast, continue their downtrend. Between 2008 and 2023, First-Class Mail halved, and the North America postal services market share for letters slipped accordingly. Still, legal documents, voter materials, and direct-mail marketing keep a rump demand that supports selective investments in high-speed letter sorting technology meant to safeguard remaining profitability.

By Destination: International Shipments Outpace Domestic Growth

Domestic traffic retained an 80.65% hold over the North America postal services market in 2025, serving 167 million U.S. addresses and millions more in Canada and Mexico every delivery day. High fixed-route density aids cost absorption, and operators layer parcels atop mail rounds to maximise last-mile productivity.

International services, though smaller, exhibit a 3.55% CAGR because of cross-border e-commerce and near-shoring tailwinds. Harmonised customs codes, electronic advance data, and new trade configurations under USMCA spur volume even as tariff shifts create temporary volatility. USPS revised customs forms in April 2024, mandating HS codes to accelerate clearance in 30+ nations, improving customer satisfaction scores on outbound parcels.

By End-User: C2C Segment Shows Surprising Strength

C2C consignments, driven by peer-to-peer resale platforms and social-commerce gifting, are forecast to grow 4.1% annually to 2031. Lightweight parcels, prepaid return labels, and kiosk drop-offs fuel the segment’s low-touch model. Meanwhile, B2C retains 65.75% share of the North America postal services market thanks to large-scale retail operations shipping daily to urban and rural addresses alike.

B2B flows remain essential for warranty parts, financial documentation, and regulated samples. Nevertheless, their growth has tempered as enterprises adopt digital document workflows. Operators advertise chain-of-custody tracking and dedicated account teams to keep B2B churn low, especially in medical devices and aerospace verticals that still prize paper originals.

By Delivery Mode: Air Transport Gains Altitude

Road networks dominate with 72.05% share, offering the only economically viable option for dense last-mile distribution across sprawling suburbia. Fleet electrification, improved telematics, and unified sort-to-route models are expected to sustain road’s central role. The North America postal services market size linked to road modes is projected to inch along near the headline CAGR.

Air transport, however, charts a 2.95% CAGR, its role amplified by cross-border priority parcels and return-to-origin logistics for high-value goods. UPS now lifts most USPS air consignments, integrating postal volumes into its own cargo aircraft schedules for higher load factors. Capacity expansions at secondary airports and automated air-freight sorters will help carriers meet two-day national delivery promises even into remote ZIP codes.

Geography Analysis

The United States anchors the North America postal services market with 85.80% share in 2025. USPS alone handled 6.6 billion parcels last year, yet its revenue share was only 16% because private couriers charge higher average yields. The agency’s USD 40 billion transformation plan seeks to reverse negative cash flow through processing consolidation, fleet modernisation, and broader parcel pricing tiers. Amazon Logistics surpassed UPS by delivering 5.9 billion parcels in 2024, illustrating the groundswell of in-house retailer networks.

Canada faces mounting margin pressure as labour unrest and new entrants dilute Canada Post’s foothold. Market share slipped to 29% in 2024, down from 62% pre-pandemic, after a 32-day strike pushed shippers toward Purolator, FedEx, and regional specialists. In response, the Crown corporation is pouring capital into low-carbon hubs, robotic sorters, and parcel lockers to reclaim customer confidence.

Mexico shows the fastest expansion, with a 3.05% CAGR driven by near-shoring and industrial park buildouts. Cross-border flows benefit from USMCA incentives, though rural address deficits inflate last-mile costs. Niche providers have launched geocoding apps that assign plus-codes to unnumbered dwellings, bridging the gap and unlocking growth in interior states tied to manufacturing ecosystems.

Competitive Landscape

Competition in the North America postal services market is fragmenting as nimble players capture route niches. Amazon Logistics, USPS, UPS, FedEx, Purolator, and regional couriers such as LSO and Dicom now contest volume and mindshare. USPS still leads on total pieces moved, but Amazon’s integrated retail-to-doorway chain gives it an agility edge for same-day metropolitan service.

Strategic investment is centred on automation and electrification. USPS will add 106,000 new delivery vehicles by 2028, including at least 66,000 EVs uspsoig.gov. UPS has converted Atlanta and Louisville ground hubs to RFID-based parcel tracking, lifting sort accuracy above 99.5%. Canada Post’s air-cargo alliance with Cargojet expands transborder overnight capacity, countering growth from DHL and GLS.

Technology partnerships are multiplying. Pitney Bowes released ShipAccel, enabling desktop label generation and multi-carrier rating for SMBs. FedEx is piloting AI-driven dynamic route planning in 12 U.S. cities to shave fuel and overtime. These moves signal a pivot from asset-heavy models to platform-enabled ecosystems that monetise data and orchestration as much as physical carriage.

North America Postal Services Industry Leaders

USPS

Canada Post Corporation

UPS

DHL

FedEx

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- May 2025: DHL Supply Chain acquired IDS Fulfillment, adding 1.3 million sq ft of U.S. warehouse capacity to deepen e-commerce logistics for SMB customers.

- May 2025: USPS announced two-phase service-standard adjustments starting April 1 and July 1 2025 aimed at rural reliability, with projected annual savings of USD 3.6-3.7 billion.

- October 2024: USPS unveiled its first production model Next Generation Delivery Vehicle, signalling the start of multi-year deployment of low-emission trucks.

- April 2024: Canada Post detailed plans to expand its Pacific Processing Centre at Vancouver International Airport with net-zero design features.

Research Methodology Framework and Report Scope

Market Definitions and Key Coverage

Our study defines the North America postal services market as the total annual revenue earned by national-designated operators and licensed private carriers for collecting, processing, transporting, and delivering letter mail and parcels weighing up to 70 lbs across the United States, Canada, and Mexico. Revenue from ancillary retail products, financial services, air-freight forwarding, and third-party logistics is excluded.

Philatelic sales, freight shipments above 70 lbs, and non-regulated locker networks fall outside our market boundary.

Segmentation Overview

- By Type

- Standard Postal Services

- Express Postal Services

- By Item

- Letters

- Parcels

- By Destination

- Domestic

- International

- By End-User

- Business-to-Business (B2B)

- Business-to-Consumer (B2C)

- Consumer-to-Consumer (C2C)

- By Delivery Mode

- Road

- Air

- Sea

- Rail

- By Country

- United States

- Canada

- Mexico

Detailed Research Methodology and Data Validation

Primary Research

Mordor analysts interviewed executives from designated posts, regional parcel carriers, and high-volume e-commerce merchants across all three countries. Discussions explored average revenue per piece, network automation plans, and the impact of fleet electrification mandates, which refined cost curves and validated model assumptions.

Desk Research

We began with postal reports from the Universal Postal Union, the U.S. Postal Service Office of Inspector General, Statistics Canada's postal indicators, and Mexico's Instituto Federal de Telecomunicaciones, which provide baseline volumes, service standards, and tariff histories. Macroeconomic inputs, such as U.S. Census quarterly e-commerce sales, OECD retail trade indices, and the Bureau of Labor Statistics diesel price index, anchor demand and cost drivers. Annual reports and Form 10-Ks offer operator-level revenue splits, while customs shipment data accessed through D&B Hoovers and Volza help map cross-border flows. This list is illustrative; many other open and subscription sources supported data collection, validation, and clarification.

Market-Sizing & Forecasting

A top-down reconstruction of revenue uses reported mail and parcel pieces multiplied by blended average postage or contract rates, which are then adjusted for share captured by licensed private carriers. Select bottom-up checks, carrier roll-ups and sampled contract rates, cross-validate totals. Key variables include first-class mail volume erosion, parcel pieces per online order, USPS consumer price index-linked rate caps, e-commerce retail sales growth, fleet electrification capital outlay, and diesel fuel inflation. A multivariate regression projects each variable through 2030, after which scenario analysis stress-tests high-fuel and low-mail cases. Gaps in operator disclosures are bridged using three-year moving averages or nearest-neighbor benchmarks.

Data Validation & Update Cycle

Outputs pass a three-layer review: variance checks against external series, peer review by senior analysts, and final sign-off before publication. Reports refresh annually, with interim updates triggered by material events such as postage rate revisions or significant e-commerce surges.

Why Mordor's North America Postal Services Baseline Stands Out

Published market figures often diverge because firms pick dissimilar service mixes, apply different average rate assumptions, or freeze models for years.

Key gap drivers include varying treatment of private parcel revenue, differing mail-to-parcel price elasticities, and cadence. Mordor refreshes every twelve months, whereas others stretch updates to three years, amplifying drift during rapid parcel growth.

Benchmark comparison

| Market Size | Anonymized source | Primary gap driver |

|---|---|---|

| $87.88 B (2025) | Mordor Intelligence | - |

| $88.7 B (2025) | Regional Consultancy A | Treats PO box rental, philately as core revenue |

| $90.8 B (2023) | Trade Journal B | Projects forward from 2023 without mail-volume decay adjustment |

| $85.23 B (2024) | Global Consultancy C | Excludes Canada-to-US cross-border parcel contracts |

These comparisons show that our disciplined scope choices, annual refresh, and dual-path validation produce a balanced, transparent baseline that decision-makers can track back to clear variables and repeatable steps.

Key Questions Answered in the Report

What is the current size of the North America postal services market?

The market is valued at USD 88.8 billion in 2026 and is forecast to reach USD 93.56 billion by 2031.

Which segment holds the largest share in the North America postal services market?

Parcels dominate with a 58.05% share in 2025, reflecting the region’s e-commerce boom.

Why is Mexico the fastest-growing country segment?

Near-shoring of manufacturing and the creation of 128 planned industrial parks are generating additional mailroom and cross-border parcel demand, driving a 3.05% CAGR.

How are sustainability mandates influencing postal fleets?

California and other states require phased adoption of zero-emission vehicles, prompting USPS to target 66,000 electric vans by 2028.

What are the main challenges facing postal operators in North America?

Digital substitution of First-Class Mail, labour disruptions, border bottlenecks, and rural addressing gaps are among the critical restraints suppressing growth.

Who is currently the largest parcel carrier by volume?

USPS remains the largest with 6.6 billion parcels handled in 2024, though Amazon Logistics surpassed UPS to claim second place.

Page last updated on: