Market Overview

| Study Period | 2020 - 2031 |

|---|---|

| Forecast Data Period | 2026 - 2031 |

| Historical Data Period | 2020 - 2024 |

| Market Size (2026) | USD 18.60 Billion |

| Market Size (2031) | USD 22.77 Billion |

| Growth Rate (2026 - 2031) | 4.12% CAGR |

| Market Concentration | Medium |

Major Players *Disclaimer: Major Players sorted in no particular order Image © Mordor Intelligence. Reuse requires attribution under CC BY 4.0. | |

South Korea Paper Packaging Market Analysis by Mordor Intelligence

The South Korea paper packaging market size reached USD 18.60 billion in 2026 and is projected to attain USD 22.77 billion by 2031, advancing at a 4.12% CAGR over the forecast period. Structural shifts in online retail, food delivery, and environmental regulation are steering demand away from cyclical swings and toward sustained expansion in recycled and specialty substrates. Rapid growth in parcel volume at metropolitan fulfillment hubs, coupled with a 20% recycled-content floor for corrugated packaging, is compelling converters to reengineer their supply chains around domestic recovered fiber. Parallel advances in high-barrier coating technology are creating premium niches for shelf-stable foods that were once reserved for polymer-laminated or aluminum-lined structures. Multinationals are using scale to cushion pulp-price volatility, yet local players maintain an edge in quick-turn customization tailored to Korean consumer aesthetics.

Key Report Takeaways

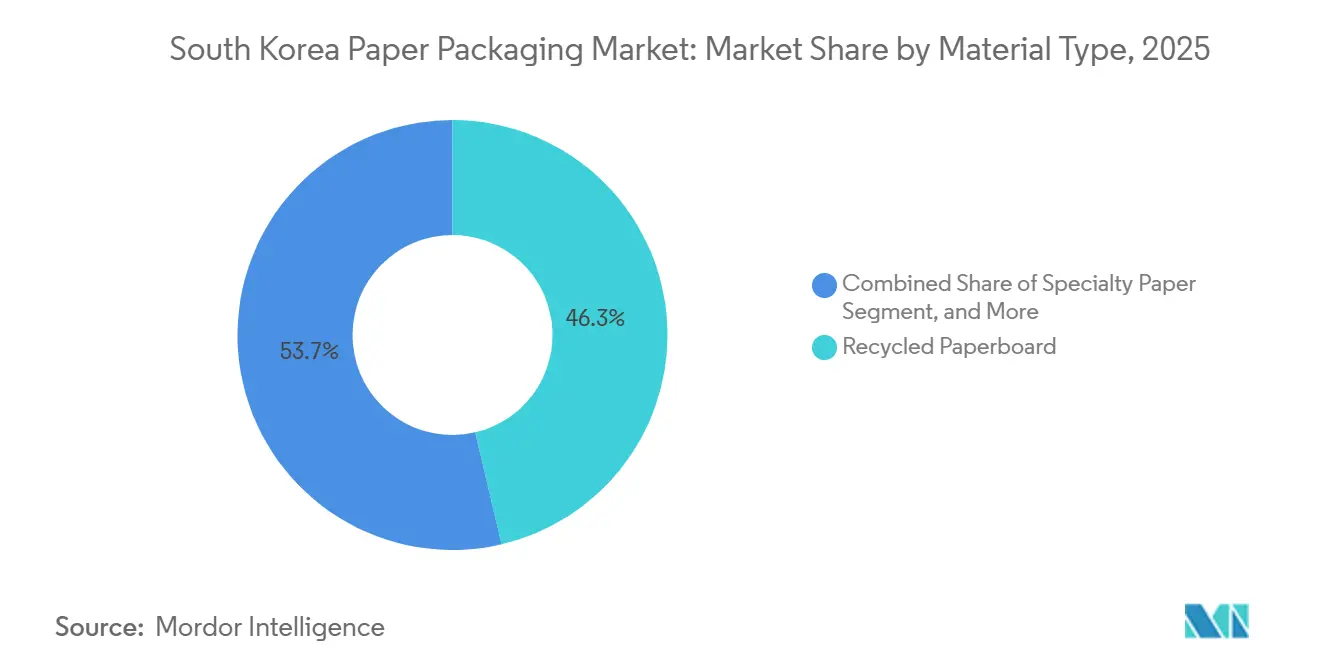

- By material type, recycled paperboard captured 46.34% of the South Korea paper packaging market share in 2025, whereas specialty paper is forecast to grow at a 5.32% CAGR through 2031.

- By product type, rigid formats led with a 54.32% revenue share in 2025; flexible paper packaging is expected to expand at a 5.64% CAGR through 2031.

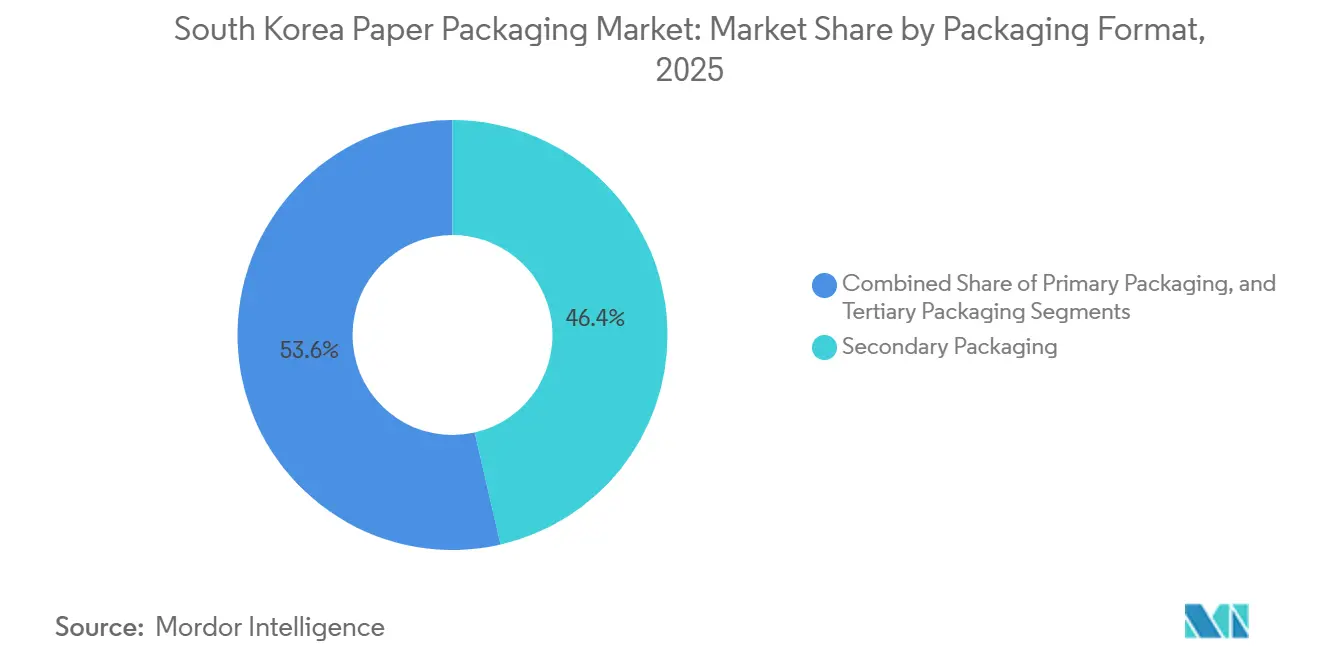

- By packaging format, secondary packaging accounted for 46.42% revenue share in 2025, while primary packaging is projected to post a 6.11% CAGR through 2031.

- By end-use industry, food applications accounted for 28.32% of the South Korea paper packaging market size in 2025 and are set to advance at a 5.98% CAGR through 2031.

Note: Market size and forecast figures in this report are generated using Mordor Intelligence’s proprietary estimation framework, updated with the latest available data and insights as of January 2026.

South Korea Paper Packaging Market Trends and Insights

Drivers Impact Analysis*

| Driver | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Surge in E-commerce Shipments | +1.2% | Seoul, Gyeonggi, Busan metropolitan areas | Short term (≤ 2 years) |

| Rising Consumer Demand for Eco-Friendly Packaging | +0.9% | National, premium uptake in Seoul and Jeju | Medium term (2-4 years) |

| Government Recycling and Plastic-Reduction Policies | +0.8% | National via Ministry of Environment EPR system | Medium term (2-4 years) |

| Expansion of Food Delivery Services | +0.7% | Urban centers with dense delivery networks | Short term (≤ 2 years) |

| Zero-Waste Commitments by Korean Brands | +0.4% | National, spearheaded by Lotte, Amorepacific, Samsung | Long term (≥ 4 years) |

| Advanced High-Barrier Paper Coating Technologies | +0.3% | R&D clusters in Daejeon and Seoul | Long term (≥ 4 years) |

| Source: Mordor Intelligence | |||

Surge in E-commerce Shipments

A 10.1% year-on-year jump in online shopping transaction value pushed November 2024 sales to KRW 19.2 trillion (USD 14.4 billion).[1]Statistics Korea, “Online Shopping Trends Survey, November 2024,” kostat.go.krParcel volumes exceeded 4.2 billion units in 2024, up from 3.8 billion in 2023, resulting in a compression of average parcel weight but an increase in total corrugated surface area.[2]Ministry of Trade, Industry and Energy, “Parcel Delivery Market Statistics 2024,” motie.go.krSame-day networks run by Coupang and Naver depend on higher-burst-strength linerboard that can survive multiple sortation cycles, spurring linerboard upgrades across the South Korea paper packaging market. Smaller, more frequent deliveries lift per-unit packaging intensity, accelerating consumption beyond pure revenue growth. Converters closest to Seoul’s logistics belts benefit from just-in-time runs that align with volatile SKU mixes demanded by e-commerce brands.

Rising Consumer Demand for Eco-Friendly Packaging

Seventy-two percent of Korean shoppers indicated a willingness to pay a 5-10% premium for recyclable packs in a 2024 survey.[3]Korea Chamber of Commerce and Industry, “Consumer Survey on Sustainable Packaging Preferences 2024,” korcham.net Amorepacific swapped 1,200 metric tons of plastic for molded-pulp trays, trimming Scope 3 emissions by 35%. Lotte Shopping has pledged to remove single-use plastics from its private-label snacks by 2025, opting for kraft paper pouches that align with household curbside collection streams. While affluent consumers in Seoul and Jeju reward such initiatives, a 12-15% cost difference between virgin board and recycled grades continues to dampen uptake in mass-market instant noodles. Even so, brand-equity gains are strong enough that cosmetics and premium snacks are switching ahead of regulatory deadlines, reinforcing momentum for the South Korea paper packaging market.

Government Recycling and Plastic-Reduction Policies

January 2024 revisions to the Extended Producer Responsibility regime enforced a 20% recycled-content mandate for corrugated cases and introduced fines up to KRW 50 million (USD 37,500) for non-compliance.[4]Ministry of Environment, “Extended Producer Responsibility System Revision 2024,” me.go.krThe December 2024 Circular Economy Promotion Act further obliged producers to finance municipal collection, inflating virgin-fiber costs by KRW 80 per kilogram (USD 0.06). To secure dependable feedstock, converters have begun purchasing stakes in regional recyclers, with domestic recycled-pulp capacity expanding 180,000 metric tons in 2024, yet still falling short of demand. Export-oriented box makers face additional scrutiny from European buyers who now insist on ISO 14021 verification, integrating environmental compliance into commercial negotiations.

Expansion of Food Delivery Services

Delivery apps processed 3.8 billion orders in 2024, a 14% increase over 2023, with packaging costs accounting for 8-12% of the restaurant order value. Each order now averages 2.3 separate paper components, up from 1.8 two years earlier, driven by an uptick in side dishes and individualized condiments. Grease-resistant yet fluorine-free coatings that comply with MFDS Standard 2024-29 are essential for hot soups and oily entrées. Pilot reusable container schemes in Seoul posted sub-40% return rates, keeping single-use paper formats as the dominant solution. Consequently, urban density keeps the South Korea paper packaging market aligned with quick-service meal growth.

Restraints Impact Analysis*

| Restraint | (~) % Impact on CAGR Forecast | Geographic Relevance | Impact Timeline |

|---|---|---|---|

| Volatile Wood Pulp Prices | -0.6% | Import-dependent mills nationwide | Short term (≤ 2 years) |

| Improved Recyclable Plastics Competing with Paper | -0.4% | Chemical-recycling hub in Ulsan | Medium term (2-4 years) |

| Skilled-Labor Shortages in Domestic Mills | -0.3% | Chungcheong and Jeolla provinces | Long term (≥ 4 years) |

| China’s Recovered-Paper Import Restrictions | -0.2% | Nationwide waste-paper export chain | Medium term (2-4 years) |

| Source: Mordor Intelligence | |||

Volatile Wood Pulp Prices

Bleached hardwood kraft pulp oscillated between USD 580 and USD 720 per ton in 2024 amid supply disruptions in Brazil and Indonesia. South Korea relies on imports for 82% of virgin pulp, so the won’s 6.2% depreciation over the same period amplified cost swings. Hansol Paper’s operating margin slid 340 basis points in Q2 2024 as pulp expenses outpaced carton-price adjustments. Smaller mills with thin hedging capacity trimmed production, dampening supply for branded converters and restraining growth across the South Korea paper packaging market.

Improved Recyclable Plastics Competing with Paper

SK Chemicals commercialized chemically recycled PET with equivalent mechanical properties to virgin resin, albeit with a 25% price premium, threatening paper in rigid-container niches. The Ulsan advanced recycling center processes 70,000 tons of mixed waste annually, producing feedstock for flexible films once slated for paper substitution. Early adopters, such as Pulmuone, chose recycled PET salad tubs over molded pulp, citing their thinner walls and improved moisture resistance. As chemical recycling scales and costs drop, paper’s addressable share in high-barrier applications could narrow, trimming 0.4 percentage points from forecast CAGR.

*Our forecasts treat driver/restraint impacts as directional, not additive. The impact forecasts reflect baseline growth, mix effects, and variable interactions.

Segment Analysis

By Material Type: Recycled Board Dominates, Specialty Paper Climbs

Recycled paperboard continued to represent 46.34% of the South Korea paper packaging market in 2025, anchored in e-commerce box demand that swelled alongside parcel-volume gains in Seoul hubs. Specialty paper, although smaller in volume, is set to book a 5.32% CAGR through 2031 as barrier-coated grades obtain food-contact certification and convince premium snack and ready-meal brands to migrate from plastic laminates. Virgin board retains relevance in aseptic cartons where food safety obliges untouched fiber streams, while kraft paper commands heavy-duty sacks for agriproducts yet faces substitution from woven polypropylene in bulk cement shipments. Molded pulp, at an 8% share, posted double-digit volume growth in electronics cushioning after LG Electronics validated compression geometries that match EPS at controlled humidity.

Commodity recycled board derives strength from the Ministry of Environment’s 20% recycled-content rule that penalizes virgin pulp usage, but post-consumer fiber variability caps penetration in direct food applications, thereby shielding specialty paper pricing. That high-margin niche now leverages boric-acid cross-linked polyvinyl alcohol coatings registering oxygen transmission below 1 cc/m²/day, allowing shelf-stable porridges and nut milks to bypass aluminum foil liners. Domestic suppliers have moved from lab to pilot scale, yet full-line commercial output is scheduled only after 2026, meaning incumbents with established coating lines can charge 40-60% premiums in the interim. Consequently, price spreads between recycled board and specialty grades will likely widen over the forecast horizon, reinforcing bifurcation within the South Korea paper packaging market.

By Product Type: Rigid Leads, Flexible Accelerates

Rigid paper formats commanded 54.32% of revenue in 2025, with corrugated boxes taking the lion’s share due to e-commerce and interplant logistics. Folding cartons served pharmaceuticals and cosmetics that prize lithographic print quality and tactile varnishes. Secondary rigid formats, such as composite cans, stuck to premium nutritional powders and gift confectionery where cylindrical form factors bolster shelf presence. Conversely, flexible paper packaging is on a 5.64% CAGR trajectory to 2031 as heat-sealable monomaterial pouches and wraps gain market approvals from global FMCG players.

Stand-up pouches based on cellulose-rich substrates achieved curbside recyclability and delivered brand-preferred matte textures that polymer films cannot replicate. Coffee, dry beverage powders, and refill packs for household cleaners illustrate the earliest wins, lifting pouches and bags subsegment growth to 6.2% per year. Wraps and twist films trail because compostable biopolymer blends offer similar end-of-life benefits at thinner gauges. As regulatory scrutiny shifts toward multilayer plastics, the flexible paper value pool is expected to stretch, enabling converters with extrusion-coating and hot-tack adhesive know-how to monetize brand migration into recycle-ready solutions and thus drive the South Korea paper packaging market.

By Packaging Format: Primary Packs Surge on Direct-to-Consumer Brands

Secondary packaging accounted for 46.42% of the revenue share in 2025, serving as the backbone of e-commerce distribution. However, primary packs are forecast to grow at a rate of 6.11% annually, as DTC cosmetics and nutraceutical brands emphasize unboxing rituals that reinforce their premium positioning. Primary folding cartons and molded-pulp inserts are moving upscale, featuring debossed logos, pearlescent inks, and smart-label integrations that authenticate product provenance while satisfying curbside recyclability metrics.

In contrast, tertiary transit formats are plateauing under competition from reusable plastic crates within Korean automotive supply chains, which emphasize closed-loop cost savings. Further impetus for primary-pack acceleration stems from the Circular Economy Promotion Act, which levies higher EPR fees on multi-layered systems, effectively penalizing extraneous secondary shells. Innovations in nanocellulose coatings with optical and RF transparency now enable RFID tags to be integrated without the use of metalized foil, providing brands with real-time inventory visibility while maintaining a mono-material paper envelope. Given these dynamics, primary packaging’s economic share of the South Korea paper packaging market is poised to rise faster than its tonnage share, sweetening margins for converters specialized in value-added print finishing.

By End-Use Industry: Food Stays in Front

Food accounted for 28.32% of the South Korean paper packaging market size in 2025 and is projected to grow at a 5.98% CAGR to 2031, driven by online grocery fulfillment and government subsidies for compostable lunch trays in public schools. Beverage followed at 24% share, dominated by aseptic cartons, where Tetra Pak Korea booked KRW 1.1 trillion (USD 825 million) revenue in 2024.

Personal care and cosmetics, at 14%, are shifting toward molded-pulp trays and paper tubes that align with clean-beauty narratives, outpacing growth in healthcare cartons that nonetheless benefit from stringent anti-tamper mandates. The industrial and electronics sectors lag behind food growth as reusable totes and minimized packaging take hold, but molded pulp continues to eat into EPS cushioning around smartphones and home appliances. The relative outperformance of food will therefore anchor bulk board demand, while cosmetics and nutraceuticals will catalyze high-margin specialty paper orders, sustaining an overall balanced opportunity set across the South Korea paper packaging market.

Geography Analysis

The Seoul Capital Area accounted for 52% of national paper-pack consumption in 2025, driven by its dense population, the headquarters of top cosmetics and food brands, and an integrated cluster of import ports, distribution centers, and printing corridors. Locating 68% of corrugated output within 100 km of Incheon Port enables rapid inflow of raw materials and export of finished goods, thereby shortening lead times for multinational FMCG accounts. Busan and its adjoining industrial corridor seized 18% share thanks to automotive, shipbuilding, and electronics export logistics that depend on heavy-duty corrugated transit cases.

Chungcheong provinces delivered 14% of the volumes and house numerous pharmaceutical and functional-food plants, whose GMP requirements translate into high-specification folding cartons with serialized barcodes. This region also attracts investment in nanocellulose-coating pilot lines due to the proximity of KAIST and Yonsei labs, positioning it as an incubator for next-generation barrier solutions. Jeolla and Gangwon provinces contributed 10% and 6% respectively, with demand skewing toward fresh-produce trays and tourism-driven single-use packs. Yet both face labor shortages as median mill-worker age now exceeds 52 years, prompting government subsidy programs for mill modernization outside Seoul to balance regional development.

Recycling infrastructure remains uneven; Seoul and Gyeonggi collected 78% of paper waste in 2024 versus 62% in rural areas. Differential EPR fees attempt to level the field but concurrently elevate fiber prices outside metropolitan zones. Busan enjoys sea-freight advantages for Southeast-Asia pulp, trimming inbound costs by up to 15% yet is land-constrained for capacity expansions. Jeju Island, celebrated for carbon-neutral tourism, posts only 1.2% of national demand, hampered by 20-25% higher shipping costs. Taken together, the geographic mosaic creates logistical arbitrage opportunities, but the South Korea paper packaging market will remain centered on the Seoul Capital Area for both supply and demand through 2031.

Competitive Landscape

The market has moderate fragmentation. Global giants such as Smurfit WestRock, International Paper, and Amcor import scale efficiencies in pulp procurement and R&D; yet, local brands like Hansol PaperTech, Rengo Korea, and Oji Interpack Korea leverage proximity, cultural alignment, and quicker artwork changeovers to defend their accounts. The Smurfit-WestRock merger in July 2024 combined a USD 34 billion behemoth with 500 converting plants, increasing pulp-buying power but also prompting EU divestiture mandates that diverted leadership bandwidth away from Asia for several quarters.

Technology is proving decisive. Hansol PaperTech invested KRW 28 billion (USD 21 million) in digital presses and inline coating, cutting setup times 40% and making micro-run folding cartons profitable for influencer-driven DTC launches. Amcor signed a supply MOU with a Korean petrochemical player to guarantee advanced recycled resins for regional customers starting 2025, underscoring an aggressive pivot into circular feedstocks that could squeeze virgin-fiber converters. Smaller firms are experimenting with purchasing consortia for recycled pulp, yet coordination friction and free-rider behavior dilute bargaining gains.

Regulatory barriers add another moat, as new entrants must bankroll collection schemes or pay EPR fees that erode margins by as much as 12%. Given these dynamics, consolidation pressures are likely to intensify, but niche specialists in barrier-coated papers and molded-pulp cushioning still find defensible pockets within the South Korea paper packaging market.

South Korea Paper Packaging Industry Leaders

International Paper Company

Graphic Packaging International Corporation

Tetra Laval Group

Smurfit WestRock

Amcor plc

- *Disclaimer: Major Players sorted in no particular order

Recent Industry Developments

- June 2025: Pulmuone released its 2024 Integrated Report outlining the roll-out of paper-based insulated shippers, molded-pulp trays, and label-free bottles, and confirmed plans to triple the volume of paper-insulated packaging supplied to grocery e-commerce partners by 2026, a move expected to lift domestic demand for specialty coated board.

- January 2025: International Paper closed the acquisition of DS Smith, giving the combined group USD 34 billion in sales and wider containerboard reach that could reshape Asian export flows.

- September 2024: Amcor inked an MOU with a Korean petrochemical firm to source advanced recycled inputs for Asia-Pacific food and healthcare packs starting in 2025.

- July 2024: Smurfit Kappa and WestRock completed their merger, creating Smurfit WestRock with 500 converting plants worldwide.

South Korea Paper Packaging Market Report Scope

The market for the study encompasses the revenue generated from the sales of paper packaging products, including folding cartons and corrugated boxes, across various end-user applications within its scope. The market tracks the consumption of paper packaging products in the country. The analysis is based on the market insights captured through secondary and primary research. The market also examines the major factors influencing the growth of the South Korean paper packaging market, including drivers and restraints.

The South Korea Paper Packaging Market Report is Segmented by Material Type (Virgin Paperboard, Recycled Paperboard, Kraft Paper, Specialty Paper, and Molded Pulp), Product Type (Flexible Paper Packaging, and Rigid Paper Packaging), Packaging Format (Primary Packaging, Secondary Packaging, and Tertiary/Transit Packaging), and End-Use Industry (Food, Beverage, Healthcare and Pharmaceuticals, Personal Care and Cosmetics, Industrial, and Other End-Use Industries). The Market Forecasts are Provided in Terms of Value (USD).

By Material Type

| Virgin Paperboard |

| Recycled Paperboard |

| Kraft Paper |

| Specialty Paper |

| Molded Pulp |

By Product Type

| Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | |

| Other Flexible Paper Packaging | |

| Rigid Paper Packaging | Folding Carton |

| Corrugated Boxes | |

| Other Rigid Paper Packaging |

By Packaging Format

| Primary Packaging |

| Secondary Packaging |

| Tertiary / Transit Packaging |

By End-Use Industry

| Food |

| Beverage |

| Healthcare and Pharmaceuticals |

| Personal Care and Cosmetics |

| Industrial |

| Other End-Use Industries |

| By Material Type | Virgin Paperboard | |

| Recycled Paperboard | ||

| Kraft Paper | ||

| Specialty Paper | ||

| Molded Pulp | ||

| By Product Type | Flexible Paper Packaging | Pouches and Bags |

| Wraps and Films | ||

| Other Flexible Paper Packaging | ||

| Rigid Paper Packaging | Folding Carton | |

| Corrugated Boxes | ||

| Other Rigid Paper Packaging | ||

| By Packaging Format | Primary Packaging | |

| Secondary Packaging | ||

| Tertiary / Transit Packaging | ||

| By End-Use Industry | Food | |

| Beverage | ||

| Healthcare and Pharmaceuticals | ||

| Personal Care and Cosmetics | ||

| Industrial | ||

| Other End-Use Industries | ||

Key Questions Answered in the Report

What is the projected value of the South Korea paper packaging market in 2031?

The market is forecast to reach USD 22.77 billion by 2031.

Which material currently leads demand in South Korea’s paper packs?

Recycled paperboard holds the top spot, accounting for 46.34% of the market share in 2025.

How fast is specialty paper expected to grow in South Korea?

Specialty grades are projected to advance at a 5.32% CAGR through 2031.

Which end-use sector is forecast to expand the quickest?

Food packaging is set to grow at 5.98% annually, outpacing beverages and electronics.

How are government regulations shaping paper packaging demand?

A mandatory 20% recycled-content rule and new collection-finance obligations are pushing converters toward closed-loop fiber sourcing.

What impact will improved recyclable plastics have on paper formats?

Chemically recycled PET and related plastics may shave 0.4 percentage points off paper CAGR by reclaiming high-barrier rigid-container niches.

Page last updated on: