Market Overview

| Study Period | 2021 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

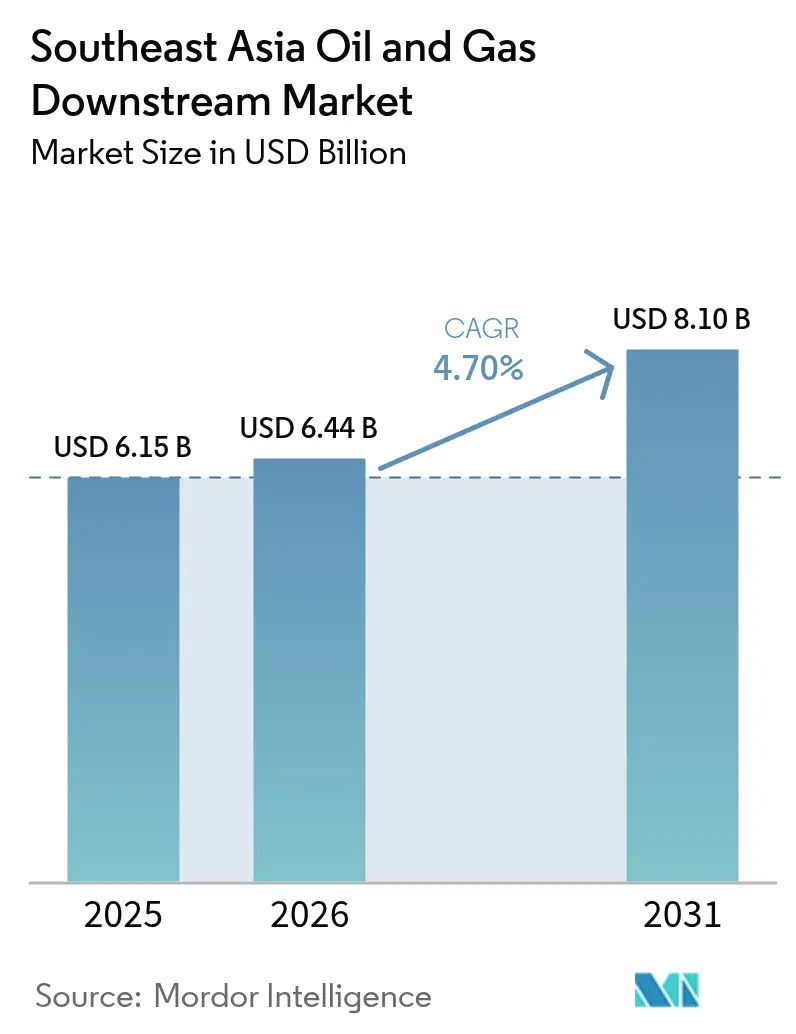

| Base Year Market Size (2025) | USD 6.15 Billion |

| Market Size (2026) | USD 6.44 Billion |

| Market Size (2031) | USD 8.1 Billion |

| Growth Rate (2026 - 2031) | 4.70% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

Southeast Asia Oil And Gas Downstream Market Analysis by Mordor Intelligence

The Southeast Asia Oil And Gas Downstream Market size is expected to grow from USD 6.15 billion in 2025 to USD 6.44 billion in 2026 and is forecast to reach USD 8.1 billion by 2031 at 4.7% CAGR over 2026-2031.

Accelerated transitions from stand-alone refining toward integrated petrochemical platforms, stronger post-COVID-19 aviation fuel demand, and stricter marine fuel regulations position the Southeast Asian oil and gas downstream market for resilient expansion despite feedstock price volatility. Competitive differentials now hinge on carbon-pricing readiness, IMO 2020-compliant bunker production, and Euro-V fuel upgrades, each of which elevates capital-spending requirements but also unlocks premium margin pools. Sustained integration with digital-control architectures and AI-enabled predictive maintenance reduces unplanned downtime by up to 12%, enabling refineries to adjust product slates in real-time, which supports profitability throughout demand cycles.[1]Technology report, “Downstream Integration Drives Competitive Advantage,” Wall Street Journal, wsj.com Regional policies—especially Singapore’s rising carbon tax and Indonesia’s forthcoming emissions levy—provide monetary incentives for carbon-capture investments that future-proof asset values within the broader Southeast Asian oil and gas downstream market.

Key Report Takeaways

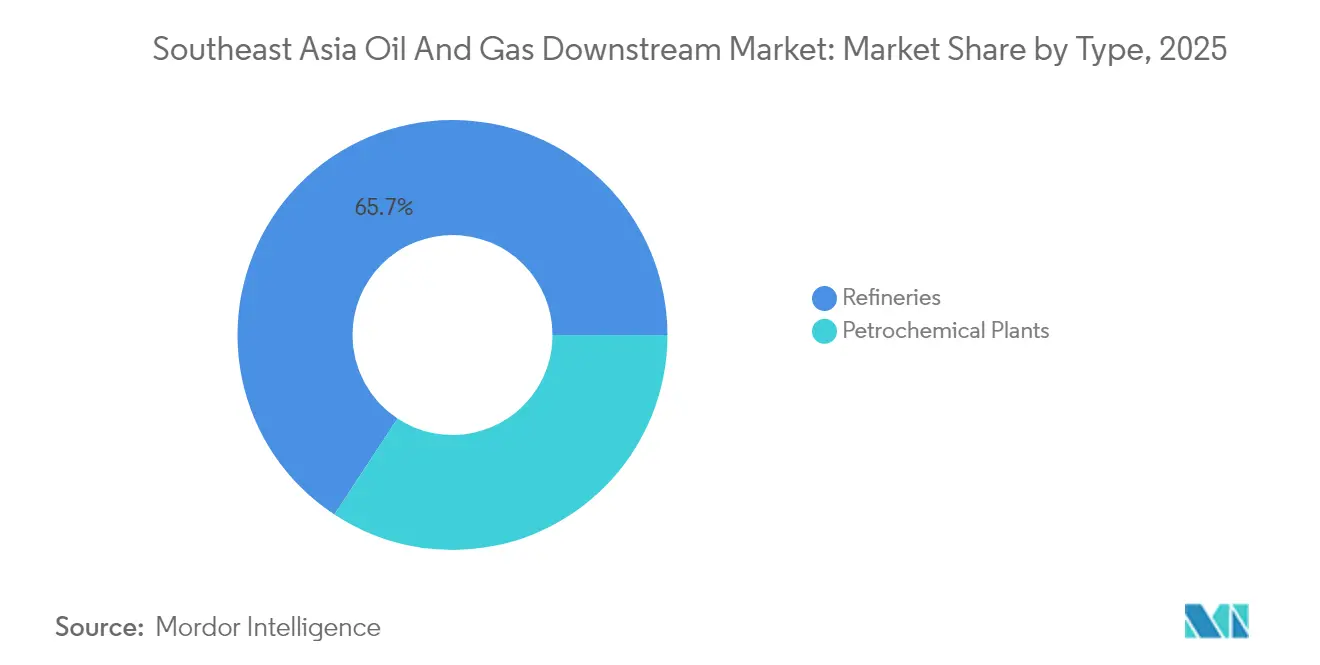

- By type, refineries held 65.74% of the Southeast Asia oil and gas downstream market share in 2025; petrochemical plants posted the fastest growth rate of 6.02% through 2031.

- By product type, refined petroleum products accounted for 61.12% of the Southeast Asia oil and gas downstream market size in 2025, while petrochemicals are projected to advance at a 6.78% CAGR to 2031.

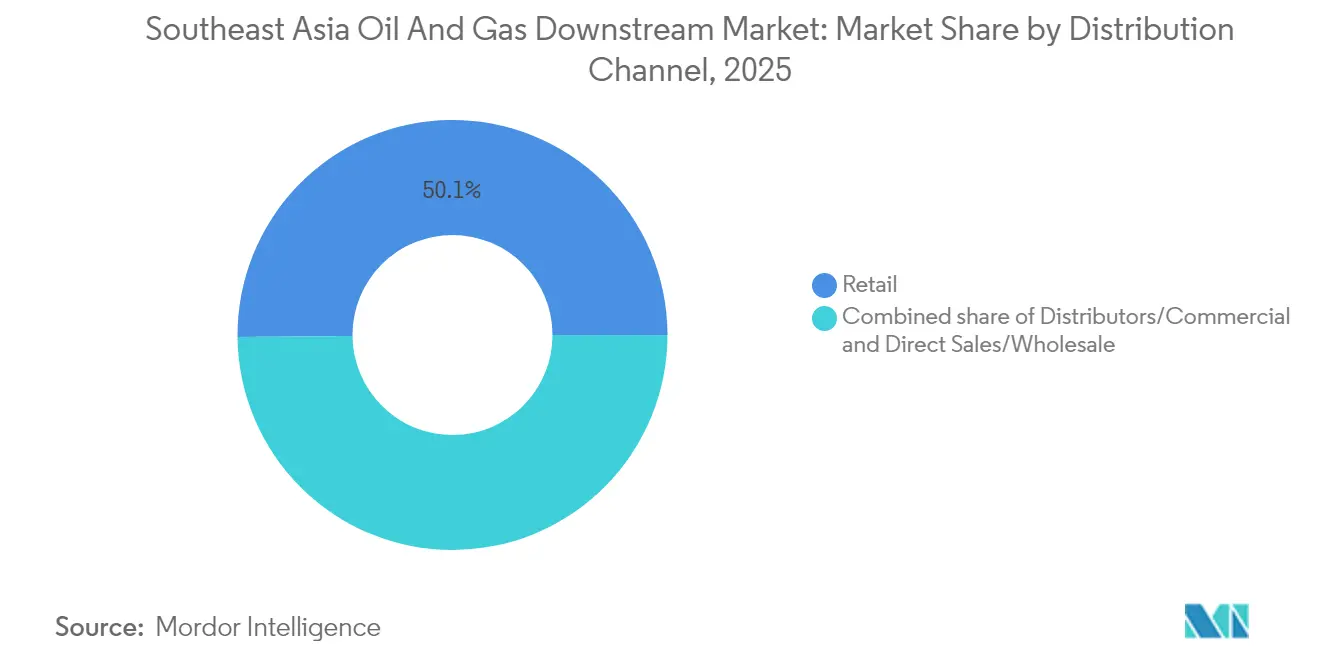

- By distribution channel, retail captured 50.14% of the Southeast Asia oil and gas downstream market size in 2025; distributors and commercial channels are forecast to expand at a 5.63% CAGR during 2026-2031.

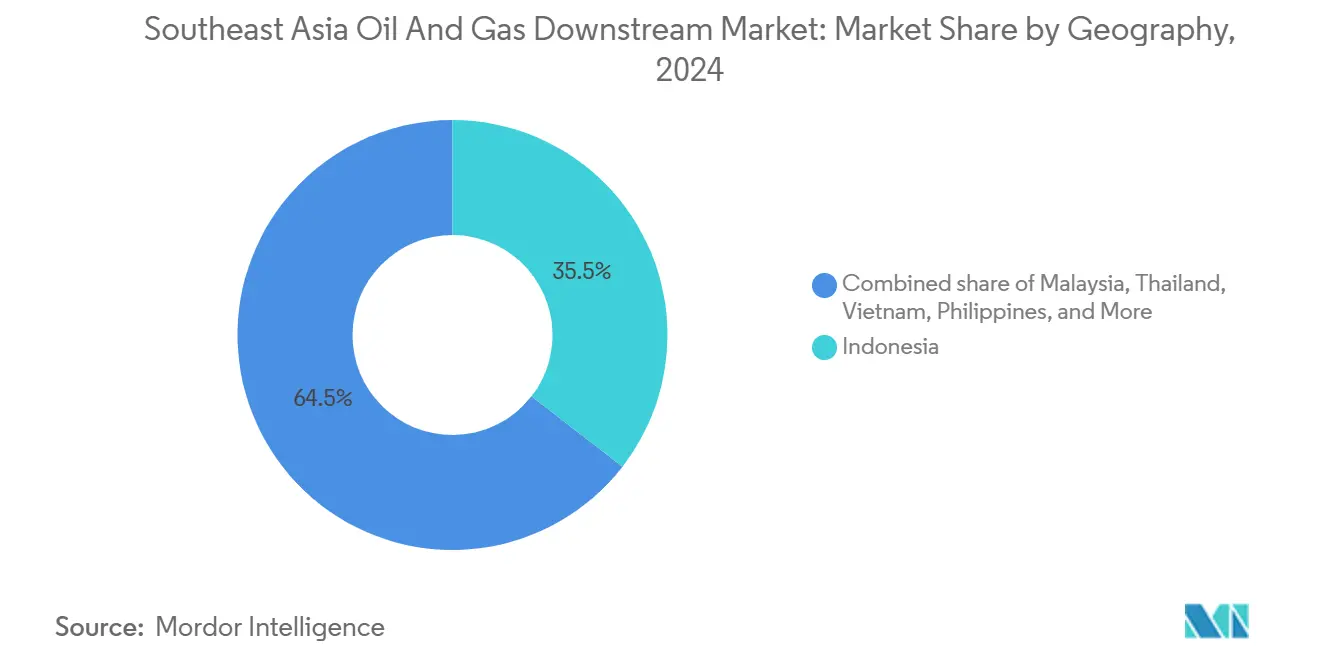

- By geography, Indonesia commanded 35.08% of the Southeast Asia oil and gas downstream market size in 2025, whereas the Philippines delivered the fastest growth rate of 5.79% over the outlook period.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of 2026.

Southeast Asia Oil And Gas Downstream Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Rapid recovery of regional jet-fuel demand post-COVID | +1.0% | Singapore, Malaysia, Thailand aviation hubs | Short term (≤ 2 years) |

| Rising regional integration of carbon-pricing schemes | +0.7% | ASEAN core markets, Singapore leadership | Medium term (2-4 years) |

| Expansion of IMO 2020-compliant bunkering hubs | +0.8% | Singapore, Malaysia, Indonesia ports | Short term (≤ 2 years) |

| Mainstream fuel-quality upgrades (Euro-V standards) | +0.6% | Indonesia, Thailand, Vietnam domestic markets | Medium term (2-4 years) |

| Accelerated petrochemical integration at existing refineries | +0.9% | Malaysia, Indonesia, Thailand integrated complexes | Long term (≥ 4 years) |

| AI-driven predictive maintenance reducing OPEX | +0.4% | Regional, early adoption in Singapore, Malaysia | Short term (≤ 2 years) |

| Source: Mordor Intelligence | |||

Rapid Recovery of Regional Jet-Fuel Demand Post-COVID

Aviation traffic across ASEAN rebounded sharply, pushing 2024 jet-fuel liftings at Singapore Changi to 8.2 million t, 15% above the 2019 baseline.[2]Aviation desk, “Singapore Changi Fuel Consumption Exceeds Pre-Pandemic Levels,” Reuters, reuters.com Parallel upticks at Kuala Lumpur International and Suvarnabhumi airports were sufficient to justify refinery configuration shifts toward higher jet-fuel yields. Airlines such as AirAsia and Singapore Airlines restored fleet utilization while expanding secondary-city routes, which require multi-node fuel logistics and create stable pull-through for integrated supply contracts. Refineries equipped with advanced hydro-treaters capture premium spreads on certified aviation fuel, thereby reinforcing the margin resilience of the Southeast Asia oil and gas downstream market. Demand visibility encourages capital outlays for distillate-selective units that can toggle between jet fuel and diesel depending on seasonal crack spreads. Predictable volume signals also help downstream operators negotiate long-term offtake agreements that underpin balance-sheet planning across new integration projects.

Rising Regional Integration of Carbon-Pricing Schemes

Singapore lifted its carbon levy to SGD 25 t-CO₂ in 2024 and will incrementally raise it to SGD 80 by 2030, a move mirrored by Thailand’s pilot trading system and Indonesia’s 2025 tax framework.[3]Policy bureau, “Singapore Carbon Tax Expansion Incentivizes Refinery Efficiency,” Financial Times, ft.com Differentiated CO₂ costs prompt operators to deploy flare-gas recovery, heat-integration retrofits, and post-combustion capture, thereby reducing unit emissions and creating tradable credits that offset compliance expenses. Financial centers in Kuala Lumpur and Singapore facilitate cross-border credit markets, enabling portfolio optimization for multi-country operators. Plants that couple carbon capture with hydrogen-ready furnaces position themselves for the looming scrutiny of global customers on Scope 3 emissions. Early adopters already monetize lower-carbon diesel and bunker blends through premium contracts with multinational logistics firms seeking verifiable emission reductions. Collectively, carbon-pricing harmonization supplies both carrot and stick incentives that accelerate technology uptake within the Southeast Asia oil and gas downstream market.

Expansion of IMO 2020-Compliant Bunkering Hubs

Sales of 0.5%-sulfur marine fuels at Singapore surpassed 47.8 million t in 2024, cementing the city-state’s global leadership. Neighboring hubs, Port Klang and Batam, added hydrotreating and blending units, increasing compliant bunker output by 40% since 2020. Strategic geography along Asia-Europe lanes guarantees throughput, while port authorities streamline quality-assurance protocols, reinforcing buyer confidence. The bunker boom spurs investment in co-located storage, shore power, and alternative fuels such as methanol and ammonia, creating ancillary revenue streams. Shipowners locking in long-term supply contracts drive predictable demand, allowing refiners to hedge against softening gasoline margins. Competitive dynamics, therefore, favor multi-site networks capable of synchronized product allocation, a trend that amplifies the regional importance of the Southeast Asia oil and gas downstream market.

Accelerated Petrochemical Integration at Existing Refineries

Malaysia’s Pengerang Integrated Complex illustrates the economic rationale: shared utilities and unified feedstock pools increase the overall return on invested capital by 250 basis points compared to stand-alone assets. Indonesia’s Cilacap upgrade adds ethylene and propylene streams that satisfy domestic polymer demand and open export channels to China. Integration mitigates fuel-demand cyclicality, reallocating naphtha and atmospheric residue toward higher-value chemical outputs during periods of compressed transport-fuel cracks. Process-control algorithms adjust cutpoints in real-time, maximizing aromatics or light olefins as market spreads dictate, which underpins sustained earnings even in downturns. The approach is expected to diffuse rapidly across the Southeast Asian oil and gas downstream market, with Thailand’s Map Ta Phut complex already executing specialty-chemical expansions aimed at producing electronics-grade materials. Long-cycle integration thus becomes a cornerstone strategy for maintaining competitive relevance throughout the decade of the energy transition.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| High capital cost escalations amid EPC supply-chain crunch | -0.8% | Regional, acute in complex projects | Short term (≤ 2 years) |

| Growing EV penetration suppressing gasoline demand | -0.6% | Thailand, Indonesia urban centers | Medium term (2-4 years) |

| Stringent green-bond taxonomy limiting fossil-fuel financing | -0.5% | Singapore, Malaysia financial centers | Medium term (2-4 years) |

| Skilled-labour shortages for complex turnaround projects | -0.4% | Regional, concentrated in specialized skills | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

High Capital-Cost Escalations Amid EPC Supply-Chain Crunch

Steel and specialty-alloy prices surged 40% between 2022 and 2024, while delivery lead times for large-bore reactors stretched to 24 months, inflating outlays on hydrocrackers and ethylene crackers. Samsung Engineering and Hyundai Engineering reported procurement delays on Pengerang and Balikpapan units, forcing schedule re-baselines and eroding project net present values. Financing structures now incorporate larger contingency cushions and index-linked escalation clauses, adding complexity to credit-committee approvals. Operators with robust supplier alliances and modular construction plans partially offset cost blowouts, but smaller players confront prohibitive entry barriers. Persistent bottlenecks threaten to defer capacity-addition timelines, softening near-term supply growth in the Southeast Asia oil and gas downstream market.

Growing EV Penetration Suppressing Gasoline Demand

Thailand’s 2024 EV penetration reached 9% of new-vehicle sales, supported by tax holidays and charging infrastructure subsidies. Indonesia’s nickel-based battery value chain is accelerating local EV manufacturing, projecting a potential 15-20% reduction in gasoline demand in Jakarta by 2030. Retail forecourts thus confront traffic attrition, pressuring throughput and ancillary convenience-store sales. Refiners counter by tilting toward jet kerosene, marine gas oil, and petrochemical feedstocks less exposed to electrification. Although internal-combustion fleets are expected to dominate in the medium term, consumption elasticity signals a long-term plateauing of gasoline output, nudging strategic capital expenditures toward diversified product slates across the Southeast Asian oil and gas downstream market.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Type: Refinery Scale Anchors, Petrochemical Plants Propel Growth

Refineries commanded 65.74% of 2025 revenue, but petrochemical units are expected to deliver the Southeast Asia oil and gas downstream market’s fastest 6.02% CAGR through 2031. The refinery cohort leverages economies of scale, coastal logistics, and crude-flex configurations that can shift from sweet to sour slates as price spreads fluctuate. Singapore’s integrated cluster alone processes 1.5 million bpd and feeds export pipelines across ASEAN. Nevertheless, the sustained risk of gasoline demand propels operators toward steam-cracker add-ons and aromatics extraction, which monetizes competitive naphtha economics.

Petrochemical integration increases the overall margin per barrel by converting incremental naphtha into ethylene-based derivative chains. Malaysia’s RAPID complex embodies this shift, deploying unified off-gas recovery and shared cogeneration to lower unit costs. Thailand’s Map Ta Phut expansion packages niche elastomers and specialty olefins for automotive component suppliers, reinforcing non-fuel value capture. The approach minimises exposure to motor-fuel cycling, future-proofing asset bases against electrification and decarbonization headwinds across the Southeast Asia oil and gas downstream market.

By Product Type: Petrochemicals Outpace Refined Fuels

Refined petroleum products retained a 61.12% share in 2025, with exports of gasoline, diesel, and compliant bunker fuel through well-established routes to Australia and Northeast Asia. However, petrochemicals are expected to lead growth at a 6.78% CAGR, supported by escalating demand for polymers used in packaging, construction, and durable goods manufacturing. Yields of ethylene, propylene, and aromatics from integrated sites underpin ASEAN’s aspiration to displace imports.

Lubricants occupy a premium niche, with base oil and additive blending drawing on Group III feedstocks produced at regional hydro-processing facilities. Branded lube marketers pursue original-equipment-manufacturer approvals to secure aftermarket loyalty. The evolving product mix delivers resilience, as higher-value chemicals and specialty lubricants shield margins when transport fuel prices crack—a scenario anticipated during widespread EV adoption—fortifying the competitiveness of the Southeast Asia oil and gas downstream market.

By Distribution Channel: Retail Dominates, Commercial Flows Accelerate

Retail fuels remained the largest channel, accounting for 50.14% in 2025, underpinned by over 40,000 service stations across Indonesia, Thailand, and Malaysia. Loyalty apps and convenience-store formats enhance non-fuel revenue streams, partially insulating forecourt economics from erosion in gallonage. Meanwhile, distributor/commercial channels show a 5.63% CAGR, driven by aviation-fuel uplift, marine-fuel sales, and bulk diesel contracts serving independent power producers.

Digital order-management platforms enable bulk customers to schedule deliveries and obtain sulfur-content certificates, thereby increasing service stickiness. Direct sales/wholesale caters to industrial clusters that need customized fuel blends, such as low-pour-point marine gas oil for refrigerated cargo. Commercial-channel sophistication enhances supply-chain transparency and mitigates inventory holding costs, thereby reinforcing demand capture in the Southeast Asia oil and gas downstream market.

Geography Analysis

Indonesia led with a 35.08% share in 2025, processing roughly 1.6 million bpd across Cilacap, Balikpapan, and Dumai, and capturing Euro-V premium spreads through recent hydrocracker retrofits. Pertamina's USD 15 billion petrochemical outlay aims to close a domestic polymer deficit projected at 3 million t by 2027. Regulatory frameworks grant import-tariff relief on cracker equipment, accelerating execution schedules.

Malaysia follows, anchored by PETRONAS's Pengerang Integrated Complex, which pairs 300,000 bpd of refining with 3.3 million t of olefins and aromatics capacity. Carbon-capture pilots at the site reduce Scope 1 emissions by 15%, generating voluntary credits that offset Singapore's carbon-levy exposure for inter-company shipments. Thailand sits third, leveraging Map Ta Phut's petrochemical depth and PTT's nationwide retail grid; the country also scales bunkering infrastructure at Laem Chabang, courting vessel traffic diverted from tighter Singapore berthing slots.

The Philippines posts the fastest 5.79% CAGR, courtesy of Petron's modernization efforts that add Euro-V capability and polypropylene lines, while meeting surging transport fuel demand linked to infrastructure build programs. Vietnam advances its refining self-sufficiency through Nghi Son Phase 2, securing feedstock from Middle East supply contracts and boosting aromatics exports to China. Singapore, although physically constrained, maintains its hub status through sophisticated derivatives trading and integrated storage and blending assets that balance regional supply and demand. Myanmar and Brunei contribute niche capacities and exploit cross-border swaps to mitigate domestic scale limitations, rounding out geographic diversity within the Southeast Asia oil and gas downstream market.

Competitive Landscape

Competitive Landscape

The market displays moderate concentration, with national champions PETRONAS, Pertamina, and PTT, along with ExxonMobil, Shell, and TotalEnergies, securing roughly 65% of the aggregate regional capacity, leaving a competitive fringe of mid-tier refiners and specialty chemical players. Integrated state firms wield regulatory latitude and domestic distribution power, while IOCs inject deep process know-how and global marketing muscle. Hybrid joint ventures—such as PTT-Aramco at Map Ta Phut—combine crude supply security with petrochemical technology, thereby spreading risk across the entire value chain.

Digital transformation proves decisive. Thai Oil’s AI-driven control loops trim energy intensity by 5%, while Shell’s Singapore complex leverages machine-vision drones to map corrosion hot-spots, reducing inspection downtime. Early leaders in emissions capture, such as PETRONAS at Pengerang Phase 2, negotiate premium contracts with consumer electronics brands requiring low-carbon plastics. Commercial agility likewise matters: Pavilion Energy’s freight-optimization algorithms match bunker-fuel dispatches with vessel ETAs, slashing demurrage costs.

Competitive tension escalates as EV uptake pressures gasoline margins. Forward-looking refiners are pivoting toward aviation fuel, marine distillates, and chemical derivatives that are less vulnerable to electrification. Simultaneously, renewable-fuel entrants—including Neste’s former Singapore assets now under Shell—challenge incumbents on carbon intensity metrics. Success increasingly depends on orchestrating feedstock flexibility, digital efficiency, and portfolio diversity to secure long-term viability across the Southeast Asian oil and gas downstream market.

Southeast Asia Oil And Gas Downstream Industry Leaders

PTT Public Company Ltd

PT Pertamina

Shell plc

Petroliam Nasional Berhad

Exxon Mobil Corp

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- September 2025: Petron has become the first oil company in the Philippines to be recognized by the Department of Energy as an official training center for the liquefied petroleum gas (LPG) industry.

- July 2025: China’s biodiesel specialist Zhuoyue New Energy plans to invest RMB 700 million (USD 97.5 million) in a new Thai plant. The project will give the company its first production foothold in Southeast Asia and help Thailand boost local supplies of low-carbon transport fuel.

- December 2024: Indonesia’s petrochemical heavyweight, Chandra Asri Group, has hired domestic contractor IKPT to increase capacity at its Ciwandan Butene-1 and MTBE units by more than 25%. The upgrade reduces reliance on imports and frees up additional feedstock for products ranging from synthetic rubber to cleaner-burning gasoline, thereby enhancing both domestic supply and export potential.

- September 2024: Thai Oil installed advanced digital control systems across its refineries, boosting efficiency and enabling predictive maintenance.

Southeast Asia Oil And Gas Downstream Market Report Scope

The processes of refining, marketing, and eventually selling petroleum products are referred to as downstream. In the downstream business, a corporation refines crude oil and natural gas and markets and sells petroleum products to wholesale and retail customers. Processed natural gas is often sold directly to electric and gas utilities.

The Southeast Asia oil and gas downstream market is segmented by refineries, petrochemical plants, and geography. The report also covers the market size and forecasts for the oil and gas downstream market across major countries in the region. For each segment, the market sizing and forecasts have been done based on refining capacity (thousand barrels per day).

By Sector

| Refineries |

| Petrochemical Plants |

By Product Type

| Refined Petroleum Products |

| Petrochemicals |

| Lubricants |

By Distribution Channel

| Direct Sales/Wholesale |

| Distributors/Commercial |

| Retail |

By Geography

| Indonesia |

| Malaysia |

| Thailand |

| Vietnam |

| Philippines |

| Singapore |

| Myanmar |

| Rest of Southeast Asia |

| By Sector | Refineries |

| Petrochemical Plants | |

| By Product Type | Refined Petroleum Products |

| Petrochemicals | |

| Lubricants | |

| By Distribution Channel | Direct Sales/Wholesale |

| Distributors/Commercial | |

| Retail | |

| By Geography | Indonesia |

| Malaysia | |

| Thailand | |

| Vietnam | |

| Philippines | |

| Singapore | |

| Myanmar | |

| Rest of Southeast Asia |

Key Questions Answered in the Report

How large will the Southeast Asia oil and gas downstream market be by 2031?

Forecasts place the value at USD 8.1 billion, up from USD 6.15 billion in 2025.

Which downstream segment is growing fastest?

Petrochemical plants are projected to expand at a 6.02% CAGR through 2031 as integration strategies accelerate.

Why is Indonesia pivotal to regional downstream dynamics?

A 35.08% revenue share, a 1.6 million bpd refining system and USD 15 billion in planned petrochemical capacity make Indonesia the anchor market.

How does carbon pricing impact refinery economics?

Rising levies in Singapore and planned taxes in Indonesia incentivize efficiency upgrades and carbon-capture deployment that lower net emissions and unlock premium low-carbon product pricing.

What does IMO 2020 compliance mean for regional bunkering?

Southeast Asian ports added 40% compliant fuel capacity since 2020, securing long-term marine-fuel demand for refineries configured with advanced hydrotreaters.

How is EV adoption reshaping gasoline demand?

Thailand’s 9% EV sales share and Indonesia’s battery-supply push point to a medium-term erosion of urban gasoline demand, urging refiners to diversify toward jet fuel, marine distillates and chemicals.

Page last updated on: